Artículos

Effect of financial reform and fiscal decentralization In Bone, Indonesia

Efecto de la reforma financiera y la descentralización fiscal en Bone, Indonesia

A.I. WALINONO iqbal.walinono@yahoo.com

A.R. KADIR rahmankadir90@yahoo.com

A.I. ANWAR aianwar@fe.unhas.ac.id

A.I. WALINONO iqbal.walinono@yahoo.com

A.R. KADIR rahmankadir90@yahoo.com

A.I. ANWAR aianwar@fe.unhas.ac.id

Effect of financial reform and fiscal decentralization In Bone, Indonesia

Utopía y Praxis Latinoamericana, vol. 26, no. Esp.2, pp. 49-64, 2021

Universidad del Zulia

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International.

Received: 25 February 2021

Accepted: 22 March 2021

Abstract: This paper aims to discuss the Effect of Financial Reform and Fiscal Decentralization on Financial Governance in Bone, Indonesia. Financial performance analysis can be done by looking at the ratio of the degree of fiscal decentralization, regional financial dependence, regional independence, the effectiveness and efficiency of ROI, and compatibility of direct spending to analyze the effect of financial performance on the Human Development Index (HDI). This research found that the HDI in Bone Regency 2010-2019 was influenced by the direct expenditure compatibility ratio.

Keywords: Financial reform, financial decentralization, financial governance, HDI, ROI..

Resumen: Este documento tiene como objetivo discutir el efecto de la reforma financiera y la descentralización fiscal en la gobernanza financiera en Bone, Indonesia. El análisis del desempeño financiero se puede hacer observando la relación entre el grado de descentralización fiscal, la dependencia financiera regional, la independencia regional, la efectividad y eficiencia del ROI y la compatibilidad del gasto directo para analizar el efecto del desempeño financiero en el Índice de desarrollo (IDH). Esta investigación encontró que el IDH en Bone Regency 2010-2019 estuvo influenciado por el índice de compatibilidad del gasto directo.

Palabras clave: Reforma financiera, descentralización financiera, gobernanza financiera, HDI, ROI..

INTRODUCTION

The success of the development, especially human development, can be assessed by seeing how big the problems in society can be resolved. These problems can be identified through the level of life expectancy, the expectancy of school length and the average length of schooling, expenditure per capita, geometric mean, and arithmetic growth of an area. However, the problem is that the achievements of human development are partially varied, in which certain aspects of development have succeeded, and other aspects of development have failed (Alkaraan: 2018; Dasic et al.: 2020, pp. 1755-1760; Haseeb et al.: 2020, pp. 723-745; Li, Peng,& Lv: 2019, pp. 507-516).

Regional financial reform marked by a change in the development paradigm from a centralized to a desentalistic one (O'Brien: 2019, pp. 3-16). The division of authority into a part of the policy direction is known as regional autonomy. The granting of broad autonomy to the regions is directed at accelerating the realization of community welfare through improved services, empowerment, and community participation (Andhika: 2018, pp. 17-31; Baktybayev: 2020, pp. 1-11). In addition, through autonomy, regional areas are expected to be ableto increase competitiveness by taking into account the principles of democracy, equity, justice, privileges, and specificities, as well as potential and regional diversity in the system of the Unitary State of the Republic of Indonesia (Amalia & Purbadharmaja: 2014, pp. 257-263). In order to achieve the goal of regional autonomy, the District Government of Bone must make improvements and changes to the system and structure of regional financial management for the better (Vasylieva et al.: 2018).

Regional autonomy is believed to be the best way to promote regional development because through regional autonomy, autonomy in carrying out development can be carried out effectively and efficiently (Harliyani & Haryadi: 2016, pp. 129-140; Metrick & Rhee: 2018, pp. 153-172). Central government policiesthat impose regional autonomy are concrete steps in realizing true government decentralization. The purpose of the Central Government to grant autonomy rights to regional governments is to accelerate the realization of community welfare through improved services, empowerment, and community participation. With thetransfer of authority from the center, local governments have a greater responsibility to utilize the potential oftheir regions (Amalia & Purbadharmaja: 2014, pp. 257-263).

The main problem faced by regional financial reforms since the implementation of regional autonomy, there are still many regions, especially Bone regency, which have not been maximal in implementing regional autonomy policies. Almost fifteen years since the implementation of regional autonomy, currently, the financialcapacity of the Bone district government is still very dependent on revenues from the central or provincial levels. This can be seen from the level of independence of the Bone district government is still low (Pérez: 2019).

Regional autonomy has mandated local governments to carry out tasks. One of the main tasks of theregional government is explained in the Law on Regional Government Number 23 of 2014, is to carry out autonomy to the maximum extent, except for government affairs, which are government affairs, to improve public welfare, public services, and regional competitiveness. The achievement of human development goals, as reflected in the Human Development Index (HDI), is highly dependent on the government's commitment as a provider of supporting facilities.

