Artículos

Corruption Prevention Using the Concept of Single Identity Number in Taxation Management Data Bank

Prevención de la corrupción mediante el concepto de número de identidad único en elbanco de datos de gestión fiscal

H. POERNOMO hpoernomook@gmail.com

B.R. SARAGIH bintan.saragih@uph.edu

H.S BUDI

T. SUPRIADI me@taufiqs.com

H. POERNOMO hpoernomook@gmail.com

B.R. SARAGIH bintan.saragih@uph.edu

H.S BUDI

T. SUPRIADI me@taufiqs.com

Corruption Prevention Using the Concept of Single Identity Number in Taxation Management Data Bank

Utopía y Praxis Latinoamericana, vol. 26, no. Esp.1, pp. 167-181, 2021

Universidad del Zulia

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International.

Received: 05 December 2020

Accepted: 10 February 2021

Abstract: This study examines the relationship between self- assessment policy, Single Identity Number (SIN), and tax management data bank with tax revenue and corruption prevention. It is used the descriptive analysis with an inductive method in which the researchers describe the state of the object under study, collect and analyze data to provide a systematic, logical explanation. It is showed that SIN can simplify the population database system, ensure the data population's integrity and accuracy, and integrate all financial and non-financial data. The results imply that using a Single Identity Number can improve tax revenue and corruption prevention.

Keywords: Corruption prevention strategy, Single Identity Number, SIN, taxation management data bank..

Resumen: Este estudio examina la relación entre la política de autoevaluación, el Número Único de Identidad (SIN) y el banco de datos de gestión tributaria con los ingresos tributarios y la prevención de la corrupción. Se utiliza un análisis descriptivo con un método inductivo en el que los investigadores describen el estado del objeto en estudio, recopilan y analizan datos para brindar una explicación lógica y sistemática. Se muestra que el SIN puede simplificar el sistema de base de datos de población, garantizar la integridad y precisión de la población de datos e integrar lo financiero y no financiero. Los resultados implican que el uso de un número de identidad único puede mejorar los ingresos fiscales y la prevención de la corrupción.

Palabras clave: Estrategia de prevención de la corrupción, número de identidad único, SIN, banco de datos de gestión fiscal..

INTRODUCTION

Taxes are the primary source of state revenue, which continues to increase every year. At present, not less than 82.5% of state revenue is derived from the tax sector (Ichsan, Choirunnisa, & Haryadi: 2018). As of August 2019, the realization of tax revenue reached IDR801.16 trillion from the target of IDR1,577.56 trillion or around 50.78%. This achievement was still lower than the realization of August 2018, which reached IDR799.46 trillion or around 56 14%. The realizations of September, October, November, and December 2018 were consecutively 63.26%, 71.39%, 79.82%, and 92.41% or equivalent to IDR1,315.93 trillion from the target of IDR1,424 trillion. Meanwhile, in 2017 the realization of tax revenue reached IDR1,151.5 trillion from the target of IDR1,283.6 trillion or around 89.71%. The development of tax in the last three years has a relatively similar pattern, reflecting no innovations to ensure tax revenue.

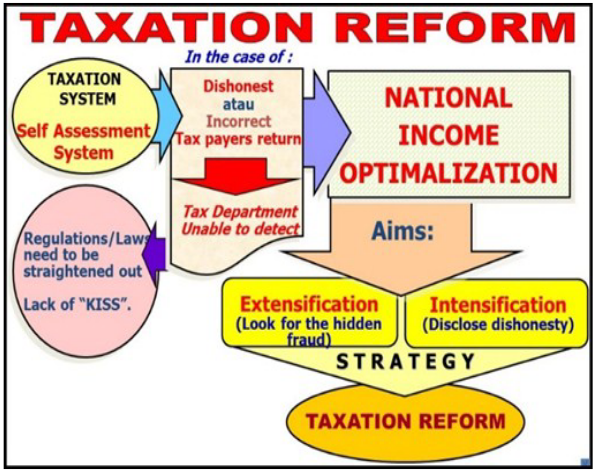

The government should not rely only on intuition, experience, and subjectivity to determine tax revenue's strategic decisions. It should be based on a system such as a self-assessment system policy is one of the systems issued by the government (Baxter et al., 2018). The self-assessment system concept is that taxpayers are given the trust to calculate and pay their taxes. Implementing the self-assessment system obligation is outlined in the Tax Return (SPT) (Anjanni: 2019, pp. 1-10). Taxpayers are obliged to report every additional economic ability and net wealth in their tax return form. The taxpayer submits a completed and signed form to the DGT regularly and within a determined time limit.

Therefore, the tax return form must be documented systematically and safely. Indonesia's taxationsystem currently does not support an integrated and online taxation information and monitoring system, so data and facts are not transparent. Some regulations prohibit access to financial transaction data for tax purposes (Montalvo et al.: 2020, pp. 103520-103526; Berentsen et al.: 2016, pp. 303-323).

