Article

Board Interlocking and Accounting Choices in Brazilian Electric Energy Companies with Stock Exchange

Board Interlocking e Escolhas Contábeis em Empresas Brasileiras de Energia Elétrica com Ações na Bolsa

Flávio Ribeiro flavioribeiro@unicentro.br

Ademir Clemente ademir@ufpr.br

Flávio Ribeiro flavioribeiro@unicentro.br

Ademir Clemente ademir@ufpr.br

Board Interlocking and Accounting Choices in Brazilian Electric Energy Companies with Stock Exchange

BBR. Brazilian Business Review, vol. 20, no. 1, pp. 38-55, 2023

Fucape Business School

Received: 01 May 2020

Revised document received: 28 June 2020

Accepted: 10 March 2022

Abstract: This article aims to analyze the influence of stability and the intensity of board interlocking on accounting choices. The sample consists of 57 companies in the electricity sector out of a total of 59 with shares traded on Brasil, Bolsa, Balcão (B3), analyzed in a a period ranging from 2010 to 2016. This resulted in 177 different connections between companies. Company stability and intensity of existing relationships between the boards were used as proxies for an interlocking framework. For determining the accounting choice, an attempt was made to identify similarities between the choices adopted by the companies. The findings reveal considerable changes in the connection structures of companies. This began with the formation of a major network in the years 2010 and 2011, and ended with five well-defined groups in 2016. The results suggest that stability and intensity of connections favor dissemination of accounting choices. This is especially true for choices related to measurement and classification. These findings converge with Connelly and Slyke (2012) according to whom the existence of common counselors favor the access and dissemination of information between companies.

Keywords: Board Interlocking, Board Interlocking stability, Intensity of Board Interlocking, Accounting Choices, Electricity Sector.

Resumo : Este artigo tem como objetivo analisar a influência da estabilidade e da intensidade do board interlocking nas escolhas contábeis em companhias do setor de energia elétrica com ações negociadas no Brasil, Bolsa e Balcão (B3), no período 2010-2016. Para isso foi utilizada uma amostra constituída por 59 companhias, das quais 57 apresentaram as informações necessárias para a realização da análise, resultando em 177 diferentes conexões entre as empresas. Como proxies para o board interlocking, empregaram-se a estabilidade e a intensidade das conexões entre os profissionais dos conselhos, e para as escolhas contábeis buscou-se identificar a semelhança entre as escolhas adotadas pelas empresas. Os achados revelam consideráveis mudanças nas estruturas das conexões das companhias, partindo da formação de uma grande rede nos anos de 2010 e 2011, para a constituição de cinco grupos bem definidos em 2016. Os resultados sugerem que a estabilidade e intensidade das conexões favorecem a disseminação das escolhas contábeis, principalmente quando relacionadas a mensuração e classificação. Esses achados convergem com os de Connelly e Slyke (2012) segundo os quais a existência de conselheiros em comum favorece o acesso e a disseminação de informações entre empresas.

Palavras-chave: Board Interlocking, Estabilidade do Board Interlocking, Intensidade do Board Interlocking, Escolhas Contábeis, Setor de Energia Elétrica.

1. Introduction

According to Baysinger and Butler (1985) the board of directors (BD) is an essential part of corporate governance structure, helping to solve agency problems inherent in organizations’ management. Although the main role of the BD is aligned with the protection of investors' interests, recent studies have shown that its members can influence the decision-making of organizations when they simultaneously serve more than one company. This phenomenon of interconnection between directors is known as board interlocking. Pfeffer and Salancik (1978) state that when a professional is appointed to a board of directors, he or she is expected to provide resources to help the company develop. They suggest that the adoption of board interlocking can provide several benefits such as: i) provision of specific resources, ii) assistance in obtaining support from important elements external to a company, iii) legitimation, and iv) creation of a channel of communication between organizations.

Regarding the creation of a communication channel between organizations, Connelly and Van Slyke (2012) state that the existence of common directors in different companies favors the access and dissemination of information. Empirical studies have investigated this prerogative on the most varied corporate practices, such as: director compensation (Addy et al., 2014; Balsam et al., 2017; Boivie et al., 2015; Crespí-Cladera & Pascual-Fuster, 2015; Kim et al., 2015), mergers and acquisitions (Cai and Sevilir, 2012; El-Khatib et al., 2015; Renneboog & Zhao, 2013), investments in research and development (Han et al., 2015; Helmers et al., 2017), corporate reputation (Chandler et al., 2013), earnings management (Chiu et al., 2013; Ribeiro & Colauto, 2016).

Perceptibly, literature converges from the perspective that access and dissemination of accounting practices can be facilitated by board interlocking. However, none of these studies focus on accounting method choices. Indeed, from an information perspective, literature indicates that accounting methods are selected to reveal information and forecasts about company's future cash flows (Holthausen & Leftwich, 1983; Watts & Zimmerman, 1990). Thus, accounting methods are relevant to company values and impact future cash flows (Han et al., 2017).

Holthausen (1990) suggests that if board professionals bring a comparative advantage in accessing resources and obtaining information for their companies, they will have more power and influence over the estimation of the companies' future cash flows. Therefore, the choice of accounting methods is a very important decision made by the board members. These professionals use their choics of accounting methods to signal their vision about the prospects of their companies, and to improve the reliability and relevance of accounting information (Han et al., 2017).

In light of this, it is understood that the presence of common directors across two or more companies can also influence the decision on the accounting choices of organizations. This tends to occur with greater emphasis when connections are stable and intense. Considering what has been revealed, this article aims to analyze the influence of stability and intensity of board interlocking on accounting choices in companies in the electric energy segment with shares traded on the B3 stock exchange, in the period of 2010-2016.

According to Silveira (2004), the Brazilian economy presents a high concentration of ownership and, thus, the role of a board of directors stands out for minimizing agency costs between controllers and minority shareholders.

Furthermore, specifically in the Brazilian electricity sector, there has been a restructuring in recent years, due to the high demand for distribution and production of electric energy, converging on a greater participation of the private sector (Serafim, 2011). No doubt, the peculiar characteristics of Brazil and the electric energy segment represent a fertile ground for research in the field of finance.

The term stability here indicates the ability of links between boards of directors to be maintained over time. This stability of connections can favor the flow of information between organizations, helping the dissemination of corporate practices. On the other hand, intensity refers to the magnitude with which connections are made. Thus, the presence of a board member acting in two organizations has a lower intensity than the presence of two or more connected members.

