Artículos

A critical analysis of customs-business partnership compliance the import and export enterprises with customs law and regulation

Análisis crítico de la asociación aduanera-empresarial y cumplimiento de las empresas de importación y exportación con la ley aduanera y la regulación

V.D NGUYEN vunguyentc@yahoo.com

P.G AQUINO jesusper186@gmail.com

D. HONG LE Dlehong@yahoo.com

V.D NGUYEN vunguyentc@yahoo.com

P.G AQUINO jesusper186@gmail.com

D. HONG LE Dlehong@yahoo.com

A critical analysis of customs-business partnership compliance the import and export enterprises with customs law and regulation

Utopía y Praxis Latinoamericana, vol. 24, núm. Esp.5, pp. 349-358, 2019

Universidad del Zulia

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-CompartirIgual 3.0 Internacional.

Recepción: 01 Octubre 2019

Aprobación: 08 Noviembre 2019

Abstract: This research systematically presents the multifarious information and data from secondary and primary sources to provide the results of articles and papers relative to Customs-Business Partnership that affect the compliance of import and export enterprises based on customs law and regulation. The authors have established the theoretical model to analyze the Customs-Business Partnership in Vietnam. The authors conducted a survey involving 202 enterprises from the cities of Hanoi, Hai Phong, Dong Nai, Ho Chi Minh, Binh Duong, and Vung Tau, respectively, on August 2018. By using and performing a multivariate regression method and analysis, the paper gives predictions following the Binary logistic regression.

Keywords: Binary Logistic Regression, Customs-Business Partnerships, Compliance, Import And Export Enterprises.

Resumen: Esta investigación presenta sistemáticamente la información y datos múltiples de fuentes secundarias y primarias para proporcionar los resultados de artículos y documentos relacionados con la Asociación de Aduanas y Negocios que afectan el cumplimiento de las empresas de importación y exportación de acuerdo con las leyes y regulaciones aduaneras. Los autores han establecido el modelo teórico para analizar la Asociación de Aduanas y Negocios en Vietnam. Los autores realizaron una encuesta con 202 empresas de las ciudades de Hanoi, Hai Phong, Dong Nai, Ho Chi Minh, Binh Duong y Vung Tau, respectivamente, en agosto de 2018. Mediante el uso y la realización de un método y análisis de regresión multivariante, el documento da predicciones siguiendo la regresión logística binaria

Palabras clave: Alianzas Aduanas-Negocios, Cumplimiento, Empresas de Importación y Exportación, Regresión logística binaria.

1.INTRODUCTION

One of the revenue-generating collecting agencies as the financial arm of the government is the customs that implement the customs laws and regulations that primarily aimed to prevent and interrogate illegal shipments. It is the agency that has been given the authority to access cross-border transactions, which are considered uniquely placed among border agencies (Mikuriya: 2012). Based on traditional functions of customs, the agency primarily acts as collecting agent for taxes and duties at the border, controlling goods that enters and leaves the national territories and imposition of penalties on illegal or unlawful actions or dispositions. However, in most cases, businesses express disappointments in the imposition of regulations and mandate by customs that often the cause of frustrations with the customs officers when making transactions with them. In fact, according to the data provided by Transparency International (2009) on Corruption Perceptions Index 2009, customs was listed among one of the most corrupt institutions with complicated border procedures that mostly become a hindrance on business activities. This is also accompanied by other business complaints that include border delays and miscommunications between custom officers (Grainger: 2010).

However; in continuous commitment to improve, the 21st century has become a gateway for establishment of more improve custom services worldwide and according to Jeannard (2010), the adoption of client-centric policy that emphasized the important role of customs in becoming more responsive to stakeholders by assuring them the specific standards of service delivery and benchmark for measuring service quality. The functions of customs evolve dramatically in response to the changing nature of pressures from both domestic and international environments that paved the way into trade facilitation that aimed at simplifying and harmonizing customs procedures thus, possessing major challenges to the agency. Lots of customs administrations worldwide pursue a partnership with business and reaped valuable benefits in terms of quality of service provision from custom authorities, including revenue collection, trade facilitation, trade security, and citizen/industry protection (Mikuriya: 2012).

