Artículos

Received: 17 July 2020

Accepted: 18 August 2020

DOI: https://doi.org/10.5281/zenodo.3987580

Abstract: A sample of 250 students (121) males and (129) females in grades 10-12 participated in this study of their preferred thinking methods. The Methods of Thinking Assessment, which was prepared by Sternberg and Wagner (1991), was used as the data gathering tool. Analysis of data revealed that the preferred methods of thinking were in descending order; legislative, external, hierarchical, judicial, conservative, anarchist, local, internal, monarchic, and global. Also, analysis of data revealed significant differences in all dimensions of the overall score being better for female students; however, no significant differences were found about grade level.

Keywords: Learning styles, Preferred thinking methods, Thinking methods, Thinking styles..

Resumen: Una muestra de 250 estudiantes (121) hombres y (129) mujeres en los grados 10-12 participaron en este estudio de sus métodos de pensamiento preferidos. Los métodos de evaluación del pensamiento que fueron preparados por Sternberg y Wagner (1991) se utilizaron como herramienta de recopilación de datos. El análisis de los datos reveló que los métodos de pensamiento preferidos estaban en orden descendente; legislativo, externo, jerárquico, judicial, conservador, anarquista, local, interno, monárquico y global. Además, el análisis de los datos reveló diferencias significativas en todas las dimensiones de la puntuación general que es mejor para las alumnas

Palabras clave: Estilos de aprendizaje, Estilos de pensamiento, Métodos de pensamiento preferidos, Métodos de pensamiento..

INTRODUCTION

As one of the areas in Indonesia, Batam is one area that continues to carry out development to progress, the development of an area would require substantial funding and planning. In running an administration area, in this case, the city of Batam, local revenue is key in determining fast or slow development in Batam. Understanding Local Revenue according to Act No. 33 of 2004 on Financial Balance between Central and Regional Article 1 paragraph 18 that "revenue, after this Referred to as PAD is the earned income areas levied by local regulations following the legislation." Local Revenue (PAD) is regionally sourced from the local income tax, the result of Retribution, the effects of the wealth management and other areas separated local revenues are legitimate, the aims to provide flexibility to the regions in Mobilizing funds in the implementation of regional autonomy as the embodiment of the principle of decentralization.

Local taxes comes from state taxes handed over to the area as a local tax where the supply is carried out under the legislation. A local tax levied by the regions based on the strength of laws and regulations other laws, in this case, is regulated by the Regions. Then the local tax money used to fund the implementation of the household affairs of the area or to finance local expenditure as a public legal entity. Then the next local revenue sources are Retribution Retribution where are local taxes as payment for the use or acquire the services of employment, business or area belonging to the public interest, or for services rendered by either indirectly or indirectly area. Implementation charges levied by region and imposed on anyone who utilizes or services supplied sniffing area. Currently the management of zakat in Batam yet a part of the revenues, in Indonesia, only the province of Aceh that has specific policies related to the management of zakat to be used as part of the local income before taxes and Retribution. In Islam, zakat is a treasure that must be removed if it has met the requirements to be set and distributed to Reviews those who deserve it. Therefore, the application of zakat as local revenue should be adjusted and regulated by special rules. Use of Zakat as one source of income (PAD) cannot be equated with taxation and Retribution areas where charity should be treated specially in its management. This is because, zakat Obtained distribution cannot be delayed, so it does not necessarily follow that the government budgeting mechanism carried out per year. Zakat as one source of revenue is only applicable in the province of Aceh. This was the following Reviews those set out in Article 180 paragraph (1) letter d of Law Number 11 the Year 2006 concerning the Government of Aceh. However, the management of zakat funds should be treated specially, because charity is not a currency area in general and the existing rules of how to channel it. According to general terms, Maslahah is to bring all forms of expediency or reject any possibility that damage. More details maslahah is an expression of easements or anything that is associated with it, while the cost is the things that are still associated with it, while the price is the things that are painful or anything that is affiliated. Judging from the material, maslahah divided over the public good and private benefit the good public roommates (maslahah umma) is concerning the interests of the people. This does not mean the public good for the benefit of everyone, but it could take the form of the majority of the people.

