ARTICLES

CORPORATE OWNERSHIP NETWORK: THE HIERARCHICAL CAPITALISM IN THE BRAZILIAN CONTEXT

RED DE PROPIEDAD CORPORATIVA: EL CAPITALISMO JERÁRQUICO EN EL CONTEXTO BRASILEÑO

REDE DE PROPRIEDADE CORPORATIVA: CAPITALISMO HIERÁRQUICO NO CONTEXTO BRASILEIRO

Mário Sacomano msacomano@ufscar.br

Evandro Marcos Saidel Ribeiro esaidel@usp.br

Mário Sacomano msacomano@ufscar.br

Evandro Marcos Saidel Ribeiro esaidel@usp.br

CORPORATE OWNERSHIP NETWORK: THE HIERARCHICAL CAPITALISM IN THE BRAZILIAN CONTEXT

Revista de Administração de Empresas, vol. 63, no. 2, pp. 1-25, 2023

Fundação Getulio Vargas, Escola de Administração de Empresas de S.Paulo

Received: 17 November 2021

Accepted: 26 July 2022

ABSTRACT: Several studies have indicated a type of hierarchical capitalism in Latin America, characterized by the presence of multinational and state corporations, diversified multi-enterprise groups, low-skilled labor, and segmented labor markets. From the perspective of ownership networks, we explore who the owners of large Brazilian corporations are. These networks reveal actors and groups with prominent positions in the structure and ownership of companies. Thus, this article proposes to 1) describe the ownership network of the largest Brazilian corporations; 2) analyze the density, average degree, modularity, and the number of components connected in this network; 3) analyze measures of weighted degree centrality, intermediation, and eigenvector; 4) identify and analyze subgroups in the network, and 5) relate the configuration of the ownership network with hierarchical capitalism in the Brazilian context. The results point to prominent positions of financial shareholders, the Brazilian state (state-owned firms), and groups composed mostly of large multinationals, financial firms, families, and state-owned firms, confirming that the ownership structure is strongly linked to these players.

Keywords: Corporate control, ownership networks, network analysis, financialization, brazilian corporations.

RESUMEN: Varios estudios han señalado un tipo de capitalismo jerárquico en América Latina, caracterizado por la presencia de corporaciones multinacionales y estatales, grupos multiempresariales diversificados, mano de obra poco cualificada y mercados laborales segmentados Desde la perspectiva de las redes de propiedad, exploramos quiénes son los dueños de las grandes corporaciones brasileñas. Estas redes revelan actores y grupos con posiciones destacadas en la estructura y propiedad de las empresas. Así, este artículo se propone: 1) describir la red propietaria de las mayores corporaciones brasileñas; 2) analizar la densidad, el grado medio, la modularidad y el número de componentes conectados en esta red; 3) analizar medidas de grado ponderado de centralidad, intermediación y vector propio; 4) identificar y analizar subgrupos en la red y 5) relacionar la configuración de la red propietaria con capitalismo jerárquico en el contexto brasileño. Los resultados apuntan a posiciones destacadas de accionistas financieros, del Estado brasileño (empresas de propiedad estatal) y de grupos compuestos mayoritariamente por grandes multinacionales, empresas financieras, familias y empresas de propiedad estatal, lo que confirma que la estructura de propiedad está fuertemente vinculada a esos actores.

Palabras Clave: Control corporativo, redes de propiedad, análisis de redes, financiarización, corporaciones brasileñas.

RESUMO: Vários estudos têm apontado para um tipo de capitalismo hierárquico na América Latina, caracterizado pela presença de corporações multinacionais, estatais, grupos multiempresariais diversificados, baixa qualificação da mão de obra e mercados de trabalho segmentados. A partir da perspectiva das redes proprietárias – que revelam atores e grupos com posições proeminentes na estrutura e propriedade das empresas – exploramos quem são os donos das grandes corporações brasileiras. Assim, este artigo propõe: 1) descrever a rede proprietária das maiores corporações brasileiras; 2) analisar a densidade, o grau médio, a modularidade e o número de componentes conectados nessa rede; 3) analisar medidas de centralidade de grau ponderado, intermediação e autovetor; 4) identificar e analisar subgrupos na rede e 5) relacionar a configuração da rede proprietária com o capitalismo hierárquico no contexto brasileiro. Os resultados indicam que acionistas financeiros, o Estado brasileiro (por meio de empresas estatais) e grupos compostos majoritariamente por grandes multinacionais, empresas financeiras, famílias e empresas estatais estão em posições proeminentes, confirmando que a estrutura de propriedade está fortemente atrelada a esses atores.

Palavras Chave: Controle corporativo, redes proprietárias, análise de redes, financeirização, corporações brasileiras.

INTRODUCTION

The control of the largest corporations is a multidisciplinary topic that has been studied for decades (Berle & Means, 1932; Fichtner, Heemskerk, & Garcia-Bernardo, 2017; Fligstein, 1990; Jensen & Meckling, 1976), ownership being one of the ways of corporate control. The type of shareholders strongly impacts corporate performance and strategies. Financial control, for example, is often characterized by high profitability and the concept of maximization of shareholder value (Fligstein & Brantley, 1992; Wahl, 2006).

The initial studies by Vitali, Glattfelder, and Battiston (2011) and Glattfelder and Battiston (2019) encouraged us to explore this network structure in the Brazilian economy. In the study by Vitali et al. (2011), the network analysis is presented as an alternative way to quantify the global corporate control network. The authors identified the existence of a strongly connected core in which every member owns shares in every other member. Therefore, the total network control flows largely through this core. Nearly 40% of the control over the largest world corporations’ economic value is held by a small group of shareholders (less than 0.02% of the total network control’s shareholders are part of this core).

Considering global corporate ownership over time, Glattfelder and Battiston (2019) suggest that a global economic shock negatively affects many individuals but can only have a marginal impact on the existing power structures. The authors also state that power remains extremely concentrated in the hands of a few individuals and organizations. According to their results, less than 0.0009% of the actors in the global ownership network have the potential to influence slightly more than one-sixth of the operating revenue of firms worldwide.

Furthermore, the concept of ownership networks allows us to understand who controls assets, shares, and strategic decisions within the organizations (Kogut & Walker, 2001). The analysis of these networks reveals actors with central and prominent positions to access resources and information (Bahamonde, Bollen, Eelejalde, Ferres, & Poblete, 2018; Corrado & Zollo, 2006; Vitali et al., 2011). Ownership networks also help us to comprehend the markets since the economic power and corporate control are reflected by ownership links (Glattfelder, 2010).

According to Carvalho and Vidotto (2007), after the mid-1990s, there was an expansion of foreign capital in the Brazilian banking and infrastructure sectors (Campos, 2018). Bruno and Caffe (2017) reported that the growth of the financial flow in the Brazilian economy occurred mainly in the 1990s. In the intra-corporate context, studies such as those developed by Miranda, Crocco, and Santos (2017) and Moraes (2017) converge when identifying business practices aligned with the financial logic and the maximization of shareholder value in the national corporate context. In the study of Bonizzi, Kaltenbrunner, and Powell (2020), emerging market economies are presented as subordinated to global financialized capitalism. Kaltenbrunner and Painceira (2018) also indicate this financialization process in the Brazilian context, where financial transformations are fundamentally shaped by their subordinated integration into a financialized and structured world economy.

The Brazilian corporate context has been characterized by an increasing presence of financial institutions, especially large banks and investment funds, in the shareholders' structures. More specifically, the largest corporations are facing the strong presence of state and local firms in key economic sectors (Coutinho & Belluzzo, 1998; Lazzarini, 2011; Moreira & Puga, 2000; Plihon, 2005). The existence of large multinationals of different business sectors and possible groups with high centrality measures and high control values in the network are also factors that are expected in the analysis of ownership network in the Brazilian context (Carvalho, 2018; Schneider, 2009; Vitali et al., 2011).