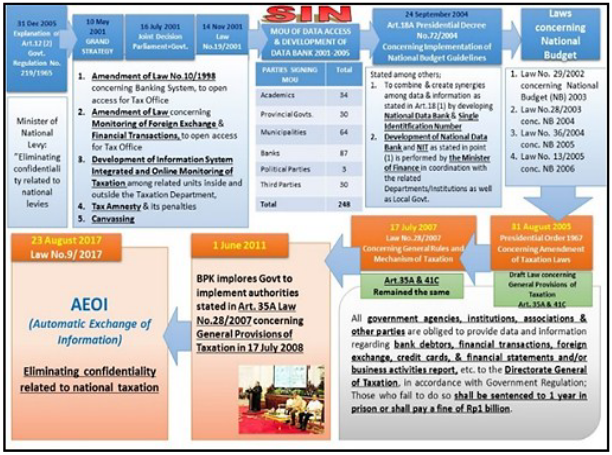

In 2001, a grand strategy of tax administration reform and modernization provided a fundamental change in all aspects of taxation. The strategy covered morals, ethics, the integrity of tax apparatuses, tax policy, service to taxpayers, and supervisory reforms (Paulin: 2019, pp. 5-38). The tax apparatus's moral and ethical reforms are carried out by strengthening the tax officers' spiritual side through religious and social activities. Integrity reform is carried out through internal consolidation efforts, external oversight cooperation with the Ombudsman, complaint channels, and establishing a code of ethics.

Tax policy reform is pursued through an amendment of the Taxation Law. Service reform is carried out by providing taxpayers' convenience in obtaining information and services from an account representative. Speedy service is supported by a modern, online, and real-time administration system such as e- registration, e-filling, e-payment, e-mapping, and smart mapping.

Supervision reforms are carried out in the form of 1) intensification or revealing dishonesty in filling out tax returns, and 2) extensification or increasing the number of taxpayers by searching for hidden potentials in the management data bank, e-mapping and smart mapping applications, single identity number (SIN), and law enforcement.

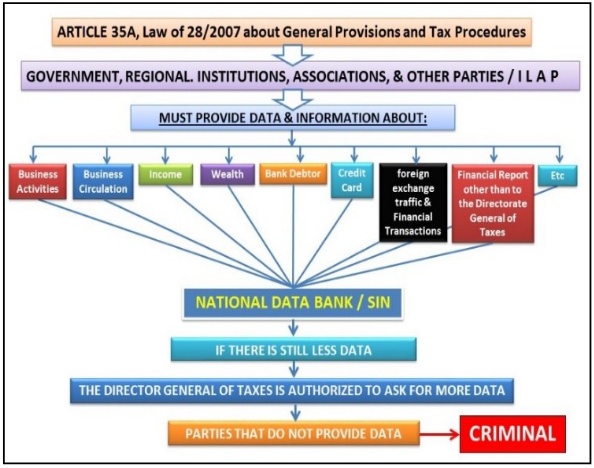

The basis for the implementation of SIN in taxation is stated in Law No. 28 of 2007 (UU KUP), Article No. 35A and 41C. Each government agency, institution, association, and other parties must provide data and information relating to taxation to the DGT, the provisions of which are governed by government regulations. Furthermore, Article 41C states that every person who intentionally fails to fulfill the obligations mentioned earlier shall be sentenced to a maximum imprisonment of one year or a maximum fine of IDR 1 billion. The General Provisions and Tax Procedures Law underwent the fourth amendment to Law No. 16 of 2009, which proves that the self-assessment system is powerful if supported by a management data bank and recognized by all parties.

SIN system is the only practical way for the taxation sector to create data connectivity so that tax monitoring can be done effectively, thus preventing corruption in Indonesia.

Figure 1. SIN Scheme as Anti-Corruption Prevention

Information technology (IT) plays a significant role in supporting the implementation of SIN. The law provides space for law enforcers (Police, Attorney General's Office, and Corruption Eradication Commission) to obtain and use electronic information to strengthen evidence of corruption cases (Le & Doan: 2019, pp. 100600-100660). The use of IT also affects audit quality conducted by BPK as a state finance external auditor and the Supreme Audit Institution of Indonesia (Supriadi et al.: 2019a, pp. 1760- 1769; Supriadi et al.: 2019b, pp. 475-493). Indeed, IT is the backbone of corruption prevention.

Against that background, problems with implementing SIN as a strategy to prevent corruption inIndonesia can be explained by answering the following questions:

-

What is SIN's arrangement as an information management system for implementing regulations in Indonesia's taxation field?

-

How can the implementation of SIN as part of the Tax Management Data Bank be used as a strategy to prevent corruption in Indonesia?

-

What is the ideal setting for SIN in the Tax Management Data Bank as part of a strategy to prevent corruption in Indonesia?

