Artículos

Effect of good village governance implementation in Indonesia

Efecto de la implementación de la buena gobernanza de las aldeas en Indonesia

D.A munir donyahmadmunir@gmail.com

S Mulyani sri.mulyani@unpad.ac.id

B Akbar bahrullah.akbar@unpad.ac.id

D.A munir yosephmm@yahoo.co.id

D.A munir donyahmadmunir@gmail.com

S Mulyani sri.mulyani@unpad.ac.id

B Akbar bahrullah.akbar@unpad.ac.id

D.A munir yosephmm@yahoo.co.id

Effect of good village governance implementation in Indonesia

Utopía y Praxis Latinoamericana, vol. 25, no. Esp.2, pp. 233-243, 2020

Universidad del Zulia

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 3.0 International.

Received: 22 March 2020

Accepted: 30 April 2020

Abstract: This study aims to examine the effect of the implementation of good village governance in Indonesia, its competence and performance, based on the level of fraud and its fund management. Data was collected by conducting a survey of 1,080 management-level respondents in village government. The results found that the poor implementation of the good village governance reveal a high level of fraud in the management of funds. This condition was reflected in the lack of equitable development and the failure to alleviate poverty.

Keywords: Competence, good village governance, Indonesia, Level of fraud, Performance..

Resumen: Este estudio tiene como objetivo examinar el efecto de la implementación de la buena gobernanza de las aldeas en Indonesia, su competencia y desempeño, basado en el nivel de fraude y su gestión de fondos. Los datos se recopilaron mediante la realización de una encuesta a 1.080 encuestados a nivel gerencial en el gobierno de las aldeas. Los resultados encontraron que la baja implementación de la buena gobernanza revelan un alto nivel de fraude en la gestión de fondos. Esta condición se reflejó en la falta de desarrollo equitativo y el fracaso en el alivio de la pobreza.

Palabras clave: Buen gobierno de las aldeas, competencia, indonesia, nivel de fraude, desempeño..

INTRODUCTION

The government of Indonesia issued Law No. 6 of 2014 about villages, aiming to advance the economy of rural communities and overcome national development gaps by strengthening such locales as the subject of development. To reach the goals, the government began to distribute village funds in 2015 to 74,954 villages throughout Indonesia. The number of village funds allocated in 2015 was IDR. forty billion while it was IDR. 70 billion in 2019. A significant increase in the distribution number of funds requires the village government to implement high performance. Such performance should be reflected as a value that can be created by an organization using productive assets compared to the amount expected by capital owners. Verweire and Van (2004) stated that performance issues are crucial because of various influencing factors, such as governance and employee competence. Also, the findings from Lane, (2010) revealed that oversight is the primary factor leading to low performance in the public sector. Furthermore, Cohen and Sayag (2004) argued that one cause of fraud and accounting problem is the weakness of corporate governance. The corporate governance as a hard structure emphasizes a soft structure as a support mechanism for corporate governance in the form of compliance with laws and regulations and role of regulators in public institutions, Lukviarman (2016). Regulations concerning the implementation of good village governance are stated in UU No 28 Tahun 1999. It mentions that the implementation of public services must be carried out thoroughly, full of responsibility, effectively, efficiently, free from corruption, collusion, and nepotism. Fraud in governance will lead to low performance (Dechow et al.: 1996, pp. 1-36; Beasley et al.: 2000, pp. 441-467; Komekbayeva et al.: 2016, pp. 2227-2237).

Hitt et al. (2009) defined competence as a combination of knowledge, skills, attitudes, and experience.

Similarly, Yukl, (2010), Steward and Brown (2011), and Moeller (2014) posited that human resource competencies consist of knowledge, skills, and abilities. Knowledge is a combination of previous experiences, insights, and data, forming an organized memory (Zikmud et al.: 2010). Besides knowledge, skills are necessary to drive improvement in crucial processes (Atkinson & Wilson: 2012, pp. 1-12). The skills that an individual has can be in the form of conceptual skills, interpersonal skills, and technical skills (Daft: 2010, p.12). Furthermore, the ability is a person's capacity to complete the tasks he in charge of by utilizing intellectual skills and physical abilities (Robbins: 2007, p.54). Also, Mulyani and Fettry (2016) found that competent resources can reduce the level of fraud in a company. This research is highly essential since it provides empirical evidence of the village fund program level of success by examining the occurrence of fraud. The findings of this study can also be utilized as a material for evaluation and development of future village fund programs.