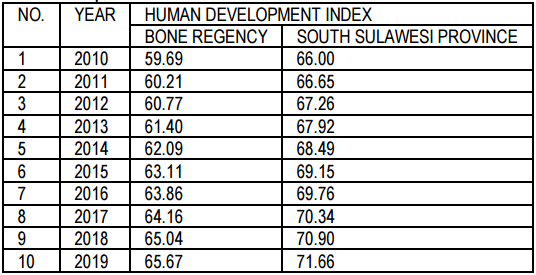

Source: Processed data from BPS, South Sulawesi

From the table above, it can be seen that in the last ten years, the human development index in Bone Regency is still below the Human Development Index for South Sulawesi Province. Nevertheless. The Human Development Index for Bone Regency continues to increase every year in line with the Human Development Index for South Sulawesi Province

The most crucial element in the administration of governance and development in the regions is to carry out regional financial management properly. It is under development aspirations and demands of the community. To create areas with high human quality, local governments use the APBD to finance development in various sectors. The Bone Regency government must work hard to reduce the poverty rate. The low capacity and capacity of regional financial management will often have adverse effects, namely the low level of services for the community and the inability to increase the HDI. Government performance is often used asa reference in observing the level of public welfare, one of which is financial performance. There are quite alot of measuring tools to assess the government's financial performance, including the analysis of financial ratios to the Regional Budget (APBD).

From the income side, there are two performance measures, namely revenue growth, which illustrates that the government's performance in obtaining revenue has increased or decreased every year, and the ratio of the degree of decentralization, which describes the level of regional independence. Meanwhile, from the expenditure side, there are also two measurements, namely the growth of expenditure, which is useful to determine the development of expenses from year to year, and the balance of expenditure ratio, which describes the balance between expenditures. Under the preamble to the 1945 Constitution of the Republic of Indonesia, the main ideals of the Indonesian people are to form a government of the Indonesian State whichprotects the entire Indonesian nation and all the blood of Indonesia and to promote the general welfare and the intellectual life of the nation. Therefore, it is expected from the management of existing revenues and expenditures allocated appropriately for the welfare of the community.

Previous research has proven that there is an effect of financial performance on HDI. Sutaryo (2015)found that the ratio of the degree of fiscal decentralization has a positive impact on HDI, and the ratio of independence has a negative effect on HDI. Meanwhile, the scholars found the influence of the ratio of the degree of fiscal decentralization and the ratio of direct expenditure to HDI (Harliyani & Haryadi: 2016, pp. 129- 140). This explains that the increase in the ratio of fiscal decentralization and the ratio of direct expenditure compatibility will also increase the human development index.

METHODOLOGY

Type and Data Sources

This study uses secondary data in the form of a time series in the form of financial reports of the Bone Regency government from 2010-2019. The data used in this study were Bone Regency data is Report on the realization of the Regional Budget for Bone Regency during the 2010-2019 and Human Development Index (HDI) of Bone Regency during the period 2010-2019.

Data Analysis

Financial performance is seen from the ratio of the degree of fiscal decentralization, regional financial dependence, regional independence, the effectiveness of ROI, the efficiency of ROI, and the compatibility of direct expenditures, can be formulated as follows:

Fiscal Decentralization Degree Ratio

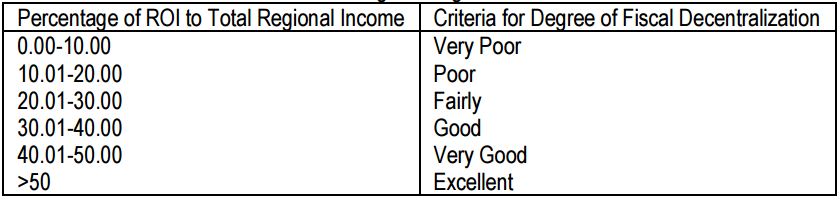

Fiscal decentralization is the delegation of responsibilities and the distribution of power and authority for decision-making in the financial sector, which includes aspects of revenue (tax assignment) and aspects of expenditure (expenditure assignment). The following formula can measure the fiscal Decentralization Degree Ratio.