The realization has been attained, viewing the importance of implementing efficient and effective customs administration that should start with the customs in facilitating legitimate trade wherein developing and developed countries have to recognize and practice by partnering and interacting with the business. Ireland et al. (2011) highlight the importance of partnerships to counter the incidence of corruption and at the same time, a desirable attempt to reform and modernization efforts. As an example, the trade community will be benefited lower transaction costs, prompt custom clearance, custom procedures, and predictability. However, this is not precisely the case of the customs in Vietnam, where this study is primarily anchored (Chen et al.: 2015).

Nowadays, Vietnam's economy has integrated more and more deeply into the world economy. Import- Export turnovers have increased rapidly in value. In particular, those turnovers grow from USD 203.66 billion in 2010 to USD 349.2 billion in 2016. Besides, Vietnam has also signed and came into force of 10 FTAs, concluded two FTA negotiations, and continued four other FTAs negotiations. The government has also strengthened the enforcement of the Action Plan related to Resolution n019-2015/NQ-CP, Resolution n036a- 2015/NQ-CP, Resolution n019-2016/NQ-CP, Resolution n035-2016/NQ-CP, and Resolution n019-2017/NQ- CP in order to implement provisions of those FTA effectively and efficiently and to improve the fair and transparent business environment. One of the most critical components of the plan is to develop the Customs- Business Partnerships (CBP) which benefits not only efficiency of capacity-building work, customs reform and modernization, but also transparency and predictability of customs procedures, lower transaction cost, and voluntary compliance of import and export enterprises with customs law and regulation. Therefore, the analysis of Customs-Business Partnerships affecting the compliance of import and export enterprises is very significant in the theoretical approach and policy performance (Zhang & Preece: 2011).

The theoretical framework about Customs-Business Partnerships is emphasized in some papers, including: First, Customs-Business Partnerships was based on Public-private partnerships (PPPs) which devotedto forms of association between the public and private sectors in the mid-1950s (Dahl & Lindblom: 1953; Bower: 1983). Besides, the recommendations of international organizations like the OECD and the World Bank encouraged the application of PPPs as the optimal model for resource allocation (Wettenhall: 2003). In this context, a clear and overall definition of the partnership was given by Brinkerhoff (2002): Partnership is a dynamic relationship among diverse actors, based on mutually agreed objectives, pursued through a shared understanding of the most rational division of labor based on the respective comparative advantages of each partner. The partnership encompasses mutual influence, with a careful balance between synergy and respective autonomy, which incorporates mutual respect, equal participation in decision making, mutual accountability, and transparency.

Second, Customs-Business Partnerships became one of the important and spirit components in the Revised Kyoto Convention (WCO: 1999). It is evident that transitional standard 3.32, and standard 1.3, 6.8, 7.3, 8.5, 9.1 and 9.2 of its General Annex emphasize partnerships between the customs and business informal consultative relationships, application of special procedures for authorized persons, customs control, enforcement of information technology and providing changes of customs law, administrative arrangements or requirements (Wei: 2013).

Third, the Trade Facilitation Agreement including Articles 2, 7.7, 12(1) and 23(2) approaches to CBP through main contents of comment on the proposed introduction or amendment of laws and regulations related to the movement, release, and clearance of goods. Trade Facilitation Measures for Authorized Operators, such as: (i) low documentary and data requirements as appropriate; (ii) low rate of physical inspections and examinations as appropriate; (iii) rapid release time, as appropriate; deferred payment of duties, taxes, fees and charges; (iv) use of comprehensive guarantees or reduced guarantees; (v) a single customs declaration for all imports or exports in a given period; (iv) and clearance of goods at the premises of the authorized operator or another place authorized by Customs (WTO: 2014).

