Article

Evidence of the impact of religiosity on earnings management in Brazil

Evidências do impacto da religiosidade no gerenciamento de resultados no Brasil

Simone Miranda dos Santos

Sirlei Lemes

Neirilaine Silva de Almeida

Simone Miranda dos Santos

Sirlei Lemes

Neirilaine Silva de Almeida

Evidence of the impact of religiosity on earnings management in Brazil

Revista de Contabilidade e Organizações, vol. 16, e186587, 2022

University of São Paulo

Received: 05 June 2021

Accepted: 20 April 2022

Published: 24 July 2022

Abstract: The international literature points to evidence of the relationship between religiosity and the types of earnings management in countries that do not adopt the International Financial Reporting Standards. Therefore, the aim of the study is to investigate the association between religiosity and earnings management, in a country that adopts international standards. The earning management was estimated by the accruals and the real activities for a sample of 122 companies listed in Brasil, Bolsa, and Balcão in the period from 2010 to 2017. Religiousness corresponded to the percentage of people who declared to have a religion in the municipality where the company is headquartered. Through regression by the Ordinary Least Squares method, with panel data, it was verified that religiosity is negatively associated with accrual earnings management and positively associated with real earnings management. This result can be explained by risk aversion, a social norm used in the literature to characterize religious people. In religious environments, and therefore with a greater aversion to risk according to this literature, the manager would tend to use more real earnings management than accrual earnings management due to the risk of detection by auditors and regulatory bodies. This research contributes to the expansion of the understanding of the determinants of accounting quality, under the aspect of earnings management as well as the development of research on earnings management by pointing to religiosity as an additional variable in the theoretical models. The measure of religiosity is a limitation of the study, as the respondents' statements may differ from practice, and also the measure is subject to variations by neighborhood or region, in companies located in larger cities.

Keywords: Accruals discretionary, Real activities, Risk aversion, Social Norm Theory.

Resumo: A literatura internacional aponta evidências da relação entre religiosidade e os tipos de gerenciamento de resultados em países não adotantes das International Financial Reporting Standards. Diante disso, o objetivo do estudo é investigar a associação entre a religiosidade e o gerenciamento de resultados, em um país adotante das normas internacionais. O gerenciamento de resultados foi estimado por meio dos accruals e das atividades reais para uma amostra de 122 companhias listadas na Brasil, Bolsa, Balcão no período de 2010 a 2017. A religiosidade correspondeu ao percentual de pessoas que declararam possuir religião no município da sede da empresa. Por meio de regressão pelo método Ordinary Least Squares, com dados em painel, verificou-se que a religiosidade está negativamente associada ao gerenciamento de resultados por meio dos accruals e positivamente associada ao gerenciamento de resultados por meio das atividades reais. Esse resultado pode ser explicado pela aversão ao risco, norma social utilizada na literatura para caracterizar os religiosos. Em ambientes religiosos, portanto com maior aversão ao risco segundo essa literatura, o gestor tenderia a utilizar mais o gerenciamento de resultados por meio das atividades reais e menos gerenciamento de resultados por meio dos accruals em função do risco de detecção por auditores e órgãos reguladores. A pesquisa contribui com a expansão do entendimento dos aspectos delineadores da qualidade da informação contábil, sob a vertente do gerenciamento de resultados, bem como incrementa as pesquisas sobre gerenciamento de resultados, ao indicar a religiosidade como variável adicional nos modelos. A medida de religiosidade é uma limitação do estudo, pois a declaração dos respondentes pode diferir da prática e a medida também está sujeita a variações por bairro ou regiões, em empresas localizadas em municípios maiores.

Palavras-chave: Accruals discricionários, Atividades reais, Aversão ao risco, Teoria das Normas Sociais.

1 INTRODUCTION

Researchers have made efforts to identify how economic and institutional factors, as well as the personal characteristics of managers, can explain outcome management. However, social factors, such as religiosity, can also affect the management of results, since religion is an important social norm that exercises control over beliefs and behaviors (Kennedy & Lawton, 1998). Otherwise, earnings management is a mechanism of manipulation resulting from the decisions and actions of managers, and these decisions and actions can be influenced by religious norms (Kennedy & Lawton, 1998).

The Social Norm Theory suggests that executives, who may or may not be religious, are influenced by the religious norms of the population (Grullon, Kanatas & Weston, 2009; Dyreng, Mayew & Williams, 2012; McGuire et al., 2012). The greater the religiosity understood as the strength of religion, the greater the influence of religious norms on the decisions of individuals (Bjornsen, Do & Omer, 2019). Therefore, the greater the reflection of these norms, transmitted by the actions of individuals, in the social environment. It is these religious norms that can influence managers' decisions regarding earnings management.

The earnings management through accrual earnings management (AEM) occurs when the manager manipulates the results through accounting choices (Paulo, 2007). The earnings management from real activities (Real Earnings Management - REM) arises from the operational decisions of managers (Roychowdhury, 2006). Both methods result from managers' decisions, but the first is related to accounting standards and the second to business practice.

A positive association between religiosity and REM is evidenced. A negative association between religiosity and AEM suggests that companies based in more religious regions use less AEM and more REM (McGuire et al., 2012; Cai, Li & Tang, 2018). However, these studies were conducted in countries that did not compulsorily adopt International Financial Reporting Standards (IFRS) such as the United States and China. Your adoption can affect the way the manager chooses earnings management, as the flexibility of principled standards provides greater opportunity for opportunistic behavior. In Brazil, the adoption of IFRS began in 2008 and triggered the migration of the AEM level to the REM (Cupertino, Martinez & Costa Jr, 2017). Although this adoption affects the way results are managed, no evidence of the relationship between religiosity and earnings management methods in countries that adopted IFRS was identified.

