Artículos

Received: 21 June 2019

Accepted: 18 December 2019

DOI: 10.4067/S0718-83582020000200001

Abstract: The relationship between the exchange rate and the consumer price index (CPI) has been extensively covered. However, aggregated approaches hinder the possibility of identifying specific features of this effect over different sectors of the economy, particularly regarding changes in relative prices. This paper aims to examine the dynamics of the rental housing market at a given shift in the exchange rate. We evaluate the case of the real estate market of Buenos Aires, due to its peculiar configuration: the coexistence of a highly dollarized sales segment and a market of housing rentals in which the operations are denominated in local currency. For this purpose, we carry out a two-step panel regression of spatially disaggregated offer rent prices to estimate the pass-through in a non-tradable market. The estimates show an exchange pass-through to rental prices exceeding 30%, more significant than we would have expected.

Keywords: rental market, pass-through, exchange rate, inflation, Buenos Aires.

Resumen: Múltiples autores han abordado extensamente la relación entre el tipo de cambio y el índice de precios al consumidor (IPC). Sin embargo, los enfoques agregados impiden la posibilidad de identificar características específicas de este nexo en diferentes sectores de la economía, particularmente en relación a los cambios en los precios relativos. El objetivo de este trabajo consiste en examinar la dinámica del mercado de viviendas en alquiler ante fluctuaciones en el tipo de cambio. Se evalúa el caso del mercado inmobiliario en la Ciudad Autónoma de Buenos Aires, debido a su configuración peculiar: la coexistencia de un segmento de ventas altamente dolarizado y un segmento de alquileres en el que las operaciones están denominadas en moneda local. Con este objetivo, se llevó a cabo una regresión de panel en dos etapas de precios de alquiler de oferta espacialmente desagregados para estimar el efecto transferencia en un mercado no transable. Las estimaciones muestran una traslación de precios de alquiler superior al 30% ante fluctuaciones cambiarias, lo que representa una mayor significatividad de lo esperado.

Palabras clave: mercado inmobiliario, efecto transferencia, tipo de cambio, inflación, Buenos Aires.

Introduction

Given shifts in the exchange rate, economic research has tended to focus on their pass-through to general import and local prices. However, we argue that aggregated approaches hinder the possibility of identifying specific dynamics of this effect over different sectors of the economy, particularly regarding changes in relative prices.

Real estate market in Argentina is featured by a high degree of dollarization since mid-70s (Gaggero & Nemiña, 2013), which implies that while construction costs -i.e. materials and wages- are paid in local currency, apartments and houses are bought and sold in dollars. This particular set up places the real estate market as a sector of special interest as regards the impacts of exchange rate movements over local price changes. Moreover, the real estate market constitutes a relevant sector of the economy for multiple reasons. Firstly, this market trades real estate which, even though it can be taken as store of value, has an essential use value for people; secondly, access to housing constitutes a human right enshrined in the Universal Declaration of Human Rights and in the National Constitution; and finally, real estate sector is closely related to the construction industry, a highly labor-intensive activity.

Considering the above, if house purchases are made in foreign currency, exchange rate movements must be fully passed through to housing prices in terms of what local currency earners have to save in order to afford the same price. What is less straightforward is that exchange rate fluctuations have impact over the rental market as well, where one price cannot be dissociated from another, as long as owners fix the annual rent of a good acquired in foreign currency, but whose monthly income flow is paid in local currency (Baer & Di Giovambattista, 2018).

Given that, for at least a decade, the percentage of tenants has been remarkably growing in Buenos Aires -while 27.7% of families were tenants in 2008, in 2017 they represent 37.8% of the population, according to the Annual Household Survey of the CABA-, the aim of this paper is to provide evidence of the relationship between exchange rate fluctuations and housing prices. In particular, by means of a disaggregated approach based on domestic geolocated prices of the real estate market, this work seeks to identify and measure the exchange rate pass-through (ERPT) on rent prices for the Autonomous City of Buenos Aires (CABA). This represents an element, not yet fully explored, involved in the housing access problem.

National government housing policy had tried to address this issue in 2016 by creating a large scale mortgage program based on a new unit of account called purchasing power unit (UVA, in its Spanish acronym). One year later, the house purchases with loans had grown more than 400%, which has led to a rise in house selling prices. Furthermore, even though the system was developed to keep the low monthly payments -as much as a normal rent-, the UVA inflation-linked indexation mechanism (both on principal and interest) has triggered a situation in which the debtors owe more than what they had borrowed.

