Artículos

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 3.0 International.

Received: 22 March 2020

Accepted: 30 April 2020

DOI: https://doi.org/10.5281/zenodo.3809363

Abstract: The purpose of this paper is to measure how effective the utilization of management accounting information system on the gas business station and its impact on the quality of information and optimization for decision- making. Effectiveness measured in the context of policies, people, processes and systems. This research was conducted in 235 gas stations located in the Western part of Java involving 235 respondents using questionnaire instruments and in-depth interviews with a key person. The results of the research revealed that the utilization of management accounting information systems has a positive impact on the quality of information.

Keywords: Indonesia, Information quality, anagement accounting information system, optimization decision making..

Resumen: El propósito de este documento es medir qué tan efectiva es la utilización del sistema de información de contabilidad de gestión en la estación de negocios de gas y su impacto en la calidad de la información y la optimización para la toma de decisiones. Efectividad medida en el contexto de políticas, personas, procesos y sistemas. Esta investigación se realizó en 235 estaciones de servicio ubicadas en la parte occidental de Java que involucraron a 235 encuestados utilizando instrumentos de cuestionarios y entrevistas en profundidad con personas clave. Los resultados de la investigación revelaron que la utilización del sistema de información contable de gestión tiene un impacto positivo en la calidad de la información.

Palabras clave: Calidad de la información, Indonesia, optimización de la toma de decisiones, sistema de información contable de gestión..

INTRODUCION

Over the years, the Government of Indonesia through one of the energy State Owned Enterprise, PT Pertamina (Persero) is trying to fulfill its obligation to distribute fuels across Indonesia. Pertamina finds a way to manage the energy supply chain including to the remote areas. In 2015, they built an information system to help management to monitor supply chain across the region and to ensure that Pertamina can distribute fuels right on time to avoid shortage. Their objective is in line with who found that information system utilization is important to help management in the decision making process since they need information relevant to the organization’s objective.

Pomberg et al. (2012, pp.100-114) said that accounting information system helps the manager to make decisions regarding the logistic management. Only for the managers with high capacity business and located near the center of economic who are using the information system on the decision-making process. The result was positive that they can reduce the logistics cost. Mulyani et al. (2016, pp. 552-560) said information systems able to increase production quality and reduce services cost. It is also more efficient, effective and can be part of knowledge sharing. The information system also is part of internal control and makes decision- making more effective.

Gorla et al. (2010, pp.207-228) mentioned that the efforts to increase the information system services quality can increase the organization’s performance. With the limited resources of the organizations, the highest priority is to develop an information system and its services to increase information quality. False decision-making will cost the organization a huge amount of money. Berisha-Shaqiri (2014) said that when the leader made the decision, they have to consider any information, hence the integrated information system development will create good profit and will increase efficiency, and competitiveness.

LITERATURE REVIEW, THEORETICAL FRAMEWORK, AND HYPOTHESES

Utilization of the Management Accounting Information System

The utilization of information system is the key to success on information technology development and on the information technology implementation such as adoption, acceptance, and diffusion (Agarwal: 2000; Burton-Jones & Straub: 2006, pp. 228-246; Straub et al.: 1995, pp. 1328-1342). Suzan et al. (2019, p.629) said the success of management accounting information system implementation has a significant impact on the performance improvement of the organization or company. It proves that the successful implementation of an information system will increase company performance. Based on the above definitions, the concept of this variable is the system which is used by the management to achieve the competitive advantages to produce high-quality services (Mason & Ragowsky: 1997, pp. 278-287; Whitten & Bentley: 1998; Agarwal: 2000; Aziz& Macredie: 2005, pp. 468-476; Stair & Reynolds: 2010; Laudon & Laudon: 2012, p.143; Mulyani et al: 2016,pp.552-560).

