Article

The effects of dark personality traits on the relationship between competitive climate and budget participation

Os efeitos dos traços sombrios de personalidade na relação entre clima competitivo e participação no orçamento

Amanda Beatriz Nasatto Corrêa amandanasatto10@hotmail.com

Carlos Eduardo Facin Lavarda elavarda@gmail.com

Amanda Beatriz Nasatto Corrêa amandanasatto10@hotmail.com

Carlos Eduardo Facin Lavarda elavarda@gmail.com

The effects of dark personality traits on the relationship between competitive climate and budget participation

Revista de Contabilidade e Organizações, vol. 16, e196853, 2022

University of São Paulo

Received: 21 April 2021

Accepted: 12 September 2022

Published: 23 December 2022

Abstract: This study aims to determine the influence of competition on budget participation, moderated by dark personality traits (machiavellianism, psychopathy, narcissism, and sadism). The research used a quantitative, descriptive, and experimental approach. The sample comprises 170 valid answers from undergraduate students in administration, accounting, and economics programs offered at public and private higher education institutions. The analysis used descriptive statistics to categorize the respondents. Also, partial least squares approach to structural equation modeling (PLS-SEM) was adopted using the SmartPLS-version 3 software to verify the research hypotheses. The results show that the presence of competition affects managers’ behavior and leads them to increase participation in budget setting. When evaluating the effect of narcissistic personality moderation on this relationship, individuals tend to decrease their budget participation. The direct effect of machiavellianism on budget participation is positive. The relationships between the moderating effect of machiavellianism and psychopathy, and the direct effect of psychopathy and narcissism on budget participation, did not show statistical significance. Overall, it is concluded that competition, the moderating effect of narcissism, the direct effect of machiavellianism, and demographic variables, such as gender, age group, and undergraduate program, can be considered antecedents of budget participation. This research allows managers to deepen their knowledge about the antecedents of budget participation and enables the verification of the effect of competition and dark personality traits in the organizational environment.

Keywords: Competition, Budget participation, Personality traits, Dark triad, Dark tetrad.

Resumo: O objetivo deste estudo é determinar a influência da competição na participação no orçamento, moderada pelos traços sombrios de personalidade (maquiavelismo, psicopatia, narcisismo e sadismo). A pesquisa utilizou uma abordagem quantitativa, descritiva e experimental. A amostra é composta de 170 respostas válidas de acadêmicos dos cursos de administração, ciências contábeis e ciências econômicas de instituições de ensino superior públicas e privadas. Na análise dos dados, foram utilizadas estatísticas descritivas para categorizar os respondentes e técnica de Modelagem de Equações Estruturais (MEE) estimada a partir de Mínimos Quadrados Parciais (Partial Least Squares - PLS), por meio do software SmartPLS-versão 3, utilizadas para verificação das hipóteses de pesquisa. Com esses resultados, estima-se que a presença da competição afeta o comportamento dos colaboradores, e faz com que o colaborador aumente a participação no processo orçamentário. Ao avaliar o efeito da moderação da personalidade narcisista nessa relação, os indivíduos tendem a diminuir sua participação no orçamento. Já o efeito direto do maquiavelismo na participação no processo orçamentário é positivo. As relações do efeito moderador do maquiavelismo e psicopatia, e o efeito direto da psicopatia e narcisismo na participação no orçamento, não apresentaram significância estatística. No geral, conclui-se que a competição pode ser considerada antecedente da participação no orçamento, assim como o efeito moderador do narcisismo, o efeito direto do maquiavelismo e de variáveis demográficas, como gênero, faixa etária e curso. A pesquisa possibilita aos gestores aprofundar o conhecimento a cerca dos antecedentes da participação no orçamento, além de possibilitar a constatação do efeito da competição e dos traços sombrios de personalidade no ambiente organizacional.

Palavras-chave: Competição, Participação no orçamento, Traços de personalidade, Dark triad, Dark tetrad.

1 INTRODUCTION

Experimental research has shown increased interest in budget participation and managers’ behavior toward reporting (Naranjo et al., 2017; Schreck, 2015). However, a substantial part of the studies has focused on the consequences of participation in budget setting and not on its antecedents (Weiskirchner-Merten, 2020; Hopwood, 1976; Brownell, 1982; Young, 1988; Bimberg et al., 1990).

For Lau et al. (2018), new studies should address which factors motivate employees to participate in budget setting and how these factors influence such participation. For Fletcher et al. (2008), intraorganizational competition depends on the individual’s characteristics and context. Thus, competition and budget participation can be studied together. Furthermore, Mahlendorf et al. (2015) suggest addressing variables that analyze how the employee’s personality and context can indirectly influence budget participation, as potential interaction effects are not sufficiently explored in the literature.

Studies on managers’ personality traits point out individuals’ preferences regarding budget setting, the effects on the relationship between budget participation and performance, and other variables in this relationship (Lunardi et al., 2019). For Suchanek (2021), there is a literature gap in research about dark personality traits combined with behavioral biases, while Nguyen et al. (2021) point out a gap in studies adopting a person-centered approach to examining these traits.

Given this context, the article intends to answer the following research question: what is the influence of competition on budget participation moderated by dark personality traits? The study aims to determine the influence of competition on participation in budget setting moderated by machiavellianism, psychopathy, narcissism, and sadism.

This study addresses the gap observed by Nguyen et al. (2021) and adopts a person-centered approach to examine dark personality traits in the organizational context. The dark personality traits that make up the dark tetrad (Paulhus, 2014) are explored as antecedents of budget participation, as recommended by Mahlendorf et al. (2015), Weiskirchner-Merten (2020), and Lau et al. (2018).

In addition, the research follows the suggestion from Kay and Saucier (2020) and O’Boyle Jr. et al. (2012) and explores the behavior of individuals with dark personality traits in their organizational activities. The sample comprised undergraduate business students, contributing to filling the gap identified by Bailey (2019), who suggests that new research should include sociodemographic variations considering the students’ countries.

The study’s contribution to the literature on dark personality traits lies in verifying this theme’s direct and moderating relationships and demonstrating the ability of these traits to progress in the corporate context (D’Souza & Jones, 2017). The literature on the negative results of dark personality traits (Nübold et al., 2017) focuses only on the negative side of these individuals in the organization, leaving a gap in exploring positive aspects. Wu and Lebreton (2011) point out that several studies focused, for example, on leadership, justice, and business ethics, benefit from the insights these personality traits provide.

As practical contributions, this study offers insights for recruiters or employees working in people management departments when choosing profiles for specific or managerial positions. In addition, the research suggests that managers focus on reflecting their attitudes and those of their employees in the organizational environment (D’Souza & Jones, 2017). The findings allow managers to deepen their knowledge about the antecedents of participation in budget setting and verify the effect of competition and dark personality traits in the organizational environment.

2 THEORETICAL FRAMEWORK

2.1 Participation in budget setting and competition

Employee motivation to define the budget is consolidated through participation (Lau et al., 2018). When participating in budget setting, employees believe that their opinions are valuable for distributing resources and defining goals (Tokilov et al., 2019).

