Artículos

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International.

Received: 28 August 2020

Accepted: 29 October 2020

DOI: https://doi.org/10.5281/zenodo.4155757

Abstract: There has been an increased focus among recent studies on bank profitability. However, there is a gap in the literature in terms of the relationship and causalities between profitability and bank concentrations. To close this gap, this study investigates whether the concentrations of 5 and 7 banks have an impact on bank profitability by using the wavelet coherence technique covering the period 1995Q1-2017Q3. As expected, it is observed that bank profitability and banking concentrations of 5 and 7 banks significantly fluctuated in the period 2000 and 2003. In Turkey, bank concentrations significantly cause the banks’ profitability at different time periods.

Keywords: Bank concentration, profitability, Turkey, wavelet coherence..

Resumen: Ha habido un mayor enfoque entre los estudios recientes sobre la rentabilidad bancaria. Sin embargo, existe una brecha en la literatura en términos de la relación y causalidades entre la rentabilidad y las concentraciones bancarias. Para cerrar esta brecha, este estudio investiga si las concentraciones de 5 y 7 bancos tienen un impacto en la rentabilidad bancaria mediante el uso de la técnica de coherencia wavelet que cubre el período 1995Q1-2017Q3. Como era de esperar, se observa que la rentabilidad bancaria y las concentraciones bancarias de 5 y 7 bancos fluctuaron significativamente en el período 2000 y 2003. En Turquía, las concentraciones bancarias causan significativamente la rentabilidad de los bancos en diferentes períodos.

Palabras clave: Coherencia wavelet, concentración bancaria, rentabilidad, Turquía..

INTRODUCTION

Researchers in developed countries have conducted many scientific and theoretical studies on bank profitability in recent years. The negative effects of bank profitability on both financial and economic stability have been discussed in those studies, while the effect of the profitability on financial crises has also been emphasized. However, only a limited number of studies have reviewed the relationship between bank profitability and bank concentrations. This study scrutinizes the causal relationship between bank profitability and bank concentration in both the short and long run by using the wavelet coherence technique. Therefore, we aim to reveal scientific findings that can assist policymakers while also closing the existing gap in the literature. Therefore, on the basis of these findings, various recommendations will be made.

Banks make a profit by earning more money than they pay in expenses and fees. A large proportion of a bank’s profit comes from interest and fees that it demands for its services. The most important fees of the banks are the interests that are paid for liabilities and deposits. As well known, the main assets of a bank are the stocks and shares in addition to credits for enterprises and other organizations. Their principal debt is the deposits and the money that they have borrowed from other banks. Bank assets can be measured as the return-on-assets and return on resources. The classical criteria of bank profitability are the return on assets (ROA), return on equity (ROE) and net interest margin (NIM). Banks use assets are for generating income. Credits, stocks and shares are the assets of a bank that are used for providing the major part of the bank’s income. However, a bank needs to have money by receiving money from other banks or by selling debt securities to collect money for credits in order to buy stocks and instruments. Banks cannot use all of their assets for monetization, primarily because they need to have sufficient funds available to meet customers’ demands to withdraw cash. These funds are stored in either safe deposit boxes or automatic teller machines (ATM). A bank, at the same time, should keep a separate account (credit loss reserves) to cover any losses incurred when customers cannot pay their credits back. The money in credit loss reserve cannot be accepted as income; accordingly, it does not contribute to profit. Equity capital profitability is the primary concern of bank owners, because this is the gain arising from investments and is not only based on the return on assets but also the total value of the assets that generate income. Moreover, a bank needs to receive payments by taking on more debt or bank capital to buy more assets. Accordingly, owners prefer to use debts instead of their own capital if they want to generate higher income, because this situation will significantly increase their revenue.

