Artículos

Indonesian local governments' commitment to the quality of the education sector

Compromiso de los gobiernos locales de Indonesia en la calidad del sector educativo

I. YATUN isma.yatun@bpk.go.id

S. MULYANI sri.mulyani@unpad.ac.id

S WINARNINGSIH srihadi.winarningsih@unpad.ac.id

C. SUKMADILAGA citra.sukmadilaga@unpad.ac.id

I. YATUN isma.yatun@bpk.go.id

S. MULYANI sri.mulyani@unpad.ac.id

S WINARNINGSIH srihadi.winarningsih@unpad.ac.id

C. SUKMADILAGA citra.sukmadilaga@unpad.ac.id

Indonesian local governments' commitment to the quality of the education sector

Utopía y Praxis Latinoamericana, vol. 26, no. Esp.2, pp. 347-361, 2021

Universidad del Zulia

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International.

Received: 27 February 2021

Accepted: 24 March 2021

Abstract: This study aims to test empirically whether the commitment of regional heads and the oversight function of local parliaments influence the performance of education through the quality of education sector expenditure. It is empirically proven that the commitment of regional heads and the oversight function of local parliaments have a significant and positive effect on improving the quality of government expenditure. Both variables also positively affect the performance of education in Indonesia indirectly through the quality of education sector expenditure. This study indicates that improving the quality of education sector expenditure improves educational performance.

Keywords: Local expenditure quality, commitment of regional heads, parliamentary oversight, educational performance, structural equation modelling.

Resumen: Este estudio tiene como objetivo probar empíricamente si el compromiso de los jefes regionales y la función de supervisión de los parlamentos locales influyen en el desempeño de la educación a través de la calidad del gasto del sector educativo. Se demuestra empíricamente que el compromiso de los jefes regionales y la función de supervisión de los parlamentos locales tienen un efecto significativo y positivo en la mejora de la calidad del gasto público. Ambas variables también afectan positivamente el desempeño de la educación en Indonesia indirectamente a través de la calidad del gasto del sector educativo. Este estudio indica que mejorar la calidad del gasto del sector educativo mejora su desempeño.

Palabras clave: calidad del gasto local, compromiso de los jefes regionales, supervisión parlamentaria, desempeño educativo, modelado de ecuaciones estructurales.

INTRODUCTION

Education is one of the most fundamental factors for a country. The quality of education generates proficient human resources that can improve people’s welfare. The relationship between the quality of education and indicators of a country's welfare, such as long-term economic growth, is revealed by Hanusek and Woessman (2020). In Indonesia, Law Number 23 of 2014 concerning local government asserts that education is an obligatory government function intended to meet the basic needs of citizens. The act further arranges the education administration authority into three government layers. The central government sets national standards for all levels of education and manages the operations of higher education institutions (i.e., universities, colleges, polytechnics, etc.); provincial governments administer secondary education (i.e., senior high schools and vocational schools); and district/municipal governments are responsible for basic education (i.e., elementary schools and junior high schools), including early childhood and non-formal education.

To finance education programs, the government is mandated to allocate a minimum of 20 percent of the state budget (APBN) and regional budget (APBD) to the education sector. the education budget in the APBN and APBD has continued to increase in the last five years. The education budget in the APBN has increased from IDR 409.1 trillion in 2015 to IDR 492.5 trillion in 2019, while in the overall APBD, the education budget had increased from IDR 235.58 trillion in 2015 to IDR 284.69 trillion in 2019. The budget increase, among other things, is invested in building schools and recruiting teachers, allowing more school-age children to access the education service. Rosser (2018) mentioned that Indonesia has been able to increase school participation rates and decrease dropout rates. Furthermore, Rosser (2018) argued that access to education is no longer the biggest challenge for Indonesia.

It is believed that the current challenge for Indonesia is how to improve its educational performance. In tertiary education, only three higher education institutions in Indonesia were ranked in the world's top 500 universities in 2018, namely Universitas Indonesia (ranked 277), Institut Teknologi Bandung (ranked 331), and Universitas Gajah Mada (ranked between 401 to 410). At the secondary education level, the overall score of the 2018 Program for International Student Assessment (PISA) showed that Indonesia was ranked 73 out of 77 countries for students’ performance in reading, mathematic, and science (Schleicher: 2019, pp. 35-65). This achievement was among the worst in Southeast Asia. At the basic education level, the average score in the computer-based national exam (UNBK) for the 2015–2018 period showed a downward trend for junior and senior high schools, including vocational schools. Although there was an increase in UNBK test results in 2019, the overall UNBK score was still below the graduation standard required by the government (Nasution & Surbakti: 2020, pp. 35-55).

