Artigos

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-SinDerivar 4.0 Internacional.

Recepción: 12 Junio 2020

Aprobación: 01 Enero 2021

Abstract: We investigate how the bankruptcy rate of Brazilian companies behaves in face of changes in such macroeconomic variables as GDP, exchange rate, money supply, interest rate, stock market behavior, new businesses and inflation rate by segregating the analysis by size ( small, medium and large). For the period 2010-2020 there is evidence that an increase in economic activity decreases the bankruptcy rate of large and medium-sized companies and that increased competition increases the bankruptcy rate of companies of all sizes. In general, the bankruptcy rate of large companies is more influenced by macroeconomic variables, while small companies seem to have a more constant bankruptcy rate, being less influenced by macroeconomic variables.

Keywords: corporate bankruptcy, macroeconomic variables, vector autoregression, size.

Resumo: Investigamos como a taxa de falência de empresas brasileiras se comporta frente a mudanças em variáveis macroeconômicas como PIB, câmbio, oferta de moeda, taxa de juros, comportamento do mercado acionário, abertura de novas empresas e taxa de inflação, segregando a análise por tamanho (pequenas, médias e grandes). Para o período de 2010 a 2020 há evidências de que um aumento da atividade econômica diminui a taxa de falência de empresas grandes e médias e que o aumento da concorrência aumenta a taxa de falência de empresas de todos os tamanhos. De um modo geral a taxa de falência de empresas grandes é mais influenciada por variáveis macroeconômicas, enquanto as empresas pequenas parecem apresentar uma taxa de falência mais constante, sofrendo menos influência de variáveis macroeconômicas.

Palavras-chave: falência, variáveis macroeconômicas, vetor autorregressivo, tamanho.

1 INTRODUCTION

When starting or managing a business project, businessmenand entrepreneurs must bear in mind that they are taking risks that might bankrupt their firms. According to Everett and Watson (1998), three types of risk can influence or restrict a company's success. They are: the risks associated with macroeconomic factors, the sector in which the company operates and the organization's internal characteristics. The latter is the most studied aspect of the three. The literature has focused, above all, on analyzing the influence of microeconomic factors on the probability of bankruptcy. Financial characteristics of firms are emphasized, such as indebtedness, liquidity and profitability (SANVICENTE; MINARDI, 1998; ALMAMY, ASTON; NGWA, 2015; ALAMINOS; DEL CASTILLO; FERNÁNDEZ, 2016; LIBERMAN; BARBOSA; PIRES, 2017). Nevertheless, macroeconomic (exogenous) factors play a non-negligible influence on a company's survival. After all, firms in general have a limited capacity to influence the economic environment in which they operate (EVERETT; WATSON, 1998).

Therefore, the main motivation of this study is to examine how macroeconomic factors affect the bankruptcy of Brazilian companies. Studies that measure the impact of the economic environment on the aggregate bankruptcy rate have already been carried out around the world by using different assumptions and variables (eg, ALTMAN, 1983; PLATT; PLATT, 1994; LIU, 2009; HARADA; KAGEYAMA, 2011; ZHANG; BESSLER; LEATHAM, 2013; SALMAN; FUCHS; ZAMPATTI, 2015). For Brazil, few studies (CONTADOR ,1985; MARIO; CARVALHO, 2007; JACQUES; BORGES; MIRANDA, 2020; GARCIA, 2018) have related business insolvency and macroeconomic policy. None of those studies were conducted for companies of different sizes and nationwide. For this reason, reassessing the relationship between macroeconomic variables and bankruptcy in the country is timely and an important contribution to the literature. Managers, on the other hand, can gain insights into the importance of the macroeconomic environment in management, especially regarding the control of their liquidity and indebtedness indicators.

In this study, we used aggregate national bankruptcy data for the months between 2010 and 2020. Specifically, the percentage of occurrences over time is calculated by segregating company size (small, medium and large). The macroeconomic variables used are GDP, inflation, interest rate, exchange rate, money supply, stock market activity and new businesses creation. In addition, we analyze how the bankruptcy rates of companies of different sizes are related to one another, thus trying to understand if there is a contagion effect (the concept of contagion effect comes from a study by Lang and Stulz (1992), which states that the bankruptcy of companies in a certain sector provides negative information on that sector, thus decreasing the value of firms and increasing the chance of bankruptcy of other firms in the same sector. In this specific application, we would like to see if the bankruptcy of large companies can influence the bankruptcy rate of small companies, and vice versa). For that, a vector autoregression model (VAR) is used, which allows for a simultaneous estimation of more than one equation.

This paper is divided into four parts, in addition to this introduction. In the next section, we discuss the main articles that study the relationship between bankruptcies and macroeconomic variables. The third part describes the database used, the variables considered and the construction of the econometric model. The fourth section presents the results. Finally, the fifth section summarizes the conclusions found.

2 LITERATURE REVIEW

Altman (1983) was one of the pioneers to study the relationship between macroeconomic factors and the bankruptcy rate, focusing on US companies in the period between 1951 and 1978. The author built a time series model by using aggregate variables that, he supposed, directly affected the propensity of companies to continue operating. The results suggest that the increase in bankruptcy propensity is linked to reductions in real GDP growth, the money supply (M2) and the stock market performance index (S&P 500), in addition to the increase in the number of new firms.

In Brazil, Contador (1985) used data from companies in the State of São Paulo between 1970 and 1984 to test the hypotheses that (i) there is a natural insolvency rate and (ii) the insolvency of some companies can affect other ones in the same economic environment. In his article, Contador (1985) argues that “the much-publicized direct relationship between an increase in corporate insolvencies and recession should not be generalized” (CONTADOR, 1985, p.16), since the bankruptcies declared during the Brazilian Miracle (a period of exceptional economic growth in Brazil) were greater than thoseobserved during 1981 and 1982, notably recession years.

Contador (1985) tested three models, each with a different dependent variable, namely: delinquency (in payment of dues) rates, bankruptcy petition ratesand bankruptcy adjudication rates. As explanatory variables, variables representing shifts in both aggregate demand and production costs (i.e., supply) were used. The results were unsatisfactory for the models regarding bankruptcy petition and bankruptcy adjudication, which, according to the author, suggests inadequate models or poor data quality. In addition, the variables that intended to capture the costs of labor and inputs had low significance and exchanged signs, which motivated the exclusion of these data from the results. In all the regressions tested, the intercept proved to be high and significant, which brings evidence of the existence of a natural bankruptcy rate. The author concludes that "the macroeconomic policy which is most conducive to the good financial health of companies is the one committed to curbing inflation and maintaining real interest rates at more modest levels” (CONTADOR, 1985, p. 26).

