Artículos

Research Audit Quality and its Impact on an Organization's Reputation

Calidad de la auditoría de investigación y su impacto en la reputación de una organización

NAJMATUZZAHRAH najmatuzzahrah74@gmail.com

SRIHADI WINARNINGISH srihadi.winarningsih@unpad.ac.id

SRI MULYANI sri.mulyani@unpad.ac.id

BAHRULLAH AKBAR bahrullah.akbar@unpad.ac.id

NAJMATUZZAHRAH najmatuzzahrah74@gmail.com

SRIHADI WINARNINGISH srihadi.winarningsih@unpad.ac.id

SRI MULYANI sri.mulyani@unpad.ac.id

BAHRULLAH AKBAR bahrullah.akbar@unpad.ac.id

Research Audit Quality and its Impact on an Organization's Reputation

Utopía y Praxis Latinoamericana, vol. 26, no. Esp.1, pp. 207-221, 2021

Universidad del Zulia

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International.

Received: 05 December 2020

Accepted: 10 February 2021

Abstract: The Audit Board of Indonesia (BPK), as an independent audit institution, was mandated by the 1945 Constitution to perform investigative audits to declare state losses. In the process of exercising its authority, BPK encounters issues related to its own organizational reputation. The objective of this research is to identify and examine how the auditor’s independence affects the quality of an investigative audit and its effect on the credibility of the BPK. The main finding of the study is that the auditor’s independence as a value has a positive impact on the BPK’s reputation, which is represented by the quality of investigative audits.

Keywords: Independence, investigative audit, audit quality, organizational reputation, BPK, corruption..

Resumen: La Junta de Auditoría de Indonesia (BPK), como institución de auditoría independiente, recibió el mandato de la Constitución de 1945 de realizar auditorías de investigación para declarar pérdidas estatales. En el proceso de ejercer su autoridad, BPK encuentra problemas relacionados con su propia reputación organizacional. El objetivo de esta investigación es identificar y examinar cómo la independencia del auditor afecta la calidad de una auditoría de investigación y su efecto sobre la credibilidad de la BPK. El principal hallazgo del estudio es que la independencia del auditor como valor tiene un impacto positivo en la reputación de BPK, que está representada por la calidad de las auditorías de investigación.

Palabras clave: Independencia, auditoría investigativa, calidad de auditoría, reputación organizacional, BPK, corrupción..

INTRODUCTION

Investigative audits conducted by the Audit Board of Indonesia (BPK) face challenges in supporting the eradication of corruption in Indonesia. Some of the challenges involve providing accurate and accountable investigative audit reports and sustaining the reputation of the organization as an institution with authority to perform investigative audits to declare state losses. To respond to the emerging challenges, the BPK has been given sufficient capacity. For instance, in Law Number 15 of 2006 concerning the Audit Board of Indonesia, Article 11 Letter C states the authority of the BPK providing expert opinion in the judicial process, in particular regarding state losses resulting from corruption. Moreover, Law Number 15 of 2004 on the Audit of State Financial Management and Accountability provides the BPK with authority to conduct investigative audit procedures to declare state losses. The purpose of the audits is to disclose the existence of fraud and irregularities according to the laws and regulations and to declare the state losses incurred.

The Supreme Court of the Republic of Indonesia continued to acknowledge the BPK’s particular authority by issuing the Circular Letter of the Supreme Court (SEMA) Number 4 of 2016, which declared the BPK to be the constitutionally mandated institution to declare state losses resulting from corruption. Since the issuance of the SEMA, the BPK has received a significantly larger number of requests from law enforcement agencies to perform audits to declare state losses. The BPK accepted 510 requests to assess state losses from law enforcement agencies in various regions of Indonesia during the period from 2017 to 2018. Although supported by the Law and the SEMA, the BPK still faces a number of challenges in implementing its authority.

With the granted authority, the BPK is challenged to produce high-quality output. In the context of investigative audits, one of the quality assessments can be undertaken using the accuracy and adequacy of the evidence presented in the audit report to support the state/local losses declared. In addition, the quality of an audit is measured by the ability to provide a firm conviction to the Panel of Judges regarding the state losses occurring as the result of discrepancies from the laws and regulations.

Multiple factors may affect the audit quality. According to Whittington & Pany, (2010), one of the factorsthat influence the quality of an audit is the specialized auditor. They stated that when an auditor becomes a specialist or an expert in a particular industry, he or she will be able to produce a higher-quality audit than an auditor who is not specialized in the specific industry of the client. This is mainly because a specialized auditor has considerable experience with and a deep understanding of the client’s industry. In some cases in which the auditor is not specialized, the quality of the audit might decrease because of the highly biased opinions of the auditor when concluding the audit evidence. Another factor that may affect the audit quality is technology. Supriadi et al., (2019 argued that, with the support of technology, auditors are able to make strategic decisions based on specific devices or systems since they do not rely solely on intuition, experience, and subjectivity factors.