Source: (Bisma, Gde, & Susanto: 2010, pp. 75-86)

Regional Financial Dependency Ratio

The ratio of regional financial dependence shows the level of dependence of local governments on the central government. The following formula can be used to measure the Regional Financial Dependency Ratio:

Source: (Bisma, Gde, & Susanto: 2010, pp. 75-86)

Regional Independence Ratio

The Regional Independence Ratio can be measured by the following formula:

Source: (Bisma, Gde, & Susanto: 2010, pp. 75-86)

Regional Original Income Effectiveness Ratio

The ROI effectiveness ratio can be measured by the following formula:

Source: (Bisma, Gde, & Susanto: 2010, pp. 75-86)

Regional Original Income Efficiency Ratio

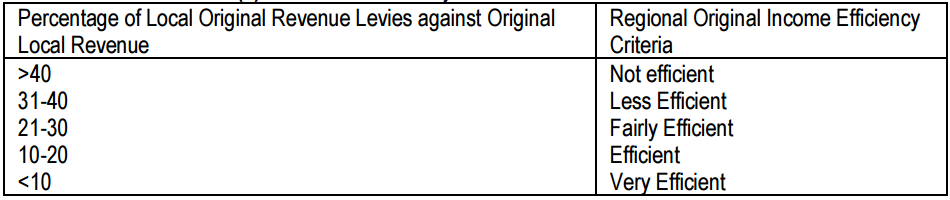

The efficiency ratio of Local Own Revenue can be measured by the following formula:

Source: (Mahmudi: 2010)

Direct Expenditure Match Ratio

The compatibility ratio for direct spending can be measured by the following formula:

Source: (Mahsun: 2006)

To analyze the extent of the influence of financial performance on the Human Development Index (HDI), Bone Regency was analyzed using multiple regression with the following model:

Y=β0+ β1X1+ β2X2+ β3X3+ β4X4+ β5X5+ β6X6+e

Where:

Y = Human Development Index

β0 = Constanta

X1 = Fiscal Decentralization Degree Ratio X2 = Regional Financial Dependency Ratio X3 = Regional Self-Reliance Ratio

X4 = Regional Native Income Effectiveness Ratio X5 = Regional Native Income Efficiency Ratio

X6 = Live Shopping Harmony Ratio

From the regression equation, several tests will be carried out for testing. The testing will be carried out in two stages, namely econometric testing (classical assumption test) and statistical test.

Operational Variable

-

The Human Development Index (Y) measures the overall level of achievement of four dimensions, namely life expectancy, expected length of schooling, and the average length of education, expenditure per capita, geometric mean, and arithmetic growth.

-

Degree of Fiscal Decentralization (X1) is a comparison between the actual revenue from the original regional revenue with the total regional revenue.

-

Regional financial dependence (X2) is the ratio between transfer income and total regional revenue.

-

Regional independence (X3) is a comparison between the realization of the balanced funds and the realization of the balancing funds with the realization of the original regional income

-

The effectiveness of local revenue (X4) is a comparison between the realization of revenue from the original region and the budget for the original regional revenue

-

The efficiency of local revenue (X5) is a comparison between the cost of collecting Regional Original Revenue and the realization of Total Regional Revenue

-

The compatibility of Direct Expenditure (X6) is a comparison of the realization of direct expenditure with total regional expenditure.

LITERATURE REVIEW

Regional Autonomy

The word autonomy comes from the Greek, which is auto which means itself, and nomous means law or regulation (Prianto: 2011). According to the Encyclopedia of Social Science, in its original meaning, autonomy is the legal self-sufficiency of the social body and its actual independence (Pratchett: 2004). The implementation of regional autonomy as regulated in Law no. 22 of 1999 concerning Regional Government and Law no. 25 of 1999 concerning Financial Balance between the Central and Regional Governments will greatly determine the continuity of Indonesia's development that is equitable and just. This became even more intense after the two laws above were revised through Law Number 32 of 2004 concerning Regional Government and Law 33 of 2004.

There are several important principles in the regional autonomy law that need to be understood, including:

-

The principle of decentralization is the transfer of government authority by the government to autonomous regions within the framework of the unitary State of the Republic of Indonesia.

-

The principle of deconcentration is the delegation of governmental authority by the government to the governor as the government's representative and/or to vertical agencies in certain areas.

-

Financial balance between central and regional governments is a government financing system within the framework of a unitary state, which includes financial sharing between central and regional governments as well as the equitable distribution between regions in a proportional, democratic, fair, and transparent manner by taking into account the potentials, conditions, and needs of the regions, in line with the obligations and distribution of authority as well as the procedures for exercising said authority, including the management and supervision of its finances.

Regional Financial Reform

Regional financial reforms began to be implemented after the enactment of Law no. 22 of 1999 and Law no. 25 of 1999. As a concrete effort, the government issued PP no. 105 of 2000 concerning the management and accountability of Regional Finance and PP. 108 of 2000 concerning the Accountability of Regional Heads in Regional Financial Management. Meanwhile, technical instructions and implementation instructions for PP No. 105 of 2000, as well as to gradually change the bookkeeping model as in the Regional Financial Administration Manual into an accounting system, the government issued Kepmendagri No. 29 of 2002, which marked an era of transition from autonomy to an ideal system. According to the scholar, the main aspects of regional financial reform include changes to the budget system, changes in regional financial management institutions, changes in the accounting system, and changes in accounting basis (Pérez: 2019).