Based on those phenomena, it is interesting to know why an increase in the education budget does not show a significant impact on the improvement of educational performance. The positive relationship between budget and performance has been revealed in various studies (Ebi and Ubi, 2017; Wahaba et al.: 2018, pp. 32- 65). Balaj (2017) argued that executing spending in a quality manner is the most important aspect of the implementation of governments’ programs and activities. Governments may allocate more resources in terms of budget for the implementation of education sector policies; nevertheless, if the policies are not implemented effectively, the expenditure may not provide the expected benefits for the public (Balaj & Lani: 2017, pp. 452 - 471).

Several studies have suggested factors related to the quality of government spending, including the commitment of regional heads and legislative oversight. Babatunde (2015) stated that leadership commitment influences the management of public expenditures. Also, legislative involvement in planning, implementing, and overseeing the budget can affect the quality of regional spending. According to Stapenhurst (2011), a budget is a tool that can be used by the legislature to warrant that government programs are implemented in accordance with the necessity of programs approved by the legislative.

Based on the phenomenon that elaborated earlier and in prior studies, the research questions that will be discussed in this study are: How significant is the influence of the commitment of regional heads on the quality of education sector spending? How much leverage does the local parliament oversight function have on thequality of education sector spending? How significant is the impact of the education sector spending quality on educational performance? How significant is the effect of regional heads’ commitment on educational performance through the quality of education spending? And how much influence does the DPRD (i.e., local parliament) oversight function have on educational performance through the quality of education sector spending? The focus on these research questions is supported by the results of our analytical review of previous literature that shows a limited number of studies examining the relationship between regional heads’ commitment and legislative oversight function in relation to the quality of education sector spending and its relationship with educational performance.

LITERATURE REVIEW

Regional Heads’ Commitment

According to Al-Azhar et al. (2014), commitment in organizations is the ability and willingness to prioritize the needs and goals of the organization by emphasizing the mission, goals, and values of the organization while having loyalty to the organization. The commitment of a regional head is a condition where regional leaders are highly committed to the improvement of community welfare through allocating more resources in the regional budget to various social service programs (Diyanayati & Weningtyastuti: 2017, pp. 173-184). The variable of regional heads’ commitment in this study is divided into five dimensions: resource allocation, organizational target and mission; policy and planning; integrity; and authority delegation and employee capacity development. The first three dimensions are further operationalized based on Hasibuan’s (2017) research. The resource allocation dimension consists of two indicators: budget allocation to the education sector and proper allocation for education personnel. The dimension of the organization’s targets and mission has two indicators, namely, setting clear educational service main goals and conducting periodic reviews and assessments on the accomplishment of the targeted objective. The policy and planning dimension also includes two indicators: establishing policies and plans to achieve the objectives and the availability of minimum educational infrastructure. The fourth dimension, integrity, refers to Johari et al. (2018) and consists of indicators of setting good values and principles and prioritizing the organizational mission above personal interests. The last dimension, delegating authority and developing employees’ capacity, consists of indicators of constructing an organizational structure that supports authority delegation and improving the capacity of the teaching workforce.

DPRD Oversight Function

The DPRD or local parliament oversight function comprises the activities of the legislative body to oversee the activities or programs executed by the executive or, specifically, the act of scrutinizing the legislature in relation to the implementation of the enacted regulations (Pelizzo & Stapenhurst: 2004, pp. 21-48; Stapenhurst: 2011, pp. 54-75). This includes overseeing the government budget. In the Indonesian context, DPRD has an important role throughout the planning and budgeting processes. The APBD draft should be submitted to the DPRD for approval. Throughout the budget execution stage, the local government is required to provide information on the implementation of programs/activities that are already stipulated in the budget. Any changes and amendments to the regional budget also require approval from the DPRD.