Fourth, WCO (2015) with Customs – Business Partnership Guidance paper analyses vital benefits (Win- Win) of Customs administration, Business and Government in designing and implementing CBP, desirable factors for successful CBP and four phases to develop CBP, including: (i) Strategic Overview and Planning,(ii) Developing Engagement Strategies, (iii) Implementation and (iv) Monitoring and Institutionalization. Notably, the paper looks at main pillars approaching joint integrity, corruption observatory, Bi-directional education/training, and consultation of information technology and customs procedure. Overall, in this context, the significance of Customs-Business Partnership can be explained by Dr. Kunio Mikuriya, Secretary-General of the WCO: ‘This CBP means that Customs cannot act alone without taking into account the interests of its partners. It must further develop consultation, promote information exchange and cooperation, and reduce the barriers to the smooth flow of trade by jointly identifying bottlenecks and offering solutions’ (Mikuriya: 2010).

Hypotheses of Customs-Business Partnership affect the compliance of enterprises with customs law and regulation. Asymmetric Information Theory (1970) by George Akerlof, Michael Spence, and Joseph Stiglitz refers to three problems related to asymmetric information, such as moral hazard, adverse selection, and principal-agent. In approaching to customs inspection and supervision, those problems have been used to explain the causes, the motivation of tax evasion and non-compliance of Vietnam enterprises (Vu: 2014). Therefore, trust, transparent, and sufficient information are major factors that strongly influence the motivation and the probability of compliance of the import and export enterprise with the customs law.

The Risk-based compliance management Pyramid approached customs management based on assessing and identifying the compliance level of import and export enterprises. It is measured by the results of administrative violations, criminal offenses, the ability to control, and self-assessment for errors in the performance of customs procedures. Factors impacting on the compliance level of enterprises include: (i) partnership between customs and enterprises facilitating customs procedures, providing information and grace in tax payment; (ii) the clarity, transparency and strictness of the customs law fighting against the illicit trade and tax evasion (iii) education and training of owner’ enterprises (Ayres & Braithwaite: 1992). Besides,the Customs - Business Partnership Guidance paper refers to one of the most important benefits of CBP that enhances voluntary compliance from business with customs law and regulation. In particular, impact of CBP on compliance is based on items of increased role in policy consultation and formulation process and customs reform and modernization programs; better understanding and appreciation of customs requirements, laws and procedures; open communication channels with Customs; better and easier access to information and joint education/ training and retraining programmes of Customs, (WCO: 2015).

2.METHODS

The samples of the research are 202 enterprises participating in import and export activities in some cities of Hanoi, Hai Phong, Dong Nai, Ho Chi Minh, Binh Duong, and Vung Tau in August 2016. The sample survey was randomly conducted for import and export enterprises that attended customs training courses, regular meetings, seminars between customs administration and enterprises at five localities having the largest export and import turnover in Vietnam.

The questionnaire is based on the theoretical framework consisting of two main sections: (i) general information of enterprises including 4 questions about type of operation, corporate headquarters, educational level of enterprise director, and duration of activity in the sector, (ii). Assessing the level of the importance of 7 items from Q7 to Q13 which explain contents of Customs - Business Partnership for compliance of the import and export enterprises with customs law and regulation (through 6 items from Q1 to Q6). The questionnaire form is delivered directly to staff members who are working directly in the import and export activities of the surveyed enterprises when they joined in the form of training courses or conferences or seminars or workshops.

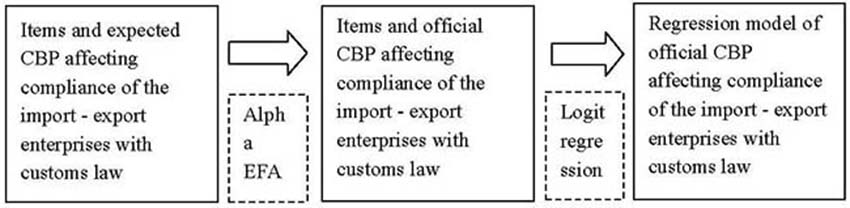

Applying descriptive statistics, Cronbach's Alpha test, exploratory factor analyses (EFA), and Binary Logistic regression with the maximum likelihood estimation method, supported by SPSS.20 software.