LITERATURE AND DEVELOPMENT HYPOTHESIS

Local Tax

Said the tax is not derived from the Arabic for the letter "p" does not exist in Arabic consonant. However, the translation of the Qur'an there is 1x the word "tax," God said that on translation: “Fight Reviews those who believe not in Allah and (also) the day then, and they do not forbid that the which has been banned by Allah and His messenger and not the religion that is true (Islam), (i.e., people) who the Book to them until they pay the jizya with a willing submission they are in a state of subjection.” (Qur'an, At-Tawbah: 2000). "And do not confuse the rights mixed with falsehood, and do not hide that it is right, for you know." (Qur'an, Al Baqarah: 2000)

Tax is one source of government revenue to finance both routine and development expenditures. As the financial resources of the State. The government seeks to incorporate as much money to the state treasury. Currently, the government can disseminate to the public to Participate to Be Obedient in paying taxes. This is done by way of legislation Enhance existing taxation and imposition of onerous if the taxpayer cannot pay taxes payable to the State Treasury promptly. Understanding the burden According to some experts, among others.

The understanding of tax under Latif (Latif: 2016) is a retribution of society by the State (government) based on laws that are enforceable and payable shall pay not to get the achievement back (contra/remuneration) directly, the results of which are used to finance State spending in governance and development.

Retribution

He knows that there will be among you those who are ill and those who walk on the earth may seek the gift of God; and other people again who fight for Allah, then recite what is easy (for you) of the Qur'an, and establish worship, pay the poor-due, and give a loan to Allah a good investment. And whatever you do to yourself you would have been obtained (return) it on the side of God as a reward the best and the greatest reward. And ask forgiveness of Allah; Allah is Forgiving, Merciful. (Qur'an, Al-Muzzammil: 2000; Sukier et al.: 2020).

Retribution areas certain payment for services or permits individual provided or provided by local Governments for the benefit of private persons or entities. According to Latif (Latif: 2016), retribution is a collection area as payment for specific services or permits individual provided or provided by local Governments for the benefit of private persons or entities. Such services can be said to be direct, which is only to pay the retribution roommates who enjoy remuneration from the state. One example is the retribution of health services at hospitals run by the government. Objects retribution is retribution on services provided or provided by local Governments. Not all can be levied by local government Retribution, but only certain kinds of services which, According to socio-economic considerations as an object worthy of Retribution.

Zakat

Allah says: “Parable (income incurred by) Reviews those who spend Reviews their wealth in the way of Allah is like a seed that grows seven ears, in every ear a hundred grains. God magnifies (reward) For Whom He will. And Allah is the area (his gift), the Knower.” (Qur'an, Surat al-Baqara: 2000). Zakat is an obligation that the great Islam. In the Qur'an, commands give charity several times juxtaposed with prayer command. Among them is the Word of God: “And Steadfast in prayer, pay the poor-due, and ruku` please with Reviews those who bow.” (Qur'an, Al Baqarah: 2000).tithe is A Certain amount of property that shall be issued by the Moslems and given to groups who deserve it (the poor and so on) According to the conditions set by syarak. Zakat is the third pillar of the Five Pillars of Islam. Zakat literally means "grow", "developing", "cleanse" or "clean". While the terminology of Shari'ah, zakah refers to the activity provides most of the wealth in the amount and specific calculations for Certain persons as specified. Zakat is one of the pillars of Islam and became one of the principal elements for the enforcement of Islamic Shari'a. Therefore, the law of zakat is obligatory (fard) for every Muslim who has fulfilled certain conditions. Zakat included in the category of worship such as prayer, pilgrimage, and fasting, which has been provided in detail based on the Qur'an and Sunnah. Zakat is also a social and humanitarian charity that can be developed following the development of humanity.

