Artículos

Islamic micro-financing schemes among financial institutions

Esquemas islámicos de microfinanciación entre las instituciones financieras

M.H Warsame mhwarsame5@hotmail.com

M.H Warsame mhwarsame5@hotmail.com

Islamic micro-financing schemes among financial institutions

Utopía y Praxis Latinoamericana, vol. 25, no. Esp.2, pp. 223-232, 2020

Universidad del Zulia

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 3.0 International.

Received: 22 March 2020

Accepted: 30 April 2020

Abstract: The present study aims to identify the importance of Islamic micro-financing schemes among the financial institutions and also determine the knowledge and attitudes of the respondents towards Shari’ah based financial products. A mixed-method approach, including quantitative and qualitative designs, has been employed by recruiting 255 and 15 respondents, respectively. The results showed no significant differences between respondents’ knowledge and access to Shari’a-compliant finance. Similarly, there were no significant differences between respondents depending on their length of stay in the UK, ethnicity, and employment status. Moreover, this required financial support and empowerment from the government and related institutions.

Keywords: Conventional banking, financial institution, islamic provisions, muslims..

Resumen: El presente estudio tiene como objetivo identificar la importancia de los esquemas de microfinanciación islámicos entre las instituciones financieras y determinar el conocimiento y las actitudes de los encuestados hacia los productos financieros basados en la Sharia. Se ha empleado un enfoque de método mixto que incluye diseños cuantitativos y cualitativos, reclutando de 255 empleadoos, 15 encuestados. Los resultados no mostraron diferencias significativas entre el conocimiento de los encuestados y el acceso a las finanzas que cumplen con Sharia. Del mismo modo, no hubo diferencias significativas entre los encuestados en función de la duración de su estadía en el Reino Unido, el origen étnico y la situación laboral. Además, esto requería el apoyo financiero del gobierno.

Palabras clave: Banca convencional, disposiciones islámicas, institución financiera, musulmanes.

INTRODUCTION

Islamic microfinance is seemed to be a new borderline, which is keenly observed by many practitioners, academics, and observers (Tamanni et al.: 2014). The Islamic and conventional microfinance banking provides a wide range of products to the disadvantaged community across the world (Nazirwan: 2015, p. 273). Both of the concepts of microfinance are accepted globally as they contribute to pulling an adverse population by enabling them to earn by getting the small capital from the microfinance institutions (Berguiga et al.: 2017). The traditional methods of financing in Islam are considered unsuitable as they charge interest that is forbidden in the financial laws of Shari’ah. This led to the trend of Islamic microfinance banking for Muslims to use financial services (Cross: 2015). Poverty is a crucial issue in the Muslim community; therefore, the Muslim community has come up with the Islamic microfinance (Nazirwan: 2015, p. 273). This provided a good opportunity for the people with lower strata communities to get an alternative and valuable source of gaining capital instead of counting on the other commercial banks (Riwajanti & Asutay: 2015, pp.1-55; Zamora-Lobato et al.: 2017, pp.133-143).

Islamic finance banking has revolutionized finance banking by providing an ethical, moral, and spiritual aspect to it (Kamruzzaman & Islam: 2015, pp.1-17). Furthermore, the Islamic finance banking has brought the millions of poor Muslims under the umbrella of earning according to the Shari’ah law, which will help them in coming out of the fence of paying interest (Ilieva et al.: 2017). Islamic finance banking is growing and changing day by day, and it is celebrated as a favorable financial industry for Muslims around the globe. Furthermore, its assets have increased to $400 billion, and the market value is being predicted to be increasing at 10-15% per annum (Dhaoui: 2015, pp.1-19; Silva et al.: 2016, pp.123-140).