In terms of originality, an important contribution to financial studies is the proposal of a new methodology to measure connections between BDs. Most studies have adopted social network variables and inclusion of dummies to represent board interlocking. Such variables have considerable limitations, such as the fact that analysis of social networks corresponds to a static representation of the social behavior of organizations and, in using dummies, the attribution of dichotomous values undervalues the impact of sharing more than one BD member. The use of the concepts of stability and intensity of connections aims to broaden the discussion on the role of board members in organizational content and explain how certain practices, more specifically accounting choices, can be disseminated among organizations.

As one of the main results found, it has been observed empirically that stable and intense connections favor the dissemination of accounting choices, especially when related to measurement and classification. These findings converge with Connelly and Slyke (2012) for whom the existence of common directors in different companies favors access and dissemination of information.

This article comprises, in addition to this introduction, four other sections: Theoretical Foundation, Methodology, Analysis and Discussion of Results and Conclusion.

2. Theoretical foundation

This section comprises the relevant concepts and theoretical foundations.

2.1. Board Interlocking Stability and Intensity

Fich and White (2005) understand that board interlocking is characterized by the presence of a professional who occupies a position of director in two or more companies. Mizruchi (1996) states that such a phenomenon occurs when a person affiliated with an organization participates in the BD of another organization. Therefore, board interlocking can be understood as a phenomenon in which members of a company’s board participate in the core of decision making for another board, establishing a link between two organizations.

For a long time, interconnected networks of boards represented a contentious phenomenon, because they could compromise the effectiveness of corporate governance. Indeed, it is reasonable to doubt that directors, who must play different roles on different boards, can effectively act in the interests of all the companies they serve (Mizruchi, 1996). However, it is also prudent to assume that having professionals sitting on the boards of other companies can facilitate the sharing of information, experience, and techniques. This can occur more evidently when connections have characteristics of stability and intensity.

The analysis of social networks makes it possible to identify in detail patterns of relationships between actors in each social situation (Marques, 1999). The basic principle of network analysis is that a structure of social relationships determines the content of those relationships. Network theorists reject the notion that people are combinations of attributes, or that institutions are static entities with clearly defined boundaries (Mizruchi, 2006).

The focus of social network analysis is the structure of social groups, seeking to identify the relationships between actors in the groups (Wasserman & Faust 1994). For a long time, a frequent criticism of network analysis has been that its proponents have succeeded in creating elegant mathematical descriptions of social structures, but not so successful in demonstrating that such structures have behavioral consequences. In no area were these criticisms more emphatic than in the study of relationships between organizations. Although some of the early studies have shown that centrality in networks between organizations is associated with identifiable organizational outcomes, including an organization's likelihood of political success (Galaskiewicz, 1979) and its investment strategies (Ratcliff, 1980), such demonstrations have been few up until the mid-1980s. Since then, studies suggesting that a company's position in networks influences its behavior have proliferated (Mizruchi, 2006).

One of the most important points about social network analysis is its role as representation. The social networks of a complex system such as a society usually represent a photograph of the structure at a given moment and not a film (Recuero et al., 2015). Therefore, it is necessary to understand that a static representation will hardly account for social complexity (Watts, 2003).

More severe criticisms are made for the use of dummies to represent board interlocking. Assigning dichotomous values to connections implies a great loss of information, underestimating their implicit characteristics, such as, for example, the fact that the impact is different depending on whether two companies share one director, or two or more. However, by the logic of using dummies, the same value would be assigned to all cases.

In view of these criticisms on the operationalization of board interlocking, this study considers two variables to characterize connections between boards: (i) Stability; and (ii) Intensity. The term stability derives from the Latin stabilĭtas and means the quality of being stable, the quality of maintaining equilibrium (Ferreira, 1986). Focusing on formation of board interlocking, stability can be understood as the ability of links between the Boards of Directors to become stable over time. For example, the stability between two companies with uninterrupted connections for years is greater than one between two companies that made their connections in just one year. It is understood that stability between organizations can favor the flow of information between them, helping the dissemination of corporate practices, which is an assumption to be tested in this study.

Another relevant feature that existing works on board interlocking have neglected is the intensity of connections. Conceptually, intensity refers to a characteristic attributed to something or someone that is present in large proportions. Normally, this characteristic is related to the fact that something manifests itself or makes itself felt with force, vigor, or something that is intense (Ferreira, 1986).

From the perspective of board interlocking, intensity refers to the magnitude with which connections are made. Thus, the presence of a board member acting in two organizations has a lower intensity than the presence of two or more connected members.

Metrics of stability and intensity are still unprecedented in studies on organizational connections. This can represent an important contribution to the effects of board interlocking.

2.2. Accounting choices and convergence process

Conceptually, accounting choices are any decisions with an objective to influence the results of accounting, including not only the financial statements themselves, but also any other information and documents derived from accounting (Fields et al., 2001). Accounting choices encompass managers' preferences for a given measurement, recognition, or disclosure procedure over another, whenever more than one procedure is equally accepted in accordance with best accounting practices (Watts, 1992)

In Brazil, the process of convergence to international standards began with the amendments to the Law 6404/76 promoted by Laws 11638/07 and 11941/09. Since the publication of Law 11638/07, the Accounting Pronouncements Committee (CPC in Portuguese) has been the main body that issues Brazilian accounting standards in accordance with the standards produced by the IASB (Silva et al., 2018).

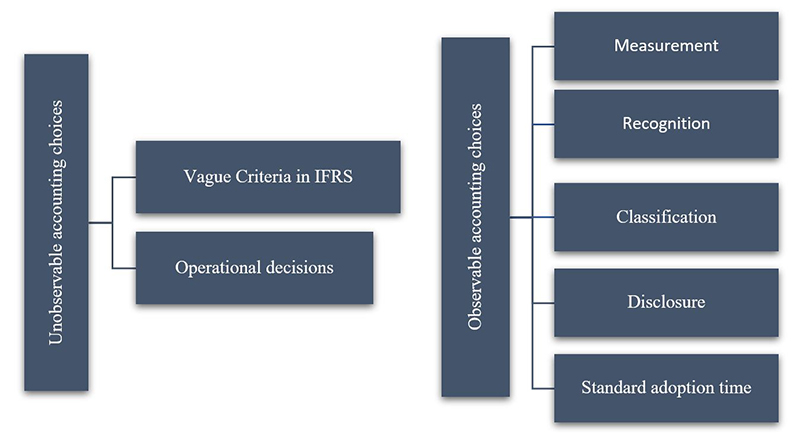

Adopting accounting standards to provide a disclosure language that meets the needs of all companies in all markets is a difficult task because the level of development in global markets differs in regards to issues such as investor or creditor protection, regulation, and enforcement (Fields et al., 2001). Nobes (2006, 2013) points out factors that contribute to differences in disclosure of accounting information. These factors were classified as overt options (observable options) and covert options (unobservable options), as shown in Figure 1.

