Artículos

Main elements of taxation in the conditions of the development of digital economy

Principales elementos de tributación en las condiciones del desarrollo de la economía digital

I A. TSINDELIANI i.tsindeliani@yandex.ru

A S. BUROVA annburrovaa@mail.ru

E V. MIGACHEVA lenamiga007@bk.ru

K T. ANISINA karanisina08@gmail.com

A A. KOPINA kopina_anna1987@gmail.com

V E. RODYGINA verona_rodygina@gmail.com

I A. TSINDELIANI i.tsindeliani@yandex.ru

A S. BUROVA annburrovaa@mail.ru

E V. MIGACHEVA lenamiga007@bk.ru

K T. ANISINA karanisina08@gmail.com

A A. KOPINA kopina_anna1987@gmail.com

V E. RODYGINA verona_rodygina@gmail.com

Main elements of taxation in the conditions of the development of digital economy

Utopía y Praxis Latinoamericana, vol. 24, núm. Esp.5, pp. 129-137, 2019

Universidad del Zulia

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-CompartirIgual 3.0 Internacional.

Recepción: 01 Octubre 2019

Aprobación: 04 Noviembre 2019

Abstract: The purpose of this article is to consider the main elements of taxation in a digital economy. On the base of the analysis, it was concluded that in conditions of digital economy, the development of information resources would provide a concretization of the provisions of the main elements of taxation and optimize the emergence and pursuance of the constitutional duties to pay taxes, as well as the calculation of tax amounts. The main provisions and conclusions can be used in scientific and practical activities when considering the issues of the legal construction of taxes.

Keywords: Digital Economy, Legal Construction, Practical Activities, Taxation.

Resumen: El propósito de este artículo es la consideración de los principales elementos de los impuestos en una economía digital. Sobre la base del análisis del estudio, se concluyó que, en condiciones de economía digital, el desarrollo de los recursos de información proporciona una concreción de las disposiciones de los principales elementos de la tributación y optimiza la aparición y el cumplimiento de los deberes constitucionales de pagar impuestos., así como el cálculo de los importes de impuestos. Las principales disposiciones y conclusiones pueden utilizarse en actividades científicas y prácticas al considerar los problemas de la construcción legal de impuestos.

Palabras clave: actividades prácticas, construcción jurídica, economía digital, fiscalidad.

INTRODUCTION

In modern conditions, it is impossible to imagine the function and development of the State and society without the use of digital technologies (Gainous: 2018). This applies to the tax law in general and to tax administration in particular. However, the development of new digital technologies requires careful analysis and improvement of legal regulation, one of the directions of which the question of the elemental composition of the tax has remained (Zhang: 2018; Shestak et al.: 2019).

The digital world also exacerbates a number of already-existing soft spots in the international tax regime. Global digital transactions involving digital goods and services, as well as intangible assets are characterized in part by their intangible nature and ease of crossing national borders. Moreover, the digital world facilitates cross-border collaboration, production, and sales of these intangible goods and services. Other tax challenges arising from the digital world include the usage of new payment systems such as bitcoin and the enhanced trading of personal information for ‘free’ services in the cross-border business-to-consumer social network context (Cockfield: 2018; Bacache-Beauvallet & Bloch: 2017; Olbert & Spengel: 2017).

Elements of the tax can be defined as internal initial functional units, which constitute together legal constructions of the corresponding tax payments. The composition of these functional units of all taxes is basically the same, so they are universal. When establishing tax payments, constructive elements are directly defined by legislative acts for each tax separately. The concept of "elements of taxation" has not been legislated directly, but the term itself is used by the Tax Code of the Russian Federation. Legislative establishment of taxes is carried out through the description of the elements of taxation (Nellen: 2015; Singh: 2017).