From the widespread formulation of the VoC (varieties of capitalism) framework developed by Peter A. Hall and David Soskice (2001), Schneider (2009) identifies particular characteristics that differentiate Latin American countries from liberal market economies and coordinated market economies (Hall & Soskice, 2001; Miller, 2010; Schneider, 2009). Schneider (2009) suggests that Latin America has a long and distinct form of hierarchical capitalism characterized by the presence of multinational corporations, the state, multi-business diversified groups, low qualification of workforce, and segmented labor markets. Additionally, the control of large corporations is associated with large groups of multinationals, financial shareholders, the state, and families (Cárdenas, 2016; Schneider, 2009; Wolff, 2016). Our main proposition is that the hierarchical capitalism argument distinguishes the Brazilian economy. Multinational corporations, state, and multi-business diversified groups have a significant prominent position in network ownership. Some studies have explored the networks in the Brazilian corporate context, such as those developed by Carvalho (2018) and Lazzarini (2011). However, there is a lack of studies using ownership network to analyze the corporate control of the largest corporations in Brazil. Moreover, herein we measure the degree of proprietary concentration of these large groups, as proposed by Vitali et al. (2011). Thus, the main research questions are:

-

Who are the owners of the largest corporations in Brazil?

-

Does the Brazilian corporate context exhibit this hierarchical capitalism configuration appointed by Schneider (2009)?

-

Is the corporate control of the largest corporations associated with large groups of multinationals, financial shareholders, the state, and families?

Answering these questions permits a deep understanding of the domain of foreign capital in the Brazilian economy and the strong presence of financial institutions in the ownership structures of the largest national corporations. This paper then proposes:

- 1. to describe the ownership network of the largest corporations in Brazil;

- 2. to analyze the density, average degree, modularity, and the number of connected components;

- 3. to analyze the weighted-degree centrality, betweenness centrality, and eigenvector centrality for all individuals in the network;

- 4. to identify and analyze subgroups in the network; and finally

- 5. to relate the ownership network configuration to the hierarchical capitalism in the Brazilian context.

The results show that financial shareholders and actors related to the Brazilian state hold prominent and central positions in the network structure. Community detection reveals the existence of groups mostly composed of large multinationals, financial firms, families, and firms linked to the Brazilian state. These communities also have the highest values of control flow. The prominent positions of financial actors in the network indicate a possible financialization process of the corporate control of the largest corporations in Brazil. Therefore, the results reveal the significant presence of the state, large family companies, and multinationals in the network structure. The next section will explore important theoretical fundamentals for the development of this research.

THEORETICAL FRAMEWORK

In this section, the theoretical framework will be discussed considering the corporate control, networks, financialization process, and hierarchical capitalism in the Brazilian context.

Corporate control and networks

From the “embeddedness” concept, Granovetter (mainly in his paper entitled "Economic action and social structure") claims the use of network analysis in economic sociology (Swedberg, 2004). From this approach, the task of economic sociology is to describe how economic actions are structured through networks (Swedberg, 2004). The analysis of social networks starts from a structural conception, where imbricated action networks socially constitute the market. Moreover, since the 1970s, network analysis has also been applied to the study of relations among organizations (Hafner-Burton, Kahler, & Montgomery, 2009; Murdie, 2014; Scott, 2004). Among recent studies on this topic, we can cite the work by Uzzi, Amaral, and Tsochas (2007), Oberg, Korff, and Powell (2017), and Fu and Cooper (2020). The concept of ownership corporate network is supported by this perspective, as reported by Vitali et al. (2011) and Wilson, Buchnea, and Tilba (2018).

Ownership is one of the ways through which corporate control is exercised (Gill, Vijay, & Jha, 2009). The ownership structure is the corporation’s patrimony distribution in terms of votes, capital, and identity of shareholders. There are different types of shareholders - institutional, internal and “blockholder” shareholders, families, business groups, and governments (Boyd & Solarino, 2016) - and their nature strongly influences and impacts corporations’ strategy and performance. For example, control by shareholders of the financial type often leads to actions and results to guarantee high profitability and maximization of shareholder value. The control by this type of shareholder is also associated with low sales growth (Fligstein & Brantley, 1992; Wahl, 2006).

Studies developed by Sacomano, Carmo, Ribeiro, and Cruz (2020), Fichtner et al. (2017), and Ireland (2012) show the domain and influence of financial institutions on large corporations’ ownership structure. According to Vitali et al. (2011), ownership networks are structures that represent ownership links between shareholders and corporations, justifying why studies on ownership networks are relevant to corporate governance. They analyze this network based on topological properties, such as the number of two-length paths indicating mutual cross-shareholding. In the large connected component, there is a large and strong connected group, where each one of its members is the shareholder of each one of the other members.

Vitali et al. (2011) also discuss network control concentration. Considering the economic value of the ownership participations, the authors state that the control flows to a connected strong little core of corporations, whose nature is mostly financial. The results show that just 0.61% of the top shareholders accumulate 80% of the control over the value of all firms in the network. In the study by Jeude, Aste, and Caldarelli (2019) conducted in February 2018, it is possible to note that the multiplex network of German and British corporations represent different types of corporate control relations: R&D alliances, board interlocking, ownership links, and mutual cross-shareholder. Among the results found by the authors is the relationship between corporate performance and the centrality of these firms in the multiplex network. It is worth mentioning that the layers of this network present a non-trivial overlap.

Sacomano et al. (2020) studied the ownership network of the global automobile sector and financial institutions, mainly passive investment funds such as Black Rock, Vanguard Group, and State Street, which were shown to have the highest centrality measures. The findings pointed to a financialization process of corporate control in the automobile industry and may explain the shareholder-value orientation in this companies’ corporate control. The detection of communities indicated that corporate ownership is strongly influenced by geographic, historical, and ethical ties.

Ownership networks allow us to understand who has the capital, who owns it, and who controls the economic assets (Glattfelder, 2010). In this study, we analyze the ownership links in the Brazilian corporate context. To this end, we performed the corporate network analysis, which proved to be a great tool for studying the ownership network of the largest corporations in Brazil.

Financialization and hierarchical capitalism

A key concern of the varieties of capitalism (VoC) approach is the topic of corporate governance (Hall & Soskice, 2001; Lazonick, 2010; Vitols, 2001). Through the VoC framework, it is possible to study links between external investors and other actors relevant to the firm, focusing on the integration and complementarities of different institution members of a capitalist regime (Hall & Soskice, 2001; Vitols, 2001). Among the studies that use the VoC approach, we can cite those conducted by Vitols (2001), who analyzed the varieties of corporate governance in Germany and the UK, and Lazonick (2010), who addressed the financialization of corporate decision-making in US corporations.

The US stands out regarding the VoC since the country has a more liberal and market-based capitalist regime (Bizberg, 2014; Hall & Soskice, 2001). In contrast, other countries (Germany, for example) have a regime based on social actors. In countries such as Japan and Korea, banks and industries operate in a regime based on the economy. In France, the regime is based on the state (Hall & Soskice, 2001; Bizberg, 2014; Boyer, 2005). In Latin America, societies are heterogeneous and hierarchic, as suggested by Schneider and Soskice (2009) and Bizberg (2014).

Capitalism in Latin America is hierarchically distinguished by four dimensions that structure business access to essential inputs of capital, technology, and labor: diversified business groups, multinational corporations, low-skilled labor, and atomistic labor (Schneider, 2009). The author investigates how an institution’s existence or strength (large business groups, for example) affects another dimension, such as labor markets. According to the author, the relations in a hierarchical market economy become even more clearly hierarchical because most firms are directly controlled and managed by their owners - either prominent families or foreign firms. Schneider (2009) suggests that inter-firm relations are sometimes competitive: while some sectors are oligopolistic, others are regulated by the state. In this paper, we explore how corporate financial control is continually influencing the Brazilian market dynamics. Considering the facts pointed out by Schneider (2009), we suggest proposition 1.

-

Proposition 1: From the corporate control perspective, Brazilian corporate ownership exhibits evidence of hierarchical capitalism.