In addition to the adoption of IFRS, Brazil differs from the countries analyzed in previous studies (McGuire et al., 2012; Cai, Li & Tang, 2018) compared to other factors. According to World Bank (2021), the number of national companies listed in 2017 in Brazil (335 companies) is lower than in China (3,485 companies) and the United States (4,336 companies). It is still possible to verify, according to the same body, lower annual growth of Gross Domestic Product (Brazil: 1.3229%, China: 6.9472%, and the United States: 2.3327%). The high school completion rate in 2012 in Brazil and China was 65% and 55%, respectively, while in the United States it was 91% in 2013 (World Bank, 2021). These data show differences in the capital market, in the growth of the economy and in the level of education of countries.

Considering the literature presented that indicates the relationship between religiosity and accounting, the following research problem is: what is the association of religiosity with the earnings management accruals-based and real-activities? Therefore, the aim of this study is to investigate the association between religiosity and earnings management accruals-based and real-activities.

There is little consensus in the literature on the determinants of earnings management (Callen, Morel & Richardson, 2011). Identifying factors that may influence the decision of managers is relevant to the effect of these decisions on accounting results, the main metric to evaluate the company's performance (Graham, Harvey & Rajgopal, 2005). In addition, investigations focused on only one method of managing results are not able to capture the entire effect of earnings management (Fields, Lys & Vincent, 2001; Cupertino et al., 2017). Thus, studies that consider both earnings management methods have the potential to generate more robust and complete results.

Earnings management is not related to religiosity or religious denomination at the country level, suggesting the need for investigations at the micro-level (Callen et al.,2011). McGuire et al. (2012), Cai et al. (2018), Grullon et al. (2009) and Du, Jian, Lai, Du & Pei (2015) investigated this relationship at the micro level, but in countries that did not adopt IFRS. The present study complements the previous findings by identifying the relationship between the two forms of earnings management and religiosity at the micro level, in a country that adopted these standards.

Identifying how religious social norms influence the behavior of managers and their relationship with earnings management contributes to improving the decision model of investors, allowing a better assessment of the entity's situation. To achieve the goal, two measures of earnings management were estimated. Regression was used for the treatment of data by the Ordinary Least Squares method, for the period from 2010 to 2017, and a sample of Brazilian publicly held companies. The results indicated that religiosity is negatively associated with AEM and positively associated with REM and, thus, the research hypotheses could not be rejected.

2 THEORETICAL FRAMEWORK

2.1 Earnings management and religiosity

Earnings management is identified when there is a purposeful change in accounting results to achieve particular objectives (Martinez, 2001) and can occur through AEM or REM. The AEM derives from the accrual method, which allows modifying the time of the reported profit, without direct consequences on cash flow (Roychowdhury, 2006). Managers can also manage the result through operational decisions. The REM occurs when the manager performs deviations from normal operational practices, motivated by the demonstration of the achievement of goals (Roychowdhury, 2006).

The decision of the manager to manage results can be influenced by religious norms (McGuire et al., 2012). The Theory of Social Norms postulates that individuals will act in a way that fits the behavioral norms of the groups with which they associate (Dyreng et al., 2012). It is presumed that executives live in the vicinity of corporate headquarters, so the degree to which undesirable management behavior is tolerated by a company may be a reflection of community values (Grullon et al., 2009).

The manager does not need to be an active participant of any religion, because only the interaction with religious individuals exposes executives to rules and standards understood by a social group (Dyreng et al., 2012). The manager who lives with more religious people has a greater influence of religious beliefs, which can induce decision-making (McGuire et al., 2012; Dyreng et al., 2012). It is the religious environment in one area, not the personal religious belief of a chief executive officer (CEO), which affects accounting conservatism (Ma, Zhang, Gao & Ye, 2020). Earnings management and accounting conservatism are two interrelated topics on the quality of accounting information (Ma et al., 2020).

Religious norms affect managers' decisions on how to manage the result through risk aversion (Cai et al., 2018). Religious individuals exhibit a more risk-averse behavior compared to non-religious individuals (Miller & Hoffmann, 1995). The relationship between religiosity and risk aversion is justified because risk-averse individuals seek religion to try to reduce uncertainty in their lives (Hilary & Hui, 2009), and is also a social norm used to characterize religious individuals (Dyreng et al., 2012).

Risk aversion refers to the tendency to avoid the worst situation, and this worst situation, when it comes to earnings management, is that is detected (Cai et al., 2018). Auditing contributes to the detection of earnings management by reducing AEM, without minimizing REM (Martinez, 2011). As much as the auditor can assume the company's policies, he cannot question the actions taken in the normal course of business (Graham et al., 2005), that is, operational decisions are controlled by the manager and cannot be challenged by auditors (Gunny, 2005).

The AEM presents a higher risk of scrutiny by the Securities and Exchange Commission (SEC) (Gunny, 2005; Roychowdhury, 2006), which increases the likelihood of detection. Therefore, The REM is considered the safest way to manage profits in the presence of auditors and regulatory bodies because it is more difficult to detect (Cai et al., 2018; Gunny, 2005; Roychowdhury, 2006; Graham et al., 2005). Thus, managers in more religious areas, therefore more risk-averse, are likely to prefer the REM when compared to the AEM.

2.2 Previous studies

There is evidence of a negative association between religiosity and AEM, measuring local religiosity by the per capita number of adherents of a religious denomination and by the per capita number of churches (Grullon et al., 2009), through answers to three questions related to the existence of religious affiliation, the importance of religion and the weekly attendance to cults (McGuire et al., 2012), by the distance between the religious temples and the company's headquarters (Du et al., 2015) and the number of religious installations around the company's headquarters (Cai et al., 2018).

The results suggest that the religiosity of the community around the company is a significant factor in the decision to manage results and that religiosity can mitigate the AEM, due to the higher risk of detection, when compared to the REM, which underlies the first hypothesis:

H1: religiosity is negatively associated with the accruals-based earnings management.

