Article

Accounting faculty (re)formation: a reflection on Brazilian doctoral programs

(Re)Formação docente em Contabilidade: uma reflexão sobre os programas de doutorado no Brasil

Camilla Soueneta Nascimento Nganga camillasn@ufu.br

Silvia Pereira de Castro Casa Nova silvianova@usp.br

João Paulo Resende de Lima joaopaulo.lima@glasgow.ac.uk

Camilla Soueneta Nascimento Nganga camillasn@ufu.br

Silvia Pereira de Castro Casa Nova silvianova@usp.br

João Paulo Resende de Lima joaopaulo.lima@glasgow.ac.uk

Accounting faculty (re)formation: a reflection on Brazilian doctoral programs

Revista de Contabilidade e Organizações, vol. 16, e191038, 2022

University of São Paulo

Received: 29 September 2021

Accepted: 30 May 2022

Published: 07 October 2022

Abstract: In this paper, we analyze the faculty training in Brazilian Accounting doctoral programs, focusing on the curricular components' analysis of teaching and research courses. We gathered the data through the Sucupira platform, using the following information from the 2019 CAPES collection, considering the 15 doctoral courses in Accounting that exist in the country: doctoral course objectives; research lines; research projects; disciplines (training for teaching); disciplines (training for research); and teaching internships. Regarding teaching training, the current scenario is preoccupying because it presents few changes concerning previous studies. Our findings point to few initiatives for initial pedagogical training, forcing faculties to take responsibility for their own pedagogical development. As for research training, the results indicate training based on methodological and quantitative methods courses, demonstrating a mainstream-focused training. Based on these results, we hope to contribute to the reflection on faculty (re)training in Brazilian Accounting doctoral programs at a time of expansion and consolidation.

Keywords: Teacher education, Teaching, Research, Doctoral education, Accounting education.

Resumo: No presente trabalho problematizamos a formação docente em Contabilidade no Brasil, por meio da análise dos componentes curriculares voltados para o ensino e pesquisa dos cursos de doutorado da área de Ciências Contábeis. A coleta de dados foi realizada na plataforma Sucupira, considerando as seguintes informações da coleta CAPES de 2019 dos 15 cursos de doutorado existentes no país: objetivos do doutorado; linhas de pesquisa; projetos de pesquisa; disciplinas (formação para o ensino); disciplinas (formação para a pesquisa); e estágio docência. No tocante à formação voltada para o ensino, o cenário atual é preocupante, pois apresenta poucas mudanças em relação aos estudos anteriores, demonstrando poucas iniciativas para a formação pedagógica inicial, fazendo com que os docentes se autorresponsabilizem por seu desenvolvimento didático-pedagógico. Acerca da formação para a pesquisa, os resultados indicam uma formação pautada por disciplinas de caráter metodológico e métodos quantitativos, demonstrando uma formação voltada para o mainstream. A partir desses resultados, esperamos contribuir para a reflexão sobre a (re)formação docente nos programas de doutorado em Contabilidade no Brasil, em um momento de expansão e consolidação da área.

Palavras-chave: Formação docente, Ensino, Pesquisa, Doutorado, Ensino contábil.

The one who forms forms oneself and reforms through forming and those who are formed form by being formed Paulo Freire

1 INTRODUCTION

Graduate programs are seen as the main locus for formal learning, both for teaching and research. In this scenario, such programs play an important role in providing professional teacher development and socialization, as well as the initial training of researchers and teachers (Austin, 2002; Andere & Araujo, 2008; Lima et al., 2017; Wille, 2017; 2018).

From a legal standpoint, in the scope of higher education, Law 9.394 of 1996, which instates the guidelines and bases of brazilian education, establishes that “preparation for the exercise of higher education will take place at the postgraduate level” degree, primarily in master's and doctoral programs. This indication reinforces the importance of graduate programs in Accounting as spaces that provide teacher training. In this sense, programs need to provide training opportunities for teaching in a systematic and intentional way (Nganga et al., 2016; Farias et al., 2020).

The expansion of stricto sensu postgraduate courses in Accounting Sciences in Brazil is remarkable. Data from the Coordination for the Improvement of Higher Education Personnel (CAPES) indicate that, of the 29 Graduate Programs in the Accounting Sciences (PPGCCs) area, 26 programs were created after 1998 (CAPES, 2021).

In this context, research shows a greater focus of PPGCCs on scientific production and the lack of spaces and opportunities for pedagogical training (Comunelo et al., 2012; Laffin & Gomes, 2014; Nganga et al. 2016; Onohara, 2018; Silva et al., 2018). One of the possible explanations for this focus is the tendency of CAPES to evaluate programs mainly by their level of scientific publishing (Kuenzer & Moraes, 2005; Patrus et al., 2018). In other words, the programs adapt to the evaluation requirements, which become guidelines for the adopted actions and strategies.

Thus, if there is a discussion about the lack of content related to teacher training within the scope of master's and doctoral courses in the area, some evidence show that these may not be contributing fully to researchers' training (Nganga, 2019). The fact that programs focus on scientific production may be related to the number of publishing and not necessarily to the quality of development, process and contribution of research projects (Gendron, 2005; 2015).