Other recent studies suggest that emerging market economies are subordinated to global, financialized capitalism (Bonizzi et al., 2020; Kaltenbrunner & Painceira, 2018). In this sense, financialization is a multidimensional process that impacts society, economy, and business (Zwan, 2014). In a simpler conception, Lira (2008) defines financialization as a macroeconomic phenomenon characterized by the appropriation of economic assets by the financial market. Financialization in an internal corporative context can change the management process and the strategies of firms from “holding and investing” to “downsizing and distributing.” Thus, the maximization of shareholder value is considered the principle of corporate governance (Lazonick & O'Sullivan, 2000; Miranda et al., 2017). According to Krippner (2005) and Epstein (2005), this phenomenon is a new accumulation pattern, where profit comes more from financial channels and less from production and services.

About emerging market economies, Bonizzi et al. (2020) investigate the financialization phenomena from global structural transformations through the internationalization of the circuits of capital within the last half-century. According to Bonizzi et al. (2020), this internationalization is marked by the US-dollar market-based finance and characterized by the institutionalization of wealth, the transformation of banking, the proliferation of new financial instruments, and an increased governance role for finance. Thus, this configuration altered the geographic transfer of value from subordinate regions and actors to superordinate ones, reinforcing the subordinate role of emerging market economies in the extraction, realization, and transfer of value and constraining the agency of both public and private actors from subordinate regions (Bonizzi et al., 2020).

Brazil has the twelfth economy in the world and the largest in Latin America, with a nominal GDP of USD 1.444 trillion (WorldBank, 2021). Its shares in world total exports and total imports are 1.19% and 0.93%, respectively, which places the country among the 30 largest importers and exporters in the world (World Trade Organization [WTO], 2020). The Asian economies are characterized by their great economic dynamism, while Brazil and South Africa are often linked to uncertain economies (Fleury & Fleury, 2006). Still, regarding Brazil, Taylor (2020) argues that developmentalism has endured based on the notion of ‘institutional complementarities’ since firms and politicians have developed strategies that are ‘individually first-best, but collectively suboptimal’ (Taylor, 2020).

Kaltenbrunner and Painceira (2018) observed the Brazilian economic context and reported that recent changes in the relationship between financial practices and economic actors are shaped by their integration into and subordination to the world economy. The analysis of two processes supports these findings. The first is the reserve accumulation and the financialization of banks and households. The second is the continued external vulnerability in emerging market economies (Bin, 2016; Coutinho & Belluzzo, 1998; Panceira, 2011).

In the Brazilian economic context, mainly from the 1990s, there has been a process of commercial and financial liberalization and growth of financial flow, bringing uncertainty and fragility to the economy. In their study on Brazilian open capital corporations considering the period from 1995 to 2008, Miranda et al. (2017) reported that these corporations used financial practices, especially indebtedness, to generate wealth for the shareholder (maximization of shareholder value), focusing on short-term results. By analyzing the financialization process of Embraer, Moraes (2017) identified the domain of the fictitious form under the real and productive form. The author observed an advance in the use of financial instruments, such as shares, debt securities, bank papers, and derivation, and the presence of investment funds as main shareholders. This recent study (Kaltenbrunner & Painceira, 2018) showed some evidence of how corporative ownership in the Brazilian economy is associated with financial logic (Bruno, Diawara, Araújo, Reis, & Rubens, 2011; Miranda, Crocco, & Santos, 2009; Miranda et al., 2017). Regarding the financialization process, we suggest proposition 2:

-

Proposition 2: The corporate ownership of the largest corporations is highly centralized and intermediated by financial institutions.

Therefore, this study seeks to contribute to analyzing the ownership structure of large Brazilian corporations. According to Schneider (2009), Latin American capitalism is hierarchical and has four large dimensions. This analysis facilitates the incorporation of factors such as the state and transnational corporations, which are strongly present in the developing countries. The ownership network with the prominent and central presence of large corporations and the state converges with the economic configuration defended by Schneider (2009).

RESEARCH METHOD

From a methodological point of view, this research is exploratory, qualitative, and uses content and document analysis to describe ownership networks (Collins & Hussey, 2005). The data sources were collected from Orbis Database and Market Screener (MarketScreener, 2020; Orbis, 2020). The “Valor1000” ranking produced in 2019 by the Brazilian newspaper Valor Econômico was used as a reference to obtain the sample of corporations (Valor1000, 2019). The 122 corporations selected from this ranking operate in 22 different business sectors. This sample represented nearly 42% of Brazil’s GDP in 2020 and was selected to represent the Brazilian economy. We selected at least four corporations for each of these sectors, and the selection was ordered according to the annual net revenue.

The following information about each corporation was obtained to characterize the sample: economic value (for banks, the annual net profit; for other corporations, the annual net revenue), country of origin, and business sector. This information was extracted from the “Valor1000” ranking (Valor 1000, 2019). The companies’ ownership was obtained from the data sources Orbis and Market Screener (MarketScreener, 2020; Orbis, 2020): 90 ownership structures from files in the “.xls” format and 32 ownership structures from HTML online pages, respectively. In both cases, the extraction was automatized by Python scripts. For both data sources, “.csv” files (“comma-separated values”) containing information on shareholders were generated for each corporation.

A network is a set of nodes and links among these nodes. According to Vitali et al. (2011), the nodes are actors (corporations or people), and the links are control relations among these actors. For the authors, ownership links have a control measure that involves ownership participation and firms’ economic value. The control measure used in this research was defined as , where is the ownership participation of the actor i in the actor j, and is the economic value of corporation j.

The network generating process was also automatized by Python scripts. From the “.csv” files of the 122 ownership compositions, two “.csv” files were generated for the nodes and links. An identifying number, label, and type (banks, funds, people etc.) were attributed to each node. The links were related to the source, target, and weight attributes. Before the final network, a data cleaning process was performed in the nodes and edges, which was automatized by Python scripts using configuration files. In the nodes file, switches of large labels and the union of nodes with the same label were made. In the edges file, the weights of the links were updated with the control measure defined above.

Network analysis can be performed on the actors, relationships, or the entire network structure (Sacomano et al., 2020; Wasserman & Faust, 1994). Herein, we considered network-level measures, node-level measures, community detection, and control flow. The obtained network-level quantities were the average degree, modularity, density, and the number of connected components.

In the non-directed network, the node degree is the number of links connected to this node. For this case, the average degree c of a network with n nodes and m edges is . For the directed network, there are in-degree and out-degree measures. For a network with n nodes and m edges, the average in-degree and average out-degree is (Newman, 2010). The density measure is the proportion of edges present in the network regarding the maximum total number of edges. Modularity measures the network division force in modules. The connected component is a set where all nodes are connected.

The node-level measures considered were “weighted-degree centrality,” “betweenness centrality,” and “eigenvector centrality.” Centrality measures indicate influence, power, and groups (Sacomano et al., 2020). The “weighted-degree centrality” measures the nodes that are more central and important in the network (Newman, 2010). The “betweenness centrality” measures how much a node is in the path among other nodes, while the “eigenvector centrality” measures how much a node is connected with other nodes of the network (Newman, 2010).

The community detection tasks aim to identify sets of nodes that are more densely connected with other nodes of this set and less densely connected with other nodes out of this set (Vitali & Battiston, 2014). The communities can have prominent structural positions and facilitate access to resources, power, and information (Borgatti, Everett, & Johnson, 2013; Newman, 2010; Sacomano et al., 2020). We used Gephi software to calculate all measures (Bastian, Heymann, & Jacomy, 2009). This software uses the modularity optimization-based algorithm described by Blondel, Guillaume, Lambiotte, and Lefebvre (2008) for community detection tasks.

RESULTS

In this section, we present the results of the ownership network analysis in four sections: sample description, network-level measures, node-level measures, and communities.