Local Revenue

The Government and people responsible for the welfare of the people by looking for local revenue plumber legitimate and lawful, the commands of Allah: “And let the fear of God Reviews those who supposed to leave behind Reviews their weak children, they worry about the (welfare) them. Therefore, let them fear Allah andlet Them Correctly Pronounce words.” (Qur'an, An Nisa: 2000). Based on Law No. 33 2004 chapter 1 verse 15 describes that revenue is the revenue that the region from sources within its territory imposed under the bylaws following the legislation in force. Latif (Latif: 2016) states that local revenue is derived from the financial resources of each region. If the number of local revenue increases, then the area needs will be met for the prosperity of the people is also increasing.

Of the opinions Expressed above can be concluded that the revenue is one part of the local fiscal income derived from revenue sources within its own country imposed under the legislation in force and Become one of the capital base of local governments to finance the construction and shopping fulfill Reviews their areas.

Maslahah

To get maslahah then people should not be redundant, Allah ordered: “Son of Adam, wear beautiful clothes in every (enter) mosque, eat and drink, and do not exaggerate. Allah loves not Reviews those who exaggerated.” (Qur'an, Al A’raaf: 2000). Maslahah comes from the word meaning salaha, which means either the opposite of bad words or damaged. Maslahah is masdar one word, which means that benefits or irrespective of the damage. Maslahah in Arabic are acts that push the human kindness. In a general sense, all things that are beneficial to humans, both regarding interest or make a profit, or in the sense of avoiding such Rejecting or resist damage. Prosperity is the ability to make ends meet

Maslahah in control is a form of prosperity, and prosperity is the ability to make ends meet. The welfare of the local government can be seen from the PAD. The analysis used to calculate the health of the local government is proxied by the growth rate of PAD. The growth rate of PAD measure the ability of local governments to maintain or increase the success in collecting revenue from period to period. High revenue growth may indicate that the local government has made optimal Efforts in exploring sources of income in the region. Prosperity level will undoubtedly have an impact on improving the quality of public services as evidence of an increase in local government performance. (Safitri: 2019).

METHODS

Regional Revenue as Intervening Against Maslahah

God commands that all aspects of life Aimed at seeking maslahah, Allah says: “Those are the ones who buy the fallacy with the instructions, it is not fortunate to commerce them, and they are not guided.” (Qur'an, Al-Baqara) Based on Law No. 33 2004 chapter 1 verse 15 describes that revenue is the revenue that the region from sources within its territory imposed under the bylaws following the legislation in force. Suprayitno (Suprayitno: 2020, pp. 1-7) defines that income is the acceptance obtained area from sources within its region levied by local regulations following the law in effect. Of the opinions Expressed in the above, it can be concluded that the revenue is one part of the local fiscal income derived from revenue sources within its own country imposed under the legislation in force and become one of the capital base of local Governments to finance development and fulfill its regional spending. To enhance the independence of the region, local governments should seek to explore and improve Reviews their financial resources continually. One of the problems encountered in Efforts to Increase local revenue is a weakness regarding measurement/assessment of the polling area. Y production and fairness (Suprayitno: 2020, pp. 1-7).

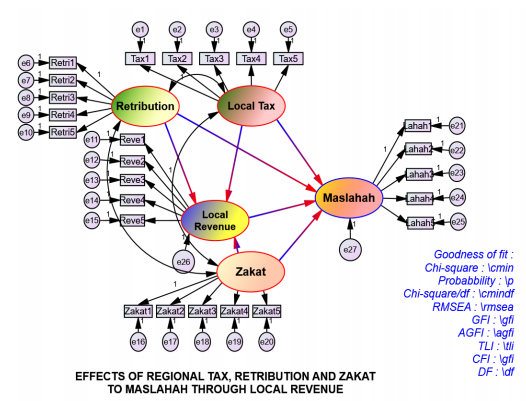

Model Thinking

The frame of mind is made based on the facts, observation and study of literature, supported by previous studies and therefore this framework contains a relationship or influence between the variables involved in the research by supporting documentation, and Cleary define the relationship between variables exists, and Also it can be used the base to solve the problems as well as a logic flow that exists between variables that will be very relevant to the issue under study.