The Islamic banking sector seems to be dominant in the Islamic finance industry. It has increased by greatmeans in the past two decades and collected $1.9 trillion in the form of assets prevailing across the Muslim and non-Muslim regions around the globe (Aydin & Iqbal: 2018, pp.174-196). Furthermore, Islamic microfinance is a key element for economic growth and development for most of the communities as its key objective is to increase human resources (Dhaoui: 2015, pp.1-19). Financers have predicted that this development will provide encouragement for economic growth by minimizing poverty and unemployment rate among the youth. This will result in the augmentation of social and economic capacity offered by the entrepreneurial with the moral and Islamic values (Ali: 2015, pp.313-326). However, the debates are initiated on the topic of interest charge by saying that if the interest is removed, then there will not be anything to provide balance in the demand and supply in the economy (Dhaoui: 2015, pp.1-19).

The Islamic idea in finance banking has influenced the microenterprises by giving financial and non- financial guidance and the commitment to the principles of cooperation, transparency, and understanding (Islam & Alam: 2016, pp.1-9). However, the funds provided to the Islamic microfinance are contributed by Islamic institutions such as Awqaf, Qard-Hasan, Zakat, Sadaqat, and other forms of charity (Avais: 2014, pp.2250-3153; Luo et al.: 2018, pp.1-8; Belentsov et al.: 2019, pp. 201-207).

The study is significant as it reveals the impact of Islamic microfinance banking that can be discussed onthe economic as well as a social basis. The providence of financial facilities to the disadvantaged community will allow them to grow their economic wellbeing, reduce the problems, and become a part of the development. Furthermore, this will let them increase their earning. On the economic impact, the latest empirical study has been conducted by Islamic Bank Bangladesh Limited, revealing an improvement in household income by providing loans to the people. The present study aims to identify the importance of Islamic micro-financing schemes among financial institutions. The study has also depicted the knowledge and attitudes of the respondents towards Shari’ah based financial products.

METHODS

Study Design

The present study has employed a mixed-methods approach, including the qualitative and quantitative designs, to identify the significance of Islamic micro-financing schemes among the financial institutions. The study has analyzed the attitudes, experiences, and opinions of the UK Muslims towards Shari’ah based financial products through semi-structured interviews and survey questionnaires based on the Likert scale.

Study Participants

The study has recruited the UK based Muslims from different ethnicities. The researcher decided some key places to select the target sample, such as mosques, shops, and restaurants serving halal food, Muslim community organization, and the streets Muslims living in. Probability sampling, specifically judgmental and convenience sampling techniques, were used in this study to recruit respondents. The sample size selected for quantitative analysis was 255. For the qualitative analysis, 15 individuals were recruited from the sample of 255 individuals, who were customers of commercial banks, including the private Banks, Government Banks, and customers of Foreign Banks.

Data Collection

The primary data was collected through the questionnaires, firstly the responses were included in the questionnaire and allowed the amendments in it. Then a random sample was selected and provided them with the amended questionnaires. However, the comments raised by the interviewees were notified, and the response from this group was again incorporated in the questionnaire, and this is how the final version was generated to collect the data.

For the qualitative analysis (thematic analysis), the data from the respondents was collected through semi-structured interviews that comprised of open-ended questions. The questionnaires were administrated personally in commercial Banks (Private Banks, Government Banks, and Foreign Banks). The main aim of the questionnaire was to explore the perception of customers regarding the banking industry, product quality, service quality, attitude of staff towards the customer, pricing factor, and perception of customer regarding the Bankers. The questionnaire consisted of 10 different questions to examine the people’s understanding and perception towards microfinance services.

Data Analysis

The data gathered through the questionnaire was entered in the SPSS software for the final analysis and the statistical analysis of the data was carried out as descriptive statistical analysis based on percentages and frequencies (Asylgaraeva et al.: 2019, pp. 84-103).

The respondents recruited for qualitative analysis were requested to give their opinions regarding the efficiency of Islamic microfinance programs in UK, in terms of planning, outreach and operation, and impact on the economy. The responses obtained from the respondents drew a clear picture of what were the perceptions of respondents about a bank and what were the realities. Moreover, the responses have been evaluated by making themes and explaining the views of each respondent regarding product quality, service quality and pricing factor, attitude of staff towards customer, and perception of customer regarding bankers. A thematic analysis approach has been used to analyze the data collected from participants.