Measurement of utilization of management accounting information system are using nine indicators such as: (Rice & Rogers: 1980, pp.499-514; Doll & Torkzadeh: 1998, pp.171-185; Beaudry & Pinsonneault: 2005, pp. 493-524; Aziz & Macredie: 2005, pp. 468-476)

- 1. Problem-solving

- 2. Decision rationalization

- 3. Customer service

- 4. Operational adaptation

- 5. Technology adaptation

- 6. Organizational adaptation

- 7. User satisfaction

- 8. Effectiveness

- 9. Efficiency

Information Quality

According to Haag and Cummings (2009), information considered as high quality when it is relevant and useful in the decision-making process. McLeod and Schell (2004) identified information quality as relevance, accuracy, timeliness, completeness. Based on the above definitions, the concept of information quality in this study is the process to guarantee that the information from the information system is useful in the decision- making process (Haag & Cummings: 2009; Bawden & Robinson: 2009, pp. 180-191; Stair & Reynolds: 2010).

Measurement of information quality is using seven indicators from this literature, such as (Zhuang& Burns, 1994, pp. 10-19; McLeod & Schell: 2004; Laudon & Laudon: 2012, p.143; O'Brien & Marakas: 2011):

- 1. Relevance

- 2. Accuracy

- 3. Accessibility

- 4. Timeliness

- 5. Completeness

- 6. Clarity

- 7. Consistency

Decision Making Optimization

According to Griffin and Morehead (2014, p.208), decision-making is the process, which used to select one of the action as the problem-solving method. Decision-making is the process to select one alternative solution from several alternatives (Griffin & Morehead: 2014:208). Management accounting has a role in helping the managers to make the decision. The decision was made with selected action (McLeod & Schell: 2004). Based on the above definitions, the concept of decision-making optimization is a selection process to choose the best alternative from several alternatives systemically to use as a key in problem-solving (McLeod& Schell: 2004; Griffin & Morehead: 2014).

Measurement in this study for decision-making optimization is using these four indicators, such as (McLeod: 2007; Dehdar et al.: 2019, pp. 31-36) decision can solve the problem accurately; 2) there is no negative impact from the decision; 3) faster Decision-making; 4) on time decision-making.

METHODS

Sample

Measurement of the effectiveness of the Utilization of Management Accounting Information System and Its Impact on Information Quality and Optimization for Decision Making carried out in 235 gas stations in Pertamina Western Region of Java (DKI Jakarta, West Java, and Banten province). Data were collected using questionnaire instruments and in-depth interviews. Data collection carried out in 70 days by directly send out the online questionnaire link to the respondents then visiting the analysis unit to do an in-depth interview (Prokhorova: 2019, pp. 216-232).

Each respondent gets an explanation before answering the questionnaire question, and it ensured that the respondents who have the right to give answers are the owner and manager of the gas station who are directly involved in the utilization of the information system. Data collected through a questionnaire successfully reach 228 valid respondents (97.02% of the population).

Validity and Reliability of Instrument

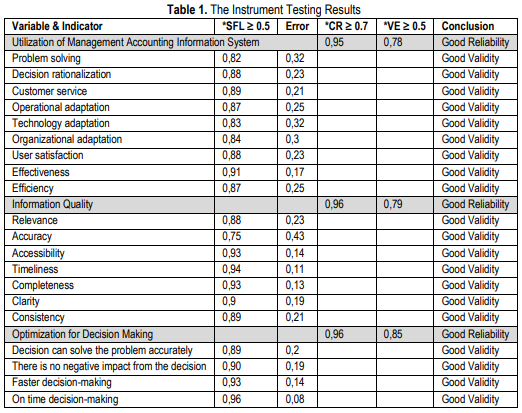

As mentioned above, the questionnaire to measure all the variables developed from the literature. Although this questionnaire item has been tested previously, it needs to be re-tested its validity level and reliability to ensure how well the concept can be defined by dimensions or indicators (Hair et al.: 2014). In thisquestionnaire, respondents asked to rate 20 items, using a 5-scale Likert approach (Sugiyono: 2011; Mustafin et al.: 2019, pp. 318-331). A value of 1 indicates a "strongly disagree" condition until value 5 indicates a "strongly agree" condition.