Based on theoretical research, the regression estimation model and implementation process are proposed as follows:

- Variables of the research model

Dependent variable (Y), the compliance of import and export enterprises with the customs law and regulation, receives binary value, in which Y = 1 if the enterprise in compliance with the customs law and regulation, and Y = 0 if the enterprise is non-compliance with the customs law and regulation. Y variables are aggregated according to the mean () of the items from Q1 to Q6 with a 5-point Likert scale, which expresses meanings from none (1) to many (5). The content of items is the application of accounting standards (Q1), audit of financial statements (Q2), applying internal control for customs procedures (Q3), payment of taxes, fees on time (Q4), detected commercial frauds (Q5), and prosecution or administrative penalties of customs offices or over customs offices (Q6).

Independent variables (Xi) reflect the expected factors (contents of Customs -Business Partnership)affecting customs compliance of import and export enterprises. The Xi variables represent the 3 factors proposed in the theoretical model. Support of the customs administration for the import and export enterprises (X1) represents the four items: Q7 (enterprises join free training courses and seminars related to new customs law, regulations and requirements organized by Customs), Q8 (enterprises join free training courses and seminars related to contents of customs valuation, harmonized system of goods, origin of goods, intellectual property rights, and administrative statements organized by Customs), Q9 (enterprises join free training courses and seminars related to contents of risk management, compliance management in customs context, post clearance audit, and components and operations of VNACCS/VCIS systems organized by Customs) and Q10 (enterprises join free annual conference, regular meeting, and seminars organized by Customs); Formal consultation of Customs administration for the import and export enterprises (X2) represents the 2 items: Q11 (enterprises are enthusiastically supported by customs officers about formal consultation in enforcement ofcustoms procedures and information technology), Q12 (enterprises approach easily to information about new customs law, regulation and requirements on Customs websites or Customs office buildings); Joint integrity, corruption observatory (X3) represents item: Q13 (enterprises take part in activities of customs, Vietnam Chamber of Commerce and Industry (VCCI) fighting against corruption, illicit trade, tax evasion). Those items are measured by the 5-points Likert scale with the meaning of the scale from disagreement (1) to a very agreement (5) or poor (1) to good (5). Besides, the dummy variable Edu, which is the educational level of owner’ enterprises, has to mean value Edu = 1 if the level is over the master's degree and values Edu = 0 if it is below.

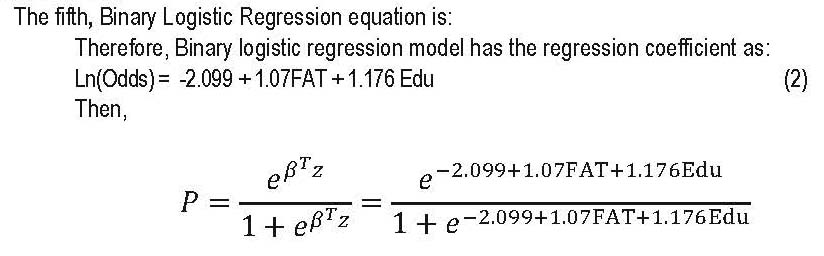

The Binary Logistic regression model is applied and based on the Maximum Likelihood estimation methodin order to estimate the coefficients (βi) in the linear relation between independent variables Xi and Ln (Odds) (The probability of the compliance of the import and export enterprises with customs law and regulation) according to the model:

Ln (Odds) = β0 + β1X1 + β2X2 + β3X3 + β4Edu +ui (1)Odds = P0/(1-P0) where P0 is the probability when Y = 1 and P= 1-P0 is the probability when Y = 0.

The theoretical hypothesis proposes that the coefficients of β1, β2, β3, β4 receive a value> 0; on the other hand, Xi affects Ln (Odds) positively.

Figure 1. The process of the proposed research

Source: Author’s proposal

3.RESULTS

Result of Cronbach's Alpha Reliability Analysis:

Carrying out a reliability analysis of Cronbach’s Alpha with six items from Q1 to Q6, which measure the dependent variable (Y), the outcome of Cronbach's Alpha is 0.73.

