Articles

Esta obra está bajo una Licencia Creative Commons Atribución 4.0 Internacional.

Recepción: 03 Diciembre 2019

Aprobación: 08 Octubre 2020

DOI: https://doi.org/10.13037/gr.vol37n110.6495

Abstract: The informal economy is important for emerging economies but is neglected by the financial literature, particularly by studies that analyze credit operations executed informally in the retailing market, which is a very common practice by Micro and Small Enterprises (MSEs) in Brazilian cities. Therefore, this study aims to analyze the management of informal commercial credit (ICC) in MSEs, specifically the profile of entrepreneurs and the business practice associated with its adoption. The results show that ICC is used by almost 80% of the studied companies; that 43.5% of these companies would not be able to survive without it; and that, in more than 60% of these companies, at least 20% of their revenue is obtained through ICC. We observed that the education of entrepreneurs, the company revenue, and the costs related to collections management are associated with granting ICC and with the risk perceived by entrepreneurs regarding the operation.

Keywords: Informal Commercial Credit, Risk Perception, Micro and Small Enterprises.

Resumo: A economia informal é importante para as economias emergentes e, mesmo assim, é negligenciada pela literatura financeira, especialmente pesquisas que analisam operações de crédito feitas informalmente no mercado varejista, prática essa bastante utilizada pelas micro e pequenas empresas (MPEs) brasileiras. Assim, esse estudo tem como objetivo analisar a gestão da oferta de crédito comercial informal (CCI) em MPE, com destaque para o perfil do empresário e as práticas empresariais associadas à sua adoção. Os resultados mostraram que a oferta de CCI é utilizada por quase 80% das empresas pesquisadas; que 43,5% delas não conseguiriam sobreviver sem sua adoção; e que, em mais de 60% das empresas que o utiliza, pelo menos, 20% do seu faturamento é obtido por meio da oferta de CCI. Observou-se também que a escolaridade do empresário, o faturamento da empresa e os custos relacionados às ações de cobranças estão associados à concessão do CCI e ao risco percebido pelo empresário na operação.

Palavras-chave: Crédito Comercial Informal, Percepção de Risco, Micro e Pequenas Empresas.

1 INTRODUCTION

The movement of the economy in a society is given by the circulation of durable and non-durable goods, which generates a flow of financial wealth in a city, state, or country. It is common to define a country’s Gross Domestic Product (GDP) as the entirety of the wealth it generated within a given period of time. However, the GDP calculation does not take into account the informal economy, which can be defined as the production of goods and services, whether legal or not, that are not included in GDP estimations (SMITH, 1994).

Schneider, Buehn and Montenegro (2010) explain that the informal economy includes the production of goods and services which are deliberately hidden from public authorities in order to avoid fees, taxes and social contributions, or to avoid complying with certain labor norms such as minimum wage and job security standards.

The informal economy (and, consequently, the offer of ICC) are usually not part of the statistics prepared by governmental bodies (e.g. the Brazilian Development Bank, Banco Nacional de Desenvolvimento Econômico – BNDES) or by credit protection agencies (e.g. Experían-Serasa), mainly due to the difficulty to obtain this data (SANTOS; MENDES-DA-SILVA; GONZALEZ, 2018), which Schneider, Buehn and Montenegro (2010) justify by explaining that those involved in this type of activity do not with to be identified.

However, despite the negligence of public and private bodies and the academy itself, and according to estimations by Schneider, Buehn and Montenegro (2010), the average size of the informal economy (as a percentage of GDP) in 2007 was 28.3% in developing countries, 41.1% in transition countries (Eastern Europe and Central Asia), and 19.4% in high-income countries that are members of the Organization for Economic Co-operation and Development (OECD).

Regarding the national context, Gonzalez et al. (2013) analyzed a sample of 2,885 individuals and 284 cities in all Brazilian regions and prepared an overview of the access and use of financial services considering four categories (bank accounts, savings accounts, credit and insurance), finding that 17% of the respondents declared that they use informal credit – the so-called “on the cuff”. Kumar (2004) found that 46% of the interviewees declared that they have some type of informal credit, from moneylenders to borrowing money from family/friends, or buying “on the cuff” at the grocery store.

These findings are a reflex of the financial segregation that exists in the country, which, according to Anderloni et. al (2006), is related to the difficulties of individuals of more vulnerable classes in gaining access to the financial system in all its dimensions, such as opening a checking account, to payment forms other than cash, or to satisfactory interest rates. In addition, both those categorized as “unbanked” (having no access to a formal banking institution) and those categorized as “underbanked” (having restricted access to banking services) are, according to Crocco, Santos and Figueiredo (2013), more likely to seek the informal financial market, where informal credit can be found.

According to Caouette, Altman and Narayanan (2009), the expansion of credit for certain sectors of a country may explain the reason why some countries are developed and others are underdeveloped. Dow (1987) created models composed of different patterns showing how the financial system works in certain sectors and regions. These patterns helped understand the more developed regions based on the market liquidity promoted by optimistic agents, who enabled and contributed to the existence of more credit in circulation. It is also important to emphasize the influence of credit on social change and evolution, since it helps people achieve goals and is considered an agent that causes or facilitates the movement of goods and services.

Furthermore, according to Allen, DeLong e Saunders (2003), the retail credit market faces specific challenges due to its characteristics and should not be analyzed with the same models used for the analysis of large loans, because, among other reasons, loans in this sector are mostly granted to small and uncategorized clients.