Generally, a budget-setting process can motivate subordinates (Birnberg et al., 2007; Dani et al., 2017; Derfuss, 2016) when implemented with their participation (Lunardi et al., 2019), i.e., with managers involved in budgeting preparation, execution, and control (Monteiro et al., 2021). According to Dani et al. (2017), the level of participation and understanding of this process can influence managers’ behaviors.

The findings of Schreck’s (2015) experimental study demonstrate that participants tend to report honestly, even with competitive economic pressure. However, this tendency decreased with the introduction of rivalry competition, which led to an increase in false statements and individual earning maximization by misrepresenting private information.

Competition may be positive or negative (Keller et al., 2016). Positive because individuals have the instinct to compete with each other (Deci & Ryan, 2000; Keller et al., 2016), increasing motivation and attention to the task and, consequently, improving performance (Fletcher et al., 2008). However, negative behaviors may be instigated, for example, harming others or exploiting oneself (Kohn, 1992).

Organizations have a high level of competition due to individuals’ natural tendency to compete with each other (Deci & Ryan, 2000; Keller et al., 2016). Thus, competitive employees commit to the organization when noticing a high level of competition (Lam, 2012). When they realize that their personality and the organizational context coincide (Lam, 2012) - since participation in budget setting converges the employees’ goals with the objectives of the organization - they are motivated to achieve organizational objectives (Siallagan et al., 2017) increasing their participation in budget preparation and development.

Competition involves different reward distribution views, performance comparison with peers, internal competition, and social status comparison (Fletcher et al., 2008; Li et al., 2016). Another aspect of competition is rivalry, which tends to extend the psychological effects of economic pressure (Schreck, 2015). Rivalry awakens the desire to win through social comparison in situations of competitive performance, especially if it discloses information about the competitors’ performance (Schreck, 2015).

Given these findings, the following research hypothesis is formulated:

-

H1: Competition favors participation in budget setting.

The competitive environment is relevant for dark personality traits (McLarnon & Tarraf, 2017; Nübold et al., 2017). Consequently, it is possible to explore the relationships between these traits and the perceived work environment (Spurk & Hirschi, 2018).

2.2 Dark personality traits

The dark personality trait is a relatively recent topic in academic studies, emerging due to its usefulness for psychologists interested in personality factors (Bailey, 2019). Research involving traits of machiavellianism, psychopathy, narcissism, and everyday sadism are labeled as dark tetrad (Buckels et al., 2013; Paulhus, 2014).

According to Koehn et al., (2019), studying personality traits coupled with evolutionary models of personality is likely to offer comprehensive and new ways of understanding these traits. For the authors, because research on sadism is in its initial stage, studies should dedicate to determining where, why, and how this trait is important and useful to add it to the dark triad.

Zeigler-Hill and Besser (2019) focused on the role difficulties in self-functioning and identity play in the relationship between dark personality and workplace outcomes. Harrison et al. (2018) found that the traits that make up the dark triad are relevant psychological antecedents of fraudulent behavior.

However, each trait affects a certain part of the decision-making regarding the unethical process. For example, narcissism leads individuals to act unethically for their particular privilege. Machiavellianism goes further, changing perceptions about opportunities in order to deceive others, whereas psychopathy differs in how individuals rationalize their fraudulent behavior (Harison et al., 2018).

Paulhus (2014) offers characteristics of these traits. For the author, a Machiavellian is a strategist and is cautious when taking advantage, while narcissists lack empathy for individuals they “walk over” while seeking public appreciation. Psychopaths, on the other hand, take what they want and do not care if they hurt others, and sadists look for opportunities to observe people or induce suffering in others.

The findings of D’Souza, Lima, Jones, and Carré (2019) demonstrate that the moderating effect of the dark triad traits is significant and positive in the relationship between maximizing personal and company gains. In addition, these findings reveal the common characteristics of manipulation, insensitivity, and dishonesty when exploring the interactive effect between the dark traits (D’Souza et al., 2019).

Individuals with the highest level of a dark trait can be selected for specific occupations, thus becoming valuable assets. Kay and Saucer (2020) argue that these individuals add value to the organization and advocate further research on this issue.

Competition can be used as an indicator of the perceived environment, as the dark personality is attracted (Jonason et al., 2015) and significantly affected by competitive situations in the organizational context (Nübold et al., 2017). The competitive environment has high relevance for dark personality traits (McLarnon & Tarraf, 2017; Nübold et al., 2017), and consequently, it is worth studying the relationships between these traits and the perceived work environment (Spurk & Hirschi, 2018).

Jonason et al. (2015) found that competitiveness tends to be stressful for all individuals. Thus, an extreme level of competition can cause damage to the organization and work teams. According to Spurk and Hirschi (2018), there are positive relationships between the dark triad, its sub-traits, and competition, highlighting that dark behavior is more common in the older age group (50-59 years) when compared to young adults from 25-34 years old. However, there was no difference between age groups regarding the relationship between competition and change in dark traits or their sub-traits.

In view of the positive relationship that Spurk and Hirschi (2018) found between dark traits and competition, the traits can also be useful for the organization in certain job positions (Kay & Saucier, 2020). Thus, the expectation is that the dark traits of mid-level managers will increase their participation in budget setting in a competitive environment. Thus, the following research hypotheses are formulated:

-

H2a: Machiavellianism moderates the relationship between competition and budget participation.

-

H2b: Psychopathy moderates the relationship between competition and budget participation.

-

H2c: Narcissism moderates the relationship between competition and budget participation.

-

H2d: Sadism moderates the relationship between competition and budget participation.

3 METHODOLOGY

This research is quantitative, descriptive, and experimental. The population comprises business students in undergraduate administration, accounting, and economics programs at public and private Brazilian universities. Experimental research with students has shown results compatible with research with practitioners (Lakey et al., 2008; Majors, 2016).

Human resources departments focus on research conducted with business students since these individuals will likely be in managerial positions soon and have a high potential to generate dysfunctional organizational behaviors (Bogdanovic et al., 2018). For the authors, applying this type of research helps predict the professionals’ economic efficiency and prevents unwanted economic outcomes in different organizations.

The hypotheses were tested through a mixed experiment with a 1 (between-subjects) x 4 (within-subjects) factorial design. The study followed Aguiar (2017), who recommended participant randomness as there were two different variables (budget participation and dark personality traits) (Aguiar, 2017).

Data collection was conducted by contacting the coordinators of undergraduate administration, accounting, and economics programs via e-mail, asking them to forward the link with the research instrument to the students. The research instrument was available online from March 08, 2021, to May 31, 2021. A cover letter accompanied the instrument with information on ethical commitments. A total of 1,644 students accessed and responded to the questions. However, the average completion rate was 13% (14% for the control group and 12% for the experimental group), and the final sample consisted of 170 valid responses, which is an adequate number, according to Aguiar (2017). On average, 87% of the responses received were incomplete, and 3% were invalidated because they were answered by students from other undergraduate programs not targeted in this study or because the responses were unrelated to the questions.

The dependent variable - budget participation - was evaluated based on the adaptation of the experiment by Gallani et al. (2019). In this experimental research, the participants took on the role of a company’s production manager and were the bearers of a classified piece of information (the real production cost).