Overt options are understood as arising from measurement, disclosure, classification criteria, as well as choices in stages of adoption of standards. These choices are easily identified in accounting reports. Covert options, on the other hand, result from managers’ operational decisions, as well as from gaps in accounting standards, and involve professional judgment (Silva et al., 2016).

With adoption of IFRS, accounting began a process of transitioning from accounting based on rules to accounting based on principles, in order to improve the representation of the economic-financial situations of companies, which increased the subjectivism arising from professional judgment (Bennett et al., 2006). This subjectivism in applying IFRS is provided by its flexibility and allows accounting choices.

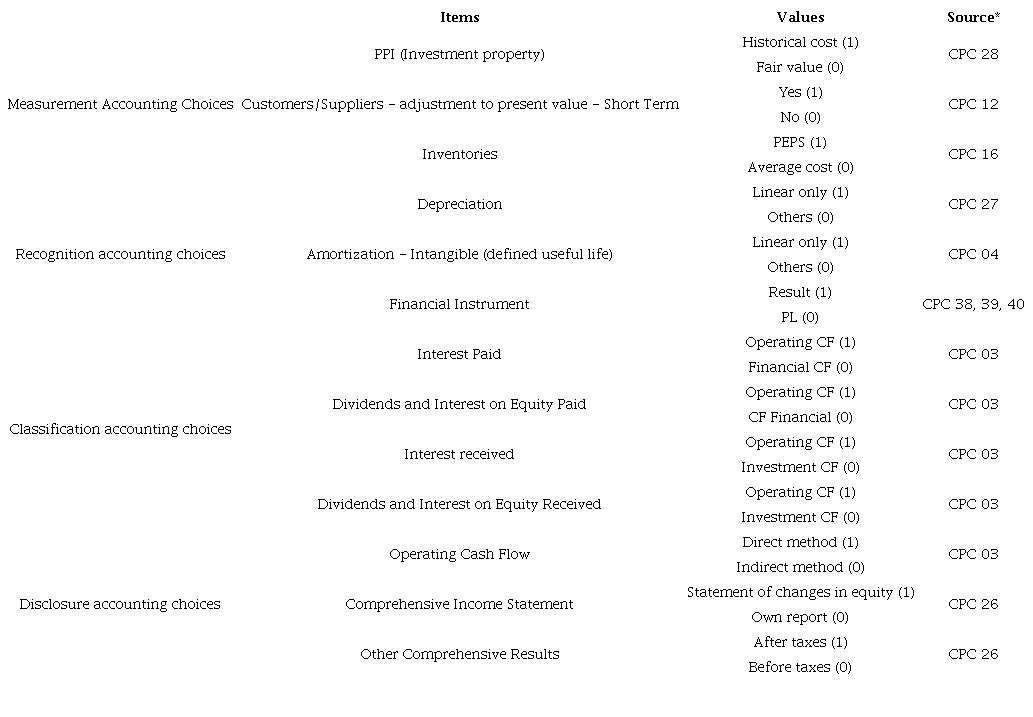

With the advent of convergence to international accounting standards, flexibility of decisions regarding accounting choices underwent changes, which included measurement, recognition, classification, and disclosure criteria. In relation to measurement criteria, these stand out: (i ) investment property; (ii) adjustment to present value of short-term assets and liabilities; and (iii) inventories. Regarding recognition, the following should be noted: (i) methods of depreciation of fixed assets; (ii) methods of amortization of intangibles; and (iii) financial instruments. As for classification, the elements of Statement of Cash Flows (SCF) are: (i) interest paid; (ii) dividends and interest on equity paid; (iii) interest received; and (iv) dividends and interest on equity received. Finally, disclosure criteria encompass: (i) Statement of Cash Flows; (ii) Comprehensive Income Statement; (iii) other comprehensive income statements.

3. Methodological notes

From a theoretical perspective, this is a positivist study that proposes to empirically investigate the stability and intensity of connections between companies Board of Directors’ (direct) and their relationships with decisions on accounting choices (indirect).

The sample was restricted to Brazilian companies in the electricity sector that have connections with another company through their BD professionals, and which show the necessary information to identify the accounting choices over the period from 2010 to 2016. This sector has peculiar characteristics, such as a high level of connections, which can contribute to understanding the techniques used. The B3 stock exchange’s electricity sector is made up of 59 companies, of which 57 provided the information necessary to carry out the analysis, resulting in 177 connections between the companies. The two excluded companies did not present information for the entire period.

3.1. Variables and Analysis Model

To obtain the variables related to accounting choices, two steps were carried out. First, the standards that present different options for measurement, recognition, classification, and disclosure of accounting information were identified. Then, after the identification of the norms, the accounting choices of the sampled companies were mapped based on the accounting reports.

Table 1 presents the items that make up the similarity metric of accounting choices. These items were obtained from Andrade et al. (2013); Han et al. (2017); Maciel et al. (2018); Moreira et al. (2015); Pinto et al. (2015); Scherer et al. (2012); Sedki et al. (2018); Silva and Barranco (2015); Silva and Martins (2018); Silvestre and Malaquias (2015); Simeon and John (2018); Souza et al. (2015).

Source: Authors (2020). *CPC refers to Accounting Pronouncements Committee

For the metric of similarity of accounting choices, each item received a dichotomous valuation, either 0 or 1. Subsequently, the values obtained by the individual companies were compared with the other companies with which they maintain a connection. In the case of equal values, a value of 1 (one) was assigned, for divergent values, it was 0 (zero). Then, the items of each classification (measurement, recognition, classification, and disclosure) were added and divided by the total of each classification. For example, for measurement choices, the maximum similarity is 6. If in comparing with a connected company the result was 4, a value of 4/6 or 0.67 was assigned. The values thus calculated can vary between 0 and 1 and, therefore, Logit Regression was adopted.

To determine the values of variables related to accounting choices, the sample was segregated into 3 parts, the middle part was disregarded, assigned a value of 1 to scores in the upper tercile, and 0 (zero) to scores in the lower one.

Board interlocking stability and intensity were used as independent variables. Stability is understood as the ability of connections to be constant over the years, that is, the maintenance of the simultaneous presence of members on the boards of companies.

To identify the stability of connections the Formulário de Referência (Reference Form) of each company was accessed. Subsequently, item 12.5/6 (section 12) was consulted, which specifies the composition and professional experience of the management and the fiscal council. There, the names of all members that make up the executive board, the BD and the fiscal council can be identified.