Governance

The Scholar from Indonesia argues that the reason for the government to carry out governance, the existence of good governance arises because of irregularities in the implementation of democratization so as to encourage citizen awareness to create a new system or paradigm to oversee the running of government so that it does not deviate from its original goal (Wasistiono: 2003). The demand for realizing a state administration capable of supporting the smooth and integrated implementation of the duties and functions of state administration and development can be realized by practicing good governance (Rahim: 2019, pp. 133- 142). The three pillars of basic elements that are interrelated with each other in realizing good governance are as follows; first, transparency, namely openness in government, environmental, economic, and social management; second, participation, namely the application of democratic decision-making and recognition of human rights, freedom of the press and freedom of expression/aspirations of the public, and the last is accountability, namely the obligation to report and answer from those entrusted with the mandate to accountfor the success or failure of the trustee until the one who gives the mandate is satisfied, and if it does not exist or is not satisfied, it can be subject to sanctions (Osborne & Gaebler: 1992).

The Effect of Governance on Financial Management

The influence of governance on financial management, according to Scholars, suggests that regional financial management demands greater accountability and transparency while still paying attention to the principles of fairness and appropriateness (Halim & Kusufi: 2012; Sutduean, Harakan, & Jermsittiparsert: 2019, pp. 711-719; Fahmi: 2017, pp. 69-86). Meanwhile, Law no. 33 of 2004 Article 66 paragraph 1 states that regional finances must be managed in an orderly manner, obeying laws and regulations, efficient, economical, effective, transparent, and responsible with due regard for justice, appropriateness, and benefits for the community. Therefore, regional financial management is implemented with an output-oriented performance approach, using the concept of value for money and the principles of good government governance. Local governments carry out the mandate of the community in the form of regional financial management, which is required to be transparent and accountable in their responsibilities.

Transparency of information, especially financial and fiscal information, must be carried out in a form that is relevant and easy to understand. One of the important accountabilities related to regional financial management is financial accountability. Financial accountability is the responsibility of public institutions to use public funds (public money) economically, efficiently, and effectively, no waste and leakage of funds, and corruption. Financial accountability is very important because it is the main focus of society. This accountability requires public institutions to produce financial reports to describe the financial performance of the organization to outside parties.

Financial accountability is related to avoidance of public and public abuse. The stages in financial accountability, starting from the formulation of a financial plan (budgeting process), implementation and financing of activities, evaluation of financial performance, and implementation of reporting. In other words, accountability involves the obligation to present and report on regional financial management into regional financial reports. Financial reports are one of the tools to facilitate the creation of transparency and public accountability. Local government financial reports are presented in a comprehensive manner. The scholar suggests the same thing that state and regional finances are managed effectively and efficiently through good governance, which has three main pillars, namely: transparency, accountability, and participation (Ahmad: 2011).

The Effect of Financial Information Systems on Financial Management

The influence of financial information systems on financial management according to PP No.56 of 2005 article 1 point 15 that the Regional Financial Information System hereinafter is abbreviated as SIKD documents, administers, and processes regional financial management data and data related to IAN into the information presented to the public and as retrieval decisions in the framework of planning, implementing and reporting the accountability of local governments. According to scholar states that the Regional Financial Information System is a system that documents, administers, and processes regional financial management data and other related data into the information presented to the public and as decision making in the framework of planning, implementation and accountability, and regional government (Ahmad: 2011).

The Effect of Regional Financial Management on Financial Performance

The influence of regional financial management on financial performance according to Government Regulation Article 4 No.105 of 2000 affirms that regional financial management must be carried out in an orderly manner, obeying the prevailing laws and regulations, efficient, effective, transparent, and responsible with due regard for justice and justice. Obedience. If the management of regional finances is carried out properly in accordance with the regulations that have been set, it will certainly improve the financial performance of the region itself.

Scholars state that performance is a manifestation of the obligation to account for the success or failure of the implementation of the organization's mission in achieving the goals and objectives that have been determined by a coverage medium which is carried out periodically (Shen: 2019, pp. 160-177). This is clarified by scholars who state that the facts in the field show that the uncertainty of human resources from the regions is one of the causes of poor regional financial management so that it will affect the financial reports of regional governments and unsatisfactory regional performance (Arun & Kamath: 2015, pp. 267-287).