The statistical results of instrument validity and reliability testing wrote in Table 1 below. According to Hair et al. (2014) if the value of the standard factors loading (SFL) ≥ 0.50, then the indicator declared as a significant and valid measurement tool. While reliability testing uses the Construct Reliability (CR) and Variance Extracted (VE) size approaches. Constructions have good reliability or level of consistency if the CR value is 70 0.70, and the value of VE 0 0.50 (Ghozali: 2014).

Data in Table 1 shows that the 20 indicators used declared as valid instruments. The majority value of loading factors is above 0,5, while the reliability of indicators (CR) exceeds the threshold of 0,7 and the VE value is entirely above 0,5. Thus, it concluded that all items on the instrument declared valid and reliable to measure the Utilization of Management Accounting Information System and Its Impact on Information Quality and Optimization for Decision Making.

Data Analysis

Data analysis uses descriptive and verification approaches. Descriptive analysis aims to describe quantitatively the level of effectiveness of this study. While the verification analysis uses the SEM method with the Lisrel 8.8 statistical software, it aims to prove the research hypothesis. Analysis of sample data will be applied to the population through the t-statistics test with a confidence interval of 95% and a risk level of error at α = 5%.

RESULTS

Demographic Information

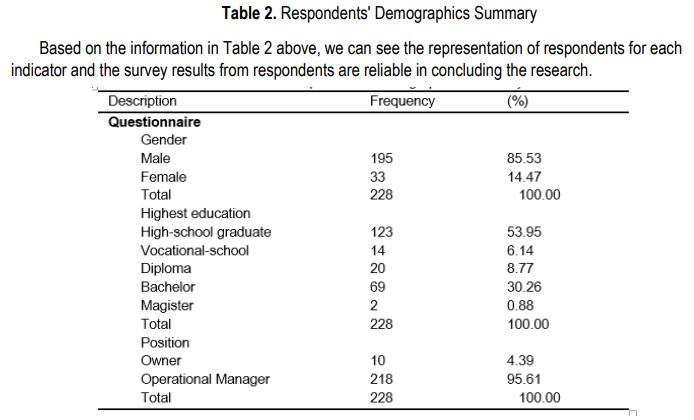

Data in Table 2 below show demographic information of research respondents. From 235 samples only valid for 228 respondents. Male respondents (85.53%) were the majority compared to female respondents (14.47%). From the level of education, the majority of respondents were high school graduates (53.95%), bachelor (30.26%), diploma (8.77%), and vocational school (6.14%), magister (0.88%) with a majority-position as operational manager (95.61%).

Based on the information in Table 2 above, we can see the representation of respondents for each indicator and the survey results from respondents are reliable in concluding the research.

Goodness of Fit

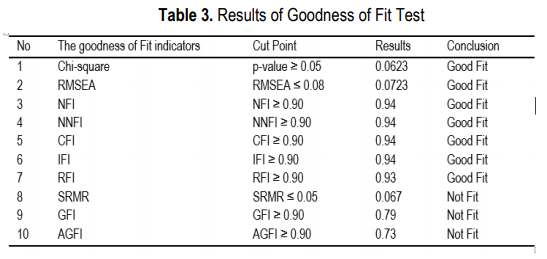

Below are the test results of the goodness of fit of this research. See Table 3.

Data in Table 3, refer to Schumacker and Lomax (2010, p.76) shows that the values of NFI, NNFI, CFI, IFI, RFI, GFI, AGFI ≥ 0,90, the value of chi-square = 0,0623≥ 0.05, and the value of RMSEA = 0,0723 ≤ 0,08 means that the model is fit. While the SRMR value = 0,067 ≥ 0,05 indicates the model is not fit. 7 out of 10 indicators is matching and show good results, so it can be concluded that this research model has very good. After the model is declared fit, then the hypothesis is tested, the results are seen in Table 4.