In addition to the challenge of producing quality audit report output, the BPK encounters issues concerning its organizational reputation. There are several cases in which the BPK’s credibility has been disputed. One example occurred when the BPK was reported to the Indonesian Police Authority regarding the results of the BPK’s investigative audit of the Century Bank. The report stated that the BPK’s audit results were considered to be weak and unclear. Iskandar Sitorus of Indonesian Audit Watch (IAW) considered the results of the BPK’s investigative audit of the Century Bank to be invalid as it was more of an audit with a specific purpose than an investigative audit. The quality of the audit results was incomplete because the BPK could not infer anyone’s guilt in the Century Bank’s case. The audit even failed to mention the details of the figures clearly. Another example that cast doubt on the BPK’s reputation was the verdict given to the former BPK’s Principal Auditor in a bribery case regarding an Unqualified Audit Opinion given to the Ministry of Villages, Development of Disadvantaged Regions, and Transmigration’s Financial Report. The BPK’s reputation was called into question, even more when the defendant was sentenced to seven years of imprisonment.

Despite being challenged for its reputation and audit quality, independence in performing audits remains a key feature that affects the audit quality and the institution’s reputation. (Knechel: 2016, pp. 215-223) stated that auditors’ independence is a factor that strongly influences the quality of investigative audits (Sembiring et al.: 2020; Abubakar and Obansa: 2020; Alam and Shakir: 2019; Bhatti and Akram: 2020). auditors’ independence also contributes to the organizational reputation (Truong et al.: 2020). This paper will explore the relationship between auditors’ independence, audit quality, and the BPK’s reputation.

Based on the background described, the research questions can be formulated as follows:

- 1. How much influence does independence have on the quality of investigative audits?

- 2. How much influence does the quality of investigative audits have on the BPK’s reputation?

- 3. How much influence does independence have on the BPK’s reputation?

- 4. How much influence does independence have on the BPK’s reputation through investigative auditquality?

METHODOLOGY

This research uses descriptive and causal–explanatory methods by performing hypothesis testing. Descriptive methods, according to (Sekaran & Bougie: 2016), are conducted to ascertain and describe the characteristics of variables of interest in a given situation. Meanwhile, causal–explanatory studies, as (Eden et al.: 2020) stated, are conducted to determine whether one or more variables describe the cause or effect of one or more yield variables.

The examination mainly focuses on the influence of independence on the quality of investigative audits and its implications for the BPK’s reputation. The variable operationalization is the following:

- 1. Auditors’ independence: independence in audit program planning, independence in audit implementation, and independence in reporting.

- 2. Investigative audit quality: using the auditor’s competency dimensions, implementation of investigativeaudits, and the reporting of investigative audits.

- 3. The BPK’s reputation: using firm-wide perception dimensions and audit team perception.

This research is conducted in the environment of the Law Enforcement Agency Task Force throughout Indonesia, and the respondents are investigators from the Police of the Republic of Indonesia (Polri), the Attorney General of the Republic of Indonesia (Kejagung), and the Corruption Eradication Commission (KPK) (Sari et al.: 2020, pp. 212-220), who have collaborated in investigating cases through investigative audits conducted by the BPK throughout Indonesia as selected research populations (Sarwono et al.: 2018, pp. 79-89).

The research population is 127 units consisting of 71 task forces in the Police Department, 55 units in the Prosecutor’s Office, and one task force in the KPK. Due to the difference in characteristics between one task force and another, the population set out in this study is 94 units composed of 267 investigators. The instruments in this study are questionnaires and the structured question interview.

This study can be classified as survey research, as it uses systematic interviews as a measurementmethod to collect information. The questions in the interviews were carefully chosen and organized, and posed accurately to each respondent (Eden et al.: 2020). The survey was conducted using questionnaires with differential semantic scale data and measured on the basis of an attitude scale using the semantic approach.

In quantitative research, according to (Sugiyono: 2015), the methods used to analyze the data will involve descriptive statistics and inferential statistics. The research hypotheses will be evaluated following the approach of structural equation modeling (SEM).

RESULTS

Descriptive Statistics Analysis

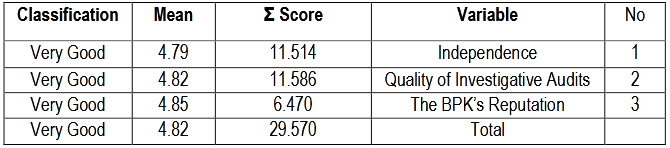

The variables in this study consist of auditors’ independence, the quality of investigative audits, and the organization’s (the BPK’s) reputation. Based on 267 interviewees’ responses, the descriptive statistical analysis provided data on average scores and the response classification for each variable as set out in Table 1. Each variable has total scores and is classified as “very good.” The total score for all the variables is 29,570, with an average score of 4,82, and is marked as “very good.”