Figure 1. Model Thinking

Hypothesis

1). Local Tax effect on the local revenue in Batam, 2). Effects Retribution to the local income in Batam, 3). Zakat effect to the local income in Batam, 4). Local Tax effect against Maslahah in Batam, 5). Retribution against Maslahah effect in Batam, 6). Zakat effect against Maslahah in Batam, 7). Regional Income as intervening against maslahah in Batam.

Research Methods

In this study, the variables can be divided into independent variables (independent variables) are variables that effect, consisting of (X1) local taxes, (X2) Retribution, (X3) Zakat. Another variable is the dependent variable (dependent variable) is the variable that is affected, or roommates become due for Reviews their independent variables. In this study, there is a two dependent variable an intervening variable (intervening variable) is (Y) of Revenue, and the dependent variable (dependent variable) is (Z) Maslahah.

Population

A population is a group of people, events, something that has certain characteristics. If Researchers use all elements of the society into the research of data, it is called a census, if part of it is called a sample. (Suhendi: 2018). The population of this study was employees and administrators in the Office of the Management Board of Taxes and Retribution of Batam, Batam City Badan Amil Zakat-MUI, The Department of Public Welfare, and as many as 195 people.

Sample

The sample is an element of the population selected to represent the people in the research (van Bruinessen: 2018). In this study, the sample size adapted to the analysis, the models used is Structural Equation Model (SEM). In this regard, the sample size for SEM used the models estimates the maximum likelihood estimation(MLE) is 100-200 samples (Esposito & DeLong-Bas: 2018), or as much as 5-10 times the number of parameters estimated (Kuforiji: 2019). In this study, the number of respondents of 195, then the amount of the sampled using the census as many as 190 respondents, consisting of:

Table 1. Respondents Table.

RESULTS

Effect Analysis with SEM

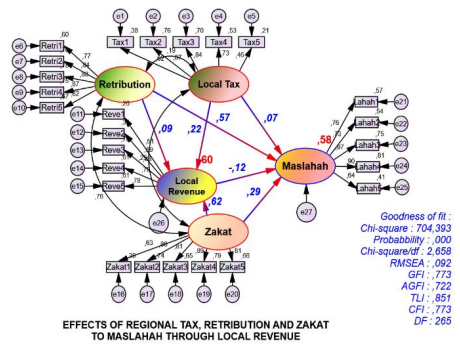

By the purpose of the Study to Determine the Effects of Local Taxes, Retribution, Zakat, Local Revenue, and Maslahah, the Data was Analyzed using Structural Equation Modeling (Structural Equation Modeling = SEM) the which is a set of statistical techniques that allow testing of a series of relationships that are Relatively complicated simultaneously. To simplify the analysis, the hypothesis made in the equation models SEM as follows:

Figure 2. The full model of Taxes Local Variables, Retribution, Zakat, Regional Income, and Maslahah.

Based on the picture above, do the analysis of the measurement models with parameter lambda,structural model analysis, and analysis of determination, Goodness of Fit to effect Local Taxes, Retribution, Zakat, Local Revenue, and Maslahah.

Testing Analysis Model Parameter Measurement with Lamda ( i)

To test the parameters, lambda uses a standardized value estimate (regression weight) in the form of a loading factor. If the value of the standardized estimate (regression weight) (Importar imageni)> 0:50, CR> t table = 2.000, and Probability (P).