The tax is considered established only in that case when taxpayers and elements of taxation have been identified, namely, the object of taxation, tax base, tax period, tax rate, tax calculation procedure, the procedure, and terms of tax payment. In appropriate cases upon determination of the tax act of legislation on taxes and fees can also provide tax benefits and grounds for their use by the taxpayer. In this regard, in the scientific literature, scientists divide the elements of the tax into mandatory and optional. In the absence of even one obligatory element, the tax is not considered to be established and not to be a subject to levy. The optional elements include tax relief. The absence of a tax benefit does not affect on the invalidity of the tax. Among mandatory elements of the legal construction of the tax there are also those that are established by the legislative (representative) bodies of the subjects of the Russian Federation and local self-government in respect of regional and local taxes. Thus, according to paragraphs 3.4 of Article 12 of the Tax Code of the Russian Federation, when establishing regional taxes, legislative (representative) bodies of State power of the constituent entities of the Russian Federation may determine: tax rates, order (procedure) and terms of payment of taxes (if these elements of taxation are not established by the Tax Code of the Russian Federation). Similar rules apply while establishing local taxes.

Thus, such tax elements as the object of taxation, the tax base, the tax period, the procedure for calculating the tax, and taxpayers are always determined by the Tax Code of the Russian Federation. The composition of the tax specified in Article 17 of the Tax Code of the Russian Federation is considered in the narrow sense.

In the broader terms, the composition of the tax is the maximally detailed list of elements and includes: the regulatory basis, the taxable entity, the amount of tax, the time (terms) for payment, the responsibility for the commission of a tax wrongdoing, the taxpayer's right to appeal against the actions of tax authorities (Tsindeliania: 2016, pp. 3937-3946).

It should be noted that this sphere of social relations has been subjected to the most frequent changes; it also affects the very system of national tax law.

It is important to note that “for today, the regulation of fiscal levies in Russia is such that an important role is assigned to the judiciary in determining the elements of taxation (fees)” (Vasyanina: 2015, pp. 23 - 26). Based on the literature analysis, we found out that there is no single opinion relating to the taxation of products in digital economy. Therefore, the purpose of this study is to review and identify the main elements of taxation in the digital economy, such as the taxpayer, the object of taxation, the tax base, the tax rate, and the tax calculation procedure.

1.METHODS

The digital economy is a kind of economy that is almost completely tied to using the Internet. Clients, and often resources, are mined through the global network. Figure 1 depicts the main elements of the digital economy.

Figure 1. Objects of Digital Economy in the Taxation Sphere

This article analyzed the Tax Code of the Russian Federation, specifically Article 19, Article 226 of the Tax Code, paragraph 1 of Article 24, Articles 21-23, paragraph 1 of Article 38, and paragraph 3 of Article 45. Methods used to analyze the Tax Code were the system analysis, comparative-legal method, formal-legal method, historical-legal method, and generalization method.

2.RESULTS

A taxpayer or a taxable person is one of the necessary elements of the legal construction of the tax, without which the tax cannot be recognized as established. According to the definition given in Article 19 of the Tax Code of the Russian Federation, organizations and individuals are recognized as taxpayers; if they are obliged to pay taxes in accordance with the code.The considered definition is general and intended to designate a certain group of subjects of tax legal relations.

The payment of tax is the stage of fulfillment of the tax obligation and, if we systematically examine the rules of the Tax Code of the Russian Federation, then it can be noticed that tax payments are not always assigned to the taxpayer, which is due to the tasks of tax administration and the need to create a convenient way of fulfilling the tax obligation.

For example, Article 226 of the Tax Code defines the procedure of calculating and paying taxes on personal income by tax agents. According to the second paragraph of this Article, tax agents, except for a number of cases specified in the Tax Code of the Russian Federation, must calculate the amount of tax and pay it in respect of all incomes of the taxpayer, whose source is the tax agent.

The introduction of the tax by a tax agent is not a feature of only the personal income tax. There are similar rules in the chapters defining the procedure for payment of value added tax and profit tax. It is necessary to pay attention to the fact that according to paragraph 1 of Article 24 of the Tax Code of the Russian Federation, the tax agent is charged with calculating.