Source: Data processing results (2020)

Confirmatory Factor Analysis (CFA)

The model conformity is measured using confirmatory factor analysis (CFA). CFA is carried out to determine the unidimensionality of the indicators that describe a factor or a formed variable. The CFA of each variable is described as follows:

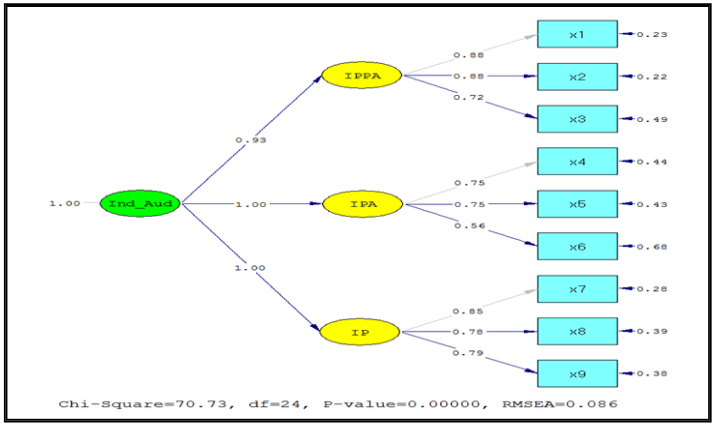

1- Independence Variable (X)

Independence as a variable (X) is measured through three dimensions consisting of nine indicators. The CFA test results using the second-order model of the auditors’ independence variable are shown in Figure 1.

Figure 1. CFA Test of the Independence Variable (Standardized)

According to Figure 1, no dimension has a factor loading value of more than 1. However, the value of the RMSEA is still more than 0.08. Thus, re-specification is necessary. Below are the CFA test results after the re-specification of the independent variable.

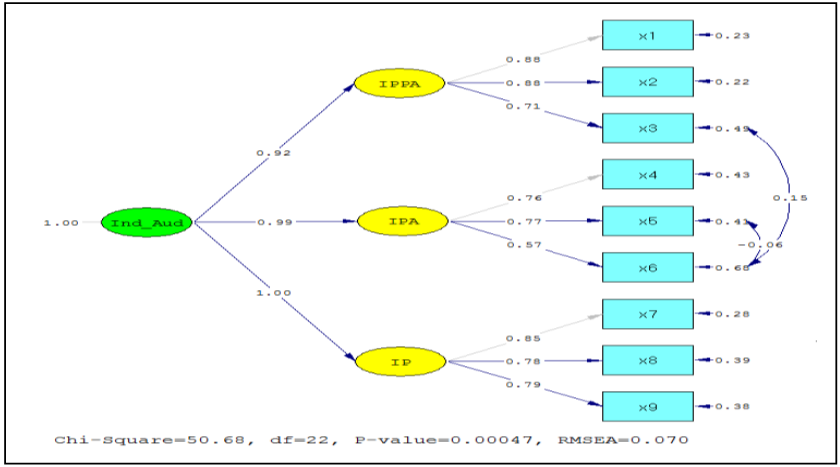

Figure 2. CFA Test of the Re-specification of the Independence Variable (Standardized)

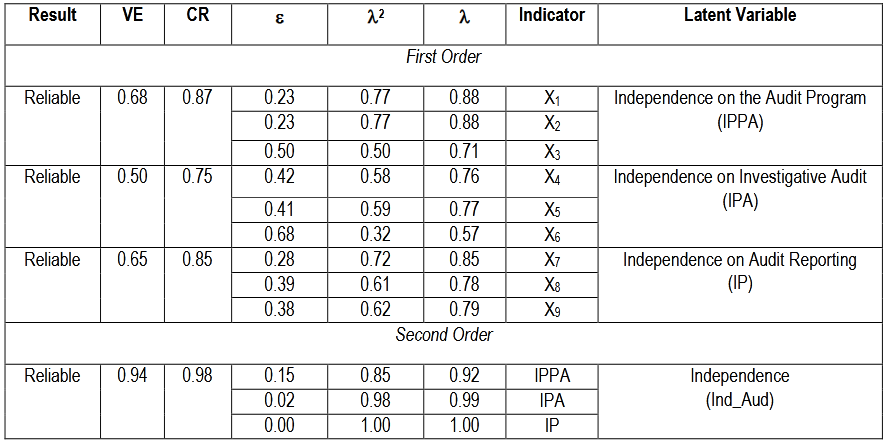

Based on the CFA test results in Figure 2, all the indicators have a standard factor load value of more than 0.5, so it can be concluded that each of these indicators is valid as an independent variable measuring instrument with a value of RMSEA = 0.070 < 0.08. The details of the standard factor load value are as follows:

Source: Data processing results (2020)

Based on the second-order test results of the independent variable, all the dimensions have a factor loading above 0.5; hence, all the dimensions are valid as independence variable measurements. The IAR dimension has the highest factor loading value; consequently, the IAR dimension reflects the strongest degree of independence as a variable. However, the factor loading of the IAP dimension shows the lowest value; therefore, it is the weakest dimension in reflecting independence as a variable.

The CR value is 0.98 > 0.7, and the VE value is 0.94 > 0.5; therefore, all the independence dimensionsare reliable and consistent in measuring independence as a variable.

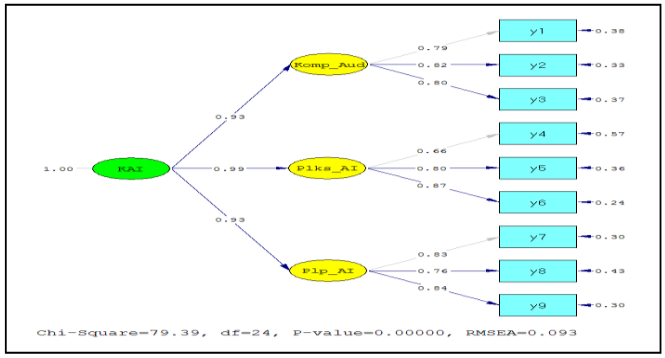

1- The Quality of Investigative Audits Variable (Y)

The quality of investigative audits (Y) is measured using three dimensions consisting of nine indicators. The following figure shows the CFA test results using the second-order model of the quality of investigative audits variable.