Table 2. Standardized Regression Weights Indicator Local Taxes, Retribution, Zakat, Local Revenue,and Maslahah

Table 3. Regression Weights Indicator Local Taxes, Retribution, Zakat, Local Revenue, and Maslahah

Measurement Analysis of Determination

Analysis of the measurement models with determination is used to determine the contribution of exogenous variables on endogenous variables for this analysis of used square Multiple Correlation. Multiple Correlation magnitude Square can be seen in the following table.

Table 4. Squared Multiple Correlations: (Group number 1 - Default model)

After a discussion of the theory and implementation of the study, the results of this study can be summarized as follows:

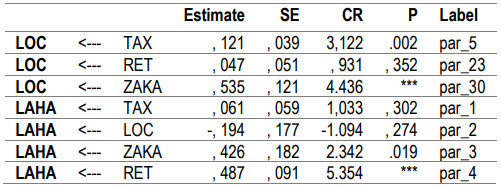

1) Tax latent variable effects on the latent variables of Revenue has standardized estimate (regression weight) of 0.221 to Cr (Critical ratio = identical to the value t-test) of 3,122 on probability = ***. CR value 3,122> 2,000 and Probability = *** <0.05 indicates that the latent variables Taxes on Income latent variable area is a significant positive. This study demonstrates the truth verse of the Qur'an "Fight Reviews those who believe not in Allah and (also) the day then, and they do not forbid that the which has been forbidden by Allah and His messenger and not the true religion (Islam), (i.e., people) who the Book to them until they pay the jizya with a willing submission they are in a state of subjection.”( Qur'an, At-Tawbah: 2000)

2) Retribution against a possible variable effect of the latent variables of Revenue has the standardized estimate (regression weight) of 0.093 to Cr (Critical ratio = identical to the value t-test) of 0.931 on a probability = 0.352. CR value 0.931 <2.000 and Probability = 0.352> 0.05 indicates that the Securities latent variable levies against latent variables of Revenue was positively insignificant. These findings share Word of Allah: "He knows that there will be among you those who are ill and those who walk on the earth may seek the gift of God; and other people again who fight for Allah, then recite what is easy (for you) of the Qur'an, and establish worship, pay the poor-due, and give loan to Allah a good loan.” (Qur'an, Al-Muzzammil: 2000)

3) Zakat latent variable effect to the regional revenue has standardized estimate (regression weight) of 0.617 to Cr (Critical ratio = identical to the value t-test) of 4.436 on a probability = ***, Value CR = 4.436>2.000 and Probability = *** <0.05 indicates that the latent variable Securities Zakat against latent variables of Revenue is a significant positive. This analysis strengthens theory in the Qur'an "Parable (income incurred by) Reviews those who spend Reviews their wealth in the way of Allah is like a seed that grows seven ears, in every ear a hundred grains. God magnifies (reward) For Whom He will. And Allah is the area (his gift), the Knower. “(Qur'an, Al-Baqara: 2000)

4) Local taxes latent variable effect on revenue against latent variables Maslahah have standardizedestimate (regression weight) of 0,067 to Cr (Critical ratio = identical to the value t-test) of 1,033 on probability= 0.302. CR value 1.033 <2.000 and Probability = 0.302> 0.05 indicates that the hidden variable Securities Exchange Taxes on Maslahah latent variable is not significantly positive. The greater the payoff means, the greater the role of local taxes on revenue, and vice versa if the result of the comparison is too small means that the role of local taxes on revenue IS ALSO small (Furqani et al.: 2019, pp. 391-411). These findings are evidence of the truth of the Qur'anic passage, "And do not confuse the rights mixed with falsehood, and do not hide that it is right, for you know." (Qur'an, Al Baqarah: 2000) Withdrawal of Local Tax law is based positive (non-Islamic) so that its contribution Maslahah (inner and outer well-being and the world hereafter) is positive, not significant,