Sample description

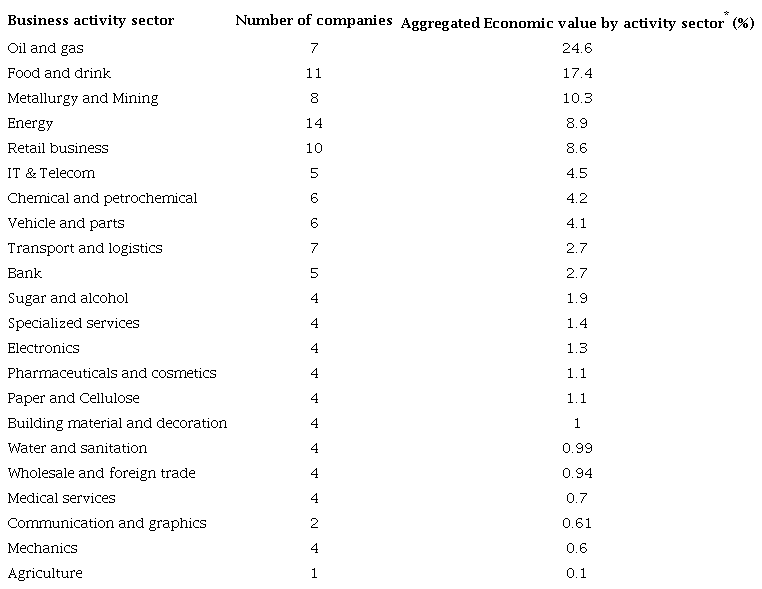

The sample is comprised of 122 corporations. The business sectors with the most companies in the sample are energy, foods and drinks, retail business, metallurgy and mining, transport and logistics, and oil and gas (Table 1). Most of the corporations evaluated are Brazilian (67%), followed by American (7.4%) and European (19.67%) companies.

* Annual liquid profits for banks. Annual liquid revenues for the other sectors

Regarding economic value, firms from the oil and gas (24.6%) and food and drink (17.4%) sectors stand out. Petrobras, which presents the highest value of annual net revenue (and almost twice the annual net revenue of JBS, the company that comes in second place), evidences the strength of the oil and gas sector in the Brazilian economy. The presence of other companies operating in the oil and gas industry among the six first corporations in this list (such as Raizen, Ultrapar, and Braskem) reinforces the sector’s strength.

The oil and gas sector has seven companies in the sample and represents 24.6% of the annual net revenue, while the food and drink sector represents 17.4% even though it counts eleven companies. The energy sector has 8.9% of the annual net revenue and is listed after the metallurgy and mining industry with 10.3% of the sample’s annual net revenue (although the last counts six corporations less than the former). For banks, the research considered the annual net profits. They were listed as the sixth highest aggregated economic value.

Network-level measures

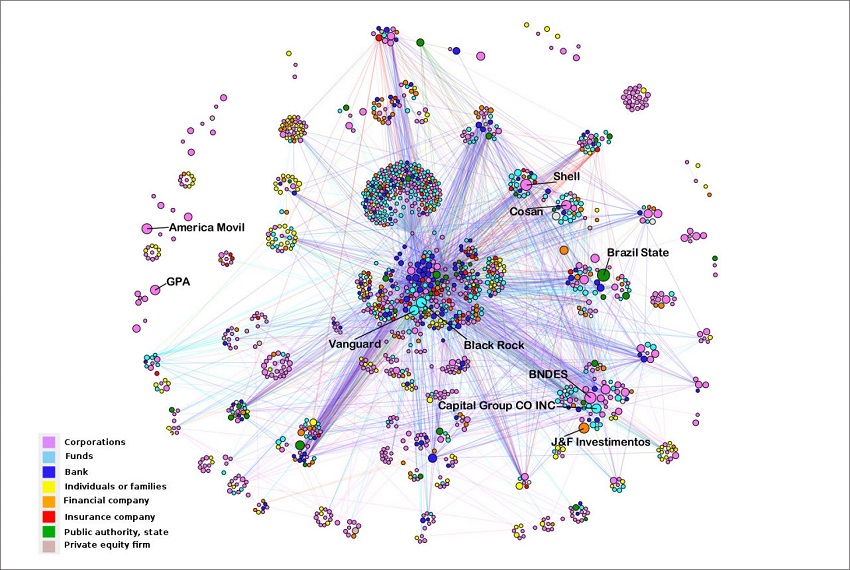

The network constructed from the sample had 1397 nodes and 3253 edges, as shown in Figure 1.

Figure 1

The corporate ownership network of the largest corporations in Brazil*

*The node sizes are proportional to their weighted out-degree measures. The colors of nodes represent the types of these nodesSource: Elaborated by the author.

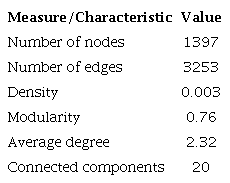

Table 2 shows the network-level measures.

The ownership network exhibits a low-density value. It is sparse and presents low cohesion between the nodes. The cohesion indicates the connectivity - density (number of ties in the network, expressed as a proportion of the possible number) the simplest measure of cohesion in the network analysis (Borgatti et al., 2013). Additionally, it is a highly modularized network, i.e., it has a high number of subgroups (or communities) of nodes with a high connection between each other.

A connected component is the maximal set of nodes in which every node can reach the others by some path (Borgatti et al., 2013). In this study, twenty connected components were considered. However, a large component has 92% of the network nodes, suggesting that this node-set is connected. Despite the low-density value, this large component can be explained by the presence of “hub” nodes with high centrality measures and shareholders in dozens of firms, for example, large passive investment funds (Black Rock, Vanguard, and Dimensional). The average degree is low compared to that of these “hub” nodes.

Regarding the global structure, the network is sparse and has low global density. However, a large connected component is explained by the presence of “hub” nodes, i.e., nodes with high centrality measures and unique options of paths among many nodes in the network.

Node-level measures

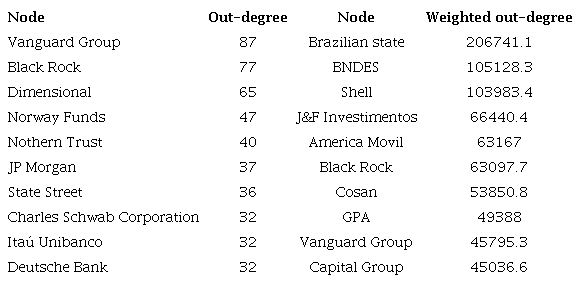

In this study, two measures of degree centrality were considered: out-degree and weighted out-degree centralities. Table 3 shows the ten highest values, which come from financial corporations. For the out-degree measure, passive investment funds such as Black Rock, Vanguard Group, and Dimensional have the highest values. This measure, however, does not consider the economic value of the ownership relation and only indicates the corporations often present in the ownership structures.

On the other hand, in weighted out-degree measures, the economic value of the ownership links is considered. The Brazilian government and the corporations linked to the government (such as BNDES) have the highest values of weighted out-degree, but not the highest values of out-degree because they are shareholders of a few corporations, thus having large economic value. Vanguard Group and Black Rock funds have high weighted out-degree values and the highest out-degree values, as they are present in several ownership structures of valuable firms.

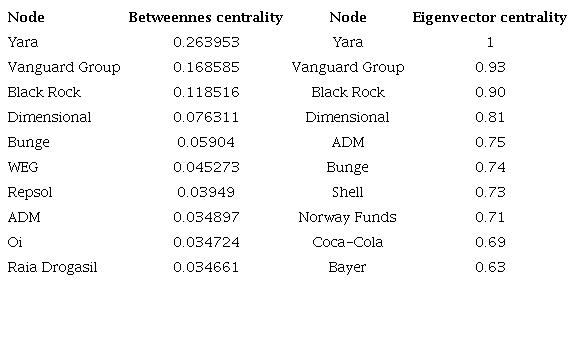

Table 4 shows the ten highest betweenness centrality measures. The betweenness centrality indicates actors with the potential for controlling flows through the network (Borgatti et al., 2013). It is possible to see that the three largest passive investment funds have the highest values. This is mainly due to the fact that these funds have high values of out-degree, as they are shareholders of dozens of valuable firms. Corporations of the initial sample, such as Yara and Bunge (from the agriculture sector), also have high values. However, this happens mostly because these corporations have a set of shareholders that are not common for other corporations.

Table 4 also shows the ten highest eigenvector centrality measures. This indicator is a measure of popularity where a node with high eigenvector centrality is connected to nodes that are well connected to each other (Borgatti et al., 2013). The high values of corporations of the initial sample (Yara, ADM, Shell, Bunge, Coca-Cola, and Bayer) can be justified by the fact that such firms have high values of centrality in-degree (as they have many shareholders links). Some of these links are also from shareholders with high out-degree measures, collaborating for the growth of their eigenvector measures. Large passive investment funds also emerge with high values of eigenvector measures. These actors do not have high values of in-degree centrality; they have high values of out-degree centrality, as they are shareholders of many corporations in the network with elevated values of in-degree centrality, thus increasing their eigenvector centrality measures.

