Artículos

Designing an integrated reporting guidance: an initiative to improve environmental and social reporting quality

Diseño de una guía de informes integrados: una iniciativa para mejorar la calidad de los informes ambientales y sociales

A. PRATAMA arie.pratama@fe.unpad.ac.id

W. YADIATI winwin.yadiati@unpad.ac.id

N. DEWI TANZIL nanny.dewi16@unpad.ac.id

J. SUPRIJADI jadi.suprijadi@unpad.ac.id

A. PRATAMA arie.pratama@fe.unpad.ac.id

W. YADIATI winwin.yadiati@unpad.ac.id

N. DEWI TANZIL nanny.dewi16@unpad.ac.id

J. SUPRIJADI jadi.suprijadi@unpad.ac.id

Designing an integrated reporting guidance: an initiative to improve environmental and social reporting quality

Utopía y Praxis Latinoamericana, vol. 24, núm. Esp.5, pp. 218-238, 2019

Universidad del Zulia

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-CompartirIgual 3.0 Internacional.

Recepción: 01 Octubre 2019

Aprobación: 06 Noviembre 2019

Abstract: Environment and social reporting need to be done in a comprehensively way. Integrated reporting provided opportunities to integrate social and environmental aspects with traditional financial reporting. This research trys to add a new improvement in scoring integrated reporting. A new scoring system consisted of39 indicators derived from integrated reporting components. This system also provides scoring ranging from none to excellent. This scoring system might be used in the future by companies, auditors, or regulators in conjunction with assessing the quality of the integrated report.

Keywords: Auditor, Conjunction, Integrate, Reporting.

Resumen: El medio ambiente y los informes sociales deben realizarse de manera integral. Los informes integrados brindaron oportunidades para relacionar aspectos sociales y ambientales con los informes financieros tradicionales. Esta investigación trató de agregar una nueva mejora en la calificación de informes integrados. Un nuevo sistema de puntuación consistió en 39 indicadores derivados de componentes integrados de informes. Este sistema también proporciona puntajes que van desde ninguno hasta excelente. Este sistema de puntuación podría ser utilizado en el futuro por compañías, auditores o reguladores junto con la evaluación de la calidad del informe integrado.

Palabras clave: Auditor, Conjunción, Informes, Integración.

1.INTRODUCTION

There is a significant change in how the stakeholder makes decisions. Stakeholders changed from capitalism to a socialism view (Freeman et al.: 2007), that is, a shifting concern from revenue-profit-dividend into sustainability-environmental-society (Adams & McNicholas: 2007; Freeman et al.: 2010). One of the concerns in reporting is a full and detail explanation of companies' business operations. Traditional form of reporting has several concerns: (1) It usually focused only on the financial aspect, none or few explanations on non-financial aspect (Craven & Marston: 1999; Gray: 2001; Montabon et al.: 2007; Dhaliwal et al.: 2011).

(2) It usually focused on past performance, not provide a clear link between past, present, and future performance (Gray et al.: 1996; Adams: 2004, pp.731-757; Williams: 2008; Stent & Dowler: 2015); (3) It constructed using a "silo", rather than "integrated" paradigm, resulting in a thick "catalog" report. (DiPiazza & Eccles: 2002; Ho & Wong: 2003; Eccles & Krzus: 2010; Higgins et al.: 2014). The weakness of the current form of corporate reporting has to lead the International Integrated Reporting Committee to establish a new form of reporting, called Integrated reporting.

Since the introduction of the framework, many companies around the world implement the integratedreporting concept in their reporting. South Africa became the first country that required all listed companies to create integrated reporting. The implementation of integrated reporting was not without challenges. Executives and management of the companies perceived that the benefit of integrated reporting is not exceeding the implementation costs (Steyn: 2014, pp.476-503; Lodhia: 2015). Furthermore, Busco et al. (2013) found that executives and management were still reluctant to disclose the business model and risks faced by the company since it can be brought negative consequences for the company if users read the report. Eccles & Krsuz (2014) also added that many executives and management would not implement integrated reporting voluntarily. Currently, they were making the report simply because the rules told them to do so. These challenges, perhaps the reasons why integrated reporting, are still not implemented by many companies around the world. Dumay et al. (2017) showed that only 494 companies around the world already implement integrated reporting. Pistoni et al. (2018) found that the overall quality level of integrated reporting is still low, and the "content" of reporting scored very low. However, this is not the case for all companies. Companies in extractive and manufacturing industries have a better quality of reporting due to the nature of the business that might damage natural and social environmental (Van Zyl: 2013; Serafeim: 2015; Stubbs et al.: 2015; Pratama: 2017).

Integrated reporting can also improve the current practice of environmental and social reporting. Investors currently demand to know how good a company manages the environment and social issues, but current reporting lack of integrated thinking, so the presentation of these issues only limited to monetary numbers (Hoang: 2018). The company needs to disclose risks associated with environmental and social issues and the long-term strategy to mitigate the risks; and integrated reporting framework can facilitate that information (Adams: 2017). Integrated reporting is also aligned with Sustainable development Goals (SDG) by providing media to report the company's activities related to 17 areas of SDG (Nunes et al.: 2016). Integrated reporting is also aligned with many reporting standards concerning environmental and social reporting, like Global Reporting Initiative (GRI) or Sustainability Accounting Standards (SAS) (Schooley & English: 2015; Adams: 2017; Global Reporting Initiative: 2018). Integrated reporting elements might be elaborated with reporting elements from GRI or SAS so that it can present more robust and comprehensive information about environmental and social issues.

Improvement of integrated reporting can be started by improving the quality of the disclosure of the contents (Solomon & Maroun: 2012; Atkins & Maroun: 2015). The integrated reporting framework stated that the framework is a principle-based. Consequently, judgments will be used heavily. Judgments can have a positive and negative impact. On the positive sides, judgments provide room for reporting flexibility, e.g., different companies might have a different core business process, and the companies might free to choose what aspect that needs to be disclosed most (Bennett et al.: 2006; Sunder: 2010; Ahmed et al.: 2013). On thenegative sides, judgments might lead to a company to select or modify the information so it can always represent a good or positive and hiding the negative side, or the "cherry-picking" practice. (Church et al.: 2008; Flower: 2015). Eccles et al. (2012) research stated that some precise, more ruled based integrated reporting tools needed to be established. Principle-based reporting will always feature the rule because the full principle- based would negatively affect the comparability of the report (Bradbury & Schröder: 2012; Bamber & McMeeking: 2016). Achim & Borlea (2015), suggested that one of the ruled based tools will be a device to assess the quality of the reporting or "scoring system".