Also in Brazil, Mario and Carvalho (2007) conducted an exploratory study on the influence of macroeconomic variables on the level of indebtedness between different sectors in the Brazilian market. The authors found evidence that the GDP and the base rate of the economy influence several sectors in the country. Jacques, Borges and Miranda (2020) also analyzed these influences in B3 sectors, concluding that the exchange rate and GDP were the variables that showed the greatest association with liquidity, indebtedness and profitability indicators. Garcia (2018) analyzed the bankruptcy rate of small businesses, finding evidence that they were negatively influenced by GDP and by the simplification of the tax system, measured by a dummy referring to the adoption of the system known as Simples Nacional from the middle of 2007.

Turner, Coutts, and Bowden (1992) investigated the impact of the Thatcher government measures on the UK bankruptcy rate. Using the initial set of variables proposed by Altman (1983) as a reference, the authors added aggregate variables such as companies' profit level, interest rate and inflation rate. Their results indicated clear evidence of a structural break in the bankruptcy rate during the Thatcher years, highlighting that bankruptcies became more sensitive to changes in economic cycles. More recently, Liu (2004) found evidence that changes in the UK bankruptcy rate are associated with interest rates, credit, profits, prices and new business creation in the short and long term.

Following the same line of temporal regression modeling and the choice of macroeconomic variables, Platt and Platt (1994) introduced a variable hitherto not used in the cited literature: the profits of individual business owners. Focusing its research on small enterprises, the results found for the years 1969 to 1982 suggest that economic conditions, production costs and new business creation are determinants in the rate of bankruptcy of U.S . companies.

Utilizing a different econometric approach, Everett and Watson (1998) studied the bankruptcy rate of small businesses by using logistic models and data from shopping centers in Australia, in the period 1961-1990. The main objective of the authors was to model the relationships between unsystematic and systematic risks, and the bankruptcy rate of small companies. As non-systematic (that is, specific and diversifiable) risks are considered the risks of the sector and of the company itself – such as, for example, management problems and lack of capital. For systematic risks, the general economic environment is considered. Everett and Watson (1998) built their model in two steps. First, the impact of unsystematic and systematic risks was tested through the variables of company age and time period. In the second step, the time period variable is replaced by macroeconomic variables. It is concluded that there is a positive relationship between bankruptcy, interest rate and unemployment rate. However, counterintuitively, the relationship between bankruptcies and employment and retail sales rates also showed a positive relationship.

By using the same logistical modeling approach and segregating systematic and non-systematic risks, Oliveira (2014) investigated the main causes of insolvency in the Portuguese manufacturing industry between 2004 and 2012. The results indicate that non-systematic risks – measured by financial indicators and human capital characteristics of companies – proved to be relevant toexplain insolvency in this type of industry. As for systematic risks (measured by macroeconomic variables), it is concluded that periods of GDP growth and low interest rates contribute to the decline in bankruptcy cases.

Also in the European context, Salman, Friedrichs and Shukur (2011) modeled the bankruptcy rate of small and medium-sized Swedish companies by using quarterly data for the period 1986 to 2006. The authors conclude that, in the long run, bankruptcies are positively related to real wages and negatively related to industrial activity level, money supply, GDP and economic openness. More recently, Salman, Fuchs and Zampetti (2015) estimate Poisson, Quasi-Poisson and Binomial regressions based on the number of Swedish companies that went bankrupt in the years 1985 to 2008, as a function of exchange and interest rates, business productivity, trade openness and degree of globalization of the Swedish economy. Its results indicate that exchange and interest rates are decisive for the bankruptcy of a company, in addition to the degree of openness of the economy. This last factor dictates the degree of efficiency of companies, thus making companies more efficient and less susceptible to bankruptcy.

By using the vector autoregression (VAR) approach utilized in this study, Liu (2009), Harada and Kageyama (2011) and Zhang, Bessler and Leatham (2013) employ different variables to study the bankruptcy rate in the United Kingdom, Japan and the United States, respectively. Liu (2009) finds, for the years 1966 to 2003, different influences of macroeconomic variables. In particular, the author highlights structural changes in the impact of variations in macroeconomic variables on thebankruptcy rate of British companies: bankruptcies became more sensitive to changes in the UK money supply after 1980. Harada and Kageyama (2011) observed results compatible with expectations, highlighting that interest rate increments visibly increase the rate of bankruptcy of Japanese companies.

Finally, Zhang et al. (2013) related the aggregate of U.S. bankruptcies for the years 1980 to 2004 by using four macroeconomic variables: aggregate corporate profits, producer price index, interest rate, and capital market activity. The authors find evidence of an endogenous relationship between bankruptcy rate and interest rate – that is, a simultaneous relationship between these two variables, where one affects the other. For the other variables used in the model, the relationship with the bankruptcy rate is exogenous and, therefore, there is a unique relationship between them: corporate profits, producer prices and capital market activity cause changes in the bankruptcy rate, but the reverse does not occur.