A bank uses leverage when it increases debts to pay assets; otherwise, the profitability of the bank remains limited to fees and increasing the interest rate. However, interest distribution is limited by the amount that the bank has to pay for liabilities and the amount of debt that the bank can take. Since deposits compete with investments and the banks compete with each other for depositors, banks have to pay the minimum market fee. Similarly, since there is competition with other banks, banks can receive significant amounts of money for credits and enterprises can sell debt for commercially backed securities or bonds. Thus, the interest rate is not large and the bank can make only net interest income by increasing the number of credits by using leverage compared to the amount of bank capital.

A bank needs to maintain profitability in order to survive in a competitive banking environment. Cheap funding resources should be found to make a profit. Profit is not only a result but also a tool that allows banks to succeed in a competitive environment. The focus of a bank’s management and its policies is to increase profitability. It is important for investors to pay the money back for operations to continue. Bank profitability facilitates organic and healthy growth while it also allows potential investors to invest more without receiving capital investment from stakeholders. This gain made by the bank strengthens its own capital at the same time.

Undoubtedly, elasticity in the banking sector is of particular concern to the potential profitability. Bankswork to strengthen their capital structure through self-financing. The macroeconomic and legal environments of the banking system have changed over time and the determinants of profitability have been specified. From2002 onwards, macroeconomic improvement in Turkey has played a crucial role in regaining capital while restructuring processes in the banking sector, increasing the attraction of foreign investors and the application of Basel-III have all made significant contributions to profitability. The number of banks in the Turkish banking sector decreased in the domestic crisis period-2000-2001- . The number of banks reached a peak of 79 in 2000, while the number was 68 in 1995. The number of banks went into a decline as a result of the crisis in 2001, whereby it decreased to 51 in 2005 and then 49 in 2010. The number ultimately reached 52 in 2017.

The risks caused by the global and country-wide crisis for the sector were analyzed in this research. We found that there is a positive relationship between increasing bank profitability and the size of assets of big banks based on data from the years between 1995 and 2017. The reasons for this situation are as follows: the decrease in the number of banks caused by the crisis conditions; sinking banks; syndicated banks consisting of three or four banks; and such banks being bought by other banks with the largest assets. According to the theory that the big fish eats the little one, since big banks give a large number of credits in non-crisis periods, the problems during a crisis increase because of currency rises, interest rate hikes, increased inflation, cessation of economic growth and production, and a decrease in exports.

The next section in this paper provides a general outlook on the literature covering this concept. The third part presents the relevant data. The methodological techniques used in this study can be seen in the fourth section. The final part presents the discussion and a conclusion.

LITERATURE REVIEW

The rapid increase in business operations has caused the investment and financing expenses of commercial and industrial producers to continuously increase. It is impossible to cover all those expenses with a certain amount of money. This is because there is a need for a credit system for production to continue and distribution channels should be provided. Accordingly, the level of bank profitability is directly proportional to this. It can be seen in the studies in the banking literature that there are many determinants of bank profitability. However, we have not found any studies that have reviewed the relationship between bank concentrations and bank profitability in the short and long term, which denotes the unique aspect of our research. Hence, our study creates new avenues for research on this issue in addition to closing the gap in the banking literature.

In the literature, there are many studies on the determinant factors of Non-performing Loans. Some of the related studies are as follows: Louzis et al. (2012); Hassan et al. (2014); Kasman and Kasman (2015); Tettey (2017); Korkmaz et al. (2016); Francis et al. (2018); Anastasiou et al. (2019); Demirgüç and Levie, (2006), Berger et al. (2004); Diallo and Koch (2018); Ali et al.(2018) and Albaity et al. (2019).

Cernohorsky and Prokop (2015) conducted a study and evaluated the relationship between profitability and concentration degree in banking markets in the Czech Republic, Austria, and Belgium. The Herfindahl- Hirschman index was computed based on banking market data for the period 2003 - 2012. The findings indicated that there is an inverse relationship between concentration degree and the size of the profitability of the banking sector in the Czech Republic. Based on the methods applied, they concluded that there was no relationship between concentration and profitability in the Austrian and Belgian banking sectors. Regarding the Czech Republic, as the concentration of banks increased, the profitability decreased (Cernohorsky and Prokop: 2015, pp. 40-49).

