Artículos

Implementation and Performance of Accounting Information Systems, Internal Control and Organizational Culture in the Quality of Financial Information

Implementación y desempeño de sistemas de información contable, control interno y cultura organizacional en la calidad de la información financiera

I. FARIDA ida190262@gmail.com

S MULYANI sri.mulyani@unpad.ac.id

B. AKBAR bahrullah.akbar@unpad.ac.id

S.D. SETYANINGSIH sdsetyaningsih@gmail.com

I. FARIDA ida190262@gmail.com

S MULYANI sri.mulyani@unpad.ac.id

B. AKBAR bahrullah.akbar@unpad.ac.id

S.D. SETYANINGSIH sdsetyaningsih@gmail.com

Implementation and Performance of Accounting Information Systems, Internal Control and Organizational Culture in the Quality of Financial Information

Utopía y Praxis Latinoamericana, vol. 26, no. Esp.1, pp. 222-236, 2021

Universidad del Zulia

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International.

Received: 05 December 2020

Accepted: 10 February 2021

Abstract: This study uses a survey method, and the sample used as the unit of analysis in this study is the Consolidated Work Unit at the Financial Bureau or the Financial Center at Ministries and State Institutions throughout Indonesia. The data analysis method uses the Structural Equation Modeling (SEM) approach assisted by the LISREL program. The results showed that the Implementation of Accounting Information Systems, the Implementation of Internal Control Systems, and Organizational Culture significantly influence the Quality of Financial Statements and Performance.

Keywords: Information Systems, Internal Control Systems, Organizational Culture, Implication Quality.

Resumen: Este estudio utiliza un método de encuesta y la muestra utilizada como unidad de análisis es la Unidad de Trabajo Consolidado en la Oficina Financiera o el Centro Financiero en los Ministerios e Instituciones Estatales de Indonesia. El método de análisis de datos utiliza el enfoque de Modelado de ecuaciones estructurales (SEM) asistido por el programa LISREL. Los resultados mostraron que la Implementación de Sistemas de Información Contable, la Implementación de Sistemas de Control Interno y la Cultura Organizacional influyen significativamente en la Calidad de los Estados Financieros y el Desempeño.

Palabras clave: Sistemas de información, sistemas de control interno, cultura organizacional, calidad de implicación.

INTRODUCTION

Presidential Regulation No. 29 of 2014 concerns the Accountability Systems of Government Institutions. Specifically, this regulation regulates how government institutions report their performance in accordance with the provisions of the applicable laws and regulations. With this regulation, the measurement and reporting of the performance of government institutions can be performed in a more systematic and structured manner.

In practice, the performance measurement system in Indonesian government institutions has not been implemented properly. In 2010, out of all local governments, only nine provinces and five regencies or cities received B (Good) scores. In 2012, however, this condition experienced a decline in which only two districts received B (Good) scores, namely Sukabumi and Sleman. In 2015, Kemenpan RB reported that the performance of government institutions was still inefficient. This is evident from the results of the evaluation with a low predicate of 77 Ministries/Institutions (K/L), there are no K/L who received an AA value, 4 K/L received an A value, 21 K/L received a BB value, 36 K/L received a B value, and 16 K/L received a CC value. This condition was seen in 2016, which indicates that the K/L has neither fully nor optimally implemented its functions (Atkinson & McCrindell: 1997, pp. 20-22; Coyle: 2018; Ong et al.: 2009, pp. 397- 403; Din et al., 2021, pp, 1,10).

In addition, an Unqualified Opinion (WTP) from an institution cannot guarantee that the institution is free from corruption. There are many corruption cases involving officials from institutions that obtain WTP. However, financial reports remain an important factor that becomes the path to an orderly and transparent administration of state financial management.

The relationship between reporting quality and organizational performance has been investigated by several researchers, for example, Biddle, Hilary, & Verdi (2009); Ferrero & Martínez (2014); Mulyani, Hassan, & Anugrah (2016), who said that companies with better quality financial statements have good performance. Lev & Thiagarajan (1993) state that accounting plays a vital role in promoting the accountability, efficiency, and effectiveness of public services. The quality of information will improve the quality of management in seeing changes around the organization so as to respond to these changes quickly and accurately (Biddle et al.: 2009, pp. 112-131; Lev & Thiagarajan: 1993, pp. 190-215; Martínez- Ferrero: 2014, pp.49-88; Mulyani et al.: 2016, pp. 552-560).

One important factor that can affect the quality of financial reporting is the accounting information system. The existence of an information system (application/software) will facilitate and reduce the level of errors in the preparation of financial statements. This information system can minimize the risk of typos, miscounting, misclassification of accounts, and other errors so as to present information in financial statements more accurately and validly (Kewo & Afiah: 2017, pp. 1-12; Ribeiro & Prataviera: 2014, pp. 651- 660).

