Artículos

Local Governments Accountability: A Content Analysis of the Financial Audit Reports

Responsabilidad de los gobiernos locales: un análisis de contenido de los informes de auditoría financiera

Local Governments Accountability: A Content Analysis of the Financial Audit Reports

Utopía y Praxis Latinoamericana, vol. 25, núm. Esp.1, pp. 184-195, 2020

Universidad del Zulia

Recepción: 04 Marzo 2020

Aprobación: 30 Abril 2020

Resumen: Esta investigación examina la responsabilidad financiera de los gobiernos locales, basada en los estados financieros auditados del gobierno regional. Los datos recopilados de los estados financieros se centraron en los fondos de la aldea transferidos del Gobierno Central a los gobiernos locales en la provincia de Papua, Indonesia. Las autoridades regionales funcionan como intermediarios para transferir los fondos a las aldeas. Se aplica un análisis de contenido cualitativo, utilizando criterios de las Normas de Contabilidad Financiera del Gobierno (GFAS). El análisis revela que los informes financieros todavía tienen muchas deficiencias; casi todos los informes no utilizan el GFAS. Se concluye que las insuficiencias de los informes indican el déficit de responsabilidad financiera.

Palabras clave: Contabilidad financiera, descentralización fiscal, fondos de aldea, Indonesia..

Abstract: This research examines the financial accountability of local governments, based on the audited Regional Government Financial Statements. Data collected from the financial statements focussed on the village funds transferred from the Central Government to local governments in Papua Province, Indonesia. The regional authorities function as intermediaries to transfer the funds to villages. For analysis, the research applies a qualitative content analysis, using criteria from the Government Financial Accounting Standards (GFAS). The analysis reveals that financial reports still have many deficiencies; almost all reports do not utilise the GFAS. The study resolves that insufficiencies of reporting indicate the shortfall of financial accountability.

Keywords: Financial accountability, fiscal decentralization, Indonesia, village funds..

INTRODUCTION

The financial decentralization literature reveals the transfer of funds from the central government to regional governments. The literature describes that the central government allocates funds to the local governments for carrying out development and for providing public services to the local communities. The theory of decentralization explains that local governments understand the situation and problems to serve citizens better than the central government. Local governments can work more swiftly and answer to the needs of citizens (Oates, 1993).

According to Martinez-Vazquezet al. (2017) the study of fiscal decentralization has received much attention from researchers for three reasons. First, there is the widespread belief that fiscal decentralization is an effective policy to improve the efficiency of public spending. Second, fiscal decentralization can fix the failures of a centralized bureaucracy under the ruling political regimes in some developing countries. Third, fiscal decentralization can break the grip of the central government on the regional economy, especially regions rich in natural resources.

Since 1999, the fiscal decentralization policy in Indonesia began.

This policy gives authority to regionalgovernments to finance regional affairs regulated in the Law on Regional Government (Law 22/1999). In the same year the Law on Central and Regional Financial Balance (Law 25/1999) was issued, which became the basis for implementing fiscal decentralization1.

The Indonesian government transfers several types of funds to local governments. Since 1999, the government has transferred the General Allocation Fund (DAU), the Tax and Non-Tax Profit Sharing Fund (BHPBP), the Special Allocation Fund (DAK), the Special Autonomy Fund (DOK) and several other types. Transfer funds have a substantial contribution to the regional budget. The Ministry of Finance noted 66 per cent of regional income came from transfer funds in the fiscal year 2017 (Kementerian Keuangan, 2017).

Since 2015, the Government of Indonesia has extended the practice of fiscal decentralization by transferring funds to the village governments. The Government rules the village funds by the enactment of Law Number 6 of 2014 concerning Villages (Law 6/2014). The Village Fund (Dana Desa, DD) is a transfer fund from the Government’s national budget provided to village authorities throughout Indonesia. The funds are sent to the district/city budget to be forwarded to the village governments. Distribution of DD is not direct to the village governments. This phenomenon is decisive considering there are district / city governments channeling the distribution.