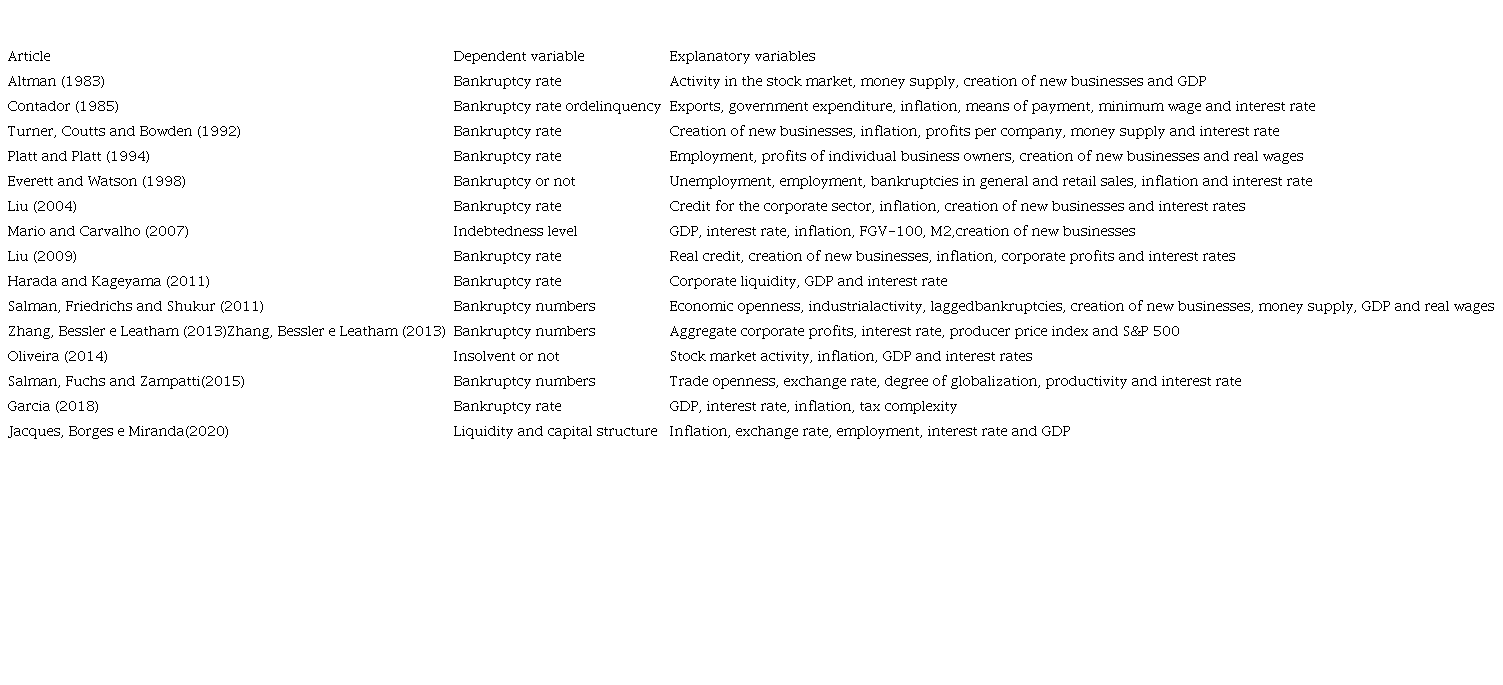

Table 1 lists the dependent and explanatory variables used in the works cited.

lists the dependent and explanatory variables used in the works cited

The methodology is presented below, containing information from the database, description of the variables and the econometric model used in the article.

3 METHODOLOGY

3.1 Database and variable descriptions

The data used in this study are monthly based, for the period between 2010 and 2020. This allows for an analysis of lagged effects, as well as possible seasonality and trends. The data are provided by Serasa Experian, the Central Bank of Brazil, the Brazilian Institute of Geography and Statistics (IBGE) and the Institute for Applied Economic Research (IPEA).

In line with the foregoing discussion, several studies use the ratio (rate) of bankruptcies as a dependent variable – that is, the proportion of bankruptcy adjudicated in relation to a certain number of companies in operation (see Table 1). However, it is relevant to note that many authors use a proxy for the number of companies in operation in the formulation of the bankruptcy rate. Altman (1983) and Platt and Platt (1994), for example, use the bankruptcy ratio for every 10,000 active companies. While Everett and Watson (1998) use the population size of Australia as a proxy for the number of companies in operation, as, according to the authors, it was not possible to find reliable information.In this study, to calculate this rate, the calculation of bankruptcies adjudicated for a specific size of company was carried out, month by month, based on the total number of companies operating in that year, considering they are all the same size as the company in question. The history of the number of monthly bankruptcies was obtained through a database of economic indicators from Serasa Experian (2021). This database contains the number of adjudicated bankruptcies segmented by small, medium and large companies, which allowed for an in-depth study of the characteristics of each size.

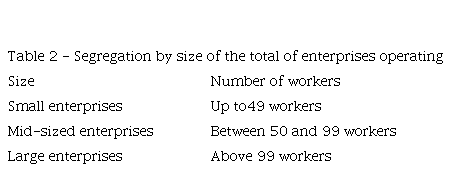

The number of companies in operation was extracted from the Central Register of Companies (CEMPRE), through the IBGE Automatic Recovery System (SIDRA, 2021) website, which is formed by companies and other organizations registered with the National Register of Legal Entities. These data are updated annually through economic surveys conducted by IBGE. The information available refers to companies and local units that, in the reference year, were active. To segregate into small, medium and large companies, the IBGE methodology utilizedto classify companies in the service sector by number of employees was adopted (Table 2). It was assumed that all analyzed companies belong to this sector because, according to Perrin and Vettorazzo (2017), in 2016, the service sector was responsible for approximately 73% of the national GDP. This is a limitation of the study, since such data are not available for all sectors of the economy.

For the explanatory variables, the model used is based on the assumptions of Altman’s (1983), who uses aggregate-level variables hoping that they will have an impact on the companies' propensity to continue operating. For this purpose, indicators that capture the following economic characteristics are used: the health of the economy and companies, credit supply, stock market activity, new business creation and changes in the price level.

3.1.1 The health of the economy and firms

It is the economic characteristic that is expected to have the greatest impact on the rate of bankruptcies, as it exerts an influence on corporate revenues. Two variables are used: the variation in the monthly real gross domestic product (GDP) and the monthly exchange rate, focused on the ratio of reais (the Brazilian currency) per dollar.

Used in most studies related to the interest of this work, the variation in real GDP allows us to capture the health of both the aggregate economy and companies in general, serving as a proxy for company revenues. It is expected that the change in GDP is negatively related to the proportion of bankruptcies, as it is reasonable to relate a more heated economy to healthy companies, which indicates a possible drop in the number of bankruptcies observed. However, it is noteworthy that “the relationship between company insolvencies and the economic cycle is not as stable and direct as it is supposed to be” (CONTADOR, 1985, p.20).

With regards to the exchange rate, any sign (positive or negative) is plausible as this relationship can vary according to the characteristics of the companies. For those whose revenues are more dependent on imports, a positive relationship between the exchange rate and bankruptcies is expected, as the exchange rate impacts, above all, the cost components. As for export-oriented companies, a negative relationship is expected: If the U.S. dollar/real conversion rate rises, this will generate higher revenues. As, historically, Brazil has had a relatively closed economy and exchange rate increases are linked to more turbulent moments in the national economic scenario, it is reasonable to expect that the positive relationship between the exchange rate and bankruptcies will outweigh the effects of a negative relationship.