The next factor that can affect the quality of financial reporting is an internal control system. This is because the internal control system is a procedure or system designed to control, supervise, and direct the organization in order to achieve a goal. This is supported by Altamuro, Lynne, & Beatty (2010) and the opinion of Humbul Kristiawan, Deloitte's international consulting office partner (2016), who argues that the reliability of internal control has a significant impact on the quality of financial statements and suggests that the Government establish a Task Force to aid the Internal Control of Financial Statements (Altamuro & Beatty: 2010, pp. 58-74; Isaac et al.: 2018, pp. 60-78; Sari et al.: 2017, pp. 157-166).

The next factor that influences the quality of financial statements is organizational culture. Organizational culture is a pattern of basic assumptions that are shared and learned through problem- solving in the form of internal adaptation and integration; additionally, it can be taught to new members. Djanegara (2016) and Mulyani and Ratifah (2015) both documented that organizational culture is one of the most important factors in supporting an organization to produce quality financial reporting; this indicates that good organizational culture can result in the availability of timely, accurate information that is both comparable and reliable. The effect of the implementation of internal control systems, accounting information systems, and organizational culture on the quality of financial reporting is expected to improve the performance of government institutions (Zulifqar et al., 2020, pp. 665-675; Simkin et al.: 2014). Despite this, the relationship of these three factors to organizational performance is too distant. Therefore this studyuses the quality of institutional reports as an intervening variable. The reason for this is because when someone wants to assess the performance of an agency, the tool used as the basis for evaluation is financial statements. A good financial report is supported by the implementation of the government's internal control system, the implementation of the accounting information system, and organizational culture; specifically, the good work culture of the members of the organization is expected to be proven by the existence of this research (Adrian-Cosmin: 2015, pp. 1-12; Gavrea et al.: 2011, pp. 1-12; Martínez-Ferrero: 2014, pp. 49-88; Rotberg: 2016).

LITERATURE REVIEW

Agency Theory

Jensen and Meckling (1976) define agency relationships as contracts where one or more people (principal) involve another person (agent) to perform services on their behalf, which includes the delegation of authority over decision making to agents (Jensen & Meckling: 1976, pp. 305-360).

A principal-agent framework is a promising approach through which to analyze public policy commitments because its creation and implementation involve contractual issues related to information asymmetry, moral hazard, bounded rationality, and adverse selection (Eisenhardt: 1989, pp. 57-74).

Accounting Information System

The accounting information systems put forward by Bagranoff, Simkin, & Norman (2014) mean that an accounting information system is a collection of data and processing procedures that create information that users need. Accounting information systems are a set of components that collect accounting data, store them for future use, and process them for end-users (Edwita et al.: 2017, pp. 285-290; Stair & Reynolds: 2020; Simkin et al.: 2014).

It can subsequently be concluded that the Implementation of Accounting Information Systems is a series ofmanual and computerized procedures ranging from data collection, recording, and summarizing to report financial positions and operations at the State Ministry/Institution.

Government Internal Control System

The definition of internal control can be understood as an integral process that is influenced by the management and personnel of the entity and is designed to overcome risks and to provide reasonable assurance that pursuing the entity's mission and achieving the objectives of carrying out operations that areorderly, ethical, economical, efficient, and effective and that fulfill accountability obligations comply withapplicable laws and regulations, in addition to safeguarding resources against loss, misuse and damage (Benedek et al.: 2014, pp. 290-296; Sari et al.: 2017, pp. 157-166).

Internal control systems have a crucial role in realizing financial accountability. Weak financialsystems in government institutions occur because of weak design and implementation of internal control systems. The internal control system has a role in ensuring that in operational and financial management activities, public sector institutions carry out their activities economically, efficiently, effectively, and in accordance with regulations (Dewi et al.: 2019, pp. 1373-1384; Edwita et al.: 2017, pp. 285-290).

Organizational Culture

Organizational culture is reflected in something that is valued, the dominant leadership style, language and symbols, procedures and routines, and the definition of success that makes the organization unique. Furthermore, the definition of organizational culture, according to Deshpande, John, & Frederick (1993), is mutually agreed with rules, norms, and values that shape employee attitudes and behavior (Deshpandé et al.: 1993, pp. 23-37).

Based on the aforementioned definitions, the organizational culture reflects the rules, norms, and values applied in an organization manifested in the form of work spirit, working to achieve the agreed-upon organizational goals (Elsbach & Stigliani: 2018, pp. 2274-2306; Rotberg: 2016).

Quality of Financial Reporting

Financial reporting is a process that starts from a transaction/event, then selects an accounting policy, then implements that policy. Financial reporting also involves estimation and consideration, as well as the disclosure of transactions, events, policies, and balances that have been made.