Bashir (2007) conducted a study using bank-level data from different countries. They reviewed the performance of Islamic banks in 12 Middle East / North Africa (MENA) countries, with a particular focus on the effect of their risk levels on the profitability and efficiency of the banking sector. He found that that there were remarkable differences between the profitability and risk levels of Islamic banks and their traditional counterparts. A closer examination of the data revealed that Islamic banks remain small and do not represent a serious competitive threat for other banks. Banking markets in many Islamic countries have become more integrated and open to foreign banks. Therefore, this allows Islamic banks to operate side-by-side withconventional banks. On the other hand, Islamic banks could become popular in many countries and could grow significantly in a relatively short time. However, they have remained small and less concentrated. The performances of Islamic and classical banks in the MENA region were compared. The results of the comparison did not support the assumption that the presence of Islamic banks harms the profitability and efficiency of domestic banks. However, although Islamic banks are more profitable compared to classical banks, they work inefficiently. Imperfections in Islamic banks are associated with the limited number of instruments that are used to absorb liquidity and manage the risk in short-term fund placement. Since Islamic banks remain limited with regard to the type of operation that they can finance, it seems that their portfolios are based on balance and noninterest finance. More specifically, they only focus on the retail banking sector as trade financing. Therefore, their portfolios are riskier compared to classical banks. Regarding their size and concentration levels, Islamic banks do not become a serious threat to classical banks. It is found that when the achievements in profitability and liquidity management above are considered, MENA countries can benefit from liberalizing entry restrictions for the Islamic banks. In general, as can be seen above, only opening the banking sector to Islamic banks does not solve the bank efficiency problem; service delivery should be increased or the banking sector should be transformed into an economic growth engine. Hence, serious efforts are required to enhance the banking sector (Bashir: 2007).

According to the results of the study by Ajide and Ajileye (2015), the Nigerian banking industry hasexperienced a series of important reforms including structural and behavioral adjustments. Entry into the banking sector is difficult as the structure protects existing companies from competitive pressure. This situation may cause a concentrated industry/market. The general results rejected the hypothesis of market power, which assumes that market concentration increases bank profitability. This related study reviewed the effect of market concentration on bank profitability by using time series data for the years between 1991 and 2012 from the Nigerian banking industry. The overall results rejected the hypothesis that 'as the market density increases, bank profitability increases'. Additionally, bank concentration levels are negatively affected due to crises and market vulnerabilities. Policymakers need to make reasonable predictions when making decisions regarding bank consolidation structure as this decision has numerous consequences for the future (Ajıde & Ajileye: 2015; Villalobos et al.: 2018; Hernández et al.: 2019; Ramírez et al.: 2019).

Hakimi et al. (2015) investigated whether the density of the Tunisian banking sector affected profitability for the period 1980-2009. The main results of the study revealed that density had positive effects on the profitability of Tunisian banks. Moreover, another advantage for the banks and economy was that banks in Tunisia adopted various industrial strategies (Hakimi et al.: 2015).

Olweny and Shipho (2011) determined and evaluated the effects of factors peculiar to banks. Theyresearched asset quality, liquidity, operational cost-effectiveness and income diversity on the profitability of commercial banks in Kenya. An explanatory approach was adopted by using a panel data research design to achieve the abovementioned goals. Annual accounts of 38 banks in Kenya for the period 2002-2008 were obtained from the CBK and Banking Survey 2009. They concluded that factors specific to banks were more important than market factors. The study revealed that profitable commercial banks are those that make more effort. Those banks endeavor to improve their asset quality maintain a sufficient amount of liquid assets and use income diversification strategies instead of focused strategies by increasing their capital base, lowering the operational costs and decreasing the ratio of non-performing loans. However, in terms of the descriptive analysis of these factors based on bank size, big banks show better performance than small and medium scaled banks; in other words, this better performance means outstanding profitability performance (Olweny & Shipho: 2011, pp.1-30).