In this context, this study aims to analyze the management of the offer of informal commercial credit (ICC) in MSEs, specifically the profile of entrepreneurs and the business practices associated with its adoption. Our specific objectives are to understand the main factors taken into account by entrepreneurs when deciding to carry out this type of transaction, as well as their opinion regarding customer default. This study defines ICC as the operations carried out between MSEs and their customers through promissory notes, post-dated checks, or simple notes that may or may not contain the customer’s signature (known in Portuguese as notinhas).

According to data from the Brazilian Micro and Small Enterprises’ Support Service (Serviço Brasileiro de Apoio às Micro e Pequenas Empresas – SEBRAE, 2017), in 2015, there were around 6.8 million establishments of MSEs, representing 54% of the formal jobs in private, non-rural establishments in the country (17.2 million) and almost 44% of the wages paid to workers. Between 2005 and 2015, MSEs created 6.1 million formal jobs (representing 55.3% of the growth in the period and an average growth of 4.5% per year), and the actual average income of formal employees increased by 2.6% per year. This result is higher than the growth of the actual average income of all workers in the formal market (2.1% per year) and of the workers allocated in medium-sized and large enterprises (1.6% per year).

According to Douette, Lesaffre and Siebeke (2012), in most countries in the world, MSEs contribute with more than 50% of the GDP and employ around 40% of the workforce. In Brazil, MSEs represent 27% of the GDP according to data from SEBRAE (2018). Furthermore, according to Torre, Pería and Schmukler (2010), small enterprises have become an essential topic for economists and politicians because they represent a majority, which leads to a strong impact on a country’s economic indicators, attracting interests to offer financial and tax incentives to foster their development. Given the above, the justification for this study is based on the fact that MSEs are one of the main pillars supporting the economy, in addition to being essential for political and social stability.

Considering that this study was carried out in Ituiutaba-MG, a city with 104,067 inhabitants as of 2018 (IBGE, 2019), we believe a better understanding of this informality of credit management in a city of this size may lead to improvements in the city’s business practices. In addition, this study may help the entrepreneurs who fit our profile improve their management system and understand the influence and importance of informal credit for their companies. We believe that identifying the variables taken into account by entrepreneurs during the ICC offer, as well as their stance regarding customer default, are of great importance for managing a small commercial company.

It is important to mention that this topic is not widely explored in the literature on finances, and we did not find studies analyzing this type of credit operation, be it at the national or international level. When researching the topic of credit, filtering for micro and small commercial companies, and adding the keyword “informal”, the evidence was related to the informal financing of micro and small companies. Since we will examine the profile of credit offer by these companies in this research, that is, the other side of the story, we expect to fill a gap in the literature that is essential for the evolution of knowledge in the financial area and of micro and small regional companies. In addition, little is known about the development and the size of the informal economy around the world (SCHNEIDER; BUEHN; MONTENEGRO, 2010), and this trait is even more present in the Brazilian market.

2 THEORETICAL FRAMEWORK

Credit – and everything involved in it – is related to the companies’ working capital, which corresponds to all short-term resources from either current assets or liabilities, which can generally be converted into cash within a maximum term of one year. Therefore, the management of working capital in an organization corresponds to the identification, organization, planning and management of its short-term resources, essentially, but not exclusively, cash, bank accounts, savings accounts, customers, inventory, suppliers and short-term loans.

It is a challenge for any company to make a good management of working capital in such a way as to be able to reconcile its payments with receipts and maintain an inventory with no shortage of goods for customers but also no lack of liquidity, taking into account high storage costs and damage/thefts, short-term loans that are not fixed, with credit that is within conditions and terms that satisfy the customer but also that can be financed by the company.

A company can survive many years with no profit or income whatsoever, but it is unlikely to survive without good management of working capital. Especially for MSEs, good management is even more important due to several factors such as the low availability of options for financing the company’s activities and the high interest rates of bank financing. Alvarenga (2016) carried out a study aiming to analyze the determining factors of MSEs mortality and the main finding was the lack of sufficient working capital to run the company associated with difficulties to access capital with financial institutions.

Regarding the reasons why working capital is a determining factor for MSEs mortality, a study carried out in the state of Minas Gerais showed that the main difficulties in managing an MSME’s working capital are the low level of informatization of the company’s financial systems, followed by the lack of synchronization between payments and receipts, failing to bill overdue debts, and poor inventory management (SILVA; FONSECA; BITARAIS, 2018).

And although the cash management of MSEs is normally an asset of more concern when it comes to working capital, there are several other issues such as negligence by the company’s managers regarding their credit and billing policies.

A credit operation is defined as a process carried out between surplus agents, considered to be savers, and deficit agents, who need financial resources. Credit is defined as the exchange of a present value for the promise of future reimbursement. To better understand this concept, we need two fundamental notions: the trust expressed by the promise of payment, and the period of time established between the borrower and the lender.

According to one of the first authors to analyze the relationship between credit and the economy (BECKMAN; OTTESON, 1949), the offer of credit needs to be seen as an important strategic resource to help reach the goal of financial administration, namely the maximization of value for stakeholders.

According to Minussi, Damacena and Ness (2002), the activity of granting credit is influenced by a country’s microeconomic, political and governmental conditions, fluctuating between defensive conservatism and responsible aggressiveness. In that sense, according to the authors (ibid., p. 111), “credit systems normally result from a layer of attitudes, responses and behavioral patterns that derive from the organizational strategic level and, many times, from the chief executive responsible for the area”, while “the philosophy of the organization, tradition and existing patterns are additional incorporated factors”.

A process of credit analysis aiming to determine a customer’s suitability and financial capacity to pay commonly uses the technique known as the Cs of Credit, reflecting the opinion, experience or feeling of the company’s analysts or executives as described by Minussi, Damacena and Ness (2002).