Hypothesis Test

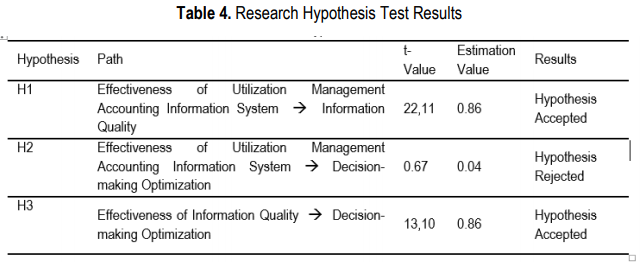

Data in Table 4, shows the research hypothesis is proven to be accepted because the value of the t- value is 7,24 (95% confidence level, and 5% error level) greater than the minimum t-value value of 1,96. This means that there is a positive relationship between the effectiveness of the application of accrual accounting and the quality of fiscal transparency. While the estimated value of 0,54 shows that the effectiveness of the application of accrual accounting has a positive effect much of 54% on the quality of fiscal transparency.

DISCUSSION

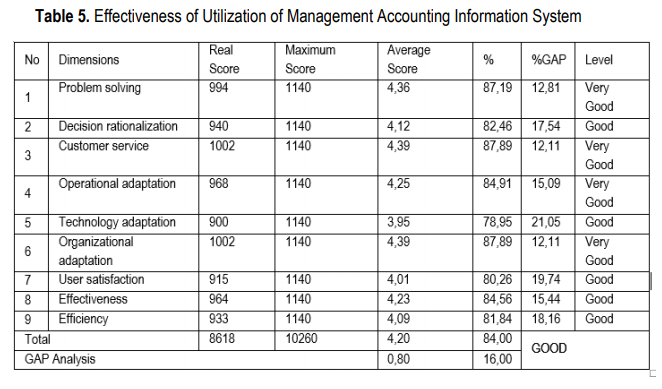

Measurement of the effectiveness of the application of accrual accounting using respondents' responses arranged in the form of a score range. The score range is made as a reference for grouping the results of the scoring, with criteria: (1) 1,00 – 1,80 is Strongly Disagree. (2) 1,81 – 2,61 is Disagree. (3) 2,62 – 3,42 isAverage. (4) 3,43 – 4,23 is Agree. (5) 4,24 - 5,00 is Strongly Agree. Measurement results see Table 5.

Table 5, shows that the overall effectiveness of the utilization of the management accounting information system is at a good level with a good score of 4,20 from 5 point scales. Nevertheless, there is still a GAP with 16% caused by the GAP between the indicators. For example, technology adaptation, user satisfaction, and efficiency are the highest with more than 18% GAP.

Technology adaptation has 21,05% GAP, user satisfaction has 19,74% GAP and efficiency has 18,16% GAP for the reason that there is a condition when an employee still needs to use manual mode to input the data into the system and need to form a manual logbook on the paper. Also, they cannot find a feature that may help them to calculate the stock status. Sometimes they are confused with that situation.

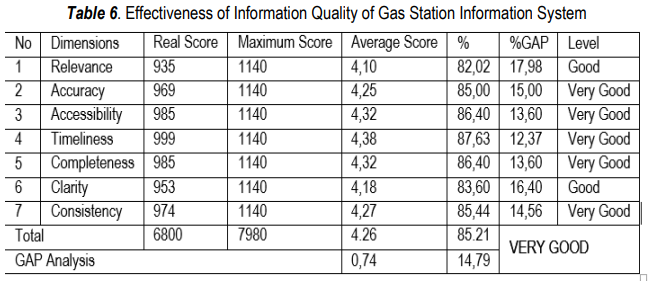

Table 6 shows that the variable declared as very good with an average score of 4,26 from 5 point scales. Nevertheless, there is still a GAP between indicators such as relevance with 17,98% and clarity with 16,40%. Overall, the system is good and everyone may access from multiplatform, PC, Tablet, Mobile-phone. It is good since everyone can remotely monitor the gas station operation from anywhere.