The presence of district/city entities as intermediaries in transferring funds can cause financial accountability problems. Most local government entities still have problems with financial accountability. About 75 per cent of audit reports on the Regional Government Financial Report (LKPD) in Papua Province still have a disclaimer opinion. The opinion indicates a lack of accountability and financial transparency. The leading causes of this problem are ineffectiveness of the Internal Control System (SPI), non-compliance with regulations, poor quality of human resources, lack of leadership commitment, and lack of supporting technology (Harun & Kamase, 2012).

Accountability of village funds in this study is defined as the appropriateness of presentation anddisclosure of funds in the Regional Government Financial Report (LGFR or LKPD). This report is annually audited by the Supreme Audit Board of Indonesia (SAI or BPK), which then issues a Financial Audit Report (FAR or LHP).

The imprecision of financial accountability is seized as the foremost reason for this research. Financial accountability and management of public funds are among the most sensitive aspects of government activity in democracies. For Indonesia, since 2003, this country entered a new era in directing and controlling government finances. In that year, Indonesia enacted the State Finance Law (Law 17/2003), followed by two other laws governing the country's National Treasury (Law 1/2004) and Audits and Financial Management (Law 15/2004).

Accounting and auditing infrastructures are the primary vehicles in advancing the accountability of government finances. Chan emphasized that government financial accounting and reporting aim to protect and control public money and carry out accountability(Chan, 2003). To drive financial accountability, accounting and financial reporting regulate with government accounting standards. This standard consists of some criterion for assessing the accountability practiced by many countries(Allen, 2002).

The literature cites some definitions of financial accountability but is still changing. Every individual paperformulates the definition according to its operational needs. Premchand explains that the definition keeps on changing(Premchand, 1999). For this paper, financial accountability is interpreted as compliance by financial managers in preparing and submitting financial reports to stakeholders and the general public. This accountability can be measured by the criteria of conformity with government accounting standards and the adequacy of the information presented. Financial accountability is designed to furnish information to the public about government financial conditions and performance, service efforts, and achievements. The urgency of the topic is among others revealed by the practice of non-compliance with regulations including the possibility of misuse of public funds. To analyze the issue, the author elaborates the assessment criteria from the Government Financial Accounting Standards (GFAS) applied in Indonesia.

The research topic of fiscal decentralization has received much attention in economics, government administration and politics. Numerous studies illustrate the practice of devolution in developed and developing countries. The impact of fiscal decentralization on poverty, economic growth, income distribution, education and health services has been well documented in numerous publications publications (Kis-Katos & Sjahrir, 2017). The misuse and corruption of transfers funds have also got the attention of some scholars(Rinaldi, Purnomo, & Damayanti, 2007). However, the success of fiscal decentralization studies has not been accompanied by accountability and transparency research. For researchers in government financial accounting, this topic is momentous to add to the information of "how can misuse and corruption occur in the process of transferring funds between government entities?"

METHODS

This research practices a case study strategy as a means to provide a deeper understanding of how specific organizations as a unit of analysis choose a new accounting system. Yin (2017) proposed that a case study approach can be applied to develop and form theories. In contrast to quantitative approaches, a qualitative approach is designed to explain why and how issues connect to particular settings. The use of the method has previously appeared in various accounting studies investigating accounting changes in an organization(Feng, Cummings, & Tweedie, 2017).

The present study gained data from three kinds of documents: regulations of village funds, financial auditreports, and data from the Central Statistics Bureau. There were 87 audit documents utilized in the study. The reports belong to 29 local governments issued in three reporting years of 2015-2017. The statements were obtained from the Central Office of Supreme Audit Institution (BPK), Jakarta. The report consists of three books: Book I comprises the Local Government Financial Report, Book II holds audit results of the Internal Control System, and Book III contains the Compliance Audit Report.

Other documents used are regulations. Three regulationshave become fundamental references for DD management, namely:

(1) The provision on village financial management from the Ministry of Home Affairs;

(2) The rules on the priority usage of village funds, from the Ministry of Villages, Development of Underdeveloped Regions, and Transmigration;

(3) The procedures for allocation, distribution, use, monitoring and evaluation from the Ministry of Finance.

