Artículos

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 3.0 International.

Received: 02 March 2020

Accepted: 10 April 2020

DOI: https://doi.org/10.5281/zenodo.3808567

Abstract: The operational audit uses to explain cost variances that occurred in the delivery of healthcare services to inpatients utilizing the BPJS. This study aimed to identify cost variance between actual cost and set tariff for inpatients management of chronic ischemic heart disease, cerebral stroke, final-stage of renal disease, and diabetes mellitus type-2. This study had shown that cost containment via cost monitoring and cost management could be obtained. Variance cost of managing some diseases is unavoidable due to the unique patient's characteristics and different costing methods. Steps could be taken up to ensure the operations are performed effectively and efficiently.

Keywords: Cost containment, cost variance, hospital, operational audit..

Resumen: El uso de auditorías operativas explica la diferencia en los costos incurridos al proporcionar servicios a los pacientes hospitalizados que usan BPJS. Este estudio tiene como objetivo identificar la diferencia de costo entre los costos reales y las tasas establecidas para la hospitalización de los tratamientos cardíaco isquémicos crónicos, infarto cerebral, enfermedad renal en etapa terminal y diabetes tipo 2. Se puede obtener la contención de costos a través del monitoreo y la administración de costos. El costo de la variación para manejar varias enfermedades no se puede evitar debido a las características y al método de diferencia de costos. Se toman medidas para garantizar que las operaciones se lleven a cabo de manera efectiva y eficiente.

Palabras clave: Auditoría operativa, contención de costos, hospital, variación de costos..

INTRODUCTION

Financing healthcare for the people in Indonesia is via social or national health insurance, which was introduced in 2014 (National Team for the Acceleration of Poverty Reduction: 2015). The government has launched the Healthcare and Social Security Agency (BPJS) which applied INA-CBGs (Indonesian Case- Based Categories) for its payment mechanism at all hospitals, primary healthcare, and clinics (National Team for the Acceleration of Poverty Reduction: 2015). INA-CBGs which were regulated in Regulation No. 27, applied the case-mix system which is standardized by the health ministry. The coding is according to ICD-10 (International Classification of Disease) and ICD-9 CM (Clinical Modification) for every medical procedure and service tariff (Ifalahma: 2013, pp. 15-18). In the same year, the health service tariff of the National Health Insurance program was regulated in Regulation No. 59 (Ministry of Health of Republic of Indonesia: 2014a).

The INA-CBGs had applied a payment model through prospective payment whereby every service including the needs of medical equipment and others had been counted as a package according to the case or disease groups (National Team for the Acceleration of Poverty Reduction: 2015). The INA-CBGs payment model is the number of claims that Healthcare and Social Security Agency pay in advance to healthcare facilities for their services, according to the diagnosed illness (National Team for the Acceleration of Poverty Reduction: 2015). This payment model has 1,077 tariff groups consisted of 789 codes of inpatient group and 288 codes of the outpatient group (Ministry of Health of Republic of Indonesia: 2014b). It motivates hospitals to develop instruments for quality control service and cost containment, namely Clinical Pathway and Clinical Practice Guidelines (PPK) as the standard guidelines for the treatment of diseases (Budiarto & Sugiharto: 2013, p. 7). Also, INA-CBG’s tariff warrants the health services to be paid in equal value according to diagnosis code and medical treatment. Hospitals are committed to provide quality clinical care, not disregard the needs to meet the treatment tariffs that had been agreed upon.

Operational audit is an assessment towards operational activities or operational method and procedurein an organization which aim to assure efficiency rate and its effectiveness (Guy et al.: 2003); to know whether the activity was conducted effectively, efficiently and economically (Gabby: 2015, pp. 303-304; Syah: 2019, pp. 71-88); and to identify activity or program which needed recommendation of management (Bhayangkara: 2008). This assessment could give information to the management about the operational problem and help to solve the problem by suggesting any action (Guy et al.: 2003; Knechel & Salterio: 2016). The operational audit should be done by the auditing team annually to reveal any odd result such as cost variance and discrepancy. The hospital could utilize operational audits for actual operational costs to achieve high efficiency along with improving the quality of health service.