RESULTS

Financial Performance of Bone Regency Fiscal Decentralized Degree Ratio

Table 8 shows the ratio of the degree of budgetary decentralization of Bone Regency in 2014-2019. Fromthe table, it can be seen that the calculation results of the realization of ROI to total regional income. The ratio of the highest degree of fiscal decentralization occurred in 2017, amounting to 12.74% with the criteria of Less, and the lowest occurred in 2012, amounting to 2.58% with very few criteria.

Source: BPKAD of Bone regency (2020)

Based on the average level of fiscal decentralization in Bone Regency is 7.52%, so that it is classified according to the assessment criteria for the level of DDF from Bone Regency, which is still very low. The high level of dependence of the Bone Regency government through revenue optimization is indicated by the contribution of ROI in supporting regional revenue, which still has a high dependence on the balance of funds sourced from central transfers to finance local development. In the future, Bone Regency must continue to strive to increase its original regional income by exploring new regional potentials and developing regional potentials that have been running.

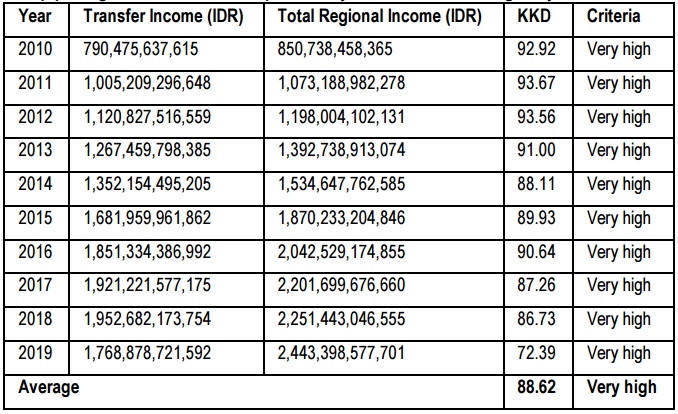

Regional Financial Dependency Ratio

Based on the ratio of regional financial dependence in Bone Regency during 2010-2019, it can be seen from the results of calculating the realization of transfer income to total income can be explained in the following table:

Source: BPKAD of Bone regency (2020)

The highest regional financial dependency ratio is shown in table 9. In 2013, it was 93.67% with very high criteria, and the lowest in 2019 was 72.39% with very high criteria. The average level of regional financial dependence of Bone Regency on the central government shows a very high percentage of 88.62%. Nevertheless. When viewed in table 8. From 2016 to 2019, the value of the regional financial dependency ratio has continued to decline. From this data, it can be seen that in 2017-2019 Bone District continues to strive to optimize local revenue and slowly reduce the level of dependence on the center.

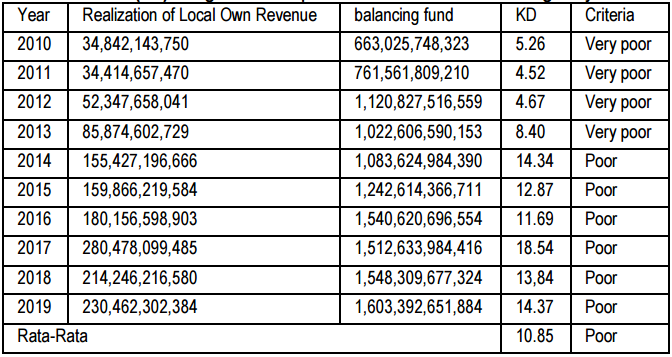

Regional Independence Ratio

Based on the regional independence ratio of Bone Regency during 2014-2019, it can be seen from the results of the calculation of the realization of ROI against the balance funds in table 10. The highest independence ratio in 2017 was 18.54%, with the criteria of Less, and the lowest self-reliance ratio occurred in 2011 at 4.52% with very few criteria. The average ratio of the regional independence level of Bone Regency is 10.85%, classified according to the criteria for assessing regional financial independence.

Source: BPKAD of Bone regency (2020)

The independence of regional finances shows the ability of local governments to finance government activities. Development and services to people who have paid taxes and levies as a source needed by the region finance regional expenditure (Halim & Kusufi: 2012; Fahmi: 2017, pp. 69-86).

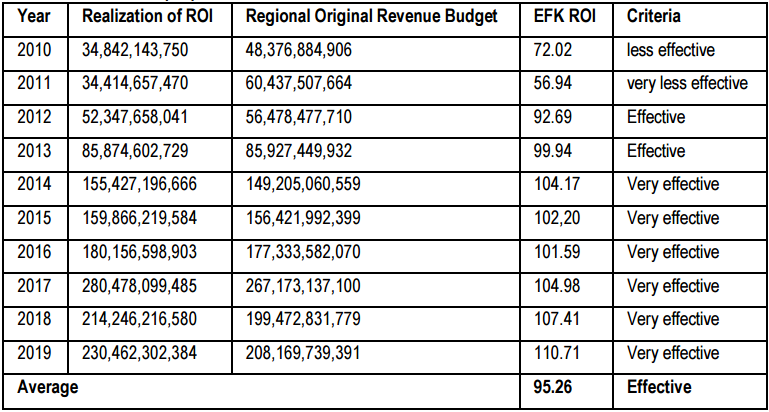

Regional Original Income Effectiveness Ratio

Based on the effectiveness ratio of ROI in Bone Regency during 2010-2019, it can be seen from the results of the calculation of the realization of ROI against the ROI budget that can be explained in table 11.