Figure 3. CFA Test of the Quality Variable (Standardized)

Based on the CFA test results shown in Figure 3, all the indicators have a standard factor load value of more than 0.5; however, they have an RMSEA value of 0.093 > 0.08. Therefore, re-specification of thequality variable (KAI) is required. Below are the CFA test results after the re-specification of the quality variable.

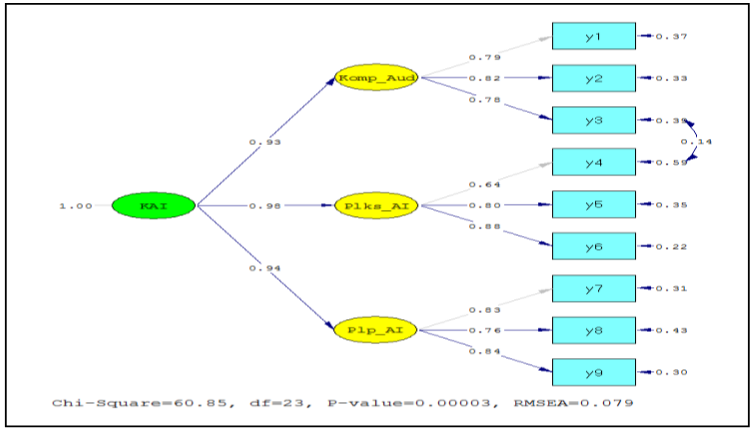

Figure 4. CFA Test of the Respecification of the Quality Variable (Standardized)

The CFA test results in Figure 4 show that all the indicators have a standard factor load value of more than 0.5; hence, each indicator is valid as a measure of the quality (KAI) variable with a value of RMSEA =0.079 < 0.08. The details of the standard factor load value are as follows:

Source: Data processing results (2020)

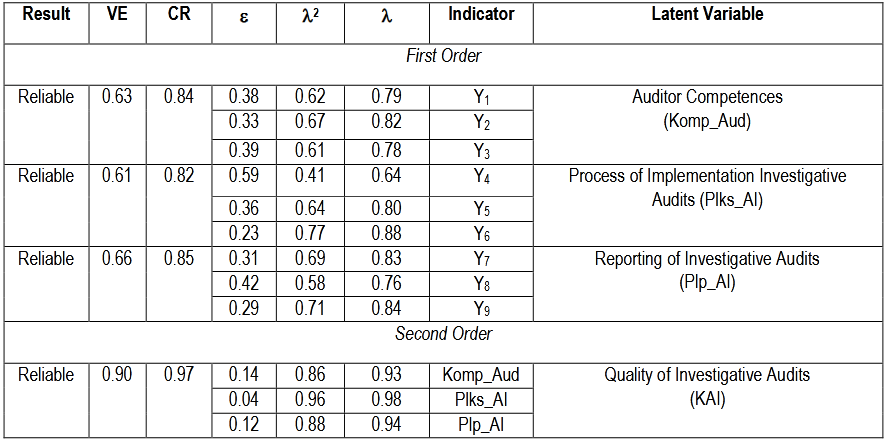

Based on Table 3, the first-order results for the AC, PIIA, and RIAR dimensions suggest that all the indicators have a factor loading above 0.5. Therefore, all the indicators are valid for measuring each dimension. All the CR values are above 0.7, and the VE values are above 0.5, meaning that all theindicators are reliable. Furthermore, the results show that all the indicators are consistent in measuring each dimension.

Referring to the second-order test result of the quality variable shown in Table 3, it can be noted that allthe dimensions have factor loadings above 0.5; hence, all the dimensions are valid in measuring the quality variable. The PIAA dimension’s factor loading has the highest value, so it is the strongest dimension in reflecting the quality variable. However, the lowest value of the factor loadings is that of the AC dimension. Hence, it is the weakest dimension in reflecting the quality variable. The CR value is 0.97 > 0.7 and the VE value is 0.90 > 0.5; consequently, all the indicators are reliable.