LITERATURE REVIEW

Implementation of good village governance

Neumayer (2003) defined governance as a government which respects political and citizens' rights by law, provides practical and non-corrupt public services, and utilizes public resources accountably and transparently. Its main goal is social welfare. Also, according to Stoker (2008), governance is a set of new managerial aids which enables the government to be efficient in providing services to the public. To measure the implementation of good village governance, this study used a dimension developed by Jinarat and Quang, (2003), Hout, (2007), Umar (2006), and UU No 28 Tahun 1999, namely accountability and transparency.

The competence of village apparatus

Competency is knowledge (education, expertise, and experience) and work ethic (Cheng & Tsan-Ming: 2010). According to Steward and Brown (2011), competence is a collection of productive elements, expertise, and skills in an organization to reflect itself differently from competitors. Furthermore, Steward andBrown (2011) posited that competence could be symbolized as an ability to perform. However, Moeller (2014) argued that an organization should determine the competence level needed for various tasks as well as specify these needs at a level requiring knowledge and skills. In this study, the competence of village apparatus was measured by a dimension developed by Spencer and Spencer (1993), Daft (2010), Sanchez, Klot and Spincer (1997), they are knowledge, experience, and attitude.

Fraud in village fund management

Arens et al. (2014) stated that fraud is a deliberate act to deceive, a trick, or a dishonest way to take or remove money, property, legitimate property rights of others due to any action or fatal impact from such action. Fraud is divided into two types, financial report fraud and misuse of assets. The level of fraud can be identified by dimensions of financial statement fraud, fraud on assets (asset misappropriation), and financial fraud (Singleton & Singleton: 2010; Selomo & Govender: 2016, pp.1-10; Asylgaraeva & Bocharov: 2019, pp. 208- 228).

Village government performance

Performance is a description of achievement in conducting an activity/ program/ policy to attain targets, objectives, visions of an organization as writing in its strategic plan Mahsun (2006). Meanwhile, Verweire and Van (2004) defined performance as a value in the size of money created by the organization using productive assets compared to the value expected by capital owners. Consequently, financial information should be able to provide various details on organization or company. Business performance measurement can be divided into two main types of accounting data and market-based data derived from the stock market value. In this study, performance variables of village government were measured by dimensions developed by Mardiasmo (2009) and Lusthaus et al. (2002), they are economical, efficient, and effective.

METHODS

The use of information systems in implementing good village governance can lower the fraud level (Mulyani et al., 2019). Omar and Katerine (2011) studied manufacturing companies in Malaysia and found that the implementation of corporate governance is characterized by the presence of external auditors, internal auditors, a board of directors, audit committee, and anti-fraud specialists who can lower fraud in the company. It is in line with the research findings by Magnanelli (2010), revealing that corporate governance can reduce the fraud level. Similarly, Agrawal and Chadha (2005) found that governance mechanisms are strictly related to companies’ possibility of conducting restatement regarding corporate income report. Furthermore, research by Laws (2011) using an analysis unit of manufacturing companies in the U.S., revealed that good governance mechanisms practice by the company is negatively related to its fraud level. Based on this fact, the first hypothesis was formulated:

The implementation of good village governance (GGG) can reduce fraud in village funds (FR)

The findings of Cohen and Sayag (2012) showed that when managers apply professional standards and possess high integrity towards the company, fraud can be reduced. It is in line with the finding of Smith and Politowski (2008), which stated that management competence is reflected in commitment and actions related to risk management to prevent fraud practices. Similarly, Morgan (2007) posited that employee competency has a positive effect on performance and design quality. Besides, competence can decrease various weaknesses, such as fraud and cheating practices in the company. Thomas and Gibson (2003) stated that tone at the top through the development of competent employees plays an active role in preventing fraud on the organization by ensuring all of its members implement the value system within company. Baloyi (2005) found that internal auditor capability is one of the tools in the scheme to prevent and detect employee fraud.