Communities

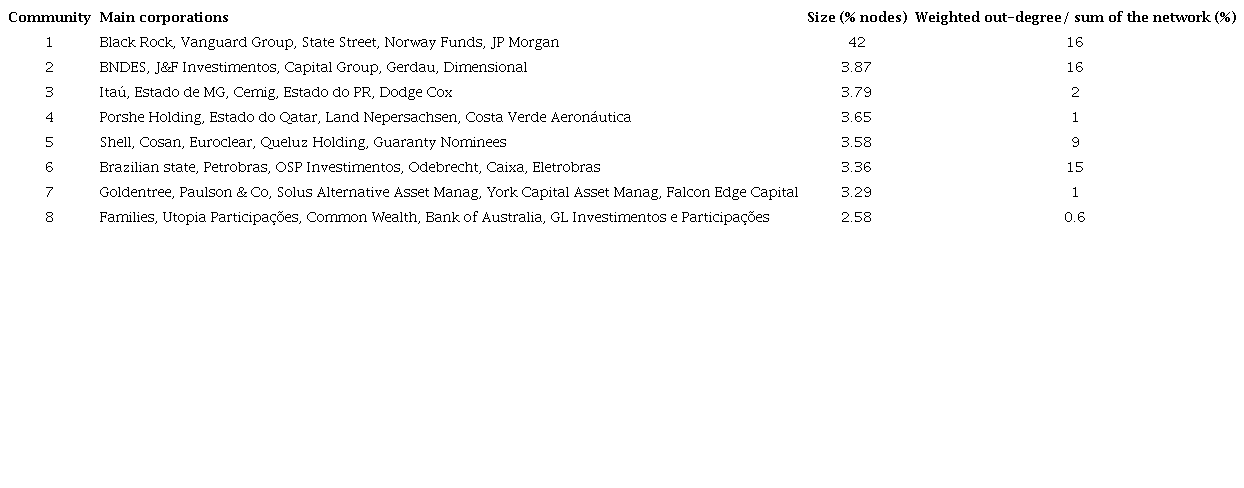

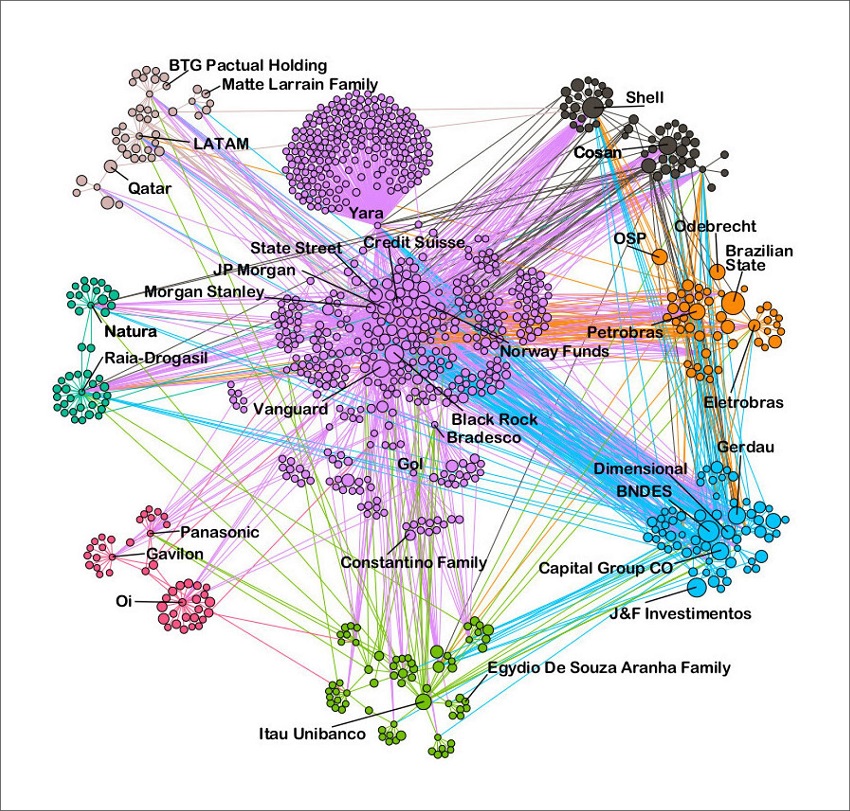

Modularity measures the clustering quality, i.e., the division of a network into subgroups (or communities) (Borgatti et al., 2013). Based on the high modularity value, 53 communities were identified in the network. However, Group 1, mostly composed of financial firms such as large investment funds and banks, has approximately 42% of the network nodes. Table 5 presents the eight largest communities by the number of nodes. Figure 2 shows these eight communities. For each of them, we obtained the sums of the members’ weighted out-degree measures and considered the participation of this sum in the total control of the network.

Figure 2

The eight largest communities of the corporate ownership network

Source: Elaborated by the author.

The group size does not necessarily indicate more control since small groups, such as 5 and 6, have total participation in control close to the values found for the large groups. The high value of Group 1 can be explained by the presence of large passive investment funds, such as the “Big Three” (Vanguard, Black Rock, and State Street). According to Fichtner et al. (2017), these three funds are the largest shareholders in 88% of the 500 largest American firms. The presence and strength of these funds and other financial firms in the economies and corporations are evidenced by studies conducted by Krippner (2005), Davis (2008), and Davis and Kim (2015). The high value of Group 2 can be mainly attributed to the presence of BNDES and J&F Investments - Brazilian corporations that are shareholders in important sectors of the economy and are among the five greatest shareholders of the network.

The high value of Group 6 is mostly related to the presence of the Brazilian government and corporations that are linked to the government (such as Caixa, Petrobras, and Eletrobras). The high value of Group 5 value can be explained by the presence of corporations linked to strong sectors of the economy, such as Shell and Cosan, which are shareholders of the oil and gas sector. These eight communities have about 62% of the network control. This result suggests a possible ownership concentration since the main corporations of these groups hold significant portions of the total control of the network.

DISCUSSIONS

The results reveal that the ownership network has a low density and is sparse and highly modularized into blocks. The node-level centrality measures and the communities show that financial shareholders (mainly the banks and largest passive investment funds), large corporations, and companies linked to the Brazilian state have the highest network scores. The centrality measures are related to the intermediation within the network (Borgatti et al., 2013; Newman, 2010).

The largest passive investment funds (such as Vanguard Group and Black Rock) and the fact that banks have shares of dozens of firms from different sectors indicate a possible financialization process of the largest corporations in Brazil, yet with a strong presence of the state (Lazzarini, 2011; Miranda et al., 2017; Moraes, 2017) and traditional family businesses (for example, Monteiro Aranha, Constantino, Hermínio de Moraes, Godoy Bueno). The presence of business elite networks and state-business relations in the Latin American context was also evidenced by Cárdenas (2016) and Wolff (2016). These facts confirm proposition 1 since, from the corporate control perspective, Brazilian corporate ownership shows evidence of hierarchical capitalism.

Thus, financial firms, families, and the Brazilian government own a relevant part of the largest corporations in the country and are prominent actors in these companies. This configuration converges to a financialization of the economy (Krippner, 2005) and the hierarchical capitalism proposed by Schneider (2009). This paper explores the intriguing structures of the ownership network of the largest corporations in Brazil since studies on network analysis in the Brazilian corporate control context, such as those reported by Carvalho (2018) and Lazzarini (2011), are still scarce.

Regarding the research questions of this study, the results indicate that large passive investment funds and banks (including Black Rock, Vanguard, State Street, and JP Morgan), the Brazilian state, and corporations that are linked to the government present the highest centrality measures. These findings converge on a form of corporate governance characterized by hierarchical relations where the firms are directly controlled and managed by their owners, either prominent families or foreign firms. The existence of sectors dominated by large corporations and sectors regulated by the state is also congruent with the findings of Schneider (2009). These findings corroborate proposition 2, which asserted that financial institutions intermediate the corporate ownership of the largest corporations in Brazil.