One of the problems that could be identified in the operational audit at the hospitals regarding INA-CBGs and health costs to the actual tariff from the hospital is cost variance. The cost variance here is the difference between the INA-CBGs tariff and the actual amount spent by the hospital in rupiah value. Cost variance could occur when there is inefficiency in delivering services such as slow or late in the delivery of the services, mistakes occurred, and provision of unnecessary treatment (Jacobs: 1997). This study aimed to describe the procedure via an operational audit and to identify cost variance for cases of Chronic Ischemic Heart Disease, Cerebral Infraction, End-stage Renal Disease, and Non-insulin Dependent Diabetes Mellitus without complication among the patients who utilized national health insurance, at PHC Hospital, Surabaya, Indonesia.

METHODS

Study design, time and location

This was a form of economic evaluation study whereby patients with selected diseases were assessed intensively and meticulously about the treatment and procedures received. After this, the cost of the treatment and procedures were determined and compared with the stated social health insurance (BPJS) tariff to see whether there is any cost variation.

Retrospective healthcare utilization data were collected for patients admitted to PHC Hospital, Surabaya,Indonesia. Data from July 2015 to February 2016 was obtained from the social health insurance (BPJS) record. The medical conditions selected for the research were chronic ischemic heart disease, cerebral infarction, end-stage renal disease, and non-insulin dependent diabetes mellitus without complication. The diseases were chosen because they were the common diseases observed with the highest cost variances based on the pre-research conducted in PHC Hospital.

Study population and sampling

The study was conducted among inpatients diagnosed with chronic ischemic heart disease, cerebral infarction, end-stage renal disease, and non-insulin dependent diabetes mellitus without complications at PHC Hospital, Surabaya, Indonesia. A total of 304 records of a patient who were under social health insurance (BPJS) were retrieved between July 2015 and February 2016. A simple random sampling formula by Slovin (1960) was applied to obtain 76 medical records. The distribution of the cases was 23 chronic ischemic heart diseases; 10 cerebral infarction; 33 end-stage renal diseases; and 10 non-insulin dependent diabetes mellitus without complication.

Methods of data collection

A checklist to extract data from the medical records was developed which included the patients’ name, medical record number, the ward type, admission procedure, time of admission, date of admission, time of discharge, date of discharge, length of stay, complications, time of health service, frequency of patient examination, actual cost (Rupiah), and INA-CBGs package (Rupiah). Also, a more detailed cost was obtained from the record of treatment, INA-CBGs Treatment software, and drug prescriptions record from the pharmaceutical unit of the Hospital. Two forms were developed, the first one was a comparison table of the actual cost stipulated from the treatment given and procedures performed, and on INA-CBGs cost, while the other was cost observed for other types of billings (Shumilovskikh et al.: 2019, pp. 513-528).

In-depth interviews (IDI) with the head of functional medicine staff and managers of PHC hospital were also conducted to ascertain whether there are available Clinical Pathways (CP) for the selected diseases, and if so whether the CPs had been followed when treatment was given to the patients. These CPs are considered as the standard practice guidelines that ideally should be followed for efficient management of patients with the diseases.

Type of ward

Two types of the ward were included in this study. Ward 1 consists of rooms with a single bed, while Ward 2 has rooms for shared patients; usually for two patients. The charges of room facilities for Ward 1 are more expensive than Ward 2. Similarly, the charges for treatment and procedures are more in Ward 1 than Ward 2 although the same treatment/procedures applied to patients at both wards.

Data analysis

All the collected data on healthcare utilization for the treatment and procedures and the tariff for the same diseases were tabled in the Microsoft Excel spreadsheet for description and comparison. This study had eased the auditing process (operational audit). The flow of treatment and resources used; including time taken for each step in the management of diseases were analyzed to match the standard practice guidelines such as CPs.