The names of professionals with their respective CPF numbers (the Brazilian federal register of individuals) were tabulated for each year. Subsequently, a filter was applied to identify professionals who work simultaneously on two or more boards. The connections between the companies and their duration were identified. Some lasted only a year, but others became constant over the whole period.

As control variables, the classification of companies as state-owned and private, corporate governance and issuance of ADRs (American depositary receipts) were used. To identify the presence of state-owned companies, a dummy variable was used, which received a value of 1 if a company was state-owned, according to Camilo et al. (2012). The variable referring to corporate governance separates the companies that participate in the segments of corporate governance from others. Also, according to Silveira et al. (2004), companies that presented ADRs received value 1, and 0 was assigned to others.

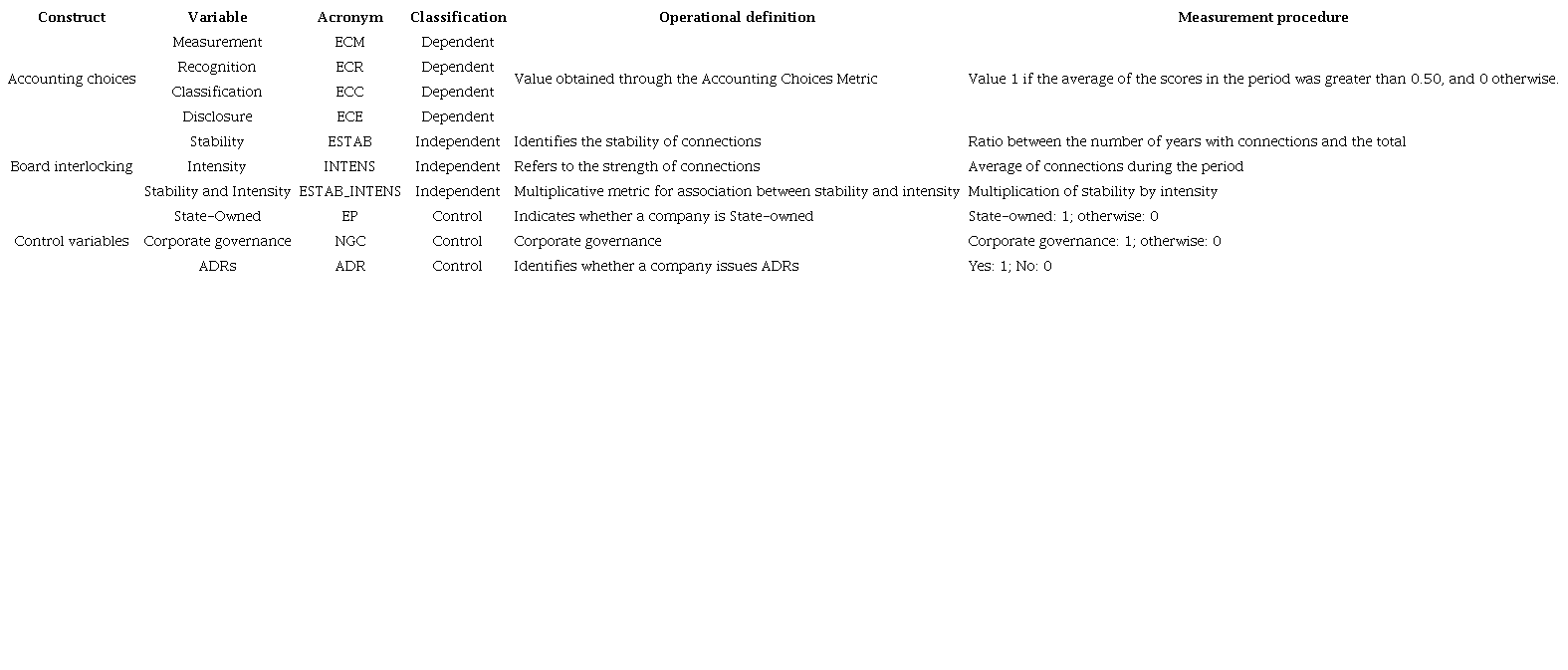

Table 2 describes variables and their operational definitions.

Source: Authors (2020).

Based on the variables defined in Table 2, the following models were specified:

Where:

ECM - Measurement Accounting Choices

ECR - Recognition Accounting Choices

ECC - Classification Accounting Choices

ECE - Disclosure Accounting Choices

ESTAB - Stability of connections

INTENS - Intensity of connections

ESTAB_INTENS - Stability and Intensity of connections

EP - State-owned

NGC - Corporate governance

ADR - ADRs

ε - Statistical disturbance

Then, Logit Regression Analysis was performed to test the effects of board interlocking stability and intensity on the similarity of accounting choices.

4. Analysis and Discussion of Results

The panorama of connections between companies revealed considerable changes in the structure of network, from a large network in 2010 and 2011 to the formation of five well-defined groups in 2016. The electric energy sector has nine well-defined groups of companies. These groups showed stability in their connections during the 7 year period analyzed. Among the stable connections are the connections made by Cemig, Light and Teasa, in addition to the Northeastern energy network formed by Conserv, Termopernanbuco, Elektro Redes, Itapebi, Coelba, Afluente, Neoenergia and Uptick, which represent the largest number of interconnected companies.

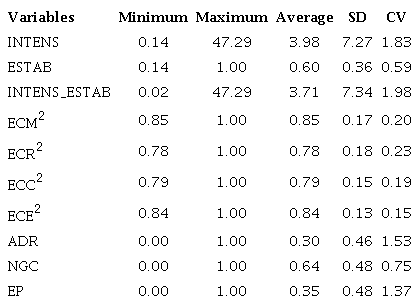

The results of descriptive statistical analysis are presented in Table 3.

Source: Authors (2020). Notes: (1) INTENS: Intensity of connections; ESTAB: Stability of connections; INTENS_ESTAB: Intensity multiplied by Stability; ECM: Measurement Accounting Choices; ECR: Recognition Accounting Choices; ECC: Classification Accounting Choices; ECE: Disclosure Accounting Choices; ADR: American Depositary Receipt; NGC: Corporate governance; EP: State-owned. (2) Dichotomized values according to subsection 3.1.

Descriptive statistics show that the average intensity of connections is approximately 4 members per connection, however the standard deviation is high, which suggests the presence of heterogeneous numbers of connections, that is, while some companies present more than forty members in common some others present only one professional in common.

Regarding stability, most connections last longer than 4 years (0.60 x 7 years = 4.2 years). This result indicates that connections between companies in the electricity sector are, in general, stable and show few oscillations.