LITERATURE REVIEW

a) State authority in the context of Administrative Beschikking

In the administrative context, the state authority, beschikking, is indeed inseparable from legality's underlying principle. Legality governs every state's action towards its citizens and forms the basis of state and government administration. The technologies can also improve taxpayer services, achieve tax compliance, and implement new audit mechanisms, especially considering the large volume of data generated (Faúndez-Ugalde et al.: 2020, pp. 105400-105441). The substance of legality is an authority or the ability to carry out legal actions. H. D. Stoit said, "authority is an understanding derived from the law of government organizations, which can be explained as a whole of rules relating to the subject of public law in public relations." Authority is not the same as power (Macht). Power reflects only the right to do or not to do, while Authority reflects rights and obligations. The rights mean the power to regulate and manage itself, while the obligations mean the power to run the government in an orderly mandate as a whole (Faúndez- Ugalde et al.: 2020, pp. 105400-105441).

b) General Review of State Finances

The development of state finance law began in the late twentieth century when the state began to interfere in its citizens' affairs. Such a type of state that distinguishes it from the classical state is called the modern welfare state.

Good governance will be well implemented when state finance management needs to be carried out in a professional, open, and accountable manner, following the Constitution's basic rules. From the four statutory provisions (Martinez & Cooper: 2017, pp. 6-20; Alawattage & Azure: 2019, pp. 102070-102075). State finance is defined as rights and obligations that have monetary value in the form of money or goods owned by the state. State finance can also be interpreted as government wealth obtained from revenues, debt, loans, spending, fiscal policy, and monetary policy.

c) Responsive Theory as a Strategy to Prevent Corruption

The Responsive Theory from Philip Nonet and Selznick, in a book titled "Law & Socialization in Transition: Toward Responsive Law," is used to describe the state's authority to formulate the SIN as an effort to prevent corruption or tax evasion (Nonet & Selznick: 2003). Someone who has had a tax id number means it has been registered as a taxpayer ready to fulfill their tax obligations. Many benefits both individuals and business entities, for instance, as a prerequisite for opening a bank account, apply for a credit proposal, conduct business transactions (Andreas & Savitri: 2015, pp. 163-169). It explains that developing countries will reach a legal development level as developed countries if they followed the developed countries' path (Di Pietro & Butticè: 2020, pp. 101540-101543). Progressive Theory (Buckenmaier et al.: 2020) is the sociology of law, which was previously introduced by Maxmillian Weber. There are similarities and relationships between Satjipto Rahardjo's Progressive Theory and Nonet- Selznick's Responsive Theory. Progressive Theory rejects law normatively, while Responsive Theory recognizes that the state has the Authority to determine social interests changes through law. Law should provide more than just legal procedures. It must be competent, fair, and recognize the public's wishes and commit to achieving substantive justice (Dekker & Breakey: 2016, pp. 187-193). The Responsive Theory in the context of this paper is the responsive legal order as a strategy to prevent criminal acts of corruption through the SIN in a taxation management data bank.

d) The Concept of SIN

Population registration is recording biodata and events and the issuance of documents in identification, card, or certificate(Dekker & Breakey: 2016, pp. 187-193). Population registration can be ineffective due to a lack of coordination among government agencies. Different agencies require residents to register the same data multiple times with different methods (Mohan & Razali Raja Yaacob: 2004, pp. 217-227). As a result, population data lacks validity. The Single Identification Number (SIN) can overcome this problem as a reference for accurate population data.

In the taxation sector, the SIN is different from the Taxpayer Identification Number (NPWP), which has been in effect since the tax self-assessment system in 1984. In principle, each taxpayer will be given a unique number that applies nationally and remains attached to the taxpayer despite address movements. Changes only occur in the Tax Office (KPP) code where it is registered. This KPP Code Number is added behind the unique number (Polzer Ngwato: 2012, pp. 561-572; Lee et al.: 2018, pp. 88-98).

METHODOLOGY

The approach used in this qualitative research is the socio-legal approach. Qualitative research is based on methods that investigate a social phenomenon and human problems. In this study, the researchers make a complex picture, examine words and reports from the respondents' views, and conduct studies on natural situations (Tonon: 2015, pp. 1-10; Bleiker et al.: 2019, pp. S4-S8). According to Peter Mahmud Marzuki, socio-legal research places law as a social phenomenon. Law is only seen from the outside while focusing on individuals' behavior or society concerning the law (de Oliveira Rodrigues et al.:2019, pp. 12-30, Benzmüller et al.: 2020, pp. 103348-103350).

Socio-legal research conducts textual studies in which articles in regulations, laws, and policies can be critically analyzed, the meaning and implications for legal subjects explained, and various new combined methods of legal and social science developed (Weber: 2020, pp. 105370-105380; Blandy & Hunter: 2012). The socio-legal approach aims to clarify issues about legal aspects and explore empirical realities in society. Law is not only seen as a normative entity that is independent or theoretical but is also seen as a part of the social system that is related to other social variables (Hswen et al.: 2020, pp. 113140-113142; Albiston & Leachman: 2015, pp. 1-10). The qualitative method expects to find hidden meanings behind the objects and subjects under study. It enables the understanding of people personally and sees them as they express their world views. It focuses on the general principles that underlie phenomena in human life or socio-cultural patterns using the community's culture (Rodrigo & Palacios: 2021, pp. 120390-120394). This study combines socio-legal with an empirical juridical approach to analyze the workings of law in society.