Based on prior studies by Pelizzo & Stapenhurst (2004), Simson et al. (2011), and Stapenhurst (2011), the variable of DPRD oversight function in this research is divided into three dimensions that consist of ex-ante supervision, ex-post supervision, and the supporting structure of the DPRDs’ oversight function. Indicators for ex-ante supervision consist of the education commission hearing, the plenary sessions hearing, and the drafting of the regional budget and its amendments. For ex-post supervision, the indicators are the right of interpellation, the right to assert an opinion and public debate, debriefing time, and attestation of the budget realization report. Lastly, indicators for the supporting structure of the DPRD’s oversight function consist of legislative commission and budget agency.

Quality of Educational Sector Expenditures

Expenditure quality as effective, efficient, transparent, and accountable government spending that is executed in a timely manner and is allocated in accordance with the regional development priorities. Wahyuni et al. (2017) further indicated that expenditure quality in the education sector consists of five dimensions, namely the expenditure priorities, budget allocation, timeliness, expenditure effectiveness, and the transparency and accountability of the expenditure. The priority dimension has only one indicator, which is the consistency of the education program priorities. The allocation dimension consists of indicators for increasing the allocation of education sector capital expenditure and ensuring the allocation accuracy of education sector subsidies. The timeliness dimension consists of indicators of the timeliness of the approval of APBD, the timeliness of budget execution in the education sector, and the timeliness of revenue realization. The dimensions of effectiveness and efficiency consist of the efficiency indicator and the effectiveness indicator for education sector expenditure. Lastly, the dimensions of transparency and accountability consist of indicators of accountability, transparency, and external auditor’s opinion on local governments’ financial reports.

Educational Performance

Chapman and Adams (2002) defined educational performance as an achievement of educational success that is measured from the perspective of inputs, processes, outputs, and outcomes. The input dimension, according to Chapman and Adams (2002), is the resources used to provide education services in the region. It consists of five indicators, namely human resources, facilities and infrastructure, source of funds, citizen's awareness, and regulations and policies. The process dimension is the service provided to students by educational providers (Chapman & Adams: 2002, pp. 75-96). It has three indicators, namely organizational structure, teaching materials, and teaching methods. According to Chapman and Adams (2002), the output dimension is the short-term and direct result of the teaching and learning process, while the outcome dimension is the long-term impact of the education system. Indicators for the output dimension are student test scores and achievements, while indicators for the outcome dimension are the average length of schooling, literacy rates, school accreditation, and school participation rates.

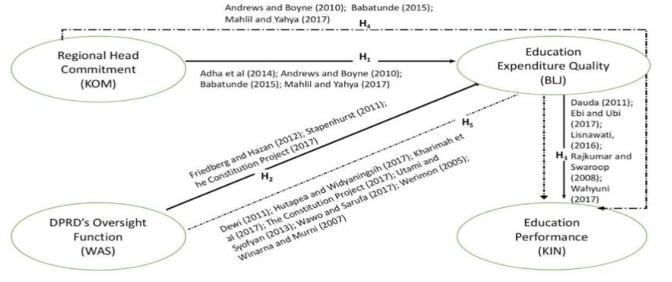

The robustness of the relationship between the exogenous variables (the regional heads’ commitment, the DPRDs’ oversight function, and the quality of education sector expenditure) and the endogenous variable of educational performance that underlies this study is illustrated in the conceptual framework in Figure 1, which is used to develop research hypotheses.

Figure 1. Conceptual Framework

At the local government level, the commitment of regional heads reflects the willingness to set a vision, mission, and programs in accordance with the needs and priorities of the regions to achieve maximum results (Al-Azhar et al.: 2014, pp. 32-58; Erlina & Muda: 2017, pp. 301-312). Since leaders influence the management of public spending, Babatunde (2015) argued that there is a significant positive effect of leadership quality on spending quality in terms of public expenditure management. A good organizational management system is not sufficient if it is not supported by leadership character and strong commitment from the leadership (Andrews & Boyne: 2010, pp. 443-454). Therefore, a hypothesis can be built that:

H1: The commitment of the regional head has a positive effect on the quality of education sector expenditure.