The research instrument instructed the respondents about their role as production department managers. Their responsibility includes submitting a budget request to their superior (the manager of the company’s division) for the next period of activities. After completing the request, the research instrument was set to reply to the participant approving the solicitation or granting more or less budget, considering whether the participant was in the control or experimental group. The reply from the research instrument offered the participant information on the budget for each period. Thus, the participant had to perform this task four times, starting with a known production cost to prepare the budget request for the second period, using the reply to prepare the request for the third period, and so on.

After completing this task, the participants evaluated their participation in the budget using the Milani instrument (1975), adapted by Leach-López et al., (2007), on a 7-point Likert scale. The independent variable in the evaluation of budget participation was competition in the organizational environment, adapted from Schreck (2015).

The moderating variable - dark personality traits - was measured using the short dark triad (SD3) instrument developed by Jones and Paulhus (2014) and O’Meara et al. (2011), translated by D’Souza and Lima (2019), which consists of 27 items, 9 items for each trait (machiavellianism, psychopathy, and narcissism), with a 7-point Likert scale (1 = disagree totally; 7 = totally agree).

The use of SD3 is widespread in the literature (Bogdanovic et al., 2018; Dinic et al., 2020; D’Souza & Lima, 2019; D’Souza et al., 2019; Jonason et al., 2018; Heym et al., 2019; Kayani et al., 2019; Kay & Saucir, 2020; Kowalski et al., 2018; McKee et al., 2017; Sekscinska & Rudzinska-Wojciechowska, 2020; Wu et al., 2019). Table 1 presents the research variables.

Finally, data on demographic variables were collected (gender, age, undergraduate program, type of university, experience in the job market). For Hambrick (2007), the demographic variables age and work experience influence the individuals’ personalities. Age is a demographic variable of interest for human resources practices since perceptions about the work environment are related to the change in personality of older employees (Spurk & Hirschi, 2018), while gender is strongly related to dark personality traits (Carter et al., 2015). The variable “region” refers to the location of the respondents in Brazil. The use of this variable is justified since it has been used in other national studies such as Luca et al. (2011) and Lucena et al. (2021). Finally, the variable “type of university” may influence the individual’s dark personality traits (Bailey, 2019).

Participants were randomly assigned (through the Google App script tool) one of two scenarios when clicking on the link to participate in the experiment: the control group and the experimental group. This tool controls the number of responses to strike a balance between the two scenarios. The groups were equivalent so any differences are attributed to exposure to the levels of independent variables (Babbie, 2010). Each scenario was developed in a single experimental session.

The experimental group was submitted to the treatment of competition, using the modes of competition in the study by Schreck (2015) - rivalry and economic pressure. The participants were induced to perceive economic pressure in the allocation of resources for production by a superior manager, considering the amount approved for the next period. The control group was not submitted to the competition for resources. The participants simply had to report the production cost they believed necessary for the next period, i.e., the competition did not influence the production manager’s participation in the budget setting.

As there was no competition in this organization and dispute for resources, in the first two periods, the participants already noticed that regardless of the amount they requested as production cost, the superior manager in all periods would approve the maximum cost, i.e., BRL 8.00. Given this context, participants had a strong economic incentive to overestimate their production costs. The superior manager’s neglect to analyze the budget was necessary to test whether dark personality traits would encourage participants to maximize budget slack by misrepresenting the classified information (production cost).

The analysis used descriptive statistics to categorize the respondents. Also, partial least squares approach to structural equation modeling (PLS-SEM) was adopted using the SmartPLS-version 3 software. PLS helps to address the theoretical requirements flexibly, as it allows testing parts of a theoretical model indicated in the literature. This is possible since the approach was designed for small samples (less than 200 cases) (Sosik et al., 2009).

4 RESULTS ANALYSIS

4.1. Testing the research hypotheses

The respondents were mostly female (56.5%), aged between 17 and 22 years (39.4%), from the southern region of Brazil (45.3%), studying at a public university (63.5%), studying administration (45.9%), in the 4th year of the program (30%), with market experience (58.2%).

The hypotheses were tested using PLS-SEM. The approach implied: a) evaluating the measurement model (testing the validity and reliability of the model constructs); and b) analyzing the structural model (verifying path coefficients and statistical validity of the relationships between the constructs).

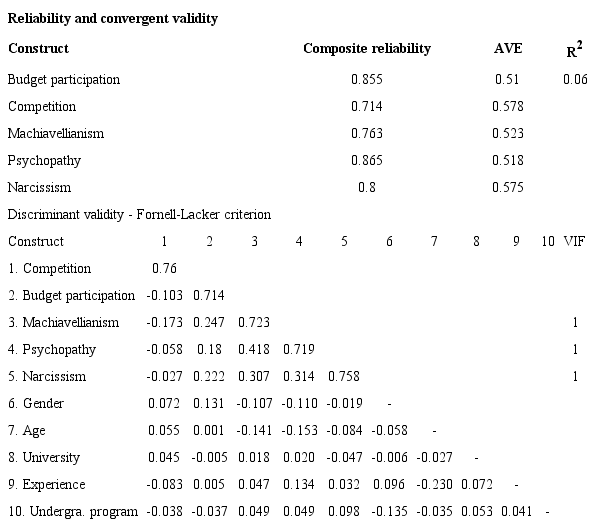

Table 2 presents the measurement model’s validity and reliability criteria (Ringle et al., 2014). When analyzing the composite reliability, all investigated constructs obtained values greater than 0.7. Next, convergent validity was verified using the Average Variance Extracted (AVE). All constructs had values greater than 0.5, corroborating Hair Jr. et al. (2016).

The Fornell-Lacker criterion recognizes that the constructs are different from each other (Hair et al., 2016), and it was used to verify the model’s discriminant validity. Finally, the analysis observed the absence of multicollinearity, given that the variance inflation factor (VIF) values were less than 5, as Hair et al. (2016) recommended.

Table 2 does not show the results for sadism because the construct was excluded from the model. All assertions presented negative coefficients; therefore, it was impossible to test the construct’s reliability and validity. This finding differs from the studies by O’Meara et al. (2011) and Buckels et al. (2013), where the construct was valid.

The next step was interpreting the structural model and observing and analyzing the relationships between the constructs using a trend scheme with statistical validity (Hair et al., 2016). The interpretation was carried out by applying bootstrapping techniques (with rotation of 5,000 subsamples) and blindfolding. This interpretation allowed us to examine the hypotheses (Table 3).

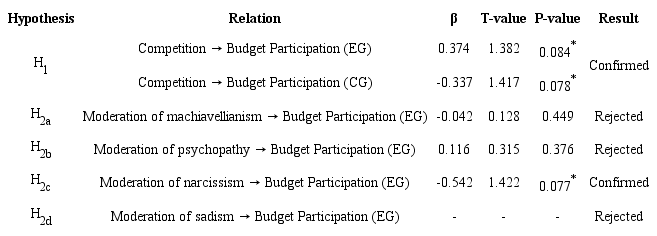

It is worth stressing that there was no inference of competition in the control group, meaning that competition’s effect on budget participation was not measured. On the other hand, there was an inference of competition in the experimental group, and it was possible to analyze whether the presence of this independent variable modified the participants’ behavior. Thus, the experimental group showed that competition positively and significantly affected participation in budget setting (β = 0.374, p = 0.084), and in the control group, the absence of competition negatively and significantly affected participation (β = - 0.337, p = 0.078). Such results confirmed H1 (significance level of 10%), which shows that the control group’s participation in budget setting is greater.

