Artigos

Effects of credit rating changes on capital structure of Latin American firms

Efeitos do rating de crédito sobre a estrutura de capital das empresas latino-americanas

Effects of credit rating changes on capital structure of Latin American firms

Revista de Contabilidade e Organizações, vol. 13, pp. 1-14, 2019

Universidade de São Paulo, Faculdade de Economia Administração e Contabilidade de Ribeirão Preto

Received: 27 January 2019

Accepted: 20 May 2019

Abstract: This study investigates whether non-financial Latin American firms adjust their capital structure in order to maintain certain rating levels. The credit rating-capital structure (CR-CS) hypothesis suggests that firms assume less debt after rating downgrades, aiming to retrieve necessary conditions to restore a better rating. Through panel data analysis for the 2000-2014 period and by using the generalized method of moments (GMM), we show that a rating downgrade does not accelerate the speed of adjustment to the target, indicating that firms do not target minimum rating levels, as predicted by the CR-CS hypothesis. Although, rating changes are related to firms’ capital structure, we conclude that Latin American firms do not adjust their capital structure to maintain certain rating levels.

Keywords: Capital structure, Credit rating, Partial adjustment, Target leverage, Latin American firms.

Resumo: O presente estudo verifica se as empresas latino-americanas não financeiras ajustam a sua estrutura de capital com a finalidade de manter determinado rating de crédito. Segundo a hipótese “credit rating-capital structure” (CR-CS), as empresas diminuem o nível de endividamento após um rebaixamento de rating, visando restabelecer as condições necessárias para retomar o rating anterior. Por meio da análise de dados em painel para o período de 2000 a 2014, utilizando-se do método dos momentos generalizados, os resultados mostram que um rebaixamento de rating não acelera a velocidade de ajuste em direção ao endividamento-alvo, indicando que as empresas não buscam atingir níveis mínimos de rating de crédito, como prediz a hipótese CR- CS. Embora o rating de crédito tenha apresentado relação com a estrutura de capital das empresas latino-americanas, conclui-se que elas não ajustam a estrutura de capital a fim de manter determinado rating.

Palavras-chave: Estrutura de Capital, Rating de Crédito, Ajuste parcial, Endividamento-alvo, Empresas latino-americanas.

1 INTRODUCTION

Credit ratings serve two purposes: they certify the firm’s current financial condition (initial credit rating) and signal a change in the firm's financial choices (rating changes, i.e., upgrades and downgrades) (Cornaggia, Krishnan & Wang, 2017; Fracassi, Petry & Tate, 2016). The maintenance of a good credit rating provides benefits to a firm mainly associated with a reduction in its cost of capital. In contrast, a credit rating downgrade may trigger a re-negotiation between the firm and its fund suppliers that might affect the subsequent interest rates charged by creditors, resulting in increased coupon rates on bonds and high costs of accessing capital markets or issuing securities (Wojewodzki, Poon & Shen, 2017; Agha & Faff, 2014). In this context, is the interest in benefits (or in avoiding costs) associated with the maintenance of certain rating levels likely to influence managerial decisions? Studies carried out primarily among United States firms suggest so, indicating an influence of credit rating on capital structure decision-making (Agha & Faff, 2014; Kemper & Rao, 2013; Michelsen & Klein, 2011; Hovakimian, Kayhan & Titman, 2009; Kisgen, 2009; Kisgen, 2006; Grahan & Harvey, 2001).

The credit rating-capital structure (CR-CS) hypothesis proposes that firms that are facing an imminent rating change or have suffered a rating downgrade make more conservative capital structure decisions, in the sense of assuming less debt (Kisgen, 2006). According to Kisgen (2006), firms target minimum rating levels, and a rating downgrade predicts capital structure decisions better than changes in leverage. Huang and Shen (2015) found results consistent with the CR-CS hypothesis, in which downgraded firms adjusted their capital structure more rapidly than non-downgraded firms, especially in developed countries.

In Latin America, rating change announcements have a significant impact on stock prices in Argentina, Brazil, Chile, and Mexico (Freitas & Minardi, 2013), but its effects on capital structure decisions are still incipient (or neglected) in these countries. Rogers, Mendes-da-Silva, and Rogers (2016) presented evidence that credit rating changes are not determinants of capital structure in Latin American firms. However, the authors analyzed this relationship believing that companies can predict the imminence of a rating reclassification and not considering the impact on capital structure after rating changes.

We aim to identify whether publicly traded non-financial firms in the leading Latin American countries (Brazil, Argentina, Mexico, Chile, and Peru) promote adjustments in their capital structure to maintain certain rating levels. To this end, we assessed the firms’ capital structure after different rating changes (maintenance, downgrades, and upgrades), using the model of partial adjustment to target leverage proposed by Flannery and Rangan (2006) to test the trade-off theory behavior. We add to the model of Flannery and Rangan (2006) a representative variable of credit re-rating, similar to Kisgen (2009). If the credit rating is not relevant to firms’ capital structure decisions, then rating changes should not influence subsequent capital choices. The sample period for the tests is 2000 to 2014.

This study contributes to the literature by providing a better understanding of credit rating relevance and hence the accuracy of the CR-CS hypothesis in Latin American firms, given the more recent process of development of capital markets compared to developed countries. Freitas and Minardi (2013, p. 442) emphasized that international investors consider Latin America in their portfolio as a whole instead of a single country. Besides, the growth and development of the Latin American capital market have attracted more investors, and consequently, higher coverage of the rating agencies, especially since 2004 (Freitas & Minardi, 2013).

Our results show that even though rating downgrades influence the firms' capital structure in Latin America, firms do not target minimum rating levels as predicted by the CR-CS hypothesis. We conclude that financial decisions targeting leverage levels are more representative in the capital structure of Latin American firms than financial decisions targeting minimum rating levels since the acquisition of resources is a first-order necessity compared to maintaining a certain rating level.