That is, quantity indicators' achievements may be occurring at the expense of quality, incurring a possible stagnation in the area (Moser, 2012; Rebele & Pierre, 2015; Lima et al., 2020), in addition to the decrease in the innovative character of the themes and research approaches (Gendron, 2008), as well as a departure from accounting practice (Hopwood, 2007). From this context, the general objective of the study is to problematize teaching formation in Accounting in Brazil, through the analysis of the curricular components aimed at teaching and research of doctoral courses in the Accounting Sciences area.

Reflecting on how the training process for research in Accounting takes place in the programs is essential, considering its impact on the consolidation of the field, as well as the need to think and build research that, in fact, contribute critically and reflectively to the area, institutions and society in general. In discussions concerning teacher training in Accounting, an important and possible point of analysis in the face of this work is that understanding the training process related to teaching in Accounting brings the possibility of analyzing and understanding those who are the main agents in the training of accounting professionals within the scope of higher education.

In this context, such an analysis is relevant due to the observed multiplier effect, since stricto sensu graduate courses in Accounting Sciences have the potential to contribute to the training of trainers, that is, professors who are probably acting or will act in the training process of undergraduate students in Accounting Sciences and, therefore, in the training of professionals and Brazil's future professors in the area.

As contributions, we hope that this article enables advancing the discussion on teacher training in Accounting Sciences by discussing the curricular components both for didactic and pedagogical training, as well as for research, since national literature focus mostly on didactic and pedagogical training. For the practice, our reflections can guide training actions in doctoral courses in Accounting, inform curricular changes in such courses, in addition to supporting actions by regulatory bodies and associations representing graduate programs.

As contributions, we hope that this article can advance the discussion on teacher training in Accounting Sciences by discussing the curricular components both for didactic and pedagogical training, as well as for research, since in the national literature the focus is mostly on didactic training. and pedagogical. For practice, our reflections can guide training actions in doctoral courses in Accounting, inform curricular changes in such courses, in addition to supporting actions by regulatory bodies and associations representing graduate programs.

2 PREVIOUS STUDIES - TEACHING TRAINING IN ACCOUNTING IN BRAZIL

In 1965, the Federal Council of Education (CFE) issued the Sucupira Appraisal (Appraisal n. 977/65) with the aim of establishing definitions related to the concept, levels and purpose of graduate studies. The first two objectives indicated by the Appraisal (CFE, 1965, p. 165) should be highlighted, as they indicate that the postgraduate sector will act in the formation of “[...] competent professorship that can meet the quantitative expansion of our higher education, guaranteeing, at the same time, the elevation of the current levels of quality; 2) to stimulate the development of scientific research through adequate preparation of researchers”.

From a practical point of view, previous studies demonstrate a scenario contrary to what the first objective of the Sucupira Appraisal points to regarding pedagogical training. Laffin and Gomes (2014) concluded that there is no organic proposal for the pedagogical training of teachers in PPGCCs, even though such training is pointed out in their objectives. Nganga et al. (2016) showed, through documentary research, the existence of a timid offer of subjects related to training for teaching in the analyzed programs.

If the PPGCCs are intended to be spaces that contribute to the teacher training of their students - as the Sucupira Appraisal and the work of Laffin and Gomes (2016) show -, in theory, they should contribute to the training of teachers and researchers that minimally reflect the educational process, the epistemology of knowledge, the process of building scientific knowledge, considering its limits, methods and multiple possibilities (Comunelo et al., 2012; Patrus & Lima, 2014).

Farias and Araújo's study (2016) proceeded with the analysis of the perception of teachers in the Accounting area in relation to training spaces for teaching. In view of the research findings, pedagogical preparation may be restricted to the efforts of teachers in the area (Farias & Araujo, 2016), a scenario reinforced by the information presented in Table 2.

The research by Onohara (2018), attempting to update the study by Nganga et al. (2016), through the verification of possible changes in the pedagogical components offered by Brazilian PPGCCs, identified that, even with the expansion that occurred in the scope of postgraduate courses in Accounting in the country since that research was carried out - from 18 to 29 programs - few changes have been made in relation to the offer of subjects related to training in the pedagogical area: there are still subjects of higher education methodology, mostly elective, with different workloads.

In the context of Wille's research (2018), the author concluded that the teaching internship has as one of its main purposes the approximation between professors and undergraduate students, through the performance of intern graduate students, since undergraduate students indicated that they feel closer to the interns to ask questions and share concerns. According to the author, it is essential that graduate students participate in the entire subject process, from initial planning to the final evaluation of it, and that graduate students receive feedback and share experiences with supervising professors (Wille, 2018).

In this way, we observed that the existing literature in Accounting Sciences presents several indications of the lack of intentional and systematized pedagogical training offered by PPGCCs. At the same time, we noted that the research focuses on the discussion of teacher training, exclusively aiming at training for teaching without taking into account training for research. In the present study, research and teaching are considered to be complementary practices in education (Freire, 2012).

3 METHODOLOGICAL ASPECTS

To achieve the proposed research objective, we carried out a qualitative research with a documentary character. Thus, data were collected about the curricular components of the doctoral courses in Accounting. Data collection was carried out in February 2021, obtained from Sucupira platform. The following information was obtained from the CAPES collection for the year 2019: doctoral objectives; research lines; research project; subjects (training for teaching); subjects (training for research - teaching internship).

Currently, the Accounting Sciences subarea, an integral part of the Administration, Accounting and Tourism area, includes 29 postgraduate programs, with 15 programs offering academic doctoral and master's courses and 14 programs offering academic master's courses only (CAPES, 2019a).