5) Zakat potential variable effect against latent variables Maslahah has a standardized estimate (regression weight) of 0.294, with Cr (Critical ratio = identical to the value t-test) of 2.342 on a probability =0.294. CR value 2.342> 2.000 and Probability = 0.019 <0.05 indicates that the Securities latent variables Maslahah Zakat against latent variables are significantly positive. The Word of God supported this research: "Parable (income incurred by) Reviews those who spend Reviews their wealth in the way of Allah is like a seed that grows seven ears, in every ear a hundred grains. God magnifies (reward) For Whom He will. And Allah is the area (his gift), the Knower. "(Qur'an, Al-Baqarah: 2000) Reviews those who give most of his wealth to the people in need with a sincere heart and solely for worshipping Allah. Then Allah will double the reward for Reviews those who spend Reviews their wealth, even if only a grain of rice then Allah will double one. Because God is omniscient, all-seeing again, this is God's promise to contribute alms to the significant positive maslahah.

6) Regional Income latent variable effect against latent variables Maslahah have standardized estimate (regression weight) of -0.116, with Cr (Critical ratio = identical to the value t-test) of -1,094pada probability = 0.274. -1.094 CR value <2.000 and Probability = 0.274> 0.05 indicates that the latent variables Effects of Revenue against Maslahah latent variable is not the significant negative. This research is the Word of God: "And let the fear of God Reviews those who supposed to leave behind Reviews their weak children, they worry about the (welfare) them. Therefore, let them fear Allah and let them Pronounce words correctly”. (Qur'an, Al Nisa: 2000). Mandatory and important not to be defeated by vague (dissenting), therefore the area is an absolute revenue by source: local tax, donation, charity, and so forth. Evidence that areas dominated by local income taxes do not contribute maslahah, therefore local revenues should be maximized through potential zakat.

7) Retribution against the latent variable effect of the latent variable Maslahah have a standardizedestimate (regression weight) of 0.573 to Cr (Critical ratio = identical to the value t-test) of 5.354 on a probability= ***, CR Value 5.354> 2.000 and Probability = ** * <0.05 indicates that the Exchange levies against positive Maslahah significant latent variables. According to Barizah et al. (Barizah et al.: 2007), Retribution is a collection area as payment for specific services or permits individual provided or provided by local Governments for the benefit of private persons or entities. Such services can be said to be direct, which is only to pay the retribution roommates who enjoy remuneration from the state. One example is the retribution of health services at hospitals run by the government. Objects retribution is retribution on services provided or provided by local Governments (Ropi: 2017, pp. 101-116).

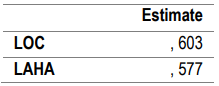

8) Multiple Correlation Square value for the variable of Revenue times 100% = 0,603X100% = 60.3%. Thus it can be stated that the change in Revenue is the effect of Taxes, levies, and Zakat of 60.3%. The rest ya 100% -60.3%. % = 39.7% is the effect of other variables that have not been included in this study. Value Square Multiple Correlation Taxes, Levies and Zakat and Income Regional determination = 0,577x100% = 55.7%. Thus it can be stated that the change is the effect Maslahah Taxes, Levies, and Zakat, and Income at 55.7%, the rest = 100% -55.7% = 44.3% is the effect of other variables that have not been included in this study. These findings show the effect of the independent variable selection of the dependent variable is quite appropriate for Multiple Correlation Square Values above 50%.

DISCUSSION

Analysis of Goodness of Fit

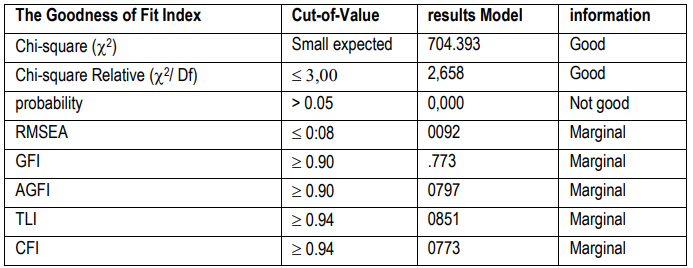

Based on test criteria, Chi-square ( 2), Relative Chi-square ( 2/ Df), RMSEA, GFI, AGFI, TLI, and CFI above and Goodness of Fit value Amos processing results as shown in the figure above, it can be prepared the following table.