Source: BPKAD of Bone regency

The highest effectiveness ratio occurred in 2019, reaching more than 100% of 110.71% of the set budget. The lowest effectiveness ratio occurred in 2011 at 56.94%, with very few effective criteria. This is due to the revenue realization far below the target. The average ROI effectiveness ratio from 2010-2019 was 95.26% with effective criteria. The district's ROI ratio has continued to increase from year to year. It can be said that the use of the public budget has reached the predetermined target.

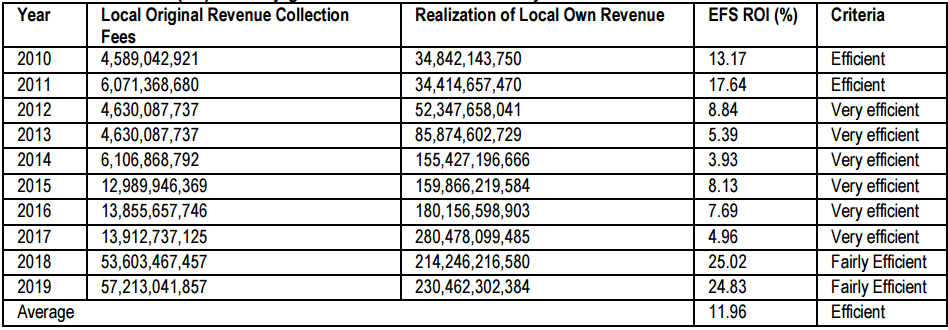

Regional Original Income Efficiency Ratio

The efficiency ratio of Locally-generated revenue in Bone Regency during 2010-2019 is shown in table12.

Source: BPKAD of Bone regency

The highest Bone Regency efficiency ratio occurred in 2018 at 25.02%, with the criteria being quite efficient. This happens because the cost of obtaining ROI is increasing. The increase in the cost of collecting ROI was not without reason. The increase in levies is carried out to improve facilities and infrastructure in terms of improving service facilities in collecting taxes and levies by using a system that is faster and easier and is offset by local revenue, which continues to increase. The lowest efficiency ratio occurred in 2014 at 3.93%, criteria for very efficient. This occurs because the costs spent to obtain ROI are still very minimal or very efficient criteria. The average efficiency ratio is 11.96% with efficient criteria.

Direct Expenditure Match Ratio

The compatibility ratio of direct expenditure in Bone Regency in 2010-2019 and the calculation of the realization of direct expenditure compared to the total expenditure is shown in table 13.

Source: BPKAD of Bone Regency

The lowest compatibility ratio for direct expenditure was 25.56%, with inconsistent criteria. Meanwhile, the highest direct expenditure compatibility ratio occurred in 2016, amounting to 49.20 criteria, which are quite harmonious. The average direct expenditure compatibility ratio for the district in 2010-2019 was 38.44%, with the criteria being quite compatible with the total expenditure of Bone Regency. The Bone Regency government needs to carry out systematic and continuous supervision and control to anticipate the occurrence of deviations from the funds that will be allocated to direct and indirect expenditures.

The Effect of Financial Performance on the Human Development Index

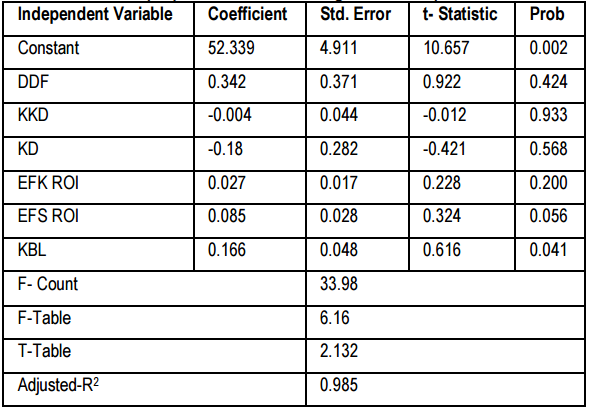

Estimates of the influence of financial performance on the Human Development Index in Bone Regency are shown in the following table:

DISCUSSION

Determinacy R2 (Adjusted-R2)

The analysis results obtained from the coefficient of determination amounted to 0.985. The value of 0.985 is a variation of the change in HDI, which is explained by six regional financial performance variables, namely the ratio of the degree of fiscal decentralization. The ratio of regional independence. ROI effectiveness ratio. ROI efficiency ratio and the direct expenditure compatibility ratio have an effect of 98.5% on the Human Development Index in Bone Regency. At the same time, the remaining 2.5% is described by other variables not included in this research model.