3.1.2 Liquidity

The money supply, represented by the real amount of the M2 variable, represents the availability of credit for companies. It is expected that the relationship between the supply of credit and the bankruptcy rate is negative, assuming that credit is usually only available to companies that do not have their solvency compromised (ALTMAN, 1983).

Another widely used variable, the interest rate, stipulates the cost of credit for companies and is represented by the main measure of interest in the Brazilian market, the SELIC rate, which is defined by the Central Bank. The SELIC should present a positive relationship with the proportion of bankruptcies because a higher interest rateleads to an increase in companies' financing costs, thus making the viability of newprojects more difficult.

3.1.3 Stock Market activity

We use the Ibovespa one-month realized volatility index as a proxy for stock market activity. The aim is, therefore, to capture investors' expectations and it is expected that its relationship with the proportion of bankruptcy rate will be inverse. It is reasonable to relate a rise in the index with better economic prospects for individuals and investors and, thus, for healthy companies in general (ALTMAN, 1983).

3.1.4 New business creation

Suggested by Altman (1983) and used in several articles, the creation of new businesses is linked to increased competition in the market. According to economic theory, the greater the competition, the greater the pressure on firms' profit margins. Therefore, companies that have higher costs and less efficient management will be more susceptible to bankruptcy. Furthermore, according to Jovanovic (1982), young companies are more likely to fail, as they are still in the process of learning about their industry and their management capabilities. Therefore, a positive relationship between the creation of new companies and bankruptcy rate is expected.

3.1.5 Price level changes

We use inflation measured by the Extended National Consumer Price Index (IPCA) as a reference for price level change. The variation in the inflation rate is important to explain the predictability of the economic environment. In general, the greater the inflation, the greater the level of uncertainty about future flows (WADHWANI, 1986). Therefore, a positive sign is expected, that is, an increase in inflation generates an increase in the proportion of bankruptcies.

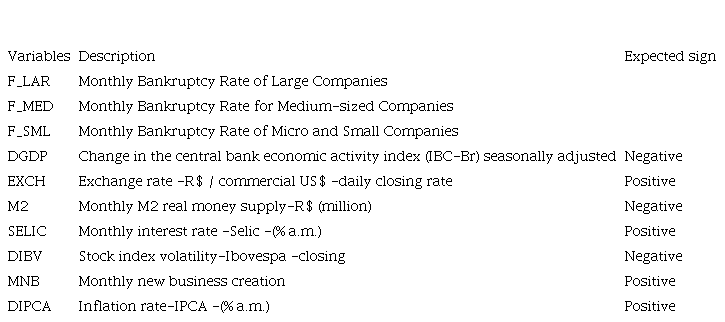

Table 3 shows a detailed description, as well as the expected sign of each variable used in the model.

shows a detailed description as well as the expected sign of each variable used in the model

Through a preliminary analysis, it was verified the need to apply the logarithmic transformation to the data series of M2 and MNB (monthly new business creation) because they present a very heterogeneous behavior (i.e., a less stable variance over time).

3.2 Econometric Model

As indicated above, we used a vector autoregression (VAR) model in this study. The VAR is a generalization of univariate time series regression models for the multivariate case, where each equation of a system defined by the VAR is regressed by the ordinary least squares method as a function of the lags of the variables of interest and other explanatory variables.The general VAR (p) model is expressed as follows:

𝑋𝑡𝑡=𝜙𝜙0+𝜙𝜙1𝑋𝑋𝑡𝑡−1+⋯+𝜙𝜙𝑝𝑝𝑋𝑋𝑡𝑡−𝑝𝑝+𝜓��0𝑍𝑍1+𝜓𝜓1𝑍𝑍𝑡𝑡−1+⋯+𝜓𝜓𝑝𝑝𝑍𝑍𝑡𝑡−𝑝𝑝+𝜀𝜀𝑡𝑡 (1) Where 𝜙𝜙0 is the 𝑛𝑛𝑥𝑥 1 vector of the intercepts; 𝜙𝜙1, ...,𝜙𝜙𝑝𝑝 are 𝑛𝑛𝑥𝑥𝑛𝑛 matrices of the lagged coefficients of the endogenous variables; 𝜓𝜓0, ...,𝜓𝜓𝑝𝑝 are 𝑛𝑛𝑥𝑥𝑛𝑛 matrices of the current and lagged coefficients of the exogenous variables; 𝜀𝜀𝑡𝑡 is the 𝑛𝑛𝑥𝑥 1 vector of errors.

In this case, we estimate a trivariate VAR, that is, the vector 𝑋𝑋𝑡𝑡 is 3𝑥𝑥 1representing three equations, one for each category of company size: small, medium and large.

According to Gujaratti and Porter (2011), the stationarity of the variables used in a time series model is essential. Otherwise, there is a risk of obtaining self-correlated results, in addition to the possibility of estimating a spurious regression (i.e., where a high correlation is found between the regression variables when, in reality, there is no significant relationship between them). To assess the stationarity or not of the variables, graphical analyses and an observation of the correlograms of each variable can be performed. In addition, the Augmented Dickey-Fuller (ADF) test is widely used in the literature and indicates the presence of a unit root in each time series. A series with a unit root is, by definition, not stationary.

Finally, once the models are estimated, a detailed analysis of the residuals is carried out. The purpose is to check the quality of the estimates, applying the White test (to check if the errors are homoscedastic), Jarque-Bera (to check if the errors are normally distributed) and the LM test (to check if there is a serial correlation between the errors).

4 RESULTS

4.1 Descriptive analysis

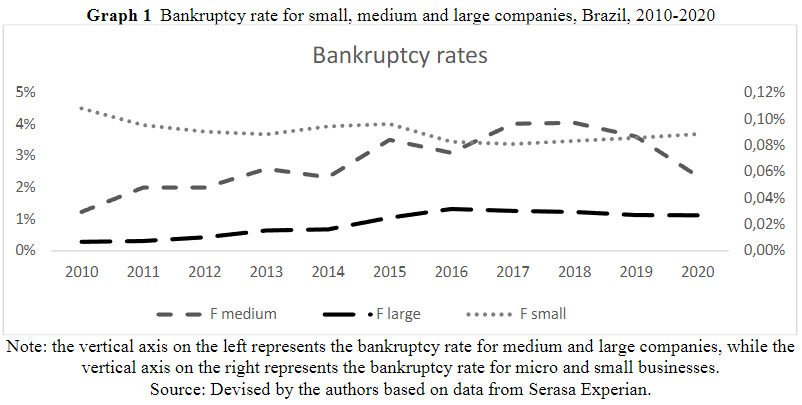

Graph 1 shows the trajectory of the bankruptcy rate for small, medium and large companies in the period analyzed. It is possible to note that, between 2010 and 2020, the bankruptcy rate for small businesses remained relatively constant. In contrast, rates for medium and large companies have shown an upward trend over the years, especially from 2014 onwards, which coincides with the deterioration of the political and economic situation in the country (NETO; CARDOSO; PENA, 2019).