In respect to accounting choices, the similarity scores between companies that make up connections do not differ substantially, although such similarities being higher in measurement (0.85) and disclosure (0.84).

The statistics of the control variables indicate that most companies do not have securities traded on the American stock exchanges (ADRs), as the average is below 0.5. In addition, there is a predominance of private companies in the sector, which differ in respect to corporate governance.

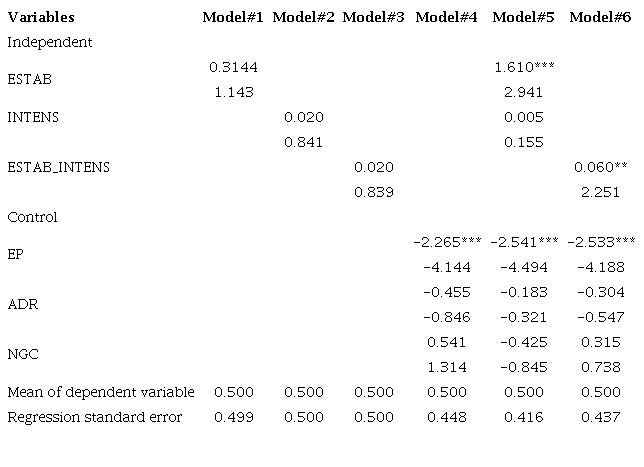

The results of Logit Regression are shown in Tables 4, 5, 6, and 7.

Source: Authors (2020). Notes: ***, **, * indicate a significance level lower than 1%, 5% and 10%, respectively. INTENS: Intensity of Connections; ESTAB: Stability of Connections; INTENS_ESTAB: Intensity multiplied by Stability; ECM: Measurement Accounting Choices; ADR: American Depositary Receipt; NGC: Corporate Governance; and EP: State-owned. Model#1 probes the influence of Stability (ESTAB). Model#2 investigates the relationship with Intensity (INTENS). In Model#3, the influence of the multiplicative variable Stability x Intensity (ESTAB_INTENS) is verified. Model#4 employs the control variables State-owned (EP), Corporate Governance (NGC) and American Depositary Receipt (ADR). Model#5 is performed with the control variables, Stability, and Intensity. Model#6 employs the control variables and the multiplicative variable ESTAB_INTENS.

Measurement accounting choices describe choices regarding the method a company adopts to assess an economic event (Silva, 2016). The results indicate that measurement accounting choices are significantly influenced by the stability of connections between boards (p < 0.01). This suggests that the number of professionals simultaneously present in more than one board of directors tends to favor dissemination of choices related to measuring investment property, adjusting to present value, and measuring inventories.

Furthermore, measurement accounting choices are also influenced by the origin of companies' own capital. The findings indicate that private equity companies tend to present greater similarity between accounting practices.

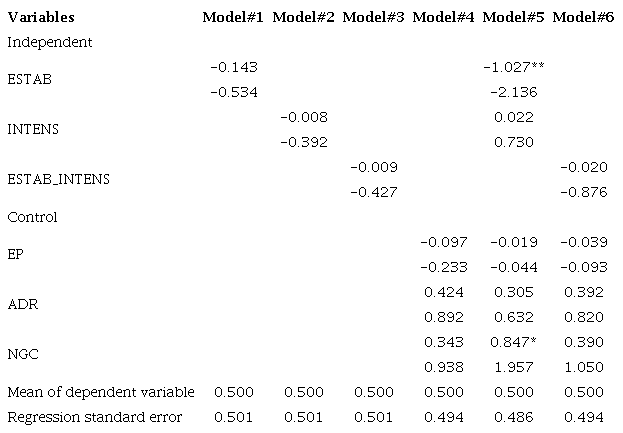

Source: Authors (2020). Notes: ***, **, * indicate a significance level lower than 1%, 5% and 10%, respectively. INTENS: Intensity of Connections; ESTAB: Stability of Connections; INTENS_ESTAB: Intensity multiplied by Stability; ECR: Recognition Accounting Choices; ADR: American Depositary Receipt; NGC: Corporate Governance; and EP: State-owned. Model#1 probes the influence of Stability (ESTAB). Model#2 investigates the relationship with Intensity (INTENS). In Model#3, the influence of the multiplicative variable Stability x Intensity (ESTAB_INTENS) is verified. Model#4 employs the control variables State-owned (EP), Corporate Governance (NGC) and American Depositary Receipt (ADR). Model#5 is performed with the control variables, Stability, and Intensity. Model#6 employs the control variables and the multiplicative variable ESTAB_INTENS.

Recognition accounting choices (Table 5), refer to the way a given economic event is recognized in terms of its impact on financial statements, altering income values, equity components and cash flows. The results indicate that stability of connections negatively influences similarity of recognition accounting choices (Model#5). This does not support the idea that the dissemination of accounting practices could be evidenced from connections established by companies’ BD members.

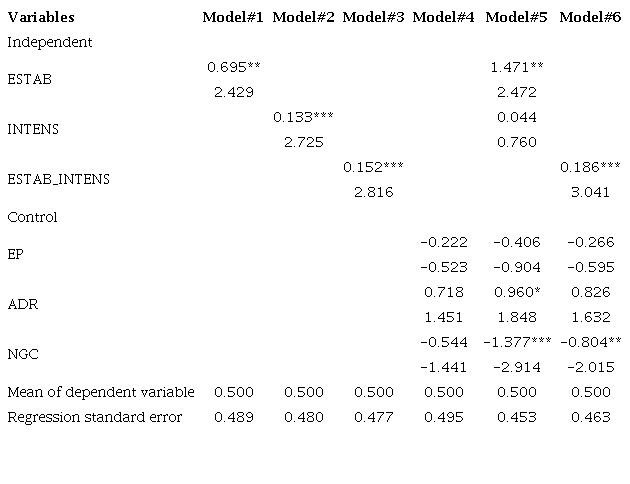

In Table 6, the results referring to the classification accounting choices are presented.

Source: Authors (2020). Notes: ***, **, indicate a significance level lower than 1%, 5% and 10%, respectively. INTENS: Intensity of Connections; ESTAB: Stability of Connections; INTENS_ESTAB: Intensity multiplied by Stability; ECC: Classification Accounting Choices; ADR: American Depositary Receipt; NGC: Level of Corporate Governance; and EP: State-owned Companies. Model#1 probes the influence of Stability (ESTAB). Model#2 investigates the relationship with Intensity (INTENS). In Model#3, the influence of the multiplicative variable Stability x Intensity (ESTAB_INTENS) is verified. Model#4 employs the control variables State-owned (EP), Corporate Governance (NGC) and American Depositary Receipt (ADR). Model#5 is performed with the control variables, Stability, and Intensity. Model#6 employs the control variables and the multiplicative variable ESTAB_INTENS.