The scoring system serves as a tool to achieve excellent quality in reporting, which can lead to betterfinancial performance and quality of management (Churet et al.: 2014).

Previous researches have tried to formulate a scoring system, such as Barth (2017), Pistoni et al. (2018), but there is still room to improve the system, especially the dimension of scoring and the level of details. This research will be tried to elaborate on a better scoring system that provides an adequate level of details and explicit score attributes, so the users and preparers of integrated reporting might evaluate and analyze the integrated reporting easier. In the wake of the audit of integrated reporting, this article can also provide insight to the auditors regarding elements that necessary to be investigated. This article is a systematic literature review. First, this article would describe the reporting quality concept to get an understanding of the level of reporting the company should achieve that. Second, this article explained the development of the integrated reporting scoring system, by exploring the IIRC standards and relevant literature, and finally in the conclusions and recommendations, this article would provide several insights on how this integrated scoring system might improve the reporting quality, and provide several recommendations for implementation and for further research as well.

To fulfill the purpose of the reporting, the information presented in the report must fulfill qualitative characteristics (Scott: 2009; Yadiati: 2010; Kieso et al.: 2019). In financial reporting perspectives, there were fundamental (relevant and representational faithfulness) and enhancing qualities of reporting (comparability, timeliness, verifiability, and understandability) (van Beest et al.: 2009; IASB: 2010). In the information system perspectives, the quality can be achieved if the information fulfills these criteria: relevant, accurate, timeliness, and complete. Generally, a good quality report can be assessed from the information provided therein. Previous researches had proposed several proxies to indicate the quality of reporting, such as: earnings quality (Dechow et al.: 2010; Lin et al.: 2014), accruals quality (Arthur et al.: 2005), conservatism (Francis et al.: 2005), value relevance (Barth et al.: 2008). All the proxies used in this research were all the accounting- numbers and stated in financial terms. Financial and accounting numbers cannot be understood easily by the report's user, and the practice of creative accounting can undermine the quality of the report (Sherman & Young: 2016). Financial accounting numbers need high expertise and literacy, which not all of the report users have (McDaniel et al.: 2002).

Tang et al. (2016) proposed that the disclosure level can also measure reporting quality. Siagian et al. (2013) stated that the principle-based standard implementation requires heavy disclosures on the assumptions, considerations, and the choices of the judgments. Integrated reporting quality was best measured by the narrative descriptions, rather than used a symbol or syntax like in the financial reporting (Cosma et al.: 2018). Pistoni et al. (2018) proposed that integrated reporting quality should consist of 4 elements: (1) Background, which assess the motivation and preparation made by the company to construct such a report. (2) Content, which assess the information provided by the report; (3) Reliability and assurance, which assess the verifiability and whether there is an audit or review of such information; (4) Form, which assess the outlines, page layout, and editing of the report. From all these elements, content is the main issue. Wild & Van Staden (2013) reported that the investor still not feel any benefit of integrated reporting because the company still not following the content, as instructed by the IIRC framework. Haller & van Staden (2014) also mentioned that the IIRC framework placed an importance on the link between 6 types of capital employed and the outcomes of each capital employed, or the value-added. Adams (2013) and Hughen et al. (2014) alsoagreed that the content of the integrated reporting would reduce asymmetric information, and the disclosures of the content will be the main focus of the company's analyst.

In the aspect of environmental and social reporting, Wong (2011) described the qualitative characteristics of such reporting must include: relevance, clarity, free from bias, comprehensiveness, timeliness, and comparability. Integrated reporting can accommodate these qualitative characteristics by setting a framework that consists of elements and guiding principles. IIRC stated that a full set of integrated reporting must have 9 components, namely: (1) Organizational overview and external environment, (2) Governance, (3) Business model, (4) Risks and opportunities (5) Strategy and resource allocation, (6) Performance, (7) Outlook, (8) Basis of preparation and presentation and in doing so, takes account of, (9) General reporting guidance. There are several guiding principles that must be adhere when prepared integrated reporting, namely: (1) Strategic focus and future orientation, (2) Connectivity of information, (3) Stakeholder relationships, (4)Materiality, (5) Conciseness, (6) Reliability and completeness (7) Consistency and comparability. The complete set of the framework would be practical to prevent impression management by companies, in which companies tend to promote only good environmental and social news and conceal bad news (Diouf & Boiral: 2017, pp.643-667). Al Farooque & Ahulu (2017) also stated that industry needs robust guidelines to deliver quality reporting, robust guidelines including the integrated framework for social, environmental, and economic inputs and performances.

2. METHODS

Disclosure of information is compulsory to reduce information asymmetry to enable users of the report made a better judgment (Beyer et al.: 2010). However, much research about disclosure only measures the disclosure on the one side, either the perceived importance of disclosure (details) or the extent of the disclosure (index-based) (Robbins & Austin: 1986). Many research about disclosure use disclosure index, in which the researcher will prepare a disclosure checklist consists of many items to disclose, and the disclosure level will be determined by the number of items disclosed divided by total items to disclosed (Cormier et al.: 2005; Brammer et al.: 2008; Pavlopoulos et al.: 2017). The disclosure level measured by disclosure index is simple and can be automated by using an automated machine or software but can hide the true nature of the disclosure (Beyer et al.: 2010; Berger: 2011). Marston & Shrives (1991) suggested that the researcher needs to look into a more qualitative aspect of the disclosure. They argue that the disclosure index tends to treat all the disclosure components as equal. In reality, there will be a different priority or importance level of information for investor decision making (Urquiza et al.: 2009).

On the other hand, disclosure based on the details will provide more detail and accurate assessment of the quality because the measurement expanded from "exist or not exist", to "bad or good" (Cheung et al.: 2010). The details can be provided by assigning numbers indicating "bad", "adequate", "good", etc. However, the weakness of this measurement is the substantial subjectivity of the assessor. The scoring sheet or matrix need to be produced to serve as a guideline for the assessor to reduce the subjectivity. Healy & Palepu (2001) stated that disclosure checking based on the details required sufficient knowledge in the field of content analysis. The reliability can also be increased by assigning two or more assessors to assess the disclosure quality so that the results can be compared and analyzed. Current research concerning integrated reporting quality was still limited by using the disclosure index. As far as the researcher knows, none of this research uses a scoring based on the quality of the information disclosed. The researcher proposed to measure the quality of integrated reporting based on the IIRC framework.