RESULTS

The data analysis method used is descriptive analysis with the inductive method. The researchers describe the state of the object under study, collect and analyze data to provide a systematic, logical explanation, draw up a picture of the problem under study, then conclude to answer the problems.

a) Legal products regarding SIN in the field of taxationThe Indonesian Tax Reform is supported by the Program to Form Taxation Management Data Bank into a National Management Data Bank through the SIN.

Figure 2. Tax Reform

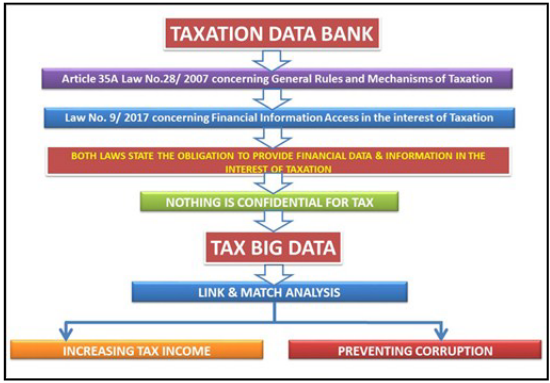

Article 35A Law No. 28 of 2007 provided the DGT with the trust to own and manage the Tax Management Data Bank and mitigate and balance the risk of Indonesia's self-assessment system. No other government organs have a more significant power than the DGT. Only to DGT, all parties in Indonesia are required to submit data/ information related to taxation, whether it is credit card bills, electricity, water usage, telephone, or car buyer data.

The trend of taxation is moving towards more transparency, away from banking secrecy, also the secrecy of the capital market and insurance industry. Ten years after Article 35A was passed, Law No. 9 of 2017 further strengthened the DGT's bargaining position to open access to financial data.

This new law was born due to the Automatic Exchange of Financial Information (AEoFAI) agreement sponsored by the Organization for Economic Co-operation (OECD) to increase financial data transparency. Indonesia, although not a member of the OECD, was explicitly invited to participate in the project. Indonesia was not the only country to ratify the law related to access to financial information for taxation.

This new law allows DGT to peek at the financial data of bank customers, capital markets, insurance, and other financial institutions according to international tax treaties, which were previously untouchable.

The picture below shows SIN's journey to obtain legal certainty from 2009 to 2017.

Figure 3. SIN Road Map

b) SIN as an integral part of information systems

SIN is a tool for integrating data that can be utilized to improve the nation’s welfare. In developing a SIN- based system, there are principles as applied by other countries:

-

SIN is a unique identification within the national boundaries.

-

SIN is developed without the risk of duplication.

-

SIN format is easy to remember because it is used for various systems.

-

SIN can be the basis on which other dimensions can be attached.

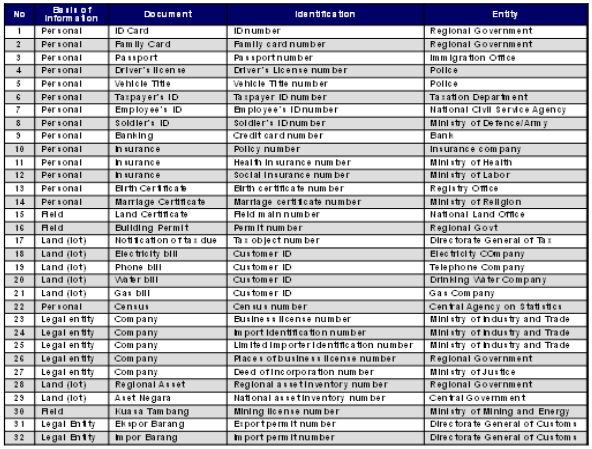

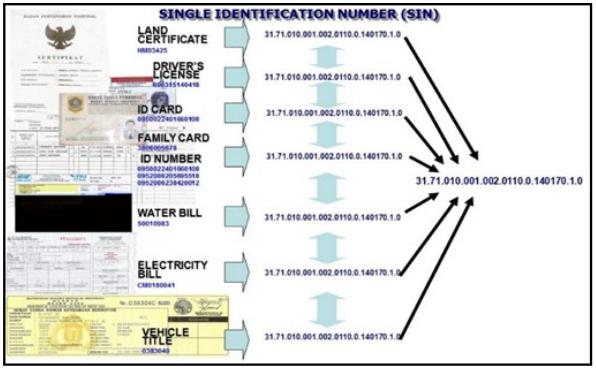

In Indonesia, there are at least 32 unique identity numbers issued by different institutions. If a physical card is issued for each one, it will make an Indonesian’s wallet thick because a person needs to carry at least 16 cards. Besides the ID card (KTP), there is the driver’s license (SIM), vehicle registration (STNK), credit cards, tax ID number (NPWP), employee ID number (NIP Cards), insurance cards, and the list goes on.