RESULTS

Quantitative Analysis

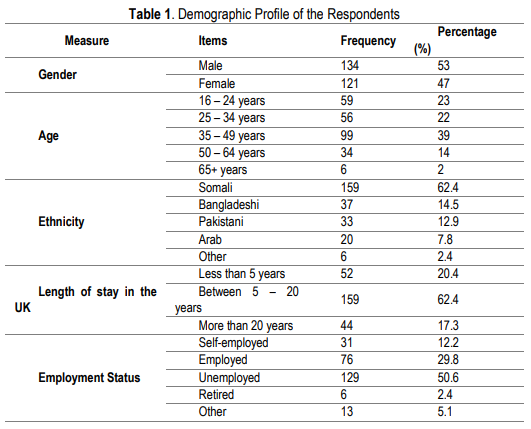

In the first step of conducting quantitative analysis, the study presented general characteristics of sample respondents, who participated in the survey. Table 1 has shown the demographic profile of the respondents.

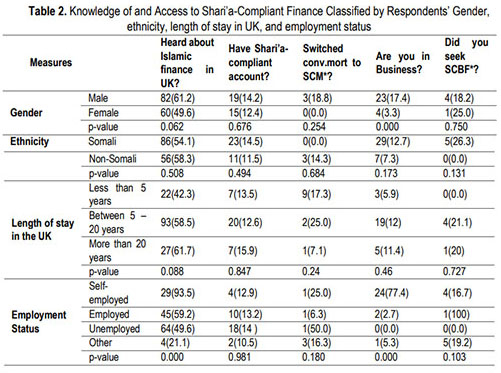

It is evident that the less affluent UK Muslims do not access the available Shari’a-compliant financial products to the extent that is expected. The knowledge and access to Shari’a-compliant finance based on their gender, ethnicity, length of stay in UK, and employment status has been presented in Table 2. Table 2 has shown that there were no significant differences between respondents’ knowledge and access to Shari’a- compliant finance. However, there was exception in business where males seem to be enterprising as compared to their female counterparts. As far as ethnicity was concerned, there were no significant differences between respondents. Similarly, there were no significant differences between respondents depending on their length of stay in UK and employment status.

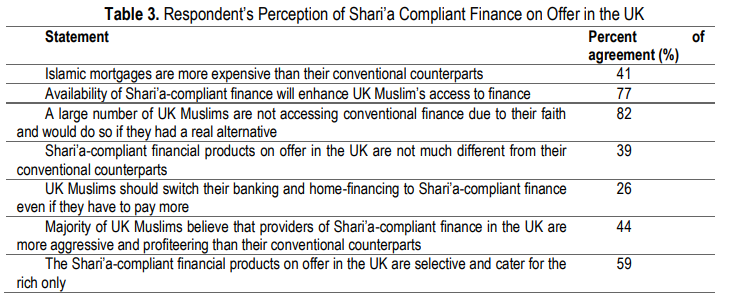

Table 3 has presented the analysis of less affluent perceptions of UK Muslims regarding the Shari’a- compliant financial products.

Qualitative Analysis

In the second part, the results of the present study are based on the interview analysis given by the customers of commercial banks including the private Banks, Government Banks and customers of Foreign Banks. The respondents had poor prospects and potential markers having conventional banking mindsets. However, they need financial support and empowerment from the government and related institutions.

Knowledge about Shari’a-compliant financial products

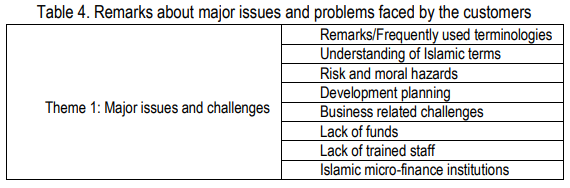

Table 4 has shown the common remarks, words, or statements stated by the respondents, when they were asked about the major issues and challenges faced in the implementation of Islamic micro-financing schemes among the financial institutions. Some of the interviewees stated that they had to face great challenges in the market, despite of increased proportion of Muslim communities. One of the respondents stated that;