Hahn (2008) researched the banking market conditions and determinants of banking profitability in Austria using panel econometric analysis. He also tested the structure-conduct-performance hypothesis, efficient structure theory, and relative market power hypothesis. Moreover, the author verified whether Austrianbanking markets are competitive. The empirical findings supported the theory that there is high competition in the Austrian banking sector, while profitability declined and banking concentration decreased.

Alagöz et al. (2016) argued that the crisis in the Turkish banking sector in 2001 caused numerous structural changes. Moreover, they argued that profitability and concentration in the Turkish banking sector are were parallel to each other between the years of 2003 and 2009. Profitability and concentration rates in the period following the global crisis moved in the same way in accordance with the general theory. It was also observed that profitability in the Turkish banking sector started to decrease after 2009.

Trujillo‐Ponce (2013) empirically analyzed the factors that determined the profitability of Spanish banksfor the period between 1999 and 2009. They concluded that the high profitability is associated with the highcredit percentage in total assets, high deposit ratio, high efficiency, and low precarious asset rate. Additionally, higher capital ratios increase the bank return if the return on assets (ROA) is used as the profitability probability. They observed that scale economy, scale or scope are not accepted as evidence for economic conditions in the Spanish banking sector. Finally, the study revealed the differences in terms of the performances of commercial and savings banks. The results provided empirical evidence related to the assumption that low-quality assets in bank balance sheets are important for banks’ characteristics. This assumption is sensible when we consider that non-performing loans and credit loss provisions are significant factors.

Acaravcı and Çalım (2013) expressed in their study that the profitability of the banking sector is the most important financial system tool for the future of the economy. They specified macroeconomic factors that affect the profitability of commercial banks in the Turkish banking sector by using the ‘Johansen and Juselius cointegration test’. The empirical findings of Acaravcı and Çalım (2013) can be summarized as follows; i) Public banks maintain liquid assets to minimize liquidity risk. Banks with private equity and foreign banks have more opportunities for investing in various short-term liquid assets; ii) Public banks should make the effort to attract more deposits as normal funding. However, deposits for private and foreign banks have an insignificant effect on profitability; iii) Credit is a measurement of the source of income of banks. Bad credits decrease profitability in banks with private equity, while the credits of foreign banks positively affect profitability; iv) Wages and commission expenses have no significant impact on profitability for all the banks; v) Diversifying big bank operations negatively affects returns; vi) As the need for external financing decreases, the profitability of public and private banks increases simultaneously. However, low capital generates high bank returns in foreign banks; vii) The banking sector is sensitive to the general development of the economy. Banks can easily collect credits and extend the time of credits via real sector growth; viii) The real exchange rate has an important effect on profitability in public and foreign banks; ix) The 2001 economic crisis had negative effect on the overall Turkish banking sector (Acaravcı & Çalım: 2013).

Data

The time-frequency dependency between NPL and the concentration rate of the size of assets of the biggest 5 and 7 banks in the Turkish banking sector was investigated by the wavelet coherence approach for the years between 1995-2017 by using quarterly data.

METHODS

We have researched bank concentrations and the time-frequency dependency of bank profitability by using the wavelet coherence technique. The original form of the wavelet approach was developed by Goupillaud et al. (1984). The primary innovation of wavelet coherence is that rather than only one dimension of time, it allows analysis using both time and frequency dimensions (Kirikkaleli & Sowah Jr: 2020; Kirikkaleli: 2020, pp.3). Therefore, we simultaneously analyzed the short and long-term causal relations between banking concentration and bank profitability in the case of Turkey. Multiscale decomposition establishes a naturalframework that enables frequency-based behavior to be displayed in order to research the connection between banking concentration and bank profitability

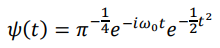

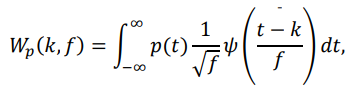

The Wavelet equation (ψ) is a part of the Morlet wavelet family (Nourani et al.: 2019a, pp. 75-84):

It is applied in series observations that have limited periods.