Meanwhile, in developed countries, such as the United States, one simply needs to remember the Social Security Number.

Dozens of scattered data must be put together so that supervision can take place by system as multiple data will cause overlapping and data leakages. In Indonesia, a person can acquire more than one KTP easily. The Population Administration Act, which the Ministry of Home Affairs drafted, admits that it has not developed a single identity

-

The identity of a person is connected with the real world, usually with organizations or other people. SIN is designed to replace all existing identification numbers and has the nature of:

-

Unique, no multiple identities;

-

Standard, identity structure is the same nationally;

-

Complete, covering data throughout Indonesia;

-

Permanent, may not change;

-

Integrated.

Figure 4. Unique IDs in Indonesia

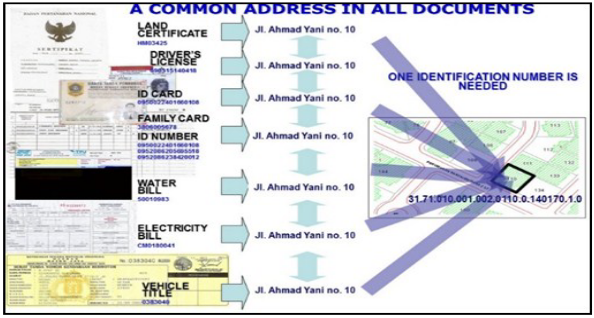

SIN, which serves as a "unifying code," is the best approach, uniting various population information systems owned by agencies without overhauling the agency's database's primary form. SIN is issued by the central government for each citizen, while the local government’s role is to register and record the population data. Collaboration between both governments is needed to include the SIN on every citizen’s identity card in Indonesia.

Figure 5. SIN Unifying Concept (1)

Figure 6. SIN Unifying Concept (2)

Here are the functions of SIN:

-

Simplifying the population database system (with consolidation and virtualization of storage, server, and database);

-

Ensuring integrity and accuracy of population data (the identity of the population can be through fingerprints, retina eyes, blood vessels in the palms, etc.);

-

Being a reference number for all kinds of purposes (business, education, health, public facilities, taxes, etc.);

-

Integrating all databases (including jobs, education, expertise, etc., to improve the education system).

c) SIN as an integral part of the Tax Management Data Bank is a Strategy to Prevent and Eradicate Corruption

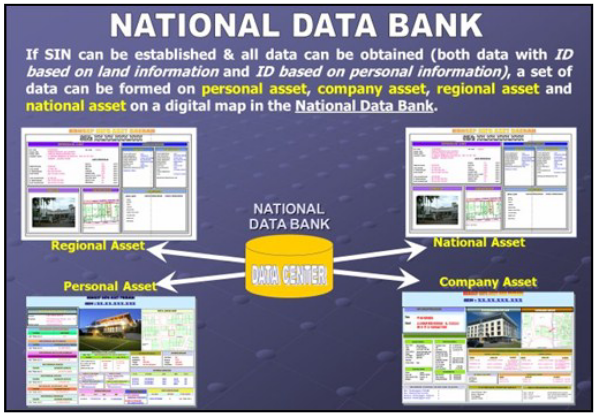

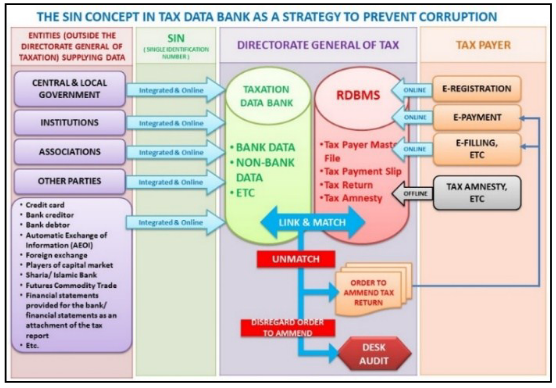

SIN has almost a similar concept as that of Social Security Number in the United States. SIN automatically integrates financial and non-financial data into the nationally centralized Taxation Management Data Bank and matches transactions against tax returns. This mechanism enables SIN to detect fraud automatically, create voluntary compliance, force honesty, and curbing corruption.

Figure 7. National Management Data Bank

DISCUSSION

SIN can be realized only if it is supported by adequate IT infrastructure to link and match the data scattered in various agencies. After the link and match occur, then consolidation will occur, and finally, synergy.

The authors believe that SIN will enable automatic corruption detection without repression. In most cases, corruption is revealed only by chance, for example, from a confession or information from somebody. With SIN, corruption can be discovered by the system.

It should not be challenging to realize SIN in Indonesia. Almost all institutions have digital databases. For example, the National Land Agency has land data; banks have financial transactions; Police have vehicle ownership data; Directorate General of Customs and Excise has export-import data.