As regards local administration, housing policy (both for rent and sale) has been based on the lack of regulation (Vera Belli, 2018). In the few cases in which the local government has tried to intervene in the market, it was through partial programs, such as “Alquilar se puede” [Rent is possible], “Primera Casa” [First house] and “Garantías BA” [BA Guarantees] that relied on market mechanisms and lacked from enforcement action towards the owners, who could reject families that were part of the programs. Unfortunately, none of these strategies have had success in solving the housing access problem (Vera Belli, 2018). As a result, the Ombudsman’s Office of the CABA has reported a rise in early termination of rental agreements as a result of the increasing burden of the rent on the budget.

For this reason, shedding light on the mechanisms that explain the movements of urban rent, as well as on the specificities of the link between the exchange rate and rental prices, is fundamental to the planning of public policies on access to housing. That is to say, it is fundamental to the preservation of housing access and to highlight that sectoral distributive effects of exchange rate shifts have not been fully covered by the literature. In other words, in a context of low regulation in the rental market, knowing the economic criteria used by owners to adjust the offer rental prices is critical to define housing and real estate policies aimed to maintain the purchasing power of wages. The rest of the article is organized as follows: In section 2 we discuss pass-through transmission channels, regarding both aggregated consumer price index and real estate market prices. In Section 3 we present a brief review of the literature on disaggregated approaches on pass-through studies. Next, in Section 4 we describe the sources of information and methodology applied to estimate the exchange rate pass through on rental prices. Afterwards, in Section 5, we report and discuss the results of the estimated models and finally, in Section 6 we present the concluding remarks.

Pass-through transmission channels

General case

The bilateral exchange rate allows to link foreign and local currency costs and, at the same time, foreign and local currency selling prices. While the former refers to the exchange rate as a channel through which prices and income distribution can be affected, the latter represents the possibility of comparing the evolution of prices of similar goods in different countries. Such links are closely related to a central and controversial reference of the economic theory of international trade: the Law of One Price (Montanari, 1804; Tullio, 1981), both in its absolute and relative version.

The law states that the price of two reasonably similar goods cannot be consistently dissimilar between countries. The absolute version expresses that the prices of similar goods must be equal whereas the relative one regards not the prices, but their change. The law becomes more meaningful under the assumption that arbitration between two goods alike with different prices could be done without facing more costs, such as transport or trade barriers (Isard, 1977).

Domestic prices will react to a devaluation of the exchange rate as long as the local cost structure includes either imported or exported inputs and final goods. In other words, the ERPT over local prices does not work only through final imported goods, but also over internal goods and services in whose production imported inputs are needed, and finally over exportable goods whose prices are defined in the international market.

A second link between local prices and the exchange rate is associated to the evolution of real wages as a cost of production. Even under a cost structure not permeated by international trade an indirect second round effect can exist if wage goods become affected by the exchange rate shift. If a significant decline of real wages should happen, there would be an attempt for a recomposition of the lost purchasing power. That, in turn, would result in a distributive conflict which will resolve, either in a recomposition of the distribution in favor of workers, or in a gradual pass-through to final prices of that recovery of nominal wages. The composition of the basket of wage goods as well as workers bargaining power are decisive factors of this indirect effect which can affect all productive sectors.

Real Estate rental market

Rental market has its own features. From the perspective of the owner, the crucial element is that the rent is given by an income flow denominated in local currency, whereas the selling price is fixed in dollars. On the other hand, from the side of the tenant, the rent paid does not include expenses, taxes or public services, for which they are charged aside, and constitute the total amount payable for housing services. Sometimes, certain services, as gas or water provision, are paid by the building as a whole and then apportioned on the basis of the area of the apartments. And even a same set of amenities -v.g. janitor, cleaning, garbage collection, lift- can represent different amount of expenses in two buildings of the same quality but unequal quantity of apartments.

In fact, in CABA in certain buildings, we verified that, due to the presence of amenities such as swimming pool, gym or private security, there is a trade-off between expenses and rent. Whereas in the premium group the expenses represent a 26% of the rent, in apartments where these features are not present, this share decreases to 21.6% in our sample. Thus, at a certain point, the higher the expenses are the lower the rent becomes in relative terms. Otherwise stated, even though initially one could think that the owners of an apartment in this kind of buildings would charge as much as possible for the square meter, high expenses may force them to give up on a part of their rent.