In this subjective credit analysis technique (the Cs of Credit), the decision is based on acquired experience, availability of information, and the analyst’s understanding of the risk posed to the business. The process is composed of 5 main categories, namely: character, which is associated with the customer’s market suitability; capacity, which refers to the decision regarding the customer’s ability to convert their investments into revenue; capital, which is the customer’s financial situation; collateral, which is the customer’s assets and wealth; and conditions, which refers to the understanding of the customer’s ability to pay even if adverse external factors occur (SANTOS, 2015).

Credit and the payment forms offered by MSEs are important benefits that they need to offer in order not to lose sales; however, unfortunately, customer credit analysis techniques are not commonly used by MSEs, even simple ones such as the Cs of Credit.

The main forms of consumer credit that exist in the Brazilian market are checks, credit cards, boletos, installments, private labels, direct customer credit (CDC), promissory notes, leasing, and real estate credit. According to Guimarães e Neto (2012), consumer credit usually leads to a high volume of low values for MSEs because there is a high number of customers. The authors (ibid.) state that the methods used to analyze these consumers are limited because there is a large mass of customers and data collection is difficult, which often leads to incomplete registrations.

When it comes to MSEs, it is common practice to carry out credit transactions registered in promissory notes, post-dated checks and notinhas. Despite the existence of this market and the hypothesis that the offer of ICC is important for this profile of enterprise, these types of credit operations are not studied by the literature on finance.

3 METHODOLOGY

This study involved MSEs located in Ituiutaba-MG. The first step was estimating the amount of companies established in the city. We determined through the Chamber of Shopkeepers (Câmara de Dirigentes Lojistas – CDL) that the city had a total of 531 companies associated with the chamber. From that list, we selected companies from the sectors of commerce and services such as clothing and footwear stores, opticians, fishing supplies stores, snack bars, grocery stores, ice cream parlors, bakeries, technical assistance, laundries, clothing manufacturing, and weight training academies, among other sectors. These activities were chosen because, according to SEBRAE (2017), commerce was the activity involving the highest number of MSEs in the country in 2015 (45.2%), followed by the services sector (39.1%).

The parameters used to select which of the MSEs would participate in the study were based either on the number of employees or on revenues, following the criteria of SEBRAE (2013).

Using these parameters, we found 320 companies associated with the CDL that fit the profile we established for the study. Although we did not collect information on all these companies, at the end of the application of the questionnaire there were 301 companies in the sample.

The first nine questions of the questionnaire encompassed general aspects of the companies and entrepreneurs. The purpose of these questions was to learn about the profiles of the companies/owners and identify potential influences of those profiles on the way they deal with informal credit. The references we adopted to categorize each of these variables were the groups determined by the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística – IBGE), the National Classification of Economic Activities (Classificação Nacional de Atividades Econômicas – CNAE), and the classification of SEBRAE.

The remaining questions were prepared according to the information required regarding the offer of ICC, which was identified during the planning and questionnaire preparation steps (pilot study and pre-testing of the questionnaire). It is important to mention that the application of the complete questionnaire was only carried out for companies operating with the offer of ICC. Otherwise, after the questions related to the profile of the company and owners, we asked a single additional question regarding the reasons why the company did not use informal credit (question 18 in the questionnaire).

Question 10 is related to the credit instruments used by the companies for credit sales. The answers to this question were used to build a dichotomous variable in which: 0 = Credit cards, boletos, booklets, and companies that do not offer credit sales; and 1 = post-date checks, notinhas and promissory notes. In this case, the answer category 1 indicates the presence of informal credit in the company’s total revenue. This variable was associated with the other variables related to profile of the company and owners in order to detect potential connections, which were statistically verified through the Chi-square test (χ2).

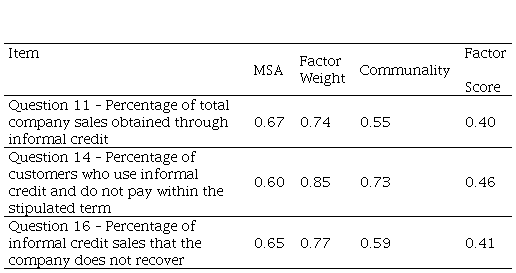

For companies that adopt an ICC instrument, we asked four ordinal questions: question 11 (%Informal credit/credit sales), question 13 (Average term with informal credit), question 14 (%Informal credit/delays) and question 16 (%Informal credit/losses). These questions sought to assess the credit risk perceived when offering ICC. From these questions, which were considered items of the aforementioned construct, we adjusted a model of Exploratory Factor Analysis (EFA) expecting to estimate a common factor (latent trait) to measure the credit risk perceived when offering ICC. Our initial perception was that these four items were likely to be correlated, and that, despite using a subjective measure through the opinion of the owners, which is susceptible to measurement errors, a credit risk factor could be reliably obtained in statistical terms about the offering of informal commercial credit.

In addition, we proposed the independent application of an EFA on question 15, which was conceived to assess the billing policies adopted by the companies who offer ICC. This question has a 4-point Likert scale (1 = Never, ..., 4 = Always) and its last item (15.9 “No billing policies are enforced”) was separated to be use used as a convergent verification item.