RESULTS

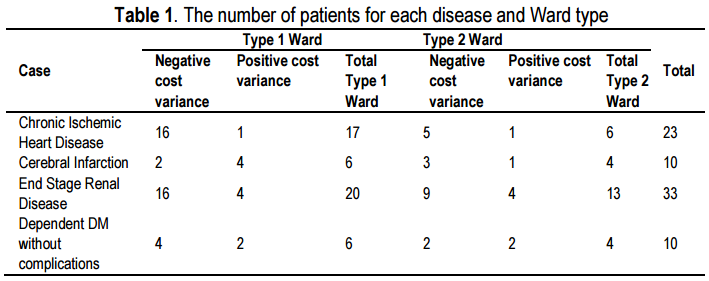

The distribution of patients for various diagnoses and the type of ward they were admitted are as shown in table 1. The table also showed the number of patients according to the type of cost variance.

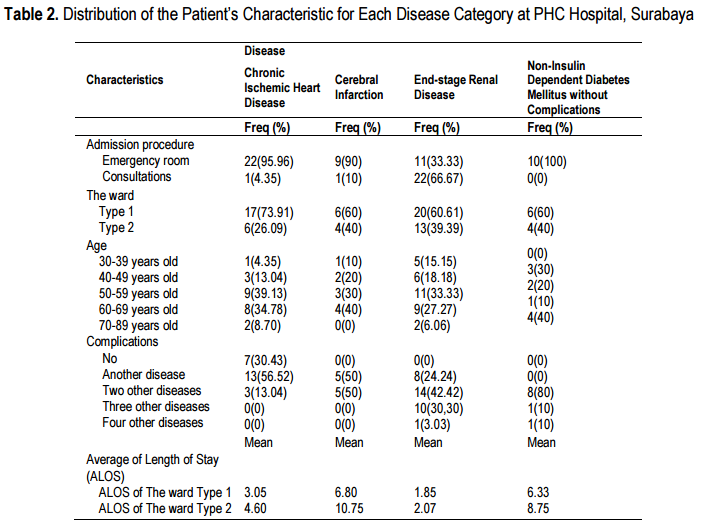

More detail information on the admissions is as shown in Table 2 which depicted that the majority of patients were admitted through the emergency room and had requested to be admitted to Ward 1. The majority of the patients with chronic ischemic heart disease and end-stage renal disease were aged 50-59 years old. As for cerebral infarction, the majority of the patients were from among the 60-69 years old group, while for non-insulin dependent diabetes mellitus without complication, the majority were between 70-89 years old group. Patients from all disease types had two or more co-morbidities. Both admissions to Ward 1 and 2 had the same length of stay (LOS).

Table 2 also compared the actual activities performed to the standard operating procedures (SOP) or CPs. These were the activities provided to patients who were financed by the Social Health Insurance for their admission at the hospital. Most specialists who attended patients with ischemic heart disease had complied with its developed SOP, while the SOP of other diseases had not been complied with.

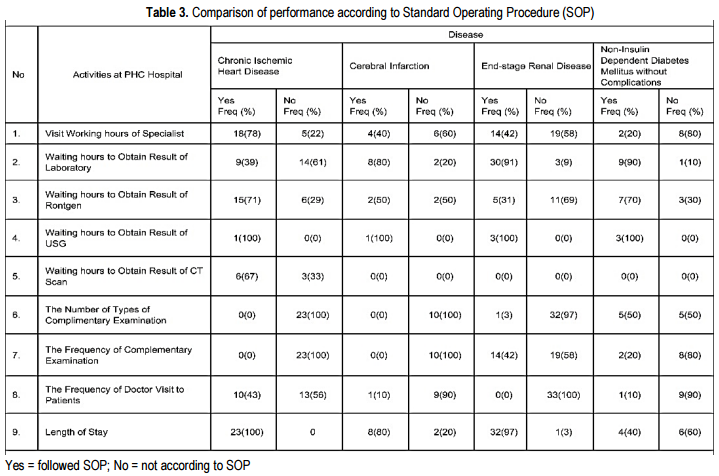

As can be depicted from Table 3, several activities for all disease categories had been performed to a great percentage according to the SOP i.e. waiting hours to obtain the result from laboratory, Rontgen, USG, and CT scan. On the contrary, activities like the number of each complementary examinations and its frequency of performance, and the frequency of doctor’s attending to patients were not following the standard. As compliance to the set LOS, the SOP had been followed by all disease categories, except for non-insulin dependent diabetes mellitus without complications (Ageeva et al.: 2019, pp. 1-14).