The next section defines the research hypotheses, besides summarizing the theoretical framework on credit rating and capital structure. Section 3 describes the methodological procedures employed and identifies the data, variables, and analysis models. Section 4 presents the analysis of the results. The last section contains our final considerations and conclusion.

2 CREDIT RATING AND CAPITAL STRUCTURE

2.1 Hypotheses

The credit rating relevance for capital structure decision-making was documented by Graham and Harvey (2001) in a comprehensive survey with North American chief financial officers, who indicated the preservation of credit rating as the second primary concern to determine corporate leverage. Motivated by this finding, Kisgen (2006) conducted the seminal empirical investigation of credit rating influence on capital structure by analyzing debt and equity issuances of firms that were in the imminence of credit re-rating. According to the credit rating- capital structure hypothesis, initially formulated in Kisgen (2006) and consolidated in Kisgen (2009), firms bound to achieve a rating upgrade should issue less debt relative to equity to favor conditions to obtain the upgrade. Likewise, firms near a rating downgrade should adopt the same position, but in this case, aiming to avoid a downgrade.

Kisgen (2009) relied on two different models of capital structure decision to evaluate the impact of credit rating changes. First, rating changes (upgrades and downgrades) were inserted as explanatory variables to explain the firms’ net debt issuance, making his model similar to that adopted in Kisgen (2006), but analyzed from the perspective of the decisions made after the rating changes. Additionally, Kisgen (2009) included the rating changes variables in a partial adjustment model of capital structure to the target leverage. Both models allowed assessment of a re-rating impact on the subsequent debt level, and the latter also enabled evaluation of the rating impact on target leverage balance of the capital structure.

The results corroborated the CR-CS hypothesis’ propositions, suggesting a reduction of more than 2.0% in leverage, as a percentage of assets, compared with non-downgraded firms. For rating upgrades, in turn, the results indicated no impact on subsequent capital structure decisions. Finally, analysis of capital structure balance showed that a downgrade accelerates the adjustment toward the firm’s target leverage, whereas an upgrade will not influence the pace of adjustment.

We investigate the following three hypotheses based on the CR-CS hypothesis’ propositions:

H1: The balance of the capital structure toward target leverage occurs more rapidly for downgraded firms.

H2: Downgraded firms are more likely to promote a subsequent reduction in debt level compared with non-downgraded firms.

H3: A credit rating upgrade does not influence subsequent changes in the capital structure.

2.2 Empirical evidence

Hovakimian et al. (2009) investigated the existence of target credit rating levels, as well as their influence on capital structure. According to the authors, although firms are often subject to shocks that lead them to deviate from their target ratings, they will make financing choices that allow them to move back towards their rating targets if rating concerns are relevant. To assess this assumption, the authors revisited traditional studies on target leverage and added analysis of deviations relative to target rating levels. The results demonstrated that firms make decisions regarding debt issuance and repurchase aimed at maintaining the target capital structure. However, firms are more likely to issue equity rather than debt when the rating level is below the target, as well as when debt is above the desired level. The opposite, however, was not found to be accurate, indicating that the above-target rating, as well as below-target leverage, does not influence the firms’ capital structure decisions.

Michelsen and Klein (2011) re-evaluated capital structure decisions near credit rating changes, but with a more representative sample, composed of firms from the United States, Europe, the Middle East, and Africa. The results obtained by Michelsen and Klein (2011) reinforce the propositions of the CR-CS hypothesis. First, the relationship verified for imminent upgrades and downgrades is not symmetrical, being more intense near a downgrade. That is, the possibility of rating downgrade induces an economically more conservative capital structure policy than that observed for a possible upgrade, reinforcing that managers target minimum rating levels. Also, the authors found that the CR-CS hypothesis effects are economically more significant in countries with broader capital markets, such as the United States, the United Kingdom, Germany, and France.

Using a similar approach to that of Michelsen and Klein (2011), Kemper and Rao (2013) analyzed capital structure decisions of United States firms, but unlike the previous studies based on observation of seasonal variations, the authors analyzed quarterly changes in the capital structure.

Kemper and Rao (2013) found that firms responded differently to the possibility of rating upgrades and downgrades. Whereas firms near a rating upgrade issued less debt relative to equity, those near a downgrade issued more debt, contradicting the results of Hovakimian et al. (2009) and Michelsen and Klein (2011). The authors argued that if the rating was a first-order managerial concern, the possibility of a rating downgrade should induce a more conservative capital structure.

There are also studies that have explored legal and institutional issues, such as Huang and Shen (2015) and Wojewodzki, Poon, and Shen (2017). Huang and Shen (2015) investigated how cross-country variations in institutional variables affect the relationship between rating changes (downgrades and upgrades) and firms’ capital structure. The authors found that downgraded firms expedite the adjustment speed, corroborating Kisgen (2009) and Michelsen and Klein (2011) and that the leverage ratios adjust faster in stable legal and institutional countries. In a similar study, Wojewodzki, Poon, and Shen (2017) found that in countries with a more market-oriented financial system, the impact of credit ratings on firms’ capital structure is more significant and the adjustment is faster.

Rogers, Mendes-da-Silva, Neder, and Silva (2013) and Rogers et al. (2016) investigated the relevance of credit rating on capital structure in Latin American firms based on the approach adopted by Kisgen (2006). The results did not confirm the CR-CS hypothesis’ propositions, indicating that the proximity of credit re-rating does not influence capital structure. According to Rogers et al. (2013, p. 336), it is possible that credit re-rating outlook does not affect the capital structure of non-financial Latin American firms. However, the authors analyzed the issue without considering the impact on capital structure after rating changes.

Unlike Rogers et al. (2016) and Rogers et al. (2013), this study uses the CR-CS hypothesis’ propositions to verify the effects of credit rating changes on capital structure of Latin American firms after different ratings changes, considering that firms assume less debt after rating downgrades aiming to retrieve necessary conditions to restore a better rating. The present study broadens the understanding of the CR-CS hypothesis concerning the behavior of the Latin American firms since the institutional environment of these firms differ from more economically developed markets, such as those studied by Kisgen (2009, 2006).