The two proposed EFA models were estimated from the correlation matrix, by principal components, using varimax rotation and the eigenvalue criterion > 1 to determine the number of factors. To adjust the AFE models, we followed the recommendations of the literature and paid attention to: a) communalities greater than 0.30; b) significant Bartlett’s test of sphericity; c) measures of sampling adequacy (MSA) > 0.50; d) factorial loads greater than 0.40 as it is a relatively large sample; e) Kaiser-Meyer-Olkin measure (KMO) > 0.60; f) percentage of the total variance explained by all factors around 50%; and g) Cronbach’s alpha > 0.60. The factor scores originated in the models were estimated by the regression method with standardized factor scores, relating among them the company/owner profile variables and questions 10 and 12.

Due to the intrinsically ordinal character of most variables, including the factors that were estimated in the EFA, we chose to use nonparametric tests: i) Spearman’s Correlation (ρ); Mann-Whitney Test (Z); and Kruskal-Wallis Test (χ2). However, because questions 10 and 12 allow multiple answers, we used the t-test adjusted for multiple comparisons via Benjamini-Hochberg to evaluate the relationship of the factors estimated in the EFA for these questions due to the lack of a comparable test in the non-parametric field. We believe that, despite the lack of normality of the variables, the t-test would present asymptotically reliable results due to the sample size. It is worth mentioning that, to carry out the statistical tests, we adopted the procedure of agglutinating the classes/categories of the company/owner profile variables with few observations, except for Spearman’s Correlation. We used a significance level of 5% and the SPSS v.24 software for the analyses.

4 RESULTS

4.1 Profile of the companies and owners

The main area of activity of most of the 301 companies in the study is retail business, which corresponds to 75.4% of the sample. Next, we have the food industry with 10.0%, and sales and repair of motor vehicles and motorcycles with 6.6%. Regarding the time of activity of the companies, 63.1% have been operating for more than 5 years, while 9.0% have been operating for less than 1 year. Therefore, the sample is comprised mostly of solid companies, which is an important characteristic for evaluating their management of informal credit, assuming they already have experiences in this practice.

Regarding the number of employees, 63.5% stated that they have between 1 and 4 employees, and 24.3% have between 5 and 9, which means 87.8% of them can be considered micro-enterprises in this classification. Regarding gross monthly revenue, 16.3% of the companies have a revenue of less than or equal to R$ 5,000.00 (five thousand reais), and 49.8% have revenues between R$ 5,000 (five thousand reais) and R$ 30,000 (thirty thousand reais): in this classification, 66.1% of them can be considered micro-enterprises. The questionnaire also showed that 28.2% of the companies have revenues higher than R$ 30,000 (thirty thousand reais) and lower than or equal to R$ 300,000 (three hundred thousand reais), which means they can be considered small enterprises. Only 1.3% of the companies declared revenues higher than R$ 300,000 (three hundred thousand reais), and 13 companies (4.3%) refused to answer this question.

Regarding the profile of the owner, we found that 60.0% of the entrepreneurs interviewed are between 35 and 54 years old, and only 3.7% are below 24 years old. Compared to national data, this percentage is lower than the 72.5% (2015 data) of employers between 35 and 64 years old (SEBRAE, 2017). The data collected also showed that 39.5% of the entrepreneurs have only completed high school or technical education, while 24.6% have higher education and 1.7% have no formal education. Therefore, almost 65% of the employers in the sample have completed high school or higher education, which is similar to the national average of 69.5% in 2015 (SEBRAE, 2017). Most of the 301 entrepreneurs interviewed are male (66.8%), which is consistent with the national scenario, in which the proportion of female employers was 27.3% in 2015, and with the scenario in Minas Gerais, in which it was 25% in 2015, according to SEBRAE (2017).

We can outline the type of profile in the sample as micro-enterprises whose main activity is retail business and which have been operating in the market for more than 5 years. In addition, most of their owners are men between 35 and 54 years old who have completed high school/technical education or higher education.

4.2 Description of credit information

First, we analyzed the payment forms offered to customers by the MSEs in the sample, which enabled us to determine the amount of companies who offer informal credit sales. Only 14 of the 301 companies in the study informed that they do not offer any sort of credit sales. This means that more than 95% of the MSEs participating in the study offer credit sales.

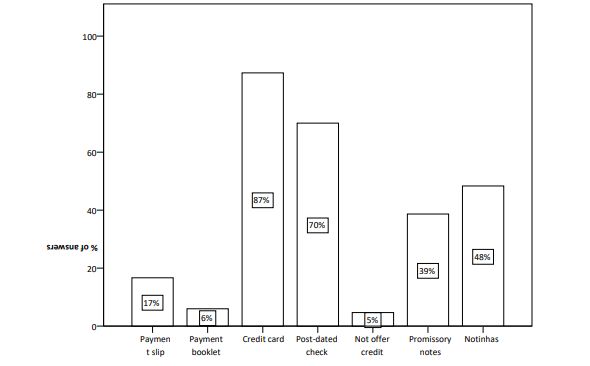

Among the companies who offer credit sales, the most frequent payment form used is credit cart, representing 87% of the answers (). We can also see in Figure 1 that 70% of the MSEs informed that they accept post-dated checks, while 48% accept notinhas and 39% accept promissory notes. Additionally, 237 of the companies (79%) accept at least one of the forms of payment considered in this study to be instruments of ICC offering, and 64 of the companies (27%) accept all 3 of those forms of payment. These numbers demonstrate the importance of these forms of payment for the MSEs that participated in the study. Indeed, according to the answers to question 17, 43.5% of the 237 companies in the sample who offer ICC stated that they would not survive if they did not offer those forms of payment.

Graph 1 - % of answers about the credit instruments used

Elaborated by the authors.