Next, the moderation of dark personality traits (machiavellianism, psychopathy, narcissism, and sadism) was tested individually concerning competition and budget participation. To capture the effect of competition on budget participation, only the experimental group’s results are observed.

* = significance level of 10%. EG = experimental group. EC = control group

First, the moderating effect of machiavellianism was tested, which proved negative and insignificant in the relationship between competition and budget participation (β = - 0.042, p = 0.449), thus rejecting H2a. When testing the moderating effect of psychopathy, this moderation in the relationship between competition and budget participation was positive and not significant (β = 0.116, p = 0.376), thus rejecting H2b.

The moderating effect of narcissism showed that the moderation of narcissism in the relationship between competition and participation in the budget has a negative and significant effect (β = - 0.542, p = 0.077). Thus, H2c was accepted at the significance level of 10%.

Finally, the moderating effect of sadism on the relationship between competition and budget participation could not be evaluated because the construct did not show validity and reliability in the measurement model. Figure 1 presents the results of the relationships proposed in the model.

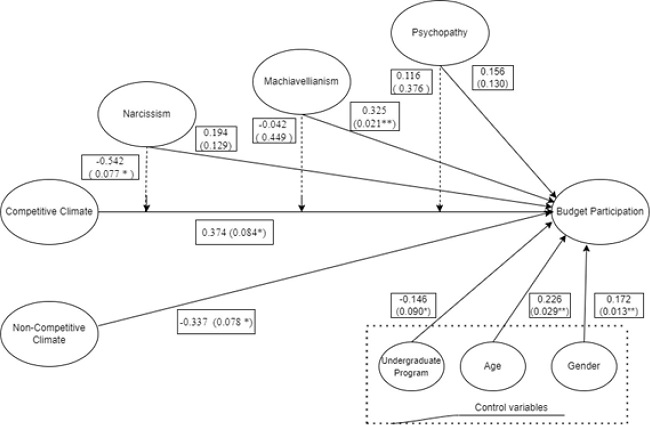

Figure 2

Structural model

Note 1: * = significance level of 10%; ** = significance level of 5%.Note 2: Dashed line indicates the moderator effect.Source: Elaborated by the authors.

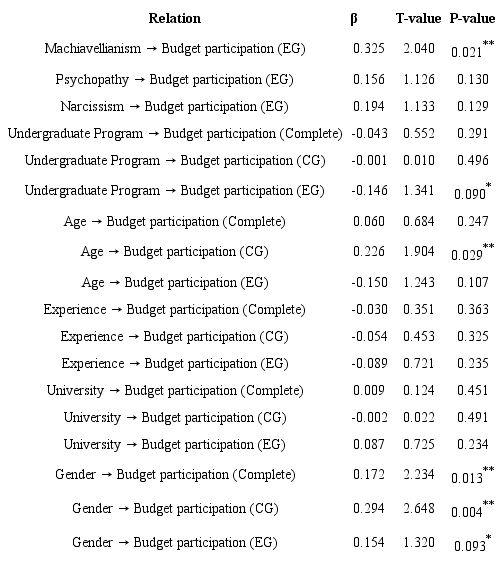

Additional tests were performed (Table 4) to test the direct effect of dark traits on budget participation. Machiavellianism positively and significantly affected budget participation at a level of 5% (β = 0.325, p = 0.021). Therefore, individuals with machiavellian personalities tend to participate more in the budgeting process. Psychopathy and narcissism positively affect budget participation (β = 0.156, p = 0.130; β = 0.194, p = 0.129, respectively).

* = signifigance level of 10%;** = significance level of 5%. EG = experimental group. EC = control group.

In addition to testing the direct effect of dark traits, the effect of demographic variables on budget participation was tested. For the experimental group, the undergraduate program variable negatively and significantly affected (at the 10% significance level) budget participation (β = - 0.146, p = 0.090). Therefore, accounting students tend to participate less in budget setting than administration and economics students.

For the control group, the age variable positively and significantly affected (at the 5% significance level) budget participation (β = 0.226, p = 0.029). Thus, older individuals - over 29 years old - tend to participate more in budget setting.

In both groups (control and experimental), the gender variable affected participation in a positive and significant way (5% level) (β = 0.172, p = 0.013). Thus, women tend to participate more in budget setting.

4.2. Discussion of results

The results of the structural model’s evaluation support the discussion of the research findings considering the literature. Hypothesis H1 considered the direct relationship between competition and budget participation, suggesting that the experimental group, exposed to the competition variable, obtained greater participation in budget setting. H1 was confirmed, and the effects of competition on budgetary practices were corroborated (β = 0.374; p = 0.084).

This finding is aligned with Schreck (2015), who found that managers, even in the face of competition arising from economic pressure, requested values more honestly. In addition, it reinforces the finding of Brown et al. (1998) that competition has direct positive effects on establishing organizational goals.

The complementary results between the experimental and control groups confirming that competition can be a characteristic related to the environment (Fletcher et al., 2008). The level of participation depended on the context the participant was exposed to (presence or absence of competition in the organizational environment).

The confirmation of H1 reveals one more positive aspect of the competition to be added to the literature: competition helps in elaborating and defining the budget (Keller et al., 2016). Thus, this study corroborated Fletcher et al. (2008) and Deci and Ryan (2000) that competition is a context-dependent characteristic, considering that the environment in which the individual was inserted changed their level of budget participation. This means that competition and budget participation are elements that predict subordinates’ motivation to participate in budget setting.

Due to non-significant results, hypotheses H2a and H2b were rejected (β = - 0.042, p = 0.449; β = 0.116, p = 0.376, respectively). Both results differ from Nübold et al. (2017), who estimate that dark traits are significantly affected by competitive situations in the workplace. Hypothesis H2c was accepted (β = - 0.542, p = 0.077), thus demonstrating that narcissism has a negative and significant moderating effect on the relationship between competition and budget participation.

Therefore, the more the individual presents narcissistic personality traits, the less budget participation in a competitive organization. This result is in line with Nübold et al. (2017), who show that narcissism is significantly affected by organizational competition, and with the finding of Jonason et al. (2015) that narcissists do not see their workplace as competitive.

However, this finding is not consolidated in the literature. For example, Spurk and Hirschi (2018) found that, in general, the relationship between dark personality traits and competition is positive, while Jonason et al. (2015) generalized that the dark personality is attracted by competition.

It was possible to observe that competition for budgetary resources between departments/units in the perception of narcissists imposes many restrictions in a way that does not arouse the interest of this personality type. It is known that narcissists are only concerned with being powerful and superior to others (Raskim & Terry, 1988).

However, the differences in the findings when observing the traits that make up the dark triad corroborate the recommendation by Jonason et al. (2015) to evaluate traits separately and at an individual level. Each dark trait has a different moderating effect: i) the results were not significant for the machiavellian and the psychopath personalities in the face of competition, while ii) the narcissistic personality exposed to competition results in less budget participation.

As for the direct effect of dark personality traits (machiavellianism, psychopathy, and narcissism) on budget participation, the machiavellian individual tends to participate in budget setting. However, the results do not have statistical significance for individuals with traits of psychopathy and narcissism.