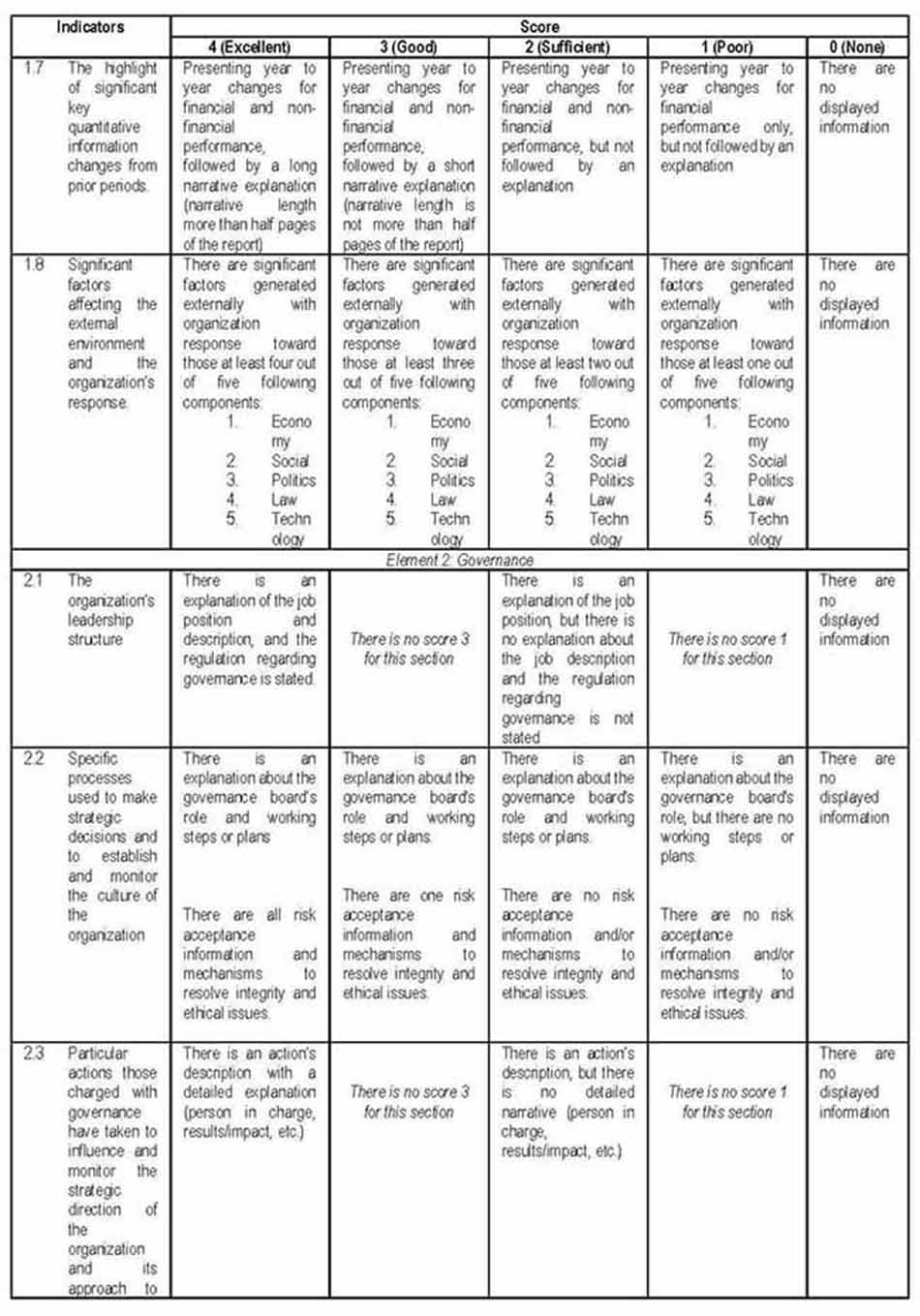

The first element, organizational overview, and external environment serves as an introduction for users to gain more understanding about the principal activities of the company, and how the activities were affected by (1) the internal strengths and weaknesses, and (2) the external opportunities and threats (Xue et al.: 2008; Filatotchev & Nakajima: 2010). In the internal environment aspect, many readers of the report will base theirdecision on the first impressions of the company (Chen et al.: 2009). A first impression is a form of business communication, and the objectives of the communication are to "seduces" investors to read more pages of the particular report (Parhankangas & Ehrlich: 2013). Illustrations in forms of tables, numbers, and graphs are also contributed in explaining the long narrative story, into an informative and exciting story (Briscoe: 1995; Guffey & Loewy: 2010; Bovee & Thill: 2010). Completeness of the information was also pivotal for a reader so that they can access the level of competitiveness. In the marketing context, the understanding of the macro external environment (such as: political, social, economic, etc) and micro external environment (such as: five forces model) can form a basis for a clear assessment of the competitiveness and economic sustainability of the company (Forman & Hunt: 2005; Ingenbleek: 2007). There are 8 indicators (20,51%) for this element, which were taken directly from IIRC's standard. The focus in assessment for this element is whether the reader of the reports has sufficient and complete information about the environment in which it is operated. The significant percentage showed the implementation of the "first impressions", this element must appease the investors, and serves as a foundation.

The second element, governance, serves as an "ensuring mechanism" that the internal and external environment was equipped with complete monitoring and supervision mechanisms, and it secures from any possibilities of inefficient or ineffective acts (Salvioni & Bosetti: 2006; Kachouri & Jarboui: 2017). Readers usually want to understand two things from governance: (1) structure and (2) mechanism (Brennan & Solomon: 2008). Readers also want to assess whether those charged with governance were able to implement the proper actions to maintain the governance (Bozec & Dia: 2015), and how the governance clearly contributed to the improvement of the business (Cremers & Nair: 2005; De Haes & Van Grembergen: 2008). The importance of governance was significantly increased in the era of information technology. The more channel or media to report, and linkage between capital – process – value is the main content of such a governance report (Kolk & Pinkse: 2010; Hrebicek et al.: 2011). The matrices provide 7 points (17,95%) about the governance, and as the principle of the governance, the assessment will be based on the accountability and transparency of the information, and the linkage between the environment – governance – and process.

The third element, the business model, serves as a "main picture" of the company's value creation. The business model is a general representation of the companies’ process of delivering products or services (Osterwalder & Pigneur: 2010). The traditional business model usually consists of 3 things: (1) Input, which is a resources used to deliver a final product or service; (2) Process, which is a combination between resource and activity to convert that resource into final product; and (3) Output, which is a product or service (Chesbrough: 2010; Teece: 2010; Thompson & MacMillan: 2010, pp.291-307). The business model is usually described slowly in the report since the business model is providing information concerning companies' main activities, including any risks, resources, regulations, and performance expectations (Demil & Lecocq: 2010). The contemporary business model places a significant emphasis on innovation and outcomes (Zott et al.: 2011). Innovation can be a signal for significant business improvement, and the innovation might have future positive or negative outcomes (Bocken et al.: 2014). There are seven indicators of business model, and together with previous elements, there are 22 indicators, representing 56,41% of all the indicators. This condition showed us that the main emphasis of well-integrated reporting is whether the company able to present comprehensive business activities, along with its monitoring mechanism and any external and internal factors that might affect the activities (Morros: 2016; Velte & Stawinoga: 2016).