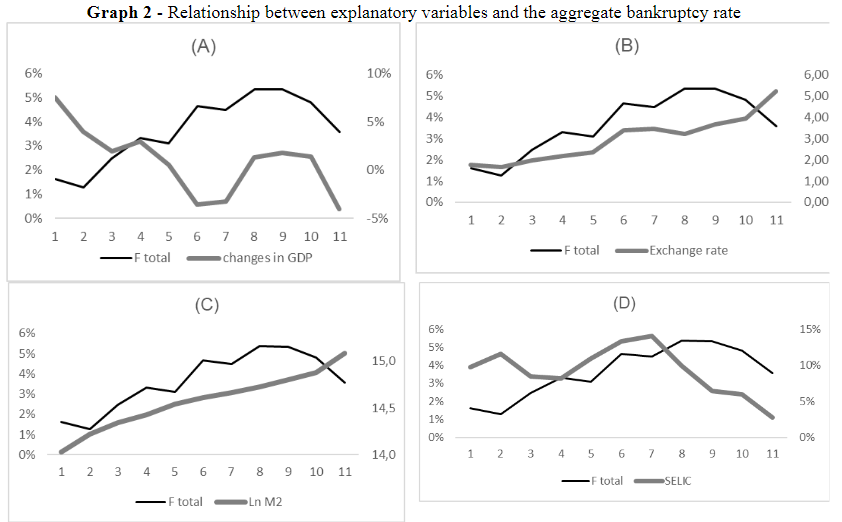

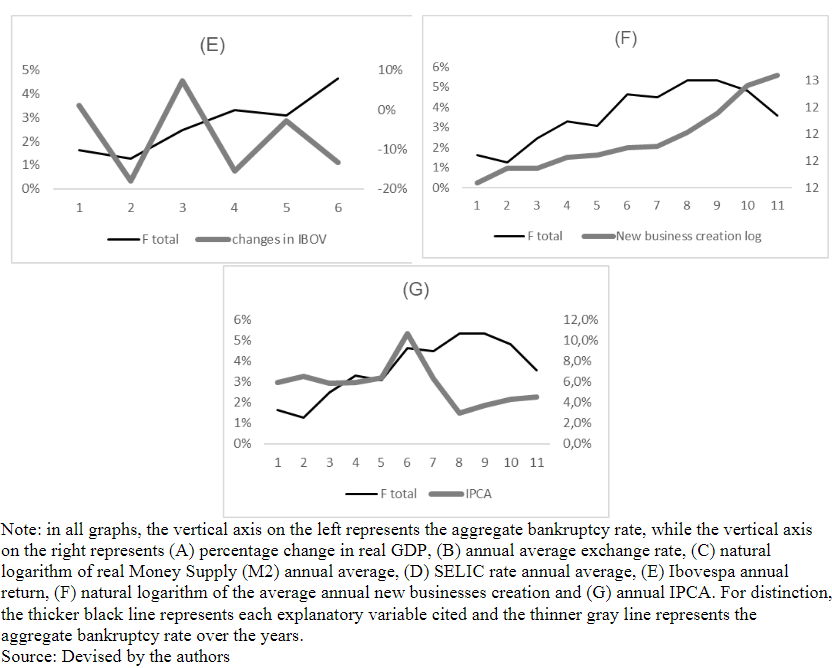

Graph 2 relates each explanatory variable used in the model with the total bankruptcy rate. Bankruptcy rates by size have been aggregated for the sole purpose of making the graph easier to read. The figure indicates a positive relationship between bankruptcies and the explanatory variables in practically all cases, with the exception of the Ibovespa index, which, as mentioned before, is responsible for capturing the expectations of economic agents.

Among all the relations presented, two are noteworthy, as they indicate relations that are contrary to expectations: GDP and M2 Money Supply (charts A and C). However, it is noteworthy that, in 2015, the relationships found graphically for these two variables were within expectations. An explanation for this may lie in the fact that 2015 was a year of strong economic downturn (CAOLI; CURY, 2016), thus adjusting the relationships between the variables.

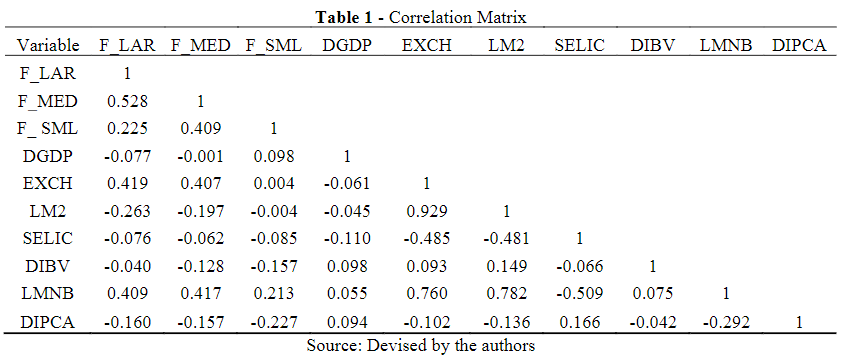

By analyzing the correlation matrix between the variables (Table 1), there is a correlation between the bankruptcies of companies of the 3 sizes, and the bankruptcy of medium-sized companies is moderately correlated with both the bankruptcy of large companies and small-sized ones. The relationship between large and small business bankruptcies is weaker, but it exists. This descriptively indicates that there may be some kind of contagion between bankruptcies of different company sizes, depending on the economic condition of the country. When assessing the relationship between economic variables and bankruptcies, it is possible to note that small companies only present weak or very weak correlations with the variables used in the model, not being so dependent on the economic situation in the aggregate. These correlations corroborate the finding in Graph 1: companies of this size apparently show a different behavior from the other two sizes of companies studied and there seems to be a constant percentage of bankruptcy over time.