As regards the link between the exchange rate and the rental price, the latter has no replacement cost. It is nothing more than a rent derived from the land. Real estate investments for rental require an initial foreign currency expenditure at the moment of purchasing the property and, from then on, it provides an annual rent flow, although there can be local currency maintenance costs. A particular feature of this kind of investments in Buenos Aires is that: a) the transaction is made in dollars whereas the rent is set in pesos, and b) properties have undergone a steady process of valuation in foreign currency of their market prices (Baer & Kauw, 2016; Di Giovambattista & García, 2013).

As a result, under the assumption that there is no need to deduct foreign currency expenses, all increases in rental prices after a shift in the exchange rate will have one of either three objectives: a) to preserve its purchasing power; b) to maintain it in terms of foreign currency, or c) to represent a constant share of the selling value of the property, whose trend is growing (Baer & Di Giovambattista, 2018).

Literature on disaggregated pass-through

To some degree, the main constraints when trying to review studies that measure sectoral pass-through are: 1) the problem of finding accurate and periodic sectoral prices, and 2) the degree of thorough knowledge of the international trade normative is required to estimate the effective real exchange rate of each market. Sectors are divided in sub-industries, and each good might have a different tariff, which can turn into heterogeneous movements of the effective real exchange rate for each good after a devaluation of the nominal exchange rate. These hindrances are mentioned by Meyer and von Cramon-Taubadel (2005) as a lack of information of the market conditions, a common flaw of empirical studies.

Regarding the case of the rental segment of the real estate market, as it was previously introduced, it should be noted that it is a sector with low degree of regulation, in which non tradable goods are exchanged, and consequently with no direct links with trade policy. Thus, a shift in the nominal exchange rate will (not) affect the decision of modifying the local currency rent, with no mediations whatsoever set by the trade policy. To the best of our knowledge, there are no applied studies on rental market pass-through for the argentine case, although a reference piece of research for this topic is that of Soffer (2006), about Israel’s real estate market.

Considering that this market is highly dollarized (more than 90% of rental contracts are either settled in dollars or indexed to the exchange rate), it becomes a particularly interesting case of analysis to our purpose. In fact, according to its results, more than half of the total exchange rate pass-through is explained by the partial effect related to the rental market, providing evidence of one of the main benefits of disaggregated studies. The measured pass-through effect in that market is 70% and is carried out contemporaneously with depreciation episodes (using a quarterly dataset).

Other academic papers, although not focused on real estate market, account for heterogeneities of the cost pass-through effect at different moments of the process. Those constitute examples of the need of single-market studies and the shortcomings of general research using consumer price indices. For instance, Richards, Gómez and Lee (2014) identify differences of pass-through and consider the role of manufacturers, retailers and brands. Pollard and Coughlin (2004), for their part, show that most firms respond asymmetrically to large and small changes in the exchange rate, being the pass-through positively related to the size of the change. According to Mumtaz, Oomen and Wang (2011), for the United States, the omission of a sectoral heterogeneity factor leads to an overestimation of the pass-through effect. In addition, Antoniades and Zaniboni (2016) find that the effect is 25 per cent higher for supermarkets than for small stores, accounting for a remarkable difference in the pricing strategy, even for an equivalent set of goods. Loy, Holm, Steinhagen and Glauben (2015) perform an analysis for the dairy market taking into account differences across brands within same goods for the German retailers. Using a threshold error correction model, they identify a faster and larger effect for private brands than for national producers (for a survey see Meyer and von Cramon-Taubadel, 2005).

Sources and methodology

Sources of information

The main aim of this research is to isolate and measure the ERPT over real estate rental prices. To this end, and in the light of the lack of high frequency public statistics of rental prices for the Autonomous City of Buenos Aires, a panel dataset was built with information of rental advertisements on the internet.

This panel dataset includes information that is strictly linked to the real estate dynamics for the formal rental segment, and information concerning the evolution of macroeconomic variables, used as control variables in the estimations of the exchange rate pass-through on rental housing prices. The dataset consists of 55000 observations for 30 neighborhoods between November 2017 and April 2019, clustering the observations on a fortnightly basis.