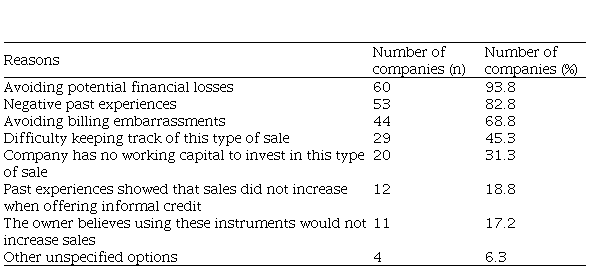

Table 1 presents the reasons why the companies in the sample do not sell through ICC. We found that 93.8% of the companies that do not offer ICC do not do so because of potential financial losses, and 82.8% because they have had negative experiences in the past with this type of credit operation. In addition, 68.7% (also a high percentage) informed that they do not offer ICC because they prefer to avoid billing embarrassments, and 45.3% because they consider it difficult to keep track of these types of sales.

These findings tell us that the main problem keeping MSEs from offering informal credit is the risk of default, both due to past experiences and due to the expectation of loss. This may indicate that the owners of MSEs would be willing to sell on credit through informal payments if they were able to implement a more efficient management of their billing policies.

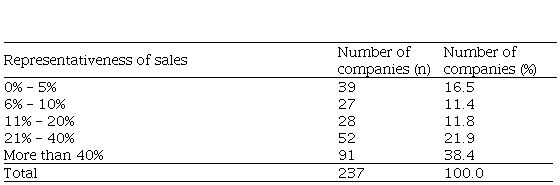

In order to more reliably determine the role of offering ICC for the MSEs in the study, we sought to identify the importance of this type of sale in the company’s total sales. To do so, we asked about the representativeness of informal credit offers in the total sales of these companies. This question was asked directly to the owners, which implies that the answers represent their perceptions, which can be different from the real data.

Reasons why companies in the sample do not offer informal commercial credit

Elaborated by the authors.

Source: Elaborated by the authors.

Out of the 237 of the companies that offer ICC, 43.5% stated that they would not survive if they did not offer these forms of payment. As seen on Table 2, we found that 38.4% of the companies obtain more than 40% of their gross revenue through the offer of ICC, and 21.9% obtain between 21% and 40% of their revenue that way; that is, for more than 60% of the companies in this study, the offer of ICC represents at least 20% of the gross revenue. This indicates a significant representativeness of informal credit sales for MSEs, confirming the opinions of 43.5% of the owners who stated that their companies would not survive without ICC.

Sales of companies in the sample obtained through informal commercial credit

Elaborated by the authors.

Source: Elaborated by the authors.

In a credit granting process, it is normal for companies to analyze the customer’s economic and financial situation and their ability and willingness to pay the debt, as well as their registration data and other information. Although this information is relevant in a credit granting process, we suspect these were not the main reasons for micro and small entrepreneurs to sell through notinhas, promissory notes and post-dated checks due to the peculiarities of this type of sale.

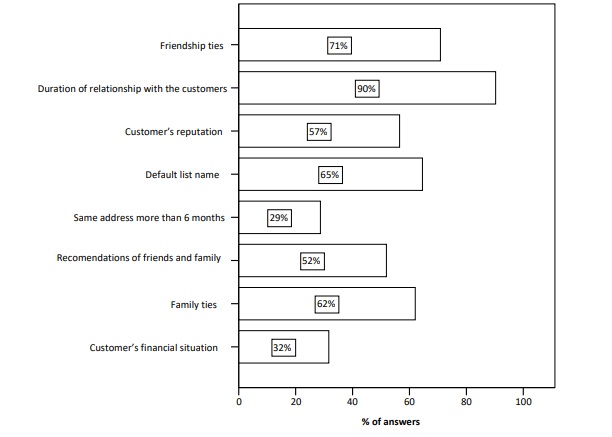

Therefore, we sought to identify the main criteria taken into account by micro and small entrepreneurs in the decision process involved in credit sales through informal forms of payment (). One of the most important criteria indicated by the MSEs in the study was the duration of relationship with the customer. 90.3% of the MSEs believe that this criterion is important when selling to a customer through ICC, which is in line with the traditional credit risk evaluation that usually sees “friendly customers” as presenting a lower credit risk than new customers.

Other important criteria that MSEs take into consideration were friendship ties, family ties and recommendations of friends and family. We can see from Figure 2 that around 70% of the companies interviewed stated that they offer informal credit sales to friends, 62% stated that they do so for family members, and 41% stated that do so for certain customers because they were recommended by friends or family members. Unlike the criterion of duration of relationship, these criteria can be considered specific of MSEs and are relevant to understanding the dynamic of their ICC granting process.

Graph 2 – Items taken into account by the company when offering credit sales through informal commercial credit

Elaborated by the authors.

Other relevant criteria were not being known for having bad credit (65%) and the customer’s reputation (57%), which were common in any process of credit granting. Although the customer’s financial situation is one of the most relevant factors in a credit granting process and is included in the “Cs of Credit”, it is not predominant in the offer of ICC granted by MSEs, considering that only 32% of the companies in the study stated that they take this criterion into account for their evaluation.

Regarding payment terms, 77.2% of the companies that use ICC stated that payments usually occur between 16 and 60 days. However, 20.3% stated that they allow payments for this type of sale after more than 60 days, which may lead to several problems for MSEs since they usually do not have enough working capital to maintain this strategy. In addition, these long terms may lead to default and losses. 28.7% of the 237 companies stated that more than 40% of the clients who make purchases through ICC delay their payments, and 47.7% stated that they do not recover between 5% and 32% of this credit, which is considered a financial loss.