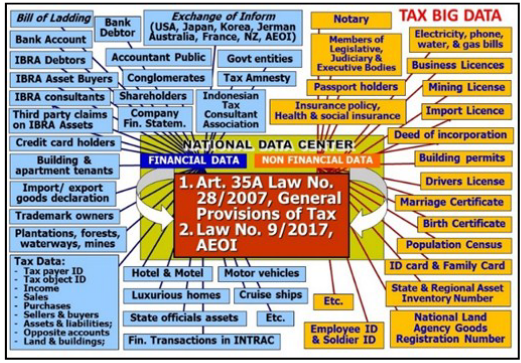

As SIN integrates various data, including tax payment data, it eliminates secrets by building an asset information system, a Taxation Management Data Bank, a centralized management data bank that consists of financial and non-financial data. Taxation Management Data Bank contains data from various institutions such as the Corruption Eradication Commission (KPK), the Audit Board of the Republic of Indonesia (BPK), Attorney General's Office, Police Department (Polri), the Ministry of Law and Human Rights (Kemenkum- HAM), State-Owned Enterprises (BUMN), National Land Agency (BPN), Regional Governments (Pemda), Indonesian Financial Transaction Reports and Analysis Center/INTRAC (PPATK), Bank Indonesia (BI), and others.

Figure 8. Taxation Management Data Bank

All of this data is ready to be juxtaposed with data of citizens’ activities. The various citizens’ data may contain the flow of money from corrupt practices or other illegal actions. SIN combines official data from government and non-government institutions and data from citizens’ activities on an ongoing basis.

At this point, the SIN mechanism will carry out comparisons or audits by linking and matching the data.

The system will reveal any discrepancies. Data mismatch will indicate a potential violation or crime, or deviation from rules and regulations.

By linking taxpayers' transaction data with their transaction counterparts, DGT will know the correct amount of tax returns, making it a useful tool to test taxpayers' honesty when implementing tax self- assessment. It can even calculate the total tax returns that should be. So, with SIN, Indonesia's tax ratio can be expected to rise.

SIN has more significant benefits for DGT in which tax officers are facilitated in their work, minimizing examination activities, putting more effort into service and counseling.

The Taxation Management Data Bank will reduce contact between DGT officers and taxpayers aselectronic checks can be performed at the office. This way, the examination can run faster, easier, and cheaper. In some instances, the officer will still need to meet taxpayers for a physical inspection or confirm certain information.

The amount of data examined is also more massive. Examiners can conduct population checks usingdata connected online, on-time, and in real-time with the Taxation Management Data Bank.

SIN will also benefit taxpayers as data transmission automation makes it easier and faster to send documents, making follow-ups on the examination speedier results, thus reducing tax hassle.

Figure 9. The Distribution of Data and Information Systems in Indonesia

The picture above shows the distribution of financial and non-financial data and information systems in Indonesia in the government and private sectors linked to each other.

SIN can act as a corruption prevention system built nationally, as an implementation strategy and action plan, a resource management system, and coordination, monitoring, and evaluation system. With SIN, there will be no more hidden, late, inaccurate, irrelevant data. Corrupt practices will be put to a halt, such as companies providing different financial statements for different purposes like banking, tax, and shareholders purposes.

Figure 10. SIN’s Concept in the Taxation Management Data Bank as a Strategy to Prevent Corruption

In the spirit of Making Indonesia 4.0, SIN is a "bridge" between various information systems used by Ministries and taxpayers. Most taxpayers started switching to electronic recording of financial transactions. So, DGT examiners must be able to handle electronic data during inspection.

d) SIN as a systemic approach to prevent corruption

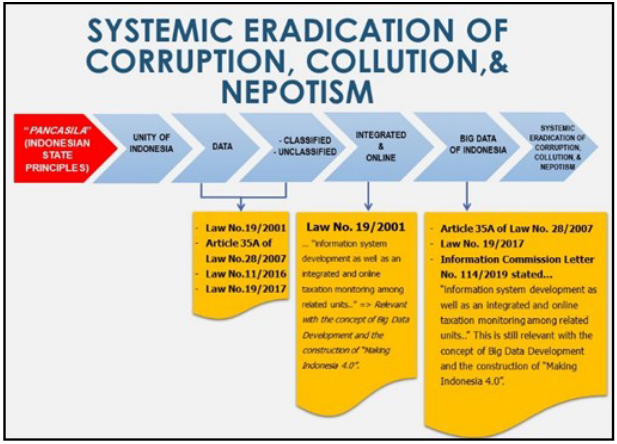

Irregularities in tax payments and reporting hurt state revenues. Misuse of state money by unscrupulous officials results in enormous losses for the state. Therefore, sound data management, such as the Taxation Management Data Bank, is essential to promote accountability. It can be utilized for audit activities. With more and more data being received through SIN, DGT can detect corruption or irregularities earlier, making taxpayers think twice before cheating, reducing the opportunity for corruption. After all, systemic corruption must be overcome with a systemic approach too.