Performing reliability analysis of Cronbach’s Alpha with seven items corresponding with 3 predicted explanatory variables Xi; the correspondent results are X1 (0.858), X2 (0.6), X3 (1). Therefore, all of Cronbach’s Alpha coefficients are over 0.6, and their corrected item-total correlation coefficients of 13 items are above

1.3. So, those 13 items are selected to carry out Exploratory Factor Analysis (EFA).

Thanks to the basis of Reliability Test Cronbach's Alpha, the research analyzes EFA with six items relating to Y, from Q1 to Q6, and obtains KMO = 0.76 (>0.5), and value of Bartlett's Test with Sig. = 0.000 (<0.05). The percent of the variance in initial eigenvalues extracted at 51.47% (>50%) shows that one selected factor can explain 51.47% variation of data. Hence, the extracted scales are acceptable. The stopping point when extracting the factor with eigenvalue = 2.48 (≥ 1), representing for variation part is explained by each satisfied factor.

Analyzing EFA with seven items from Q7 to Q13, there are two new groups of factors with seven selecteditems. The percent of the variance in initial eigenvalues extracted at 58.5% (>50%) shows that two selectedfactors can explain 58.5% variation of data. Hence, the extracted scales are acceptable. The stopping point when extracting the factor with eigenvalue = 1.367 (≥ 1), representing for variation part is explained by each satisfied factor. KMO = 0.790 (>0.5), and the value of Bartlett's test with Sig. = 0.000 (<0.05) interpret that applying factor analysis is suitable. (Appendix A, B, and C)

In order to perform logit regression between two new factors (FATi) and dependent variable Y, the research calculates the values of FATi based on items' average value in each factor. The value of responsevariable Y is converted into the binary form based on the average value of items. If the value is greater than or equal to 3.5, then Y = 1, and less than 3.5, then Y = 0.

The descriptive statistic of some variables in the model: the dependent variable Y, considered in 202 samples, has 165 samples Y = 1 (account for 81.7%) and 37 samples Y = 0 (account for 18.3%). The factors FATi have mean value and std. Deviation, which respectively is FAT1 (2.98 and 0.92) including items of Q7, Q8, Q9 and Q10, FAT2 (3.41 and 0.68) including items of Q11, Q12, and Q13. FAT (explains Customs- Business Partnership) is calculated by mean (FAT1, FAT2). It has a mean value (3.19) and std. deviation (0.65). Besides, the dummy variable Edu which is the educational level of owner’ enterprises has mean value at 0.38 and 77 values at Edu = 1 (Edu = 1 if the level is over master degree, account for 46.1%) and 125 values at Edu = 0 (Edu = 0 if it is below, and equal master degree account for 53.9%).

Among two regressed variables, there are FAT and dummy variable Edu with dependent variable Y. According to the output of regression, the article carries out many tests relating to the model, in which:

The first, Wald Test about the statistical significance of correlation coefficients

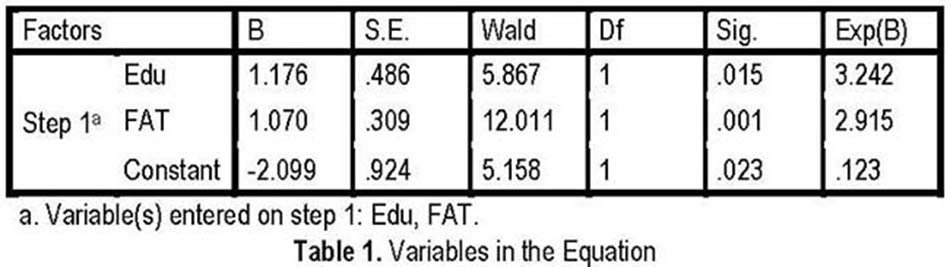

Wald test considers the statistical significance of factor coefficients with regard to the dependent variable (Y) in the model. By accessing table 1, Sig. of factors FAT, Edu and Constant, in turn, have the value at 0.001, 0.015, 0.023 < 0.05, so that the the relationship between explanatory variables and explained variable has general statistical significance over 95% and same direction with Ln(Odds), being appropriate with theoretical model.

With Table 2, the outcome receives the value of -2 Log-likelihood = 169.108a is quite small and Nagelkerke R Square = 0.177, representing the fair appropriateness of the overall model. It means 17.7% of the variation of the dependent variable (Y) is explained by two significant independent variables in the model, 83.7% remain is determined by other factors outside the model.