Furthermore, employee competence in utilizing information technology is proven to be able to reduce fraud (Supriadi et al.: 2019, pp.1-13; Abreu et al.: 2016, pp.111-121). Based on this fact, the next hypothesis was established:

Competence of village apparatus (AC) has a negative effect on fraud level in village funds (FR)

Agrawal and Chadha (2005) found that companies committed fraud generally have a high level of manager turnover. It is hoped that the company can escape the crisis immediately due to its deteriorating performance. It was also revealed that fraud had a negative effect on performance in companies in Ghana. Furthermore, research by Lane (2010) showed that the lack of competence and effectiveness of internal control carried out by the company's internal audit indicate a variety of fraud leading to its low performance. Studies on banks and financial institutions in India, found that fraud at banks and such institutions was due to their ineffectiveness in applying due diligence and the lack of professionalism among its executives. Based on this fact, the third hypothesis was formulated:

The level of fraud in village funds (FR) negatively affects the performance of village governance (PR)

Implementation of good village governance has a positive impact on village governance performance (Uskara et al.: 2019). Lockwood (2010) found that the principles of good village governance are closely related to high performance. Research of Bhagat and Bolton (2008) showed that good governance has a positive effect on future stock market performance. Meanwhile, Sanusi (2015) who studied oil and gas companies in Indonesia also found the same results. His findings revealed that the implementation of good governance has a positive effect on company performance. Likewise, Mousa et al., (2012) depicted that there is a positive relationship between corporate governance and organizational performance. Based on this fact, the fourthhypothesis was designed:

The implementation of good village governance (GGG) will improve the performance of village governance (PR)

Wang and Kuo (2010) found that staff development through the decision support system can provide the latest and timely information regarding assets and financial obligations in each company. Hence, it will support the decision-makers in funding. A similar sentiment was also conveyed by Mahmood (2007) that the implementation of total quality management requires a thorough transformation in organizational operations. Such an application can only be attained by providing qualified employees in the company. Management should place competent employees and uses its power to make crucial and strategic decisions. Thus, they need to make these changes. Oropesa et al., (2016) revealed that top management’s support by providing competent human resources had a positive effect on economic benefits and the quality of the financial report. Based on this fact, the fifth hypothesis was formulated

Competence of village apparatus (AC) will improve the performance of the village government (PR) Research Method

This research used a saturated sample to confirm data and results validity of 270 village governments asanalysis units. The data was collected with a survey by distributing questionnaires directly to 1,080 respondents of village managers (village secretary, village treasurer, Village Supervisory Agency, Village Community Institutions). Also, interviews on selected samples were conducted. Furthermore, the data analysis employed Structural Equation Model-Lisrel.

RESULTS

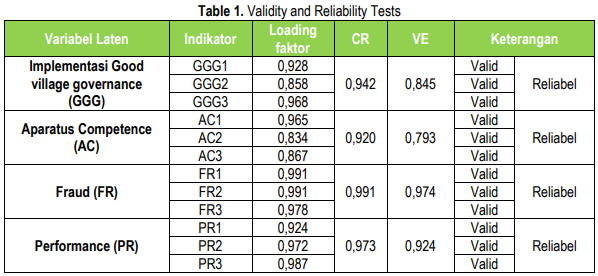

Validity and reliability depict accuracy of the questionnaire as a measurement of variable precision and by examining the relationship between indicators and variables. Before the hypothesis testing stage, all variables must pass validity and reliability testing. In this study, the validity was tested by loading factor while the reliability was assessed by using construct reliability. Table 1 shows the results of each variable testing.

Based on the test results in Table 1, all indicators depict a loading factor standard value of > 0.50 andConstruct Reliability of > 0.70. Hence, all of them meet the validity and reliability criteria.

Structural Model Testing

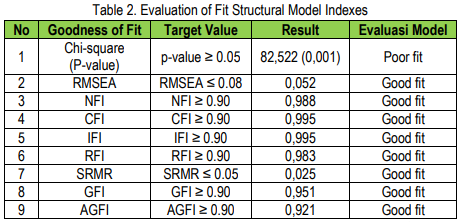

This test aims to determine whether the research model can be used to test hypotheses by applying the Goodness of Fit Index (GOFI) indicator. A model meets the criteria if the evaluation results show Good Fit. Based on the results presented in Table 2, the values of GFI, NNFI, NFI, AGFI, RFI, IFI, CFI were > 0.90, meaning the model to be tested is in a good fit. Hence, this research model is acceptable and can be employed at hypotheses testing stage.