Also, the large communities with high control values in the network identified in the study corroborate the findings presented by Schneider (2009) regarding large and diversified business groups. These groups maintain direct hierarchical control over dozens of separate firms and a small number of huge groups and multinationals, which account for large shares of economic activity. These findings are similar to those reported by Fichtner et al. (2017), Davis (2008), Sacomano et al. (2020), Miranda et al. (2017), Carvalho (2018), and Lazzarini (2011). The study by Fichtner et al. (2017) presents the leading role of the “Big Three” (Vanguard, Black Rock, and Dimensional) as shareholders of the largest firms in the US. Davis (2008) also points out that large funds achieve high levels of structural prominence in the US economy. Similarly, Sacomano et al. (2020) show the central positions of the large passive funds in the ownership network of the largest automobile corporations.

In the Brazilian context, Miranda et al. (2017) suggest that financialization affects the control structure and the shareholders’ profiles of Brazilian non-financial firms. When analyzing the ownership network of the largest corporations in Brazil, Carvalho (2018) shows the prominent positions of large passive investment funds and state-owned enterprises in this network. Centrality measures are appropriate to understand the network influence (Borgatti et al., 2013; Newman, 2010). The results show that the financial institutions, mainly banks and large investment funds, occupy prominent structural positions in the network, evidenced by their high centrality measures. As suggested, these firms have the highest degree, betweenness, and eigenvector values. These actors are shareholders of dozens of firms in the sample and have intermediary positions in the network. In addition, according to their high weighted out-degree and out-degree measures, large passive investment funds are shareholders of several corporations from different sectors with strong economic value, for example, the oil and gas and food and drinks sectors.

The presence of large passive investment funds, banks, and other financial firms as shareholders and with prominent positions in the ownership network indicates the financialization of these firms’ control. Unlike active mutual funds, passive index funds often replicate existing stock indices, causing a re-concentration of corporate control and giving passive asset managers the “ability to exercise the voting power of the shares owned by their funds” (Fichtner et al., 2017, p. 300). These findings corroborate previous studies on financialization (Bonizzi et al., 2020; Borghi, Sarti, & Cintra, 2013; Kädtler & Sperling, 2002; Kaltenbrunner & Painceira, 2018; Lung, 2004; Sacomano et al., 2020). Fligstein (2001) argues that the recent process of financialization consists of a change in the corporate control conception, causing shareholders to push their agendas of maximizing the return from the growth of corporate stock value. However, financialization is not a homogeneous process because inside an industry, multiple forms of control may exist, as emphasized by the various types of capitalism reported in the literature (Coates, 2002; Hall & Soskice, 2001; Morgan & Kristensen, 2006; Sacomano et al., 2020).

Also with prominent positions in the network are the Brazilian state and corporations linked to the government. For example, the Brazilian government and the state-owned bank BNDES have high weighted out-degree measures because they are shareholders of key sectors with high economic value for the Brazilian economy. These actors are shareholders of corporations from important sectors such as the energy and oil and gas sectors, corroborating the studies by Cuervo-Cazura, Inkpen, and Musacchio (2014), Aldrighi and Postali (2010), and Evans (2012). Lazzarini (2011) suggests the existence of a “capitalism of ties” in Brazil, with the participation of the state (mainly through state-owned enterprises) and large business groups controlling the largest corporations in the country.

Private firms such as Shell and Cosan are shareholders of a few oil and gas corporations and participate in key sectors with substantial economic value. J&F Investments, American Movil, and GPA also have high centrality values, as they are shareholders of important sectors, such as the food industry, IT & Telecom, and retail business.

The privatization process in Brazil has increased since the beginning of the 1990s, especially with the National Privatization Program defined by the government in 1991 in different sectors (Cardoso, Maia, Santos, & Soares, 2013). For Rodrigues and Jurgenfeld (2019), this privatization process is related to the financialization process, presenting speculative characteristics due to the presence of banks and investment funds among the main buyers. Our findings indicate the prominent positions of financial firms (mainly banks and large investment funds) in the network, reinforcing the financialization process of the corporate control of the largest corporations in Brazil.

The recent neoliberal agenda promises to reinforce this privatization process of state-owned enterprises, strengthen implications for controlling these corporations and decrease the prominent position of the Brazilian state in the ownership network.

The results obtained herein show that firms linked to the Brazilian state, large multinationals, and large financial firms form large groups in the network, causing these communities to present high control measures and have the highest control values. The presence of large groups, large multinationals, and the state as large shareholders with a strong influence in late developing countries is also evidenced by Schneider (2009) when studying Latin American hierarchical capitalism.

CONCLUSIONS

This study analyzed the ownership network of the largest corporations in Brazil and aimed to investigate the possible hierarchical capitalism in the Brazilian corporate sector. Regarding the global structure, the network was dense, sparse, and highly modularized with a large connected component. These findings corroborate the study by Lazzarini (2011) about the ties of capitalism in the Brazilian context, which shows that large multinationals and the state are strong shareholders of the corporate sector. The results also confirm the findings by Taylor (2015) and Schapiro and Pereira (2019) on state ownership in the economy.

According to the centrality measures, financial actors (mainly large passive investment funds), large multinationals, the state, and actors linked to the Brazilian government are in central and influential positions in the network, which can then indicate a financialization process of the corporate control in Brazil and also reinforce the strength of the state in key sectors of the economy. Davis and Cobb (2010) state that “finance has altered power relations within firms by privileging one particular constituency (shareholders), changing metrics of performance (shareholder value), and re-orienting pay and human resource practices (to promote increases in share price)” (p. 39).

Regarding the groups, we identified large groups of large multinationals, families, financial firms, the state, and corporations linked to the Brazilian government. These groups were found to have the highest control value (sum of weighted out-degree) of the network. This configuration converges to the hierarchical capitalism form in Latin America presented by Schneider (2009).

Further studies on the effects of these prominent structural positions on the performance of corporations can contribute to deepening this research. Other forms of corporate control (board interlocking and R&D alliances, for instance) in a multiplex network can also be considered in future studies.

This study presented the corporate ownership network of the largest corporations in Brazil. The analysis of this network showed the structural prominence of the largest financial firms and the state as shareholders of these companies. In this analysis, we identified groups of corporations with high control values and a possible ownership concentration. This configuration is close to the hierarchical capitalism described by Schneider (2019), demonstrating the influence of financial firms as shareholders in the Brazilian corporate context. The contribution of this paper fills a gap in the literature regarding studies on corporate control in the Brazilian context from a network analysis approach and presents findings that converge to hierarchical capitalism in Brazilian companies.

REFERENCES

Aldrighi, D., & Postali, F. A. S. (2010). Business groups in Brazil. In A. Colpan, T. Hikino, & J. Lincoln (Eds.), The Oxford handbook of business groups (Vol. 1, pp. 353-386). Oxford: Oxford University Press, UK.

Bahamonde, J., Bollen, J., Eelejalde, E., Ferres, L., & Poblete, B. (2018). Power structure in Chilean news media. PLoS ONE, 13(6):e0197150. https://doi.org/10.1371/journal.pone.0197150

Bastian, M., Heymann, S., & Jacomy, M. (2009). Gephi: An Open Source Software for Exploring and Manipulating Networks. Proceedings of the International AAAI Conference on Web and Social Media, 3(1), 361-362. Retrieved from https://ojs.aaai.org/index.php/ICWSM/article/view/13937

Berle, A., & Means, G. (1932). The modern corporation and private property (Vol. 1). New York, USA: Editor Macmillan.

Bin, D. (2016). The politics of financialization in Brazil. World Review of Political Economy, 7(1), 106-126. https://doi.org/10.13169/worlrevipoliecon.7.1.0106

Bizberg, I. (2014). Types of Capitalism in Latin America. Interventions économiques. 49.https://doi.org/10.4000/interventionseconomiques.1772

Blondel, V., Guillaume, J. L., Lambiotte, R., & Lefebvre, E. (2008). Fast unfolding of communities in large networks. Journal of Statistical Mechanics: Theory and Experiment, 2008(10), 1000-1008. https://doi.org/10.1088/1742-5468/2008/10/p10008

Bonizzi, B., Kaltenbrunner, A., & Powell, J. (2020). Subordinate financialization in emerging capitalist economies. In The Routledge international handbook of financialization (pp. 177-187). Routledge.