Furthermore, the role of the quality of financial reporting is crucial because this report becomes procedures, organizers, equipment, and other elements to realize the accounting function in an organization from the start of a transaction/event, then selects accounting policies, then applies the policy to financial reporting in government organizations (Chen et al.: 2010, pp. 233-259; Muda et al.: 2018; Ribeiro & Prataviera: 2014, pp. 651-660).

Performance

Performance is a Figure of the level of achievement of the implementation of tasks in an organization in an effort to realize its goals, objectives, mission, and vision.

The concept of performance can fundamentally be seen from two aspects, namely, the performance ofemployees (individuals) and organizational performance. Employee performance is the work of individuals in an organization, while organizational performance is the totality of the work achieved by an organization (Abubakar and Obansa, 2020).

This performance is an illustration of the level of achievement of the performance of tasks completed by all employees in an organization or government institution. Improving performance in an organization or government institution is the goal or target to be achieved by organizations and government agencies in maximizing an activity (Gavrea et al.: 2011, pp. 1-12; Mariani et al.: 2017).

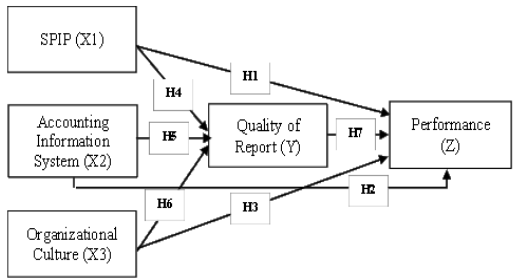

HYPOTHESIS DEVELOPMENT

The Influence of Government Internal Control Systems on Reporting Quality

Internal control is designed to achieve the objectives of the reliability of financial reporting, as per Moeller (2011) and Messier (2008). Additionally, the research conducted by Karamanou & Nishiotis (2009) identified that internal control determines the quality of corporate financial reporting. Furthermore, internal control has a significant impact on the reliability of financial reporting. When companies face internal control problems, governance mechanisms encourage management to take corrective actions to correct these problems and ensure the reliability of reported financial information (Benedek et al.: 2014, pp. 290-296; Mariani et al.: 2017, pp. 49-88; Muda et al.: 2018).

H1: Government internal control systems affect the quality of reporting.

The Influence of Accounting Information Systems on Reporting Quality

Accounting information systems greatly contribute to preparing various reports, including financial and supervisory reports, as well as compiling expenditure management systems.

Accounting information systems can facilitate an institution's financial reporting process because themanagement of data into accounting information can be done through the system so that it can reduce the risk of recording errors; this will then result in the information presented and disclosed in financial statements increasing in quality and reducing the possibility of material misstatement (Sari et al.: 2017, pp. 157-166; Simkin et al.: 2014; Stair & Reynolds: 2020).

H2: Accounting information systems affect the quality of reporting.

The Influence of Organizational Culture on Reporting Quality

Organizational culture has become an important factor in the quality of corporate financial reporting because organizational culture can shape how companies’ management and employees behave.

Garrett, Hoitash, & Prawitt (2014) and Uwajumogu et al. (2019) found that an increased concentrationof companies and external auditors had a positive effect on disclosure, while the intensity of reporting and the culture of the external organization had a negative effect on disclosure (Garrett et al.: 2014, pp. 1087- 1125; Rotberg: 2016).

H3: Organizational culture influences the quality of reporting.

The Influence of Government Internal Control Systems on the Performance of Ministries/Institutions

Internal control provides an independent assessment of the quality of managerial performance in carrying out the responsibilities given. Fadzil & Haron (nd) state that an effective internal control system is in fact related to the success of the organization in achieving its targets and objectives because of the existence of effective internal control, thus suggesting that an organization should regularly review the reliability and integrity of financial information (Fadzil et al.: 2005; Sari et al.: 2017, pp. 157-166).

H4: Government internal control systems influence the performance of ministries/institutions.

The Influence of Accounting Information Systems on the Performance of Ministries/Institutions

In the government sector, the use of Information Technology (IT) has assisted the government inmodernizing administration in the fields of accounting, finance, project management, inventory control, and counter service operations. Damanpour & Gopalakrishnan (2001) revealed that companies would only achieve high performance when they are able to carry out technological development. Moreover, Cascarino (2007) states that the implementation of both government accounting systems and regional financial management affects the internal control function ((Maria, 2020; Mehboob & Othman, 2020).

H5: Accounting information systems affect the performance of ministries/institutions.

The Influence of Organizational Culture on the Performance of Ministries/Institutions

The relationship between culture and company performance is that the company culture becomes a social control system in the company so that employees have a relatively similar culture. With a relatively similar culture being expected to have an impact on the behavior and mindset of other employees, ultimately, the company's goals will be achieved. Harrison & McKinnon (1986) found that leadership culture positively influences company selection decisions. Houqe, van Zijl, Dunstan, & Karim (2012) document the positive influence of IFRS implementation and investor protection on earnings quality (Rotberg: 2016).