This finding differs from the fact that only the level of budget participation influences managers’ behavior (Dani et al., 2017). In this case, it is observed that personality, more specifically machiavellian, can also influence participation in the budget process.

The study compared the divergent results between the moderating relationships and direct relationships of machiavellian and narcissistic personality traits. Machiavellianism, in the moderating effect, played the role of inhibiting budget participation in a competitive context. However, when the machiavellian individual is not exposed to competition, the direct relationship between this personality and budget participation tends to be positively and significantly affected.

This change in the effects of relationships reinforces that the machiavellian personality can be changeable under the action of external stimuli (Bereczkei, 2015). Furthermore, machiavellians are considered capable of doing whatever is needed to achieve their goals (Mendonça et al., 2018).

As in machiavellian, the narcissistic personality found a difference in the effects of their relationships. Narcissistic moderation had a negative and significant effect and a direct and positive effect with no statistical significance. Narcissists have a sense of self-importance that encourages greedy or selfish attitudes (Bailey, 2019). It is possible to say that the moderation effect was negative because competition motivates the sense of self-importance of this personality type. Thus, the individual has selfish attitudes, such as not participating in budget setting. On the other hand, the absence of competition does not stimulate this sense of self-importance, which entails participation in budget setting.

Thus, the results of this study indicated that budget participation could be directly affected in two ways: i) positive: by competition, machiavellianism, gender, and age group; ii) negative: by the undergraduate program. In addition, budget participation can be enhanced by moderating variables, in this case, by narcissism.

5 CONCLUSION

This study examined the influence of competition on budget participation moderated by dark personality traits (machiavellianism, psychopathy, narcissism, and sadism) with a sample of 170 undergraduate students in administration, accounting, and economics programs offered at public and private higher education institutions in Brazil.

The results confirmed that competition influences managers’ budget participation. Thus, the individual exposed to competition is positively related to budget participation. In general, competition can be considered an antecedent of budget participation, as are the moderating effect of narcissism and the direct effect of machiavellianism and demographic variables, such as i) gender, ii) age group, and iii) undergraduate program.

This study contributes to the literature and offers some practical implications. Its empirical results can help in studies dealing with the role of budget participation in the workplace to develop more complete models.

The findings add to the literature on competition and budgetary practices by suggesting that the distribution of budget values between departments/units can also contribute to competition. Also, the results confirm that the moderating effect of narcissism, the direct effect of machiavellianism, and gender, age group, and course can be considered antecedents of budget participation.

As practical contributions, the findings enable organizations and top managers to understand the conditions under which mid-level managers participate or not in budget setting. The organization benefits from analyzing the work environment’s positive and negative effects on the mid-level managers’ behavior and how personality traits affect the organizational climate and budgeting practices. This study contributes to public administration indirectly by benefiting organizations in general that end up impacting the government.

It was possible to identify that machiavellian and narcissistic personalities are suitable for organizations that do not have competition and aim to increase the mid-level managers’ participation in budget setting. It is recommended that machiavellians in non-competitive work environments assume mid-level managerial positions due to the budget participation seen in this experiment.

The study has limitations and recommendations for future research. The low statistical significance in the moderation effects of machiavellian and psychopathic personality on the relationship between competition and budget participation and the direct effects of narcissists and psychopaths on budget participation, it is suggested that studies address this effect in other samples to deepen the results of these traits in the organizational environment. The impossibility of affirming the validity and reliability of the sadism construct is a limitation of the study and future research should expand the sample. Finally, due to the complexities of the individuals’ responses regarding the dark personality traits, the study is subject to the effects of other variables not adressed in this research.

Future research could adopt and use control instruments to mitigate different effects on human behavior. In addition, the findings encourage further studies encompassing other variables that can also be considered antecedents of budget participation and deepen the discussion of the dark traits in budgetary practices.

REFERENCES

Aguiar, A. B. (2017). Pesquisa experimental em contabilidade: propósito, desenho e execução. Advances in Scientific and Applied Accounting, 10(2), 224-244. https://doi.org/10.14392/asaa.2017100206

Babbie, E. (2010). The Practice of Social Research, 12a ed. California, Wadsworth Cengage Learning.

Bailey, C. D. (2019). The joint effects of narcissism and psychopathy on accounting students’ attitudes towards unethical professional practices. Journal of Accounting Education, 49, 100635. https://doi.org/10.1016/j.jaccedu.2019.08.001

Bereczkei, T. (2015). The manipulative skill: Cognitive devices and their neural correlates underlying Machiavellian’s decision making. Brain and Cognition, 99, 24-31. https://doi.org/10.1016/j.bandc.2015.06.007

Birnberg, J. G., Luft, J., & Shields, M. D. (2007). Psychology theory in management accounting research. In. Chapman, C. S.; Hopwood, A. G.; Shields, M. D. Handbooks of Management Accounting Research, 1(4), 113-135. DOI: https://doi.org/10.1016/S1751-3243(06)01004-2

Bimberg, J., Shields, M., & Young, S. M. (1990). The case for multiple methods in empirical management accounting research (with an illustration from budget setting). Journal of Management Accounting Research, 2, 33-66.

Bogdanović, M., Vetráková, M., & Filip, S. (2018). Dark triad characteristics between economics & business students in Croatia & Slovakia: what can be expected from the future employees? Entrepreneurship and Sustainability Issues, Entrepreneurship and Sustainability Center, 2018, 5 (4), 967-991. https://doi.org/10.9770/jesi.2018.5.4(19)

Brown, S. P., Cron, W. L., & Slocum Jr., J. W. (1998). Effects of trait competitiveness and perceived intraorganizational competition on salesperson goal setting and performance. Journal of Marketing, 62, 88-98. https://doi.org/10.1177/002224299806200407

Brownell, P. (1982). Participation in the budgeting process: when it works and when it doesn’t. Journal of Accounting Literature, I, 124-150.

Buckels, E. E., Jones, D. N., & Paulhus, D. L. (2013). Behavioral confirmation of everyday sadism. Psychological science, 24(11), 2201-2209. https://doi.org/10.1177/0956797613490749

Carter, G. L., Campbell, A. C., Muncer, S., & Carter, K. A. (2015). A Mokken analysis of the Dark Triad ‘Dirty Dozen’: Sex and age differences in scale structures, and issues with individual items. Personality and Individual Differences, 83, 185-191. https://doi.org/10.1016/j.paid.2015.04.012

Dani, A. C., Zonatto, V. C. S., & Diehl, C. A. (2017). Participação Orçamentária e Desempenho Gerencial: Uma Meta-Análise das Relações Encontradas em Pesquisas Desenvolvidas na Área Comportamental da Contabilidade. Advances in Scientific and Applied Accounting, 10(1), 54-72. DOI: 10.14392/ASAA.2017100104

Deci, E. L., & Ryan, R. M. (2000). The" what" and" why" of goal pursuits: Human needs and the self-determination of behavior. Psychological Inquiry, 11(4), 227-268. https://doi.org/10.1207/S15327965PLI1104_01

Derfuss, K. (2016). Reconsidering the participative budgeting-performance relation: A meta-analysis regarding the impact of level of analysis, sample selection, measurement, and industry influences. The British Accounting Review, 48(1), 17-37. https://doi.org/10.1016/j.bar.2015.07.001