The fourth element, risks and opportunities, only contain two indicators, as per IIRC standards. The main emphasis is the descriptions of the risks and any relevant actions to cover or mitigate the risks, or in other words, risk management (Linsley & Shrives: 2006). Risk reporting was usually provided due to a specific mandatory requirement like BASEL or Enterprise Risk Management (ERM) (Dobler: 2008). Therefore, in some industries like banking or technology, this element is well represented. Naturally, risks were a concern since, in the era of traditional reporting, therefore, to avoid high political costs, the company must present the information to the investors (Miihkinen: 2012). The corporate governance sections were also discussing therisk management (Elshandidy & Neri: 2015), so it explained why the disclosure requirement in this component was low.

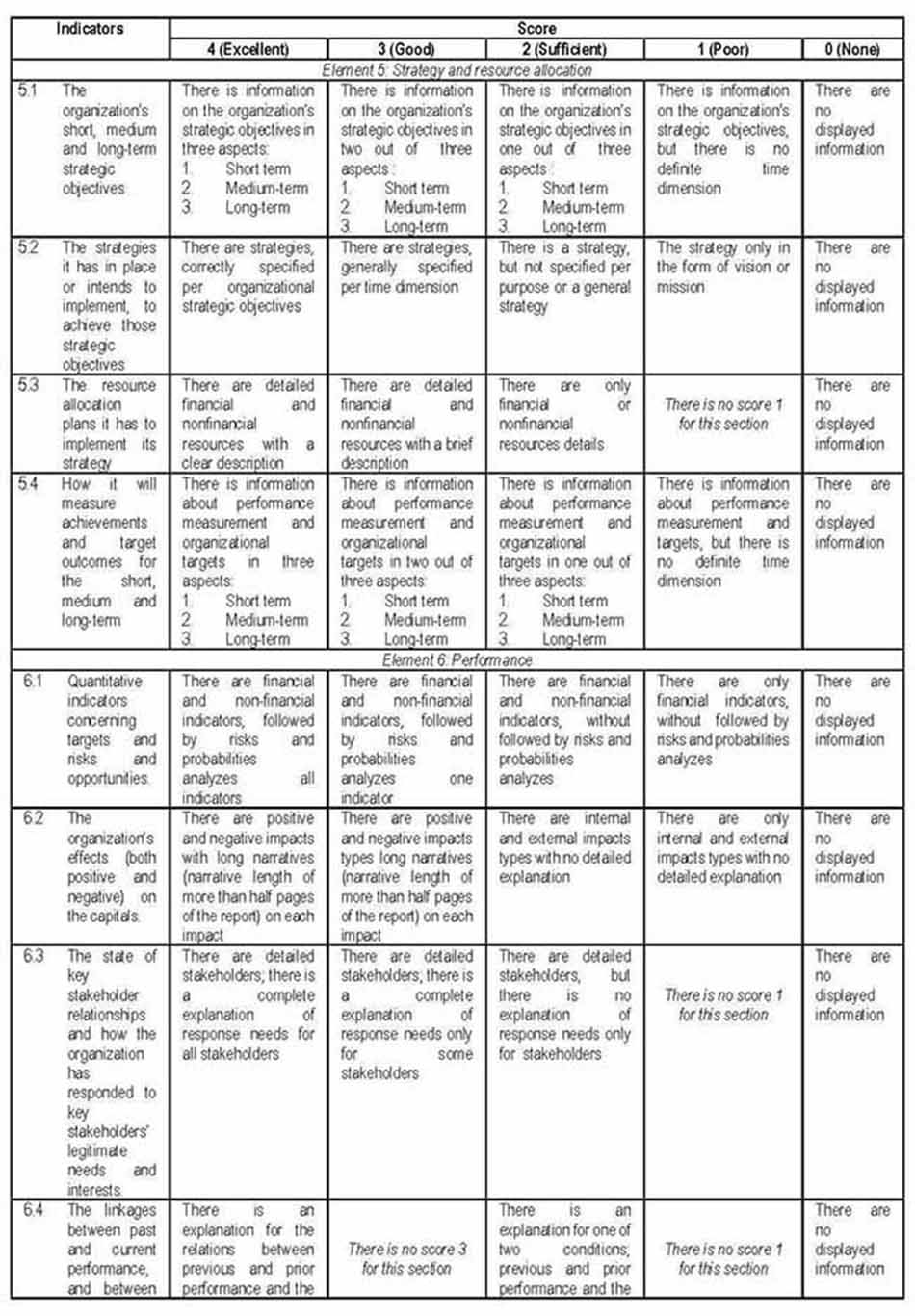

The fifth element, strategy and resource allocation describe the (1) strategic objectives, including the target outcomes in different period; (2) strategy to achieve those objectives; and (3) resource to support the implementation of the strategy. There are four indicators set by IIRC to measure these elements. Naturally, strategy and objectives were established by the companies, and it is typical for disclosing it on various media. The main emphasis of reporting strategy is to analyze whether the resource was adequately allocated in order to pursue the strategy (Venkatesan & Kumar: 2004). Regarding the period, most of the companies emphasize their outcomes on the long-term objectives, since strategy naturally deals with long term issues (Yip: 2004, pp.17-24). The long-term objectives must be derived to form medium and short term, so the company has a clear direction to pursue (Brauer: 2013).

The sixth element, performance, is regarded to be a “sole” objective of the reporting. Performance reporting is considered a mechanism to eliminate agency problems, by asking the agent to report their accountability of resource utilization to the shareholders (Franco-Santos et al.: 2007; Nudurupati et al.: 2011). Performance report was usually about past financial performance only, but the current form of reporting also demanded a non-financial performance with present and future orientation (Bernardi & Stark: 2015). The traditional report also tends to emphasize positive results and limited to satisfy shareholder needs (Sierra- Garcia et al.: 2013). The new integrated reporting informs both positive and negative outcomes and also not only to shareholders but also to all relevant stakeholders (Melloni et al.: 2017).