Classification accounting choices are related to the way in which equity, income, and cash flows are provided in financial statements. The results suggest that stability and intensity of connections favor dissemination of choices around classification accounting. According to the theory of resource dependence, interconnected advisors can provide unprecedented and detailed information and knowledge that is obtained from other companies and that is relevant and crucial for decisions and strategies (Shropshire, 2010). Thus, board interlocking provides comparative advantages in corporate decisions, including decisions on accounting methods, due to its ability to acquire and interpret information (Rao et al., 2000).

The results also indicate that corporate governance negatively influences the similarity of classification accounting choices. In other words, companies that do not belong to the corporate governance levels tend to present greater similarity in accounting practices with companies with which they are connected.

There are also signs that companies with securities traded on American stock exchanges tend to present greater similarities between choices related to the form of disposition in financial statements of equity, income, and cash flow elements. Silveira et al. (2004) state that adapting to corporate governance practices required by the Securities and Exchange Commission (SEC) for the release of ADRs can increase the company's visibility. Considering that such companies follow both the Brazilian and the North American accounting model, there would be an incentive for them to present greater similarity.

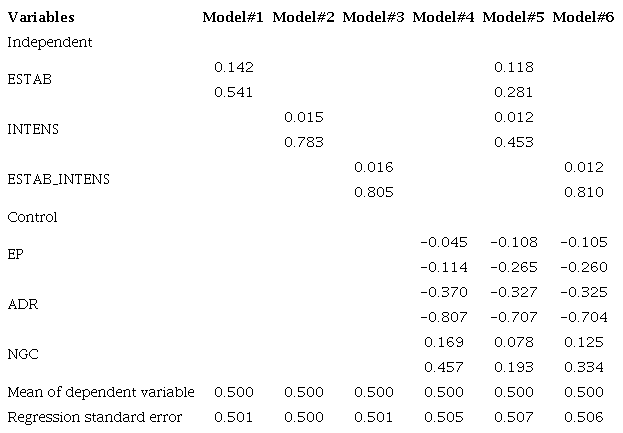

In Table 7, the results referring to disclosure accounting choices are presented.

Source: Authors (2020). Notes: ***, **, * indicate a significance level lower than 1%, 5% and 10%, respectively. INTENS: Intensity of Connections; ESTAB: Stability of Connections; INTENS_ESTAB: Intensity multiplied by Stability; ECE: Disclosure Accounting Choices; ADR: American Depositary Receipt; NGC: Level of Corporate Governance; and EP: State-owned Companies. Model#1 probes the influence of Stability (ESTAB). Model#2 investigates the relationship with Intensity (INTENS). In Model#3, the influence of the multiplicative variable Stability x Intensity (ESTAB_INTENS) is verified. Model#4 employs the control variables State-owned (EP), Corporate Governance (NGC) and American Depositary Receipt (ADR). Model#5 is performed with the control variables, Stability, and Intensity. Model#6 employs the control variables and the multiplicative variable ESTAB_INTENS.

Disclosure accounting choices refer to the way accounting information is disclosed. The findings indicate that stability and intensity of connections do not have significant effects on the similarity of disclosure accounting choices. These results do not support the idea that the number of connections and their durability favor the dissemination of disclosure accounting practices.

5. Conclusion

In this paper, we analyzed the influence of stability and intensity of board interlocking on the accounting choices made by companies in the electricity sector who traded shares on the B3, over the period 2010-2016. For this, a sample of 59 companies was used, of which 57 presented the necessary information, resulting in 177 different connections between the sampled companies.

A priori, the results demonstrated the existence of interesting links that often become hidden for investors in the tangle of companies listed on the stock exchange. Such links can influence investment decisions, especially when considering the premise of diversification.

Regarding the intensity of connections between members of boards of directors, the highest average of professionals occurred in 2013, with approximately 4.18 members connected in each connection, followed by the years 2010, 2015, and 2011. In 2012, there occurred the lowest average number of connections between companies: 3.69. The results also indicated that the overall average intensity of the connections is 3.98. This average is high because companies such as Cemig Distribuição and Cemig Geração e Transmissão, for example, had an average of 47 professionals in common in the period.

In general, measurement accounting choices showed a considerable level of similarity. On the average, 85% of the accounting information are similarly evidenced in connected companies. This high level of homogeneity can also be observed in the choices associated with disclosure of the financial statements. The results show that measurement accounting choices, classification accounting choices, and disclosure accounting choices were practically stable from 2012 onwards, indicating that companies that established board of directors’ connections did not significantly change their accounting practices.

Furthermore, the results suggested that the stability and intensity of connections favor dissemination of accounting choices, especially when related to measurement and classification. These findings converge with Connelly and Slyke (2012) for whom the existence of common directors favors access and dissemination of information.

The results achieved complement several studies (Addy et al., 2014; Balsam et al., 2017; Beckman & Haunschild, 2002; Cai et al., 2014; Chandler et al., 2013; Chiu et al., 2013; Han et al., 2015; Helmers et al., 2017; Ribeiro & Colauto, 2016; Wong et al., 2015) which have empirically confirmed that board interlocking can be considered an important information channel.

Finally, the results found are limited by the sample of companies investigated, as well as by the variables and techniques used. For future studies, the analysis can be expanded considering other control variables, such as business models, and adoption of the same auditing companies, which can culminate in common accounting practices.

References

Addy, N., Chu, X., & Yoder, T. (2014). Voluntary adoption of clawback provisions, corporate governance, and interlock effects. Journal of Accounting and Public Policy, 33(2), 167-189. https://doi.org/10.1016/j.jaccpubpol.2013.12.001

Andrade, M. E. M. C., Silva, D. M. da, & Malaquias, R. F. (2013). Accounting Choices in Investment Properties. Revista Universo Contábil, 9(3), 22-37. https://doi.org/10.4270/ruc.2013320

Balsam, S., Kwack, S. Y., & Lee, J. Y. (2017). Network connections, CEO compensation and involuntary turnover: The impact of a friend of a friend. Journal of Corporate Finance, 45, 220-244. https://doi.org/10.1016/j.jcorpfin.2017.05.001

Baysinger, B. D., & Butler, H. N. (1985). Corporate Governance and the Board of Directors: Performance Effects of Changes in Board Composition. Journal of Law, Economics & Organization, 1(1), 101-124.