4.2 Model adequacy and formulation

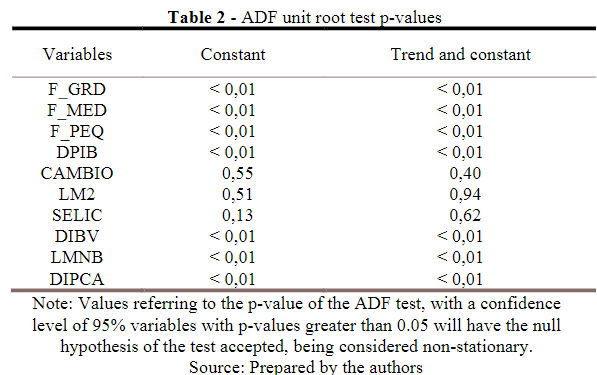

As mentioned earlier, for a temporal data series to be properly modeled, it must be stationary. For this, the Augmented Dickey-Fuller (ADF) test was applied to all variables at the level. As indicated in Table 2, with a 95% confidence level, the variables that are not stationary at the level, and in the test with trend and constant, were EXCH (exchange rate), LM2 and SELIC. These variables will be used in difference. We decided to take the test with trend and constant into account due to the nature of the variables used in the proposed model.

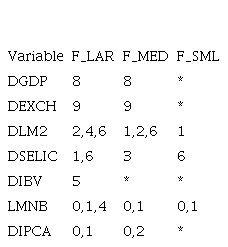

Cross-correlations between the three dependent variables and the seven explanatory variables were also analyzed. For each explanatory variable, the lags in which the cross-correlations with the dependent variables are statistically different from zero and more relevant were considered in the model. As shown in Table 3, the past values of the variables responsible for capturing the health of the economy and companies did not correlate with the lags in the bankruptcy rate of small companies; however, this relationship is relevant for medium and large companies, where correlations were found with both short-term and long-term effects on GDP and the exchange rate.

Regarding liquidity, past values of the variables responsible for capturing this effect proved to be relevant for companies of all sizes, in different ways. For small and medium-sized companies, money supply proved to act more quickly than for large companies. The SELIC rate, on the other hand, presented relevant lags in 6 months for companies of all sizes. Past expectations, measured by the Ibovespa index, in turn, were only relevant for large companies, slowly.

The variable used to measure competition, through the creation of new companies, showed different effects for each company size. Past values showed (i) a rapid influence on the bankruptcy rate of all company sizes, (ii) a medium-term influence for large companies.

Finally, inflation rate only showed irrelevant lags for small businesses. For large and medium-sized companies, inflation has a rapid influence.

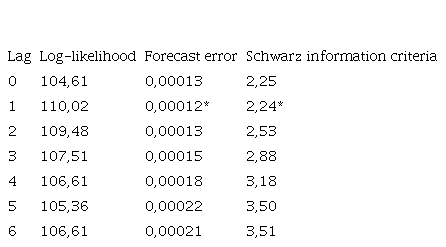

With the variables properly stationary (i.e., considered in their first differences) and the most relevant initial lags for the explanatory variables decided, the ideal number of lags for the dependent variables was analyzed using the Schwarz (SC) information criterion (Table 4). We opted, then, to use the 1-month lag as it is the lowest value of the Schwarz information criterion.

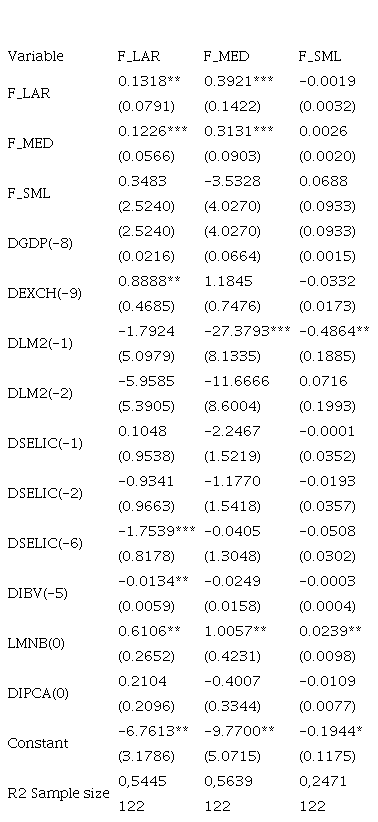

Therefore, with all the information in hand, we estimated a first version of the vector autoregression model (VAR). From this model, the lags of the explanatory variables in which no estimate of the bankruptcy rate, for the 3 company sizes, was relevant with a 10% significance level were removed. With that, we get the final model (section 4.3). Regarding the residual analysis, the homoscedasticity of the errors was not rejected based on the White test (p-value = 0.3268); the normality of the errors was not rejected either based on the Jarque-Bera test (p-value = 0 .7075) and there is no autocorrelation of the errors up to lag 6 based on the LM serial correlation test (p-value = 0.4562). Therefore, the model's assumptions were tested and considered valid with a 5% significance level.

Variations in GDP are relevant for medium and large companies, with a lag of 8 months. This lag is reasonable since, in general, larger companies have greater resilience to turbulent periods in the economy. The sign found matches expectations, exposing a negative relationship between GDP and bankruptcies. That is, in a heated economic scenario, it is assumed that companies' revenues are higher, which reduces the proportion of insolvent companies. For small businesses, on the other hand, a relationship between changes in the bankruptcy rate and the behavior of GDP was not found. The insignificance of the GDP indicates that small companies (and, eventually, new ones) have their own survival dynamics that are independent, to some relevant extent, from the scenario of economic upturn or deceleration. This is an important contribution to the literature that was only possible to verify through the segmentation of companies of different sizes and will be discussed in Section 5.

The exchange rate, in turn, is only relevant for large companies, with a lag of 9 months. Its relationship with the bankruptcy rate is positive, as found by Salman, Fuchs and Zampetti (2015). For small and medium-sized companies, exchange rate changes are not relevant to change bankruptcy rates, perhaps because the size of these companies does not allow a relevant dynamic with exports and imports. Everett and Watson (1998) also found no evidence of the influence of exchange rates on small business bankruptcy rates.

The variables that capture the availability of credit (money supply and the SELIC rate) present different behaviors in the short and medium term. Money supply is only relevant for medium and small companies, and in the short term, whereas the SELIC rate is relevant for large companies and for a period considered medium. The short-term effects are as expected. That is, an increase in the money supply causes a drop in the bankruptcy rate of companies, while an increase in the cost of credit, measured by the SELIC rate, is associated with an increase in the bankruptcy rate. These results are in line with Contador (1985), for the Brazilian case, and with several other international studies such as those of Turner, Coutts and Bowden (1992) and Salman et al. (2105). Cutting credit, by reducing the money supply and/or increasing its cost, generates an increase in the bankruptcy rate of companies.