4.3 Profile of entrepreneurs and business practices associated with offering informal commercial credit

Out of the 301 companies in the sample, around 22% stated that they do not use any ICC instrument, or do sell on credit. The comparison of this classification (0 = does not adopt ICC; 1 = adopts at least one ICC instrument) to other company/owner profile variables did not generate a significant association, except regarding gross monthly revenue, where we found that companies with higher revenue (> R$ 30,000) tend to use more ICC instruments than companies with lower revenue (≤ R$ 5,000) (χ.= 7.176; p-value=0.028).

As mentioned in the methodology section, we asked four ordinal questions aiming to determine the credit risk perceived with the offer of ICC. The adjustment of the initial EFA model with all four items considered presented a two-factor solution, with question 13 (Average term stipulated for the customer to pay with informal credit) isolated into a single factor. Therefore, we chose to exclude this item and obtained the solution presented on Tabela 3.

Factor model of perceived credit risk with informal commercial credit practices

Elaborated by the authors. KMO = 0.63; Bartlett (χ2) = 132.39 (p-value < 0.001); % Explained Variance = 62.35%; Cronbach’s Alpha = 0.70.

Notes: KMO = 0.63; Bartlett (χ.) = 132.39 (p-value < 0.001); % Explained Variance = 62.35%; Cronbach’s Alpha = 0.70.

Source: Elaborated by the authors.

All adjustment measures were adequate according to the criteria established in the methodology section, and the estimated factor, which in this study is the perceived credit risk with ICC practices, was found to be reliable. Higher factor scores indicate higher perceived credit risk levels with ICC practices.

Relating the factor scores to the profile variables, we found that perceived credit risk with ICC practices is negatively associated with the educational levels of company owners (ρ=-0.17; p-value=0.009): the higher the educational level of entrepreneurs, the lower their risk perception regarding the ICC carried out by the company.

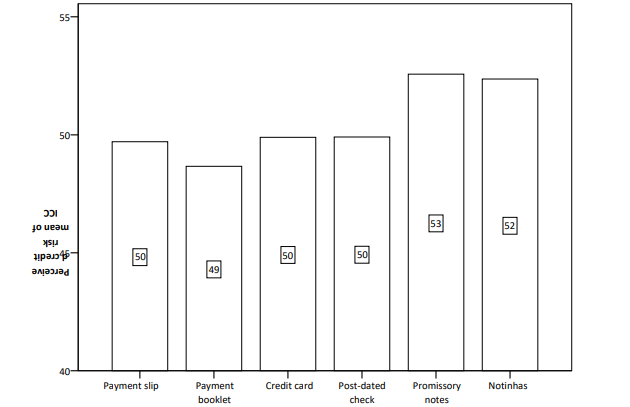

We also related the perceived credit risk scores with ICC practices to the ICC instruments and the reasons to adopt them. By applying the t-test corrected by Benjamini-Hochberg, we found statistically significant differences (p-value < 0.05) between the companies that use promissory notes and notinhas as credit instruments and the companies that use the other credit instruments we listed. These findings demonstrate that owners perceive ICC, especially promissory notes and notinhas, to be riskier than other credit instruments.

Figure 3 helps better visualize these differences: the standardized perceived credit risk scores with ICC practices were normalized at base 100 [normalized score = 100 x (standardized score + 6)/2] for better clarification.

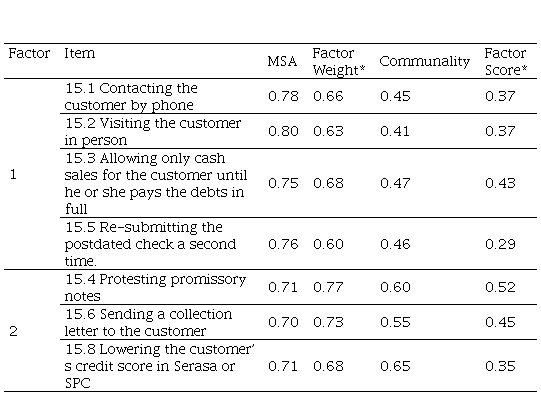

To analyze the companies’ practices associated with billing policies, the initial EFA model for all billing policies items showed a bad adjustment, mainly due to the low communality of item 15.7 (Collecting overdue payments through a lawyer). This finding was somewhat expected since few companies indicated that they collect overdue payments through a lawyer, which meant this item showed low variability and discriminating power. After removing said item, the model and its measures of adequacy were as shown in Table 4.

Figure 3

Graph 3 – Perceived credit risk and instruments used in credit sales

Elaborated by the authors.

Overall, the model is considered acceptable since most of the measures of adequacy are inside the criteria listed in the methodology section, except for the Cronbach’s Alpha of the first factor, which was slightly below the established value. Nevertheless, since most measures were adequate, such as the KMO and the high factor weights, we chose to continue using this model. In fact, other similar models with variations in the extraction and rotation techniques and compatible in statistical and theoretical terms were obtained and their factor scores correlated. Since the correlations between the scores in the model of Table 4 and these other simulated (alternative) models were very high (ρ> 0.80), we believe that the results presented are not dependent on the statistical techniques used and the same conclusions could be reached.

It was interesting to observe that, from a theoretical point of view, the items agglutinated around two very intuitive factors: the first factor may be called billing policies with non-explicit cost, and the second factor may be called billing policies with explicit cost.

It is worth mentioning that the first factor was positively correlated with the item “No billing policies are enforced” (ρ=0.38; p-value<0.000), and that same item was note correlated with the second factor as initially expected for a convergent validity.

When relating the two factors emanating from the EFA for the billing policies with the profile variables, the following results were found:

1) There is a positive correlation (ρ=0.27; p-value<0.000) between billing policies with non-explicit costs and the number of employees.