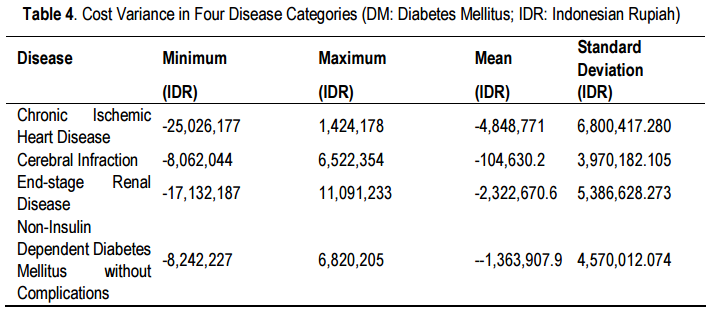

Based on the operational audit conducted, cost variance was observed whereby there were differences between the actual cost and cost decided according to the INA-CBG’s package, for each disease category (Table 4). Negative cost variance means that the actual cost is cheaper than INA-CBG’s package cost, while positive cost variance means that the actual cost is higher than INA-CBG’s package cost. Thus, it was observed that the smallest cost variance was for chronic ischemic heart disease while the biggest cost variance was for end-stage renal disease. The greatest cost variance observed was for cerebral infarction whereby the difference between the actual cost and INA-CDGs package cost was IDR104,630.2.

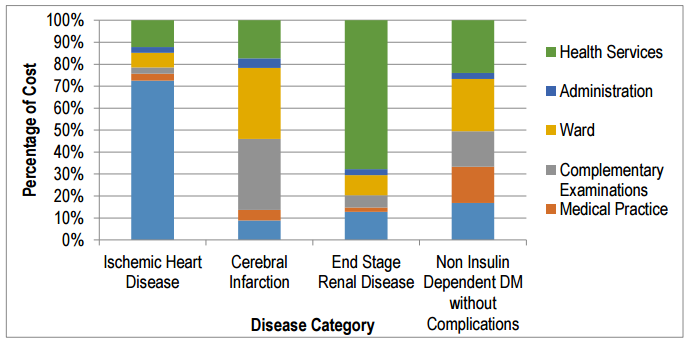

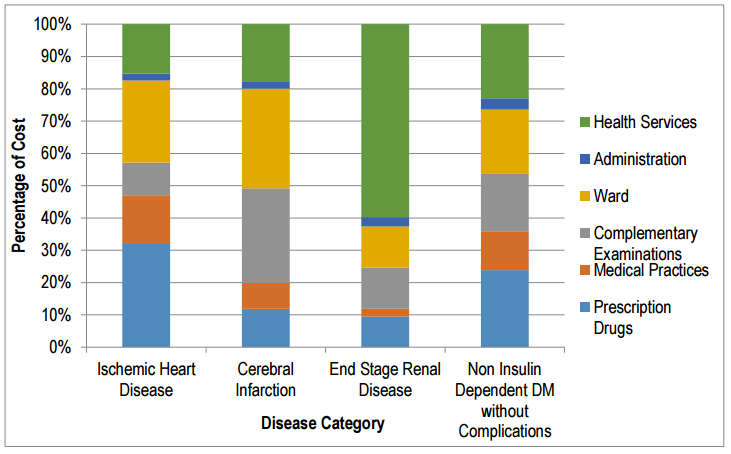

Figure 1 showed the percentage of the cost for the various cost components within each disease category for patients financed by the Social Health Insurance. When cost according to activities was compared between admission to Ward 1 and 2, the biggest difference was seen for the disease category chronic ischemic heart disease; however, in both wards, the dominant cost was for drugs. The percentages of cost for other activities (ward cost, health services, administration, complementary examinations, and medical practice) in both Ward 1 and 2 were fairly similar.

Figure 1. Percentage composition of actual cost in inpatients stayed at Ward 1

Comparing the percentage of the cost for each activity according to disease category, the end-stage renal disease had used a great percentage of the cost for health services in both ward 1 and 2. As for patients with non-insulin dependent diabetes mellitus without complications, the cost was highest for health services and drugs at Ward 1 and Ward 2, respectively.