Law Number 23 of 2014 outlines the duties of the DPRD in overseeing the activities of regional governments, starting from approving the drafting process of the regional budget to approving the accountability report of the budget execution. The main function of a budget is to control the performance of local government in accordance with the legislative expectation, as the representation of the community needs. Stapenhurst (2011) further explained that a budget is a tool that can be utilized by the legislature to assure government activities match with the planned activities approved by the people's representatives. Therefore, a hypothesis that can be drawn is:

H2: DPRD's oversight function has a positive effect on the quality of education sector expenditure. Several studies have shown a significant and positive relationship between education sector spending and educational performance. In terms of the degree of spending value, and Ebi and Ubi (2017) recommended that the government invest heavily in the education sector, particularly in the provision of educational facilities. In terms of the quality of spending, Wahyuni et al. (2017) found that spending quality has a positive effect on performance, measured by timeliness, efficiency and cost-effectiveness, the accuracy of expenditure allocation, and accountability and transparency. Furthermore, Rajkumar and Swaroop (2008) suggested that the factor that determines the effectiveness of public spending on basic education is good governance, which is in line with Wardhani et al.'s (2017) research, which argued that education spending and governance affect performance. Hence, we develop a hypothesis that:H3: The quality of education sector expenditure has a positive effect on educational performance. Regional heads in Indonesia are authorized by the President to manage regional finances (Government of Indonesia, 2003). As a result, the commitment of regional heads is closely related to local government spending policies. Andrews & Boyne (2010) revealed that regional heads as leaders in their regions should not only lead their government officers but also lead their communities so that the government programs can be executed successfully. It is in line with research from Babatunde (2015) that showed a positive relationship between the quality of leadership and public welfare. In the context of local government, the role of the regional head is to encourage all elements in the organization to work harder and attain optimal performance (Erlina & Muda: 2017, pp. 301-312), from planning the budget to regional expenditure execution as a proxy for performance improvement. Therefore, we develop a hypothesis that:H4: The commitment of regional heads has a positive effect on educational performance through the quality of education sector expenditure.

Most of the world’s legislative institutions take part in the arrangement of the government budget alongside the executive. They also mentioned that parliamentary oversight of the budget is a focal point in the legislative supervision function. Several previous studies have underlined the influence of parliament members' comprehension of APBD governance, which has a positive impact on the quality of DPRD oversight, especially on outputs of programs and activities (Winarna & Murni, 2007, pp. 136-152). Another study that highlighted local parliament members’ knowledge found that the level of local government financial transparency had a positive impact on local parliament members' understanding of local government budgets. Parliament memberswho have a proper understanding of local government budgets are more effective in exercising their role of overseeing budget execution. This, in turn, helps local governments to attain the expected performance targets. Hence, we develop a hypothesis that:H5: DPRD's oversight function has a positive effect on educational performance through the quality of education sector expenditure.

METHODOLOGY

This research is a quantitative study using descriptive and causal explanatory methods to test the research hypotheses. We chose samples from local governments in Java and Sumatra with the consideration that the occurrence of the education phenomenon as explained earlier and the majority of students, teachers, and schools in Indonesia are located on the islands of Java and Sumatra. The research population is 267 local governments consisting of 63 municipal governments and 204 district governments that are in charge of the elementary and junior high school administration.

Data were collected through a survey method using an eight-point semantic scale questionnaire distributedto two respondents in each local government: the chairperson or member of the DPRD's educational commission and the head of the local education department. The survey was carried out online from 10 April 2020 to 29 May 2020, and questionnaires were filled directly by targeted respondents. A total of 111 local governments consisting of 23 municipalities and 88 districts participated in this study. The collected data are explained descriptively. The mean scores, standard deviations, and demographics of respondents are presented, and correlations between variables were tested to verify the research hypotheses. The verification analysis and hypothesis testing were developed using a conceptual structural equation modeling approach, while the data were processed using LISREL 8.8 statistical software.

RESULTS

Profile of Respondents

The participants in this study were 222 respondents consisting of 111 heads of local education departments, 73 chairpersons of the DPRD’s education commissions, and 38 members of the DPRD’s education commissions. There were 201 male respondents (91%) and 21 females (9%). The education level of the respondents was varied: 97 respondents (44%) held a Master’s degree, 83 respondents (37%) held a Bachelor’s degree, and the rest held a high school/vocational degree (18 respondents; 8%), a doctoral degree (14 respondents; 6%), or diploma degree (10 respondents; 5%). The educational background of the majority of respondents was non-economic (180 respondents: 81%), while the rest majored in economics non-accounting (39 respondents; 18%) and accounting (3 respondents; 1%). In terms of the service length of the respondents, a total of 161 respondents (73%) had held their current position for less than two years, 56 respondents (25%) for between three and ten years, and three respondents (1%) for more than ten years (1%); two respondents (1%) refused to answer. Classified by age, the majority of respondents were 50 years old or more (124 people; 56%); others were aged 40–49 years (22 people; 10%), 30–39 years (47 people; 21%), and under 30 years (29people; 13%).