3 RESEARCH DESIGN

3.1 Data and sample

We use the accounting and financial databases by Thomson One system (Thomson Reuters). The initial search included data from 876 publicly traded non-financial firms in Brazil, Argentina, Mexico, Chile, and Peru, during the period 1999-2014, of which only firms with a credit rating and without missing values were maintained for the composition of a balanced sample. The final sample consists of 97 firms. The period for the tests is 2000 to 2014.

The final sample is composed by 32 Brazilian firms, 27Mexican firms, 20 Chilean firms, 10 Argentinean firms, and 8 Peruvian firms. The assessment was performed using the long-term domestic issuer credit rating, the most widely used by firms, designated by the agencies Standard & Poor’s (S&P) and Moody’s, whose ratings are available in the Thomson One system. This study comprises 850 rating records, including 333 credit re-ratings that occurred during the survey period, with 146 downgrades (17% of the rating records) and 187 upgrades (22%). Table 1 shows the distribution of assigned ratings-year and rating changes (downgrades, upgrades, and maintenances) by country and sector (see also Appendix A).

| Raw materials | Consumer goods | Industry | Services | Oil & Gas | Telecom | Utilities | Total | ||

|---|---|---|---|---|---|---|---|---|---|

| Downgrade | 4 | 2 | 0 | 0 | 3 | 1 | 18 | 28 | |

| Upgrade | 22 | 2 | 8 | 0 | 5 | 3 | 46 | 86 | |

| Brazil | Maintenance | 47 | 5 | 15 | 0 | 6 | 3 | 83 | 159 |

| Total | 73 | 9 | 23 | 0 | 14 | 7 | 147 | 273 | |

| Downgrade | 7 | 8 | 14 | 11 | 0 | 0 | 0 | 40 | |

| Mexico | Upgrade | 6 | 13 | 11 | 14 | 0 | 2 | 0 | 46 |

| Maintenance | 26 | 64 | 20 | 26 | 0 | 12 | 0 | 148 | |

| Total | 39 | 85 | 45 | 51 | 0 | 14 | 0 | 234 | |

| Downgrade | 2 | 9 | 4 | 0 | 1 | 5 | 14 | 35 | |

| Chile | Upgrade | 3 | 4 | 1 | 4 | 0 | 3 | 14 | 29 |

| Maintenance | 21 | 18 | 10 | 5 | 14 | 18 | 50 | 136 | |

| Total | 26 | 31 | 15 | 9 | 15 | 26 | 78 | 200 | |

| Downgrade | 0 | 0 | 0 | 0 | 19 | 4 | 19 | 42 | |

| Argentina | Upgrade | 0 | 0 | 0 | 0 | 7 | 2 | 9 | 18 |

| Maintenance | 0 | 0 | 0 | 0 | 16 | 4 | 35 | 55 | |

| Total | 0 | 0 | 0 | 0 | 42 | 10 | 63 | 115 | |

| Downgrade | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | |

| Peru | Upgrade | 3 | 1 | 3 | 0 | 0 | 0 | 1 | 8 |

| Maintenance | 3 | 1 | 2 | 0 | 0 | 0 | 13 | 19 | |

| Total | 7 | 2 | 5 | 0 | 0 | 0 | 14 | 28 | |

| Downgrade | 14 | 19 | 18 | 11 | 23 | 10 | 51 | 146 | |

| Total | Upgrade | 34 | 20 | 23 | 18 | 12 | 10 | 70 | 187 |

| Maintenance | 97 | 88 | 47 | 31 | 36 | 37 | 181 | 517 | |

| Total | 145 | 127 | 88 | 60 | 71 | 57 | 302 | 850 |

3.2 Definition of the variables and econometric models

Kisgen (2009) suggested that the effect of rating changes on capital structure may be verified using the model of partial adjustment to target leverage proposed by Flannery and Rangan (2006) to test the trade-off theory. The model was developed to indicate the existence of target leverage based on the adjustment speed toward the target ratio, since convergence does not occur ultimately, but partially over time, due to the presence of adjustment costs (Flannery & Rangan, 2006). According to the trade-off theory, target leverage optimizes the relationship between the costs and benefits of debt, promoting maximization of firm value (Myers, 2001).

The utilization of this method aims to verify the effect of rating changes on capital structure balance. Table 2 presents the variables used in this study. Debt Ratio is the dependent variable, and Rating Downgrade and Rating Upgrade are the independent variables. As control variables, we used Firm Size, Growth Opportunity, Profitability, Fixed Assets, Depreciation Expenses, Research & Development Expenses, a dummy for Research & Development Expenses, and Sectorial Debt Ratio.

| Variables | Definition/Calculation |

|---|---|

| I. Dependent Variable | |

| Debt Ratio | = Total Debti,t / Total Assetsi,t |

| II. Independent Variables | |

| Rating Downgrade | = Dummy variable that assumes value 1 when rating is downgraded and 0otherwise |

| Rating Upgrade | = Dummy variable that assumes value 1 when rating is upgraded and 0otherwise |

| III. Control Variables | |

| Firm Size | = Natural logarithm of Total Assetsi,t deflated |

| Growth Opportunity | = (Net incomet – Net incomet-1) / Total Assetsi,t |

| Profitability | = Earnings Before Interest and Taxi,t / Total Assetsi,t |

| Fixed Assets | = Fixed Assetsi,t / Total Assetsi,t |

| Depreciation Expenses | = Depreciation Expensesi,t / Total Assetsi,t |

| Research & Development Expenses | = Research & Development Expensesi,t / Total Assetsi,t |

| Dummy for Research & Development | = Dummy variable equal to 1 if firm did not report Research & Development Expenses and 0 otherwise |

| Sectorial Debt Ratio | = Mean debt per sector-year |

Target leverage is not an observable characteristic, so it requires a model that allows its estimation. In this study, we adopted the model proposed in Flannery and Rangan (2006), which assumes target leverage as a linear function of corporate factors associated with the capital structure, represented by equation (1):

Where DR*i,t is the target Debt Ratio (or target leverage);is the vector of firm characteristics associated with the costs and benefits of different debt levels, β is the coefficient of X, and εi,t is the error term. The variables represented by X and their expected signs (in parentheses) are as follows: Firm Size (positive), Growth Opportunity (positive/negative), Profitability (positive), Fixed Assets (positive), Depreciation Expenses (negative), Research & Development Expenses (negative), Dummy for Research & Development (negative), and Sectorial Debt Ratio (positive/negative) (Kisgen, 2009; Flannery & Rangan, 2006; Fama & French, 2002).