General two-step estimation

A two-step analysis was performed following the methodology suggested in Di Giovambattista and Rosanovich (2020). Initially a homonogenization process was carried out, so as to identify, in an isolated way, those modifications in rental values that respond specifically to movements of the exchange rate, and not to changes in the composition of the sample.

The aforementioned process involved the implementation of adjustments of rental prices according to the estimated contribution of each attribute of the property (Equations (1) and (2)). In order to reach this first step, from the total number of observations we kept the information related to: a) the rental price; b) the attributes of the property -e.g. area, age, presence of amenities-, and c) the location -e.g. neighborhood, distance to the closest metro station1-.

Such information was used to estimate the following equation in order to identify the base unit for each neighborhood, defined as the modal configuration:

Where lpsm represents the logarithm of the rental price per square meter and arises from the ratio between the rental price in local currency and the total area of the property; d, e and f account for the age, area and proximity ranges, respectively, described in Rosanovich and Di Giovambattista (2019) -for each neighborhood the base ranges were excluded-; bar represents a list of dummy variables for amenities; and sub indices i and j refer to observation and neighborhood.

Thus, the estimated regression varied on the basis of the neighborhood considered, and the obtained coefficients -which reflect the contribution of each attribute k to the rental price, in relation to the base category- were used in order to adjust those properties that do not fulfill with the characteristics of the modal configuration of the neighborhood in which they are located.

For the econometric regressions, we restricted the period between January 2018 and April 2018. This time frame is that of largest relative steadiness of the nominal exchange rate, which allows us to assume this partial analysis in terms of a cross-section database (Hsiao, 2014).

Equation two represents the transformation applied to the rental value per square meter of the observations that do not fall into the modal category of their neighborhood. So, the adjusted rental price is obtained from the following specification:

Where 𝛽 𝑖 , the by-observation adjustment factor, is calculated as the sum of the coefficients obtained from the regression for neighborhood j in which the property is located and the k attributes in which the observation does not match with the base category (Montero & Larraz, 2011).

A negative 𝛽 𝑖 refers to an observation with refers to an observation with features a less market-value than the base category of the neighborhood, for which the adjusted price reflects a compensation.

The adjustments meet the need for controlling the fact that the changes captured did not respond to differences in the composition of the sample but to an effective price change. This means that, if between two periods the share of new properties should increase, for instance, it would be possible to verify a growth in the mean price. However, this change would not account for a true rise of the rental price, but a change in the composition of the sample. In other words, what it was sought was that housing price movements referred not to the presence -or absence- of attributes of the properties but to shifts in the exchange rate.

Once this process was done, as a second step we built a fortnightly panel dataset from the median of homogenized rental prices for each neighborhood. We included the following control variables as well: the nominal bilateral exchange rate peso-dollar of the Central Bank of the Argentine Republic (BCRA); the local price of the basic food basket, taken from the evolution of supermarket prices; the monetary policy interest rate (BCRA) -an estimate of economic activity provided by the National Institute of Statistics and Census (INDEC)-; the nominal formal wages -built from the average taxable remuneration of the stable workers series (RIPTE) of the National Ministry of Work, Employment and Social Security; and, finally, an aggregated variable that combines information of prices of fuel, transport, water, gas and electricity supply rates from official sources of information. More information about the construction of these variables is set out in the Appendix.

Hence, the proposed specification for the log-log model is:

Where 𝑝𝑠 𝑚 ′ is the homogenized offer rental price for neighborhood 𝑖 at the period 𝑡; 𝑛𝑒𝑟 is the nominal exchange rate; 𝑝 is the local price of the basic food basket; 𝑟𝑎𝑡𝑒𝑠 is the price of public services and 𝑚𝑒𝑒𝑎 is the monthly estimate of economic activity. We will also consider the effect of nominal wages (𝑤) and the nominal interest rate (𝑖). All variables are expressed in logarithms.

As regards the estimator, three possibilities were considered: a) Aggregated Ordinary Least Squares (AOLS), b) Fixed Effects (FE) and c) Random Effects (RE), following the estimation methodology for panel data (Mátyás & Sevestre, 2013). In order to verify the choice of (c) estimator over (b) we run the Breusch-Pagan Lagrange Multiplier Test (Hoyos & Sarafidis, 2006). On its part, according to the significance F Test of the residuals of each panel group, estimator (b) performs better than (a). Finally, Hausman Test shows that estimators (b) an (c) are equivalent. Given the obtained results, we chose the RE estimator because it entails a more parsimonious model.