McGuire et al. (2012) and Cai et al. (2018) identified a positive association between religiosity and REM, which means that greater religiosity results in greater REM. This is because REM is less likely to be detected compared to AEM. Thus, the second hypothesis is postulated:

H2: religiosity is positively associated with the real-activities earnings management.

3 METHODOLOGY

3.1 Data collection and sampling

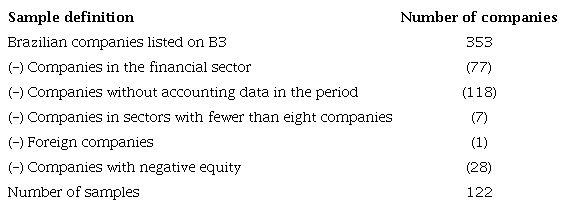

Table 1 presents the selection of the companies in the sample.

The initial sample (Table 1) was composed of companies listed in B3. Financial companies were excluded because they prepare financial statements under specific rules and also because the indebtedness index, used in this study as a control variable, is different for this sector, making it impossible to compare with other sectors. Also excluded were: a) companies in sectors with fewer than eight companies, a procedure necessary because the regressions were calculated by sector and year; b) a foreign company, due to the absence of religiosity data and some control variables and; c) companies with negative equity since they could distort the value of some indicators.

The period studied covered the years 2010 to 2017. The initial data for 2010 were due to the year of the last demographic census in Brazil. However, accounting data were collected from 2008 to calculate earnings management, which depends on information from two previous years. The research period was until 2017, the date of data of the last GDP per municipality, on the date data collection.

3.2 Research variables

The data for the calculation of the earnings management were collected in Economatica® and refer to the consolidated financial statements. For the calculation of the AEM, the total accruals were initially calculated by the cash flow approach. This approach was chosen because it presented less error in the measurement of accruals and because it is the most prudent choice (Hribar & Collins, 2002).

Discretionary accruals were estimated by the Kothari Model, Leone & Wasley (2005), which is the Modified Jones model with the inclusion of the intercept and the return on the asset (Dechow, Sloan & Sweeney, 1995; Kothari et al., 2005). The inclusion of the constant term (intercept) helps in the control of heteroskedasticity and the inclusion of return on assets contributes to controlling the company's performance (Kothari et al., 2005). Non-discretionary accruals were obtained by Equation 1.

Where: Ai,t-1 is the total asset of the company i of the period t-1; The ∆Ri,t is the change in net revenues of company i of the period t-1 to period t; PPEi,t is the balance of fixed assets (gross) of company i at the end of period t; ROAi,t is the return on company asset i in period t; ∆CRi,t is the change in the receivables (net) of company i in the period t-1 for period t; NDAi,t are the non-discretionary accruals of the company i in the period t.

Discretionary accruals would supposedly be artificial and would aim to manipulate accounting results and thus can be used as a measure for AEM. These accruals are measured by the difference between total accruals and non-discretionary accruals. The values in module were considered, and the farther from zero (positive or negative values), the higher the level of AEM.

Management measures based on real activities were calculated according to the Roychowdhury model (2006). The abnormal level of discretionary expenditure (AB_DISC), the cost of production (AB_PROD) and cash flows of operating activities (AB_CAHS) were estimated as the residues of the regressions presented in Equations 2, 3 and 4, respectively.

Where: Ai,t-1 is the total asset of the company i of the period t-1; Ri,t is the net revenue of company i in period t; Ri,t-1 is the net revenue of company i in the period t-1; ∆Ri,t is the change in net revenues of the company i from period t-1 to period t; ∆Ri,t-1 is the change in net revenues of the company i from period t-2 to period t-1; ∆Ei,t is the change in company i inventories from period t-1 to period t; DESPDISCi,t represents the operating expenses of the company i in period t; PRODi,t is the sum of the CPV with ∆Ei,t; CFOi,t is the operating cash flow of company i in period t.

REM is calculated according to Equation 5. The farther away from zero (positive or negative values) the REM, the higher the management level.

If companies manage results up they will likely have one or all of these effects: exceptionally low AB_CAHS and/or AB_DISC, and/or exceptionally high AB_PROD (Cohen, Dey & Lys, 2008). Thus, AB_DISC and AB_CAHS were multiplied by -1 so that higher values represented greater management, consistent with McGuire et al. (2012).

The variable Religiosity refers to that of the population around the company. The location of the company's headquarters was considered similar to Ma et al. (2020). This location was identified in the registration form, available on the B3 website. Data on religiosity by the municipality were obtained from the IBGE System of Automatic Recovery. Religiosity is measured by the percentage of people in the municipality who declare to have one or more religions (Ma et al., 2020).

The control variables, which characterize the population around the company, were based on McGuire et al. (2012) and Du et al. (2015). Densely populated areas may have more influential religious facilities (Cai et al., 2018) and, as a result, it is possible that the effects of religiosity on earnings management are more intense. The variable Population corresponds to the number of residents in the municipality.

It is possible that the Brazilian black population finds it difficult to speak and be heard (Caetano, 2018). The lack of opportunity for blacks to manifest and be heard is even greater in the context of populations with a significant number of black women (Caetano, 2018). In addition, black women also encounter greater difficulties in the business area (Jackson, 2020). Therefore, it is reasonable to assume that in environments with a higher rate of blacks the influence of religiosity in the earnings management is lower since this population would have difficulties in speaking and being heard. The variable Racial Composition was formed from the percentage of people from the municipality who declared to have black color. The variables Population and Racial Composition were obtained through the IBGE System mentioned.

Huang, Rose-Green and Lee (2012) documented a positive association between the age of the CEO and the quality of financial information, suggesting that older individuals are more conservative. According to Campara, Vieira, Bender Filho and Coronel (2017) the higher the level of education and income of individuals, the greater the risk tolerance. This behavior can be explained by the perception of financial security. Thus, it can be conjectured that an older population expresses more conservative social norms, and can contribute to reducing the earnings management. Hence, a population with higher income and education, therefore with greater acceptance of risks, leads to greater earnings management.