Observation on whether coding was performed according to INA-CBG; it was revealed that it was not done correctly; meaning that the coding of the diseases in the medical record as written by the specialist was not according to ICD-10. It was observed that the rate of conforming to coding for chronic heart disease was 5.88% and 33.33% at Ward 1 and 2, respectively; for cerebral infarction, it was 25% at Ward 2; end renal stage disease 40% at Ward 1; and non-insulin dependent diabetes mellitus without complications was 50% and 75%, at Ward 1 and 2, respectively.

The government of the Republic of Indonesia had ruled that all hospitals are to abide with the Law No. 44/2009 (Ministry of Law and Human Rights: 2009) which emphasized that hospitals should have sufficient funds if there is no large investment to cover its operational cost and also, they should ensure on its financial sustainability. In struggling to comply with this mandate, since the introduction of social health insurance (BPJS), the participating hospitals are obliged to charge patients according to the tariff as stated for the INA-CBG’s packages. As to upkeep the quality of medical treatment, hospitals are required to follow the agreed standard operating procedures in managing diseases such as the use of clinical pathways.

Clinical pathway aimed to increase the outcome by improving disease management while reducing the cost, so it would give positive impacts for quality health service (Panella & Marchisio: 2013, pp. 509-521; Lee et al.: 2019, pp. 448-456). By complying with CPs, effectiveness and efficiency could be obtained and thus hospitals, in general, would implement this. In this study, many cost variances were identified when the comparison of the cost was made between those paid under INA-CBG’s packages and the actual cost incurred in managing the selected diseases. From the operational audit, those findings were expected because it wasshown that not only inefficiencies in performing certain procedures were detected, but some activities were also found to be ineffective.

Nevertheless, the findings had enabled the hospital in identifying operational problems and thus could take remedial actions to overcome them besides assisting the management to advise on other improvements needed (Boynton, WC et al.: 2001; Mohammadi & Yekta: 2018, pp. 1-7). This operational audit had also given the result of cost performance which showed the difference between earned value or INA-CBG’s package and actual cost (Biafore: 2007; Marmel: 2011).

Operational audit is conducted to assess cost performance and cost monitoring of industry including healthorganization such as a hospital. PHC Hospital is one of the public hospitals in Surabaya. It has a private branch named as the Primasatya Husada Citra Company. The hospital delivers healthcare services for the management of diseases according to agreed clinical pathways to ensure clinical quality and to control the cost of managing diseases. Implementation of operational audit at PHC Hospital, Surabaya was successful because all of the objectives of operational audit (Guy et al.: 2003; Rezaee et al.: 2018) had been met such as assessment of performance, identification of areas for improvement, and recommendations made.

As is stated in the standard operating procedure of hospital and social health insurance, all patients requiring admission are to show their identity card of social health insurance and a reference letter from primary healthcare facility; unless they come through the emergency room whereby they are required to show their social health insurance card. In this study, many of the admissions were through the emergency route was because of the complications of diseases suffered by patients; more severe cases with some in critical conditions that occurred in the late hours (Lawal et al.: 2019, p. 136; Palla et al.: 2018, pp. 206-214).

DISCUSSION

In this the operational audit, the main reason identified for the delay in obtaining laboratory results was the lack of clinical pathologist on call after the office hours. Thus, the delay was expected when the investigations were ordered after office hours, especially during the weekends. This problem was similar for investigations such as Rontgen and CT-Scan.

At PHC hospital, various procedures have set the timing to indicate effectiveness as stated in the Clinicalpathways among which are the number and schedule of complementary examinations, frequency of doctor attending to patients, and length of stay. We observed that all those had not been complied with. Discrepancies occurred in the number and the schedule of complimentary examination and the frequency of doctor attending patients because they were based on the illness condition of patients. Patients who had their check-ups regularly at the hospital, need not be investigated during their short stay at the hospital. Also, patients who had brought their results from outside laboratories need not repeat the investigations upon admission. As for discrepancies in LOS, they depended on the illness condition of patients such as complication, presence of co- morbid, or side effects from drugs.