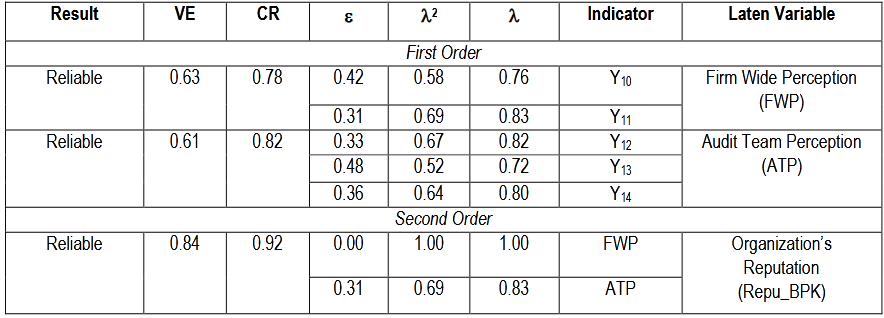

1- The BPK Reputation Variable (Z)

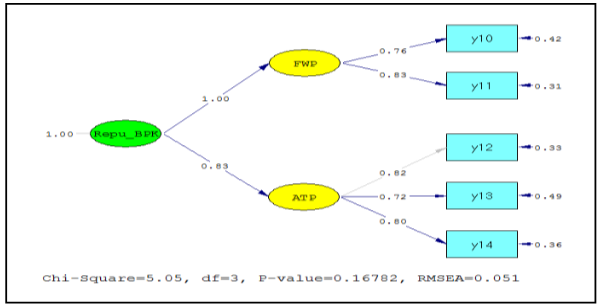

The organization’s reputation variable is measured in two dimensions consisting of five indicators. The following figure is the CFA test result using the second-order model of the reputation variable.

Figure 5. CFA Test of the Reputation Variable (Standardized)

Based on the CFA test results in Figure 5, all the indicators have a standard factor load value greater than 0.5; thus, it can be inferred that each indicator is relevant as a reputation variable. The descriptions of the standard factor load value can be found in the table below.

Source: Data processing results (2020)

The results in the above table indicate that the first-order results for the FWP and ATP dimensions suggest that all the indicators have a factor loading greater than 0.5. Thus, all the indicators are valid for measuring each dimension. All the CR values are above 0.7, and the VE values are above 0.5. Therefore,all the indicators are reliable. The results also indicate that all the indicators can be used for measuring each dimension.

The second-order test results of the reputation variable, shown in Table 4, suggest that all the dimensions have a factor loading greater than 0.5. Therefore, all the dimensions are valid in measuring the reputation variable. The FWP dimension’s factor loading has the highest value; thus, it is the strongest dimension in reflecting the reputation variable. On the other hand, the lowest value of the factor loadings is that of the ATP dimension. Thus, the ATP dimension is the weakest dimension in reflecting the reputation variable. The CR value is 0.92 > 0.7 and the VE value is 0.84 > 0.5; consequently, all the indicators are reliable in measuring the organization’s reputation variable.

Test Results of the Full Structural Model

The estimated structural model of the relationships between latent variables through the path coefficient test is presented in Table 5.

Source: Data processing results (2020)

Table 5 indicates that, in the first substructure, the independent variable (X) exerts an influence of 0.86 on the quality of investigational audits (Y). The remaining 0.14 is affected by variables other than the three independent variables. In the second substructure, it can be noted that the independent variable (X) and the quality of investigational audits (Y) exert an influence of 0.92 on the organization’s reputation (Z). Therefore, in addition to these variables, there are other variables that affect 0.08 of the reputation variable. From the coefficient value of the path, the most dominant variable influencing the organization’s reputation variable (Z) is the quality of investigative audits (Y), with a path value of 0.66, followed by the independence variable (X), with a path value of 0.21. The statistical test results are then summarized to understand how the exogenous variable independence affects the organization’s reputation variable through the quality of investigative audits variable. The results are presented in Table 6 below.

Source: Data processing results (2020)

The interpretation of the results is as follows:

1- The coefficient value of independence (X) with the organization’s reputation (Z) through the quality of investigative audits (Y) is 0.44 in a positive direction. This suggests that the greater the auditor’s independence mediated by the level of the quality of the investigative audit, the better the organization’s reputation.

2- Based on the path score, it can be noted that the effect of auditor independence on the organization’s reputation through the quality of investigative audits is 0.23 higher than the direct effect of auditor independence on the organization’s reputation of 0.21. It can therefore be concluded that the quality ofImportar listainvestigative audits is able to improve the auditor’s independent relationship with the organization’s reputation.

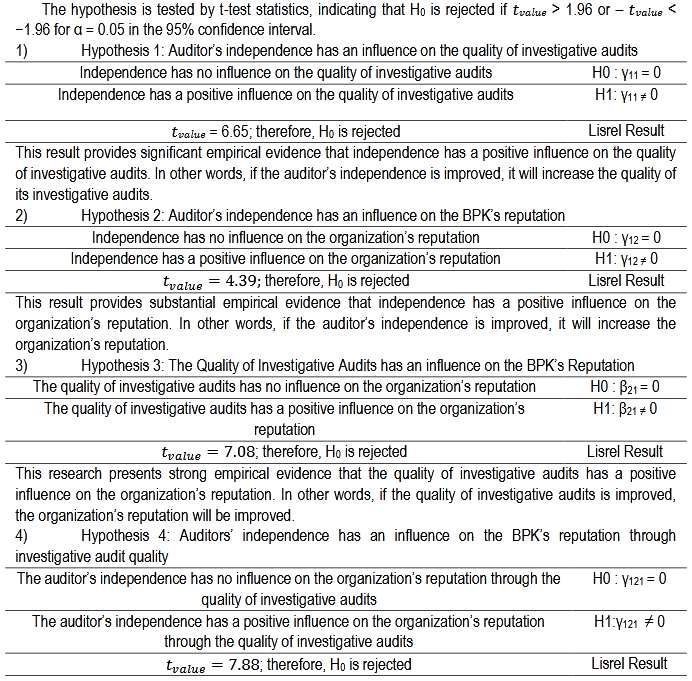

Hypothesis Testing

This research provides empirical evidence that an auditor’s independence has a positive influence onthe organization’s reputation through the quality of investigative audits.