The two main parameters of a wavelet are time, which is represented by k, and frequency, which is represented by f.

It can be seen below (Nourani et al.: 2019b, pp. 1769-1784):

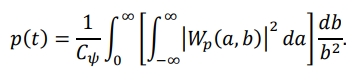

The continuous wavelet, as is shown below, is developed by time series data p (t) given as (Nourani etal.: 2019c):

The below equation shows the degenerate start times series with equation coefficient:

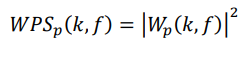

Wavelet power spectrum (WPS) provides information on the amplitude of the times series and isformulated as:

We applied the wavelet coherence approach due to the fact that it allows any correlation in compoundtime-frequency based analysis between two-time series p (t) and q (t) to be displayed.

Two time series variables are transformed into cross wavelet transformation as follows:

As suggested by Torrence and Compo (1998), Wp (k, f) and Wq (k, f) represent p (t) and q (t) CWT oftwo time series variables. Furthermore, they developed the square wavelet coherence equation as follows:

C shows time and 0 ≤ R2 (k, f) ≤ 1 is the smoothing time process. R2 (k, f) value closes to 1 and is shownby red and black if variables associated with a certain scale. Contrary, if time series have poor correlation and are shown by blue, R2 (k, f) closes to 0.

Since R2 (k, f) is a square value and it only provides information on the power of the correlation, not the direction. This is because Torrence and Compo (1998) and Pal and Mitra (2017) developed a tool to determinethe sign and magnitude of the relationship between two time series variables, which is called wavelet coherence (Kirikkaleli and Athari, 2020). The equation of wavelet coherence differential phase is as follows:

O is a real part operator while L represents an imaginary operator.

RESULTS

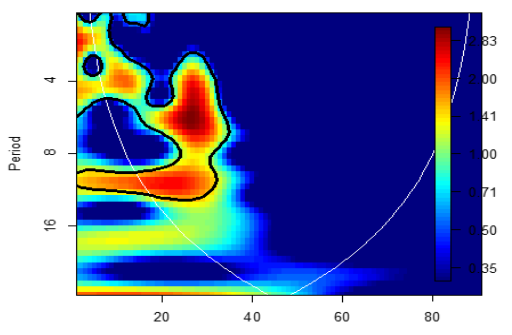

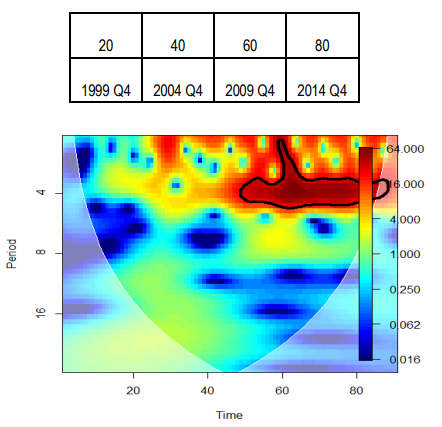

Based on the main of this paper, we explore relationship between concentrations of 5 and 7 banks and bank profitability in the Turkish banking sector over the period 1995Q1-2017Q3. To achieve this aim, we initially employed wavelet power spectrum test to capture the behavior of the time series variables. Some differences were found in terms of concentration in the Turkish banking sector before and after the crisis. One of the most important indicators in terms of determining the sizes of banks is their total assets. The findings of the analysis showed that bank concentrations as the share of assets showed an increase after the crisis. Another indicator that is a determinant of the size of assets is credit volume. With reference to the analysis findings, the concentration of big banks increased in terms of credit volume. In particular, the effect of capital increase as part of the restructuring efforts of the banks subsequently caused an increase in concentration. As shown in Figure 1, 2 and 3, there were fluctuations in profitability from 2006 to 2016, which are considered to be important. Additionally, there were also some remarkable fluctuations in bank concentrations in the short and long term between the years of 1999 and 2004.