Estimation results

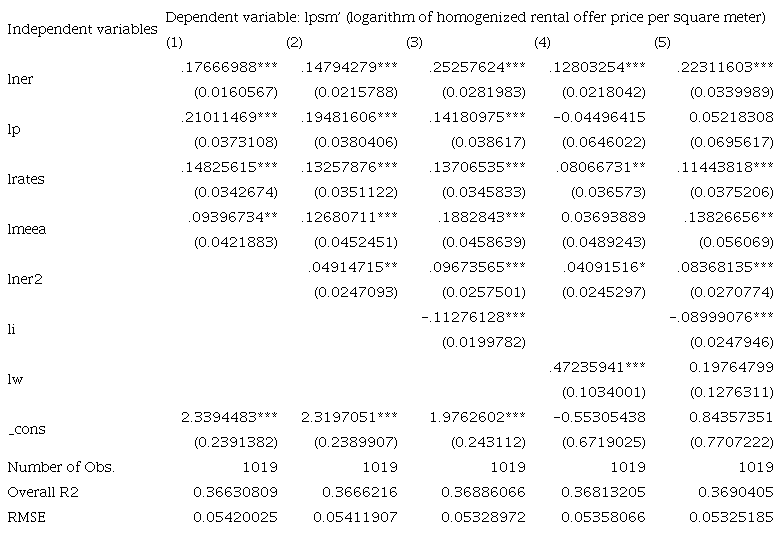

Table 1 reports the RE regression results for the base model and other extended proposals. The multiple specifications exposed are distinguished from each other according to the control variables included for the purpose of analyzing the relationship between the exchange rate and the explained variable given by the homogenized rental offer price per square meter.

Pass-through estimates

Column (1) shows the base model in which only a contemporaneous effect is captured by lner regressor. For this first specification, the control variables - public services, rates, and the basic food basket, p - are used to isolate the exchange rate pass-through on homogenized rental offer prices from other changes that might be caused by a rise in inflation. From this, we gather that for a good that almost does not have any reposition or maintenance costs -such as real estate-, the response of rental prices to a movement on the exchange rate is surprisingly strong and fast (17.6% in the same fortnight of the devaluation episode). This constitutes evidence in favor of the first of the three possible explanations outlined in section 2: that the owners want to preserve the purchasing power of their rental income flow. The pass-through effect seems far from being complete, which -if proven- would have accounted for alternatives two and three, related to keeping the foreign currency value of the rent.

The control variables included in the specification (1) reveal the relevance in terms of magnitude and statistical significance that holds the general inflationary dynamics on rental prices in the city of Buenos Aires. In particular, a 10% increase in the price index -p- increases the rental prices per square meter by 2.1%, ceteris paribus. In addition, it seems that there is also a positive relationship with activity levels, given that the monthly activity coefficient is significant and positive.

In column (2) we include, as an additional explanatory variable, the monthly lag of the exchange rate; by doing so we seek to evaluate whether the link between the variables of interest occurs immediately or presents a certain temporary delay. Once we considered such lag, our estimates grew up to 19.7% one month after the devaluation. For its part, when analyzing the coefficients of the control variables in relation with the values that they assume in specification (1), we show that the introduction of the lag of the exchange rate reduces the relevance of the variables of general inflation and of the price of public services, reinforcing, at the same time, the level of activity as a factor that explain the dynamics of real estate prices. The model performs slightly better in terms of overall R2 (OR2) and root mean square error (RMSE).

However, the model that has a more relevant improvement is the specification (3), in which the local interest rate is also included. The interest rate has a meaningly negative effect, which can be interpreted as an increase in financial costs, in accordance with the classical-Keynesian literature that estates a negative impact on wages (Pivetti, 1988), Besides, an increase in the local interest rate turns non-productive investments more attractive. That implies that the funds destined for real investment will be withdrawn from circulation, and given that the argentine economy is semi-dollarized -i.e, the currency constitutes a regular investment option-, the demand for dollars falls, which decompresses the devaluation pressures. On the other hand, the reduction of monetary aggregates as a result of the rise in interest rate would affect the level of activity. The results show that, taking into account the interest rate, which between November 2018 and May 2019 has reached a mean of 61 per cent, the ERPT coefficient increase up to 34.9% one month after the exchange rate shift.