The development of the municipality was based on the Municipal Human Development Index, which ranges from zero to one and the closer to one, the greater the human development (PNUD Brasil, 2020). Longevity (opportunity to live a long and healthy life) was evaluated by the Municipal Human Development Index of Longevity. Income (possibility of obtaining a standard of living that guarantees basic needs) was measured by the Municipal Human Development Index of Income. Education (access to knowledge) was measured by the Municipal Human Development Index of Education. These variables were obtained from the PNUD Brazil website.

Companies located outside metropolitan areas are less likely to be involved in earnings management when compared to those in metropolitan areas (Urcan, 2007). Thus, a Metropolis variable was created with the dummy equal to one for companies located in metropolitan areas and zero for the otherwise (Urcan, 2007; Dyreng et al., 2012). The identification of metropolitan areas was performed according to the classification also available in the IBGE System.

In poor economic conditions, there is greater earnings management (Cohen et al., 2008). On the other hand, McGuire et al. (2012) identified that greater economic development is associated with greater earnings management. In view of this, Economic Development was controlled in the model through the variation of gross domestic product. The Gross Domestic Product of the municipalities was also obtained from the IBGE System.

The internal environment was controlled through the characteristics of the firm. Companies with high debt ratios tend to manage results to report higher profits (Consoni, Colauto & Lima, 2017). Thus, the variable Level of Indebtedness was included in the model.

Larger companies are involved in more earnings management (Du et al., 2015) because they are more exposed to the investor market, generating greater pressure on managers to achieve specific objectives. Thus, the Company Size was included in the model through the natural logarithm of the company's total assets at the end of the year.

Previous studies have documented a negative relationship between the types of earnings management and the return on the asset. This relationship can occur because managers, when determining a poor financial-economic performance, manage the results to perform better (Joia & Nakao, 2014; Cupertino et al., 2016). The Return on assets was used to control the company's performance.

The auditing firms known as Big Four (KPMG, Deloitte, Ernest. & Young and Pricewaterhouse) contribute to mitigating the AEM (Silva et al. 2014), but without impact on the REM (Sena, Dias Filho & Moreira, 2020). In the model, the presence of large Big Four auditing companies is a dummy variable that takes the value one when the audit is a Big Four and zero otherwise. The audit data were obtained year by year from Thomson Reuters® and, when not available, the reference form was consulted on the B3 website.

Corporate governance is an alternative means that can minimize the practice of earnings management (Martinez, 2001). In other words, corporate governance mechanisms behave like inhibitors of earnings management (Barros, Soares & Lima, 2013). Corporate Governance was controlled through a dummy variable that assumes a value for companies listed at the differentiated levels of corporate governance (Level 1, Level 2, and New Market) and zero otherwise, with data collected per year.

3.3 Data processing

For the treatment of outliers, the winsorization technique was used, with all variables winsorized at the level of 99%. Regression was performed by the Ordinary Least Squares method, with panel data. The Hausman Test was used to determine the use of fixed-effects or random-effects estimators. According to Gujarati and Porter (2011), this decision can significantly affect data analysis, since the (regression) model of random effects includes random intercept extraction in a larger population and the fixed-effect (regression) model does not. In this context, concerning accrual management, the Hausman Test indicated random effects (p-value: 0.2335). With regard to management by real activities, the Hausman Test indicated fixed effects (p-value: 0.0001). The assumptions of normality, homogeneity and autocorrelation were verified and, as they were not met, a correction was made through robust standard errors, minimizing the problems of heteroscedasticity and autocorrelation. Multicollinearity was verified by the variance inflation factor and the results indicated the presence of collinearity. The regression model is presented in Equation 6.

Results Management = β0 + β1 Religiousness + β2 Population +β3 Racial Composition + β4 Longevity + β5 Income + β6 Education + β7 Metropolis + β8 Economic Development + β9 Level of Indebtedness + β10 Company Size + β11 Return on Asset + β12 Big Four + β13 Corporate Governance + ɛ

In the proposed model, the dependent variable alternatively represents one of two types of earnings management.

4 RESULTS AND ANALYSIS

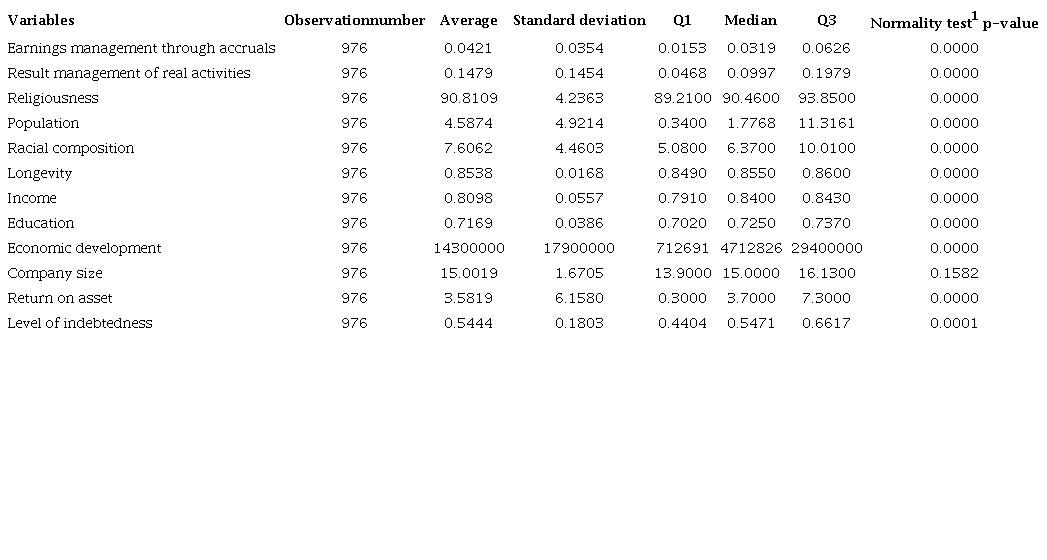

Tables 2 and 3 report descriptive statistics of the study variables, winsorized at 99%.