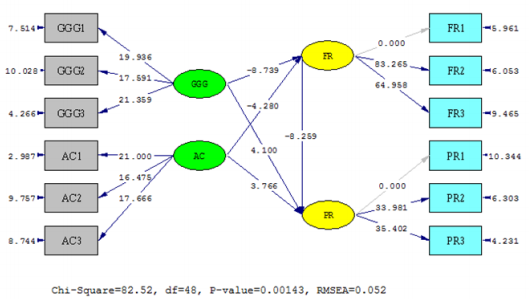

Hypotheses testing in this study was conducted using Structural Equation Model (SEM) analysis at thelevel of significance (α = 0.05). Hypothesis test results and path coefficients are displayed in Figure 1 and Table 3.

Figure 1. Full Structural Model Results (T values)

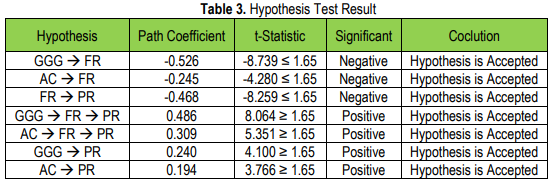

The test results revealed that GGG negatively affects the RF, which was attested with the value of T statistic at -8,739. This result indicates that the low implementation of the GGG will trigger FR. The second hypothesis showed that the AC negatively affects the RF, which was successfully supported by the T-statistic value of -4,280. This finding implies that if the village apparatus has low competence, the level of fraud management of village funds will tend to increase. Furthermore, the third hypothesis revealed that the FR negatively affects the PR with the T statistic value of -8,259. The robust implementation of GGG can improve the performance (PR) in the village government (proven by the T statistic test results of 4,100). Also, AC will increase PR. Hence, the fourth and fifth hypotheses are accepted.

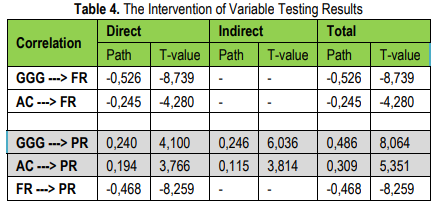

To prove that FR as an intervening variable, the results of the direct and indirect effect tests are presented in Table 4, as follows:

The line coefficient of GGG direct effect on PR was 0.240, while FR indirect effect was 0.246. Hence, the total leverage of GGG against PR over RF was 0.486 higher than the direct impact of 0.240. It indicates that the RF variables had a positive contribution to the processing of GGG relationships. Thus, the RF variables were proven as intervening variables. Similarly, the line coefficient of AC direct effect towards PR was 0.194, while FR indirect effect through was 0.115. Hence, the total impact of AC to PR through RF was 0.309 higher than the direct result of 0.194. It reveals that the RF variables have a positive contribution to the processing of AC relationships. Thus, the RF variables were proven as intervening variables. The path coefficient of GGG direct effect on PR was 0.240, and the indirect impact through FR was 0.246. Hence, the GGG total effect on PR through FR was 0.486 higher than the direct impact of 0.240. It indicates that the FR variable had a positive contribution in mediating the relationship of GGG. Thus, the FR variable was proven to be an intervening variable. Likewise, the path coefficient on the AC direct effect on PR was 0.194, while the indirect impact through FR was 0.115. Thus, the AC total effect of PR through FR was 0.309 higher than the direct impact of0.194. It shows that the FR variable had a positive contribution in mediating the AC relationship. Hence, the FR variable was proven to be an intervening variable.

DISCUSSION

The study by Omar and Katerina (2011) concerning the implementation of good governance on the level of fraud revealed that the application of corporate governance is characterized by the presence of external auditors, internal auditors, the board of directors, audit committee, and anti-fraud specialists. They can lower the level of fraud in a company. Magnanelli (2010) also found that corporate governance can reduce the level of fraud in all lines of an organization. The research by Dechow, Sloan and Sweeney (1996) showed that a weak organization implementing village governance would commit significant fraud. The high level of fraud is caused by fraud opportunity in each line of an organization. Similarly, the results of Beasley et al. (2000) showed that an organization with good village governance, such as an effective internal audit, the tone at the top and active participation of all employees in realizing organizational goals, can lower the fraud. Implementation of good village governance can be in the form of social control to prevent all types of unethical practices (bribery and corruption) and also honesty, transparency, and accountability within the organization. This research reinforces contingency theory Lawrence and Lorsch (1967) which explains that situational factors influence various efforts to reduce and even eliminate fraud in village fund management. One of the initiatives is through the implementation of good village governance by applying transparency, accountability, and community participation in village government activities as well as skilled village apparatus.