Finally, models (4) and (5) consider the impact of including wages in the regression, in (4) only wages are included while in (5) both wages and the interest rate are considered. Despite the inclusion of a key variable, it seems that it captures most of the price changes in the economy, leaving no impact whatsoever for the price level. This goes against what was expected, especially in the case of specification (4), where the prices have an inverse relation and the activity has no impact at all.

The last one, for its part, has all the variables included, and nor the wages nor the food basket prices are statistically relevant to explain the rental price movements. Although this model outperforms the others, there is almost no difference in the RMSE and OR2 criteria, and the ERPT coefficient one month after the devaluation is similar (30.6%).

All things considered, the striking finding is that housing rental prices react sharply and rapidly after a devaluation episode, even though there is no international trade channel that could propagate this consequence. Furthermore, as workers will certainly not perceive a wage recomposition as fast as the pass-through takes place, no matter how strong their bargaining power is, there will necessarily be a purchasing power loss associated to this specific market. Consequently, this implies that every upward movement of the exchange rate increasingly hinders the conditions of access to housing, not only by the purchase way, but also through the rental market.

As it was said before, this provides evidence of the behaviour of the owners, who seem to seek to keep the purchasing power of their rental income flow in a context where the general short-run ERPT for Argentina is around 28% (Ito & Sato, 2007). What makes this particularly disturbing is that a significant part of this effect is contemporaneous, when neither wages nor public services react in this way.

In addition, due to the relevance of access to housing and the increasing percentage of tenants in Buenos Aires, the findings also constitute empirical evidence for the debate over the need to regulate the dynamics of rental values, given the structural instability of the exchange rate in Argentina and the discretion of the owners to pass-through the movements of exchange rates to rental prices almost instantaneously.

Concluding remarks

One of the risks of allowing transactions in foreign currency is that it establishes a distinct difference between the parties involved. As long as a market as relevant as the real estate has its transactions made in foreign currency, the country cannot have a true unit of account. This provides a hint of the reason why a significant share of people’s savings are in dollars and why people react so quickly after a devaluation. As a result, every change in the exchange rate will have an impact, no matter the prices, because there will be needed more local currency to buy dollars, while the sellers will have a greater purchasing power, as the ERPT is never complete.

This raises the following question: what are the connections between the rental and the selling markets? In many cases owners are the same in both markets, judging by the figures of more apartments built and more tenants registered, so a growth in market concentration is a possible consequence, although this remains an unknown feature of the market, as there is no open registry of owners. However, we cannot rule out arbitrage operations, which would explain the fast pass-through registered.

This result is particularly important and unaccounted for Argentina, most likely because of the lack of single market studies on exchange rate pass-through. Our research has shown that new contracts are up to date with the shifts in the exchange rate, which leads us to propose a future investigation that deepens the analysis regarding the spatial and distributive differences of this effect. As mentioned, the findings prove that the design of public policies to intervene and promote fair access to housing should necessarily seek to decouple the exchange rate dynamics of real estate rental prices, as it has been argued for the general dynamics of goods and services by Kicillof and Nahón (2006) and Asiain (2010).

On the contrary, not only is real estate regulation virtually non-existent but also, even though contract indexation is legally forbidden since 1991, there is a de facto so called estimated inflation adjustment in all contracts. Whereas owners have the property and only have to pay the expenses as long as it is empty, on the other hand tenants have to make arrangements in order to handle a transition between the end of a contract, the scouting of new apartments, the move and the beginning of a new commercial relation with a new owner. These examples, as well as the main result of the research -the fast ERPT in a market with no significant foreign currency costs- show that there seems to be little balance of power between owners and tenants, partially associated with the supply and demand for housing, but also as a result of a general long run change in the territorial organization (Gaggero & Nemiña, 2013). Furthermore, this poses a question regarding the possibility of setting rent prices by individual agents (Jaramillo, 2009, p. 246). As it is mentioned by this author, it relies heavily on the assumption of “full competition”, a premise that has been challenged for Buenos Aires by the results of our research.