Figure 11. SIN’s Concept in Corruption Eradication

Using SIN, DGT will map significant and risky transactions based on their size and substance, which will help DGT identify potential taxpayers. With the data, DGT officials can create working papers faster. Some procedures that are usually carried out during field inspection can be performed earlier during the planning phase. For example, a comparison of evidence of cash receipts or disbursements with checking account data. During the field inspection, SIN is utilized for accessing other databases related to the inspection.

The Directorate of Data and Information and the Directorate of Information and Communication Technology are two units in charge of the Taxation Management Data Bank. The DGT leaders must be watchful and courageous in utilizing the data to detect potential tax sources. Otherwise, the DGT’s function will be undermined as they will only perform data administration.

CONCLUSION

Indonesia’s national goal can only be realized if there is synergy, cooperation, and commitment of all nation elements. A strategic effort is required to strengthen Indonesia's tax system. Tax is pivotal since more than 80 percent of the country's revenue comes from it. All stakeholders must provide support to assure tax revenues; however, this awareness is still weak.

The authors continue to disseminate the conceptual framework and the 10-year Grand Strategy of SIN (2001 to 2010) to achieve the constitutional mandate to create a just and prosperous society for the Indonesian people. Justice and prosperity can only be achieved if corruption can be eradicated systemically. The taxation system in Indonesia adopts the self-assessment system. Without the link and match mechanism, it will never be sure the taxpayers' total additional economic capacity and additional net assets. The link and match process requires full integration and an online process to compare the taxpayer's reports with the facts. SIN automatically integrates financial and non-financial data and forms the Taxation Management Data Bank, matching transaction data with tax returns. This mechanism enables the automatic detection of fraud and improves voluntary compliance in the system. The world is entering an era of tax transparency. In Indonesia, the General Provisions and Tax Procedures Law and the AEOI Law have removed various confidentiality constraints. The next step should be to build the Taxation Management Data Bank, an important strategy to increase tax revenue. The authors encourage all stakeholders and authorities to build the Tax Management Data Bank, implementing the laws prudently. An ideal tax self-assessment system requires a balance between giving taxpayers trust in determining the amount of tax return and strengthening the capacity of tax officials to track the accuracy of the reported amounts. SIN can build that balance, creating openness between the two parties while at the same time pushing efforts to eradicate corruption systemically in Indonesia.

Implementation of the Single Identity Number must be immediately implemented in all regions of the Republic of Indonesia. Other countries, especially developing countries, should also immediately implement the same thing to reduce the possibility of corruption and increase tax revenues. Future research needs to be carried out in developing countries and relies on tax revenue as the primary state revenue.

BIODATA

H. POERNOMO: is a candidate of Doctor of Law Program at Pelita Harapan University. He once held the positions of Director General of Tax, Board of Strategic Analysis, and Chairman of the Audit Board of the Republic of Indonesia. He is a lecturer and researcher at the Doctoral Program of Law, at Indonesia College of Taxation, Jakarta, Indonesia. His qualifications include Taxation, Tax Management, and Investigative Audit.

B.R. SARAGIH: is a Professor of Law at the Pelita Harapan University Jakarta Indonesia. He is deeply qualified in Law. His qualification in Criminal Law, Private and Commercial Law, Administrative and Constitutional Law, International Law, Land and Agrarian Law, Tax Law, Competition law, Regulatory theory and Health Law.

H.S. BUDI: is an Associated Professor. He is Head of Lector and a researcher at the Pelita Harapan University. He is also a lecturer and researcher of Law in several other universities in Indonesia. His qualification in Employment and industrial law, Corporate governance and social responsibility, Intellectual property, Corporate law and finance.

T. SUPRIADI: holds a Doctoral Degree in Accounting from University of Padjadjaran, Bandung, Indonesia. His qualifications include Information System Audit, Information System Management, Tax Management, Forensic Accounting, and Investigative Audit. He is also a lecturer and researcher at Indonesian College of Taxation and University of National Development, Jakarta, Indonesia.

BIBLIOGRAPHY

ALAWATTAGE, C, & AZURE, J, D,-C, (2019). "Behind the world bank’s ringing declarations of “social accountability”: Ghana’s public financial management reform". Critical perspectives on accounting, pp. 102070-102075.

ALBISTON, C, R, & LEACHMAN, G, M, (2015). "Law as an instrument of social change".

ANJANNI, I. L. P., HAPSARI, D. W., & ASALAM, A. G. (2019). "Pengaruh penerapan self assessment system, pengetahuan wajib pajak, dan kualitas pelayanan terhadap kepatuhan wajib pajak (Studi pada Wajib Pajak Orang Pribadi Non Karyawan di KPP Pratama Ciamis Tahun 2017)". Jurnal Akademi Akuntansi (JAA), 2(1), pp. 1-10.

BAXTER, J, D, DEMPSEY, J, MEGONE, C, & LEE, J, (2012). Real Integrity: Practical solutions for organisations seeking to promote and encourage integrity: London, UK.

BENZMÜLLER, C, PARENT, X, & VAN DER TORRE, L, (2020). "Designing normative theories for ethical and legal reasoning: LogiKEy framework, methodology, and tool support". Artificial Intelligence, 287, pp. 103348-103350.