Besides the above, another possible explanation in the cost variances could be due to the discrepancy of formulary between the Indonesia Neuron Specialist Association and the National Healthcare and Social Security Agency, in which case both agencies had developed their drug formulary. Also, the observed cost variances between actual and INA-CBGs tariff for the same diseases and treatment at the same hospital were due to the costing methods applied in determining the INA-CBGs tariff which applied case-mix while the actual cost was either via activity-based or mixed top-down and bottom-up costing methods. Actual cost was directly affected by LOS and the number of actual investigations performed whereby some investigations would be repeated when some results were not very clear. Besides, special investigations such as the Cath-Lab examination which is needed by patients with ischemic heart disease was not included under the case-mix method.

CONCLUSION

The operational audit was able to explain cost variances that occurred in the delivery of healthcare services to inpatients utilizing the BPJS. Availability and conformance to standard operating procedures such as Clinical Pathways are important to determine an effective and safe clinical care and efficient healthcare service delivery. Nevertheless, variance in the cost of managing some diseases is unavoidable due to the unique characteristics of patients and the difference in costing methods applied in determining the actual cost and health insurance tariff.

BIODATA

Thinni Nurul Rochmah: Dr. Thinni Nurul Rochmah, Dra.Ec., M.Kes. is a Vice Dean II in Faculty of Public Health, Universitas Airlangga Indonesia. She is an author, co-author, and journal reviewer. She has published more than 35 scientific papers and 1 book on Health Services Marketing Management. She was conducted more than 11 fully-funded research. She is expertise in Health Economy and her research interests focus on the field of Health Economy, Health Budgetting and Health Policy and Administration.

Antonius Edwin Sutikno: Antonius Edwin Sutikno, drg., Sp.Pros., M.Kes. is a Head of OPD at National Hospital, Indonesia. He is a dentist and specialist in Prostodonsia. He is Master Student on Health Policy and Administration, Universitas Airlangga, Indonesia. His research focus is on Dentistry and Health Policy and Administration.

Maznah Dahlui: Prof. Dr. Maznah Dahlui, MD., M.PH. Is a Deputy Dean in Department Social and Preventive Medicine of Faculty of Medicine, University of Malaya, Malaysia? She is an author, co-author, and journal reviewer. She has published 50 scientific papers and 3 books on Health Economy. Research Interest focus on the field of Health Economy, Public Health, and Medicine.

Mohammad Bagus Qomaruddin: Dr. Mohammad Bagus Qomaruddin, Drs., M.Sc. is a lecturer in the Department of Health Promotion and Behavioural Science, Universitas Airlangga, Surabaya, Indonesia. He is an author, co-author, and journal reviewer. He has published more than 30 articles on Health Promotion and Behavioural Science. He was conducted more than 4 fully-funded research. He is expertise in Health Promotion and Behaviour Sciences field and his research interests focus on the field of Health Promotion, Community Empowerment, and Sociology of Health.

Runaway: Dr. Ernawaty, drg., M.Kes. Is a lecturer in the Department of Health Policy and Administration, Universitas Airlangga, Indonesia. She is an author, co-author, and journal reviewer. She has published more than 15 scientific papers and 2 books on Health Policy and Administration. She was conducted more than 18 fully-funded research. She is expertise in Primary Health Care, Health Policy, and Health Budgeting. Research interests focus on the field of National Health Insurance, Maternal and Child Health, and Public Health Care.

BIBLIOGRAPHY

AGEEVA, E., FOROUDI, P., MELEWAR, T.C., NGUYEN, B., & DENNIS, C. (2019). “A holistic framework ofcorporate website favourability”, Corporate Reputation Review, pp. 1-14.

BHAYANGKARA, I (2008). "Management Audit: Implementation and Procedure". Salemba Empat, Jakarta.

BIAFORE, B (2007). "Microsoft Project 2007". The Missing Manual. O’Reilly Media Inc.

BOYNTON, WC, JOHNSON, RN & KELL, WG (2001). “Modern Auditing” (7th ed.). John Wiley & Sons Inc, New York.

BUDIARTO, W & SUGIHARTO, M (2013). "INA-CBG's Claim Costs and the Real Cost of Catastrophic Disease Inpatients for Jamkesmas Participants in Study Hospitals at 10 Ministry of Health Owned Hospitals January-March 2012", in Health Systems Research Bulletin, 16(1), p. 7.