Descriptive Statistics

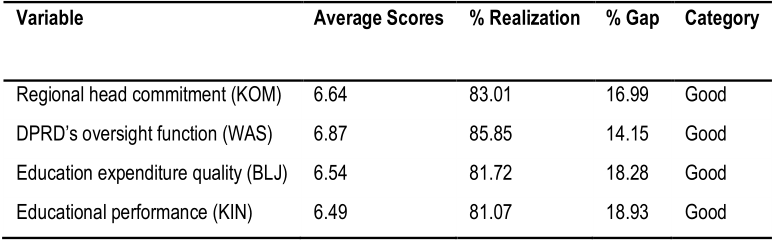

Respondents' perceptions are organized in the form of a range of scores. The range of scores is a basis for classifying the results of each respondent's answers into four categories: (1) bad, the score between 1.00 and 2.75; (2) deficient, the score between 2.76 and 4.50; (3) sufficient, the score between 4.51 and 6.25; and(4) good, score between 6.26 and 8.00. The results of the analysis of the scores for each variable are presented in Table 1.

Instruments’ Validity and Reliability

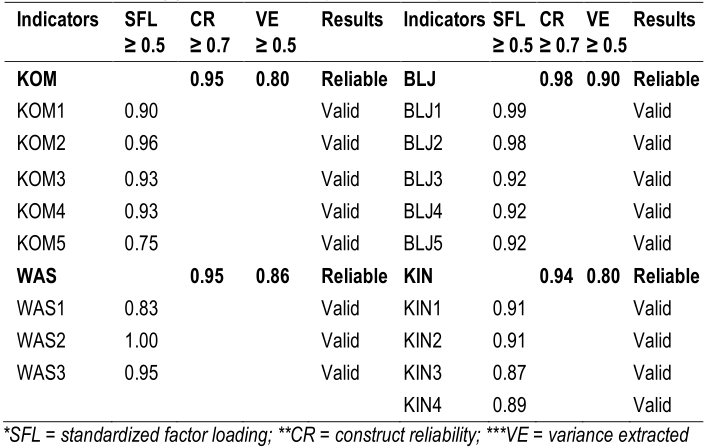

Ghozali (2009) explained that a validity test is used to measure the validity of a questionnaire, while a reliability test is used to measure the reliability of a questionnaire. A questionnaire is valid if the answers/responses to the questions/statements are able to describe properly the objects that are to be measured. A questionnaire is considered to be reliable if a respondent’s answer/response to a question/statement is consistent or stable over time. Validity and reliability are indicated by the value of construct reliability (CR) and variance extracted (VE). CR and VE values higher than 0.7 are ideal, while those above 0.5 are acceptable. Based on the test results, as presented in Table 2, all CR and VE values are above 0.7; hence the measurement model is valid and reliable.

Goodness of Fit Model Testing

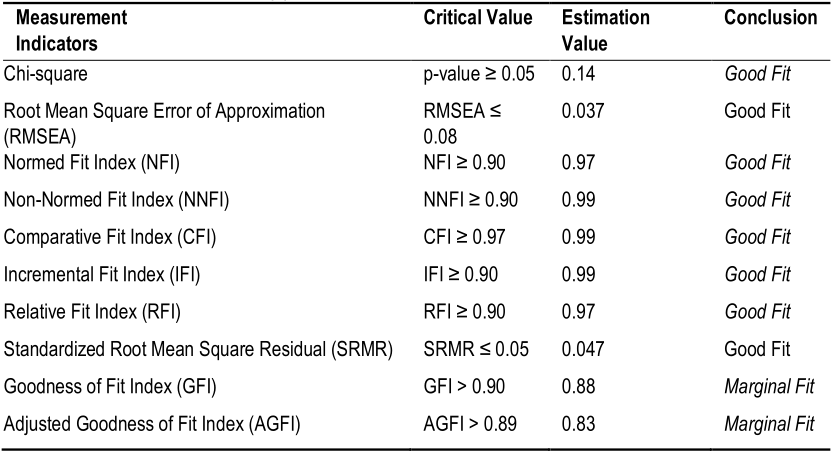

Verification analysis of structural models is performed through the goodness of fit test. This test aims to confirm whether the proposed model is fitted to the sample data (Wulandari & Murtianto: 2017, pp. 45-65).