The analysis includes the doctoral courses in Accounting Sciences; focus of the present study. This choice is justified, considering that, in general, the objective of the master's degree focuses on training for teaching, and the doctorate focuses on training for research (Andere & Araújo, 2008). For data analysis, we collected curriculum components aimed at didactic-pedagogical training and research. To this end, the academic structures of the programs were analyzed regarding the lines of research, the objectives proposed by them, as well as all the subjects offered.

4 OVERVIEW OF DOCTORAL COURSES IN ACCOUNTING SCIENCES IN BRAZIL

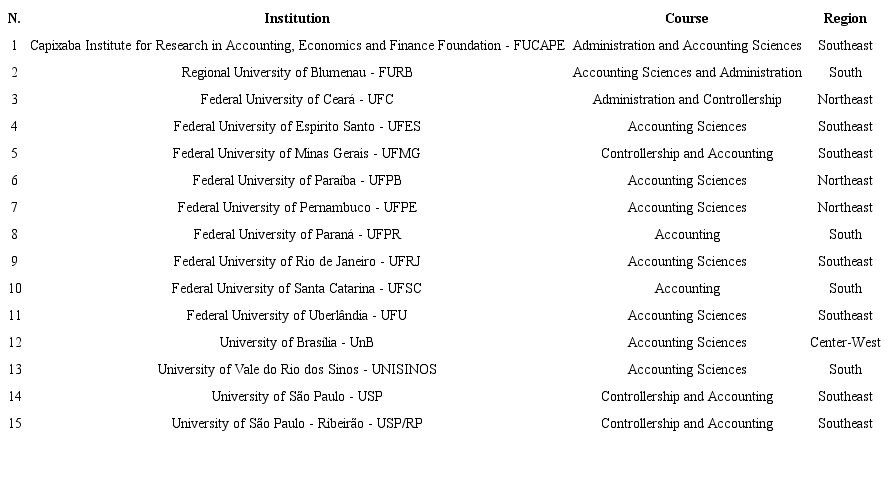

Table 1 presents the graduate programs that offer an academic doctorate in Accounting Sciences in Brazil.

The information in Table 1 allows us to verify that: there is still a strong concentration of courses in the south and southeast regions; there was a growing offer of programs in the northeast region, as a result of the effort to create the multi-institutional program; a lack in other regions, with only one course in the center-west region and none in the north region.

We emphasize here the importance of the postgraduate program in controllership and accounting at the University of São Paulo for the Accounting area in Brazil, considering that it was the first program to offer master's and doctoral courses in the area; the doctoral course beginning in 1978. It was only after 30 years that the second doctoral course in the field of Accounting was funded in the Brazil. This situation results in an influential position of this program in Accounting research carried out in the country, from the emergence of postgraduate studies in Accounting Sciences to the present day (Martins, 2012).

From the analysis of the objectives proposed by the 15 doctoral programs in the area of Accounting Sciences, we observed that, excepting UnB and UFSC programs, all other programs have as objectives the training for teaching and research.

This discussion enables to reflect on teacher training in Accounting and the need for it to be properly thought through by PPGCCs, considering training for teaching and training for research. As previously stated, doctoral courses in Accounting Sciences, in general, elicit in their objectives the training of teachers, which implies a commitment made by these courses in the development of such training.

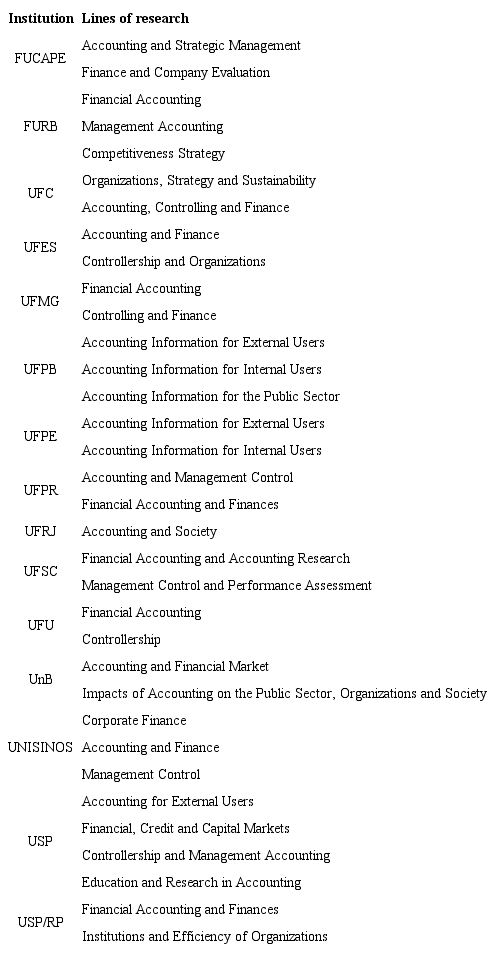

Thus, we understand that it is important to discuss the characteristics and assumptions that circumscribe training for teaching and research, bringing this discussion to the context of stricto sensu graduate studies and also to the area of Accounting Sciences. Following the analysis, the lines of research are shown in Table 2.

In general, we observe that, of the 15 doctoral courses existing in the area, only USP has a specific line of research on education and research in Accounting. UFSC, UnB and USP/RP programs, despite not having a specific line related to education and research, enable possibilities for research in these themes through interdisciplinary research lines.