DISCUSSION

1- The Influence of Auditors’ Independence on the Quality of Investigative Audits

The results of this study provide empirical evidence that the auditor’s independence contributes to the improvement of the quality of investigative audits. It can also be interpreted as indicating that the quality of investigative audits can be improved by increasing the independence of the auditor.

The IPPA, IPA, and IP dimensions can affect the quality of investigative audits based on the indicators used. The improvement of the investigative audit quality is reflected in the degree of authority that the auditors have in determining alternative techniques, procedures, and alternative procedures to be used in the examination (IPPA), the independence of determining key areas, and carrying out activities in obtaining audit evidence, as well as the freedom of the auditors from personal interests that may impede the implementation of audits (IPA) and the freedom to reveal fraud and its impact as well as the related parties to be disclosed in the audit reporting (IP).

The three dimensions of auditor independence in this study are confirmed to affect the quality of investigative audits. The results of this study correspond to the results of previous studies that have suggested that auditors’ independence is one of the factors that influence the quality of investigative audits (Knechel: 2016, pp. 215-223). Therefore, this study confirms that auditors’ independence can affect the quality of investigative audits (Ernstberger et al.: 2020, pp. 218-244).

2- The Influence of Auditors’ Independence on the Organization’s Reputation

The hypothetical test results obtained by testing the significance of the coefficient path in the structural models show that auditors’ independence has a positive influence on an organization’s reputation. It is reflected by the value of 4.39, which exceeds the threshold of 1.96 at the significance level of 95%. The findings from this study show that each dimension affects the organization’s reputation differently. Based on the level of each standard factor load value, the dimensions that best reflect auditor independence are IP (1), then IPA (0.99), and IPPA (0.92).

The results of this study provide empirical evidence that auditors’ independence affects the reputation of the organization. It can also be interpreted as showing that the organization’s reputation can be improved by improving each of the auditor’s independence dimensions. The IPPA, IPA, and IP dimensions can affect the organization’s reputation based on the indicators used. The organization’s reputation can be improved by setting out an independent audit program, audit techniques, and audit procedures (IPPA). Furthermore, independence in determining the key areas of examination, obtaining audit evidence, and removing the personal interests that impede auditing can also boost an organization’s reputation (IPA). The indicators of the IP dimension, such as independence in disclosing irregularities or fraud, establishing the value of the state loss based on the audit evidence, and having the autonomy to disclose the parties related to fraud, can be utilized to improve the organization’s reputation.

The three dimensions of auditors’ independence in this study positively affect the reputation of the organization. The results of this study are consistent with the results of previous studies that have indicated that auditors’ independence is one of the factors affecting the reputation of the organization (Hohenfels & Quick: 2018, pp. 1-49).

3- The Influence of the Quality of Investigative Audits on the Organization’s Reputation

The results of the hypothesis testing of the significance of the path coefficient in the structural model show that the quality of investigative audits has a positive influence on the reputation of the organization. It is reflected by a value of 7.08, exceeding the threshold of 1.96 at the significance level of 95%. The quality of investigative audits has three dimensions: auditor competence (Komp_Aud), the implementation of investigative audits (Plks_AI), and investigative audit reporting (Plpr_AI). Based on the level of each standard factor load value, the dimensions that best reflect the quality of investigative audits are Plks_AI (0.98), Plpr_AI (0.94), and Komp_Aud (0.93) consecutively.

The results of this study provide empirical evidence that the quality of investigative audits affects the organization’s reputation. They can also be interpreted as indicating that the organization’s reputation can be increased by improving the quality of investigative audits through the implementation of each of their dimensions. The dimensions of auditor competency, implementation of investigative audits, and investigativeaudit reporting affect the organization’s reputation according to the indicators used. Having the certification of expertise in the investigative audit field, improving the ability and experience in carrying out investigative audits (auditor competence), improving the understanding of audit risks, following the accepted standards, organizing infrastructure that supports the performance of investigative audits (implementation of investigative audits), and increasing the number of irregularities, related parties, and their impact (investigative audit reporting) are considered as ways to improve the organization’s reputation.

The results of this study are consistent with the previous studies that have pointed out that the quality ofinvestigative audits is one of the factors affecting the reputation of the organization.

The Influence of Independence on the Organization’s Reputation through the Quality of Investigative Audits

The hypothetical test results obtained by testing the significance of the coefficient path in the structural models show that auditor independence has a positive influence on the organization’s reputation through the quality of investigative audits. In this study, the testing showed both a direct and an indirect influence. The direct effect of auditor independence on the organization’s reputation of 0.21 is a smaller value than that of the indirect influence of 0.23.