Thus, the tax agent does not pay the tax but transfers it after deduction from the taxpayer, and in this case, it will be decisive - who was the owner of the funds sent to the budget system. But this distinction is not valid in the case of taxes attributable to indirect taxes, which are currently recognized the value-added tax and excises. At the moment, payment of tax for a taxpayer can be made by another person (as will be discussed in more detail below), and this also changes the requirement to track the direct connection of funds received with the budget to the taxpayer.

The general list of rights and duties of the taxpayer is fixed in Articles 21-23 of the Tax Code of the Russian Federation. However, this list is not closed, and it means the presence of additional rights and obligations contained in other Articles of the Tax Code of the Russian Federation. The list of rights and obligations of a taxpayer may vary depending on the type of taxpayer. For example, the Tax Code of the Russian Federation allocates such types of taxpayers and determines for them additional rights and obligations, as interdependent persons, controlled foreign companies and persons, controlling them, a consolidated group of taxpayers, etc. Formation of the information space, taking into account the needs of citizens and society in obtaining quality and reliable information in the conditions of development of the digital economy, allows providing the information resource "Personal account of the taxpayer" on the website of the Federal Tax Service of the Russian Federation.

According to paragraph 1 of Article 38 of the Tax Code of the Russian Federation, the object of taxation is the sale of goods (works, services), property, profit, income, expense or other circumstance that has a value, quantity or physical characteristic, the existence of which the legislation on taxes and fees links the occurrence of taxpayer obligation to pay tax. Some authors define the object of tax as a subject to taxation (Khodskiy LV, Isaev AA, Akinin PV, Zhidkova E.Yu., etc.).

The tax name often follows from the object of taxation, for example, the tax on profit, property tax, land tax, etc. What exactly is the object of the tax (profit, property, income, expense, etc.) is specified in part two of the Tax Code of the Russian Federation in the study of a certain tax; and it should be noted that when considering specific taxes, the legislator determines the "object of taxation" (personal income tax, land tax, tax, etc.) and "objects of taxation" (water tax), despite the fact that more than one is always associated with taxation objects. In the science of tax law, it is reasonably noted that in the Tax Code of the Russian Federation, there is no definition of the object of taxation as such, we see only certain types of economic activity. Legislative consolidation of the category "object of taxation" is an unconditional basis for its existence in legal doctrine. Also, this fact raises doubts about the need for the existence of a separate category "tax object." But, despite the tendency in the legal science of identifying the concepts of "tax object" and "object of taxation," there is an opinion that there are certain distinctions between these concepts.

In general, we can distinguish two opposing views on this issue, whose supporters do not raise or raise objections to the complete identification of the concepts "tax object" and "tax object."

Therefore, due to the fact that this issue has not been sufficiently studied in the science of financial and tax law, it is difficult to make a clear distinction between the meanings of the concepts "object of taxation" and "tax object." At the same time, one should agree that the presence in the legal doctrine of the category "tax object" along with the object of taxation is necessary. In this connection, in this article the terms "object of taxation" and "tax object" are considered as synonyms. If you turn to property taxes, for example, to the tax on the property of individuals, then residential houses, apartments, rooms, car places, etc. with ownership ofthese objects are the object of taxation. In this context, it is rightly noted that the right of ownership, which is the basis of personal rights and freedoms, also serves the public interest of taxation. The object of land tax is land plots that are both in the ownership right and owned by taxpayers on the right of permanent (unlimited) use or the right of lifetime inheritable possession. If there is a right of gratuitous use of the land plot or its lease, which by definition are characterized by a much less stable legal relationship with the taxpayer, then the object of this tax is absent (Cockfield: 2002).