The possibility of researching education - mainly on the pedagogical practice itself - brings the possibility of developing a teacher-researcher who reflects the practice and in practice as defended by Slomski and Martins (2008). For the authors, “being a teacher-researcher is, therefore, having an attitude of being in the profession as an intellectual who critically questions and questions himself” (p. 18).

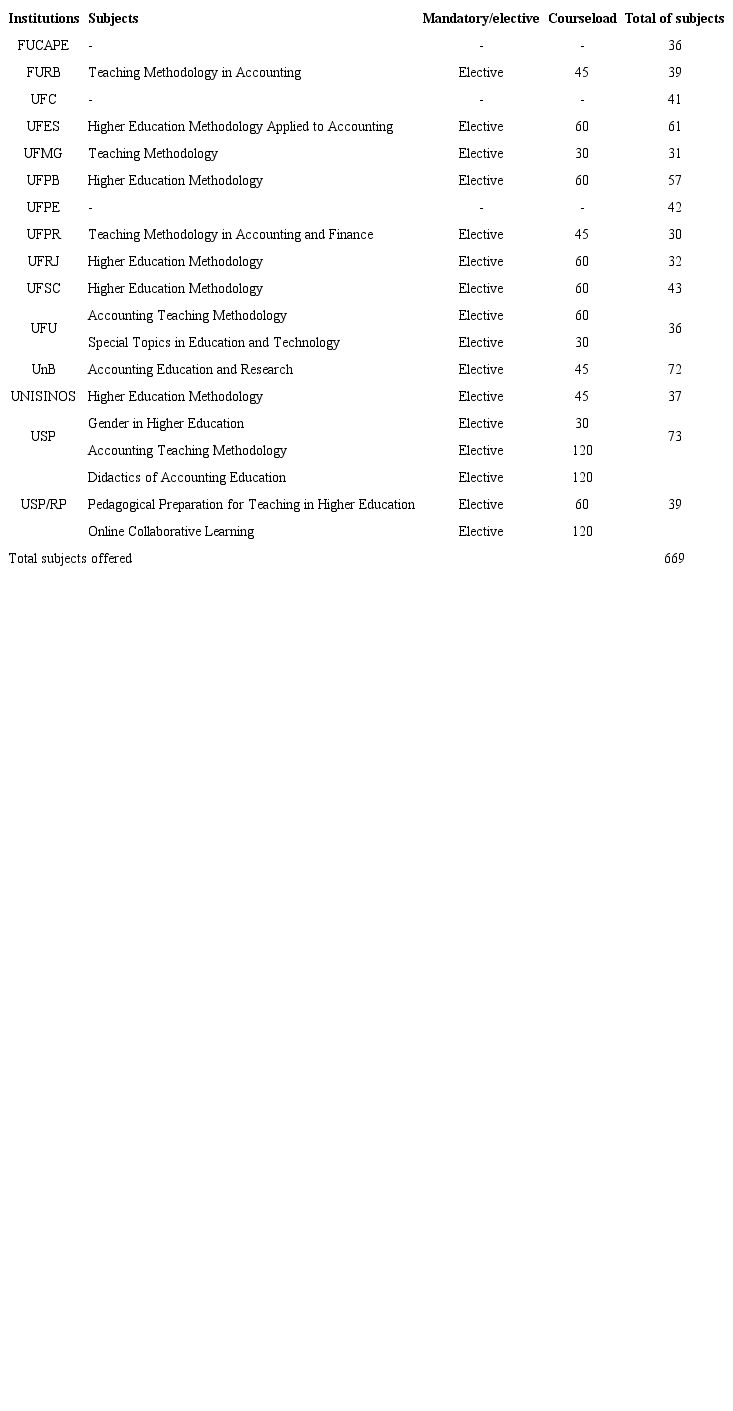

Regarding the training scenario for teaching that exists in the stricto sensu Brazilian postgraduate course, Almeida (2012) advocates that it is restricted to the subject of higher education methodology and the teaching internship. Thus, to analyze this scenario in the area of Accounting Sciences, Table 3 presents information related to subjects with didactic-pedagogical content.

The information on the subjects related to teacher training indicates a worrying picture: 11 of the 15 doctoral courses offer subjects (16 subjects) on this theme, all elective, with a courseload ranging from 30 to 120 hours, with only four of these subjects focusing on something other than teaching methodology.

The 16 subjects represent about 2.4% of the total, totaling 669 subjects. We identified that FUCAPE, UFC, and UNISINOS programs do not offer any subjects related to preparation or training for teaching. From this perspective, there is agreement with what was exposed by Laffin and Gomes (2016):

It is worth emphasizing that the subject of methodology in higher education as an optional alternative, with a courseload of 60 hours, does not constitute pedagogical training, but an approximation to the issues of the professor's work. In this context, it is assumed as another subject on the list of electives, one of free choice of the student, and stripped of articulation with a training project for teaching being, thus, tangentially characterized as training rhetoric (Laffin & Gomes, 2016, p. 4).

Although the existing literature makes it possible to verify the importance of pedagogical qualification in the process of teacher training, such training is non-existent in master's and doctoral courses in the area of Accounting Sciences in Brazil, given that it comes down to a single elective subject and, in some programs, there is no subjects being offered at all within the theme on display.

This training scenario for teaching may indicate that the university professor does not have training focused on the teaching and learning processes, which encompasses elements such as planning, class organization, evaluation, methodology and didactic strategies, interaction between professors and students, and for which they are responsible from the moment they enter the academic career (Almeida, 2012). It is worth mentioning that the context of the pandemic showed the importance of this training, considering the challenges of adapting face-to-face classes for emergency remote teaching in order to ensure the continuity of activities.