Borgatti, S. P., Everett, M. G., & Johnson, J. C. (2013). Analyzing social networks (Vol. 1). Sage, Thousand Oaks, CA.

Borghi, R. A. Z., Sarti, F., & Cintra, M. A. M. (2013). The financialized structure of automobile corporations in the 2000s. World Review of Political Economy, 4(3), 387-409. doi: https://doi.org/10.13169/worlrevipoliecon.4.3.0387

Boyd, B. & Solarino, A. (2016). Ownership of Corporations: A Review, Synthesis, and Research Agenda. Journal of Management. 42.https://doi.org/10.1177/0149206316633746

Boyer, R. (2005). How and why capitalisms differ. Economy and Society, 34(4), 509-557. https://doi.org/10.1080/03085140500277070

Bruno, M., & Caffe, R. (2017). Estado e financeirização no Brasil: Iinterdependências macroeconômicas e limites estruturais ao desenvolvimento. Economia e Sociedade, 26(SPE), 1025-1062. https://doi.org/10.1590/1982-3533.2017v26n4art8

Bruno, M., Diawara, H., Araújo, E., Reis, A. C., & Rubens, M. (2011). Finance-Led Growth Regime no Brasil: Estatuto teórico, evidências empíricas e consequências macroeconômicas. Revista de Economia Política, 31(1), 730-750. https://doi.org/10.1590/S0101-31572011000500003

Campos, P. H. P. (Março, 2018). Capital estrangeiro no setor brasileiro de infraestrutura: História e situação atual. Jornal dos Economistas, 343. Retrieved from https://bityli.com/LXzKhzCJh

Cárdenas J. (2016). Why do corporate elites form cohesive networks in some countries, and do not in others? Cross-national analysis of corporate elite networks in Latin America. International Sociology, 31(3), 341-363. https://doi.org/10.1177/0268580916629965

Cardoso, V. I. C., Maia, A. B. G. R., Santos, S. M. D., & Soares, F. A. (2013). O impacto da privatização no desempenho econômico: Um estudo em empresas brasileiras de grande porte. Revista Ibero-Americana de Estratégia, 12(3), 183-211. http://dx.doi.org/10.5585/riae.v12i3.1904

Carvalho, A. C. (2018). Participação acionária em empresas listadas na BM&FBOVESPA em 2018: Um estudo de redes (Master dissertation, University of São Paulo). Retrieved from https://teses.usp.br/teses/disponiveis/96/96132/tde-08102018-153516/pt-br.php

Carvalho, C. E., & Vidotto, C. A. (2007) Abertura do setor bancário ao capital estrangeiro nos anos 1990: Os objetivos e o discurso do governo e dos banqueiros. Nova Economia, 17(3), 395-425. http://dx.doi.org/10.1590/S0103-63512007000300002

Coates, D. (2002). Varieties of Capitalism: The institutional foundations of comparative advantage. American Political Science Review, 96(3), 661-662. https://doi.org/10.1017/S0003055402740367

Collins, J., & Hussey, R. (2005). Pesquisa em administração: Um guia prático para alunos de graduação e pós-graduação. 2. ed. Porto Alegre: Bookman.

Corrado, R., & Zollo, M. (2006). Small worlds evolving: Governance reforms, privatizations, and ownership networks in Italy. Industrial and Corporate Change, 15(2), 319-352. https://doi.org/10.1093/icc/dtj018

Coutinho, L. G., & Belluzzo, G. D. M. (1998). “Financeirização” da riqueza, inflação de ativos e decisões de gasto em economias abertas. Economia e Sociedade, 7(2), 137-150. Retrieved from https://periodicos.sbu.unicamp.br/ojs/index.php/ecos/article/view/8643156

Cuervo-Cazurra, A., Inkpen, A., & Musacchio, A. (2014). Governments as owners: State-owned multinational companies. Journal of International Business Studies, 45(8), 919-942. https://doi.org/10.1057/jibs.2014.43

Davis, G. (2008). A new finance capitalism? Mutual funds and ownership re-concentration in the United States. European Management Review, 5(1), 11-21. https://doi.org/10.1057/emr.2008.4

Davis, G. F., & Cobb, J. (2010). Resource Dependence Theory: Past and future. Research in the Sociology of Organizations, 28 21-42. https://doi.org/10.1108/S0733-558X(2010)0000028006

Davis, G., & Kim, S. (2015). Financialization of the economy. Review of Sociology, 41, 203-221. https://doi.org/10.1146/annurev-soc-073014-112402

Epstein, G. (2005). Financialization and the world economy (Vol. 1). Edward Elgar Publishing, UK.

Evans, P. B. (2012). Embedded autonomy (Vol. 1). Princeton University Press, US.

Fichtner, J., Heemskerk, E., & Garcia-Bernardo, J. (2017). Hidden power of the Big Three? Passive index funds, re-concentration of corporate ownership, and new financial risk. Business and Politics, 19(2), 298-326. https://doi.org/10.1017/bap.2017.6

Fleury, A., & Fleury, L. T. M. (January, 2006). China and Brazil in the Global Economy. IDS Bulletin, 37(1). Retrieved from https://www.ids.ac.uk/publications/china-and-brazil-in-the-global-economy/

Fligstein, N. (1990). The transformation of corporate control. Cambridge, USA: Harvard University Press.

Fligstein, N., & Brantley, P. (1992). Bank control, owner control, or organizational dynamics: Who controls the large modern corporation? American Journal of Sociology, 98(2), 280-307. https://doi.org/10.1086/230009

Fligstein, N. (2001). The architecture of markets: An economic sociology for 21st century capitalism. Princeton University Press,Princeton, N.J

Fu, S., & Cooper, K. (2020). Interorganizational network portfolios of nonprofit organizations: Implications for collaboration management. Nonprofit Management and Leadership, 31(3), 437-459. https://doi.org/10.1002/nml.21438

Gill, M. S., Vijay, T. S., & Jha, S. (2009). Corporate governance mechanisms and firm performance: A survey of literature. The Icfai University Journal of Corporate Governance, 8(1), 7-21. https://doi.org/10.1108/CG-07-2018-0244

Glattfelder, J. (2010). Ownership networks and corporate control: Mapping economic power in a globalized world (Phd thesis, ETH Zurich). Retrieved from https://www.research-collection.ethz.ch/handle/20.500.11850/152305

Glattfelder, J., & Battiston, S. (2019). The architecture of power: Patterns of disruption and stability in the global ownership network. SSRN 3314648.

Hafner-Burton, E., Kahler, M., & Montgomery, A. (2009). Network analysis for international relations. International Organization, 63(3), 559-592. https://doi.org/10.1017/S0020818309090195

Hall, P. A., & Soskice, D. (2001). An introduction to varieties of capitalism. 21-27. Retrieved from https://scholar.harvard.edu/files/hall/files/vofcintro.pdf

Ireland, P. (2012). Financialization and corporate governance. Northern Ireland Legal Quarterly, 60, 1. http://dx.doi.org/10.53386/nilq.v60i1.472

Jensen, M., & Meckling, W. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

Jeude, J., Aste, T., & Caldarelli, G. (2019). The multilayer structure of corporate networks. New Journal of Physics, 21(2), 025002. https://doi.org/10.1088/1367-2630/ab022d

Kädtler, J., & Sperling, J. H. (2002). The power of financial markets and the resilience of operations: Argument and evidence from the German car industry. Competition & Change, 6(1), 81-94. doi: https://doi.org/10.1080/10245290212672

Kaltenbrunner, A., & Painceira, P. J. (2018). Subordinated financial integration and inancialization in emerging capitalist economies: The Brazilian experience. New Political Economy, 23(3), 290-313. https://10.1080/13563467.2017.1349089

Kogut, B., & Walker, G. (2001). The small world of Germany and the durability of national networks. American Sociological Review, 66(3), 317-335. https://doi.org/10.2307/3088882

Krippner, G. (2005). The financialization of the American economy. Socio-Economic Review, 3(2), 173-208. https://doi.org/10.1093/SER/mwi008

Lazonick, W. (2010). Innovative business models and varieties of Capitalism: Financialization of the U.S. corporation. Business History Review, 84(4), 675-702. https://doi.org/10.1017/S0007680500001987

Lazonick, W., & O'Sullivan, M. (2000). Maximizing shareholder value: A new ideology for corporate governance. Economy and Society, 29(1), 13-35. https://doi.org/10.1080/030851400360541

Lazzarini, G. S. (2011). Capitalismo de laços: Os donos do Brasil e suas conexões (Vol. 1). Rio de Janeiro, RJ: Elsevier.