In view of the foregoing, it can be concluded that objects of property taxes are not individually taken property, apartment, land or vehicle, and at the same time, a legal fact related to the right of ownership, the right to lifetime inheritable possession or the right of permanent (perpetual) use land plot. Taxes whose objects are associated with the fact of the performance of certain operations are rather common. For example, an object of value added tax arises from the performance of operations for the sale of goods, works, and services, which are accompanied by the transfer of ownership from one person to another. However, the same tax as an object provides other transactions not related to the transfer of ownership. The excise is similar in construction. Such taxes actually form a separate group of taxes, the objects of which may have a mixed legal nature.

It is obvious that the tax base is regarded as a cost, quantitative, or physical characteristic of the object of taxation, which is determined for each tax independently. One cannot but agree with the opinion of scientists that the tax base is one of the tools of the State's tax policy, and this, in turn, allows the regulatory function of the tax to be realized.

The main function of the tax base, as A.V. Demin considers, is to express the object of taxation quantitatively, i.e., measure it. For this, it is necessary to select a parameter that will be used as the basis for measuring the object of taxation. However, the tax base is not just a parameter. It is a parameter expressed in certain tax units, i.e. the tax base is the size (value) of the object of taxation in units of taxation. Since the tax base and the procedure for determining they are established for each tax separately, the task of the legislator is to select from the set of possible parameters of the object of taxation the most optimal and then determine the procedure for calculating the tax base in relation to a specific tax. It is rather often, such parameters coincide for different taxes, but the tax bases are always calculated differently (Babin & Vakaryuk: 2018).

Most often, in practice, a cost (money) parameter is used. The value (monetary) parameter has VAT. Physical parameters represent a variety of physical characteristics, including area, volume, power, mass, etc. Water and transport taxes are an example (Babin & Vakaryuk: 2018, pp. 21-40). Today, the definition of the tax base for personal property tax based on the cadastral value of real estate remains one of the topical issues.

It is also disputable to establish a date with which the cadastral value, revised according to the results of the contest, is valid. In accordance with Article 403 of the Tax Code, in the event of the change of the cadastral value of the property object, according to the decision of Commission on consideration of disputes on results of definition of cadastral cost or judgment of any court, a new information about the cadastral value is taken into account when determining the tax base, starting with the tax period in which the relevant application has been submitted. Given the fact that the taxpayer actually learns about the tax base and tax liability upon receipt of a tax notice (i.e., in the new fiscal period), this provision requires adjustments (Shestak & Volevodz: 2019). The tax base is determined with the help of the methods that include: direct, indirect, conditional, lump-sum. For example, to calculate the profit tax, a direct method is used, which means measuring the tax base based on objectively existing and documented indicators.

The process of levying taxes will be effective only when the tax base accurately characterizes and determines the object of taxation. At the same time, the dependence between financial indicators and tax liabilities should be taken into account. The reliability, completeness of the collected and processed by the tax authorities with the help of digital technologies will allow improving the applicable tax forms in future. In order to ensure this process, it is necessary to harmonize tax and accounting legislation. On the one hand, themethodological approach to calculating the tax base based on accounting data requires the formation of accounting data with a greater degree of objectivity. On the other hand, the tax legislation must take into account the specifics of the formation of accounting indicators when choosing the limitations and norms that determine the method of calculating the tax base. In conditions of development of digital economy it will allow ordering algorithms of data processing and access to such data.

The tax rate as an obligatory element of taxation means the amount of tax per unit of taxation and is established either in a firm amount or as a percentage of the value of the object of taxation, or in a combined version.

In the Russian tax system, there are all three versions for setting a tax rate. However, most of the discussion for the science and practice the method of taxation, under which tax rates can be proportional, progressive, and regressive or out depending on the value received by a taxpayer income seems to be. The application of this or that method of taxation largely depends on the tax policy pursued by the State. A striking example is a tax to incomed of individuals.