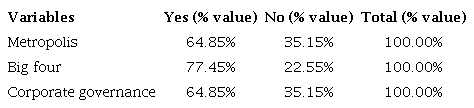

Descriptive statistics (Table 2) suggest that companies use REM more. When comparing the medians of the religiosity variable in Brazil, identified in this study, with those of the United States obtained in McGuire et al. (2012), it is possible to observe that the levels of religiosity in Brazil are higher, which may suggest a scenario with a greater possibility of influence of religious social norms in the decision of managers. Table 3 presents descriptive statistics for qualitative variables.

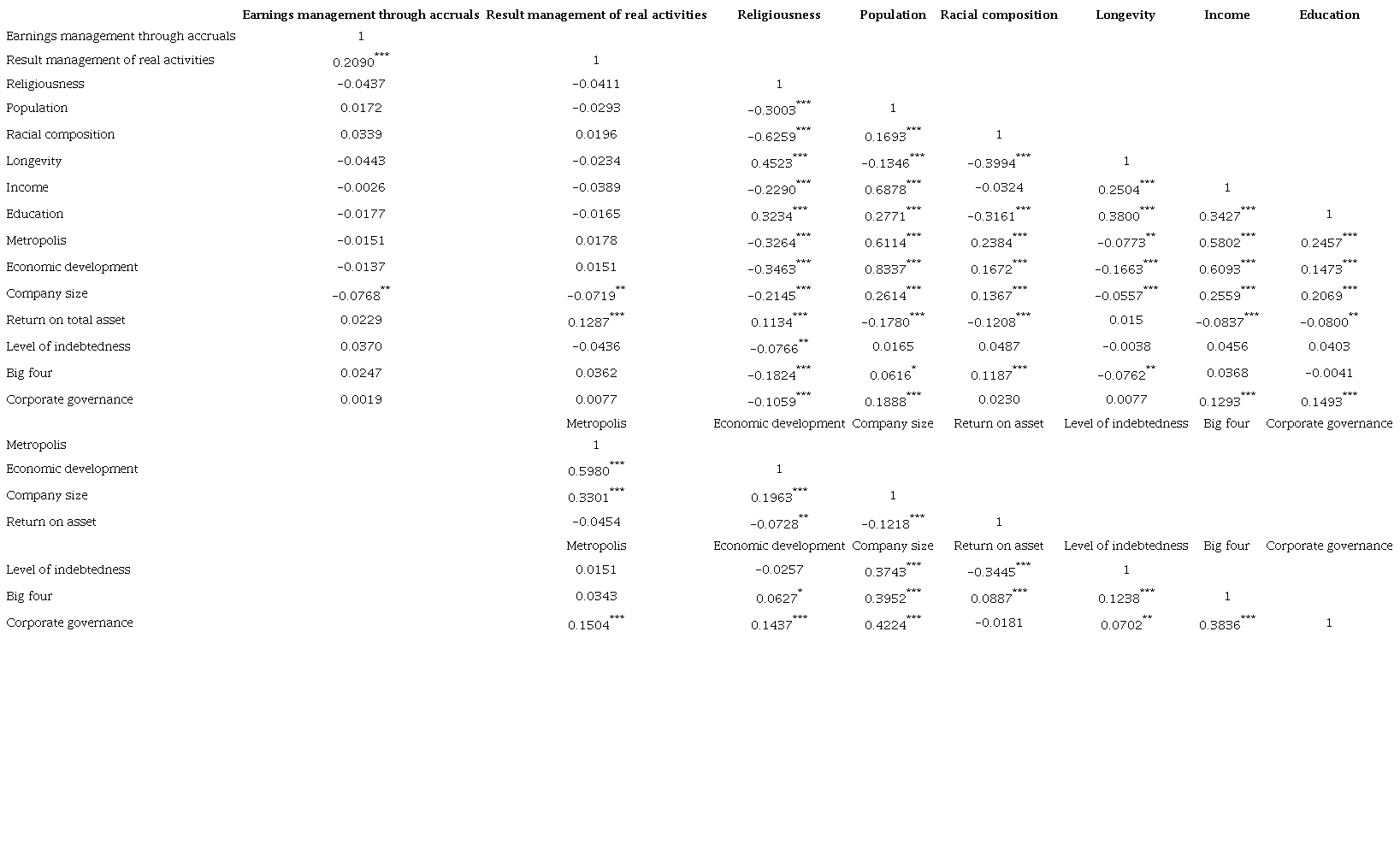

The results indicate (Table 3) that most companies were audited by the Big Four, evidence aligned with that identified by McGuire et al. (2012). The correlation matrix between the variables is reported in Appendix A. The values were calculated by Spearman's method, except for the Variable Company Size, which presents a normal distribution and the correlation was estimated by Pearson's method.

The low correlation between REM and AEM confirms that these measures capture different types of earnings management. According to the correlation matrix, Religiosity is negatively correlated with population, racial composition, income, metropolis, and economic development and positively correlated with Longevity and Education, which evidences the importance of controlling demographic characteristics, as emphasized by McGuire et al. (2012).

Regarding the correlations of the types of earnings management and control variables at the company level, a negative and significant correlation was identified between AEM and REM with the Size of the Company, suggesting that larger companies engage in less management, a result contrary to that identified by Du et al. (2015). Additionally, a positive correlation was found between REM and Return on Assets, indicating that more profitable companies tend to use this type of management, a result different from that evidenced by Cupertino et al. (2016).