Lira, F. R. F. T. de. (2008). Efeitos da "financeirização" sobre a economia brasileira. Curitiba, PR: Vitrine da Conjuntura.

Lung, Y. (2004). The changing geography of the European automobile system. International Journal of Automotive Technology and Management, 4(2/3), 137-165. https://doi.org/10.1504/IJATM.2004.005324

MarketScreener. (2020). MarketScreener. Retrieved from https://www.marketscreener.com/

Miller, R. M. (2010). Latin American business history and varieties of Capitalism. The Business History Review, 84(4), 653-657. Retrieved from https://www.jstor.org/stable/27917302

Miranda, B., Crocco, M., & Santos, F. (2017). Financeirização e governança corporativa: Um estudo sobre a estrutura de controle das empresas não -financeiras do Novo Mercado da BM&FBovespa. Brazilian Keynesian Review, 3(1), 75-94. https://doi.org/10.33834/bkr.v3i1.100

Miranda, B. P. J. D., Crocco, M. A., & Santos, F. B. (2009). Impactos da financeirização sobre o padrão de financiamento e a governança das empresas não financeiras brasileiras de capital aberto: Período de 1995-2008. XVI Seminário sobre a Economia Mineira, Diamantina, Minas Gerais.

Moraes, G. C. L. (2017). Nas asas do capital: Embraer, financeirização e implicações sobre os trabalhadores. Caderno CRH, 30(79), 13-31. https://doi.org/10.1590/S0103-49792017000100002

Moreira, M., & Puga, F. (2000). Como a indústria financia o seu crescimento: Uma análise do Brasil Pós-Plano Real. Revista Econômica Contemporânea, 5, 35-67. Retrieved from https://revistas.ufrj.br/index.php/rec/article/view/19706

Morgan, G., & Kristensen, P. H. (2006). The contested space of multinationals: Varieties of institutionalism, varieties of capitalism. Human Relations, 59(11), 1467-1490.https://doi.org/10.1177/0018726706072866

Murdie, A. (2014). The ties that bind: A network analysis of human rights international nongovernmental organizations. British Journal of Political Science, 44(1), 1-27. https://doi.org/10.1017/S0007123412000683

Newman, M. (2010). Networks: An introduction (Vol. 1). Oxford University Press, UK.

Oberg, A., Korff, V. P., & Powell, W. W. (2017). Culture and connectivity intertwined: Visualizing organizational fields as relational structures and meaning systems, structure, content and meaning of organizational networks. Research in the Sociology of Organizations, 53, 17-47. https://doi.org/10.1108/S0733-558X20170000053001

Orbis. (2020). Orbis Database. Retrieved from https://www.bvdinfo.com/en-gb/our-products/data/international/orbis

Panceira, J. P. (2011). Central banking in middle income countries in the course of financialisation: A study with special reference to Brazil and Korea (Phd thesis, University of London).

Plihon, D. A. (2005). As grandes empresas fragilizadas pela finanças. In F. Chesnais (Org.), A finança mundializada (pp. 133-151). São Paulo, SP: Editora Boi Tempo.

Rodrigues, L. H. C., & Jurgenfeld, F. C. (2019). Desnacionalização e financeirização: Um estudo sobre as privatizações brasileiras (de Collor ao primeiro governo FHC)*. Economia e Sociedade, 28(2), 393-420. https://doi.org/10.1590/1982-3533.2019v28n2art05

Sacomano, M., Carmo, J. M., Ribeiro, E. S., & Cruz, G. V. W. (2020). Corporate ownership network in the automobile industry: Owners, shareholders and passive investment funds. Research in Globalization, 2, 100016. https://doi.org/10.1016/j.resglo.2020.100016

Schapiro, G. M., & Pereira, A. S. (2019). Um palacete assobradado: A coexistência entre organizações estatais e instituições de mercado no financiamento habitacional brasileiro. Revista Direito GV, 15(3). https://doi.org/10.1590/2317-6172201936

Schneider, B. (2009). Hierarchical market economies and varieties of Capitalism in Latin America. Journal of Latin American Studies, 41(3), 553-575. https://doi.org/10.1017/S0022216X09990186

Schneider, R. B., & Soskice, D. (2009). Inequality in developed countries and Latin America: Coordinated, liberal and hierarchical systems. Economy and Society, 38(1), 17-52. https://doi.org/10.1080/03085140802560496

Scott, R. W. (2004). Reflections on a half-century of organizational sociology. Annual Review of Sociology, 30(1), 1-21. https://doi.org/10.1146/annurev.soc.30.012703.110644

Swedberg, R. (2004). Economic sociology: Today and tomorrow. Tempo Social, 16(2), 7-34. https://doi.org/10.1590/S0103-20702004000200001

Taylor, M. (2015) The Unchanging Core of Brazilian State Capitalism, 1985-2015 (October 14, 2015). School of International Service Research Paper No. 2015-8, Available at SSRN: https://ssrn.com/abstract=2674332 or http://dx.doi.org/10.2139/ssrn.2674332

Taylor, M. (2020). Decadent developmentalism: The political economy of democratic Brazil. Cambridge: Cambridge University Press, UK.

Uzzi, B., Amaral, L. A., & Tsochas, F. R. (2007). Small world networks and management science research: A review. European Management Review, 4(2), 77-91. doi: https://doi.org/10.1057/palgrave.emr.1500078

Valor1000. (2019). Ranking 1.000 maiores empresas do Brasil. Retrieved from https://especial.valor.com.br/valor1000/2020

Vitali, S., & Battiston, S. (2014) The community structure of the global corporate Network. PLoS ONE, 9(8), e104655. https://doi.org/10.1371journal.pone.0104655

Vitali, S., Glattfelder, J. B., & Battiston, S. (2011). The network of global corporate control. PLoS ONE, 6(10), e25995. https://doi.org/10.1371/journal.pone.0025995

Vitols, S. (2001). Varieties of corporate governance: Comparing Germany and the UK. In Hall & Soskice (Eds.), Varieties of Capitalism: The institutional foundations of comparative advantage (Vol. 1, pp. 337-369). Oxford University Press, UK.

Wahl, M. (2006). The ownership structure of corporations: Owners classification & typology. EBS Review, 2(21), 94-103. Retrieved from https://www.etis.ee/Portal/Publications/Display/9e9c2384-9b89-4552-ac14-9f0043b58417

Wasserman, S., & Faust., K. (1994). Social network analysis. Cambridge: Cambridge University Press, UK.

Wilson, F. J., Buchnea, E., & Tilba, A. (2018) The British corporate network, 1904-1976: Revisiting the finance-industry relationship. Business History, 60(6), 779-806. https://doi.org/10.1080/00076791.2017.1333106

Wolff, J. (2016). Business power and the politics of Postneoliberalism: Relations between governments and economic elites in Bolivia and Ecuador. Latin American Politics and Society, 58(2), 124-147. https://doi.org/10.1111/j.1548-2456.2016.00313.x

WorldBank. (2021, July 1). World Development Indicators database. Retrieved from https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?most_recent_value_desc=true

World Trade Organization. (2020). Report. Retrieved from https://www.wto.org/english/res_e/statis_e/daily_update_e/trade_profiles/BR_e.pdf

Zwan, N. Van Der. (2014). Making sense of financialization. Socio-Economic Review, 12(1), 99- 129. https://doi.org/10.1093/ser/mwt020

Author notes

*Corresponding Author

Conflict of interest declaration

The authors have no conflicts of interest to declare.