The Ibovespa index, which captures the expectations of economic agents, is relevant, with a lag of 5 months for changes in the bankruptcy rate of large companies. The sign found is negative for large companies, thus confirming that agents' expectations work as a thermometer for the economy, as found by Altman (1983), Zhang, Bessler and Leatham (2013) and Oliveira (2014).

The creation of new companies is significant for companies of all sizes, without lags. That is, changes in the level of competition generate changes in the bankruptcy rates of these companies at the same time. Such dynamics indicate that the effect of a change in the degree of competition is effectively felt instantly through the increase in business bankruptcies. In any case, the relationship found is positive, as in Altman (1983) and Liu (2009).

Finally, inflation rate was not significant, without lags, for the bankruptcy rate of companies. Inflation, as argued, affects the predictability of future flows (WADHAWANI, 1986) and, given this, it is expected that mainly medium and small companies (because they are not as solid as large ones) would present some kind of relationship between their bankruptcy rate and inflation rate, which was not confirmed in this work.

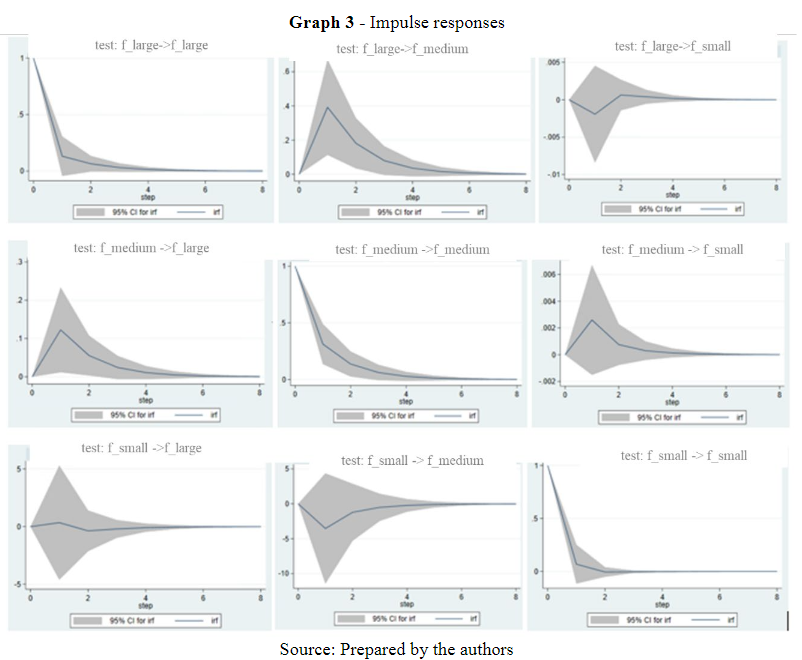

4.4 Analysis of shocks

The models presented in Table 5 allow an analysis of shocks between the endogenous variables which, in this case, are the bankruptcy rates. Through this analysis, it is possible to examine whether shocks in the bankruptcy rate of a certain type of company affect the other types, both in the studied period and in subsequent periods. Graph 3 presents the results found.

Observing the responses to impulses (Graph 3), it appears that small companies are particularly different from the other ones. Shocks in the bankruptcy rate of this type of company do not significantly affect the rates of medium and large companies in future periods. On the other hand, shocks to the bankruptcy rate of large firms do not have a significant effect on future changes in the bankruptcy rate of small firms. This apparent “detachment” from smaller companies may be linked to a specific dynamic. Highly linked to entrepreneurship, small companies have a high turnover both regarding the creation of new companies and bankruptcy petitions. Individuals are always willing to do business as entrepreneurs whether in favorable moments with the desire to see their venture bear fruit (opportunity entrepreneurship) or in recessive moments, where entrepreneurship becomes an alternative for extra income or even unemployment (necessity entrepreneurship) (ROLDÃO; MONTE-MOR; TARDIN, 2018).

Large companies, as well as others, showed the greatest response to a shock of bankruptcy of themselves. Shocks in the bankruptcy rate of medium-sized companies are also relevant, but with a lesser intensity and with a certain slowness to affect large companies (2 months). This delay may be linked to the fact that large companies take longer to feel the effect of crises, as they have more significant revenues, which guarantees them a greater safety margin. Therefore, large companies can use the bankruptcy rate of medium companies as a thermometer for future scenarios: a bankruptcy movement of medium-sized companies today can indicate troubled periods 2 months ahead.

5 CONCLUSION

Understanding the dynamics between macroeconomic variables and business bankruptcy is important both from the point of view of public policy makers and from that of businessmen and entrepreneurs. The analysis carried out in this study, based on the years 2010 to 2015, points to two general conclusions. On the one hand, for medium and large companies, it is concluded that measures that promote better economic health with GDP growth and low exchange rates contribute to a better prospect of companies' success. Small firms, on the other hand, are a different case. Its bankruptcy rate does not have any synergy with the other company sizes, suggesting some kind of dynamic of its own, a fact that is an important contribution to the literature, which was only possible to verify through the segmentation of companies of different sizes.Furthermore, these companies indicate that a favorable macroeconomic scenario is no guarantee of success, as periods of abundant credit and positive expectations presented results that were different from what was expected. In short, the bankruptcy of Brazilian companies only depends on macroeconomic factors after the firm has overcome a size barrier, perhaps managing to occupy a more specific space in the market. Understanding this dynamic more deeply is a question of future research that naturally presents itself.

With regard to managerial implications, this study finds evidence that a firm's growth exposes its performance to greater influence from the economic environment. Specifically, larger companies are more subject to the effects of negative environmental contingencies. This reinforces the importance that managers establish crisis management mechanisms. Such mechanisms, of course, must focus on the organization's ability to respond quickly to changes in macroeconomic variables. This would be the basis of the firm's resilience built through productive organizational routines. Regarding smaller companies, the results are in line with the literature that indicates a natural rate of bankruptcy, indicating that a portion of small entrepreneurs tends to fail, regardless of external conditions. Hence the importance that these firms seek bettertraining (for example, through entities that support entrepreneurship).