In order to collect and analyze the data from the reports, the research built up selection criteria applying the Government Financial Accounting Standards. Three standards are to apply in providing sufficient information in the LGFR, namely:

-

Standard Number 3 on Cash Flow Report (GFAS No. 3)

-

Accounting Bulletin Number 14 on Cash Accounting

-

Accounting Bulletin Number 21 concerning Accounting of Transfer Fund.

This study analyzes reports and regulations using a qualitative content analysis approach. Some accounting studies already practiced this method (Guthrie & Abeysekera, 2006).Hsieh and Shannon suggested three approaches to qualitative content analysis, namely conventional, directed, and summative(Hsieh & Shannon, 2005). The conventional method analyzes and categorizes information into concepts (constructs) with coding derived directly from text data. A directional approach starts the analysis by selecting concepts from theories or research findings, which then become the basis of coding. Summative content analysis involves the calculation and comparison of content, followed by the interpretation of the context in which the research is based.

RESULTS AND DISCUSSION

The villages’ funds

The Indonesian Government allocates village funds from the national budget. The funds increase every fiscal year. Starting in 2015, the Government sent funds around Rp.20,766 trillion (US$ 1,473 billion), increasing to Rp.46,982 trillion (US$ 3,332 billion) in 2016. The figure continued increasing and reached Rp.70 trillion (US$ 4,965 billion) for the fiscal year 2019. The Government allocates village funds at 10 per cent from the total transfer funds to the local governments (on top) (Government Regulation 60/2014). In 2019, each village is estimated to receive around Rp.934 million (US$ 66,235) (Ministry of Finance, 2018).

The primary purpose of transferring funds to villages is to encourage citizen participation for development. The argument is that development should begin from the kampongs because the majority of Indonesians live in villages. A sizable part of the population in the villages is still trapped in absolute poverty. According to the Central Bureau of Statistics, the number of poor people in the year 2018 was 25.67 million people, 61 per cent of whom living in rural areas (Central Bureau of Statistics, 2019). The distribution of village funds, according to President Jokowi, is a form of state policy towards "building from the periphery." (Rusdiyanta & Yono, 2018).

The Government's expectation to provide funds for villages is to continue encouraging the independentdevelopment of communities and move out of poverty. The Government expects that local governments can manage the DD properly by spending, supervising and reporting the funds according to laws and regulations. The regulations provide stages, principles and standards to follow by local governments. In the reporting stage, regional authorities should apply the Government Financial Accounting Standards, the regulation of financial accounting and reporting in Indonesian governments. Hence, the research adopts the compliance with Standards as the measure of financial accountability. A great deal of previous research into financial accountability has focused on accounting standards standards (Ellwood, 2003).

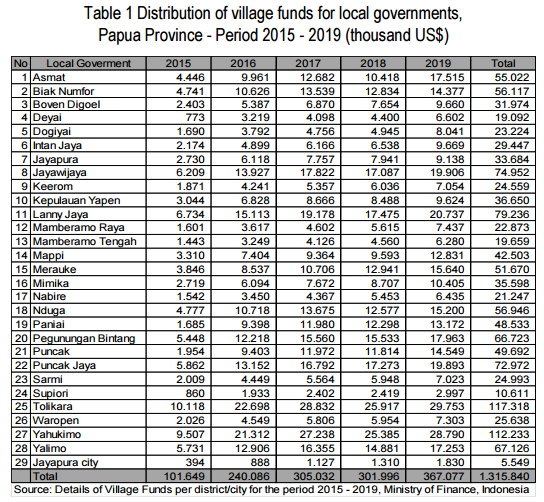

Village funds for Papua

Similar to other provinces, the districts and cities in Papua began to get DD since 2015. Total funds obtained is about US$1.316 billion, for the fiscal years 2015-2019 (Table 1). Over the past five years, two districts got more than US$100.000, namely Tolikara and Yahukimo; however, some only received US$5.000. On average every kampong gets US$68.000 for one fiscal year.