The seventh element, outlook, is generally a mechanism to provide the reader with a forecast of the future situation. There are three indicators to describe this element. Generally, outlook information more focused on the external environment's risk and opportunity, the effects of the environment to the business, and how the company's activities to prevent the risks or gaining the opportunities (Chase Jr: 2014). Implementation of information technology, like the utilization of big data and data analytics, might bolster the forecasting (Duan& Xiong: 2015). Digital tools might be disclosed and featured heavily to promote the forecasting and predictingthe future of the business.

The eighth elements, the basis for presentation and reporting, have generally required the company to present the standards or regulations related to the global companies reporting (Khadaroo: 2005). The usual reporting standard that disclosed now is accounting standards, but many jurisdictions also provided regulations to disclose environmental and social aspects, and also regarding aspects of customer safety and satisfaction (Boedker et al.: 2008). In the era of complexity, there is also some necessity to disclosed risk management activities to prevent adverse outcomes. There are four indicators in this element.

3.RESULTS

Table 1 showed the matrices proposed for scoring integrated reporting. The indicators were constructed from elements of integrated reporting. There are eight elements of integrated reporting, and the framework provides an explanation of the content of each element. To provide a detailed assessment, the researcher divides the eight elements into 39 indicators. The researcher also provides five types of score, as provided in Table 1.

4. CONCLUSIONS

Integrated reporting quality assessment needs to be done to ensure that the purpose of the integrated reporting is achieved. The matrix for integrated reporting scoring is an initiative that can be of the benefit to many parties. For the integrated report's issuer, the matrices can be used as a guide to preparing the best quality integrated report. The issuer might want to look at the first criteria in each of the 39 indicators, to ensure that the excellent integrated report will be produced. This matrix might also be useful for auditor's professions. The matrices can direct the companies to create the report using a similar trait and manner and may overcome the difficulties of auditing the integrated reporting (Oprisor: 2015). Regulators might use this matrix when it decides to enact the integrated reporting rules in their respective countries.

However, the development of integrated reporting scoring needs to be maintained, and in the future, many considerations may take into account. For example, future research might propose the specific designations, and it is score range (such as A for Excellent, etc.) to reflect the quality of the integrated reporting. The futureresearcher might also consider putting weights in each of the indicators. Although the integrated reporting framework stated that all the elements have the same priority and importance, the regulations and investor demand might be a consideration to add the weights to the indicators. Furthermore, finally, future research might also re-improve the matrices that being proposed in this article, e.g., added the indicators, expanding the score range and criteria, etc. so the integrated reporting in the future will be a very useful tool to assess the company performance and provide the investor, the accountability that they need.

BIODATA

ARIE PRATAMA: Arie is an accounting lecturer in the Department of Accounting, Faculty of Economics and Business, Universitas Padjadjaran, Indonesia. Currently, he is pursuing a doctoral degree in Doctoral Program in Accounting, Department of Accounting, Faculty of Economics and Business, Universitas Padjadjaran, Indonesia. His research interests are financial accounting, corporate reporting, public sector accounting, taxation, and accounting education.

WINWIN YADIATI: is a financial accounting professor in the Department of Accounting, Faculty of Economics and Business, Universitas Padjadjaran, Indonesia. Her research interests are financial accounting and corporate reporting. She was a Head of Department of Accounting, Faculty of Economics and Business, Universitas Padjadjaran, Indonesia, from the year 2013 – 2016.

NANNY DEWI TANZIL: Nanny is a financial accounting and managerial finance associate professor in the Department of Accounting, Faculty of Economics and Business, Universitas Padjadjaran, Indonesia. Her research interests are financial accounting, financial management, and corporate reporting. Currently, she is Head of Undergraduate Program, Department of Accounting, Faculty of Economics and Business, Universitas Padjadjaran, Indonesia.

JADI SUPRIJADI: Jadi is a statistics associate professor in the Department of Statistics, Faculty of Mathematics and Natural Science, Universitas Padjadjaran, Indonesia. His research interests are structural equation modeling application in social sciences and business.

BIBLIOGRAPHY

ACHIM, MV, & BORLEA, NS (2015). “Developing of ESG Score to Assess the Non-financial Performances in Romanian Companies”, in: Procedia Economics and Finance, 32, pp.1209-1224.

ADAMS, CA, & MCNICHOLAS P (2007). “Making a difference: sustainability reporting, accountability andorganisational change”, in: Accounting, Auditing & Accountability Journal, Vol. 20 No. 3, pp.382‐402.

ADAMS, C (2004). “The ethical, social and environmental reporting-performance portrayal gap”, in:Accounting, Auditing and Accountability Journal, 17(5), pp.731-757.

ADAMS, C (2013). Understanding Integrated Reporting. London: Routledge.

ADAMS, C (2017a). “The Sustainable Development Goals, integrated thinking and integrated report”.Retrieved from: http://integratedreporting.org/wp-content/uploads/2018/01/SDGs-and-the-integrated- report_summary_.pdf Accessed on Oct 1st, 2018.

ADAMS. C (2017b). “Five steps to aligning the SDGs with the IR Framework”. Retrieved from: https://www.icas.com/technical-resources/five-steps-to-aligning-the-sdgs-with-the-ir-framework, Accessed on Oct 2nd, 2018.

AHMED, AS, NEEL, M AND WANG, D (2013). “Does Mandatory Adoption of IFRS Improve Accounting Quality? Preliminary Evidence”, in: Contemp Account Res, 30, pp.1344-1372.

AL FAROOQUE, O, & AHULU, H (2017). Determinants of social and economic reportings: Evidence from Australia, the UK and South African multinational enterprises, International Journal of Accounting & Information Management, 25(2), pp.77-200.

ARTHUR, N, TANG, Q, & LIN, ZS (2015). “Corporate accruals quality during the 2008–2010 Global Financial Crisis”, in: Journal of International Accounting, Auditing and Taxation, 25, pp.1-15.

ATKINS, J, & MAROUN, W (2015). “Integrated reporting in South Africa in 2012: Perspectives from South African institutional investors”, in: Meditari Accountancy Research, 23(2), pp.197-221.

BAMBER, M, & MCMEEKING, K (2016). “An examination of international accounting standard-setting dueprocess and the implications for legitimacy”, in: British Accounting Review, 48(1), pp.59–73.

BARTH, ME, LANDSMAN, WR, & LANG, MH (2008). “International Accounting Standards and Accounting Quality”, in: Journal of Accounting Research, 46, pp.467-498.

BARTH, ME, CAHAN, SF, CHEN L, & VENTER, ER (2017). “The economic consequences associated with integrated report quality: Capital market and real effects”, in: Accounting, Organizations and Society, 62, pp.43-64.