F test

From the results of multiple linear regression analysis, it is obtained that the F-count value is 33.98 and the F-Table at the 95% confidence level or α = 5% is 6.16, thus F-Count> F-Table (33.98> 6.16). Then H0 is rejected, meaning the ratio of DDF.KKD.KD.EFK ROI. EFS ROI. and KBL together (simultaneously) have a significant effect on HDI in Bone Regency during the 2010-2019 period.

t-Test

The ratio of the degree of fiscal decentralization has no significant effect on HDI, with a probability value of 0.424. The coefficient value is 0.342. When viewed from the value of local revenue, each year continues to increase. However, the total regional income has fluctuated each year as a result of the transfer value of the central and provincial governments, which are still high and uncertain each year.

The regional financial dependency ratio has no significant effect on HDI, with a probability value of 0.9333. The coefficient value is -0.004. The high ratio of financial dependence on central government assistance will not affect the provision of public services because transfer revenues are used to cover indirect expenditure items that cannot be fulfilled solely by ROI. If the provision of public services is also not affected. Likewise, with HDI. The HDI, as measured by the provision of public services, will also not be affected by transfer revenues.

Regional Independence Ratio has no significant effect on HDI with a probability value of 0.568. Coefficient value -0.18. A negative and insignificant relationship can be concluded that the independence of Bone Regency explains the contradictory relationship between HDI and the Regional Independence Ratio or in otherwords, the higher the value of the regional independence ratio, the HDI value in Bone Regency will decrease or vice versa if the value of the regional independence ratio decreases it will increase Human Development Index.

ROI effectiveness ratio has no significant effect on HDI with a probability value of 0.200. The coefficient value is 0.027. From these results, it can be seen that the value of ROI that exceeds the predetermined revenue target does not affect public services to increase HDI. Therefore. HDI, as an illustration of the government's success in available service provision, will also have no effect.

ROI Efficiency Ratio has no significant effect on HDI, with a probability value of 0.056. The coefficient value is 0.085. a positive but insignificant relationship can be concluded that the more efficient the realization of the ROI collection costs on the realization of ROI, this condition encourages the creation of people's welfare.

The compatibility ratio for direct expenditure has a significant effect on HDI with a probability value of0.041 and a variable coefficient value of 0.166. A positive directional relationship means that if an increase of 1%, the compatibility ratio of direct spending will increase the HDI value by 0.1610%. The success of human development in an area cannot be separated from the amount of budget allocated for the needs of the region and enhanced human development. Good public health and education can be fulfilled through the allocation of government spending in the education and health sectors. By increasing the allocation of government spending in this sector, it can improve human development.

CONCLUSION

The financial performance of the Bone Regency government during the 2010-2019 period based on the calculation of financial ratios is as follows, the degree of fiscal decentralization criteria is very less, the dependency on regional financial criteria is very high, the criteria for regional independence are Less, ROI Effectiveness Effective Criteria, ROI Efficiency Ratio criteria for efficient, and the harmony of direct expenditure criteria is not suitable

The compatibility ratio of direct spending has a positive and significant effect on the Human Development Index (HDI) of Bone Regency. While regional financial decentralization ratio, regional financial dependence, regional independence, the effectiveness of ROI, and Efficiency of ROI in the Bone Regency had no significant effect on Human Index Development in Bone regency.

BIODATA

A.I. WALINONO: The current affiliation of Andi Muhammad Iqbal Walinono is Universitas Hasanuddin, Indonesia; E-mail: iqbal.walinono@yahoo.com; ORCID: https://orcid.org/0000-0002-7718-7008

A.R. KADIR: The current affiliation of Abdul Rahman Kadir is Universitas Hasanuddin, Indonesia; E-mail: rahmankadir90@yahoo.com; ORCID: https://orcid.org/0000-0002-5527-6018

A.I. ANWAR: The current affiliation of Anas Iswanto Anwar is Universitas Hasanuddin, Indonesia; E-mail: aianwar@fe.unhas.ac.id; ORCID: https://orcid.org/0000-0002-1801-8730

BIBLIOGRAPHY

AHMAD, Y, (2011). "Pembentukan Undang-Undang dan Perda: Cet-1".(Jakarta: Rajawali Pers. 2011).

ALKARAAN, F, (2018). "Public financial management reform: an ongoing journey towards good governance". Journal of Financial Reporting and Accounting.