H6: Organizational culture influences the performance of ministries/institutions.

The Influence of Reporting Quality on the Performance of Ministries/Institutions

Good quality financial reporting can reduce the risk of information imperfections among users of financial statements or information asymmetries. Mediocre accounting functions at the accounting entity are also the cause of late submissions of the SPJ report to the reporting entity, so that reporting on the reporting entity is not timely. Consequently, the financial statements that should be presented at regular intervals to show changes in the state of the entity are similarly inopportune (Martínez-Ferrero: 2014, pp.49-88; Muda et al.: 2018).

H7: The quality of reporting affects the performance of ministries/institutions.

Figure 1. Framework of Thinking

METHODOLOGY

Research methods

This research uses descriptive and causal-explanatory methods by testing hypotheses. In this study, researchers attempted to examine the effect of the Implementation of Accounting Information Systems (AIS), Internal Control Systems (SPIP), Organizational Culture, and the Quality of Financial Reporting and Performance.

Population and Sample

In this study, the target population was 87 ministries and institutions throughout Indonesia.

Data Collection Technique

Data collected in this study consisted of both primary and secondary data. Primary data is data or information collected by researchers through an instrument in the form of a closed questionnaire addressed to respondents. On the other hand, secondary data in this study are data or information obtained from interviews, gathering documents on the implementation of accrual accounting implementation, and the results of group discussions to deepen the analysis in explaining the conclusions of the research results.

Analytical Methods

The analytical method used in research uses quantitative concepts. This research hypothesis will thenbe tested using the Structural Equation Modeling (SEM) approach with the help of the Lisrel application. This SEM has more ability when compared to regression analysis and path analysis. SEM can simultaneously analyze the relationship between variables or what we know as path analysis and also confirm that the indicators used are appropriate in explaining the variables, which is then known as confirmatory factor analysis (CFA).

RESULTS

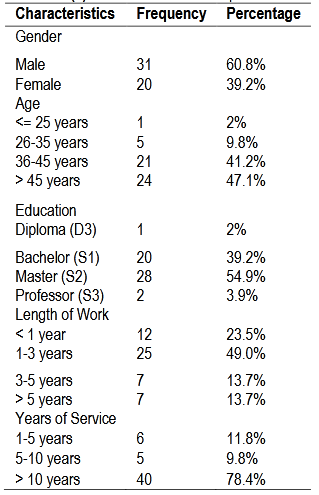

Characteristics of Respondent Profiles

The demographics of respondents obtained in this study can be seen in the following table.

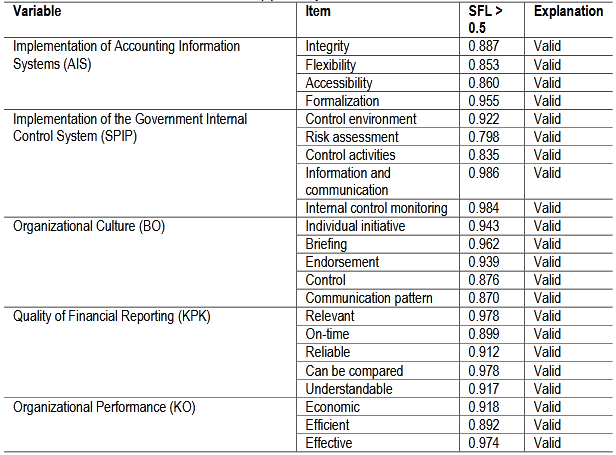

Validity Test

The validity test in this study was calculated by Lisrel, and the results were shown through a factor loading number, where the construct was said to be valid if ≥0.50 (Ghozali & Fuad, 2005). The results can be seen in Table 2.

Source: Lisrel, 2020 (processed by the author)

The validity test results contained in Table 2 illustrate the indicators in each variable with standard loading factors > 0.50, meaning that the indicators in this study show their validity as a measuring tool.

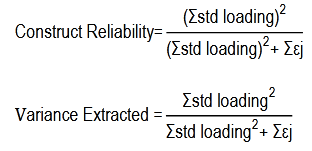

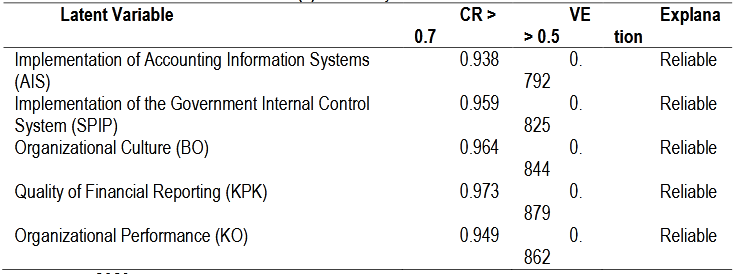

Reliability Test

Reliability was assessed by calculating the composite extracted measure and the variant extract. Both are calculated using the formula:

The instrument is said to be reliable if it meets ≥0.70 and V > 0.5. The test results are as follows

Source: Lisrel, 2020 (processed by the author)

As seen in Table 3, all latent variables have values > 0.07 and V > 0.50; thus, the respondents’ answers are consistent, and constructs are reliable.