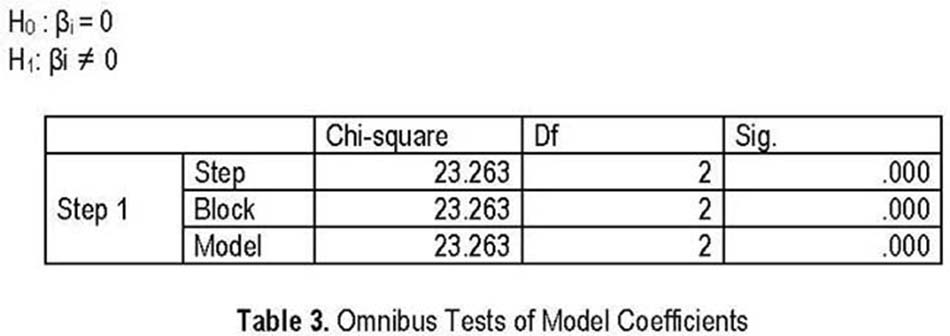

- The omnibus test is used for hypotheses:

H0 : βi = 0

H1: βi ≠ 0

According to Table 3 of Omnibus Tests, having Sig. = 0.000 (<0.05), the research rejects hypothesis H0. Hence, the overall model indicates the correlation relationship between independent variables and the dependent variable has statistical significance with a confidence interval of over 99%.

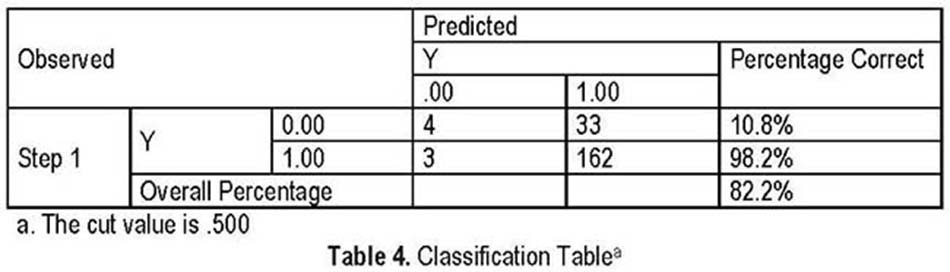

By table 4, in 165 export-import enterprises, which their answers are supposed to be compliance with customs law, the model is able to forecast exactly 162 enterprises, at the rate of 98.2%. Among 37 enterprises, which their answers are supposed to be not compliance with customs law, the model predicts precisely 4 enterprises, accounting for 10.8%. Overall, the rate of accurate predictions of the overall Binary Logistics model is 82.2%.

4.CONCLUSION

Based on the results of the regression models and the statistical value (mean, standard deviation) of the 13 items Qi being statistically significant, some solutions are proposed to improve effectively not only CustomsBusiness Partnership, but also the probability of compliance of import and export enterprises with the customs law and regulation, in which:

Firstly, it is necessary to enhance support of the customs administration for the import and export enterprises effectively and efficiently because the mean of FAT1 only achieves 2.98 and mean of items are also not high, in particular: Q7 (3.3), Q8 (2.74), Q9 (2.73) and Q10 (3.13). First of all, Customs administrationshould increase both quantity and quality of free training and retraining courses, seminars related to contents of customs valuation, a harmonized system of goods and origin of goods, intellectual property rights, and administrative statements. Contents of the courses can approach to case study and scenario research based on real import and export activities and enforcement of customs procedures. It is able to cooperate with the Faculty of Customs and Tax – Academy of Finance to organize the same courses in the provinces.

Next, training courses and seminars related to contents of risk management, compliance management in customs context, voluntary compliance, post-clearance audit, and components and operations of VNACCS/VCIS systems should focus on main topics, such as principles, methodologies, and indicators of risk management and compliance; process of risk management, compliance management, post-clearance audit, also acknowledges about operations of VNACCS/VCIS systems. It is important to select customs excellence experts to take part in those courses. Then, it is possible that Customs administration deals with rapidly the problems and difficulties of the business related to customs procedures, guarantee, deferred payment, tax exemption and drawback procedure in annual regular meetings and seminars. Finally, Customs strengthen to publish and train new customs regulations for import and export enterprises at a customs office building or regular meetings. It is also significant to enhance engagement of business about joint training courses or regular meeting, which is identified the same as one indicator of a compliance evaluation.