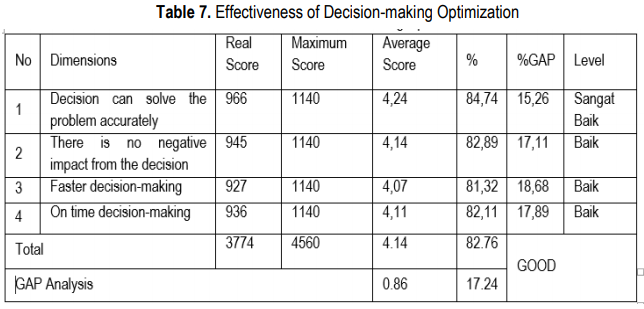

Table 7 shows that the variable declared as good with an average score of 4,14 from 5 point scales. The table also shows that there is still a GAP for faster decision-making and on time decision-making. That situation happened for the reason that there is a time buying moment when management needs to review the data from the system then they make a final statement.

CONCLUSION

This research finds that the utilization of management accounting information systems has a positive impact on the information quality of the system. Utilization of the system helped the management to deliver accurate, relevant and any other information, hence the management be able to decide regarding fill the storage tank with a new product to sell to the customers, so there will no shortage in the gas stations.

Utilization of the system also has a positive impact on the decision-making process. Management can access the status of the gas station operational storage from their mobile phones. It helped them to ease the coordination between all the employees. Information quality also has a positive impact on the decision-making process. As mentioned above, management can access high-quality information from anywhere.

An information system is the fundamentals to operate the gas station all over Indonesia. Since Pertamina is the state-owned enterprise, thus they must deliver all the products all over Indonesia including remote areas. With the development of the information system, Pertamina may ease the process, start from the internal evaluation regarding the storage tank status, until the decision made to buy the product to avoid the shortage.

BIODATA

Dicky Septriadi is a Doctoral Student of the Programme of Accounting from Universitas Padjadjaran, currently working as a professional in one of SOE in Indonesia. His research interests related to information systems.

Wahyudin Zarkasyi is a Professor of Accounting in Public Sector Accounting from Universitas Padjadjaran, currently working as a Rector of Singaperbangsa University in Karawang, Indonesia. His research interests related to information systems, government accounting.

Sri Mulyani is a Professor of Accounting Information Systems and Public Sector Accounting from Universitas Padjadjaran. She is a lecturer in the Master’s accounting programme and The Doctoral Programme of Accounting Science at the Faculty of Economics and Business, Universitas Padjadjaran. Her research interests are related to areas dealing with public sector accounting information systems and good governance.

Citra Sukmadilaga is a lecturer in the Master’s accounting programme and The Doctoral Programme of Accounting Science at the Faculty of Economics and Business, Universitas Padjadjaran. His research interests are related to financial accounting and public sector accounting.

BIBLIOGRAPHY

AGARWAL, RP (2000). Difference equations and inequalities: theory, methods, and applications. CRC Press

AZIZ, M & MACREDIE, RD (2005). “Proposing a perceived ease of use factors taxonomy for informationsystem use”. In Proceedings. IEEE SoutheastCon. pp. 468-476. IEEE.

BAWDEN, D & ROBINSON, L (2009). “The dark side of information: overload, anxiety and other paradoxes and pathologies”. Journal of information science, 35(2), pp. 180-191.

BEAUDRY, A & PINSONNEAULT, A (2005). “Understanding user responses to information technology: A coping model of user adaptation”. MIS quarterly, pp.493-524.

BERISHA-SHAQIRI, A (2014). “Management Information System and Decision-Making”. Academic Journal of Interdisciplinary Studies, 3(2), p.19.

BURTON-JONES, A & STRAUB JDW (2006). “Reconceptualizing system usage: An approach and empirical test”. Information systems research, 17(3), pp. 228-246.

DEHDAR, M, SAYEGANI, L, ARBAB, E, ARZHANDEH, M, ROSHANRAY, M, RAEISI, A & KUHI, L (2019).“Role of schools in educating the active citizen”. Journal of Social Sciences and Humanities Research, 7(02), pp. 31-36.

DOLL, WJ & TORKZADEH, G (1998). “Developing a multidimensional measure of system-use in an organizational context”. Information & Management, 33(4), pp.171-185.