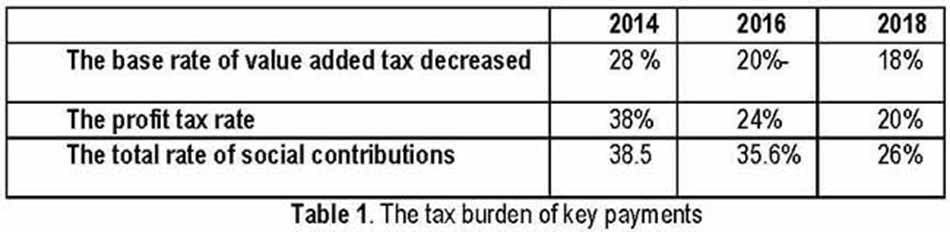

In Russia, a socially-oriented market model that assumes a higher level of social protection with increased demands on the level of the tax burden on the economy is implemented. Although Russia's historical experience of the last twenty-five years demonstrates the process of gradual reduction of the tax burden of key payments (see Table 1), in the ongoing crisis, authorities took a different course in the development of the tax system.

In the arsenal of the State, there are also latent instruments in the form of including or increasing additional coefficients to tax rates, which, on the background of unchanged rates, lead to an increase in the tax burden.

Since the spring of 2016, the Russian Federation, among 192 countries, became a member of the Paris Agreement in accordance with the United Nations Framework Convention on Climate Change (Rio de Janeiro, 1992), which includes, among other things, elements of environmental taxation, it is actual to use tax instruments in the field of environmental management. In this connection, it is of interest, for example, that regions can introduce a differentiated tax rate for transport tax, depending on the ecological class of the vehicle, which, unfortunately, has not yet found wide application in Russian regional legislation. At the same time, the positive foreign practice of the acute problem of large cities in reducing emissions of harmful substances into the atmosphere has shown the effectiveness of this tool.

Of course, the question of the success of the introduction of a progressive scale of income tax for individuals, as well as the need to raise tax rates for key taxes remains controversial. The tax policy should be correlated with the basic principles legislated by the national tax system (Article 3 of the first part of the Tax Code RF). In this connection, it is interest the scientific understanding of the principles:

(…) the scientific nature of taxation, the equality and fairness of taxation, the uniformity of taxation, the basis of taxation, the universalization of taxation, the differentiation of tax rates, the stability of tax rates, the application of progressive tax rates and the degree of their progression, with the predominance of proportional rates (Lavrenchuk: 2013, pp. 18-24).

Another element of the legal composition of the tax, established by Article17of the Tax Code of the Russian Federation, is the procedure and terms for payment of the tax. The procedure for payment of a tax is technical methods for a taxpayer, his representative, or tax agent to deposit the amount of tax in the budget system of the Russian Federation. General rules for payment of taxes are established in Article 58 of Part One of the Tax Code of the Russian Federation, and specific - by the relevant Chapter of part two of the Tax Code of the Russian Federation, which regulates a certain tax.

On November 30, 2016, amendments to the Tax Code of the Russian Federation came into effect that provide for the possibility of paying taxes (Article 45, paragraph 1, of the Tax Code of the Russian Federation); and of the insurance premiums (clause 9 of Article 45 of the Tax Code) by other persons, i.e. persons who are not a taxpayer, its representative or a tax agent. At the same time, this Article does not say which persons can fulfill the taxpayer's duty to pay tax. The above-mentioned other persons will also be able to reimburse damage for taxpayers caused to the budgetary system of the Russian Federation as a result of crimes for which criminal liability is provided (Articles 198-199.2 of the Criminal Code of the Russian Federation). In this case, the tax obligation will be considered fulfilled (subparagraph 7 paragraph 3 of Article 45 of the Tax Code of the Russian Federation).

Thus, now it became possible to pay the tax, for example, for close relatives. It should be noted that earlier such a situation was impossible, and the tax paid by another person (even close relatives) at its own expense could not be credited by the tax authorities: in this case, the taxpayer would have arrears with all the ensuing consequences (penalties and fines). However, another person who has paid the tax is not entitled to demand a tax refund paid for the taxpayer from the budgetary system of the Russian Federation.