Another possible training action is training in practice, through internship or assisting to teaching. CAPES (2010), through Ordinance MEC/CAPES nº 76/2010, established the teaching internship, defining it as “an integral part of the training of graduate students, aiming at the preparation for teaching, and the qualification of the teaching of University graduate". According to data made available by the Sucupira platform, the 15 doctoral programs in the area offer teaching internships, with a workload varying between 30 and 60 hours. UFMG, UFPB and USP programs develop the internship as a mandatory element, FUCAPE, FURB and UFSC programs indicate that it is mandatory for scholarship students only. The remainder courses offer the teaching internship to their students as an elective element.

Regarding the teaching internship, research by Onohara (2018) concluded that, although there is an indication from CAPES that internships should be mandatory for scholarship holders, 38% of PPGCCs offer the activity on a mandatory basis for scholarship holders and elective to other postgraduate students. That is, they only comply with the obligation defined by CAPES.

Despite being an important action that contributes to teacher training, there is no guidance from CAPES on how the teaching internship should be developed. For Nganga et al. (2016), such a situation can lead to subjectivities in the understanding of the way in which the programs propose the teaching internship to students.

The mandatory teaching internship without the obligation of theoretical pedagogical training through the subjects indicates the reproduction of the trial and error model that permeates teaching in Accounting - especially in the beginning of the career, as shown by Lima et al. (2015). In addition, it urges to question the formative role of the internship without the proper theoretical basis to begin teaching, since from the current scenario there is an overvaluation of practice to the detriment of theoretical knowledge that enables a reflective practice (Joaquim et al., 2013).

We believe that Wille's (2018) research exposes the potential not yet explored of the teaching internship in the context of Brazilian PPGCCs, and it can be a fundamental strategic action in the preparation of graduate students for teaching, especially if we consider the few spaces that exist in the area of Accounting for such preparation. In this sense, the initiatives presented by Schnader et al. (2016) and Callahan et al. (2016) can be considered examples in the search for pedagogical preparation strategies in the context of teaching in Accounting Sciences in Brazil.

Although pedagogical training for teaching within the programs is basically taking place through the aforementioned subject and also through the teaching internship, it is important to recognize the importance of these actions for preparation, even if they are apparently insufficient if we consider the complexities and specificities of the teaching profession. In this sense, Silva, Ferreira, Leal and Miranda (2018) investigated the contribution of the teaching methodology subject to teacher training in the context of Accounting from the experience of students who took this subject, concluding that the subject contributed to the teacher training of students, who were not yet working as teachers, as well as continuing education for those who were already working in teaching, promoting reflections and self-assessment in this latter group.

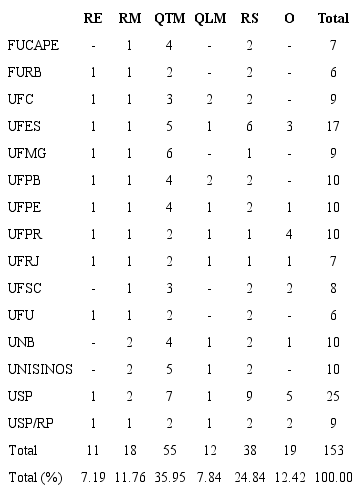

The presented scenario is problematic and points to the neglect of PPGCCs in relation to training for the teaching of their student body, since, in some cases, not even the minimum expected from them, that is, the subjects of teaching methodology and internship teaching is offered. Regarding training for research, we analyzed the curricular components made available by the PPGCCs through the offer of subjects related to the development of scientific knowledge, as indicated in Table 4.

We can verify an extensive offer of subjects related to research methods, particularly those with quantitative approaches, as well as advances in initiatives that refer to the epistemology components of research and qualitative approaches. We emphasize that no subject on critical and interpretivist research was identified in the carried-out analysis11. In addition, one of the programs offers a subject of publishing scientific papers, two programs offer subjects of scientific research practice, and a fourth program offers a subject of research productivity tools. These subjects denote a focus on academic publishing.

The scenario may indicate an approximation of the doctoral model in Brazil, similar to that in force in the United States: positivist-functionalist model, based on mathematical methods and models, an average of two years to carry out subjects focused on research, research methodologies and theoretical bases within the mainstream (Fox, 2018; Raineri, 2015). The influence of the US model on Brazilian accounting education has been remarkable ever since the translation and adoption of the book “Introductory Accounting” as one of the main books for teaching introductory accounting (Mendonça Neto et al., 2008; Mendes et al., 2021).

In the case of doctoral courses here in Brazil, the information made available on the Sucupira platform about the 15 existing courses in Accounting indicates that 11 courses offered the subject research epistemology, and eight of them were offered as mandatory.

Thus, it is assumed that teachers, when starting their teaching careers with the commitment to collaborate with the training of future accounting professionals, as well as with the development of research committed to the area, do not have the desired minimum for their professional qualification as academics, and will teach with training deficiencies or will autonomously and individually seek actions that contribute to this qualification.

Due to the fact that, based on the evidence presented, adequate training has not been offered, it is difficult to assess the impacts of its provision for these teachers in training. And, besides these teaching apprentices, this insufficient qualification has an effect on the professional preparation of graduates in the area.