Based on Law No. 8 of 2008 concerning Openness of Public Information, the village government is required to submit the financial report in media which can be accessed by the public, both in print, such as newspapers and electronically, like their official website. However, the analysis unit found that transparency in financial management was limited in providing information regarding village budget allocation. However, operational use and realization village funds have never been made public. A high number of village funds management is not accountable because the funds are held and managed directly by the village head and cannot be accounted for properly. Hence, the accountability principle is not met. On the other hand, public interest to succeed village funding program is moderately high. It is proven by community participation in various activities, especially infrastructure. Village people assist in forms of volunteers and facilities to develop infrastructure in their village. In regards to the competence of the village apparatus, the findings revealed that the majority (61.8%) of them only have a high school education. Nevertheless, management and accountability of village funds management require adequate competence, particularly in the use of technology as a means of creating financial accountability. The limited ability to employ technology, for example, has an impact on the slow process of preparing financial reports and the low use of budget. Thus,the performance of village government will also decline. Several villages with apparatuses having a Bachelor's and Master's education shows an ideal condition. It is where the level of fraud of village funds can be suppressed, and the performance of village government increases each year significantly.

This research implies that a significant rise of the village apparatus competence will have a direct impact on developing the village government performance —also, the higher their expertise, the lower the level of fraud in village funds. Currently, the village apparatus need structured training regarding the concept and technical implementation of village funds management. It is because current regulations need to be understood conceptually. Hence, they need to participate in theses professional training to fulfil the conceptual regulations. The district government should start drafting regulations for village governments to utilize information technology, such as designing village websites. Therefore, the process of planning, managing, and accounting for village funds can be carried out through e-village governance.

CONCLUSION

The level of fraud in village fund management can be decreased by strengthening the implementation of good village governance in every level and activity of village governance. Transparent, accountable, and active participation of village governance can be held liable to community and central government. Furthermore, village apparatus competence plays the primary role to improve the performance of the village government. Regular education and training related to village funds management are much needed by the village apparatus, village internal supervisors, and village facilitators to enhance their knowledge and skills. The significant rise of village apparatus competence will have a direct impact on refining village government performance —also, the better the capability of village apparatus, the lower the fraud in village funds.

BIODATA

D.A MUNIR: Dony Ahmad Munir is a student of the Doctoral Program in Accounting, Universitas Padjadjaran. He also graduated from his master program at Universitas Padjadjaran. He has been actively including himself in politics since years ago. He was a member of the House of Representatives of the Indonesian Republic. He is currently a regent of Sumedang City.

S MULYANI: Sri Mulyani is a lecturer in the accounting department, Universitas Padjadjaran. She has experienced more than 25 years in the field of information systems and good governance for the private, public, and sharia sector. She actively writes and gives consultations for analyzing and designing applied information systems, good governance, sharia finance, and others. She is currently the National Council Member, Institute of Indonesia Chartered Accountants.

B AKBAR: Bahrullah Akbar is currently a member of the Audit Board of the Republic of Indonesia (BPK-RI). He also served himself as a lecturer at the Institute of Public Administration (IPDN). He completed his doctoral program at Universitas Padjadjaran in governance science and he also studied at the University of Leicester for a postgraduate program in public sector management.

M YOSEPH: Yoseph Musa is an adjunct lecturer at Universitas Padjadjaran. He is currently serving for the Bureau of Planning and Overseas Cooperation in the Ministry of Education and Culture (Kemendikbud). He completed his doctoral program at Universitas Padjadjaran, focused on the accounting subject.

BIBLIOFRAPHY

ABREU, R, DAVID, F & SEGURA, L. (2016). “E-banking services: Why fraud is important?” Journal of Information Systems Engineering and Management, 1(2), pp.111-121.

AGRAWAL, A. & CHADHA, S (2005). “Corporate governance and accounting scandals.” Journal of Law and Economics. 48(2), pp. 371-406.

ARENS, A. ALVIN., RANDAL.J.ELDER., MARK, S. BEASLEY (2014). Auditing and Assurance Service. New Jersey: United States, Prentice-Hall Publication.

ASYLGARAEVA, G & BOCHAROV, S (2019). “On the main results of Scientific Activity Institute of Archaeology named after a. Kh. Khalikov of the Tatarstan Academy of Sciences in 2018”, Povolzhskaya Arkheologiya, 1(27), pp. 208-228.