Figure 1. Wavelet Power Spectrum for BC5

Figure 2. Wavelet Power Spectrum for BC7

Figure 3. Wavelet Power Spectrum for Profitability

DISCUSSION

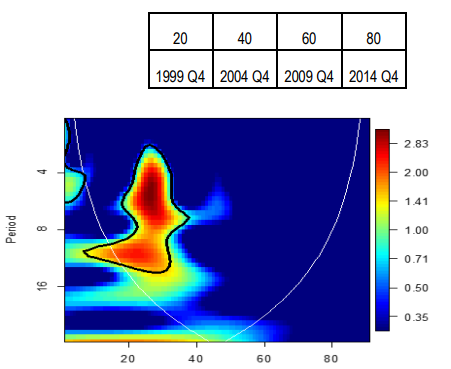

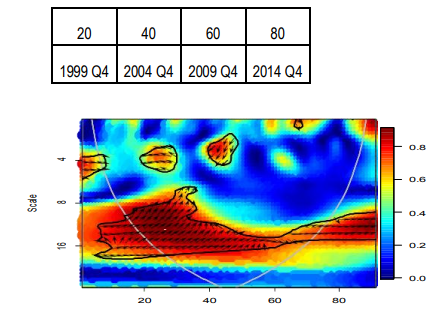

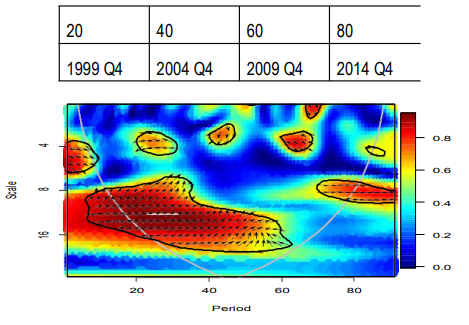

The present study uses wavelet coherence approach to capture the long and short run linkage between bank concentration and profitability in the banking sector. Figure 4 and 5 shows wavelet coherence between profitability and BC7 and wavelet coherence between profitability and BC5, respectively. In terms of the concentrations of 5 banks, bank concentration, as demonstrated by the right-up arrows, caused profitability in the short and long term between the years of 1999 and 2009. Profitability in the long run led to bank concentrations after the crisis between the years of 2010 and 2012; there was a positive correlation between profitability and bank concentration in the medium term for the period between 2013 and 2017. Bank concentrations caused profitability for 7 banks in the medium and long run for the period between 1999 and 2009. However, profitability caused concentration in the short run for the period from 2005 to 2006. Based on our observations, the 2000 banking crisis, 2001 devaluation, 2007-2008 global crises represent periods when the correlations were particularly strong.

Figure 4. Wavelet Coherence between Profitability and BC5

Figure 5. Wavelet Coherence between Profitability and BC7

CONCLUSION

We used quarterly data for the period between 1995 and 2017 to investigate the linkage between bank concentrations of 5 and 7 banks and profitability in the Turkish banking sector. A comparison of these data for the same period indicated that the results were the same for both 5 and 7 banks. There were fluctuations in profitability from 2006 to 2016, which are considered to be important. Additionally, there were also some remarkable fluctuations in bank concentrations in the short and long term between the years of 1999 and 2004.

In terms of the concentrations of 5 banks, bank concentration, as demonstrated by the right-up arrows, caused profitability in the short and long term between the years of 1999 and 2009. Profitability in the long run led to bank concentrations after the crisis between the years of 2010 and 2012; there was a positive correlation between profitability and bank concentration in the medium term for the period between 2013 and 2017. Bank concentrations caused profitability for 7 banks in the medium and long run for the period between 1999 and 2009. However, profitability caused concentration in the short run for the period from 2005 to 2006. Based on our observations, the 2000 banking crisis, 2001 devaluation, 2007-2008 global crises represent periods when the correlations were particularly strong.