Flannery and Rangan (2006) argued that the existence of adjustment costs (transaction costs associated with bond issuance) means that the capital structure is not entirely balanced but gradually balanced over time, following the equation (2). The expected value of λ, indicates λ = 0 no change in leverage between t-1 and t, and λ = 1 total balance to target leverage. Substitution of equation (1) in equation (2) then results in the model of partial adjustment to target leverage, equation (3):

Where DRi,t is Debt Ratio (leverage); DR*i,t is the target Debt Ratio (target leverage), λ is the adjustment coefficient, which shows the ratio between observed and desired debt level, Xi,t-1 is the vector of firm characteristics associated with the costs and benefits of different debt levels, β is the coefficient of X, and ε i,t is the error term. Equation (3) is used to test whether the balance of the capital structure toward target leverage occurs more rapidly for downgraded firms (H1).

Similar to the method used by Kisgen (2009), we assessed the adjustment coefficient (λ) conditional on credit re-rating using equation (3) in the total sample and three different sub-samples, composed of (i) firms-year after a rating downgrade; (ii) firms-year after a rating upgrade; and (iii) firms-year after rating maintenance. If the credit rating is an essential concern to the firm, the credit rating-capital structure hypothesis suggests a faster adjustment of the capital structure after rating downgrade compared with upgrade or maintenance. In contrast, if the credit rating is not a real concern, there would be no reason for changes in adjustment speed (Kisgen, 2009).

Furthermore, Kisgen (2009) suggested verifying the incremental effect of downgrades and upgrades on the subsequent debt, including them in equation (3), which now presents the following specification:

Where Down and Up are dummy variables, λ is the adjustment coefficient, Xi,t-1 is the vector for firm characteristics associated with the costs and benefits of different debt levels, β is the coefficient of X, and ε i,t is the error term. Equation (4) is used to test whether downgraded firms are more likely to promote a subsequent reduction in debt level compared with non-downgraded firms (H2) and to test whether a credit rating upgrade does not influence following changes in the capital structure (H3).

We used dynamic panel data models through the generalized method of moments (GMM) technique. It is important to emphasize that in a context of dynamic panel data modeling, with the presence of the lagged dependent variable among the regressors, the inclusion of the means in the model creates a correlation between the lagged dependent variable regressor and the error term, known as dynamic panel bias (Nickell, 1981). In specifying the model of partial adjustment to target leverage, Flannery and Rangan (2006) and Kisgen (2009) addressed the dynamic panel bias with substitution of lagged debt ratio (in this case, at market value) by instrumental variables formed by the book value. However, this artifice is not possible in this study due to the absence of an alternative measure of the debt ratio, considering the unavailability of market value data.

Flannery and Hankins (2013) revised the results of Flannery and Rangan (2006), using estimators developed for dynamic panel data models, and demonstrated that the Arellano-Bover/Blundell-Bond estimator (Arellano & Bover, 1995; Blundell & Bond, 1998) is the most consistent for finance studies, given the characteristics of regularly used data. In the authors’ opinion, this estimator “is reliable regardless of the level of endogeneity or dependent variable persistence and should be the default choice under these conditions, particularly if the lag coefficient is of interest” (Flannery & Hankins, 2013, p. 16).

Therefore, we adopted the partial adjustment model to target leverage with the same specification as Flannery and Hankins (2013), using of the Arellano-Bover/Blundell-Bond estimator, instrumental variables limited to a maximum of two lags, explanatory variables defined as predetermined, and inclusion of annual dummy variables to control for possible exogenous influences associated with specific periods, such as economic shocks.

4 ANALYSIS OF THE RESULTS

4.1 Previous analysis

Table 3 shows the distribution of re-rating records by level. Except for level A, all other available rating levels also present some reclassification: a downgrade, an upgrade, or both. The downgrades are fairly distributed across all levels, with most frequent occurrences for BBB (11 downgrades), B (13 downgrades), and Not Rated (31 events) - cases in which there was a loss in rating, treated as a downgrade because it exposed the firm to the same constraints. Upgrades, in contrast, are more concentrated across the macro-levels BBB, BB, and B, with 167 occurrences, almost 90% of the cases.

| Rating levels | Downgrade | % Firms-year downgraded | Upgrade | % Firms-year upgraded | Total of changes |