BENNETT, B, BRADBURY, M, & PRANGNELL, H (2006). “Rules, principles, and judgments in accounting standards”, in: Abacus, 42, pp.189-204

BERGER, PG (2011). “Challenges and opportunities in disclosure research—A discussion of “the financial reporting environment: Review of the recent literature.””, in: Journal of Accounting and Economics, 51(1-2), pp.204–218.

BERNARDI C, & STARK AW (2015). The transparency of environmental, social and governance disclosures, integrated reporting, and the accuracy of analyst forecasts. Unpublished working paper, Roma Tre University and University of Manchester.

BEYER, A, COHEN, D, LYS, T, & WALTHER, B (2010). “The financial reporting environment: a review of the recent literature”, in: Journal of Accounting and Economics, 50 (2–3), pp.296–343.

BOCKEN, NMP, SHORT, SW, RANA, P, & EVANS, S (2014). “A literature and practice review to develop sustainable business model archetypes”, in: J. Clean. Prod. 65, pp.42–56.

BOEDKER, C, MOURITSEN, J, & GUTHRIE, J (2008). “Enhanced business reporting: international trends and possible policy directions”, in: Journal of Human Resource, Costing & Accounting, 12(1), pp.14–25.

BOVEE, C, & THILL, J (2010). Business communication today. Upper Saddle River, N.J. Prentice Hall.

BOZEC, R, & DIA, M (2015). “Governance practices and firm performance: Does shareholders’ proximity tomanagement matter?”, in: International Journal of Disclosure and Governance, 12(3), pp.185-209.

BRADBURY, ME, & SCHRÖDER, LB (2012). “The content of accounting standards: Principles versus rules”, in: The British Accounting Review, 44(1), pp.1-10.

BRAMMER, S, & PAVELIN, S (2008). “Factors influencing the quality of corporate environmental disclosure”, in: Business Strategy and the Environment, 17(2), pp.120–136.

BRAUER, MF (2013). “The effects of short-term and long-term oriented managerial behavior on medium-term financial performance: longitudinal evidence from Europe”, in: Journal of Business Economics and Management, 14:2, pp.386-402.

BRENNAN, NM, & SOLOMON, J (2008). “Corporate governance, accountability and mechanismsof accountabilityy: an overview”, in: Accounting, Auditing & Accountability Journal, 21, pp.885-906.

BRISCOE, HM (1995). Preparing Scientific Illustrations. Springer-Verlag, NewYork.

BUSCO, C, FRIGO, M.L, QUATTRONE, P AND RICCABONI, A (2013). Towards integrated reporting: concepts, elements and principles. In Integrated Reporting (pp. 3-18). Springer, Cham.

CHASE JR, CW (2014). “Innovations in business forecasting: Predictive analytics”, in: The Journal of Business Forecasting, 33(2), p.26.

CHEN, XP, YAO, X, & KOTHA, S (2009). “Entrepreneur passion and preparedness in business plan presentations: a persuasion analysis of venture capitalists' funding decisions.”, in: Academy of Management journal, 52(1), pp.199-214

CHEUNG, YL, JIANG, P, & TAN, W (2010). “A transparency Disclosure Index measuring disclosures: Chinese listed companies”, in: Journal of Accounting and Public Policy, 29(3), pp.259–280.

CHESBROUGH, HW (2010). Business model innovation: Opportunities and barriers. Long Range Planning, 43, pp.354-363.

CHURCH, BK, DAVIS, SM, & MCCRACKEN, SA (2008). “The auditor's reporting model: A literature overview and research synthesis”, in: Accounting Horizons, 22(1), pp.69-90.

CHURET, C, & ECCLES, RG (2014). “Integrated Reporting, Quality of Management, and Financial Performance”, in: Journal of Applied Corporate Finance, 26, pp.56-64.

CORMIER, D, MAGNAN, M, & VAN VELTHOVEN, B (2005). “Environmental disclosure quality in large German companies: Economic incentives, public pressures or institutional conditions?”, in: European Accounting Review, 14(1), pp.3-39.

COSMA, S, SOANA, MG, & VENTURELLI, A (2018). “Does the market reward integrated report quality?”, in:African Journal of Business Management, 12(4), pp.78-91.

CRAVEN, BM & MARSTON, CL (1999). “Financial reporting on the Internet by leading UK companies”, in:European Accounting Review, 8(2), pp.321-333.

CREMERS, KJ, & NAIR, VB (2005). “Governance Mechanisms and Equity Prices”. The Journal of Finance, 60, pp.2859-2894.

DECHOW, P, GE, W, & SCHRAND, C (2010). “Understanding earnings quality: A review of the proxies, their determinants and their consequences”, in: Journal of Accounting and Economics, 50(2–3), pp.344–401

DE HAES, S, & VAN GREMBERGEN, W (2008). January. Analysing the relationship between IT governance and business/IT alignment maturity. In Proceedings of the 41st Annual Hawaii International Conference on System Sciences (HICSS 2008) (pp. 428-428). IEEE.

DEMIL, B, & LECOCQ, X (2010). Business model evolution: In search of dynamic consistency. Long Range Planning, 43, pp.227–246.

DHALIWAL, DS, LI, OZ, TSANG, A, & YANG, YG (2011). “Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting”, in: The Accounting Review, 86(1), pp.59-100.

DIPIAZZA, SA, & ECCLES, RG (2002). Building Public Trust: The Future of Corporate Reporting, Hoboken, NJ: John Wiley & Sons.

DIOUF, D, & BOIRAL, O (2017). “The quality of sustainability reports and impression management: A stakeholder perspective”, in: Accounting, Auditing & Accountability Journal, 30(3), pp.643-667.

DOBLER, M (2008). “Incentives for risk reporting: a discretionary disclosure and cheap talk approach”, in: The International Journal of Accounting, Vol. 43, No. 1, pp.184-206.

DUAN, L, & XIONG, Y (2015). “Big data analytics and business analytics”, in: Journal of Management Analytics, 2(1), pp.1-21.

DUMAY, J, BERNARDI, C, GUTHRIE, J, & LA TORRE, M (2017). “Barriers to implementing the International Integrated Reporting Framework”, in: Meditari Accountancy Research, 25(4), pp.461–480.

ECCLES, R, & KRZUS, M (2010). The Quest for the'Holy Grail'of Integrated Financial and CSR Reporting.

ECCLES, RG, KRZUS, MP, ROGERS, J, & SERAFEIM, G (2012). “The need for sector‐specific materialityand sustainability reporting standards”, in: Journal of Applied Corporate Finance, 24(2), pp.65-

ECCLES, RG, & KRZUS, MP (2014). The integrated reporting movement: Meaning, momentum, motives, and materiality. John Wiley & Sons.