BERENTSEN, A, HUBER, S, & MARCHESIANI, A, (2016). "The societal benefit of a financial transaction tax". European Economic Review, 89, pp. 303-323.

BLANDY, S, & HUNTER, C, (2012). "Socio-Legal Perspectives".

BLEIKER, J, MORGAN-TRIMMER, S, KNAPP, K, & HOPKINS, S, (2019). "Navigating the maze: Qualitative research methodologies and their philosophical foundations". Radiography, 25, pp. S4-S8.

BUCKENMAIER, J, DIMANT, E, & MITTONE, L, (2018). "Effects of institutional history and leniency on collusive corruption and tax evasion". Journal of Economic Behavior & Organization.

DE OLIVEIRA RODRIGUES, C, M, DE FREITAS, F, L, G, BARREIROS, E, F, S, DE AZEVEDO, R, R, & DEALMEIDA FILHO, A, T, (2019). "Legal ontologies over time: A systematic mapping study". Expert Systems with Applications, 130, pp. 12-30.

DEKKER, S, W, & BREAKEY, H, (2016). "Just culture:’Improving safety by achieving substantive, procedural and restorative justice". Safety science, 85, pp. 187-193.

DI PIETRO, F, & BUTTICÈ, V, (2020). "Institutional characteristics and the development of crowdfunding across countries". International Review of Financial Analysis, 71, pp. 101540-101543.

FAÚNDEZ-UGALDE, A, MELLADO-SILVA, R, & ALDUNATE-LIZANA, E, (2020). "Use of artificialintelligence by tax administrations: An analysis regarding taxpayers’ rights in Latin American countries". Computer Law & Security Review, 38, pp. 105400-105441.

HSWEN, Y, QIN, Q, WILLIAMS, D, R, VISWANATH, K, BROWNSTEIN, J, S, & SUBRAMANIAN, S, (2020)."The relationship between Jim Crow laws and social capital from 1997–2014: A 3-level multilevel hierarchical analysis across time, county and state". Social Science & Medicine, 262, pp. 113140-113142.

ICHSAN, M, CHOIRUNNISA, W, & HARYADI, G, (2018). "Measuring successful implementation of knowledge management system: A case study on ministry of finance of the republic of Indonesia". Paper presented at the 2018 6th International Conference on Cyber and IT Service Management (CITSM).

LE, A,-T, & DOAN, A,-T, (2020). "Corruption and financial fragility of small and medium enterprises: International evidence". Journal of Multinational Financial Management, 57, pp. 100600-100660.

LEE, T, W, HOM, P, EBERLY, M, & LI, J, (2018). "Managing employee retention and turnover with 21st century ideas". Organizational dynamics, 47(2), pp. 88-98.

MARTINEZ, D, E, & COOPER, D, J, (2017). "Assembling international development: Accountability and the disarticulation of a social movement". Accounting, Organizations and Society, 63, pp. 6-20.

MOHAN, J, & YAACOB, R, R, R, (2004). The malaysian telehealth flagship application: a national approach to health data protection and utilisation and consumer rights". International Journal of Medical Informatics, 73(3), pp. 217-227.

MONTALVO, J, G, PIOLATTO, A, & RAYA, J, (2020). "Transaction-tax evasion in the housing market". Regional Science and Urban Economics, 81, pp. 103520-103526.

NGWATO, T, P, (2012). "Together apart: migration, integration and spatialised identities in South African border villages". Geoforum, 43(3), pp. 561-572.

NONET, P, SELZNICK, P, & KAGAN, R, A, (2017). "Law and society in transition: Toward responsive law". Routledge.

PAULIN, A, (2019). "Understanding the public apparatus: opportunity, dominion, threat". Smart City Governance, 2(1), pp. 5-38.

RODRIGO, L, & PALACIOS, M, (2021). "What antecedent attitudes motivate actors to commit to the ecosystem of digital social innovation?". Technological Forecasting and Social Change, 162, pp. 120390- 120394.

SAVITRI, E, (2015). "The effect of tax socialization, tax knowledge, expediency of tax ID number and service quality on taxpayers compliance with taxpayers awareness as mediating variables". Procedia-social and behavioral sciences, 211, pp. 163-169.

SUPRIADI, T, MULYANI, S, SOEPARDI, E, M, & FARIDA, I, (2019a). "Influence of auditor competency in using information technology on the success of E-audit system implementation". EURASIA Journal of Mathematics, Science and Technology Education, 15(10), pp. 1760-1769.

SUPRIADI, T, SOEPARDI, E, M, & FARIDA, I, (2019b). "The use of information technology of eaudit system on audit quality". Opción, 35(89), pp. 475-493.

TONON, G, (2015). "Qualitative studies in quality of life: Methodology and practice". 55, pp.1-10 .

WEBER, R, H, (2020). "Socio-ethical values and legal rules on automated platforms: The quest for a symbiotic relationship". Computer Law & Security Review, 36, pp. 105370-105380.