The goodness of fit index test results show that the chi-square value is greater than 0.05, the RMSEA value is less than 0.08, and the SRMR value is less than 0.05, while the NFI, NNFI, CFI, IFI, and RFI values are greater than 0.90. This means the model can be declared as a good fit. However, two criteria did not meet the ‘good fit’ category, namely the GFI value of 0.88 (GFI criterion is > 0.90) and the AGFI value of 0.83 (AGFI criterion is > 0.89). Nevertheless, these values are considered to be acceptable (marginal fit) according to Wulandari & Murtianto (2017), who argued that a GFI value between 0.80 and 0.90 and an AGFI value from0.80 to 0.89 are considered as a marginal fit. Therefore, in general, the result of the goodness of fit model test shows that the model is good (fit) and acceptable (marginal fit).

Research Hypotheses Testing

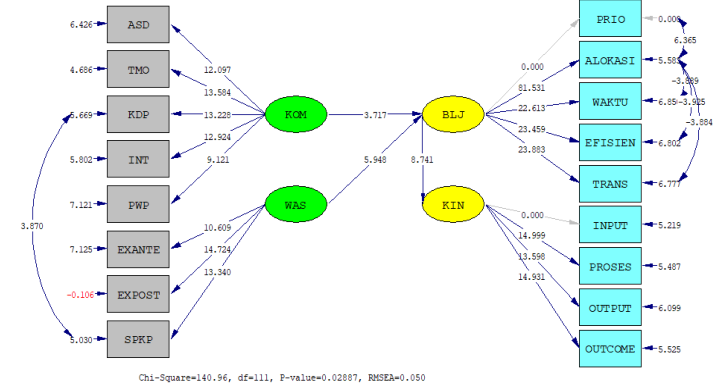

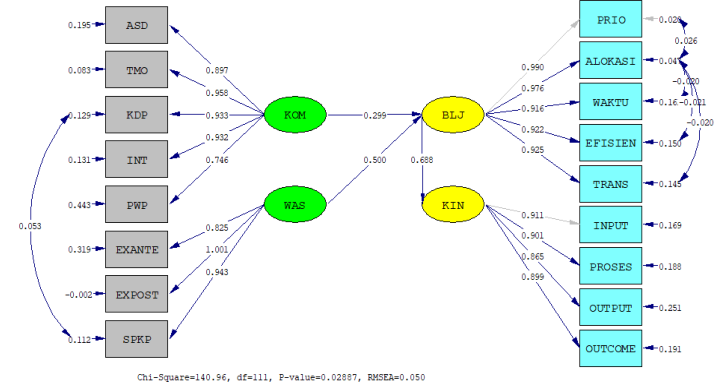

Each hypothesis was further tested by t-test statistics, with the proviso that H0 is rejected if the t-variable is smaller than the critical t-value with a confidence level of 95 percent and an error tolerance of 5 percent. To test the direct relationship, this study used a one-tailed test, so the critical value used for the t-distribution is1.64. The indirect relationship is tested using the Sobel test. The hypotheses test results from the LISREL software, illustrated in Figures 2 and 3 below, show that all hypotheses are accepted (HA are accepted and H0 are rejected).