Dinić, B. M., Wertag, A., Tomašević, A., & Sokolovska, V. (2020). Centrality and redundancy of the Dark Tetrad traits. Personality and Individual Differences, 155, 109621. https://doi.org/10.1016/j.paid.2019.109621

D’Souza, M. F., & Jones, D. N. (2017). Taxonomia da rede científica do Dark Triad: revelações no meio empresarial e contábil. Revista de Educação e Pesquisa em Contabilidade, 11(3), 296-313. https://doi.org/10.17524/repec.v11i3.1588

D'Souza, M. F., & Lima, G. A. S. F. (2019). Um olhar sobre os traços do dark triad e os valores culturais de estudantes de contabilidade. Advances in Scientific and Applied Accounting, 161-183. https://doi.org/10.14392/ASAA.2019120109

D’Souza, M. F., Lima, G. A. S. F. D., Jones, D. N., & Carré, J. R. (2019). Do I win, does the company win, or do we both win? Moderate traits of the Dark Triad and profit maximization. Revista Contabilidade & Finanças, 30(79), 123-138. https://doi.org/10.1590/1808-057x201806020

Fletcher, T. D., Major, D. A., & Davis, D. D. (2008). The interactive relationship of competitive climate and trait competitiveness with workplace attitudes, stress, and performance. Journal of Organizational Behavior: The International Journal of Industrial, Occupational and Organizational Psychology and Behavior, 29(7), 899-922. https://doi.org/10.1002/job.503

Gallani, S., Krishnan, R., Marinich, E. J., & Shields, M. D. (2019). Budgeting, psychological contracts, and budgetary misreporting. Management Science, 65(6), 2924-2945. https://doi.org/10.1287/mnsc.2018.3067

Hair Jr, J. F., Hult, G. T. M., Ringle, C. & Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications, Los Angeles.

Hambrick, D. C. (2007). Upper echelons theory: an update. Academy of Management Review, 32(2), 334-343. https://doi.org/10.5465/amr.2007.24345254

Heym, N., Firth, J., Kibowski, F., Sumich, A., Egan, V., & Bloxsom, C. A. (2019). Empathy 66 at the heart of darkness: empathy deficits that bind the Dark Triad and those that mediate indirect relational aggression. Frontiers in psychiatry, 10, 95. https://doi.org/10.3389/fpsyt.2019.00095

Hopwood, A. (1976). Accounting and Human Behavior. Englewood Cliffs, NJ: Prentice Hall.

Jonason, P. K., Wee, S., & Li, N. P. (2015). Competition, autonomy, and prestige: Mechanisms through which the Dark Triad predict job satisfaction. Personality and Individual Differences, 72, 112-116. https://doi.org/10.1016/j.paid.2014.08.026

Jonason, P. K., Foster, J. D., Csatho, A., & Gouveia, V. (2018). Expectancy biases underneath the Dark Triad traits: Associations with optimism, pessimism, and hopelessness. Personality and Individual Differences, 134, 190-194. https://doi.org/10.1016/j.paid.2018.06.020

Kayani, M. B., Zafar, A., Aksar, M., & Hassan, S. (2019). Impacts of despotic leadership and dark personality trait on follower’s sense of meaningful work: moderating influence of organizational justice. International Transaction Journal of Engineering, Management, & Applied Sciences & Technologies, 11(2), 322-342. DOI: https://doi.org/10.14456/ITJEMAST.2020.35

Kay, C. S., & Saucier, G. (2020). Insert a joke about lawyers: Evaluating preferences for the Dark Triad traits in six occupations. Personality and Individual Differences, 159, 109863. https://doi.org/10.1016/j.paid.2020.109863

Keller, A. C., Spurk, D., Baumeler, F., & Hirschi, A. (2016). Competitive climate and workaholism: Negative sides of future orientation and calling. Personality and Individual Differences, 96, 122-126. https://doi.org/10.1016/j.paid.2016.02.061

Kohn, A. (1992). No contest: The case against competition (Rev. ed.). Boston: Houghton-Mifflin.

Koehn, M. A., Okan, C., & Jonason, P. K. (2019). A primer on the Dark Triad traits. Australian Journal of Psychology, 71(1), 7-15. https://doi.org/10.1111/ajpy.12198

Kowalski, C. M., Kwiatkowska, K., Kwiatkowska, M. M., Ponikiewska, K., Rogoza, R., & Schermer, J. A. (2018). The Dark Triad traits and intelligence: Machiavellians are bright, and narcissists and psychopaths are ordinary. Personality and Individual Differences, 135, 1-6. https://doi.org/10.1016/j.paid.2018.06.049

Lakey, C. E., Rose, P., Campbell, W. K., & Goodie, A. S. (2008). Probing the link between narcissism and gambling: the mediating role of judgment and decision-making biases. Journal of Behavioral Decision Making, 21(2), 113-137. https://doi.org/10.1002/bdm.582

Lam, L. W. (2012). Impact of competitiveness on salespeople's commitment and performance. Journal of Business Research, 65(9), 1328-1334. https://doi.org/10.1016/j.jbusres.2011.10.026

Lau, C. M., Scully, G., & Lee, A. (2018). The effects of organizational politics on employee motivations to participate in target setting and employee budgetary participation. Journal of Business Research, 90, 247-259. https://doi.org/10.1016/j.jbusres.2018.05.002

Leach-López, M. A., Stammerjohan, W. W., & McNair, F. M. (2007). Differences in the Role of Job-Relevant Information in the Budget Participation-Performance Relationship among US and Mexican Managers: A Question of Culture or Communication. Journal of Management Accounting Research, 19(1), 105-136. https://doi.org/10.2308/jmar.2007.19.1.105

Li, J. J., Wong, I. A., & Kim, W. G. (2016). Effects of psychological contract breach on attitudes and performance: The moderating role of competitive climate. International Journal of Hospitality Management, 55, 1-10. https://doi.org/10.1016/j.ijhm.2016.02.010

Luca, M. M. M., Gomes, C. A. S., Corrêa, D. M. M. C., & Domingos, S. R. M. (2011). Participação feminina na produção científica em contabilidade publicada nos anais dos eventos Enanpad, Congresso USP de Controladoria e Contabilidade e Congresso Anpcont. Revista de Contabilidade e Organizações, 5(11), 145-164. https://doi.org/10.11606/rco.v5i11.34790

Lucena, E. R. D. C., Silva, C. A. T., & Azevedo, Y. G. P. (2021). A influência da capacidade cognitiva nos vieses cognitivos gerados pela heurística da representatividade. Revista Brasileira de Gestão de Negócios, 23, 180-205. https://doi.org/10.7819/rbgn.v23i1.4090

Lunardi, M. A., Zonatto, V. C. S., & Nascimento, J. C. (2019). Relationship between leadership style, encouragement of budgetary participation and budgetary participation. Estudios Gerenciales, 35(150), 27-37. https://doi.org/10.18046/j.estger.2019.150.2974

Majors, T. M. (2016). The interaction of communicating measurement uncertainty and the dark triad on managers' reporting decisions. The Accounting Review, 91(3), 973-992. https://doi.org/10.2308/accr-51276

Mahlendorf, M. D., Schäffer, U., & Skiba, O. (2015). Antecedents of Participative Budgeting-A Review of Empirical Evidence. Advances in Management Accounting. 25, 1-27. https://doi.org/10.1108/S1474-787120150000025001

McKee, V., Waples, E. P., & Tullis, K. J. (2017). A desire for the dark side: An examination of individual personality characteristics and their desire for adverse characteristics in leaders. Organization Management Journal, 14(2), 104-115. https://doi.org/10.1080/15416518.2017.1325348

McLarnon, M. J., & Tarraf, R. C. (2017). The Dark Triad: Specific or general sources of variance? A bifactor exploratory structural equation modeling approach. Personality and Individual Differences, 112, 67-73. https://doi.org/10.1016/j.paid.2017.02.049

Mendonça, M. N. R., Silva, T. M. C. F., & Silva Filho, G. M. (2018). Traços sombrios de personalidade dos estudantes de contabilidade: uma investigação a partir da short dark triad (sd3). Revista Conhecimento Contábil, 6(1), 28-51.