|---|---|---|---|---|---|

| A | 0 | 0% | 0 | 0% | 0 |

| A- | 1 | 1% | 6 | 3% | 7 |

| BBB+ | 4 | 3% | 15 | 8% | 19 |

| BBB | 11 | 8% | 17 | 9% | 28 |

| BBB- | 8 | 5% | 29 | 16% | 37 |

| BB+ | 6 | 4% | 25 | 13% | 31 |

| BB | 7 | 5% | 21 | 11% | 28 |

| BB- | 5 | 3% | 13 | 7% | 18 |

| B+ | 7 | 5% | 20 | 11% | 27 |

| B | 13 | 9% | 14 | 7% | 27 |

| B- | 11 | 8% | 13 | 7% | 24 |

| CCC+ | 6 | 4% | 5 | 3% | 11 |

| CCC | 7 | 5% | 5 | 3% | 12 |

| CCC- | 9 | 6% | 3 | 2% | 12 |

| CC | 7 | 5% | 1 | 1% | 8 |

| C | 3 | 2% | 0 | 0% | 3 |

| D | 10 | 7% | 0 | 0% | 10 |

| Not Rated | 31 | 21% | 0 | 0% | 31 |

| Total | 146 | 100% | 187 | 100% | 333 |

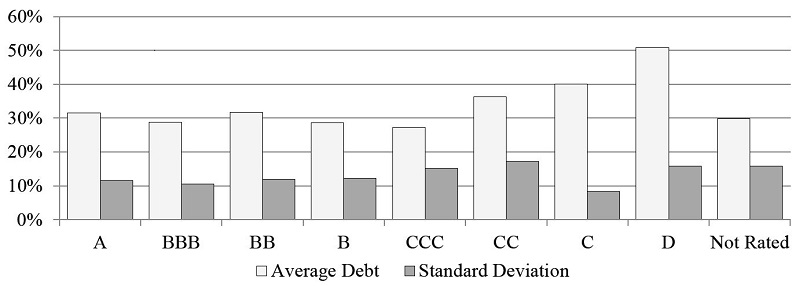

Figure 1 shows firms’ average debt and the respective standard deviation about different credit rating classifications. The result of the t-statistic confirmed that the median debt ratio of level D is higher than all the others (at 1% significance level), indicating that the firms in default are the most leveraged. In contrast, firms rated at macro-levels B and BBB presented the lowest median debt ratio levels. In the case of North American firms, illustrated in Kisgen (2006), the relation between median debt ratio and credit rating levels presented linear behavior, ranging from lower average levels for the best ratings to the highest averages for the worst ratings.

Figure 1

Average debt for broad rating

Source: Prepared by the authors.

Appendix B shows additional analyses. The higher mean debt observed before a rating downgrade could suggest leverage level as the reason for this change, given its impact on rating designation, which represents a consistent result according to the credit rating-capital structure hypothesis. However, maintenance of the same debt ratio also after downgrade suggests a different effect from that observed by Kisgen (2009), or an insufficient period for capital structure adequacy. Besides that, there is almost no change in firms’ capital structure when we segregated the overall average debt according to before (ex-ante) and after (ex-post) the rating changes (downgrade, upgrade and maintenance).

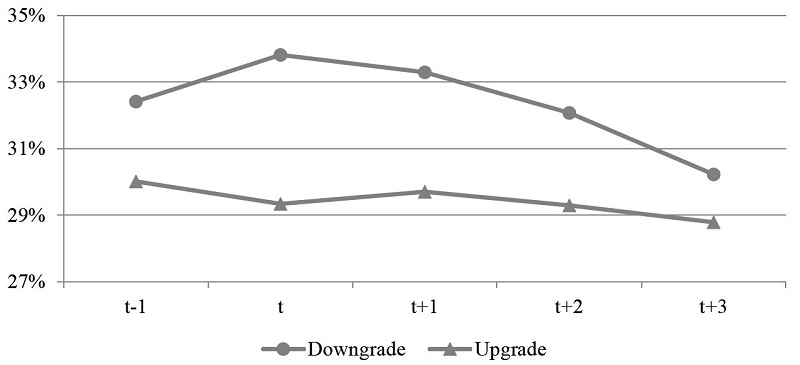

Figure 2 presents a more comprehensive perspective of debt ratio regarding to rating changes, with records of average corporate debt before, during, and after re-ratings. Interestingly, the curves suggest exactly the propositions of hypotheses H2 (reduction in leverage after a downgrade) and H3 (an upgrade does not influence the leverage). However, concerning H2, Figure 2 suggests that adjustment of debt ratio to rating downgrade requires a time interval longer than one year. Due to this characteristic, we also included the second year after a downgrade in the assessment of credit rating relevance.

Figure 2

Average debt ratio in different years (t-1, t, t+1, t+2, and t+3), before and after rating change

Source: Prepared by the authors.

Table 4 shows the average annual debt ratio variation, measured by the yearly difference of total debt as a proportion of total assets, comparatively at the moments after rating changes. Consistent with previous findings, the average annual debt ratio variation is positive in all scenarios, except for that observed after downgrades, indicating a reduction in debt ratio and agreement with hypothesis H2.

| Obs. | Average | Standard Deviation | Minimum | Maximum | |

|---|---|---|---|---|---|

| Average yearly debt variation | 1,455 | 0.0110 | 0.1085 | -2.4763 | 0.4978 |

| - Post downgrades | 137 | -0.0056 | 0.0796 | -0.3761 | 0.2025 |

| - Post upgrades | 177 | 0.0103 | 0.0829 | -0.3777 | 0.3158 |

| - Post maintenance | 1,141 | 0.0131 | 0.1148 | -2.4763 | 0.4978 |

Overall the results of this section suggest that corporate decisions are consistent with the CR-CS hypothesis (Kisgen, 2006; 2009), identified based on the following observations: (i) higher average corporate debt ratio before downgrades, (ii) subsequent gradual reduction in average debt ratio after downgrades, and (iii) predominance of capital structure decisions to reduce debt ratio after downgrades. Nevertheless, it is worth noting that the high dispersion of the average values presented requires caution in interpreting these results, which are summarized ahead together with the empirical results and statistical rigor.