ELSHANDIDY, T, & NERI, L (2015). Corporate Governance, Risk Disclosure Practices, and Market Liquidity: Comparative Evidence from the UK and Italy. Corporate Governance: An International Review, 23(4), pp.331- 356.

FILATOTCHEV, I, & NAKAJIMA, C (2010). “Internal and External Corporate Governance: An Interface between an Organization and its Environment”, in: British Journal of Management, 21, pp.591-606

FLOWER, J (2015). The International Integrated Reporting Council: a story of failure. Critical Perspectives on Accounting, 27, pp.1–17.

FORMAN, H, & HUNT, JM (2005). “Managing the influence of internal and external determinants on industrial pricing strategies”, in: Industrial Marketing Management, Vol.34, pp.133-46.

FRANCIS, J, KHURANA, I, & PEREIRA, R (2005). Disclosure incentives and effects on the cost of capital around the world, The Accounting Review, 80(4), pp.1125–1162.

FRANCO-SANTOS, M, KENNERLEY, M, MICHELI, P, MARTINEZ, V, MASON, S, MARR, B, GRAY, D, &NEELY, A (2007). “Towards a definition of a business performance measurement system”, in: International Journal of Operations & Production Management, 27(8), pp.784-801.

FREEMAN, R, MARTIN, K, & PARMAR, B (2007). “Stakeholder Capitalism”, in: Journal of Business Ethics, 74(4), pp.303-314.

FREEMAN, RE, HARRISON, JS, WICKS, AC, PARMAR, BL, & DE COLLE, S (2010). Stakeholder theory: thestate of the art. Cambridge University Press, New York, United States

GLOBAL REPORTING INITIATIVE (2018). In Focus: “Addressing investor needs in business reporting on the SDG’s”. Retrieved from: https://www.globalreporting.org/resourcelibrary/addressing-investor-needs-SDGs- reporting.pdf Accessedon: Oct 1st, 2018.

GRAY, R, OWEN, D, & ADAMS, C (1996). Accounting & accountability: changes and challenges in corporate social and environmental reporting. Prentice Hall.

GRAY, R (2001), “Thirty years of social accounting, reporting and auditing: what (if anything) have we learnt?”, in: Business Ethics: A European Review, 10, pp.9-15.

GUFFEY, ME, & LOEWY, D (2010). Essentials of business communication. Mason, OH: South- Western/Cengage Learning.

HALLER, A, & VAN STADEN, C (2014). “The value-added statement – an appropriate instrument for Integrated Reporting”, in: Accounting, Auditing & Accountability Journal, 27(7), pp.1190–1216.

HEALY, PM, & PALEPU, KG (2001). “Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature.”, in: Journal of Accounting and Economics, 31(1-3), pp.405– 440.

HIGGINS, C, STUBBS, W, & LOVE, T (2014). “Walking the talk(s): organisational narratives of integrated reporting.”, in: Accounting, Auditing & Accountability Journal, 27, pp.1090–1119.

HO, SS, & WONG, KS (2003). “Preparers' perceptions of corporate reporting and disclosures.”, in:International Journal of Disclosure and Governance, 1(1), pp.71-81.

HOANG, T (2018). The Role of the Integrated Reporting in Raising Awareness of Environmental, Social and Corporate Governance (ESG) Performance. In Stakeholders, Governance and Responsibility (pp. 47-69). Emerald Publishing Limited.

HUGHEN, L, LULSEGED, A, & UPTON, DR (2014). “Improving stakeholder value through sustainability and integrated reporting”. The CPA journal, 84(3), p.57.

IASB (2010). Conceptual Framework for Financial Reporting. London: IASB.

INGENBLEEK, P (2007). “Value‐informed pricing in its organizational context: literature review, conceptualframework, and directions for future research”, in: Journal of Product & Brand Management, Vol. 16 Issue: 7,pp.441-458.

IQBAL KHADAROO, M (2005). “Business reporting on the internet in Malaysia and Singapore: A comparative study”, in: Corporate Communications: An International Journal, 10(1), pp.58-68.

KACHOURI, M, & JARBOUI, A (2017). “Exploring the relation between corporate reporting and corporate governance effectiveness”, in: Journal of Financial Reporting and Accounting, Vol. 15 Issue: 3, pp.347-366.

KIESO, DE, WEYGANDT, JJ, & WARFIELD, TD (2019). Intermediate accounting. John Wiley & Sons.

. KOLK, A, & PINKSE, J (2010). “The integration of corporate governance in corporate social responsibilitydisclosures”, in: Corporate Social Responsibility and Environmental Management,17, pp.15-26.

LIN, Z, JIANG, Y, TANG, Q, & HE, X (2014). “Does high-quality financial reporting mitigate the negative impact of Global Financial Crises on firm performance? Evidence from the United Kingdom”, in: Australasian Accounting, Business, and Finance Journal, 8(5), pp.19–46.

LINSLEY, PM, & SHRIVES, PJ (2006). “Risk reporting. a study of risk disclosures in the annual reports of UK companies”, in: British Accounting Review, Vol. 38 No. 4, pp.387-404.

LODHIA, S (2015). “Exploring the transition to integrated reporting through a practice lens: an Australian customer owned bank perspective”, in: Journal of Business Ethics, 129(3), pp.585-598.

MARSTON, CL, & SHRIVES, PJ (1991). “The use of disclosure indices in accounting research: A review article.”, in: The British Accounting Review, 23(3), pp.195–210.

MCDANIEL, L, MARTIN, R, & MAINES, L (2002). “Evaluating Financial Reporting Quality: The Effects of Financial Expertise vs. Financial Literacy.”, in: The Accounting Review, 77, pp.139-167.

MELLONI, G, CAGLIO, A, & PEREGO, P (2017). “Saying more with less? Disclosure conciseness, completeness and balance in Integrated Reports.”, in: Journal of Accounting and Public Policy, 36(3), pp.220- 238.

MIIHKINEN, A (2012). “What DrivesQuality of Firm Risk Disclosure? TheImpact of National Disclosure Standard and Reporting Incentives under IFRS.”, in: The International Journal of Accounting, 47(4), pp.437- 468.

MONTABON, F, SROUFE, R, & NARASIMHAN, R (2007). “An examination of corporate reporting, environmental management practices, and firm performance.”, in: Journal of Operations Management 2 (5), pp.998–1014.

MORROS, J., (2016). “The integrated reporting: A presentation of the current state of art and aspects of integrated reporting that need further development.”, in: Intangible Capital, 12(1), pp.336-356.