Secondly, it is very important to enhance the formal consultation of Customs administration for import and export enterprises. One part, Customs administration should improve not only technical quality of customs officers in terms of customs valuation, harmonized system of goods, administrative statements, and new contents of customs regulations, but also professionalism and consultation attitudes of customs officers. Another part, it is necessary to facilitate import and export enterprises joining formal consultation related to the determination of customs value, harmonized system classification of goods, drawback procedure, and rate of duty. Customs are also to apply a form of automated consultations based on the interactive telephone answering systems.

Thirdly, it is clear that Customs administration should diversify new forms of communication and information exchange related to customs policies and regulations. It is possible to send documents to the email of enterprises, to cooperate with telephone companies in supporting customs regulations to enterprises, or to publish new customs regulations on important TV channels in provinces.

Fourthly, Customs administration needs to encourage customs officers and businesses to enhance customs integrity and fighting against corruption based on the recommendation of the Revised Arusha Declaration: Customs administrations should foster an open, transparent and productive relationship with the private sector. Client groups should be encouraged to accept an appropriate level of responsibility and accountability for the problem and the identification and implementation of practical solutions. Penalties associated with engaging in corrupt behavior must be sufficient to deter client groups from paying bribes or facilitation fees to obtain preferential treatment. Besides, it is able to improve the role of associations in detecting illicit trade, tax evasion, and corruption in international trade and customs declaration (WCO: 1993 and 2003).

The research has achieved the target that finds two significant factors positively affecting the compliance of import and export enterprises with customs law and regulation. Based on domestic and international papers, this research has established a theoretical model of 4 factors with 8 items impacting compliance of import and export enterprises. It used a multivariable regression of Binary logistic model on 202 survey samples and identified two major factors in the same direction statistical significance affecting compliance of import and export enterprises with customs law and regulation, including: (i) Customs-Business Partnerships; (ii) the educational level of owner’ enterprises. In addition, the study proposes four solutions derived from the results of the model. However, the regression model should be further studied in order to explain and detect new influencing factors.

BIODATA

VU DUY NGUYEN: Dr. Vu Duy Nguyen is currently the Deputy Dean of Tax and Customs Department at the Academy of Finance in Hanoi City, Vietnam. He graduated Ph.D. in Public Law at the University of Paris, France where he finished his Masters in Economics and Management. He has published a number of articles relative to Customs Administration and Business Management at peer-reviewed Business and Law Journals and even in Scopus indexed journals.

PERFECTO G. AQUINO: Dr. Perfecto Aquino, Jr is currently a Researcher cum Lecturer at the Social Science and Economics Institute and the Faculty of Business Administration of Duy Tan University in Danang City, Vietnam. He is a holder of Ph.D. in Public Administration and Business Management at the Pontifical University of Santo Tomas, Manila, Philippines, since 2001. He was formerly an Assistant Professor / Head of Business Administration Division at the Emirates College for Management and Information Technology and at the American University in the Emirates, Dubai, United Arab Emirates. He has published a number of papers at double-blind peer-reviewed journals in Business Management and Scopus indexed journals. His areas of research interest include Human Resource Management, Organizational Behavior and Leadership, Entrepreneurship and Family Business, CSR, Marketing Management and Logistics, and Supply Chain Management.

DOAN HONG LE: Dr. Doan Hong Le is presently the Vice-Director and an Associate Professor of the Social Science and Economics Research Institute of Duy Tan University in Danang City, Vietnam. He was a graduate of Doctorate in Philosophy in Business Administration at the University of Danang in Vietnam. He has successfully collaborated and has published some articles relative to Customs and Business Management at ISI and Scopus indexed journals.