4.2 Analysis of empirical results

Tables 5 and 6 summarize the estimation of the models of partial adjustment to the target leverage. The second column in Table 5 shows the results for equation (3) for the total sample, while the third, fourth, fifth, and sixth columns present the results for the base model estimated with the subsamples. The last column in Table 5 shows the results for equation (4), the base model transformed with the inclusion of the variables Downgrade and Upgrade. Table 5 presents the linear coefficient of each explanatory variable, followed by the z-statistic in parentheses. Table 6, in turn, gives the confidence interval (95%) of the lagged coefficient (β) of the Debt Ratio variable and the adjustment coefficient (λ) for each estimations just described. Note that according to the construction of the model, the adjustment coefficient is equivalent to λ = 1 – β.

| Dependent variable: Debt Ratio | ||||||

|---|---|---|---|---|---|---|

| Equation (3) | Equation (4) | |||||

| Independent variables and fit of the model | Total sample | Sub-sample: Post- downgrade 1 | Sub-sample: Post- downgrade 2 | Sub-sample: Post- upgrade | Sub-sample: Post- maintenance | Total sample |

| Downgradei,t-1 | - | - | - | - | - | 0.021 |

| - | - | - | - | - | (2.54)** | |

| Upgradei,t-1 | - | - | - | - | - | 0.004 |

| - | - | - | - | - | (0.65) | |

| Debt Ratioi,t-1 | 0.825 | 0.879 | 0.830 | 0.348 | 0.798 | 0.811 |

| (17.02)*** | (8.55)*** | (7.44)*** | (2.45)** | (10.70)*** | (16.03)*** | |

| Sizei,t-1 | 0.025 | -0.001 | 0.015 | 0.001 | 0.018 | 0.022 |

| (2.42)** | (-0.12) | (1.50) | (0.05) | (1.51) | (2.55)** | |

| GrowthOpportunityi,t-1 | 0.036 | 0.107 | 0.115 | 0.145 | 0.039 | 0.038 |

| (2.25)** | (2.16)** | (3.14)*** | (3.36)*** | (2.29)** | (2.42)** | |

| Profitabilityi,t-1 | 0.011 | -0.081 | -0.128 | 0.015 | -0.002 | 0.026 |

| (0.28) | (-0.95) | (-1.38) | (0.14) | (-0.03) | (0.71) | |

| Fixed Assetsi,t-1 | 0.024 | 0.033 | 0.128 | -0.024 | -0.006 | 0.023 |

| (0.62) | (0.35) | (1.68)* | (-0.41) | (-0.12) | (0.64) | |

| Depreciationi,t-1 | -0.568 | -0.279 | -1.608 | -0.095 | -0.579 | -0.654 |

| (-1.03) | (-0.36) | (-2.05)** | (-0.09) | (-0.84) | (-1.2) | |

| Research &Developmenti,t-1 | 1.908 | -11.248 | -6.322 | -2.456 | 2.813 | 1.466 |

| (2.51)** | (-0.68) | (-1.73)* | (-0.63) | (1.64) | (2.00)** | |

| Dummy Research &Developmenti,t-1 | -0.006 | -0.039 | 0.023 | -0.027 | -0.002 | -0.011 |

| (-0.62) | (-0.57) | (0.79) | (-0.48) | (-0.13) | (-1.18) | |

| Sectorial DebtRatioi,t-1 | 0.143 | -0.345 | -0.224 | -0.123 | 0.278 | 0.153 |

| (1.27) | (-1.01) | (-0.87) | (-0.24) | (1.24) | (1.36) | |

| Constant | -0.524 | 0.191 | -0.241 | 0.217 | -0.355 | -0.452 |

| (-2.22)** | (0.79) | (-0.87) | (0.57) | (-1.28) | (-2.26)** | |

| No. of observations | 1.358 | 137 | 130 | 177 | 1.044 | 1.358 |

| No. of instruments | 57 | 57 | 57 | 57 | 57 | 67 |

| R2 | 0.723 | 0.744 | 0.777 | 0.517 | 0.739 | 0.732 |

| Wald X2 | 715*** | 830*** | 585*** | 136*** | 294*** | 723*** |

| Test statistics (p-value): | ||||||

| AR(1) | 0.000 | 0.009 | 0.009 | 0.121 | 0.000 | 0.000 |

| AR(2) | 0.466 | 0.110 | 0,110 | 0,872 | 0,245 | 0.518 |

| Hansen | 0.803 | 0.720 | 0.721 | 0.317 | 0.248 | 0.928 |

| β | β | λ | λ | |||

|---|---|---|---|---|---|---|

| (Debt Ratioi,t-1) | (95% Conf. Interval) | (1-β) | (95% Conf. Interval) | |||

| Equation (3) | ||||||

| Total sample | 0.825 | 0.730 | 0.920 | 17.5% | 27.0% | 8.0% |

| Sub-sample: Post-downgrade 1 | 0.879 | 0.678 | 1.081 | 12.1% | 32.2% | -8.1% |

| Sub-sample: Post-downgrade 2 | 0.830 | 0.611 | 1.048 | 17.0% | 38.9% | -4.8% |

| Sub-sample: Post-upgrade | 0.348 | 0.070 | 0.626 | 65.2% | 93.0% | 37.4% |

| Sub-sample: Post-maintenance | 0.798 | 0.652 | 0.944 | 20.2% | 34.8% | 5.6% |

| Equation (4) | ||||||

| Total sample | 0.811 | 0.712 | 0.911 | 18.9% | 28.8% | 8.9% |

The coefficient of the lagged Debt Ratio indicates an average annual adjustment of approximately 17.5% (1– 0.825) of the gap between current debt ratio and target leverage (Table 6). This adjustment rate, in turn, suggests that it takes more than five years for a typical firm to eliminate this gap. This result was very near the value of 15% obtained by Flannery and Hankins (2013), which was calculated using the same estimator and specifications adopted in this study, thus suggesting similar dynamics of capital structure balancing between the firms in the United States and Latin America.

The results of Table 6 indicate a reduction in the adjustment coefficient to the level of 12% in the first year after the downgrade and a return to the level of 17% in the second year. These results represent a rejection of the hypothesis H1, which supposes an increase in adjustment speed after downgrades.

On the other hand, it is worth noting in Table 6 that the adjustment dynamics of capital structure changes only after rating downgrades (post-downgrade 1 and post-downgrade 2) when the adjustment coefficient (λ) also presents negative values in the confidence interval (95%). This result indicates a change in typical convergence, characterized by (i) decreased debt ratio with target leverage increased, or (ii) reduced target leverage with increased debt ratio. In these cases, a decrease in the adjustment coefficient indicates not only reduced adjustment speed but also the “imbalance” of the capital structure, when the current debt ratio no longer converges to the target leverage. This circumstance is consistent with the CR-CS hypothesis and is explained by Kisgen (2009) by the fact that the target leverage does not consider, in its determination, the impacts of leverage on credit rating, or the impacts of rating on fundraising conditions.