GABBY, M (2015). "Principles of Evidence-Based Policy Making in the Context of the Audit Introduction of Health BPJS Operations", in Journal Business, Accounting, and Management, 2(1), pp. 303-304.

GUY, DM, ALDERMAN, CW & WINTERS, A (2003). “Auditing (5th ed.)”. Erlangga, Jakarta.

IFALAHMA, D (2013). "Relationship of Coder Knowledge with Accuracy Code of Diagnosis for Inpatients in Community Health Insurance Based on ICD-10 at Simo Boyolali District Hospital", in Scientific Journal of Medical Records and Health Informatics, 3(2) pp. 15-18.

JACOBS, P (1997) The Economics of Health and Medical Care (4th ed.). Aspen Publisher, Maryland.

KNECHEL, WR, & SALTERIO, SE (2016). “Auditing: Assurance and risk”. Routledge.

LAWAL, AK, GROOT, G, GOODRIDGE, D, SCOTT, S & KINSMAN, L (2019). “Development of a program theoryfor clinical pathways in hospitals: protocol for a realist review”. Systematic reviews, 8(1), p. 136.

LEE, X. J, BLTTHE, R, CHOUDHURY, AAK, SIMMONS, T, GRAVES, N & KULARATNA S (2019). “Review ofmethods and study designs of evaluations related to clinical pathways”. Australian Health Review, 43(4), pp. 448- 456.

MARMEL, E (2011). “Microsoft Project 2007 Bible” (Vol. 767). John Wiley & Sons.

MINISTRY OF HEALTH OF REPUBLIC OF INDONESIA (2014a). Ministerial Regulation of Health of Republic of Indonesia No. 27/2014 about Technical Guidance of INA-CBGs System. Ministry of Health of the Republic of Indonesia, Jakarta.

MINISTRY OF HEALTH OF REPUBLIC OF INDONESIA (2014b). Regulation of Ministry of Health of Republic of Indonesia No. 59/2014 about Tariff Standard of National Health Insurance (2014). Ministry of Health of the Republic of Indonesia, Jakarta.

MINISTRY OF LAW AND HUMAN RIGHTS (2009). Law No. 44 the Year 2009 about Hospital. Ministry of Law of the Republic of Indonesia, Jakarta.

MOHAMMADI, S, & YEKTA, P, (2018). “The Effect of Emotional Intelligence on Job Satisfaction among Stuff Nurses in Intensive Care Units”. UCT Journal of Social Sciences and Humanities Research, 6(2), pp. 1-7

NATIONAL TEAM FOR THE ACCELERATION OF POVERTY REDUCTION (2015). The Road to National HealthInsurance. Anc, Jakarta.

PALLA, G, PALL, N, HORVAT, A, MOLNAR, K, TOTH, B, KOVATS, T ... & POLLNER, P (2018). “Complex clinicalpathways of autoimmune disease”. Journal of Complex Networks, 6(2), pp. 206-214.

PANELLA, M, MARCHISIO, S (2013). "Reducing clinical variations with clinical pathways: do pathways work?” in International Journal for Quality in Health Care, 15(6), pp. 509-521.

REZAEE, Z, SHARBATOGHLIE, A., ELAM, R & MCMICKLE, PL (2018). “Continuous Auditing: Building Automated Auditing Capability1”. Continuous Auditing: Theory and Application, 169.

SHUMILOVSKIKH, L. S., RODINKOVA, V. Y., RODIONOVA, A., TROSHINA, A., ERSHOVA, E., NOVENKO, E., ...& SCHNEEWEIß, J. (2019). “Insights into the late Holocene vegetation history of the East European forest-steppe: case study Sudzha (Kursk region, Russia)”, Vegetation History and Archaeobotany, 28(5), pp. 513-528.

SYAH, TYR, NUROHIM, A, & Hadi, DS (2019). “Lean Six Sigma Concept in The Health Service Process in The Universal Health Coverage of BPJS Healthcare (Healthcare and Social Security Agency)”. Proceeding UII- ICABE, 1(1), pp. 71-88.