Beckman, C. M., & Haunschild, P. R. (2002). Network learning: The effects of partner experience heterogeneity on corporate acquisitions. Administrative Science Quarterly, 47(1), 92-124. https://doi.org/10.2307/3094892

Bennett, B., Bradbury, M., & Prangnell, H. (2006). Rules, principles and judgments in accounting standards. Abacus, 42(2), 189-204. https://doi.org/10.1111/j.1467-6281.2006.00197.x

Boivie, S., Bednar, M. K., & Barker, S. B. (2015). Social comparison and reciprocity in director compensation. Journal of Management, 41(6), 1578-1603. https://doi.org/10.1177/0149206312460680

Cai, Y., Dhaliwal, D. S., Kim, Y., & Pan, C. (2014). Board interlocks and the diffusion of disclosure policy. Review of Accounting Studies, 19(3), 1086-1119. https://doi.org/10.1007/s11142-014-9280-0

Cai, Y., & Sevilir, M. (2012). Board connections and M&A transactions. Journal of Financial Economics, 103(2), 327-349. https://doi.org/10.1016/j.jfineco.2011.05.017

Camilo, S. P. O., Marcon, R., & Bandeira-de-Mello, R. (2012). Conexões Políticas e Desempenho: Um estudo das firmas listadas na BM&FBovespa. Revista de Administação Contemporânea, 16(6), 784-805. https://doi.org/10.1590/S1415-65552012000600003

Chandler, D., Haunschild, P. R., Rhee, M., & Beckman, C. M. (2013). The effects of firm reputation and status on interorganizational network structure. Strategic Organization, 11(3), 217-244. https://doi.org/10.1177/1476127013478693

Chiu, P. C., Teoh, S. H., & Tian, F. (2013). Board interlocks and earnings management contagion. Accounting Review, 88(3), 915-944. https://doi.org/10.2308/accr-50369

Connelly, B. L., & Van Slyke, E. J. (2012). The power and peril of board interlocks. Business Horizons, 55(5), 403-408. https://doi.org/10.1016/j.bushor.2012.03.006

Crespí-Cladera, R., & Pascual-Fuster, B. (2015). Executive directors’ pay, networks and operating performance: The influence of ownership structure. Journal of Accounting and Public Policy, 34(2), 175-203. https://doi.org/10.1016/j.jaccpubpol.2014.09.004

El-Khatib, R., Fogel, K., & Jandik, T. (2015). CEO network centrality and merger performance $. Journal of Financial Economics, 116(2), 349-382. https://doi.org/10.1016/j.jfineco.2015.01.001

Ferreira, A. B. de H. (1986). Novo dicionário de língua portuguesa (2nd ed.). Nova Fronteira.

Fich, E. M., & White, L. J. (2005). Why do CEOs reciprocally sit on each other’s boards? Journal of Corporate Finance, 11(1-2), 175-195. https://doi.org/10.1016/j.jcorpfin.2003.06.002

Fields, T. D., Lys, T. Z., & Vincent, L. (2001). Empirical research on accounting choice. Journal of Accounting and Economics, 31(1-3), 255-307. https://doi.org/10.1016/S0165-4101(01)00028-3

Galaskiewicz, J. (1979). The structure of community organizational networks the structure of community organizational networks*. Source: Social Forces, 57(4), 1346-1364. https://doi.org/10.2307/2577274

Han, J., Bose, I., Hu, N., Qi, B., & Tian, G. (2015). Does director interlock impact corporate R&D investment? Decision Support Systems, 71, 28-36. https://doi.org/10.1016/j.dss.2015.01.001

Han, J., Hu, N., Liu, L., & Tian, G. (2017). Does director interlock impact the diffusion of accounting method choice? Journal of Accounting and Public Policy, 36(4), 316-334. https://doi.org/10.1016/j.jaccpubpol.2017.05.005

Helmers, C., Patnam, M., & Rau, P. R. (2017). Do board interlocks increase innovation? Evidence from a corporate governance reform in India. Journal of Banking and Finance, 80, 51-70. https://doi.org/10.1016/j.jbankfin.2017.04.001

Holthausen, R. W. (1990). Accounting method choice. Opportunistic behavior, efficient contracting, and information perspectives. Journal of Accounting and Economics, 12(1-3), 207-218. https://doi.org/10.1016/0165-4101(90)90047-8

Holthausen, R. W., & Leftwich, R. W. (1983). The economic consequences of accounting choice implications of costly contracting and monitoring. Journal of Accounting and Economics, 5(C), 77-117. https://doi.org/10.1016/0165-4101(83)90007-1

Kim, J. W., Kogut, B., & Yang, J. (2015). Executive compensation, fat cats ,and best athletes. American Sociological Review, 80(2), 299-328. https://doi.org/10.1177/0003122415572463

Maciel, F. F. de S., Salotti, B. M., & Imoniana, J. O. (2018). Escolhas contábeis na demonstração dos fluxos de caixa no contexto do mercado de capitais brasileiro. Revista Universo Contábil, 13(4), 194-211. https://doi.org/10.4270/ruc.2017432

Marques, E. C. (1999). Redes sociais e instituições na construção do Estado e da sua permeabilidade. Revista Brasileira de Ciências Sociais, 14(41), 45-67. https://doi.org/10.1590/S0102-69091999000300004

Mizruchi, M. S. (1996). What Do Interlocks Do? An Analysis, Critique, and Assessment of Research on Interlocking Directorates. Annual Review of Sociology, 22(1), 271-298. https://doi.org/10.1146/annurev.soc.22.1.271

Mizruchi, M. S. (2006). Análise de redes sociais: Avanços recentes e controvérsias atuais. Revista de Administração de Empresas, 46(3), 72-86. https://doi.org/10.1590/S0034-75902006000300013

Moreira, F., Firmino, J., Santos, A., Silva, J. D., & Silva, M. (2015). Qualidade da auditoria no Brasil: Um estudo do julgamento dos auditores independentes na aderência do ajuste a valor presente nas companhias de construção e engenharia listadas na BM&F-Bovespa (Audit Quality in Brazil: A Study of the Judgment Ofthe Independent Auditors on Adoption of the Adjustment to Present Value in Construction and Engineering Companies Listed on BM&F-Bovespa). Sociedade, Contabilidade E Gestão, 10(1), 63-80. https://doi.org/10.2139/ssrn.2830937

Nobes, C. (2006). The survival of international differences under IFRS: Towards a research agenda. Accounting and Business Research, 36(3), 233-245. https://doi.org/10.1080/00014788.2006.9730023

Nobes, C. (2013). The continued survival of international differences under IFRS. Accounting and Business Research, 43(2), 83-111. https://doi.org/10.1080/00014788.2013.770644

Pfeffer, J., & Salancik, G. R. (1978). The External Control of Organizations: A Resource Dependence Perspective. Harper and Row.