2) Also regarding the other size variable, there is a positive correlation (ρ=0.18; p-value<0.006) between billing policies with non-explicit costs and gross monthly revenue.

3) The results in 1) and 2) were also found for the billing policies with explicit costs: i) positive correlation with the number of employees (ρ=0.15; p-value=0.022) and ii) with the gross monthly revenue (ρ=0.17; p-value=0.013);

4) We found a positive correlation (ρ=0.15; p-value<0.025) between billing policies with explicit costs and the owner’s educational level;

5) Companies opting for Real/Presumed/Simple Profit had a higher score than individual micro-entrepreneurs in billing policies with non-explicit costs (χ2 = 19.43; p-value <0.000).

Factor model for billing policies adopted

Elaborated by the authors. KMO = 0.74; Bartlett (χ2) = 218.92 (p-value < 0.001); % Explained Variance = 51.05%; Cronbach’s Alpha = 0.57 (Factor 1 = Billing policies with non-explicit costs) and 0.61 (Factor 2 = Billing policies with explicit costs). *Considering the maximum value, in module, loaded in each factor.

Notes: KMO = 0.74; Bartlett (χ.) = 218.92 (p-value < 0.001); % Explained Variance = 51.05%; Cronbach’s Alpha = 0.57 (Factor 1 = Billing policies with non-explicit costs) and 0.61 (Factor 2 = Billing policies with explicit costs). *Considering the maximum value, in module, loaded in each factor.

Source: Elaborated by the authors.

Additionally, the two factors for billing policies were also correlated with the perceived credit risk with ICC practices, where we found a positive and statistically significant correlation (ρ = 0.17; p-value = 0.010) only between perceived credit risk and billing policies with explicit costs. This seems to be very adequate in terms of risk perception, since this greater perception of the risk by entrepreneurs when offering ICC implies more forceful billing policies (which have costs) in order to increase the probability of recovery.

Regarding the credit instruments, there was evidence (p-value <0.05) suggesting that billing policies with explicit costs are more present in companies that use boletos, booklets and promissory notes.

Regarding the reasons for adopting ICC, companies that take into account: i) the customer’s financial situation; ii) having a permanent address for more than 6 months; iii) not being known for having bad credit; and iv) reputation when deciding to offer credit sales have higher scores in billing policies with non-explicit costs. This situation is partially repeated in the case of billing policies with explicit costs: only companies that indicated that they take into account having a permanent address for more than 6 months and not being known for having bad credit when deciding to offer credit sales have higher scores in billing policies with explicit costs.

5 FINAL REMARKS

This study sought to analyze the management of informal commercial credit (ICC) in MSEs, specifically the profile of entrepreneurs and the business practices associated with its adoption. The results showed that, out of the 310 companies in the sample, around 80% (237 companies) sell to their customers through ICC. Of these 237, 43.5% stated that they would not be able to survive without this type of sale and that post-dated checks (88.2%) are the most common instrument used, followed by notinhas (61.2%) and promissory notes (48.9%). This demonstrates the importance of this type of credit operation and indicates it is a common practice among small entrepreneurs.

Analyzing the criteria taken into account by the MSEs when deciding whether to offer credit sales through ICC, we found that duration of relationship (90.3%), level of friendship (70.9%), not being known for having bad credit (64.6%), and being family members (62.0%) were the most common factors indicated. Therefore, taking into account criteria related to friendship and family are a characteristic of ICC in the credit granting process. We highlight that these criteria are not considered in “traditional” credit risk assessment models, particularly in the Cs of Credit.

Despite the high rates of default and losses, the billing policies adopted by the MSEs in the study are also informal, with a predominance of making phone calls and interrupting sales to the customer. Only 22.8% stated that they always lower the customer’s credit score when a payment is overdue, and 75% have never taken legal action or protested a customer’s promissory notes, possibly because there are friendship and family ties with many customers.

Regarding the profile of the entrepreneurs and the business practices associated with the ICC process, we found a relationship between gross monthly revenue and the ICC instruments used by the companies; the entrepreneur’s educational level and the risk perception associated with ICC; the differences regarding risk perception in companies that adopt promissory notes and notinhas and those that adopt the other credit instruments listed in the study; and a positive correlation between perceived credit risk and billing policies with explicit costs.

The main findings of this study indicate the importance of ICC for the MSEs that participated in the research, and that the management of this type of credit operation needs to be analyzed further by companies seeking to decrease default issues and losses coming from ICC, as well as to improve their management processes. In addition, these findings are important to better understand the ICC and the business practices associated with it, providing information to help the literature on finance consider this issue more carefully, as its representativeness in the Brazilian economy is substantial due to the importance of MSEs.

Regarding the limitations of this study, we highlight that the answers were self-declared, and even though we used strategies such as the stipulation of categories to ascertain the company’s revenue, the entrepreneur may simply not say the truth about the data and facts. Another limitation was choosing only companies associated with the CDL, excluding non-members or companies associated with other entities. Regarding suggestions for future research, we recommend expanding the sample to a regional or even national scenario for a better understanding of the Brazilian reality.

Additionally, we emphasize that this research intended to show the financial practice in terms of the use of the ICC, in a city taken as a case, without going deeper into the theoretical framework that underlies the topic. For example, ICC could be discussed within the scope of the Transaction Cost Theory (TCT), which indicates that managing investments/procuring of financial resources represents minimizing the total costs arising from the financial transactions of investments and cash loans. TCT studies the costs of collecting information, the costs of negotiation, the costs of establishing contracts, and how transactional agents protect themselves against the possibility of the agreed elements not occurring.