As we have said before, the link between the exchange rate and the rental market has been scarcely analyzed. Despite this lack of a thorough understanding of the mechanisms that operate in the market, a comprehensive approach to the housing issue should not underestimate the role that the exchange rate holds over the configuration of a semi-dollarized and deregulated housing market in Argentina. These are expressions of the neoliberal reforms that have taken place since mid-70s (Mattos, 2010) and which still persist today without being taken into account in the design of public policies to promote access to housing, as we have seen with the absence of enforcement action towards the owners in the case of the public programs at the local level. All in all, it seems that a more comprehensive action is in order.

Acknowledgments

The research was performed by support of our PhD scholarships from the National Council of Scientific and Technical Research (CONICET). We would also like to thank the editor and two anonymous referees. All remaining errors are our own.

References

Antoniades, A. & Zaniboni, N. (2016). Exchange rate pass‐through into retail prices. International Economic Review, 57(4), 1425-1447. https://doi.org/10.1111/iere.12203

Asiain, A. (2010). Tipo de cambio, precios internacionales y retenciones en un modelo estructuralista de corto plazo. Economía, 35(29), 57-78.

Baer, L. & Di Giovambattista, A. (2018). Nuevas condiciones de acceso residencial en la ciudad de Buenos Aires: el impacto del crédito y la macroeconomía en el mercado de compraventa y alquiler de vivienda formal. Voces en el Fénix, (71), 132-139.

Baer, L. & Kauw, M. (2016). Mercado inmobiliario y acceso a la vivienda formal en la Ciudad de Buenos Aires, y su contexto metropolitano, entre 2003 y 2013. EURE, 42(126), 5-25. https://doi.org/10.4067/S0250-71612016000200001

Di Giovambattista, A. & García, G. (2013). Revalorización de la tierra y distribución del ingreso: un análisis para el caso argentino en el período 2001-2012 [Conference presentation]. In VI Conference of Critical Economy. Mendoza, Argentina.

Di Giovambattista, A. & Rosanovich, S. (2020). ¿Alquilar se puede? Gentrificación y pérdida de poder adquisitivo en la ciudad autónoma de Buenos Aires en 2018. Quid 16, (13), 298-324.

Gaggero, A. & Nemiña, P. (2013). El origen de la dolarización inmobiliaria en la Argentina. Sociales en debate, (5), 47-58.

Hoyos, R. d. & Sarafidis, V. (2006). Testing for cross-sectional dependence in panel-data models. The Stata Journal, 6(4), 482-496. https://doi.org/10.1177/1536867X0600600403

Hsiao, C. (2014). Analysis of panel data. Cambridge: Cambridge University Press. https://doi.org/10.1017/CBO9781139839327

Isard, P. (1977). How far can we push the "law of one price”? The American Economic Review, 67(5), 942-48.

Ito, T. & Sato, K. (2007). Exchange rate pass-through to domestic inflation: A comparison between East Asia and Latin American countries (Discussion Paper Series 07-E-040). RIETI. https://www.rieti.go.jp/en/publications/summary/07060003.html

Jaramillo, S. (2009). Hacia una teoría de la renta del suelo urbano. Bogotá: Universidad de los Andes.

Kicillof, A. & Nahón, C. (2006). Las causas de la inflación en la actual etapa económica argentina: un nuevo traspié de la ortodoxia (Documento de Trabajo 5). CENDA.

Loy, J. P., Holm, T., Steinhagen, C., & Glauben, T. (2015). Cost pass-through in differentiated product markets: a disaggregated study for milk and butter. European Review of Agricultural Economics, 42(3), 441-471. https://doi.org/10.1093/erae/jbu031

Mattos, C. d. (2010). Globalización y metamorfosis metropolitana en América Latina: de la ciudad a lo urbano generalizado. Revista de Geografía Norte Grande, (47), 81-104. https://doi.org/10.4067/S0718-34022010000300005

Mátyás, L. & Sevestre, P. (2013). The econometrics of panel data: handbook of theory and applications. Dordrecht: Springer. https://doi.org/10.1007/978-94-009-0375-3

Meyer, J. & von Cramon-Taubadel, S. (2005). Asymmetric price transmission: A survey. Journal of Agricultural Economics, 55(3), 581-611. https://doi.org/10.1111/j.1477-9552.2004.tb00116.x

Montanari, G. (1804). Breve trattato del valore delle monete in tutti gli Stati. Milano: Stamperia e fonderia di G. G. Destefanis.