Bank profitability showed a positive increase parallel to bank concentrations as a result of the increase in the concentrations of the size of assets based on new structuring and consortia or by banks taking on partners in banking sector crises periods. In summary, the change in bank concentrations during the crisis periods caused the banks’ profitability levels to change. Profitability is for a necessity for banks are recommended to adopt forward-looking policies, perform stress tests and develop 5-year profitability plans to prepare for possible crises considering the results of this study.

BIODATA

ŞÜKRÜ UMARBEYLI: Has been working in the banking and finance sector for 16 years as Asbank Terminal Branch Manager. After graduating from the Department of Mathematics and Computer at Eastern Mediterranean University in 2001, he completed his MBA in 2002, and in 2020, he completed his PhD in Business Administration at the European University of Lefke. He also writes columns and TV shows on economy and finance.He has many book chapters and articles on economics and finance.

DERVIS KIRIKKALELI: Is the current senior lecturer at the European University of Lefke. He holds a BSc in Economics from Eastern Mediterranean University (CY). He is a University of Stirling (UK) alum, where he completed his MSc and PhD in Banking and Finance. His research area is macroeconomics, environmental economics and financial economics. Currently he writes articles about the concepts of economic stability, financial stability and bank stability in emerging markets.

BIBLIOGRAPHY

ACARAVCI, S & ÇALIM, A (2013). Katılım bankalarının kârlılığını etkileyen içsel faktörler: Türkiye örneği.

AJIDE, FM & AJILEYE, JO (2015). “Market concentration and profitability in Nigerian banking industry:Evidence from error correction modeling”. International Journal of Economics, Commerce and Management, 3(1), pp.1-8.

ALAGÖZ, M, AKALIN, US & CEYLAN, O (2016). “The relationship between concentration and profitability in Turkish banking sector”. JOEEP: Journal of Emerging Economies and Policy, 1(1), pp11-18.

ALBAITY, M, MALLEK, RS & NOMAN, AHM (2019). “Competition and bank stability in the MENA region: The moderating effect of Islamic versus conventional banks”. Emerging Markets Review, 38, pp.310-325.

ALI, MSB, Intissar, T & Zeitun, R (2018). “Banking concentration and financial stability. New evidence from developed and developing countries”. Eastern Economic Journal, 44(1), pp.117-134.

ANASTASIOU, D, LOURI, H & TSIONAS, M (2019). “Nonperforming loans in the euro area: A re core– periphery banking markets fragmented?”. International Journal of Finance & Economics, 24(1), pp.97-112.

BASHIR, AHM (2007). “Islamic banks participation, concentration and profitability: Evidence from MENA countries”. In Economic Research Forum Working Paper, 4(2).

BERGER, AN, DEMIRGÜÇ-KUNT, A, LEVINE, R & HAUBRICH, JG (2004). “Bank concentration andcompetition: An evolution in the making”. Journal of Money, Credit and Banking, pp.433-451.

CERNOHORSKY, J & PROKOP, V (2016). “The Relationship of Concentration and Profitability in Banking Markets”. In 15th International Conference on Finance and Banking in Silesian University. [Conference proceedings]

DIALLO, B & KOCH, W (2018). “Bank concentration and Schumpeterian growth: theory and international evidence”. Review of Economics and Statistics, 100(3), pp.489-501.

FRANCIS, B, HARPER, P & KUMAR, S (2018). “The effects of institutional corporate social responsibility on bank loans”. Business & Society, 57(7), pp.1407-1439.

GOUPILLAUD, P, GROSSMANN, A & MORLET, J (1984). “Cycle-octave and related transforms in seismic signal analysis”. Geoexploration, 23(1), pp.85-102.

HAHN, FR (2008). “Testing for profitability and contestability in banking: Evidence from Austria”. International Review of Applied Economics, 22(5), pp.639-653.

HAKIMI, A, HAMDI, H & DJLASSI, M (2013). “Testing the concentration-performance relationship in the Tunisian banking sector”.