Milani, K. (1975). The relationship of participation in budget-setting to industrial supervisor performance and attitudes: a field study. The Accounting Review, 50(2), 274-284.

Monteiro, J. J., Rengel, R., Lunkes, R. J., & Lavarda, C. E. F. (2021). Efeito da participação orçamentária no desempenho gerencial mediado pela satisfação no trabalho e justiça procedimental. Advances in Scientific and Applied Accounting, 206-226. https://doi.org/10.14392/asaa.2020130311

Naranjo, D. G., Rivero, E. J. R, & Martín, A. E. R. (2017). Efecto del locus de control en la relación entre participación presupuestaria y rendimiento: un estudio experimental. Revista de Contabilidad-Spanish Accounting Review, 20(1), 73-81. https://doi.org/10.1016/j.rcsar.2016.07.001

Nguyen, N., Pascart, S., & Borteyrou, X. (2021). The dark triad personality traits and work behaviors: A person-centered approach. Personality and Individual Differences, 170, 110432. https://doi.org/10.1016/j.paid.2020.110432

Nübold, A., Bader, J., Bozin, N., Depala, R., Eidast, H., Johannessen, E. A., & Prinz, G. (2017). Developing a taxonomy of dark triad triggers at work-A grounded theory study protocol. Frontiers in Psychology, 8, 293. https://doi.org/10.3389/fpsyg.2017.00293

O’Boyle Jr., E. H., Forsyth, D. R., Banks, G. C., & McDaniel, M. A. (2012). A meta-analysis of the Dark Triad and work behavior: a social exchange perspective. Journal of Applied Psychology, 97(3), 557. https://doi.org/10.1037/a0025679

O'Meara, A., Davies, J., & Hammond, S. (2011). The psychometric properties and utility of the Short Sadistic Impulse Scale (SSIS). Psychological Assessment, 23(2), 523. https://doi.org/10.1037/a0022400

Paulhus, D. L. (2014). Toward a taxonomy of dark personalities. Current Directions in Psychological Science, 23(6), 421-426. https://doi.org/10.1177/0963721414547737

Ringle, C. M., Silva, D., & Bido, D. S. (2014). Modelagem de equações estruturais com utilização do SmartPLS. Revista Brasileira de Marketing, 13(2), 56-73. https://doi.org/10.5585/remark.v13i2.2717

Schreck, P. (2015). Honesty in managerial reporting: How competition affects the benefits and costs of lying. Critical Perspectives on Accounting, 27, 177-188. https://doi.org/10.1016/j.cpa.2014.01.001

Sekścińska, K., & Rudzinska-Wojciechowska, J. (2020). Individual differences in Dark Triad Traits and risky financial choices. Personality and Individual Differences, 152, 109598. https://doi.org/10.1016/j.paid.2019.109598

Siallagan, H., Rohman, A., & Januarti, I. (2017). The Dimensions of Organizational Commitment Moderates the Relationship between Budget Participation and Budgetary Slack and Its Effects on Performance. International Journal of Economic Research, 14, 103-114.

Spurk, D. & Hirschi, A. (2018). The Dark Triad and competitive psychological climate at work: A model of reciprocal relationships in dependence of age and organization change. European Journal of Work and Organizational Psychology, 27(6), 736-751. https://doi.org/10.1080/1359432X.2018.1515200

Sosik, J. J., Kahai, S. S., & Piovoso, M. J. (2009). Silver bullet or voodoo statistics? A primer for using the partial least squares data analytic technique in group and organization research. Group & Organization Management, 34(1), 5-36. https://doi.org/10.1177/1059601108329198

Suchanek, M. (2021). The dark triad and investment behavior. Journal of Behavioral and Experimental Finance, 29, 100457. https://doi.org/10.1016/j.jbef.2021.100457

Tokilov, D. U., Suputra, I. D. G. D., & Rasmini, N. K. (2019). Effect of budgetary participation in managerial performance with environmental uncertainty, leadership style, and budgetary adequacy as a moderating variable. International Research Journal of Management, IT and Social Sciences, 6(6), 50-57. https://doi.org/10.21744/irjmis.v6n6.752

Weiskirchner-Merten, K. (2020). Interdependence, participation, and coordination in the budgeting process. Business Research, 1-28. https://doi.org/10.1007/s40685-019-0090-x

Wu, J., & Lebreton, J. M. (2011). Reconsidering the dispositional basis of counterproductive work behavior: The role of aberrant personality. Personnel Psychology, 64(3), 593- 626. https://doi.org/10.1111/j.1744-6570.2011.01220.x

Wu, W., Wang, H., Lee, H. Y., Lin, Y. T., & Guo, F. (2019). How Machiavellianism, Psychopathy, and Narcissism Affect Sustainable Entrepreneurial Orientation: The Moderating Effect of Psychological Resilience. Frontiers in Psychology, 10, 779. https://doi.org/10.3389/fpsyg.2019.00779

Young, S. M. (1988). Individual behavior: performance, motivation, and control. In: K. Ferris cl., Bebaviorul Accounting Research. A Critical Analysis, pp. 229-246. Columbus, Ohio: Century VII Pubhshing Company.

Zeigler-Hill, V., & Besser, A. (2019). Dark personality features and workplace outcomes: The mediating role of difficulties in personality functioning. Current Psychology, 1-15. https://doi.org/10.1007/s12144-019-00527-z

RESEARCH ON PARTICIPATION IN BUDGET SETTING

Questionnaire / Simulation

Scenario

This simulation refers to decision-making on budgeting, and it has five parts. Part 1 offers instructions on how to conduct the activity. In part 2, you have to make budgeting decisions that will influence your salary, and in part 3, you will answer questions about your participation in the simulation. Part 4 presents you with questions about your personality, and finally, part 5 asks about demographic data.

GENERAL INSTRUCTIONS

1) There is no time limit for you to complete any parts of this simulation.

2) When you finish a part of this simulation, you can go to the next one by selecting “next” at the bottom of your screen.

3) You must complete each part of this simulation before going to the next.

4) Once you complete a part, you cannot go back to it.

PART 1 - INSTRUCTIONS

Imagine you are the production manager in a company’s division. Resources are allocated to your department each period based on the expected cost of manufacturing one unit of your department’s product. Therefore, one of your most important responsibilities is setting a budget for your department. The budget request includes the amount in BRL of funds that you would like to receive to finance your department’s production in the next period.