ATKINSON, S.P, AND WILSON (2012). “Comparing Mean Efficiency and Productivity Scores From Small Samples: A Bootstrap Methodology.” Journal of Productivity Anal, 6(137), pp. 1-12.

BALOYI, N.T (2005). Misuse intrusion architecture: prevent, detect, monitor and recover employee fraud. In The Proceedings of the Information Security South Africa. New knowledge today conference. Sandtorn, South Africa

BEASLEY, M.S, CARCELLO, J.V, HERMANSON, D.R & LAPIDES, P.D (2000). “Fraudulent Financialreporting: Consideration of industry traits and corporate governance mechanisms.” Accounting Horizons Journal, 14(4), pp. 441-467.

Bhagat ,S & Bolton, B (2008). “Corporate governance and firm performance.” Journal of corporate finance, 14, pp. 257-273.

CHENG, T.C.E & TSAN-MING, C (2010). Innovative Quick Response T.C. Edwin Cheng Programs in Logistics and Supply Chain Management. Berlin: Germany, Springer publishing house.

COHEN, A & SAYAG, G (2012). “The Effectiveness of Internal Auditing: An Empirical Examination of its Determinants in Israeli Organisations.” Australian Accounting Review, 20(3), pp. 1-11.

DAFT, R, KENDRICK, M & VERSHININA, N (2010). Management. International Edition. Florida: USA, South- Western Cangage Learning Publication.

DECHOW, P.M, SLOAN, R.G & SWEENEY, A.P (1996). “Causes and Consequences of Earnings Manipulation: An Analysis of Firms Subject to enforcement actions by the SEC.” Contemporary Accounting Research, 13, pp. 1-36

HITT, M, DUANCE, A.R & HOSKISSON, R.E (2009). “Strategic Management: Competitiveness and Globalization, Third Edition." California: USA, South-Western College Publishing.

HOUT, W (2007). “The Politics of Aid Selectivity Good governance criteria in World Bank, US and Dutch development assistance.” Abingdon: UK, Routledge Publication.

JINARAT, V & QUANG, T (2003). “ The Impact of Good Governance on organization performance after the Asian crisis in Thailand.” Asia Pacific Business Review, 10(1), pp. 21-42.

KOMEKBAYEVA, L.S, LEGOSTAYEVA, A.A, TYAN, O.A & ORYNBASSAROVA, Y.D (2016). “GovernmentMeasures for Economic Support in the Conditions of a Floating Exchange Rate of the National Currency.” International Electronic Journal of Mathematics Education, 11(7), pp. 2227-2237.

LANE, J (2010). “Management and public organization: The principal-agent framework.” The University of Geneva and the National University of Singapore. Working paper.

LAWRENCE, R.P & LORSCH, J.W (1967). “Differentiation and Integration in Complex Organization.” Administrative Science Quarterly, 12(1), pp. 1-9.

LAWS, P (2011). “Corporate Governance and No Fraud Occurrence in organizations: Hong Kong evidence.” Managerial Auditing Journal, 26(6), pp.501–518.

LOCKWOOD, M (2010). “Good governance for terrestrial protected areas: A framework, principles and performance outcomes.” Journal of Environmental Management, 91, pp.754–766

LUKVIARMAN, N (2016). Corporate Governance, Menuju Penguatan Konseptuan dan Implementasi di Indonesia. Surakarta: Indonesia, Era Adicitra Intermedia Publication.

LUSTHAUS, C, ADRIEN, M.H, ANDERSON, G, CARDEN, F & MONTALVÁN, G.P (2002). Organizationalassessment. Ottawa: Canada, International Development Research Centre Press.

MAGNANELLI, B.S (2010). The Role of Corporate governance In Financial Statement Fraud. Rome: Italy, Diss LUISS Free International University of Social Studies Press.

MAHMOOD, S (2007). Good Governance Reform Agenda in Pakistan: Current Challenges. New York: USA, Nova Science Publisher. Inc.

MAHSUN, M (2006). Measurement of Public Sector Performance. Yogyakarta: Indonesia, BPFE Publication.

MARDIASMO, M (2009). Public sector accounting. Yogyakarta: Indonesia, Andi Publication.

MOELLER, R.R (2014). Executive’s Guide to COSO Internal Controls Understanding and Implementing the New Framework. New Jersey: USA, John Wiley & Sons Publication.

MORGAN, S (2007). “Technological innovativeness as a moderator of new product design integration and top management support.” Journal of Prod Innovation Management. 7, pp.208-220.