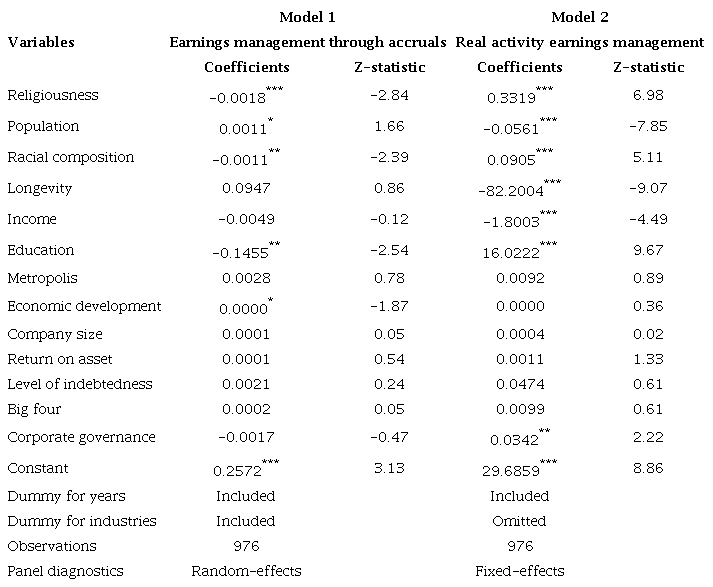

The correlation coefficients between the control variables are generally low, inflaming that the inclusion of these variables in the regression model does not strongly incur a multicollinearity problem. Table 4 displays the results for the proposed regression model.

The results of Model 1 (Table 4) show a significantly negative relationship between Religiosity and AEM (p-value < 0.01), which suggests that religiosity is capable of reducing this type of management. This finding confirms the results of Grullon et al. (2009), McGuire et al. (2012), Du et al. (2015) and Cai et al. (2018). Model 2 reveals a significantly positive relationship between Religiosity and REM (p-value < 0.01) indicating that the higher the religiosity, the higher the REM. These results are in in line with the evidence of McGuire et al. (2012) and Cai et al. (2018) and indicate that managers may be aware that a more religious population has less tolerance for the adoption of unethical practices and, therefore, can mitigate the earnings management by accruals (AEM), which is more easily identified, and prioritize the earnings management by real activities (REM).

The variables used to control the environment around the company that was significant in Model 1 were Population, Economic Development, Racial Composition and Education and, in Model 2, were Racial Composition, Education, Population, Longevity and Income, demonstrating the relevance of environmental characteristics in earnings management practices. It is pertinent to highlight that the results of the research are not convergent with the findings of Du et al. (2015), since, in their study, the variables of Population, Racial Composition, Education, Longevity and Income did not present statistical significance. This lack of convergence between the results of studies that explore the relationship between demographic characteristics and earnings management corroborates the arguments of researchers (Hilary & Hui, 2009; McGuire et al., 2012) who argue that the relationship between the variables that characterize the environment around the company and accounting information is still unclear and, consequently, needs to be further explored. Finally, it is noted that the positive relationship between The AEM and economic development supports the findings of McGuire et al. (2012).

Regarding control variables at the company level, a positive and significant relationship was identified between REM and Corporate Governance, suggesting that corporate governance is not able to minimize this type of management. The positive relationship between The REM and Corporate Governance is contrary to the expectations of the literature, which proposes that corporate governance mechanisms function as an alternative means of inhibiting earnings management (Martinez, 2001; Barros, Soares & Lima, 2013). Metropolis did not present statistical significance in either model, suggesting that the relationship investigated cannot be attributed to the location of the company in large centers or in the interior, confirming the evidence of McGuire et al. (2012).

The results support the two hypotheses established in the study and indicate that managers of companies in more religious areas would tend to manage the result through real activities, to the detriment of accruals, which suggests that the way by which religious norms are associated with the decision of managers on how to manage the result is risk aversion (Cai et al., 2018). Risk aversion may explain the negative relationship between Religiosity with AEM and positive Religiosity and REM, because REM is considered the safest way to manage results, due to the difficulty of detection by auditors and regulatory bodies (Cai et al., 2018; Gunny, 2005; Roychowdhury, 2006; Graham et al., 2005), which signals the need for other control mechanisms for the REM in parallel to the collation of religious aspects of the region. It is emphasized, however, that in this study the level of risk aversion of managers was not verified, but only pointed out that the literature supports the effect of risk aversion on the relationship between religiosity and earnings management.

Two robustness tests were performed, changing the dependent variable. The AEM was again estimated using the Modified Jones Model (1995). The correlation between the two AEM methods is 0.707 (p-value < 0.01). The results for the relationship between Religiosity and AEM remain the same (p-value < 0.01), i.e., religiosity can mitigate this management modality, regardless of the model used.

In the second robustness test, the form of REM calculation was modified. Equation 5 was dismembered into two: REM1 = ( -1* AB_DISC) + (AB_PROD) and REM2 = ( -1* AB_DISC) + ( -1* AB_CAHS), as performed in McGuire et al. (2012). The results reinforce the relationship identified in Model 2, i.e., REM1 equal to 0.192 (p-value < 0.01) and REM2 equal to 0.127 (p-value < 0.01), confirming that greater Religiosity results in higher REM.

Although Hausman test results indicated that AEM models should be estimated with random-effects, two additional tests were performed with fixed-effects estimators, since, as pointed out by Gujarati and Porter (2011, p. 603), "even if the underlying model is assumed to be stacked or randomly effected, fixed-effect estimators are always consistent". Regarding the Modified Jones Model (1995), the results with fixed-effect estimators were consistent with the findings of the random-effects model and showed that religiosity and AEM (Modified Jones Model, 1995) are negatively associated. On the other hand, concerning the AEM model - Kothari et al. (2005), the results with fixed-effects estimators were not consistent with the random-effects model and showed no significant association between religiosity and AEM (Kothari model et al., 2005). Thus, it is conjectured that the results of these additional tests (with the use of fixed-effect estimators) are partially consistent with the results of the present study, since they show the association between religiosity and AEM, by the Modified Jones Model (1995), which does not occur when the Kothari et al Model is used (2005).