The results found in this work bear criticism. Future studies may benefit from a larger (i.e., more extensive) database. For future work, a deeper analysis between the variables used in the model is also suggested, since a total independence was assumed between the macroeconomic variables and the bankruptcy rates for the three sizes of companies, and this relationship may not be purely exogenous. Finally, a more robust study considering companies' endogenous and exogenous risks, using the vector autoregression methodology, can present very interesting results, as these two types of bankruptcy risk for companies are probably related and not independent from each other.

References

ALAMINOS, D.; DEL CASTILLO, A.; FERNÁNDEZ, M. Á. A global model for bankruptcy prediction. PloS ONE, v. 11, n. 11, 2016.

ALMAMY, J.; ASTON, J.; NGWA, L. N. An evaluation of Altman's Z-score using cash flow ratio to predict corporate failure amid the recent financial crisis: Evidence from the UK. Journal of Corporate Finance, v. 36, p. 278-285, 2016.

ALTMAN, Edward I. Why businesses fail.Journal of Business Strategy, v. 3, n. 4, p. 15-21, 1983.

CAOLI, Cristiane; CURY Anay. PIB do Brasil cai 3,8% em 2015 e tem pior resultado em 25 anos. G1 - Globo Notícias,03 mar. 2016. Disponível em: http://g1.globo.com/economia/noticia/2016/03/pib-do-brasil-cai-38-em-2015.html. Acesso em: 21 set. 2017

CONTADOR, Cláudio R. Insolvência de empresas e política macroeconómica.Revista de Administração da Universidade de São Paulo, v. 20, n. 2, 1985.

EVERETT, Jim; WATSON, John. Small business failure and external risk factors.Small Business Economics, v. 11, n. 4, p. 371-390, 1998.

GARCIA, Ana Carolina. Condicionantes macroeconômicos para a falência de micro e pequenas empresas no Brasil (2006 A 2017). Trabalho de Conclusão de Curso (Graduação em Ciências Econômicas) – Universidade Federal de Uberlândia, Uberlândia, 2018.

HARADA, Nobuyuki; KAGEYAMA, Noriyuki. Bankruptcy dynamics in Japan.Japan and the World Economy, v. 23, n. 2, p. 119-128, 2011.

ACQUES, K.A.S; BORGES, S.R.P.; MIRANDA, G.J. Relações entre os indicadores econômico-financeiros e as variáveis macroeconômicas dos segmentos empresariais da b3. Revista de Administração, Contabilidade e Economia da Fundace, Ribeirão Preto, v. 11, n. 1, p. 40-59, 2020.

JOVANOVIC, Boyan. Selection and the Evolution of Industry. Econometrica: Journal of the Econometric Society, p. 649-670, 1982.

LANG, Larry HP; STULZ, RenéM. Contagion and competitive intra-industry effects of bankruptcy announcements: An empirical analysis. Journal of financial economics, v. 32, n. 1, p. 45-60, 1992.

LIBERMAN, M.; BARBOSA, K.; PIRES, J. Falência bancária e capital regulatório: Evidência para o Brasil. Revista Brasileira de Economia, v. 72, n. 1, p. 80-116, 2018.

LIU, Jia. Macroeconomic determinants of corporate failures: evidence from the UK. Applied Economics, v. 36, n. 9, p. 939-945, 2004.

LIU, Jia. Business failures and macroeconomic factors in the UK.Bulletin of economic research, v. 61, n. 1, p. 47-72, 2009.

MARIO, P. C.; CARVALHO, L. N. Ensaio Sobre A Insolvência, Indicadores de Balanços e o Relacionamento com Variáveis Macroeconômicas Estudo Exploratório. In: X Congreso Internacional de Costos. 2007.

NETO, E.C.M; CARDOSO, H.M.S; PENA, H.W.A. Uma análise política do governo temer sob a perspectiva neoliberal e a teoria crítica de Noam Chomsky. Caribeña de Ciencias Sociales, 2019.

OLIVEIRA, Marco Paulo Gonçalves. A insolvência empresarial na indústria transformadora portuguesa: as determinantes financeiras e macroeconómicas. 2014.

PERRIN, Fernanda; Vettorazzo, Lucas. Setor de maior peso no PIB, serviços caem com menor consumo de famílias. Folha de São Paulo, 07 mar. 2017. Disponível em: http://www1.folha.uol.com.br/mercado/2017/03/1864276-setor-de-maior-peso-no-pib-servicos-caem-com-menor-consumo-de-familias.shtml. Acesso em: 07 set. 2017.

PLATT, Harlan D.; PLATT, Marjorie B. Business cycle effects on state corporatefailure rates. Journal of Economics and Business, v. 46, n. 2, p. 113-127, 1994.

ROLDÃO, Tarciane; MONTE-MOR, Danilo Soares; TARDIN, Neyla. A influência da recessão econômica na intenção de empreender: uma análise cross-country baseada na crise do subprime. Organizações & Sociedade, v. 25, n. 85, p. 320-338, 2018.

SALMAN, A. Khalik; VON FRIEDRICHS, Yvonne; SHUKUR, Ghazi. The determinants of failure of small manufacturing firms: Assessing the macroeconomic factors.International Business Research, v. 4, n. 3, p. 22, 2011.

SALMAN, A. Khalik; FUCHS, Matthias; ZAMPATTI, Davide. Assessing risk factors of business failure in manufactoring sector: a count data approach from Sweden.International Journal of Economics, Commerce and Management, v. 3, n. 9, p. 42-62, 2015.

SANVICENTE, A. Z.; MINARDI, A. M. A. F. Identificação de indicadores contábeis significativos para a previsão de concordata de empresas. Manuscrito não publicado, Instituto Brasileiro de Mercado de Capitais, São Paulo, SP, 1998.

SERASA EXPERIAN. Disponível em: http://noticias.serasaexperian.com.br/indicadores-economicos. Acesso em 10 jun. 2021.

SIDRA, IBGE. Disponível em: https://sidra.ibge.gov.br/pesquisa/cempre/quadros/brasil/2015. Acesso em 17 set. 2017.

TURNER, Paul; COUTTS, Andrew; BOWDEN, Sue. The effect of the Thatcher government on company liquidations: an econometric study. Applied Economics, v. 24, n. 8, p. 935-943, 1992.

WADHWANI, Sushil B. Inflation, bankruptcy, default premia and the stock market. The Economic Journal, v. 96, n. 381, p. 120-138, 1986.

ZHANG, Jin; BESSLER, David A.; LEATHAM, David J. Aggregate business failures and macroeconomic conditions: a var look at the US between 1980 and 2004. Journal of Applied Economics, v. 16, n. 1, p. 179-202, 2013.