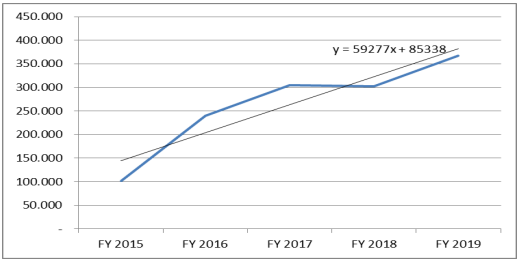

The growth index of the funds has increased, except in the 2017-2018 period (Figure1). The trend shows that every year the funds increase by US$59.000.

Every year the value of village fund transfers to districts and cities in Papua continues to grow. Figure 1 displays the coefficient increase of the transfers about US$59,277 thousand. However, the rise did not evenly distributed to all local governments. Some districts increased as high as 4 thousand dollars per year, such as Yahukimo and Tolikara; but some risen only 500 dollars, Jayapura City and Supiori district. The difference is due to the number of villages, the price expensiveness, and the population.

Figure 1- Growth of village funds in Papua Province for the fiscal years 2015-2019

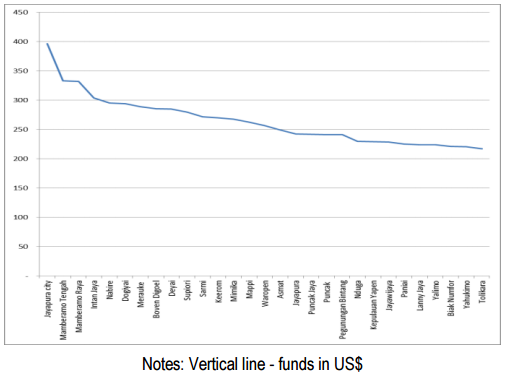

In contrast to the transferred funds for every local government entity, if we measure the funds for each village, it turns out that villages in Jayapura City seize the highest amount. Everyvillage in Jayapura City received, 60 per cent higher funding than the average village in Papua (Figure 2). This is because the number of villages in Jayapura City is only 14 entities. A small number compared to some districts with 500 villages, like Tolikara and Yahukimo.

Notes: Vertical line - funds in US$

Obligations of the Districts/City

To ensure that funds are well managedand reported, the Central Government regulates the implementation to be applied by local governments. The local governments are to obey the regulations covering the state of budget, allocation, distribution, implementation, reporting, monitoring and evaluation.

-

Budgeting. Each district/city has to prepare a budget plan for the next year. Budget values refer to budget allocations determined by the Government - the Ministry of Finance. The budget is presented as a target in the Budget Realization Report (LRA).

-

Allocation. The allocation arrangements, the funds' calculation for each village, are determined by the regulations of the regional head. The provision refers to the decision of the Ministry of Finance.The allocation has three parts, namely the primary allocation, affirmations allocation, and formula allocation. The primary allocation limits the minimum amount for any village, while the formula and affirmation allocations apply the variables of poverty, population size, and price of construction materials. The amount of formula allocation is calculated with the following weights: 10 per cent for the population variable, 50 per cent for the poverty rate, 15 per cent for the total area; and 25 per cent for geographic difficulty levels.

-

Distribution. Furthermore, the district/city government distributes the funds according to the schedule from the State Treasury: March, July and October. If the local Government receives the funds, they have to transfer them to the villages immediately - no later than seven working days. For remote areas, which have not yet been reached by banking services, the regional head can determine a special arrangement. If local governments are not compliant in distributing funds to villages, they may be subject to sanctions from the Government by delaying the General Allocation Funds (GAF or DAU) or Revenue Sharing Funds (RSF or DBH).

-

Implementation. The Central Government2 regulates the priority usage of funds. For deployment in their respective regions, regional heads set the use of funds by preparing the Technical Guidelines for the Use of Funds. The Guideline applies to regulations issued by the Government.

-

Reporting. District/city governments should spend time to facilitate villages to prepare accountability reports. Also, local governments provide semester reports to the Government.