HASSAN, HU, ILYAS, M & REHMAN, CA (2014). “Quantitative study of bank-specific and social factors of non-performing loans of Pakistani Banking Sector”. International Letters of Social and Humanistic Sciences, 43, pp.192-213.

HERNÁNDEZ DE VELAZCO, Judith .J., CHUMACEIRO HERNANDEZ, Ana C. , RAVINA RIPOLL, R & DELRIO, Nacira (2019). “Gestión ciudadana como corresponsabilidad del desarrollo social. Construcción desde la política pública en Colombia”. Opción, Año 35, Regular No.89-2: 706-730.

KARVINÁ: OPF V KARVINÉ, pp. 40-49.

KASMAN, S & KASMAN, A (2015). “Bank competition, concentration and financial stability in the Turkish banking industry”. Economic Systems, 39(3), pp.502-517.

KIRIKKALELI, D (2020). “Does political risk matter for economic and financial risks in Venezuela?”. Journal of Economic Structures, 9(1), pp.3.

KIRIKKALELI, D & SOWAH JR, JK (2020). “A wavelet coherence analysis: nexus between urbanization and environmental sustainability”. Environmental Science and Pollution Research International.

KORKMAZ, Ö, ERER, D & ERER, E (2016). “Bankacılık Sektöründe Yoğunlaşma İle Finansal Kırılganlık Arasındaki İlişki: Türkiye Örneği (2007-2014)”. Journal of Accounting & Finance, 6(9).

LOUZIS, DP, VOULDIS, AT & METAXAS, VL (2012). “Macroeconomic and bank-specific determinants of non- performing loans in Greece: A comparative study of mortgage, business and consumer loan portfolios”. Journal of Banking & Finance, 36(4), pp.1012-1027.

NOURANI, V, DAVANLOU TAJBAKHSH, A, MOLAJOU, A, & GOKCEKUS, H (2019b). “Hybrid wavelet-M5model tree for rainfall-runoff modeling”. Journal of Hydrologic Engineering, 24(5), 04019012.

NOURANI, V, MOLAJOU, A, TAJBAKHSH, AD, & NAJAFI, H (2019c). “A wavelet based data mining technique for suspended sediment load modeling”. Water Resources Management, 33(5), pp. 1769-1784.

NOURANI, V, TAJBAKHSH, AD, & MOLAJOU, A (2019a). “Data mining based on wavelet and decision tree for rainfall-runoff simulation”. Hydrology Research, 50(1), pp. 75-84.

OLWENY, T & SHIPHO, TM (2011). “Effects of banking sectoral factors on the profitability of commercial banks in Kenya”. Economics and Finance Review, 1(5), pp.1-30.

PAL, D & MITRA, SK (2017). “Time-frequency contained co-movement of crude oil and world food prices: A wavelet-based analysis”. Energy Economics, 6(2), pp.230-239.

RAMÍREZ MOLINA, R., MARCANO, M., RAMÍREZ MOLINA, R., LAY RABY, N & HERRERA TAPIAS, B(2019). “Relationship Between social intelligence and resonant leadership in public health Institutions”. Opción. Revista de Ciencias Humanas y Sociales, 35(90), pp.2477-9385.

TETTEY, PL (2017). Determinants of nonperforming loans of microfinance Companies in Ghana (Doctoral dissertation, University of Cape Coast).

TORRENCE, C & COMPO, GP (1998). “A practical guide to wavelet analysis”. Bulletin of the American Meteorological society, 79(1), pp.61-78.

TRUJILLO‐PONCE, A (2013). “What determines the profitability of banks? Evidence from Spain”. Accounting& Finance, 53(2), pp.561-586.

VILLALOBOS ANTÚNEZ, JOSÉ VICENTE & GANGA CONTRERAS, FRANCISCO. 2018. “Tecnoempresa yTecnocimiento: Una Perspectiva desde la Bioética Empresarial”. Revista Fronteiras: Journal of Social, Technological and Environmental Science. Vol. 7, No. 3: 214-230. Unievangélica Centro Universitario, (Brasil).