‘The communities having conventional banking mindset have a poor level of understanding regarding the Shari’ah terms’

The results based on the information provided by the interviewees have depicted that recently conventional and Shari’ah commercial banking are offering micro-financing. In this context, one of the respondents stated that;

‘Offering micro-finance helps in the constitution of potential contributor as all the banks tend to offer same services within a similar marketplace’

Generally, majority of the respondents believed that micro-enterprises have potential prospects but they require financial support. They stated that their potential would not be neglected if the government and related financial institutions take real actions towards the empowerment of micro-enterprises. According to one of the respondents;

‘Display of unconstructive characteristics to manage funds is a great challenge and some of the customersmisuse the funds that they obtained from financing and other businesses’

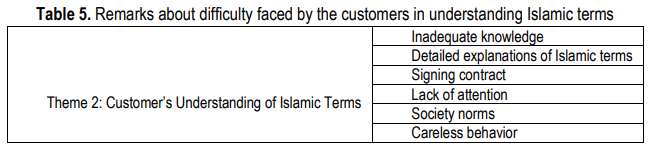

Customer’s Understanding of Islamic Terms

The responses obtained from the respondents regarding the understanding of Islamic terms depicted that more than half of the customers were not able to understand the Islamic terms that are used in the financing products. However, they themselves had claimed that they were made aware of the Islamic terms before signing the contract. One of the respondents stated that;

‘Majority of the customers have lower understanding about Islamic terms because may be the officer have higher expectations in this matter’

The analysis has shown that some of the customers started to understand the Islamic terms after they had received detailed information; although, in the start they had difficulty in understanding Islamic terms. This clearly shows that customers need more education and information about the Islamic terms. In this context, one of the respondents narrated that;

‘It becomes difficult to explain the Islamic terms to the customers when they do not care about the termsthemselves and are not focused towards their understanding’

The customers find difficulty in understanding the Islamic terms as these terms are not used commonly in daily routine life. Some of the customers had come across those terms, when they first contacted the Islamic microfinance institutions. Table 5 has depicted the terms frequently used by the customers to show the difficulty they face in understanding the Islamic terms. One of the respondents stated that;

‘I had developed understanding the terms of account that I hold myself but I believe that the new customers find difficulty in understanding’

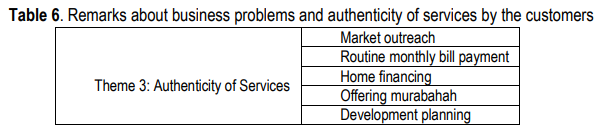

Development of Authentic Products

The analysis has also explored the factors leading to the development of customers’ businesses to come out with authentic products. In this aspect, market outreach is considered as an important factor in the development planning. Other factors include; increase of capital, improved skills, and sustainability. The local needs of the customers are fulfilled through the development of authentic products. In this aspect, one of the respondents stated that;

‘I have considered to offer new products and I do that willingly. However, I also believe that banks need to have employees with assessment certificates to obtain authorization’

The routine bill payment has been considered among the authentic services in which the financialinstitution pays the whole amount to the bank and the customer repays the amount throughout the year. The general terms used by the respondents in explaining the business problems and authenticity of services have been depicted in table 6. One of the respondents reported that;

‘I prefer and hope to provide mudharabah among the services provided, because I have thus far only offered murabahah’

DISCUSSION

The study has presented the knowledge, awareness, and understanding of UK Muslims about Islamic micro-financing schemes among the financial institutions. Financial illiteracy is among the major causes of the low demand for Islamic financial products because the access to Shari’a-compliant financial products requires some basic understanding of finance in general. There is also a need of appreciation of the distinguishing features of Shari’a-compliant financial products along with the underlying doctrine of Islamic economics. Majority of the UK financial institutions are interest-based. These institutions have perceived materialistic approach. Moreover, there is a huge expectation gap between what less affluent UK Muslims expect from the providers of Islamic financial products in the UK, and what is actually they are offered.