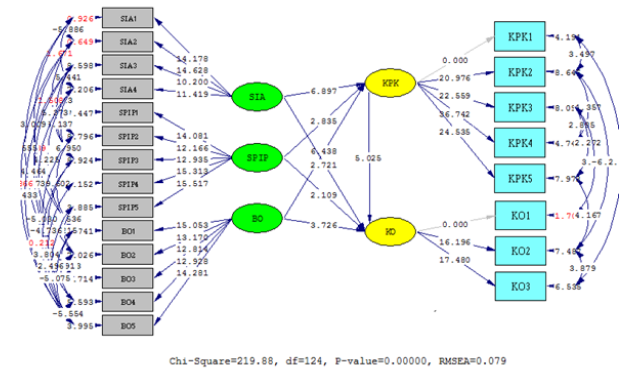

Full Structural Model Test

The results of the overall model fit test are seen in Figure 2.

Figure 2.

Structural (standardized) full model results

Figure 2 shows the results of the analysis of the path diagram relationship between the variables visited. Meanwhile, the significance test was based on a tcount of 1.99 at a 5% error rate (one tail). Significance test results for the relationship between variables are as follows.

Figure 3. Structural full model results (T-values) Source: Lisrel, 2020 (processed by the author)

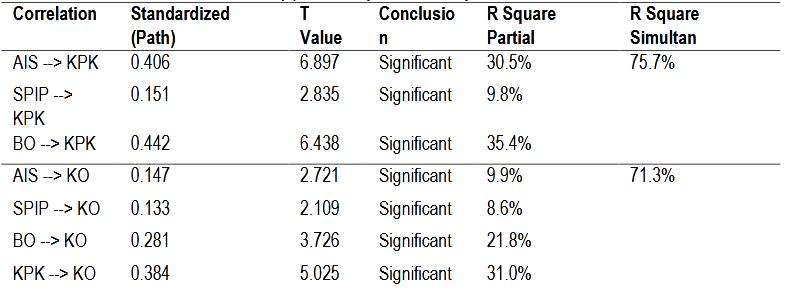

Based on Figure 3, the results of the structural estimation model of the relationship between latent variables through the Path coefficient test are summarized in Table 4.

DISCUSSION

The Influence of Government Internal Control System (SPIP) on Reporting Quality

Based on testing the hypotheses in Table 4, the tcount is 2.835 and is greater than the table (1.96) at a 5% error rate (one tail), and so H1 is accepted.

It can therefore be concluded that the government's internal control system (SPIP) affects the quality ofreporting. The SPIP becomes an integral process between management and entity personnel, who will be able to overcome risks and provide reasonable assurance that pursuing the entity's mission and achieving the objectives of carrying out operations that are orderly, ethical, economical, efficient, and effective and fulfill accountability obligations complies with applicable laws and regulations, as well as safeguardsresources against loss, misuse and damage. This will maximize the reliability of financial reporting and compliance with applicable laws and regulations (Muda et al.: 2018; Sari et al.: 2017, pp. 157-166).

The Influence of Accounting Information Systems Against Reporting Quality

Based on testing the hypotheses in Table 4, the tcount is 6.897 and is greater than the table (1.96) at a 5% error rate (one tail), so H2 is accepted.

It can be concluded that the accounting information system affects the quality of reporting. With a goodaccounting information system, an institution or organization can increase its value by improving quality and efficiency, especially in terms of supply chain efficiency and effectiveness, improving internal control structures, and improving decision making. This means that all manual procedures that enable the generation of errors can be reduced because of the computerized concept of these procedures, ranging from data collection, recording, and summarizing to reporting financial positions and operations at the State Ministry/Institution. With that concept, the information generated in the organization's management regarding the formation and achievement of specific end goals will be relevant (Simkin et al.: 2014; Stair & Reynolds: 2020).

The Influence of Organizational Culture on Reporting Quality

Based on testing the hypotheses in Table 4, the tcount is 6.438 and is greater than the table (1.96) at a 5% error rate (one tail), so H3 is accepted.

This means that organizational culture influences the quality of reporting. In terms of the audit opinion, this culture in relation to financial reporting activities can affect the quality of financial reporting in supporting an organization to produce quality financial reporting. Organizations with good organizational culture can result in the availability of timely, accurate, comparable, and reliable information (Rotberg: 2016).