NUDURUPATI, SS, BITITCI, US, KUMAR, V, & CHAN, FTS (2011). “State of the art literature review on performance measurement”, in: Computers and Industrial Engineering, Vol. 60, No. 2, pp.279-290

NUNES, AR, LEE, K, & O'RIORDAN, T (2016). “The importance of an integrating framework for achieving the Sustainable Development Goals: the example of health and well-being.”, in: BMJ global health, 1(3), p.e000068.

OPRISOR, T (2015). “Auditing Integrated Reports: Are there Solutions to this Puzzle?”, in: Procedia Economics and Finance, 25, pp.87–95

OSTERWALDER, A, & PIGNEUR, Y (2010). Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers. New Jersey: John Wiley and Sons

PISTONI, A, SONGINI, L, & BAVAGNOLI, F (2018). “Integrated reporting quality: an empirical analysis.”, in:Corporate Social Responsibility and Environmental Management, 25(4), pp.489-507.

PARHANKANGAS, A, & EHRLICH, M (2013). “How entrepreneurs seduce business angels: an impression management approach”, in: Journal of Business Venturing, Vol. 29 No. 4, pp.543-564.

PAVLOPOULOS, A, MAGNIS, C, & IATRIDIS, GE (2017). “Integrated reporting: Is it the last piece of the accounting disclosure puzzle?”, in: Journal of Multinational Financial Management, 41, pp.23–46.

PRATAMA, A (2017). “Clustering Indonesian companies’ Annual Reports: preliminary assessment of the implementation of integrated reporting by Indonesian listed companies”, in: Int. J. Globalisation and Small Business, 9(1), pp.46–54.

ROBBINS, WA, & AUSTIN, KR (1986). “Disclosure Quality in Governmental Financial Reports: An Assessment of the Appropriateness of a Compound Measure.”, in: Journal of Accounting Research, 24(2), p.412.

SALVIONI, D, & BOSETTI, L (2006). “Corporate governance report and stakeholder view. Symphonya.”, in:Emerging Issues in Management, (1), pp.24-46.

SCHOOLEY, DK, & ENGLISH, DM (2015). “SASB: A pathway to sustainability reporting in the United States.”, in: The CPA journal, 85(4), p.22.

SCOTT, WR (2009). Financial accounting theory. Toronto, Ont: Pearson Prentice Hall.

SERAFEIM, G (2015). “Integrated Reporting and Investor Clientele.”, in: Journal of Applied Corporate Finance, 27, pp.34-51.

SHERMAN, DH, & YOUNG, DS (2016). Where Financial Reporting Still Falls Short. Harvard Business Review, July – August 2016 edition.

SIAGIAN, F, SIREGAR, SV, & RAHADIAN, Y (2013). “Corporate governance, reporting quality, and firm value: evidence from Indonesia.”, in: Journal of Accounting in Emerging Economies, 3(1), pp.4–20.

SIERRA‐GARCÍA, L, ZORIO‐GRIMA, A, & GARCÍA‐BENAU, MA (2015). “Stakeholder engagement,corporate social responsibility and integrated reporting: An exploratory study.”, in: Corporate SocialResponsibility and Environmental Management, 22(5), pp.286-304.

SOLOMON, J, & MAROUN, W (2012). Integrated reporting: the influence of King III on social, ethical and environmental reporting.

STENT, W, & DOWLER, T (2015). “Early assessments of the gap between integrated reporting and current corporate reporting.”, in: Meditari Accountancy Research, 23(1), pp.92-117.

STEYN, M (2014). “Organisational benefits and implementation challenges of mandatory integrated reporting: Perspectives of senior executives at South African listed companies”, in: Sustainability Accounting, Management, and Policy Journal, 5(4), pp.476-503

STUBBS, W, HIGGINS, C, MILNE, M, & HEMS, L (2015). Financial capital providers’ perceptions of integrated reporting. Working paper: Clayton.

SUNDER, S (2010). Adverse effects of uniform written reporting standards on accounting practice, education, and research. Journal of accounting and public policy, 29(2), pp.99-114.

TANG, Q, CHEN, H, & LIN, Z (2016). “How to measure country-level financial reporting quality?”, in: Journal of Financial Reporting and Accounting, 14(2), pp.230–265

TEECE, DJ (2010). “Business models, business strategy and innovation.”, in: Long Range Planning, 43, pp.172-194.

THOMPSON, JD, & MACMILLAN, IC (2010). “Business models: Creating new markets and societal wealth.”, in: Long Range Planning, 43, pp.291-307.

URQUIZA, FB, ABAD NAVARRO, MC, & TROMBETTA, M (2009). “Disclosure indices design: does it make a difference?”, in: Revista de Contabilidad, 12(2), pp.253–277.

VAN BEEST, F, BRAAM, G, & BOELENS, S (2009). Quality of Financial Reporting: measuring qualitative characteristics. Nijmegen Center for Economics (NiCE).

VAN ZYL, AS (2013). “Sustainability and Integrated Reporting In The South African Corporate Sector.”, in:International Business and Economics Research Journal, 12(8), pp.903 – 926.

VELTE, P, & STAWINOGA, M (2016). “Integrated reporting: The currenttstate of empirical research, future research implications”, in: Journal of Management Control, pp.1-46.

VENKATESAN, R, & KUMAR, V (2004). “A Customer Lifetime Value Framework for Customer Selection and Resource Allocation Strategy”, in: Journal of Marketing, 68(4), pp.106-125.

WILD, S & VAN STADEN, CJ (2013). Integrated Reporting: Initial analysis of early reporters–an Institutional Theory approach. 7th Asia Pacific Interdisciplinary Accounting Research Conference, (pp. 26-28). Kobe.

WILLIAMS, LS (2008). “The Mission Statement: A corporate reporting tool with a past, present, and future”, in: Journal of Business Communication 45(2), pp.94-119.

WONG, R (2011). Corporate social and environmental reporting: a user perspective, Ph.D. thesis, University of Bath.

XUE, Y, LIANG, H, & BOULTON, W (2008). “Information Technology Governance in Information Technology Investment Decision Processes: The Impact of Investment Characteristics, External Environment, and Internal Context.”, in: MIS Quarterly, 32(1), pp.67-96.

YADIATI, W (2010). Teori Akuntansi: Suatu Pengantar. Bandung: Penerbit Kencana.

YIP, GS (2004). Using strategy to change your business model. Business strategy review, 15(2), pp.17-24.

ZOTT, C, AMIT, R, & MASSA, L (2011). “The business model: recent developments and future research”, in:Journal of management, 37(4), pp.1019-1042.