The topic of credit fits perfectly within this framework; however, specifically on ICC, we did not find any research and/or empirical evidence to address this relationship, even internationally. In this sense, we decided to present the survey findings in the form of a panorama, to serve as evidence of the practice of ICC in Brazil and to foment discussions, given that the vast majority of Brazilian cities are small and informal economic relations are prevalent, as seen in Ituiutaba-MG.

REFERENCES

ALLEN, L.; DeLONG, G.; SAUNDERS, A. Issues in the credit risk modeling of retail markets. Journal of Banking Finance, v. 28, n. 4, p. 727-752, 2004.

ALVARENGA, R. A. Estudos dos Fatores Contribuintes para a Mortalidade das Micro e Pequenas Empresas do Estado do Maranhão. International Journal of Innovation, v. 4, n. 2, p. 106-118, 2016.

ANDERLONI, L. et al. New frontiers in banking services: emerging needs and tailored products for untapped markets. New York: Springer, 2006.

BECKMAN, T. N.; OTTESON, S. F. Cases in credits and collections. LLC: New York, 1949.

BRASIL. Lei Complementar nº 123/2006, de 14 de dezembro 2006. Diário Oficial [da] República Federativa do Brasil, Brasília: Poder Executivo, p. 1, 2006.

CROCCO, M. A.; SANTOS, F.; FIGUEIREDO, A. Exclusão financeira no Brasil: uma análise regional exploratória. Revista de Economia Política, v. 33, n. 3, p. 505-526, julho-setembro/2013.

IBGE. Brasil: censos demográficos. 2017. Disponível em: https://cidades.ibge.gov.br/brasil/mg/ituiutaba/panorama. Acesso em: 11 de abril de 2019.

CAOUETTE, J. B.; ALTMAN, E.; NARAYANAN, P. Gestão de risco de crédito: o grande desafio dos mercados financeiros globais. Rio de Janeiro: Qualitymark SERASA, 2009.

DOUETTE, A.; LESAFFRE, D.; SIEBEKE, R. SMEs` credit guarantee schemes in developing and emerging economies: reflections, setting-up principles, quality standards. Deutsche Gesellschaft fur Internationale Zusammenarbeit (GIZ) GmbH, 2012.

DOW, S. C. The Treatment of Money in Regional Economics. In: DOW, S. C. (ed.), Money and the Economic Process. Aldershot: Eglar, 1987.

GONZALEZ, L. et al. Inclusão financeira e correspondentes bancários no Brasil. Centro de Estudos em Microfinanças, São Paulo: Fundação Getúlio Vargas, 2013.

GUIMARÃES, I.; NETO, A. Reconhecimento de padrões: metodologias estatísticas em crédito ao consumidor. Revista de Administração de Empresas, v. 1, n. 2, p. 01-14, Jul/Dez 2012.

KUMAR, A. (Coord.). BRASIL: acesso a serviços financeiros. Rio de Janeiro: Ipea, 2004. Disponível em: https://www.ipea.gov.br/portal/images/stories/PDFs/livros/BrasilAcessoAosServicosFinanceiros.pdf. Acesso em: 17 jun. 2020.

MINUSSI, J. A.; DAMACENA, C.; NESS JR.; W. L. Um modelo de previsão de solvência utilizando regressão logística. Revista de Administração Contemporânea, v. 6, n. 3, p. 109-128, 2002.

SANTOS, J. O. dos. Análise de crédito: empresa, pessoas físicas, agronegócio e pecuária. 6. ed. São Paulo: Atlas, 2015.

SANTOS, D. B.; MENDES-DA-SILVA, W; GONZALEZ, L. Deficit de alfabetização financeira induz ao uso de empréstimos em mercados informais. Revista de Administração de Empresas, v. 58, n. 1, p. 44-59, jan-fev 2018.

SCHNEIDER, F.; BUEHN, A.; MONTENEGRO, C. E. New estimates for the shadow economies all over the word. International Economic Journal, v. 24, n. 4, p. 443-461, 2010.

SEBRAE. Critérios e conceitos para classificação de empresas. 2013. Disponível em: http://www.sebrae.com.br/uf/goias/indicadores-das-mpe/classificacao-empresarial. Acesso em: 23 ago. 2013.

SEBRAE (org). Anuário do trabalho nos pequenos negócios 2015. 8º ed. São Paulo, 2017. Disponível em: https://www.dieese.org.br/anuario/2017/anuarioDosTrabalhadoresPequenosNegocios.pdf. Acesso em: 11 abr. 2019.

SEBRAE. Perfil das microempresas e empresas de pequeno porte. 2018. Disponível em: http://www.sebrae.com.br/sites/PortalSebrae/ufs/ro/artigos/perfil-das-microempresas-e-empresas-de-pequeno-porte-2018,a2fb479851b33610VgnVCM1000004c00210aRCRD. Acesso em: 28 out. 2019.

SILVA, M. G. V.; FONSECA, Z. F.; BITARAIS, A. E. Um estudo sobre a administração do capital de giro nas micro e pequenas indústrias de fundição de Divinópolis, MG. Research, Society and Development, v. 7, n. 3, p. 01-14, 2018.

SMITH, P. Assessing the size of the underground economy: the statistics Canada Perspectives. Canadian Economic Observer, v. 7, n. 3, p. 16-33, 1994.

TORRE, A.; PERÍA, M.; SCHUMUKLER, S. Bank involvement with SMEs: Beyond relationship lending. Journal of Banking & Finance, v. 34, n. 9, p. 2280-2293, 2010.

Notas de autor