The Influence of Government Internal Control Systems on the Performance of Ministries/Institutions

Based on testing the hypotheses in Table 4, the tcount is 2.109 and is greater than the table (1.96) at a 5% error rate (one tail), so H4 is accepted.

This result means that the SPIP affects the performance of ministries/institutions. This SPIP, if carried out thoroughly and efficiently within the central government and institution ministries, will have an impact on improving the application of rules in a systematic, structured, and well-documented manner so as to produce maximum performance because it directly results in all employees being required to carry out work in an orderly, controlled manner, as well as employees that are effective and efficient in their respective work environments (Sari et al.: 2017, pp. 157-166).

The Influence of Accounting Information Systems on the Performance of Ministries/Institutions

Based on testing the hypotheses in Table 4, the t-value of 2.721 and is greater than the table (1.96) at a 5% error rate (one tail), so H5 is accepted.

It can be concluded that the accounting information system influences the performance of ministries/institutions. Efforts in implementing a broad government accounting system can provide benefits and convenience for the government in realizing transparency and accountability in financial management so that the implementation of the program of activities is recorded properly and has clear measures in the presentation of financial statements (Edwita et al.: 2017, pp. 285-290; Simkin et al.: 2014).

The Influence of Organizational Culture on Performance of Ministries/Institutions

Based on testing the hypotheses in Table 4, the tcount is 3.726 and is greater than the table (1.96) at a 5% error rate (one tail), so H6 is accepted.

As such, we can determine that organizational culture influences the performance of ministries/institutions. The relationship between culture and company performance is that the company culture becomes a social control system so that employees have a relatively similar culture, with a similar culture expected to have an impact on the behavior and mindset of other employees. In the end, the company's goals will be achieved because the company has succeeded in creating a social control system for its members through a corporate culture (Chalmers et al.: 2017, pp. 831-835).

The Influence of Reporting Quality on the Performance of Ministries/Institutions

Based on testing the hypotheses in Table 4, the calculated value of 5.025 and is greater than the table (1.96) at a 5% error rate (one tail), so H7 is accepted.

The results mean that the quality of reporting affects the performance of ministries/institutions. Financial reporting plays an important role in encouraging the accountability, efficiency, and effectiveness of public services. The quality of reporting will improve the quality of management in seeing changes around the organization so as to respond to these changes quickly and accurately. The same thing is known from IPSASB (2013); this states that the allocation of resources by the government is inadequate if supported by poor quality financial information. A resulting report is a form of accountability of government institutions for the implementation of government carried out (Muda et al.: 2018).

CONCLUSION

Clearly, the SPIP affects the Quality of Reporting. The SPIP has become an integral process between management and entity personnel and will be able to overcome risks and provide reasonable assurance that pursuing the entity's mission and achieving the objectives of carrying out operations that are orderly, ethical, economical, efficient, and effective, as well as fulfilling accountability obligations, complies with the applicable laws and regulations and safeguards resources against loss, misuse, and damage. This will maximize the reliability of financial reporting and compliance with applicable laws and regulations.

Accounting information systems affect the quality of reporting. With a good accounting information system, an institution or organization can increase its value by improving its quality and efficiency, especially in terms of supply chain efficiency and effectiveness; this is in addition to improving both internal control structures and decision making because the existence of an accounting information system can make an institution's financial reporting process easier and faster.

Organizational culture influences the quality of reporting. In the quality of financial reporting,organizational culture becomes an important factor because it can shape how management and employees behave. The management and employees of an entity become an important factor in the financial reporting process because the financial statements are made by the company's management, who also determine the information disclosed in such statements.

The SPIP influences the performance of ministries/institutions. The SPIP is one of the methods adopted by the government in formulating methods to improve the internal control system so that the implementation of government activities can be carried out effectively, efficiently, transparently, and accountably through the development of internal control culture.

The accounting information system influences the performance of ministries/institutions. To that end, efforts in implementing a broad government accounting system can provide benefits and convenience for the government in realizing transparency and accountability in financial management so that the implementation of the program of activities is recorded properly and has clear measurements in the presentation of financial statements.

Organizational culture influences the performance of ministries/institutions. The company's objectives will be achieved because the company has succeeded in creating a system of social control of its members through corporate culture. Another benefit thereof is that good organizational culture can create good employee performance because of the availability of timely, accurate, comparable, and reliable information.

The quality of reporting affects the performance of ministries/institutions. To reduce information asymmetry and increase institution accountability, government institutions are required to submit accountability reports that contain the achievement of the performance of management activities carried out; this will also impact financial reporting that encourages accountability, efficiency, and effectiveness of public services.