A similar study conducted by Roberts (2013) stated that the microfinance institutions charge highereffective rates by displaying stronger profit orientations as they operate at higher costs. These results were supported by another study conducted by Mohammed and Hasan (2008), as they revealed that while saving schemes, the microfinance institutions charged as high as 100% of their credit schemes from their clients. It has been shown that some of the institutions take extra funds for covering their operational costs that is presented in the form of re-investments, government assistance, or an international political community (Sandberg, 2012). However, the main aim of these institutions should be reduction of poverty, employment creation, empowerment, and development of successful businesses.

The present study has shown that the prospects and potential markers among the respondents were not satisfactory having conventional banking mindsets. Moreover, they need financial support and empowerment from the government and related institutions. A similar study conducted by Kempson, Atkinson and Pilley (2004) showed that majority of the building societies moved to retail banking through mergers and takeovers, when the traditional distinction between banks and building societies was removed by the re-regulation of financial services. This clearly shows that certain services have been enhanced by technological advancement and the level of accessibility; although, all the intense efforts and the significant progress made in this endeavour.

It is also evident that the Muslim community is financially excluded due to their religious beliefs; however, certain social groups choose to stay away from accessing the mainstream financial services. The study has presented the UK financial system, including Shari’a-compliant finance that caters the financial needs of less affluent UK Muslim communities. These communities represent a significant proportion of the overall UK population and the extent of their financial exclusion. A similar study conducted by Cole and Robinson (2003) showed that there is much variation in the level of financial exclusion among less affluent UK Muslim communities.

CONCLUSION

The present study has helped in identifying the knowledge and attitudes of the respondents towards Shari’ah based financial products through quantitative and qualitative analysis. The results have clearly showed that the conventional UK financial system does not meet the financial services needs of less affluent UK Muslims. Due to lack of trust in the formal financial system, the less affluent UK Muslims tend to employ more informal financial services. The study results have concluded that in the current state the Shari’a- compliant financial products do not meet the financial services needs of middle-class UK Muslims. Moreover, it also lacks certain appropriate products that hinders their financial inclusiveness, enormously.

ACKNOWLEDGEMENTS

The author is very thankful to all the associated personnel in any reference that contributed in/for the purpose of this research. Further, this research holds no conflict of interest and is not funded through any source.

BIODATA

M WARSAME: Mohammed Warsame received his Ph.D.in Banking and Finance from Durham University. (UK). Dr.Warsame also holds two prestigious professional qualifications, namely, ACCA (Chartered Certified Accountant) and CIPA (Certified Islamic Professional Accountant). Dr. Warsame is currently a faculty member and the former chairman of Finance and Economics Department at the University,

BIBLIOGRAPHY

ALI, A (2015). “Islamic microfinance: Moving beyond financial inclusion.” European Scientific Journal, ESJ, 11(10), pp.313-326.

ASYLGARAEVA, G., NURETDINOVA, A., CHIZHEVSKY, A., & ANTIPINA, E (2019). “Collections of thearchaeological museum of Kazan (Volga Region) Federal University. Part 2”, Povolzhskaya Arkheologiya, 1(27), pp. 84-103.

AVAIS, M (2014). “Financial Innovation and Poverty Reduction.” International Journal of Scientific and Research Publications, 4(1), pp.2250-3153.

AYDIN, A, IQBAL, Z (2018). “Islamic Finance Approach to Financial Inclusion to Enhance Shared-Prosperity.” Financial Inclusion for Poverty Alleviation, 174(196), pp.174-196.

BELENTSOV, S. I., FAHRUTDINOVA, A. V., GREVTSEVA, G. Y., & BATRACHENKO, E. A. (2019). “FreeEducation: Fundamentals of Humanistic Pedagogics (On the Example of Activity of the German Public Figures of the Second Half of XIX--The Beginning of the XX Centuries of F. Gansberg, L. Gurlitt, G. Sharrelman)”, European Journal of Contemporary Education, 8(1), pp. 201-207.