Pinto, M. J. T., Martins, V. A., & Silva, D. M. da. (2015). Escolhas Contábeis: O caso brasileiro das propriedades para investimento. Revista Contabilidade & Finanças, 26(69), 274-289. https://doi.org/10.1590/1808-057x201512280

Rao, H., Davis, G., & Ward, A. (2000). Embeddedness, social identity and mobility: Why firms leave NASDAQ and Join NYSE. Administrative Science Quarterly, 45(2), 268-292. https://doi.org/10.2307/2667072

Ratcliff, R. E. (1980). Banks and Corporate Lending: An analysis of the impact of the internal structure of the capitalist class on The Lending Behavior of Banks. American Sociological Review, 45(4), 553-570.

Recuero, R., Bastos, M., & Zago, G. (2015). Introdução Sobre Mídia Social; O que é análise de redes sociais? In Análise de redes para mídia social (pp. 21-51). Sulina.

Renneboog, L., & Zhao, Y. (2013). Director networks and takeovers. Journal of Corporate Finance, 28, 218-234. https://doi.org/10.1016/j.jcorpfin.2013.11.012

Ribeiro, F., & Colauto, R. D. (2016). The relationship between board interlocking and income smoothing practices. Revista Contabilidade & Finanças, 27(70), 55-66. https://doi.org/10.1590/1808-057x201501320

Scherer, L. M., Teodoro, J. D., Kos, S. R., & Anjos, R. P. (2012). Demonstração dos Fluxos de caixa: análise de diferenças de procedimentos de divulgação entre empresas listadas nas bolsas de valores de São Paulo, Frankfurt, Milão e Londres. Revista de Contabilidade E Controladoria, 4(2), 37-51. http://doi.org/10.5380/rcc.v4i2.29025

Sedki, S. S., Posada, G. A., & Pruske, K. A. (2018). Differences between U.S. GAAP and IFRS in accounting for goodwill impairment and inventory: Tax treatment under the internal revenue code. Journal of Accounting and Finance, 18(4), 23-29. https://doi.org/10.33423/jaf.v18i4.421

Serafim, L., & Gomes, L. (2011). Influência da governança corporativa nas ações do setor elétrico brasileiro: uma análise através da medida ômega. Final Report of Pibic. PUC-RJ. https://www.puc-rio.br/ensinopesq/ccpg/pibic/relatorio_resumo2011/Relatorios/CSS/ADM/ADM-Leonardo%20Soares%20Serafim.pdf

Shropshire, C. (2010). The role of the interlocking director and board receptivity in the diffusion of practices. Academy of Management Review, 35(2), 246-264.

Silva, D. M. da. (2016). Escolhas contábeis e características de empresas de grande porte na adoção do IFRS em duas etapas: diagnóstico e análise. [Tese de doutorado, Universidade de São Paulo, Ribeirão Preto].

Silva, A. H. C., & Barranco, T. M. de S. (2015). Escolhas contábeis: Análise dos métodos de avaliação de estoques antes e após implementação do Ifrs. Revista de Informação Contábil, 9(2), 39-56.

Silva, D. M., Aversari Martins, V., & Lemes, S. (2016). Escolhas contábeis: Reflexões para a pesquisa. Revista Contemporânea de Contabilidade, 13(29), 129-155. https://doi.org/10.5007/2175-8069.2016v13n29p129

Silva, A. da, Brighenti, J., & Klann, R. C. (2018). Efeitos da convergência às normas contábeis internacionais na relevância da informação contábil de empresas brasileiras. Revista Ambiente Contábil, 10(1), 121-138. https://doi.org/10.21680/2176-9036.2018v10n1ID11016

Silva, D. M. da, & Martins, V. A. (2015). Escolhas de políticas contábeis nas empresas de grande porte no Brasil XXII Congresso Brasileiro de Custos, Foz do Iguaçu, Brasil.

Silva, D. M. da, & Martins, V. A. (2018). Politicas contábeis recomendadas nas normas e escolhas contábeis predominantes em companhias abertas e fechadas no Brasil. Advances in Scientific and Applied Accounting, 11(3), 372-390. http://doi.org/10.14392/asaa.2018110301

Silveira, A. M. (2004). Governança Corporativa e estrutura de propriedade: determinantes e relação com o desempenho das empresas no Brasil. [Tese de doutorado, Universidade de São Paulo, São Paulo].

Silveira, A. D. M. da, Barros, L. A. B. de C., & Famá, R. (2004). Qualidade da Governança Corporativa no Brasil e os Fatores que a determinam. 28o Encontro da ANPAD - ENANPAD, Curitiba.

Silvestre, L. N., & Malaquias, R. F. (2015). Classificação dos juros e dividendos na demonstração dos fluxos de caixa das empresas brasileiras. Revista Ambiente Contábil, 7(2), 119-134.

Simeon, E. D., & John, O. (2018). Implication of choice of inventory valuation methods on profit, tax and closing inventory. Account and Financial Management Journal, 3(7), 1639-1645. https://doi.org/10.31142/afmj/v3i7.05

Souza, F. E. A., Botinha, R. A., Silva, P. R., & Lemes, S. (2015). A comparabilidade das escolhas contábeis na avaliação posterior de propriedades para investimento: Uma análise das companhias abertas brasileiras e portuguesas. Revista Contabilidade & Finanças, 26(68), 154-166. https://doi.org/10.1590/1808-057x201500580

Wasserman, S., & Faust, K. (1994). Social Network Analysis: Methods and Applications, Structural Analysis in the Social Sciences. Cambridge University Press.

Watts, D. (2003). Small Worlds: The dynamics of networks between order and randomness. Princeton University Press.

Watts, R. L. (1992). Accounting choice theory and market-based research in accounting. The British Accounting Review, 24(3), 235-267. https://doi.org/10.1016/S0890-8389(05)80023-X

Watts, R. L., & Zimmerman, J. L. (1990). Positive accounting theory: A ten year perspective. The Accounting Review, 65(1), 131-156. http://www.jstor.org/stable/247880

Wong, L. H. H., Gygax, A. F., & Wang, P. (2015). Board interlocking network and the design of executive compensation packages. Social Networks, 41, 85-100. https://doi.org/10.1016/j.socnet.2014.12.002

Author notes

Email:flavioribeiro@unicentro.br Email:ademir@ufpr.br

Conflict of interest declaration