Furthermore, the SPIP indirectly influences Organizational Performance through the Quality of FinancialReporting. Internal control systems are a procedure or system designed to control, supervise, and direct the organization in order to achieve a goal. The system can be used by management to plan and control the company's operations, help provide reliable accounting information for financial statements, and ensure compliance with applicable laws and regulations. Therefore, effective internal control can ensure that the activities of the entity are carried out in accordance with statutory provisions and affect the resulting performance.

Accounting Information Systems have an indirect effect on Organizational Performance through Financial Reporting Quality. AIS can be a parameter for measuring and reporting government finances, which is a starting point in evaluating the performance of Ministries/Institutions that is more systematic and structured. The implementation of accounting information systems can also help reduce the errors caused by the negligence and inability of a person to prepare financial statements so that they can more accurately and validly present information. Valid information will result in unbiased decision-making and optimize performance.

Organizational Culture indirectly influences Organizational Performance through the Quality of Financial Reporting. The hope to be achieved from the existence of a good organizational culture is to make the process efficient. This can affect budget savings from the efficiency of this process so that later it can become evidence that the Ministry is very careful in managing public finances and producing quality financial reporting. Efficiency as an instrument, which we have considered normative, can have an extraordinary impact on improving institution performance.

BIODATA

I. FARIDA: is an auditor in the Audit Board of the Republic of Indonesia. She has a lot of knowledge and skills in accounting, auditing, risk management, accounting information systems, public sector accounting, financial accounting, corporate finance/financial management, and taxation. She is currently a doctoral candidate of Accounting in University of Padjadjaran.

S. MULYANI: is a Rector in University of Singaperbangsa Karawang and a lecturer in the Accounting Department, Economic and Business Faculty, University of Padjadjaran. She has experienced more than 25 years in the field of information systems and good governance for the private, public, and sharia sector. She actively writes and gives consultations for analyzing and designing applied information systems, good governance, sharia finance, and others. She is currently the National Council Member, Institute of Indonesia Chartered Accountants.

B. AKBAR: is an auditor in the Audit Board of the Republic of Indonesia and a lecturer in the Accounting Department, Economic and Business Faculty, University of Padjadjaran and Institute of Domestic Government. He has a specialization in Auditing, Public Sector Accounting, and State Finance Law.

S.D. SETYANINGSIH: is an auditor in the Audit Board of the Republic of Indonesia and a lecturer in the Accounting Department, Economic and Business Faculty, University of Pakuan. She specializes in Auditing, Public Sector Accounting, and Financial Management. accounting and financial information, accounting information systems, auditing, behavioral financial and accounting research.

BIBLIOGRAPHY

ABUBAKAR, I., & OBANSA, S. (2020). An Estimate of Average Cost of Hypertension and its catastrophic effect on the people living with h pertension: Patients’ perception from two Hospitals in Abu a, Nigeria. International Journal of Social Sciences and Economic Review, 2(2), 10-19.

ADRIAN-COSMIN, C, (2015). "Accounting information system-qualitative characteristics and the importance of accounting information at trade entities". Annals of'Constantin Brancusi'University of Targu-Jiu. Economy Series, 2(1), pp. 1-12.

ALTAMURO, J, & BEATTY, A, (2010). "How does internal control regulation affect financial reporting?". Journal of accounting and economics, 49(1-2), pp. 58-74.

ATKINSON, A, A, & MCCRINDELL, J, Q, (1997). "Strategic performance measurement in government". CMA magazine, 71(3), pp. 20-22.

BENEDEK, M, SZENTÉNÉ, K, T, & BÉRES, D, (2014). "Internal controls in local governments". Public Finance Quarterly, 59(3), pp. 290-296.

BIDDLE, G, C, HILARY, G, & VERDI, R, S, (2009). "How does financial reporting quality relate to investment efficiency?". Journal of accounting and economics, 48(2-3), pp. 112-131.

CHALMERS, L, M, ASHTON, T, & TENBENSEL, T, (2017). "Measuring and managing health system performance: An update from New Zealand". Health Policy, 121(8), pp. 831-835.

CHEN, D, Q, MOCKER, M, PRESTON, D, S, & TEUBNER, A, (2010). "Information systems strategy: reconceptualization, measurement, and implications". MIS quarterly, 10(1), pp. 233-259.

COYLE, H, (2018). "A strategic framework for performance measurement in local government: an empirical study of three district councils in the UK". University of Derby.

DESHPANDÉ, R, FARLEY, J, U, & WEBSTER JR, F, E, (1993). "Corporate culture, customer orientation, and innovativeness in Japanese firms: a quadrad analysis". Journal of marketing, 57(1), pp. 23-37.

DEWI, N, AZAM, S, & YUSOFF, S, (2019)." Factors influencing the information quality of local government financial statement and financial accountability". Management Science Letters, 9(9), pp. 1373-1384.