BERGUIGA, I, SAID, Y, & ADAIR, P (2017). The social and financial performance of Microfinance institutions in the MENA region: Do Islamic institutions perform better?. In 34th Spring International Conference, French Finance Association (AFFI).

COLE, I, & ROBINSON, D (2003). Somali housing experiences in England. Sheffield: UK, Centre for Regional Economic and Social Research, Sheffield Hallam University Press.

CROSS, A (2015). “The Viability of Islamic Microfinance: Financial Sustainability and Outreach Capabilities of Firms in the Middle East and North Africa.” (Retrieved on 2018/02/03) from: https://pdfs.semanticscholar.org/19bf/f651f169581fbc724603d24f8ea47f412548.pdf

DHAOUI, E (2015). “The role of Islamic Microfinance in Poverty Alleviation: Lessons from Bangladesh Experience.” Tunisan Institute for Competitiveness and Quantitative Studies Journal. 1, pp.1-19.

ILIEVA, J, RISTOVSKA, N, KOZUHAROV, S (2017). “Banking Without Interest.” (Retrieved on 2018/04/07) from: http://www.utmsjoe.mk/files/Vol.%208%20No.%202/UTMSJOE-2017-0802-07-Ilieva-Ristovska- Kozuharov.pdf

ISLAM, M, ALAM, M (2016). “Can Islamic micro-finance alleviate poverty? A case study from south-eastern Bangladesh.” Journal of Islamic Economics and Finance (JIEF), 2(2), pp.1-9.

KAMRUZZAMAN, M, & ISLAM, R (2015). “Evolution of Islamic Banking and Its Salient Features: An Overview.” Journal of Business and Economics, 8(1), pp.1-17.

KEMPSON, E, ATKINSON, A, PILLEY, O (2004). “Policy level response to financial exclusion in developed economies: lessons for developing countries.” Report of Personal Finance Research Centre, Bristol: UK, University of Bristol Publication.

LUO, C, LI, M, PENG, P, FAN, S (2018). “How Does Internet Finance Influence the Interest Rate? Evidence from Chinese Financial Markets.” Dutch Journal of Finance and Management, 2(1), pp.1-8.

MHAMMED, A, HASAN, Z (2008). “Microfinance in Nigeria and the prospects of introducing its Islamic version there in the light of selected Muslim countries' experience.” International Islamic University Malaysia Journal, 1, pp.1-19.

NAZIRWAN, M (2015). “The dynamic role and performance of Baitul Maal Wat Tamwil: Islamic community- based microfinance in Central Java.” Doctoral dissertation, Indonesia, Victoria University. p.273

RIWAJANTI, N, ASUTAY, M (2015). “The role of Islamic micro-finance institutions in economic development in Indonesia: A comparative analytical empirical study on pre-and post-financing states.” Access to Finance and Human Development—Essays on Zakah, Awqaf and Microfinance, 1, pp.1-55.

ROBERTS, P (2013). “The profit orientation of microfinance institutions and effective interest rates.” World Development Journal, 41, pp.120-131.

SANDBERG, J (2012). “Mega‐interest on Microcredit: Are Lenders Exploiting the Poor?.” Journal of Applied Philosophy, 29(3), pp.169-185.

SILVA, J, TEIXEIRA, C, PINTO, J (2016). “Banking desmaterialization using cloud computing.” Journal of Information Systems Engineering and Management, 1(2), pp.123-140.

TAMANNI, L, NABI, M. S. & ZOUARI, Z. (2014). “Islamic Microfinance.” (Retrieved on 2018/07/03) from: https://www.researchgate.net/publication/281032665_Islamic_Microfinance.

ZAMORA-LOBATO, T, GARCIA-SANTILLAN, A, MORENO-GARCÍA, E, LOPEZ-MORALES, J, RAMOS-HERNANDEZ, J (2017). “High School Students and their Perception of Financial Institutions: An Empirical Study in Xalapa, Veracruz.” International Electronic Journal of Mathematics Education, 12(2), pp.133-143.