AMALIA, F, R, & PURBADHARMAJA, I, B, P, (2014). "Pengaruh kemandirian keuangan daerah dan keserasian alokasi belanja terhadap indeks pembangunan manusia". E-Jurnal Ekonomi Pembangunan Universitas Udayana, 3(6), pp. 257-263.

ANDHIKA, L, R, (2018). "Discretion and decentralization: public administrators dilemmas in bureaucracy innovation initiatives". Otoritas: Jurnal Ilmu Pemerintahan, 8(1), pp. 17-31.

ARUN, T, & KAMATH, R, (2015). "Financial inclusion: policies and practices". IIMB Management Review, 27(4), pp. 267-287.

BAKTYBAYEV, B, (2020). "Analysis of the relationship between women’s participation and the rate of corruption in the post-soviet states". Journal of Contemporary Governance and Public Policy, 1(1), pp. 1-11.

BISMA, I, GDE, D, & SUSANTO, H, (2010). "Evaluasi kinerja keuangan daerah pemerintah Provinsi Nusa Tenggara Barat tahun anggaran 2003-2007". Ganec Swara, 4(3), pp. 75-86.

DASIC, B, DEVIC, Z, DENIC, N, ZLATKOVIC, D, ILIC, I, D, CAO, Y, LE, H, V, (2020). "Human developmentindex in a context of human development: review on the western Balkans countries". Brain and Behavior, 10(9), pp. 1755-1760.

FAHMI, R, A, (2017). "Manajemen Keuangan masjid di kota Yogyakarta". Al-Tijary, 3(1), pp. 69-86.

HALIM, A, & KUSUFI, M, S, (2012). "Akuntansi sektor publik". Jakarta: Salemba Empat.

HARLIYANI, E, M, & HARYADI, H, (2016). "Pengaruh Kinerja Keuangan Pemerintah Daerah Terhadap Indeks Pembangunan Manusia di Provinsi Jambi". Jurnal Perspektif Pembiayaan dan Pembangunan Daerah, 3(3), pp. 129-140.

HASEEB, M, SURYANTO, T, HARTANI, N, H, & JERMSITTIPARSERT, K, (2020). "Nexus betweenglobalization, income inequality and human development in Indonesian economy: Evidence from application of partial and multiple wavelet coherence". Social Indicators Research, 147(3), pp. 723-745.

LI, B, PENG, G, & LV, B, (2019). "Financial Structure Reform and Enterprise Debt Risk Prevention". Asian Economic and Financial Review, 9(4), pp. 507-516.

MAHMUDI, M, (2010). "Manajemen Keuangan Daerah". Jakarta: Erlangga.

MAHSUN, M, (2006). "Pengukuran kinerja sektor publik". Yogyakarta: BPFE.

METRICK, A, & RHEE, J, (2018). "Regulatory reform". Annual review of financial economics, 10, pp. 153-172.

O'BRIEN, J, (2019). "Resilience as the organising framework for reform: the dangers of metaphors in financial regulation". Law and Financial Markets Review, 13(1), pp. 3-16.

OSBORNE, D, & GAEBLER, T, (1992). "Reinventing government: how the entrepreneurial spirit is transforming the public sector (first)". New York-USA: PLUME-Penguin Group-Penguin Bookes USA: Inc.

PÉREZ, S, (2019). "Banking on privilege: the politics of Spanish financial reform".Cornell University Press.

PRATCHETT, L, (2004). "Local autonomy, local democracy and the ‘new localism’". Political studies, 52(2),pp. 358-375.

PRIANTO, A, L, (2011). "Good governance dan Formasi Kebijakan Publik Neo-Liberal". Otoritas: Jurnal Ilmu Pemerintahan, 1(1), pp. 1-12.

RAHIM, A, (2019). "Governance and good governance-a conceptual perspective". Journal of Public Administration and Governance, 9(3), pp. 133-142.

SHEN, X, (2019). "Has financial marketization reform promoted innovation?—an empirical test based on mediation effect". Open Journal of Social Sciences, 7(4), pp. 160-177.

SUTDUEAN, J, HARAKAN, A, & JERMSITTIPARSERT, K, (2019). "Exploring the nexus between supply chain integration, export marketing strategies practices and export performance: a case of indonesian firms". Humanities & Social Sciences Reviews, 7(3), pp. 711-719.

VASYLIEVA, T, A, HARUST, Y, V, VYNNYCHENKO, N, V, & VYSOCHYNA, A, V, (2018). "Optimization ofthe financial decentralization level as an instrument for the country's innovative economic development regulation".

WASISTIONO, S, (2003). "Kapita Selekta Penyelenggaraan Pemerintahan Daerah, edisi II". Fokusmedia, Bandung.