In each of several consecutive budget periods, you will communicate your budget request for the next period to your superior, the division manager. Your superior will review your budget request and approve a budget for your department’s next period. The budget your superior approves for your department can be greater than, less than, or equal to your budget request. If the value is less than the actual production cost, your unit must bear the loss.

When you were hired, you and your superior agreed that your department’s product unit cost would be estimated to be between BRL 2.00 and BRL 8.00 depending on economic conditions. Before you communicate your budget request for the next period, you are the only one who knows exactly what your department’s actual unit cost will be for the next period. So you can decide whether you want to summarize a budget request that is equal to, greater than, or less than your department’s actual unit cost for the next period.

{Information disclosed only for the experimental group}: There is a fierce dispute among the company’s units for resources from its headquarters. Therefore, units with a lower budget tend to be favored and are more likely to receive funds.

PART 2 - ACTIVITY

In this part, you will communicate with your division manager, João da Silva.

In period 1, you are preparing your budget for period 2. Your private forecasting system tells you that your unit cost in period 2 will be exactly BRL 2.75.

Complete the following budget request: My department’s budget request for period 2 is: __________ (amount filled in by participant).

Division Manager’s Response:

From: João da Silva, Division Manager.

To: Production Department Manager.

{Control group only}: I approved BRL 8.00 as a budget for your department for period 2.

{Information disclosed only for the experimental group: Only for the competitive climate group}: I approved your department’s budget for period 2. The sales department obtained a budget lower than requested, and the marketing department received 50% more than the requested amount.

In Period 2, you are preparing your budget for period 3. Your private forecasting system tells you that your unit cost in period 3 will be exactly: BRL 7.50.

Complete the following budget request: My department’s budget request for period 3 is: __________ (amount filled in by participant).

From: João da Silva, Division Manager.

To: Production Department Manager.

{Control group only}: I approved BRL 8.00 as a budget for your department for period 3.

{Information disclosed only for the experimental group}: I approved BRL 6.50 as a budget for your department in period 3. For the sales department, the budget was 20% higher than the requested amount, and for the marketing department, the approved budget was less than the requested amount.

In Period 3, you are preparing your budget for period 4. Your private forecasting system tells you that your unit cost in period 4 will be exactly: BRL 2.50.

Complete the following budget request: My department’s budget request for period 4 is: __________ (amount filled in by participant).

From: João da Silva, Division Manager.

To: Production Department Manager.

{Control group only}: I approved BRL 8.00 as a budget for your department for period 4.

{Information disclosed only for the experimental group}: I approved BRL 7.00 as a budget for your department in period 4. The budget for the sales and marketing department was 50% higher than the requested amount.

In period 4 you are preparing your budget for period 5. Your private forecasting system tells you that your unit cost in period 5 will be exactly: BRL 6.75.

Complete the following budget request: My department’s budget request for period 5 is: __________ (amount filled in by participant).

From: João da Silva, Division Manager.

To: Production Department Manager.

{Control group only}: I approved BRL 8.00 as a budget for your department for period 5.

{Information disclosed only for the experimental group}: I approved your department’s budget for period 5. The budget for the sales and marketing department was 10% less than the requested amount.

PART 3 - BUDGET PARTICIPATION QUESTIONS

Please show how the following statements fit your behavior considering part 2 you just completed (1 = strongly disagree, 7 = strongly agree).

1) I am involved in setting all portions of my budget.

2) The reasoning provided by my supervisor when budget revisions are made is very sound and/or logical.

3) I very frequently state my requests, opinions, and/or suggestions about the budget to my supervisor without being asked.

4) I have a high amount of influence on the final budget.

5) My contribution to the budget is very important.

6) When the budget is being set, my supervisor seeks my requests, opinions, and/or suggestions very frequently.

PART 4 - PERSONALITY

Please indicate how much you agree with each of the following statements (1 = strongly disagree, 7 = strongly agree).

M_1. It’s not wise to tell your secrets.

M_2. Generally speaking, people won’t work hard unless they have to.

M_3. Whatever it takes, you must get the important people on your side.

M_4. Avoid direct conflict with others because they may be useful in the future.

M_5. It’s wise to keep track of information that you can use against people later.

M_6. You should wait for the right time to get back at people.

M_7. There are things you should hide from other people to preserve your reputation.

M_8. Make sure your plans benefit you, not others.

M_9. Most people can be manipulated.

N_1. People see me as a natural leader.

N_2. I hate being the center of attention (reverse scored).

N_3. Many group activities tend to be dull without me.

N_4. I know that I am special because everyone keeps telling me so.

N_5. I like to get acquainted with important people.

N_6. I feel embarrassed if someone compliments me (reverse scored).

N_7. I have been compared to famous people.

N_8. I am an average person (reverse scored).

N_9. I insist on getting the respect that I deserve.

P_1. I like to get revenge on authorities.

P_2. I avoid dangerous situations (reverse scored).

P_3. Payback needs to be quick and nasty.

P_4. People often say I’m out of control.

P_5. It’s true that I can be nasty.

P_6. People who mess with me always regret it.

P_7. I have never gotten into trouble with the law (reverse scored).

P_8. I like to pick on losers.

P_9. I’ll say anything to get what I want.

S_1. I enjoy seeing people hurt.

S_2. I would enjoy hurting someone physically, sexually, or emotionally.

S_3. Hurting people would be exciting.

S_4. I have hurt people for my own enjoyment.

S_5. People would enjoy hurting others if they gave it a go.

S_6. I have fantasies which involve hurting people.

S_7. I have hurt people because I could.

S_8. I wouldn’t intentionally hurt anyone (reverse scored).

S_9. I have humiliated others to keep them in line.

S_10. Sometimes I get so angry I want to hurt people.

PART 5 - DEMOGRAPHIC DATA

1. Gender: ( ) Female ( ) Male ( ) Other ( ) I prefer not to inform.

2. How old are you (years)?

3. Which region of Brazil do you live in? ( ) South ( ) Southeast ( ) North ( ) Northeast ( ) Central-west.

4. What kind of university do you attend? ( ) Public ( ) Private.

5. Which degree are you pursuing? ( ) Accounting ( ) Administration ( ) Economics ( ) Other? Which: _________.

6. What year of the undergraduate program are you currently studying? ( ) 1st year ( ) 2nd year ( ) 3rd year ( ) 4th year ( ) 5th year.

7. Do you have experience in the job market:

( ) No.

( ) Yes.

If yes, how many years of experience do you have? __________.

8. If you want to receive the consolidated results of this research, please inform your email address:___________________.

Author notes

The research results show that the mid-level managers’ personalities that are more likely to contribute positively to the performance of organizations with participatory budgets that do not present interorganizational competition are the machiavellian and narcissistic personalities.

Corresponding author Tel. +55 (48) 3721-9381., E-mail: amandanasatto10@hotmail.com (A. B. N. Corrêa); elavarda@gmail.com (C. E. F. Lavarda). Universidade Federal de Santa Catarina. R. Eng. Agronômico Andrei Cristian Ferreira - Florianópolis/SC - 88040-900, Brazil.