Kisgen (2009) reported a substantial increase in the adjustment speed of downgraded firms, with the annual balance ranging from approximately 35% to 63% gap reduction between current debt ratio and target leverage. However, this increase in adjustment speed is discussed by Kisgen (2009) only in the context of a subsequent reduction in the debt ratio. Under the CR-CS hypothesis, it is logical to consider an increase in adjustment speed after a downgrade if the capital structure balance is directed to a reduction of target leverage. Otherwise, considering the acquisition of resources as a first-order necessity, it would be reasonable to assume a reduction in adjustment speed towards capital structure balance, given the more restrictive conditions arising from the post-downgrade period.

Our results indicate a substantial increase in the adjustment speed towards capital structure balance after a rating upgrade when the adjustment coefficient switches to the level of 65% gap reduction between current and desired debt levels (Table 6). The benefits of a rating upgrade could provide a favorable period for capital structure adjustments, as long as these benefits outweigh the transactional costs, as discussed in Kisgen (2009).

In the case of firms whose ratings remained unaltered the previous year, the adjustment coefficient indicates an average annual reduction of 20% in the gap between the current debt ratio and target leverage. The confidence interval (95%) of the adjustment coefficient remains positive (Table 6), reinforcing the indication that the target leverage influences the capital structure balance of firms in the Latin American countries. However, a rating downgrade does not accelerate the speed of adjustment to the target, as predicted by the CR-CS hypothesis, contrary to the findings of Hovakimian et al. (2009) and Michelsen and Klein (2011) that firms target minimum rating levels.

Re-rating impact on the subsequent debt ratio is presented in the last column of Table 5, which shows the result of the base model with the inclusion of Downgrade and Upgrade, (equation 4). The coefficient of Upgrade (Φ2 = 0.004) is not significant, confirming hypothesis H3 that a credit rating upgrade does not influence subsequent changes in the capital structure. The coefficient of Downgrade (Φ1 = 0.021), however, indicates an increase of about 2% in debt ratio, as a percentage of the total assets, after a downgrade (at 5% statistical significance). We reject hypothesis H2, as rating downgrade does not imply a subsequent reduction in the debt ratio.

Considering that the response time to downgrade may be longer than one year (see Figure 2), the results of the same estimation with two and three lags of Downgrade variable presented non-significant results (unreported). Moreover, the presence of the lagged dependent variable among the regressors was controlled as the coefficient of Downgrade was also estimated directly in the target leverage model. The result reinforces the evidences of a subsequent increase in debt ratio, of approximately 1.4% (at 10% significance).

Our results are similar to Kemper and Rao (2013) that firms issue more debt after rating downgrades, although it contradicts Kisgen (2009). According to Kemper and Rao (2013), this behavior could indicate that the acquisition of these resources is a firm’s first-order necessity, justifying their raising even in worse conditions.

The absence of others funding sources or the most significant benefit of not target minimum rating levels (compared to the cost) explain such responses to rating changes, where the embryonic stage of development of financial markets (such as the capital market) in Latin America could cause more dependence on the banking system as a funding source (Wojewodzki, Poon & Shen, 2017). These findings may also reflect the lower level of credit rating concern among Latin American managers compared with that of North American managers (Maquieira, Preve & Sarria-Allende, 2012).

The models proposed by Kisgen (2009, 2006) that gave rise to the CR-CS hypothesis are limited to explain why credit rating in Latin America does not impact the capital structure as in developed countries. Institutional characteristics such as bank-oriented financial system and the economic uncertainty of the Latin American countries affect not only the debt structure but also the credit rating changes (Michelsen & Klein, 2011). Therefore, the next step is to elaborate on a model that considers these aspects. Although the evidence is not in agreement with the CR-CS hypothesis' propositions, in consonance with Rogers et al. (2016) and Rogers et al. (2013), our results indicate that credit rating changes influence Latin American firms’ capital structure, but its effects are not associated with the maintenance of certain rating levels.

5 CONCLUSION

Although credit ratings prevail in financial markets and are assigned to practically all firms issuing bonds, and have recognized the importance attributed by most observers of these markets, the economic and financial literature still in doubt about their significance and informational content. In this respect, ratings are often neglected in studies of determinants of capital structure (see Huang & Shen, 2015), and rarely investigated in emerging markets context (e.g., Rogers et al., 2016). There is still no consensus on the influence of credit ratings (and their changes) on firms’ capital structure.

This study identified that rating changes have an impact on capital structure of Latin American firms, but not according to the CR-CS hypothesis. We found that a downgrade rating does not accelerate the speed of adjustment to the target capital structure, and downgraded firms do not promote a subsequent reduction in the debt level compared with non-downgraded firms. The downgraded firms remain more indebted than non-downgraded firms do after a credit rating downgrade.

However, some of the CR-CS hypothesis prevail for Latin America. The reduction in adjustment speed observed after downgrades, initially not expected, is consistent with the CR-CS hypothesis when conditioned to a subsequent increase in the debt ratio. As expected, the occurrence of rating upgrades does not influence the following debt ratio level, despite the substantial increase observed in adjustment speed towards target leverage. Conceptual precepts of credit rating are also verified, i.e., the higher median debt ratio associated with the worst rating levels and before downgrades, consistent with the possibility that this is the reason for reclassification. We raise the need for a model that contemplates characteristics of the Latin American region related to the financial and economic system.

Therefore, Latin American firms do not adjust their capital structure to maintain certain rating levels. Therefore, Latin American firms do not target minimum rating levels, since the acquisition of resources is a first- order necessity.