-

Monitoring and evaluation. Local governments are also required to monitor and evaluate the Remaining Budget Calculation (SiLPA). The amount of SiLPA reveals the portion of funds that have not been used by the village governments. A high amount ofSiLPA means the use of funds is not optimal. If the SiLPA reaches 30 per cent, the regional head is obliged to (1) request an explanation from the village head regarding the SiLPA, and (2) ask the inspectorate to conduct an audit. The problem of SiLPA can cause delays of DDtransfer.

The Accountability of village funds

The Government of Indonesia rules all government entities to prepare and present financial reports since 2005. These responsibilities are set out in Government Financial Accounting Standards, established in the Government Regulation Number 24, 2004. Next, the standards were replaced with accrual-based Government Financial Accounting Standards stipulated in Government Regulation Number 71, 2010.

Accrual-based accounting standards require all government units preparing and reporting seven types of reports. The reports are Budget Realization Report (BRR), Statement of Changes in the Excess Budget Balance (SEB), Operating Statement (OS), Statement of Changes in Equity (SCE), Balance Sheet, Cash Flow Statement (CFS), and Notes to Financial Statements (Notes). This study analyzes the contents of five reportsBRR, OS, Balance Sheet, CFS, and Notes. The other two reports excluded from the analysis because they only contain change summary of other reports - the LRA, and the SEB summarizes the BRR and SCE summarizes the OS.

Disclosure in the Cash Flow Statement

Local governments administer cash receipts and disbursements through the Regional Cash.At the end of the fiscal year, the government prepares a Cash Flow Statement (CFS)which presents information on cash inflows and outflows. There are four types of cash flows, namely operating activity cash flow, investment activity cash flow, financing activity cash flow, and temporary cash flow (non-budget cash flow).

The standardnumber 3 on Cash Flow Report states that the receipt and disbursement of village funds should be disclosed in the "Temporary Cash Flow" section (criterion 1). Furthermore, the funds should be named "Village Funds" (criterion 2).

The analysis for the Cash Flow Statement found:

-

None of the Cash Flow Reports presented the funds following the GFAS - the receipt and distribution of the funds should be disclosed in the Temporary Cash Flow section.

-

More than 60 per cent of the Cash Flow Report mixed the funds with other transferred funds from the central government. We, therefore, cannot identify the amount of DD from these reports.

-

More than 85 per cent of the disbursement funds did not specifically mention the name "Village Funds" in the Cash Flow Report.

From the above analysis, the paper concludes that most of the Cash Flow Reports under the study did not present DD information noticing the SAP. The users of such reports could not be able to gain enough information, such as the DD balances. This case suggests that accountability of the funds is not appropriately stated in the Cash Flow Statements.

Disclosure in the Budget Realization Report

The Budget Realization Report (BRR)shows an overview of regional revenue and expenditure prepared on the cash basis accounting. This report compares the targets and realization in the current year and the realization of the previous year.

Accounting Bulletin Number 21 concerning Accounting of Transfer Funds instructs the presentation of DD in the BRR. The Bulletin regulates that DD receipts are disclosed in the Other Central Government Transfers section, under the "Village Funds" account (criterion 3). The distribution is disclosed in the Village Transfer section, under the account name "Village Fund Distribution" (criterion 4).

The analysis of the Budget Realization Report found:

-

Only one district, Jayawijaya, consistently followed Bulletin Number 21 (criterion 3 and 4) during the three reporting years. Starting in 2016, five other districts located close to Jayawijaya met the criteria. Asmat and Jayapura City met the criteria in the year 2017.

-

Most local governments mixed the DD with other funds transferred from the Central Government. Users of financial reports could not find specific information in such a report.

The analysis suggests that most of the Budget Realization Reports have not met criteria 3 and 4. Most of the reports are not following Bulletin Number 21 on Accounting of Transfer Funds. In the end, it can be said that the financial accountability of the funds is not well considered.

Disclosure in the Operating Statement

The Operating Statement (OS) is a mandatory report in the accrual base accounting. The report presents income and expense transactions that change the equity funds of a government entity. Income transactions rise the equity funds, while the expense transactions reduce the equity funds.