In the case of research, the reflection to be made is about the training of trainers. It is these doctors and masters who will guide research projects at all levels, from scientific initiation to doctorate. Therefore, these men and women are the ones who will be responsible for training future researchers in the area, for the inauguration and consolidation of new themes and lines of research, for the constitution of new programs and for the international insertion of the area. Thus, a restricted or incomplete training causes this deficiency to be reflected in the training of future generations of researchers. Thus, as a community, we must reflect on the responsibility and consequences of designing and implementing master's and doctoral curricula that do not adequately represent the diversity and possibilities of accounting research.

There is evidence of advances around greater diversity in research: 12 subjects related to qualitative methods are offered by 10 programs. But this, in contrast to 55 subjects related to quantitative methods, offered by all programs. In addition, all programs offer the research methodology subject, totaling 18 subjects, with 3 programs offering more than one subject. Regarding the total number of subjects offered in the 15 programs, subjects related to research training account for around 22%.

Such results are in line with the reflections made by Raineri (2013), who sought to analyze socialization processes and discourses in the context of a doctoral program in Accounting in the United States. The author describes the actions and discourses issued within the program, which demonstrate the focus on academic publishing, the high valuation of quantitative methods and superficial research, and also highlights the disincentive to carry out innovative and qualitative research (Raineri, 2013).

Based on these results, the present study contributes to the reflection on teacher training in doctoral accounting programs in Brazil, at a time when the area is consolidating and expanding strongly.

Thus, after an initial period of constitution from 1970 onwards, followed by a period of strong expansion from 1998 onwards, a moment comes when this critical reflection is necessary for the area to consolidate and position itself internationally as an active, diverse and contributory research community. It is up to the generations that worked on this constitution and expansion to make this reflection and the necessary changes, which seem to us to be already underway, so that future generations inherit an area with more diversity and greater possibilities than the one that preceded them.

5 FINAL CONSIDERATIONS

The present work aimed to problematize the teaching formation in Accounting in Brazil, through the analysis of the curricular components aimed at teaching and research of doctoral courses in the area of Accounting Sciences. The importance of understanding how doctoral courses organize their curriculum lies in the role played by doctors trained/graduated in these programs.

Regarding the results found with regard to training aimed at teaching, the current scenario is worrying because it presents few changes in relation to previous studies such as the one by Nganga et al. (2016). This result indicates a possible institutionalization of pedagogical training as the professor's own responsibility throughout the career and ignores possibilities related to the initial training of this teacher. Among the possibilities to change this scenario, the possibility of a pedagogical mentoring program stands out, as highlighted by Schnader et al. (2016) in research carried out in a doctoral course in Accounting in the United States. According to the authors, the action consisted of observing classes in one semester and acting in the classroom with the supervision of a professor in the second semester, and the evidence indicated that the doctoral students felt better prepared for the beginning of their teaching careers.

Callahan et al. (2016) proposed a teaching practice activity for doctoral students to develop and practice pedagogical skills to be minimally prepared to start their teaching career. The activity was carried out over 2 semesters: in the first semester, through theoretical seminars on pedagogy, class observation and teaching practice by conducting a class observed and evaluated by mentor teachers, who were the teachers evaluated as excellent; in the second semester, with the continuity of the seminars, the conduction of a subject, under the supervision of the mentor professors, and the evaluation and self-reflection based on the feedback received from undergraduate students and supervising professors. Both works demonstrate the importance of combining theory and practice in the training of future teachers.

The results of the present study indicate that training for research is guided by subjects of a methodological nature focused on quantitative methods, demonstrating a training focused on the mainstream. It should also be noted that, in less than half of the doctoral courses, the subject of epistemology is offered as a compulsory subject, pointing to a possible uncritical training focused solely on research, since it is in this subject that we reflect on the construction of knowledge. In this sense, Haynes (2008) highlights that “as researchers, we must continually confront questions about the nature and assumptions of the knowledge we are producing, for whom we are producing it and why we are producing it” (p. 543), reinforcing the importance of reflecting on research rather than succumbing to the pressures of productivism to publish uncritically.

For future research, we suggested conducting interviews with graduates of doctoral programs to understand their training processes in a procedural way. It is also important to understand the spatial arrangement of PPGCCs in Brazil, reflecting on the possible incentives of the federal government through public policies at a given time for the higher education institutions, as well as studies on their organizational identities and social impact in the region in which they operate.

REFERENCES

Andere, M. A., & Araújo, A. M. P. (2008). Aspectos da formação do professor de ensino superior de Ciências Contábeis: uma análise dos programas de pós-graduação. Revista de Contabilidade e Finanças, 19(48), 91-102. https://doi.org/10.1590/S1519-70772008000300008

Austin, A. E. (2002). Creating a bridge to the future: preparing new faculty to face changing expectations in a shifting context. The Review of Higher Education, 26(2), 119-144. DOI: 10.1353/rhe.2002.0031

Callahan, C. M., Spiceland, C. P., David Spiceland, J., & Hairston, S. (2016). Pilot course: a teaching practicum course as an integral component of an accounting doctoral program. Issues in Accounting Education, 31(2), 191-210. DOI: 10.2308/iace-51260

Comunelo, A. L., Espejo, M. M. dos S. B., Voese, S. B., & Lima, E. M. (2012). Programas de pós-graduação stricto sensu em Contabilidade: sua contribuição na formação de professores e pesquisadores. Enfoque: Reflexão Contábil, 31(1), 7-26. DOI: 10.4025/enfoque.v31i1.13375

Coordenação de Aperfeiçoamento de Pessoal de Nível Superior - CAPES. (2021). Plataforma Sucupira - Cursos Avaliados e Reconhecidos. Retrieved from: https://sucupira.capes.gov.br/sucupira/.