REFERENCES

Agha, M., & Faff, R. (2014). An investigation of the asymmetric link between credit re-ratings and corporate financial decisions: “Flicking the switch” with financial flexibility. Journal of Corporate Finance, 29, 37-57. DOI: https://doi.org/10.1016/j.jcorpfin.2014.08.003

Arellano, M., & Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of Econometrics, 68(1), 29-51. DOI: https://doi.org/10.1016/0304-4076(94)01642-D

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115-143. DOI: https://doi.org/10.1016/S0304-4076(98)00009-8

Cornaggia, K. J., Krishnan, G. V., & Wang, C. (2017). Managerial Ability and Credit Ratings. Contemporary Accounting Research, 34(4), 2094-2122. DOI: https://doi.org/10.1111/1911-3846.12334

Fama, E. F., & French, K. R. (2002). Testing Trade-Off and Pecking Order Predictions about Dividends and Debt. Review of Financial Studies, 15(1), 1-33. DOI: https://doi.org/10.1093/rfs/15.1.1

Fávero, L. P. (2015). Análise de dados: Modelos de Regressão com Excel®, Stata® e SPSS®. 1st. Ed. Rio de Janeiro: Elsevier, 504p.

Flannery, M. J., & Hankins, K. W. (2013). Estimating dynamic panel models in corporate finance. Journal of Corporate Finance, 19, 1-19. DOI: https://doi.org/10.1016/j.jcorpfin.2012.09.004

Flannery, M. J., & Rangan, K. P. (2006). Partial adjustment toward target capital structures. Journal of Financial Economics, 79(3), 469-506. DOI: https://doi.org/10.1016/j.jfineco.2005.03.004

Fracassi, C., Petry, S., & Tate, G. (2016). Does rating analyst subjectivity affect corporate debt pricing? Journal of Financial Economics, 120(3), 514-538. DOI: https://doi.org/10.1016/j.jfineco.2016.02.006

Freitas, A. P. N., & Minardi, A. M. A. F. (2013). The impact of credit rating changes in Latin American stock markets. BAR - Brazilian Administration Review, 10(4), 439-461. DOI: https://dx.doi.org/10.1590/S1807- 76922013000400005

Graham, J. R., & Harvey, C. R. (2001). The theory and practice of corporate finance: evidence from the field. Journal of Financial Economics, 60(2–3),187-243. DOI: https://doi.org/10.1016/S0304-405X(01)00044-7

Hovakimian, A., Kayhan, A., & Titman, S. (2009). Credit Rating Targets. SSRN Electronic Journal, 1-37. DOI: http://dx.doi.org/10.2139/ssrn.1098351

Huang, Y.-L., & Shen, C.-H. (2015). Cross-country variations in capital structure adjustment - The role of credit ratings. International Review of Economics & Finance, 39, 277–294. DOI: https://doi.org/10.1016/j. iref.2015.04.011

Kemper, K. J., & Rao, R. P. (2013). Credit Watch and Capital Structure. Applied Economics Letters, 20(13), 1202- 1205. DOI: https://doi.org/10.1080/13504851.2013.799746

Kisgen, D. J. (2006). Credit Ratings and Capital Structure. The Journal of Finance, 61(3), 1035-1072. DOI: https://doi.org/10.1111/j.1540-6261.2006.00866.x

Kisgen, D. J. (2009). Do Firms Target Credit Ratings or Leverage Levels? Journal of Financial and Quantitative Analysis, 44(6), 1323-1344. DOI: https://doi.org/10.1017/S002210900999041X

Maquieira, C. P., Preve, L.A., & Sarria-Allende, V. (2012). Theory and practice of corporate finance: Evidence and distinctive features in Latin America. Emerging Markets Review, 13(2), 118-148. DOI: https://doi. org/10.1016/j.ememar.2011.11.001

Michelsen, M., & Klein, C. (2011). The Relevance of External Credit Ratings in the Capital Structure Decision- Making Process. SSRN Electronic Journal, 1-53. DOI: http://dx.doi.org/10.2139/ssrn.1960699

Myers, S. C. (2001). Capital Structure. The Journal of Economic Perspectives, 15(2), 81-102. DOI: https://doi. org/10.1257/jep.15.2.81

Nickell, S. (1981). Biases in dynamic models with fixed effects. Econometrica, 49(6), 1417-1426. DOI: https:// doi.org/10.2307/1911408

Rogers, D., Mendes-da-Silva, W., & Rogers, P. (2016). Credit Rating Change and Capital Structure in Latin America. Brazilian Administration Review, 13(2), 1-22. DOI: http://dx.doi.org/10.1590/1807-7692bar2016150164

Rogers, D., Mendes-da-Silva, W., Neder, H. D., & Silva P. R. (2013). Rating de Crédito e Estrutura de Capital: Evidências da América Latina. RBFin - Brazilian Review of Finance, 11(3), 312-341. Available at: http:// bibliotecadigital.fgv.br/ojs/index.php/rbfin/article/view/4194

Standard & Poor’s Rating Services. (2014). Guide to Credit Rating Essentials – What are credit ratings and how do they work? 19p. McGraw Hill Financial. Available at: https://www.spratings.com/documents/20184/760102/ SPRS_Understanding-Ratings_GRE.pdf/298e606f-ce5b-4ece-9076-66810cd9b6aa. Access on: August 29, 2018.

Wojewodzki, M., Poon, W. P. H., & Shen, J. (2017). The role of credit ratings on capital structure and its speed of adjustment: an international study. The European Journal of Finance, 24(9), 735–760. DOI: https://doi. org/10.1080/1351847X.2017.1354900

Appendix A

Distribution of ratings changes (downgrades and upgrades) by country and sector

Appendix B

Distribution of ratings changes (downgrades and upgrades) by country and sector

Notes

Author notes

Corresponding Author: Phone: +55 (16) 3315-9027 E-mail: tbpaschoal@gmail.com (T. B. Paschoal); matheusgomes@usp.br (M. da C. Gomes); marvalle@usp.br (M. R. do Valle) Universidade de São Paulo, Faculdade de Economia Administração e Contabilidade de Ribeirão Preto. Av. dos Bandeirantes, 3900 - Monte Alegre - Ribeirão Preto/SP -14040-900, Brasil.