In the DD transferred mechanism, the district and city only act as agents to distribute the funds for villages. They are not allowed to use the funds for their daily operation. The accounting standards (Bulletin 21) rule that the DD does not change the equity funds, so they should not report the funds in the OS (criterion 5). When a local government entity reports the funds in the OS, they are likely to claim the funds as their own equity and to report low or high equity funds.

The analysis of the OS reports found:

-

The Asmat District obeyed the Accounting Bulletin 21 that the village funds are not changing the equity funds. So Asmat District met criterion 5.

-

Other 28 local government reported that the village funds received from the Central Government as an income. They also reported the transfer funds to the villages as an expense.

Based on criterion 5, only one out of twenty-nine local governments disclose proper Operating Statements. Most local governments account the funds transferred from Central Government as their income and transfer to villages as an expense. The result is that the equity funds are misstated - higher or lower than the real position. Criterion 5 is not met.

Disclosure in the Balance Sheet

A balance sheet is a financial report about the position of assets, liabilities, and equity at a specific date.

Bulletin 14 on Cash Accounting explains that a portion of cash not belonging to the government should be disclosed in the debit side as "Restricted Cash Account" in the Non-Current Assets group (criterion 6). The credit account is "Debt to the Village Government - Village Funds", disclosed in the short-term debt section (Bulletin 21) (criterion 7).

After tracing the contents of the balance sheet, the study foundthat:

-

Asmat's balance sheet met the requirement of criterion 6 - disclosed untransferred fund in the "restricted cash account" for the year 2017.

-

Amazingly Asmat's report did not disclose the contra or credit account, "Debt to the Village Government - Village Funds" (criterion7)

-

Other local governments did not present DD balances in the Balance Sheet. It is not clear, however, whether the funds have been fully transferred or not. The accounting staff might not recognize how to present such information in the balance sheet.

From the tracing of the Balance Sheet, it is found that the reports can mislead the users. They might think that funds have already been fully transferred, but in fact, some balances are still in the local governments. So, most Balance Sheet reports do not fulfill criteria 6 and 7. Based on these findings, it is concluded that the Balance Sheets have not adequately maintained the accountability of local governments.

Disclosure in the Notes to Financial Statements

Notes to the Financial Statements (Notes) is a narrative explanation of the financial statements: Report on Realization of Budget, Report on Changes in Balance Budget, Operational Report, Report on Changes in Equity, Balance Sheet, and Cash Flow Report (PP 71/2010). CaLK also includes information about the accounting policies adopted by reporting entities and other information required by the GFAS.

Minimum disclosure of DD in CaLK should contain the untransferred balance, split down by villages (criterion 8).

The CaLK tracking recorded:

-

Only two CaLK revealed the cash balance: CaLK of Asmat and Jayawijaya districts. The CaLK also clarifies details of villages not receiving the funds in the years of 2016 and 2017.

-

No CaLK disclose any Village Fund Debt.

From the analysis of the Notes, there was not enough information to support the financial accountability of DD - indicating criterion 8 is not met.

Reasons for accountability deficiencies

The low accountability of village funds can be traced through four factors. The factors are the quality of human resources, lack of information technology, lack of internal and external audits, and a culture of forgiveness.

The first factor is human resources. In recent years, there has been an increasing amount of literature stating the shortfall of accounting staff in Indonesia (Harun, An, & Kahar, 2013).Numerous accounting staff in local governments do not have an education in accounting, so they simply rely on short training (Basri & Nabiha, 2014). There are not enough accounting staff to master the complex problems of the accounting standards. Such complex problems are regularly caused by the change of standards. Standards often change to harmonize with the new financial policies of the Government(Kaplan & Ruland, 1991). As an example, the policies of village fund transfers from the Government to local governments, which came into effect since 2015 brought a new standard, Bulletin 21 on Accrual-based Transfer Funds. This new standardis not widely acknowledged and practiced by the local governments' accountants.