MOUSA, F.M, RIYAD, M.H, MOHAMAD, A.D & IAAD, I.S (2012). “The Impact of Corporate Governance on the Performance of Jordanian Banks.” European Journal of Scientific Research, 67(3), pp.349-359.

MULYANI, S & FETTRY, S (2016). “The influence of Audit committee composition, authority, resource, and diligence toward financial reporting quality.” International Journal of Accounting, Business and Economics Research, 14(1), pp.253-275.

MULYANI, S, KASIM, E, YADIATI, W & UMAR, H (2019). “Influence of Accounting Information Systems and Internal Audit on Fraudulent Financial Reporting.” Opcion Journal, 35(21), pp. 323-338.

NEUMAYER, E (2003). The Pattern of Aid Giving. The Impact of Good Governance on Development Assistance. London & New York, Routledge Publication.

OMAR, N & KATERINA M.A.B (2011). “Fraud Prevention Mechanisms of Malaysian Village-Linked Companies: An Assessment of Existence and Effectiveness.” Journal of Modern Accounting and Auditing, 8(1), pp. 15-31.

OROPESA, M, JORGE, L.G, ALCARAZ A.A, MALDONADO, M.V & MARTÍNEZ, L (2016). “The Impact ofManagerial Commitment and Kaizen Benefits on Companies.” Journal of Manufacturing Technology Management, 27(5), pp.692-712.

ROBBINS, S.P (2007). Organizational Behavior. New Jersey, Prentice Hall International Inc.

SANCHEZ, D, KLOT, L & SPINCER, B.H (1997). Issues in Public Sector Accounting. Oxford: UK, Oxford Press.

SANUSI, A (2015). “Effect of market-oriented, good governance, and professional leadership on managerial performance International of a special unit of upstream oil and Gas: A case study of SKK Migas Indonesia.” Journal of Advances in Engineering, 8(3), pp.246-255.

SELOMO, M.R, GOVENDER, K.K (2016). “Procurement and Supply Chain Management in Government Institutions: A Case Study of Select Departments in the Limpopo Province, South Africa.” Dutch Journal of Finance and Management, 1(1), pp.1-10.

SINGLETON, T.W & SINGLETON, A.J (2010). “Fraud auditing and forensic accounting (Vol. 11).” New Jersey: USA, John Wiley & Sons Publication.

SMITH, D & POLITOWSKI, R (2008). Good Governance A risk-based management systems approach to internal control. London: UK, British Standards Institution Press.

SPENCER, L.M & SPENCER, S.M (1993). Competence at Work Models for Superior Performance. New Jersey: USA, John Wiley & Sons Publication.

STEWARD, G.L & BROWN, K.G (2011). Human Resource Management Linking Strategy to Practice. New Jersey: USA, John Wiley & Sons Publication.

STOKER, G (2008). “Governance as theory: five propositions.” International Journal of Social Sciences. 50(1), pp.17–28.

SUPRIADI, T, MULYANI, S, SOEPARDI, E.M & FARIDA, I (2019). “Influence of Auditor Competency in Using Information Technology on Success of E-Audit System Implementation.” EURASIA Journal of Mathematics, Science and Technology Education 15(10), pp.1-13.

THOMAS, A.R & GIBSON, K.M (2003). “Management is responsible, too.” Journal of Accountancy, 195(4), pp.53-67.

UMAR, H (2006). Strategic Control, Membangun Indonesia yang Bebas KKN, Berkinerja, dan Good Governance. Jakarta: Indonesia, Penerbit Universitas Trisakti.

USKARA, A, MULYANI, S & AKBAR, B.S (2019). “The effect of the Internal Control System's Effectiveness on Village Performance.” Opcion Journal, 35(89), pp. 195-214.

VERWEIRE, K & VAN, L (2004). Integrated Performance Management: a guide to strategy implementation. California: USA, Sage Publication.

WANG, Y & KUO, T (2010). “A Financial Assets and Liabilities Management Support System.” Contemporary Management Research, 6(4), pp.315-340.

YUKL, G (2010). Leadership in Organization. New Jersey:USA. Person Prentice Hall Press.

ZIKMUD, W.G, BABIN, J, CARR, J.C & GRIFFIN, M (2010). Business Research Method, 8th Edition. Boston: Massachusetts, South-Western Cengage Learning Publication.