BIBLIOGRAPHY

AYRES, I, & BRAITHWAITE, J (1992). Responsive regulation: Transcending the deregulation debate. Oxford University Press, USA.

BOWER, GH (1983). “Affect and cognition. Philosophical Transactions of the Royal Society of London”, in: B, Biological Sciences, 302(1110), pp.387-402.

BRINKERHOFF, JM (2002). “Government–nonprofit partnership: a defining framework. Public Administration and Development”, in: The International Journal of Management Research and Practice, 22(1), pp.19-30

CHEN, L, & MA, Y (2015). Study of the Role of Customs in Global Supply Chain Management and Trade Security Based on the Authorized Economic Operator System. Journal of Risk Analysis and Crisis Response, 5(2), pp.87-92.

DAHL, A, & LINDBLOM, C (1953). Politics, Economics, and Welfare. New York: Harper & Bros.

GRAINGER, A (2010). The role of the private sector in border management reform. BORDER, p.157.

IRELAND, R, Cantens, T, & Yasui, T (2011). An overview of performance measurement in customsadministrations. W CO Research Papers, (13), pp.1-10.

JEANNARD, S (2010). Focusing Customs on Client Service. WCO News 61 (February), p.24.

MIKURIYA, K (2010). speech delivered on International Customs Day 2010, Brussels, 26 January 2010, viewed 1 August 2010.

MIKURIYA, K (2012). Expansion of Customs-Business Partnerships in the 21st Century. The Global Enabling Trade Report 2012, 1.

PANDEY, PN (2016). “Customs-Business Partnership including AEO Programme. WCO”. Retrieved on May 30, 2019, from: http://www.wcoomd.org/-/media/wco/public/global/pdf/events/2016/global-aeo- conference/presentations/session-2-track-d_customs_business-partnership-inlcuding-aeo.pdf?la=en.

TRANSPARENCY INTERNATIONAL (2009). Corruption Perceptions Index 2009. Geneva: Transparency International.

VU, ND (2014). “Application of information technology to treat asymmetric information in customs proceduresPolicy implications”, in: Journal of Finance, Number, 602, pp.70-75.

WCO (1993 and 2003). “The revised arusha declaration: Declaration of the customs co-operation council concerning good governance and integrity in customs”, Done at Arusha, Tanzania, on the 7th day of July 1993 (81st/82nd Council Sessions) and revised in June 2003 (101st/102nd Council Sessions). Retrieved on July 1, 2019, from: http://www.wcoomd.org/-/media/wco/public/global/pdf/about-us/legal- instruments/declarations/revised_arusha_declaration_en.pdf?la=en

WCO (2015). “Customs-Business Partnership Guidance”. Retrieved on June 1, 2019, from: http://www.wcoomd.org/en/media/newsroom/2015/july/~/media/E2B8A58843F44C55AD21BBE9BA2672B3. ashx.

WCO (2015). “WCO instruments and tools relevant for CBM”. Retrieved on June 1, 2019, from: http://www.carecprogram.org/uploads/events/2016/25-CBM-Subregional- Workshop/Presentations/Session%202%20-%20WCOinstrumentsandtoolsrelevantforCBM.pdf

WCO. (1999). “International convention on the simplification and harmonization of customs procedures”, Revised Kyoto Convention. Retrieved on May 30, 2019, from: http://www.wcoomd.org/en/topics/facilitation/instrument-and- tools/conventions/pf_revised_kyoto_conv/kyoto_new.aspx

WEI, L (2013). “Customs-Business Partnerships: A Case Study on The China Customs Goods Classification- Inadvance Specialist Programme”, in: Customs Scientific Journal CUSTOMS, 3(1), pp.57-69

WETTENHALL, R (2003). “The rhetoric and reality of public-private partnerships”, in: Public Organization Review, 3(1), pp.77-107.

WTO (2014). Trade Facilitation Agreement. Retrieved on June 10, 2019, from:https://www.wto.org/English/docs_e/legal_e/tfa-nov14_e.htm

ZHANG, S, & PREECE, R (2011). “Designing and implementing Customs-Business partnerships: a possible framework for collaborative governance”, in: World Customs Journal, 5(1), pp.43-62.