The second factor is information technology (IT). Any local government financial reports are generated from a Local Government Accounting System (LGAS or SAPD). Report compilation is no longer prepared manually, but with a computer application system. This computer application system needs to be adjusted to any new standard. If a new standard is introduced, a local government needs to adjust the LGAS immediately. The lack of programmers to resolve the LGAS according to the new standards soon brings another problem to the preparation of financial reports. Most local governments in Papua still lack experienced programmers, so they have to hire the IT consultants from outside Papua.Indonesia still had difficulty meeting the needs of IT experts, because around 75 per cent of graduates worked in industries that were engaged in non-IT fields (kompas.com,25/11/2013).

The third factor is internal and external auditors. In Indonesia, the Ministry of Home Affairs’ Regulation concerning Guidelines for Reviewing Local Government Financial Reports (Permendagri 4/2008) states that the internal auditors are required to review the financial statements before being audited by external auditors. This provision implies that internal auditors should have the ability to review the suitability of the reports; however many internal auditors have not been effective in conducting this review due to their limited competencies. Also, the external auditors of SAI have some restrictions to audit the financial reports because of the wide scope audit and the time limitation for audit activities (IAB, 2016).

The fourth factor is the culture of forgiveness. Some policies implemented in Papua are often followed by a coaching stage. Coaching stage means the execution of a program still in the preliminary process, and it needs some time to be thoroughly evaluated. When there is a problem in the implementation, it is often associated with the "coaching stage". It is the same when something is wrong with the implementation of accounting standards; it needs to be forgiven. Some recent studies suggest that forgiveness is an interpersonal process that focuses on behavior, such as reconciliation, which leads to the restoration of social harmony. The forgiveness is also often used as an euphemism covering up corruption(Flicker & Bui, 2018; Znoj, 2017).The forgiveness is also often used as an euphemism covering up corruption (Szeftel, 1998).

CONCLUSION

In conclusions, the lack of accountability in village transfer funds are, on the one hand, a consequence of the mismatch between accounting standards set by the Central Government and accounting capabilities in the local governments. On the other hand, this lack of accountability opens up opportunities for undetectable corruption on various levels of government. The fact that the total amounts spent for village transfer funds are rising spectacularly every year despite a near-total lack of accountability – at least in the province of Papua raises questions of responsibility within the ministry of finance itself.

The study of financial accountability is a research topic that continues to get attention. Analysis of financial accountability is quite likely to expand due to the availability of audited financial reports from the Supreme Audit Institution (SAI).Criteria applied in the research can be enhanced using the same Government Accounting Standards. In doing so, other researchers are encouraged to add more criteria. This study signals an alternative way to examine financial accountability by using audited financial statements, which are now available from Indonesia's SAI.

BIODATA

Agustinus Salle: Is a lecturer at Accounting Department, University of Cendrawasih. Indonesia

Acknowledgements

I would like to express my very great appreciation to Prof. Dr. Heinz peter Znoj from the Institute of Social Anthropology, University of Bern, Switzerland for his valuable and constructive suggestions for this research work. His willingness to give his time so generously has been very much appreciated.

BIBLIOGRAPHY

ALLEN, T. L. (2002). “Public accountability and government financial reporting”. In Models of public budgeting and accounting reform (Vol. 2, pp. 11–36).

BASRI, H. & NABIHA, A. K. S. (2014). “Accountability of local government: The case of Aceh Province”, Indonesia. Asia Pacific Journal of Accounting and Finance, 3(1), 1–14.

CENTRAL BUREAU OF STATISTICS (2019). Statistical yearbook of Indonesia 2019. Jakarta.

CHAN, J. L. (2003). “Government accounting: An assessment of theory, purposes and standards”. Public Money & Management, 23(1), 13–20. https://doi.org/10.1111/1467-9302.00336

ELLWOOD, S. (2003). “Bridging the GAAP across the UK public sector”. Accounting and Business Research, 33(2), 105–121.