5 FINAL REMARKS

Based on the hypothesis that religiosity is negatively associated with the earnings management through accruals (AEM) and positively associated with the earnings management through real activities (REM), it was investigated whether religiosity mitigates the AEM and encourages the REM. Religiosity was measured by the percentage of religious people around the company, with a sample of 122 Brazilian companies for the period from 2010 to 2017.

It was evidenced that greater religiosity results in lower AEM and higher REM. These results suggest that managers, influenced by religious social norms, prefer the REM to the AEM. The preference for REM is justified by the lower risk of detection. It is inferred that religiosity acts as a social norm capable of influencing the decision of managers, as proposed in the Theory of Social Norms.

These findings were documented by controlling variables at the external and internal levels of the companies. Two robustness tests were also performed, with the results pointing in the same direction.

The findings add knowledge regarding the influence of religiosity on earnings management in Brazilian companies, indicating that the proposed relationship for an IFRS adopting country, such as Brazil, is the same as that identified in countries such as the United States and China, which did not adopt these standards (McGuire et al., 2012; Cai et al., 2018). In other words, evidence suggests that the adoption of IFRS may have no impact on the relationship between religiosity and earnings management, suggesting that future research may amplify this discussion.

A more religious environment around the company may indicate that in that company there is less AEM and higher REM, and this evidence may allow the increase of investment analysis models with the variable religiosity. Additionally, research on earnings management may consider religiosity as an additional variable in the models.

The measure of religiosity is a limitation of the study because the percentage of people who claim to have a religion may be different from that of people who actively participate in a religious cult or community. In addition, as the measure is by the municipality, companies in larger municipalities may be subject to variations in the measure by neighborhoods or regions, generating a more dispersed effect of religiosity. Future research can advance in this aspect, in addition to the association with other measures of quality of accounting information. The complexity of the relationship between demographic characteristics and earnings management, as well as the lack of consensus in the literature on the subject, also means further studies.

REFERENCES

Barros, C. M. E., Soares, R. O., & Lima, G. A. S. F. de. (2013). A relação entre governança corporativa e gerenciamento de resultados em empresas brasileiras. Revista de Contabilidade e Organizações, 7(19), 27-39. https://doi.org/10.11606/rco.v7i19.55509.

Bjornsen, M., Do, C., & Omer, T. C. (2019). The influence of country-level religiosity on accounting conservatism. Journal of International Accounting Research, 18(1), 1-26. https://doi.org/10.2308/jiar-52270.

Brasil, Bolsa Balcão (B3). (2020). Empresas listadas. Available at: http://www.b3.com.br/pt_br/produtos-e-servicos/negociacao/renda-variavel/empresas-listadas.htm.

Caetano, S. C. S. A (2018). Os avanços na fala das mulheres negras. Anais do Encontro Estadual de História e Democracia: precisamos falar sobre isso, Guarulhos, SP, Brasil, 24. https://www.encontro2018.sp.anpuh.org/site/anaiscomplementares.

Cai, G., Li, W., & Tang, Z. (2018). Religion and the method of earnings management: evidence from China. Journal of Business Ethics, 161(1), 71-90. https://doi.org/10.1007/s10551-018-3971-6.

Callen, J. L., Morel, M., & Richardson, G. (2011). Do culture and religion mitigate earnings management? Evidence from a cross-country analysis. International Journal of Disclosure and Governance, 8(2), 103-121. https://doi.org/10.1057/jdg.2010.31.

Campara, J.P., Vieira, K. M., Bender Filho, R., & Coronel, D. A. (2017). Entendendo a tolerância ao risco: proposição de um modelo logit multinomial. Revista de Administração da UNIMEP, 15(2), 1-30. http://www.redalyc.org/articulo.oa?id=273752467001.

Cohen, D. A., Dey, A., & Lys, T. Z. (2008). Real and accrual-based earnings management in the pre- and post-sarbanes-oxley periods. The Accounting Review, 83(3), 757-787. https://doi.org/10.2308/accr.2008.83.3.757.

Consoni, S., Colauto, R. D., & Lima, G. A. S. F. de. (2017). A divulgação voluntária e o gerenciamento de resultados contábeis: evidências no mercado de capitais brasileiro. Revista Contabilidade & Finanças, 28 (74), 249-263. https://doi.org/10.1590/1808-057x201703360.

Cupertino, C. M., Martinez, A. L., & Costa Jr., N. C. A. da. (2017). Earnings management strategies in Brazil: Determinant costs and temporal sequence. Contaduría y Administración, 62(5), 1460-1478. https://doi.org/10.1016/j.cya.2016.11.002.

Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management. The Accounting Review, 70(2),193-225.

Du, X., Jian, W., Lai, S., Du, Y., & Pei, H. (2015). Does religion mitigate earnings management? Evidence from China. J Bus Ethics, 131, 699-749. https://doi.org/10.1007/s10551-014-2290-9.

Dyreng, S. D., Mayew, W. J., & WIlliams, C. D. (2012). Religious social norms and corporate financial reporting. Journal of Business Finance & Accounting, 39(7-8), 845-875. https://doi.org/10.1111/j.1468-5957.2012.02295.x.

Economatica. (2020). Banco de Dados. Recuperado de: https://economatica.com/.

Fields, T. D., Lys, T. Z., & Vincent, L. (2001). Empirical research on accounting choice. Journal of Accounting and Economics, 31(1-3), 255-307. https://doi.org/10.1016/S0165-4101(01)00028-3.