Coordenação de Aperfeiçoamento de Pessoal de Nível Superior - CAPES. (2019). Plataforma Sucupira - Coleta CAPES 2019. Retrieved from: https://sucupira.capes.gov.br/sucupira/.

Dunn, K. A., Hooks, K. L., & Kohlbeck, M. J. (2016). Preparing future accounting faculty members to teach. Issues in Accounting Education, 31(2), 155-170. https://doi.org/10.2308/iace-50989

Farias, R. S. de, & Araújo, A. M. P. (2016). Percepção dos professores de Contabilidade quanto aos espaços formativos para o ofício da docência no Brasil. Revista de Contabilidade e Organizações, 28, 59-70. https://doi.org/10.11606/rco.v10i28.124789

Farias, R. S. D., Stanzani, L. M. L., Lima, J. P. R. D., & Araújo, A. M. P. D. (2020). Preparação para a docência universitária: um estudo dos espaços formativos. BASE: Revista de Administração e Contabilidade da Unisinos, 17(4), 606-633. https://doi.org/10.4013/base.2020.174.04

Fox, K. A. (2018). The manufacture of the academic accountant. Critical Perspectives on Accounting, 57, 1-20. https://doi.org/10.1016/j.cpa.2018.01.005

Haynes, K. (2008). Moving the gender agenda or stirring chicken's entrails? Where next for feminist methodologies in accounting?. Accounting, Auditing & Accountability Journal, 21(4), 539-555. DOI: 10.1108/09513570810872914

Hopwood, A. G. (2007). Whither accounting research. The Accounting Review, 82(5), 1365-1374. Retrieved from: https://www.jstor.org/stable/30243502

Kuenzer, A. C., & Moraes, M. C. M. de. (2005). Temas e tramas na pós-graduação em educação. Educação e Sociedade, 26(93), 1341-1362. http://dx.doi.org/10.1590/S0101-73302005000400015

Joaquim, N. D. F., Boas, A. A. V., & Carrieri, A. D. P. (2013). Estágio docente: formação profissional, preparação para o ensino ou docência em caráter precário?. Educação e Pesquisa, 39(2), 351-365. https://doi.org/10.1590/S1517-97022013000200005

Laffin, M., & Gomes, S. M. S. (2014). The pedagogical training of teachers in stricto sensu programs in Accounting Sciences. Australian Journal of Basic and Applied Sciences, 8(18), 255-265. Retrieved from: http://www.ajbasweb.com/old/ajbas/2014/December/255-265.pdf

Laffin, M., & Gomes, S. M. S. (2016). Formação pedagógica do professor de Contabilidade: o tema em debate. Education Policy Analysis Archives, 24, 1-31. http://dx.doi.org/10.14507/epaa.24.2372

Lei n. 9.394, de 20 de dezembro de 1996. (1996, December 23). Estabelece as diretrizes e bases da educação nacional. Diário Oficial da União, seção 1.

Lima, F. D. C., de Oliveira, A. C. L., Araújo, T. S., & Miranda, G. J. (2015). O choque com a realidade: dormi contador e acordei professor... REICE: Revista Iberoamericana sobre Calidad, Eficacia y Cambio en Educación, 13(1), 49-67. Retrieved from: https://revistas.uam.es/reice/article/view/2799

Lima, J. P. R. de, Vendramin, E. de O., & Casa Nova, S. P. D. C. (2017). Identidades acadêmicas em uma era de produtivismo: o (des)alojamento das mulheres contadoras. Trabalho apresentado no XX Seminários em Administração - SEMEAD, São Paulo, SP. Retrieved from: http://login.semead.com.br/20semead/arquivos/1863.pdf

Lima, J. P. R. de, & Bertolin, R. V. (2022). Avaliação da aprendizagem no processo de formação docente em Contabilidade. Desafio Online, 10(1). https://doi.org/10.55028/don.v10i1.10003

Lima, R. S., Serrano, A. L. M., & Ferreira, L. O. G. (2020). Perspectiva Kuhniana sobre a Ciência Contábil: do surgimento do paradigma ao período de crise. Revista Catarinense da Ciência Contábil, 19. https://doi.org/10.16930/2237-766220202985

Martins, E. A. (2012). Pesquisa contábil brasileira: uma análise filosófica. Tese de doutorado, Faculdade de Economia, Administração e Contabilidade, Universidade de São Paulo. DOI: 10.11606/T.12.2012.tde-14022013-171839

Mendes, D., Fonseca, A. C. P. D., & Sauerbronn, F. F. (2020). Modos de ideologia e de colonialidade em materiais didáticos de Contabilidade. Education Policy Analysis Archives, 28(99). https://doi.org/10.14507/epaa.28.5061

Mendonça Neto, O. R., Cardoso, R. L., Riccio, E. L., & Sakata, M. C. G. (2008). Mudança de paradigma na Contabilidade brasileira: uma explicação fundamentada na sociologia da tradução. Contabilidade Vista & Revista, 19(2), 113-139. Retrieved from: https://revistas.face.ufmg.br/index.php/contabilidadevistaerevista/article/view/356