FENG, T., CUMMINGS, L. & TWEEDIE, D. (2017). “Exploring integrated thinking in integrated reporting–an exploratory study in Australia”. Journal of Intellectual Capital, 18(2), 330–353.

FLICKER, S. M. & BUI, L. T. T. (2018). Cross-cultural differences in interpersonal and intrapersonal understandings of forgiveness. In & W. F. . Karasawa, M. Yuki, K. Ishii, Y. Uchida, K. Sato (Ed.), Venture into cross-cultural psychology: Proceedings from the 23rd Congress of the International Association for Cross- Cultural Psychology.

GUTHRIE, J. & ABEYSEKERA, I. (2006). “Content analysis of social, environmental reporting: what is new?” Journal of Human Resource Costing & Accounting, 10(2), 114–126.

HARUN, H. & KAMASE, H. P. (2012). “Accounting Change and Institutional Capacity : The Case of a Provincial Government in Indonesia”. Australasian Accounting Business & Finance Journal, 6(2), 35–50.

HARUN, H., AN, Y. & KAHAR, A. (2013). “Implementation and challenges of introducing NPM and accrual accounting in Indonesian local government”. Public Money & Management, 33(5), 383–388. https://doi.org/10.1080/09540962.2013.817131

HSIEH, H.-F. & SHANNON, S. E. (2005). “Three Approaches to Qualitative Content Analysis Hsiu-Fang Hsieh Sarah E. Shannon Content”. Qualitative Health Research. https://doi.org/10.1177/1049732305276687

IAB (2016). Annual report 2016. Jakarta: Audit Board of the Republic of Indonesia/Badan Pemeriksa Keuangan.

KAPLAN, S. E. & RULAND, R. G. (1991). “Positive theory, rationality and accounting regulation”. Critical Perspectives on Accounting, 2(4), 361–374.

KEMENTERIAN KEUANGAN. (2017). Peraturan Meneteri Keuangan Nomor 199/PMK/.07/2017 Tentang Tata Cara Pengalokasian Dana Desa Setiap Kabupaten/Kota dan Penghitungan Rincian Dana Desa Setiap Desa.

KIS-KATOS, K. & SJAHRIR, B. S. (2017). “The impact of fiscal and political decentralization on local public investment in Indonesia”. Journal of Comparative Economics, 45(2), 344–365.

KSAP. (2010). Conceptual framework of Indonesian government financial reporting. Government Accounting Standards Committee.

MARTINEZ‐VAZQUEZ, J., LAGO‐PEÑAS, S. & SACCHI, A. (2017). “The impact of fiscal decentralization: Asurvey”. Journal of Economic Surveys, 31(4), 1095–1129.

OATES, W. E. (1993). “Fiscal decentralization and economic development”. National Tax Journal, 46(2), 237– 243.

PREMCHAND, A. (1999). Public financial accountability. In S. Schiavo-Campo (Ed.), Governance, Corrupption and Public Financial Management (pp. 145–192). Manila, Philippines: Asian Development Bank.

RINALDI, T., PURNOMO, M. & DAMAYANTI, D. (2007). Fighting corruption in decentralized Indonesia. The Local Government Corruption Study (LGCS).

RUSDIYANTA, R. & YONO, B. (2018). “Asymmetric Policy of Border Area Development in Indonesia (Joko Widodo-Jusuf Kalla Government Period)”. International Journal of Pure and Applied Mathematics, 17, 945– 953.

SUTIYO & MAHARJAN, K. L. (2017). Decentralization and rural development in Indonesia. Singapore: Springer.

SZEFTEL, M. (1998). “Misunderstanding African politics: Corruption & the governance agenda”. Review of African Political Economy, 25(76), 221–240.

TORRES, L. (2004). “Accounting and accountability: Recent developments in government financial information systems”. Public Administration and Development, 24(5), 447–456. https://doi.org/10.1002/pad.332

YIN, R. K. (2017). Case study research and applications: Design and methods. Sage publications.

ZNOJ, H. (2017). “Deep corruption in Indonesia: discourses, practices, histories”. In Corruption and the Secret of Law (pp. 53–74). Routledge.

Notas