Graham, J. R., Harvey, C. R., & Rajgopal, S. (2005). The economic implications of corporate financial reporting. Journal of Accounting and Economics, 40(1-3), 3-73. https://doi.org/10.1016/j.jacceco.2005.01.002.

Grullon, G., Kanatas, G., & Weston, J. (2009). Religion and corporate (mis) behavior. Disponível em SSRN 1472118. Retrieved from: http://www.ruf.rice.edu/~westonj/wp/Religion.pdf.

Gujarati, D. N., & Porter, D.C. (2011). Econometria básica. 5. Ed. Porto Alegre: AMGH Editora.

Gunny, K. (2005). What are the consequences of real earnings management?. Retrieved from: http://w4.stern.nyu.edu/accounting/docs/speaker_papers/spring2005/Gunny_paper.pdf.

Hilary, G., & Hui, K. W. (2009). Does religion matter in corporate decision making in America? Journal of Financial Economics, 93(3), 455-473. https://doi.org/10.1016/j.jfineco.2008.10.001.

Hribar, P., & Collins, D. W. (2002). Errors in estimating accruals: implications for empirical research. Journal of Accounting Research, 40(1), 105-134. https://doi.org/10.1111/1475-679X.00041.

Huang, H., Rose-Green, E., & Lee, C. (2012). CEO age and financial reporting quality. Accounting Horizons, 26(4), 725-740. https://doi.org/10.2308/acch-50268.

Instituto Brasileiro de Geografia e Estatística (IBGE). (2020). Sidra: Banco de Tabelas Estatísticas. Recuperado de: https://sidra.ibge.gov.br/pesquisa/censo-demografico/demografico-2010.

Jackson, T. M. (2020). We have to leverage those relationships: how Black women business owners respond to limited social capital. Sociological Spectrum, 1-17. https://doi.org/10.1080/02732173.2020.1847706.

Joia, R. M., & Nakao, S. H. (2014). Adoção de IFRS e gerenciamento de resultado nas empresas brasileiras de capital aberto. Revista de Educação e Pesquisa em Contabilidade (REPeC), 8(1). https://doi.org/10.17524/repec.v8i1.1014.

Kennedy, E. J., & Lawton, L. (1998). Religiousness and business ethics. Journal of Business Ethics, 17(2), 163-175. https://doi.org/10.1023/A:1005747511116.

Kothari, S.P., Leone, A. J., & Wasley, C. E. (2005). Performance matched discretionary accrual measures. Journal of Accounting and Economics, 39(1), 163-197. https://doi.org/10.1016/j.jacceco.2004.11.002.

Ma, L., Zhang, M., Gao, J., & Ye, T. (2020). The effect of religion on accounting conservatism. European Accounting Review, 29(2), 383-407. https://doi.org/10.1080/09638180.2019.1600421.

Martinez, A. L. (2011). Do corporate governance special listing segments and auditing curb real and accrual-based earnings management? evidence from brazil. Revista Universo Contábil, 7(4), 98-117. http://dx.doi.org/10.4270/ruc.20117.

Martinez, A. L. (2001). "Gerenciamento" dos resultados contábeis: estudo empírico das companhias abertas brasileiras. Tese de doutorado, Universidade de São Paulo, São Paulo, SP, Brasil.

McGuire, S. T., Omer, T. C., & Sharp, N. Y. (2012). The impact of religion on financial reporting irregularities. The Accounting Review, 87(2), 645-673. https://doi.org/10.2308/accr-10206.

Miller, A. S., & Hoffmann, J. P. (1995). Risk and religion: an explanation of gender differences in religiosity. Journal for the Scientific Stuldy of Religion, 34, 63-75. https://doi.org/10.2307/1386523.

Paulo, E. (2007). Manipulação das informações contábeis: uma análise teórica e empírica sobre os modelos operacionais de detecção de gerenciamento de resultados. Tese de doutorado, Universidade de São Paulo, São Paulo, SP, Brasil.

PNUD Brasil. (2010). Ranking IDHM Municípios 2010. Retrieved from: https://www.br.undp.org/content/brazil/pt/home/idh0/rankings/idhm-municipios-2010.html.

Roychowdhury, S. (2006). Earnings management through real activities manipulation. Journal of Accounting and Economics, 42, 335-370. https://doi.org/10.1016/j.jacceco.2006.01.002.

Sena, T. R., Dias Filho, J. M., & Moreira, N. B. (2020). Gerenciamento de resultados por decisões operacionais no novo mercado do brasil: uma análise da influência de auditorias big four e não big four. Revista de Gestão, Finanças e Contabilidade, 10(2), 04-21. https://doi.org/10.18028/rgfc.v10i2.7470.

Silva, A. Pletsch, C. S., Vargas, A. J., Fazolin, L. B., & Klann, R. C. (2014). Influência da auditoria sobre o gerenciamento de resultados. Revista de Contabilidade do Mestrado em Ciências Contábeis da UERJ, 19(3), 59-69. https://doi.org/10.12979/11151.

Thomson Reuters. (2020). Banco de Dados. Retrieved from: https://www.thomsonreuters.com.br.

Urcan, O. (2007). Geographical location and corporate disclosures. SSRN Electronic Journal. Retrieved from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=930433.

World Bank. (2021). DataBank. Retrieved in 02 novembro, 2021 de https://databank.worldbank.org/source/world-development-indicators.

Appendix A. Correlation matrix

Notes

Author notes

Corresponding author Tel. +55 (34) 3239-4176 E-mail: simonemirandadossantos@hotmail.com (S. M. dos Santos); sirlemes@uol.com.br (S. Lemes); neirilaine@ufu.br (N. S. de Almeida); Universidade Federal de Uberlândia. Av. João Naves de Ávila, 2121 - Bloco 1F - Santa Mônica, Uberlândia/MG - 38408-100, Brazil