GHOZALI, I (2014), Structural Equation Modeling: Teori, Konsep dan Aplikasi dengan Program LISREL 9.10 Edisi 4, Semarang: Badan Penerbit UNDIP.

GORLA, N, SOMERS, TM & WONG, B (2010). “Organizational impact of system quality, information quality, and service quality”. The Journal of Strategic Information Systems, 19(3), pp.207-228.

GRIFFIN, RW & MOORHEAD, G (2014). Managing People In Organization. South-Western: USA.

HAAG, S & CUMMINGS, M (2009). Management information systems for the information age. McGraw-Hill, Inc.

HAIR, JF, HUFIT, GM, RINGLE, CM & SARSTEDT, M (2014), A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), Los Angeles: SAGE Publications, Inc.

LAUDON, KC. & LAUDON, JP. 2012. “Management Information Systems - Managing The Digital Firm”. 12th Edition. Perason Prentice Hall.p.143.

MASON, CF & RAGOWSKY, A (1997). “On the value of information from using information systems”. In Proceedings of the Thirtieth Hawaii International Conference on System Sciences. 3, pp. 278-287. IEEE.

MCLEOD, R & SCHELL, G (2004). Sistem informasi manajemen. Indeks.

MULYANI, S, ANUGRAH, F & HASSAN, R (2016), “The critical Success Factors for The Use of Information Systems and Its Impact on The Organizational Performance”, International Business Management Journal, 10(4), pp.552-560, DOI:10.3923/ibm.2016.552.560.

MUSTAFIN, AN, KOTENKOVA, SN, SHLYAKHTIN, AE, KOTULIČ, R, KRAVČÁKOVÁ VOZÁROVÁ, I &BENKOVÁ, E (2019). “The governance of innovation in industrial enterprises”, Polish Journal of Management Studies, 20(1), pp. 318-331.

O'BRIEN, JA & MARAKAS, GM (2011). Management information systems. 9. McGraw-Hill/Irwin.

POMBERG, M, POURJALALI, H, DANIEL, S & KIMBRO, MB (2012). “Management accounting informationsystems: a case of a developing country: Vietnam”. Asia-Pacific Journal of Accounting & Economics, 19(1),pp.100-114.

PROKHOROVA, T (2019). “New sentimentality” in the novels Pismovnik by mikhail shishkin and the aviator by Eugene vodolazkin”, Vestnik Tomskogo Gosudarstvennogo Universiteta Filologiya-Tomsk State University Journal Of Philology, 59, pp. 216-232.

RICE, RE & ROGERS, EM (1980). “Reinvention in the innovation process. Knowledge", 1(4), pp.499-514.

SCHUMACKER, RE & LOMAX, RG (2010). “A Beginner’s Guide to Structural Equation Modeling”, ThirdEdition, New York, NY 10017: Taylor and Francis Group, LLC. p.76.

STAIR, RM & REYNOLDS, GW (2010). Principles of information systems, course technology. Cengage Learning, Walldorf.

STRAUB, D, LIMAYEM, M & KARAHANNA-EVARISTO, E (1995). “Measuring system usage: Implications for IS theory testing”. Management science, 41(8), pp. 1328-1342.

SUGIYONO, D (2011), Metode Penelitian Kuantitaif, Kualitatif dan R & D, Bandung: Alfabeta.

SUZAN, L, MULYANI, S, SUKMADILAGA, C, FARIDA, I. 2019. “Empirical Testing of the Implementation of Supply Chain Management and Successful Supporting Factors of Management Accounting Information Systems”. Int. J Sup. Chain. Mgt 8(4), p.629.

WHITTEN, J (1998). “L. and LD Bentley”. System Analysis and Design Methods, 4th Edition. Taipei: McGraw Hill.

ZHUANG, L & BURNS, G (1994). “Integrated Manufacturing Information System: A Three‐stage DecisionProcedure”. Integrated Manufacturing Systems, 5(3), pp. 10-19.