Table 5. Evaluation of Goodness of Fit

By paying attention to the cut-of-value and goodness of fit model results in the Table above shows the seven criteria are met, eight tests were used. The requirements have met the Chi-square ( 2), Relative Chi- square ( 2/ Df) RMSEA, GFI, TLI, AGFI, and CFI, while only one Probability that is not good. Furthermore, seven of the eight criteria are met the required standards. The models can be expressed as a good model of (Ahmad & Hassan: 2017, pp. 968-978).

CONCLUSION

Based on the research and discussion that has been done in the previous chapter, it can be concluded as follows:

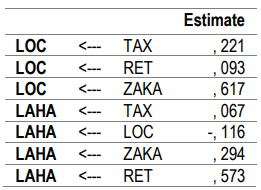

1) Tax latent variable effect on the latent variables of Revenue has standardized estimate (regression weight) of 0344 to Cr (Critical ratio = identical to the value of t-test) of 2,264 on probability = 0.024. CR value 2,264> 2,000 and Probability = 0.024> 0.05 indicates that the latent variables Taxes on Income latent variable is a significant positive area.

2) Retribution against latent variables influence on the latent variables of Revenue has the standardized estimate (regression weight) of 0080, with Cr (Critical ratio = identical to the value of t-test) of0822 on a probability = 0411. 0822 CR value <2.000 and Probability = 0411> 0.05 indicates that the effect of latent variables on the potential variable Retribution to Regional Revenue was positively insignificant.

3) Zakat latent variables influence the regional revenue has a standardized estimate (regression weight) of -0196 with Cr (Critical ratio = identical to the value of t-test) of -1991 on probability = 0.046. CR = - 1991 <2.000 and Probability = 0.046> 0.05 indicates that the effect of latent variables Zakat against latent variables of Revenue is negative not significant.

4) Tax potential variable effect against latent variables Maslahah has a standardized estimate (regression weight) of 0.028 to Cr (Critical ratio = identical to the value of t-test) of -1510 on probability = 0131.-1510 CR value <2.000 and Probability = 0131> 0.05 indicates that the effect of latent variables influence Maslahah Taxes on the latent variable is not the significant negative.

5) Retribution against latent variables influence on the latent variables Maslahah has a standardized estimate (regression weight) of -0044, with Cr (Critical ratio = identical to the value of t-test) of - 0410 on probability = 0.682. -0410 CR value <2.000 and Probability = 0.682> 0.05 indicates that the effect of the retribution on negative Maslahah latent variables was not significant.

6) Zakat potential variable effect against latent variables Maslahah has a standardized estimate (regression weight) of 0481, with Cr (Critical ratio = identical to the value of t-test) of 3703 on a probability =Importar lista***. CR value 3,703> 2,000 and Probability = ***> 0.05 indicates that the effect of latent variables Zakat Maslahah Significantly against latent variables is positive.

Latent variables influence of Revenue against latent variables Maslahah has a standardized estimate (regression weight) of -1101, with Cr (Critical ratio = identical to the value of t-test) of -4829 on probability =***. 4829 CR value <2.000 and Probability = ***> 0.05 indicates that the effect of the latent variables of Revenue against Maslahah latent variables is Significantly positive.

BIODATA

C. WIBISONO: Prof Chablullah Wibisono is a Lecture, Professor of Sharia Economics. Date of Birth is November 10, 1953, in Kendal. He is married and has four (4) Children. Lives in Sekupang, Batam City, Indonesia. His Current Job is Rector of UNIBA, Lecturer S1, S2, and S3 in UNIBA. Expert DPRD Riau Islands Province, DPS SRB States Madani, his Office address is Rectorate, University of Batam, Batam, Indonesia.