EDWITA, A, SENSUSE, D, I, & NOPRISSON, H, (2017). "Critical success factors of information system development projects". 2017 International Conference on Information Technology Systems and Innovation (ICITSI), 2(1), pp. 285-290.

EISENHARDT, K, M, (1989)." Agency theory: An assessment and review". Academy of management review, 14(1), pp. 57-74.

ELSBACH, K, D, & STIGLIANI, I, (2018). "Design thinking and organizational culture: A review and framework for future research". Journal of Management, 44(6), pp. 2274-2306.

FADZIL, F, H, HARON, H, & JANTAN, M, (2005). "Internal auditing practices and internal control system". Managerial Auditing Journal.

GARRETT, J, HOITASH, R, & PRAWITT, D, F, (2014). "Trust and financial reporting quality". Journal of Accounting Research, 52(5), pp. 1087-1125.

GAVREA, C, ILIES, L, & STEGEREAN, R, (2011). "Determinants of organizational performance: The case of Romania". Management & Marketing, 6(2), pp. 1-12.

ISAAC, O, ABDULLAH, Z, RAMAYAH, T, MUTAHAR, A, M, & ALRAJAWY, I, (2018). "Integrating usersatisfaction and performance impact with technology acceptance model (TAM) to examine the internet usage within organizations in Yemen". Asian Journal of Information Technology, 17(1), pp. 60-78.

JENSEN, M, C, & MECKLING, W, H, (1976). "Theory of the firm: Managerial behavior, agency costs and ownership structure". Journal of financial economics, 3(4), pp. 305-360.

KEWO, C, L, (2017). "The influence of internal control implementation and managerial performance on financial accountability local government in indonesiaf". International Journal of Economics and Financial Issues, 7(1), pp. 1-12.

KEWO, C, L, & AFIAH, N, N, (2017). "Does quality of financial statement affected by internal control system and internal audit?". International Journal of Economics and Financial Issues, 7(2), pp. 560-568.

LEV, B, & THIAGARAJAN, S, R, (1993). "Fundamental information analysis". Journal of Accounting Research, 31(2), pp. 190-215.

MARIA, A. (2020). Construction of an Industry Cycle Indicator for Profitability Prediction Analysis of Aggregate Firms in Bangladesh. International Journal of Social Sciences and Economic Review, 2(4), 9-18. doi:doi.org/10.36923/ijsser.v2i4.76

MARIANI, M, PITURINGSIH, E, & HERMANTO, H, (2017). "Good University Governance and Its Implication to Quality of Financial Reporting in the Public Service Agency". E-PROCEEDING STIE MANDALA.

MARTÍNEZ-FERRERO, J, (2014). "Consequences of financial reporting quality on corporate performance: Evidence at the international level". Estudios de Economía, 41(1), pp. 49-88.

MEHBOOB, F., & OTHMAN, N. (2020). Examining the Links Leading to Behavioral Support for Change: An Expectancy Theory Perspective. International Journal of Social Sciences and Economic Review, 2(4), 1-8. doi:10.36923/ijsser.v2i4.78

MUDA, I, HARAHAP, A, H, GINTING, S, MAKSUM, A,, & ABUBAKAR, E, (2018). "Factors of quality offinancial report of local government in Indonesia". IOP Conference Series: Earth and Environmental Science.

MULYANI, S, HASSAN, R,, & ANUGRAH, F, (2016)." The critical success factors for the use of information systems and its impact on the organizational performance". international business management, 10(4), pp. 552-560.

ONG, C,-S, DAY, M,-Y, & HSU, W,-L, (2009). "The measurement of user satisfaction with question answering systems". Information & Management, 46(7), pp. 397-403.

RIBEIRO, E, & PRATAVIERA, G, (2014). "Information theoretic approach for accounting classification". Physica A: Statistical Mechanics and its Applications, 416, pp. 651-660.

ROTBERG, B, (2016). "Culture and IFRS: The effect of Culture on IFRS Implementation and financial Reporting Quality".

SARI, N, GHOZALI, I, & ACHMAD, T, (2017). "The effect of internal audit and internal control system on public accountability: The emperical study in Indonesia state universities". Technology, 8(9), pp. 157-166.

SIMKIN, M, G, NORMAN, C, A, S, & ROSE, J, M, (2014). "Core concepts of accounting information systems". John Wiley & Sons.

STAIR, R, & REYNOLDS, G, (2020). "Principles of information systems". Cengage Learning.

UWAJUMOGU, N., NWOKOYE, E., OGBONNA, I., & OKORO, M. (2019). Response of EconomicDiversification To Gender Inequality: Evidence From Nigeria. International Journal of Social Sciences and Economic Review, 1(2), 61-72. doi:https://doi.org/10.36923/ijsser.v1i2.32