Auditor independence affects the organization’s reputation through the quality of investigative audits, which is reflected through the dimensions of auditor independence and improves the reputation of the organization through the mediation of the quality of investigative audits. It is argued that the auditor’s independence can improve the reputation of the organization, which is reflected in the quality of investigative audits. This study shows that auditor independence can affect the organization’s reputation through the quality of investigative audits in which the quality of investigative audits acts as an intervening variable.

CONCLUSION

The following conclusions are drawn on the basis of the observations, problem formulations, hypotheses, and research results.

1- The independence of auditors has a direct positive influence on the quality of investigative audits. An increase in the auditor independence level will result in better audit quality. The impact is attributed to the ability of auditors to develop an investigative audit program, determine the audit methodology and procedures, and determine the scope of the investigative audit.

2- Independence has a direct positive impact on the BPK’s reputation as an audit institution. The higher the level of independence possessed by the auditor, the better the credibility of the BPK’s reputation. This is affected by the extent of independence that the auditor possesses in acting against particular motives that might hinder the audit process, in disclosing fraud, in reporting the value of state losses, and in disclosing the affiliated parties.

3- The quality of investigative audits also exerts a positive impact on BPK’s reputation. The increased quality of an investigative audit report will lead to an increased perception of the BPK as a credible auditinstitution. This effect is attributed to the capacity of the auditor supported by a credential of expertise in the field of investigation, the ability of the auditor to disclose irregularities, and the implications of irregularities.

4- Independence also has a positive impact on the BPK’s reputation through the quality of investigative audits. Such an influence is attributed to the auditor obtaining the independence to determine the investigative audit program, methodology, and procedures and the independence to disclose fraud, report the value of state losses and disclose the affiliated parties.

BIODATA

NAJMATUZZAHRAH is an auditor in the Audit Board of the Republic of Indonesia who has experienced from low to high level of auditing. She has a lot of knowledge and skills in accounting, auditing, risk management, accounting information systems, public sector accounting, financial accounting, corporate finance/financial management, and taxation. She is currently a doctoral candidate of Accounting in University of Padjadjaran,

SRIHADI WINARNINGSIH is a lecturer in the Accounting Department, Economic and Business Faculty, University of Padjadjaran. She finished her doctoral program in business management focused in Accounting study. She has a specialization in auditing, accounting and financial information, accounting information systems, auditing, behavioral financial and accounting research, corporate finance, cost accounting.

SRI MULYANI is a Rector in University of Singaperbangsa Karawang and a lecturer in the Accounting Department, Economic and Business Faculty, University of Padjadjaran. She has experienced more than 25 years in the field of information systems and good governance for the private, public, and sharia sector. She actively writes and gives consultations for analyzing and designing applied information systems, good governance, sharia finance, and others. She is currently the National Council Member, Institute of Indonesia Chartered Accountants.

BAHRULLAH AKBAR is an auditor in the Audit Board of the Republic of Indonesia and a lecturer in the Accounting Department, Economic and Business Faculty, University of Padjadjaran and Institute of Domestic Government. He has a specialization in Auditing, Public Sector Accounting, and State Finance Law.

BIBLIOGRAPHY

ABUBAKAR, I., & OBANSA, S. (2020). An Estimate of Average Cost of Hypertension and its catastrophic effect on the people living with hypertension: Patients’ perception from two Hospitals in Abuja, Nigeria. International Journal of Social Sciences and Economic Review, 2(2), 10-19.

ALAM, H. R., & Shakir, M. (2019). Causes of the Passive Attitude in Children at Early Grade Level. International Journal of Social Sciences and Economic Review, 1(1), 16-21. doi:https://doi.org/10.36923/ijsser.v1i1.25

ARENS, A, A (2014). "Auditing and assurance services: an integrated approach".

BHATTI, A., & AKRAM, H. (2020). The Moderating Role Of Subjective Norms Between Online Shopping Behaviour And Its Determinants. International Journal of Social Sciences and Economic Review, 2(2), 1-09. doi:https://doi.org/10.36923/ijsser.v2i2.52

CAHYONO, A, D, WIJAYA, A, F, & DOMAI, T (2015). "Pengaruh kompetensi, independensi, obyektivitas, kompleksitas tugas, dan integritas auditor terhadap kualitas hasil audit". Reformasi, 5(1), pp. 1-12.

DUFF, A (2004). "Auditqual: Dimensions of audit quality". Institute of Chartered Accountants of Scotland Edinburgh

EDEN, L, NIELSEN, B, B, & VERBEKE, A (2020). "Research methods in international business". Springer.

ERNSTBERGER, J., KOCH, C., SCHREIBER, E. M., & TROMPETER, G (2020). "Are audit firms'compensation policies associated with audit quality?". Contemporary Accounting Research, 37(1), pp. 218-244.

GAO, Y, JAMAL, K, LIU, Q, & LUO, L (2011). "Does Reputation Discipline Big 4 Audit Firms?". CAAA Annual Conference.

HAERIDISTIA, N, & FADJARENIE, A (2019). "The effect of independence, professional ethics & auditor experience on audit quality". International Journal of Scientific & Technology Research, 8, pp. 1-12.

HALIM, A, & DAHLAN, A (2017). "The auditor’s sustainable reputation: effects of competence, independence, and audit quality".