Montero, J. & Larraz, B. (2011). Interpolation methods for geographical data: housing and commercial establishment markets. Journal of Real Estate Research, 33(2), 233-244.

Mumtaz, H., Oomen, Ö., & Wang, J. (2011). Exchange rate pass-through into UK import prices: evidence from disaggregated data (Staff Papers 14). Federal Reserve Bank of Dallas. https://www.dallasfed.org/-/media/documents/research/staff/staff1103.pdf

Pivetti, M. (1988). On the monetary explanation of distribution: a rejoinder to Nell and Wray. Political Economy. Studies in the Surplus Approach, 4(2), 275-83.

Pollard, P. S. & Coughlin, C. C. (2004). Size matters: asymmetric exchange rate pass-through at the industry level (Research Paper, 2004/13). University of Nottingham. https://doi.org/10.2139/ssrn.716001

Richards, T. J., Gómez, M. I., & Lee, J. (2014). Pass-through and consumer search: An empirical analysis. American Journal of Agricultural Economics , 96(4), 1049-1069. https://doi.org/10.1093/ajae/aau009

Rosanovich, S. & Di Giovambattista, A. (2019). Inversión pública y plusvalías urbanas. Análisis espacial y efectos no lineales de la proximidad de la red de subterráneos sobre los precios de la vivienda en Buenos Aires. Revista Transporte y Territorio, (20), 303-332. https://doi.org/10.34096/rtt.i20.6394

Soffer, Y. (2006). Exchange rate pass-through to the consumer price index: a micro approach (Foreign Exchange Discussion Paper Series, 2). Bank of Israel.

Tullio, G. (1981). The monetary approach to external adjustment: a case study of Italy. London: Palgrave Macmillan.

Vera Belli, L. (2018). La comisión inmobiliaria a cargo del propietario. Análisis descriptivo respecto a las discusiones y regulaciones recientes del mercado de vivienda en alquiler. Quid 16 , (9), 197-213.

Appendix

In order to create our control variables the following steps were taken:

- 1. Nominal exchange rate peso-dollar, fortnightly 90th percentile of the rate of the Central Bank of Argentina (BCRA)

- 2. Monetary policy rate, fortnightly 90th percentile of the rate of the (BCRA)

- 3. Fuel, weighted mean of prices of five kinds of fuel (Super and Premium gasoline; Gas Oil grade 2 and 3 and Compressed Natural Gas). The weights were calculated based on the volume sold of each fuel as percentage of the total (National Ministry of Energy and Mining).

- 4. Transport, fortnightly weighted mean of prices of tickets. The following distances were chosen as representative: Bus, the 6 to 12 km ticket; train, the 0 to 12 km ticket (Mitre, Sarmiento, San Martín, Belgrano Norte and Urquiza lines) and the subway ticket. As regards the weights for bus, train and subway, the percentages assigned were 82%, 9% and 9%, respectively, considering not only the number of passengers but also the spatial coverage (National Ministry of Transport).

- 5. Gas, fortnightly weighted mean of the fixed and variable charges for residential users R1, R2.1, R2.2, R2.3, R3.1, R3.2, representing a share 10%, 14%, 22%, 25%,15% y 15% of the demand. Afterwards, the monthly tariff was calculated using different consumption levels for low demand (from November to April, the mean of each range) and high demand (from May to September, the highest value of each range).

- 6. Water: we considered the price changes reported by the Argentinean Water and Sanitation Company (AySA).

- 7. Electricity, fortnightly weighted mean of the fixed and variable charges for the first four residential users R1, R2, R3 and R4 of Edenor and Edesur companies. Afterwards, the monthly tariff was calculated using different consumption levels for low demand (from November to April, the mean of each range) and high demand (from May to September, the highest value of each range).

- 8. Rates emerges as a weighted average of fortnightly value of fuels (15%), water (20%), transport (25%), gas (25%) and electricity (15%) previously built.

- 9. Wages, average taxable salary of formal workers (RIPTE - National Ministry of Work, Employment and Social Security).

- 10. Emae, monthly estimator of economic activity (EMAE - National Institute of Statistics and Census).

Notes