H. IRWANSYAH: Dr. H. Irwansyah is Doctor of Human Resource Management. His Date of Birth is February 8, 1969 in Medan. Lives in Sekupang, Kota Batam. His Current Job is Lecturer S2 in UNIBA, DPRD Riau Islands Province Members. His Office address is Dompak Islands, Tanjungpinang, and Kepulauan Riau, Indonesia.

E. WIDIA: Dr Elli Widia is Assistant Professor. Place and Date of Birth are Blang Pidie, July 25, 1972. Lives in Komplek Legenda Malaka Blok, Batam Centre. Her Current Job is Uniba, Lecturer S1, and S2 in Uniba and her Office address is the University of Batam, Batam, Indonesia.

A. FAIZAH: Ana Faizah’s Rank is Lecturer. She is an Assistant Professor. Place and Date of Birth are Sidoarjo, April 4, 1984. Marital Status is married and has one (1) Children (Khayra Ts. Afadhera. Lives in Griya KDA; Her Current Job is Secretary of Rector, Lecturer in Nursing Department, and Office address is Rectorate, University of Batam, Batam, Indonesia.

BIBLIOGRAPHY

AHMAD, SA, & HASSAN, SA (2017). “The Role and Effort by Ministry of Religious Affairs of the Republic of Indonesia in Consolidation and Determining the Beginning of the Holy Month of Ramadan and EID Celebrations in Indonesia”. International Journal of Academic Research and Business and Social Sciences, 7(6), pp. 968-978.

BARIZAH, N, RAHIM, A, & RAHMAN, A (2007). “A comparative study of zakah and modern taxation”. Journal of King Abdulaziz University: Islamic Economics, 20(1).

ESPOSITO, JL, & DELONG-BAS, NJ (2018). “Shariah: what everyone needs to know”. Oxford University Press.

FURQANI, H, MULYANY, R, & YUNUS, F (2019). “Zakat for Economic Empowerment (Analyzing the Models, Strategy and Implications of Zakat Productive Program in Baitul Mal Aceh and Baznas Indonesia)”. Iqtishadia: Jurnal Kajian Ekonomi dan Bisnis Islam STAIN Kudus, 11(2), pp. 391-411.

KUFORIJI, JO (2019). “The Essentials of Islamic Banking, Finance, and Capital Markets”. Rowman & Littlefield.

LATIF, J (2016). “Just money and interest: moving beyond Islamic banking by reframing discourses (Doctoral dissertation, University of Birmingham)”.

ROPI, I (2017). “The Ministry of Religious Affairs, the Muslim Community and the Administration of Religious Life”. In Religion and Regulation in Indonesia, pp. 101-116. Palgrave Macmillan, Singapore.

SAFITRI, AN (2019). “Pengaruh kontribusi pendapatan asli daerah terhadap anggaran pendapatan belanja daerah (APBD) di Kabupaten Trenggalek (Doctoral dissertation, UIN Walisongo)”.

SUHENDI, C (2018). “Corporate Social Responsibility in Islamic Perspective”. SUB THEMES, 14.

SUPRAYITNO, E (2020). “The Impact of Zakat on Economic Growth in 5 State in Indonesia”. InternationalJournal of Islamic Banking and Finance Research, 4(1), pp. 1-7.

SUKIER, H; RAMÍREZ MOLINA, R; Parra, M; MARTÍNEZ, K; FERNÁNDEZ, G & LAY, N (2020). “StrategicManagement of Human Talent from a Sustainable Approach”. Opción. Revista de Ciencias Humanas y Sociales, 36(91),pp. 929-953.

“THE HOLY QUR'AN”. Wordsworth Editions, 2000.

VAN BRUINESSEN, MM (2018). “Comparing the Governance of Islam in Turkey and Indonesia: Diyanet and the Ministry of Religious Affairs (No. 312)”. S. Rajaratnam School of International Studies.