HARRIS, M, K, & WILLIAMS, L, T (2020). "Audit quality indicators: Perspectives from Non-Big Four audit firms and small company audit committees". Advances In Accounting, 50, pp. 100400-100485.

HOHENFELS, D, & QUICK, R (2018). "Non-audit services and audit quality: evidence from Germany". Review of Managerial Science,2, pp. 1-49.

HONEY, M, G (2012). "A short guide to reputation risk". Gower Publishing, Ltd.

HUSAIN, T (2019). "An Analysis of Modeling Audit Quality Measurement Based on Decision Support Systems (DSS)". Measurement, 275, pp. 310-326

IRFAN, M, HASSAN, M, HASSAN, N, HABIB, M, KHAN, S, & NASRUDDIN, A, M (2020). "Projectmanagement maturity and organizational reputation: a case study of public sector organizations". IEEE Access, 8, pp. 73828-73842.

KNECHEL, W, R (2016). "Audit quality and regulation". International Journal of Auditing, 20(3), pp. 215-223.

KRISHNAMURTHY, S, ZHOU, J, & ZHOU, N (2006). "Auditor reputation, auditor independence, and thestock‐market impact of Andersen's indictment on its client firms". Contemporary Accounting Research,23(2),pp. 465-490.

LEE, S,-C, SU, J,-M, TSAI, S,-B, LU, T,-L, & DONG, W (2016). "A comprehensive survey of government auditors’ self-efficacy and professional Development for improving audit quality". SpringerPlus, 5(1), pp. 1- 25.

LESSAMBO, F, I, LESSAMBO, F, I, & WEIS (2018). "Auditing, assurance services, and forensics". Springer.

LOUWERS, T, J, SINASON, D, H, STRAWSER, J, R, THIBODEAU, J, C, & BLAY, A, D (2018). "Auditing &assurance services". McGraw-Hill Education.

MAUTZ, R, DAN HA SHARAF (1993). "The philosophy of auditing. saratosa, florida: american accounting association".

PATRICK, Z, VITALIS, K, & MDOOM, I (2017). "Effect of auditor independence on audit quality: A review of literature". International Journal of Business and Management Invention, 6(3), pp. 51-59.

RAVASI, D, RINDOVA, V, ETTER, M, & CORNELISSEN, J (2018). "The formation of organizational reputation". Academy of Management Annals, 12(2), pp. 574-599.

RIMKUTĖ, D (2020). "Building organizational reputation in the European regulatory state: An analysis of EU agencies' communications". Governance, 33(2), pp. 385-406.

RITTENBERG, L, E, JOHNSTONE, K, M, & GRAMLING, A, A (2010). "Auditing: A business risk approach".

SARI, E, G, RAHMAT, D, & WIDJAYA, S (2020). "The effect of fee and motivation on corruption eradicationusing kpk performance as the intervening variable". Asia Pacific Fraud Journal, 5(2), pp. 212-220.

SARWONO, A, E, RAHMAWATI, R, ARYANI, Y, A, & PROBOHUDONO, A, N (2018). "Factors affectingcorruption in Indonesia: study on local government in Indonesia". Indonesian Journal of Sustainability Accounting and Management, 2(2), pp. 79-89.

SEKARAN, U, & BOUGIE, R (2016). "Research methods for business: A skill building approach". John Wiley& Sons.

SEMBIRING, S, I, O, METALIA, M, WIDIYANTI, A, & AZHAR, R (2020). "The effect of investigative auditor's quality on audit effectiveness in proving fraudulence in the public sector". TEST, ENGINEERING & MANAGEMEN, 82, pp. 10027-10038.

SKINNER, D, J, & SRINIVASAN, S (2012). "Audit quality and auditor reputation: Evidence from Japan". The Accounting Review, 87(5), pp. 1737-1765.

SUGIYONO, P (2015). "Metode penelitian kombinasi (mixed methods)". Bandung: Alfabeta, 28, pp. 1-12.

SUPRIADI, T, MULYANI, S, SOEPARDI, E, M, & FARIDA, I (2019). "Influence of auditor competency in using information technology on the success of E-audit system implementation". EURASIA Journal of Mathematics, Science and Technology Education, 15(10), em1769.

TRUONG, Y, MAZLOOMI, H, & BERRONE, P (2020). "Understanding the impact of symbolic and substantive environmental actions on organizational reputation". Industrial Marketing Management.

WATTS, R, L, & ZIMMERMAN, J, L (1986). "Positive accounting theory".

WHITTINGTON, R, & PANY, K (2010). "Principles of auditing and other assurance services".

WILLEKENS, M, DEKEYSER, S, BRUYNSEELS, L, & NUMAN, W (2020). "Auditor market power and audit quality revisited: effects of market concentration, market share distance, and leadership". Journal of Accounting, Auditing & Finance, 0148558X20966249

XIAO, T, GENG, C, & YUAN, C (2020). "How audit effort affects audit quality: An audit process and audit output perspective". China Journal of Accounting Research, 13(1), pp. 109-127.

YATES RAUTERKUS, S, & SONG, K (2004). "Auditor's reputation, equity offerings, and firm size: the case of Arthur Andersen". AFA 2004 San Diego Meetings.