Such changes in the legislation on taxes and fees will certainly stimulate the timely receipt of mandatory payments to the relevant budgets of the budgetary system of the Russian Federation. Earlier, in 2015, the Federal Tax Service of the Russian Federation in its letters noted that, in connection with the expansion of opportunities for taxpayers, individuals to pay taxes and fees, including electronically through electronic services of the Federal Tax Service of Russia, Sberbank of Russia and other banks, a requirement for self- payment of the tax "only for myself "is an obstacle to the establishment of the most comfortable conditions for fulfillment of tax obligations by the taxpayers.

Noting the usefulness of this innovation, it should nevertheless be noted that some technical points remained unresolved. For example, Chapter 23, "Personal Income Tax", part of the second Tax Code of the Russian Federation introduced a rule of law, according to which revenues in the form of taxes, fees, insurance premiums, penalties, fines paid for a taxpayer by another individual (paragraph 5 of Article 208 of the Tax Code of the Russian Federation) are not recognized as income for the purposes of the said Chapter. Thus, it can be said that there has been a confusion of the concepts of "tax payment procedure" and "tax object." In connection with the above, a number of questions have appeared. Why were such additions not included in Chapter 25 "Corporate Profits Tax" of the Tax Code of the Russian Federation? Does this mean that the innovation extends only to the situation when an individual pays a tax for another individual? If the tax for an individual is paid by an organization or an individual entrepreneur, whether it will be income of a natural person, including if it is paid to a person for work. While noting the usefulness of this novel in general, it should nevertheless be noted that some issues of legal regulation have remained unresolved, and this is likely to be resolved by enforcement practice.

3.CONCLUSION

Payment of taxes as the main criteria for determining a taxpayer is not simply a wire transfer of taxes to the budget, but a procedure for the pursuance of an individual’s duty, including the various stages where participation of other entities is possible, if permitted by the law, so the legal status of the taxpayer does not change from the fact that the introduction of taxes into the budget system is not by them, but by anotherperson. The taxpayer has a connection with the State and other subjects of tax law, including tax authorities, which is realized through tax legal relations. Such a connection supposes the personal participation of the taxpayer in financing the activities of the State and (or) municipal entities in the amount and order, determined by law, and also includes the right of the State to apply coercion to the taxpayer carried out by special authorized bodies in the forms, prescribed by the law. That is why the definition of the range of subjects which are charged with the duty to pay a specific tax, is an obligatory element of this tax, without which it cannot be considered established. Further development of advanced digital technologies in tax administration will allow providing automatic handling of large volumes of data (big data), more efficient tax collection, more comfortable environment for the taxpayer, and, ultimately, the development of the national digital economy.

BIODATA

I A. Tsindeliani: Imeda Tsindeliani lives in Moscow, Russian Federation. He is a Candidate of Law. He works as head of department, associate professor of the Department of Financial Law of Russian State University Justice. The research interests of the author are financial law, administrative law (antitrust regulation and migration law), civil law insolvency (bankruptcy). A recent study of the author is “The Modern System of Russian Financial Law: Conceptual Approaches”.

K T. Anisina: Karina Anisina lives in Moscow, Russian Federation. She is a Candidate of Legal Sciences. She works as an associate professor of the Department of Financial Law of Russian State University Justice. The research interests of the author are financial law, mandatory payments to extra-budgetary funds, tax law, enforcement proceedings. A recent study of the author is “Legal regulation of the construction of Russian oil pipelines”.

A S. Burova: Anna Burova lives in Moscow, Russian Federation. She is a Candidate of Legal Sciences. She works as a professor of the Department of Financial Law of Russian State University Justice. The research interests of the author are issues of financial and tax law. A recent study of the author is “Legal nature of relations on the collection of notary tariffs by public and private notaries”.