Miranda, G. J. (2010). Docência universitária: uma análise das disciplinas na área da formação pedagógica oferecidas pelos programas de pós-graduação stricto sensu em Ciências Contábeis. Revista de Educação e Pesquisa em Contabilidade (REPeC), 4(2), 81-98. https://doi.org/10.17524/repec.v4i2.202

Miranda, G. J.; Casa Nova, S. P. C.; Cornacchione Júnior, E. B. (2012). Os saberes dos professores-referência no ensino de Contabilidade. Revista de Contabilidade e Finanças, 23(59), 142-153. https://doi.org/10.1590/S1519-70772012000200006

Moser, D. V. (2012). Is Accounting Research Stagnant? Accounting Horizons, 26(4), 845-850. DOI: 10.2308/acch-10312

Nganga, C. S. N. (2019). Abrindo caminhos: a construção das identidades docentes de mulheres pelas trilhas, pontes e muros da pós-graduação em Contabilidade. Tese de Doutorado, Faculdade de Economia, Administração e Contabilidade, Universidade de São Paulo, São Paulo. DOI: 10.11606/T.12.2019.tde-14082019-155635.

Nganga, C. S. N., Botinha, R. A., Miranda, G. J., & Leal, E. A. (2016). Mestres e doutores em Contabilidade no Brasil: uma análise dos componentes pedagógicos de sua formação inicial. REICE: Revista Iberoamericana sobre Calidad, Eficacia y Cambio en Educación, 14(1), 83-99. DOI: 10.15366/reice2016.14.1.005

Onohara, M. M. (2018). Componentes pedagógicos oferecidos na pós-graduação stricto sensu em Ciências Contábeis no Brasil. Trabalho de conclusão de curso, Faculdade de Ciências Contábeis, Universidade Federal de Uberlândia. Retrieved from: https://repositorio.ufu.br/bitstream/123456789/23746/3/ComponentesPedagogicosOferecidos.pdf

Parecer nº. 977. (1965, December 03). Definição dos cursos de pós-graduação. Retrieved from: www.capes.gov.br/images/stories/download/legislacao/Parecer_CESU_977_1965.pdf

Patrus, R., & Lima, M. C. (2014). A formação de professores e de pesquisadores em Administração: contradições e alternativas. Revista Economia e Gestão, 14(34), 4-29. https://doi.org/10.5752/P.1984-6606.2014v14n34p4

Patrus, R., Shigaki, H. B., & Dantas, D. C. (2018). Quem não conhece seu passado está condenado a repeti-lo: distorções da avaliação da pós-graduação no Brasil à luz da história da CAPES. Cadernos EBAPE.BR, 16(4), 642-655. https://doi.org/10.1590/1679-395166526

Raineri, N. (2013). The PhD program: between conformity and reflexivity. Journal of Organizational Ethnography, 2(1), 37-56. https://doi.org/10.1108/JOE-04-2012-0021

Raineri, N. (2015). Business doctoral education as a liminal period of transition: comparing theory and practice. Critical Perspectives on Accounting, 26, 99-107. https://doi.org/10.1016/j.cpa.2013.11.003

Rebele, J. E., & Pierre, E. K. S. (2015). Stagnation in accounting education research. Journal of Accounting Education, 33(2), 128-137. DOI: 10.1016/j.jaccedu.2015.04.003

Schnader, A. L., Westermann, K. D., Downey, D. H., & Thibodeau, J. C. (2016). Training teacher-scholars: a mentorship program. Issues in Accounting Education, 31(2), 171-190. https://doi.org/10.2308/iace-51041

Silva, C. F., Ferreira, L. V., Leal, E. A., & Miranda, G. J. (2019). Formação docente na área contábil: contribuições da disciplina de metodologia do ensino oferecida na pós-graduação stricto sensu. Sociedade, Contabilidade e Gestão (UFRJ), 14, 144-162. https://doi.org/10.21446/scg_ufrj.v0i0.23062

Silva, S. M. C. da. (2016). Tetos de vitrais: gênero e raça na Contabilidade no Brasil. Tese de doutorado, Faculdade de Economia, Administração e Contabilidade, Universidade de São Paulo. DOI: 10.11606/T.12.2016.tde-03082016-111152

Slomski, V. G., & Martins, G. A. (2008). O conceito de professor investigador: os saberes e as competências necessárias à docência reflexiva na área contábil. Revista Universo Contábil, 4(4), 6-21. http://dx.doi.org/10.4270/ruc.20084

Wille, S. B. (2018). “Feliz aquele que transfere o que sabe e aprende ensinando”: refletindo sobre ações de formação docente na pós-graduação em Contabilidade. Tese de doutorado, Faculdade de Economia, Administração e Contabilidade, Universidade de São Paulo. DOI: 10.11606/T.12.2018.tde-06112018-115030

Notes

Author notes

The results show a concerning scenario about faculty training in Accounting that has direct and indirect consequences on teaching and research quality in the field. Our reflections can guide training actions in doctoral courses in Accounting and support actions by regulatory bodies and associations representing PPGCCs.

Corresponding author Tel. +44 (0141) 330-3993, E-mail: camillasn@ufu.br (C. S. N. Nganga); silvianova@usp.br (S. P. de C. Casa Nova); joaopaulo.lima@glasgow.ac.uk (J. P. R. de Lima), Adam Smith Business School. West Quadrangle, Gilbert Scott Building. G12 8QQ - Glasgow/UK, Scotland