A A. Kopina: Anna Kopina lives in Moscow, Russian Federation. She is a Candidate of Legal Sciences. She works as a deputy head of scientific work, professor of the Department of Financial Law of Russian State University Justice. The research interests of the author are financial rights, tax law, budget law, financial monitoring. Recent studies of the author are “Actual problems of financial law”, “111 Tax Law Terms: A New Look”.

E V. Migacheva: Elena Migacheva lives in Moscow, Russian Federation. Elena is a Candidate of Legal Sciences. She works as a professor of the Department of Financial Law of Russian State University Justice. The research interests of the author are tax law issues, tax offenses. Recent studies of the author are “Mandatory payments to the road fund”, “Ensuring financial security in the process of tax control”.

V E. Rodygina: Veronika Rodygina is from Moscow, Russian Federation. She is a Candidate of Legal Sciences. She works as a professor of the Department of Financial Law of Russian State University Justice. The research interests of the author are issues of tax law of the Russian Federation and foreign countries, regulatory accounting. A recent study of the author is “Digitalization of VAT tax control: legal implications and prospects”.

BIBLIOGRAPHY

BABIN, II & VAKARYUK, LV (2018). “Features of Legal Regulation of Tax Incentives for Small Business in Post-socialist Countries”, SOCIETAS ET IURISPRUDENTIA, 6(1), pp.21-40.

BACACHE-BEAUVALLET, M & BLOCH, F (2017). “Special issue on taxation in the digital economy”, Journal of Public Economic Theory, 20(1), pp. 5–8.

COCKFIELD, AJ (2002). “The law and economics of digital taxation: challenges to traditional tax laws and principles”, Bulletin for International Fiscal Documentation, 56(12), pp. 606-619.

COCKFIELD, AJ (2018). Taxing Global Digital Commerce in a Post-BEPS World Ricardo Maitto da Silveira, Alexandre Luiz Moraes do Rêgo Monteiro and Renato Vilela Faria, eds., Tributação da Economia Digital– Desafios no Brasil, experiência internacional e novas perspectivas (Editora Saraiva, Brazil.

GAINOUS, J, WAGNER, KM & ZIEGLER, CE (2018). “Digital media and political opposition in authoritarian systems: Russia’s 2011 and 2016 Duma elections”, Democratization, 25(2), pp. 209-226.

LAVRENCHUK, EN (2013). “Characteristics of taxes in Russian Federation”, American Journal of Economics and Control Systems Management, 2(2), pp.18-24.

NELLEN, A (2015). “Taxation and today’s digital economy”, Journal of Tax Practice & Procedure, 17(2), pp. 17-26.

OLBERT, M & SPENGEL, C (2017). “International taxation in the digital economy: challenge accepted”, World tax journal, 9(1), pp. 3-46.

SHESTAK VA & VOLEVODZ AG (2019). “Modern requirements of the legal support of artificial intelligence: a view from Russia”, Russian Journal of Criminology, 13(2), pp. 197–206. (In Russian).

SHESTAK VA, VOLEVODZ AG & ALIZADE VA (2019). “On the possibility of doctrinal perception of artificial intelligence as the subject of crime in the system of common law: using the example of the U.S. criminal legislation”, Russian Journal of Criminology, 13(4), pp. 547–554. (In Russian).

SINGH, MK (2017). “Taxation of Digital Economy: An Indian Perspective”, Intertax, 45(6), pp. 467-481.

TSINDELIANIA, IA (2016). “Tax Law System”, International journal of environmental & science education,11(10), pp. 3937-3946.

VASYANINA, EL (2015). Powers of the Russian courts in the consideration of disputes arising in the sphere of establishing fiscal levies, Taxes, 3, pp. 23 - 26.

ZHANG, L, CHEN, Y & HE, Z (2018). “The effect of investment tax incentives: evidence from China’s value- added tax reform”, International Tax and Public Finance, 25(4), pp. 913-945.