Figure 2. Full Model – Loading Factors

Figure 3. Full Model – Path Coefficients

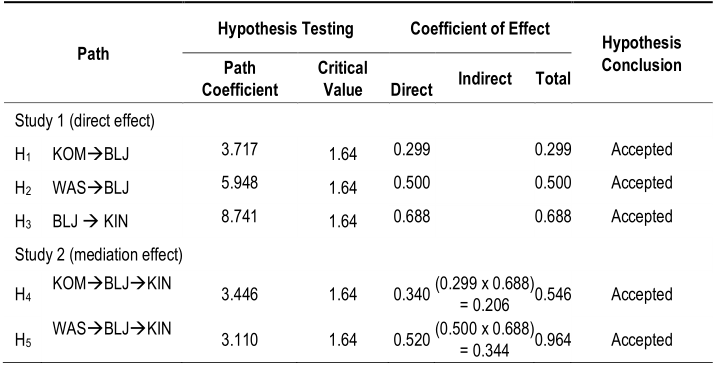

A summary of the hypothesis test results is shown in Table 4. The coefficient measurement results generated by LISREL show that the quality of education sector spending is influenced by the commitment of regional heads and the legislative oversight function, with the equation BLJ = 0.30 * KOM + 0.50 * WAS, Errorvar. = 0.57, R² = 0.43. The influence of the quality of education sector spending on educational performance is shown by the structural equation KIN = 0.69 * BLJ, Errorvar. = 0.53, R² = 0.47.

The first hypothesis shows that the path coefficient score of regional heads’ commitment to the quality of education sector expenditure is 3.717, which is greater than the critical value. Thus the null hypothesis is rejected, and H1 is accepted. It can be concluded that the commitment of regional heads has a significant positive effect on the quality of education sector expenditure, with a coefficient of determination R2 of 0.299. The second hypothesis generates a score for the path coefficient between legislative oversight and the quality of education sector expenditure of 3.484, which is greater than the critical value. Hence, the null hypothesis should be rejected, and H2 is accepted. It can be concluded that the oversight function of the DPRD has a significant positive effect on the quality of education sector expenditure, with a determination coefficient R2 of 0.500.

The third hypothesis indicates a robust path coefficient score of the quality of education sector expenditure on the educational performance of 8.741, which is above the critical value. Thus, it is necessary to reject the null hypothesis and accept H3. It can be concluded that the quality of education sector expenditure has a significant positive effect on educational performance, with a coefficient of determination R2 of 0.688. The fourth hypothesis shows that the path coefficient score of the regional heads’ commitment to educational performance through the quality of education sector expenditure is 3.446, which is higher than the critical value. Thus, it is decided to reject the null hypothesis and accept H4. It can be concluded that the commitment of regional heads has a significant positive effect on educational performance through the quality of education sector spending, with a determination coefficient R2 of 0.5457.

The last hypothesis test generated the path coefficient score of the DPRD oversight function against educational performance through the quality of education sector expenditure of 2.056, which is higher than the critical value. Thus, the null hypothesis is rejected, and H5 is accepted. It can be concluded that the oversight function of the DPRD has a significant and positive effect on educational performance indirectly through the quality of education sector expenditure, with a coefficient of determination R2 of 0.964.

DISCUSSION

Influence of Regional Heads’ Commitment on Quality of Education Sector Expenditure

Based on the hypothesis test result, the commitment of regional heads has a positive effect on the quality of education sector expenditure with a coefficient of determination of 0.299. The existence of this positive effect is due to the regional heads’ authority over the planning and implementation of APBD in accordance with laws. According to Law Number 17 of 2003 concerning state finance, the President delegates regional financial management powers to regional heads to plan, budget, implement, manage, and prepare a financial report as a manifestation of their accountability for regional budget implementation. The commitment of regional heads to allocate sufficient budgets and personnel in the education sector in accordance with the provisions and for the best interests of their regions is crucial in improving the quality of education sector spending.

Furthermore, according to this research, several indicators have strengthened the influence of regional heads’ commitment to the quality of education sector expenditure, such as delegation of authority and responsibility to subordinates; the setting of performance targets for all teaching personnel, and evaluation of their achievements; and efforts to improve the capacity and competency of relevant education personnel. This supports the research of Babatunde (2015), where leaders influenced the management of public spending. Andrews & Boyne (2010) further explained that a good public management system optimizes leaders’ managerial capacity to improve local governments’ performance through the integration of effective leadership.

Budget allocation for the education sector in the APBD continues to increase to meet the mandatory 20 percent of the APBD's portion. However, from 2015 to 2019, the majority of local governments were still dependent on transferred funds from the central government to meet the requirement of their education sector budget provisions. This indicates a limitation for the regional heads to exercise their commitment to improving the quality of education sector spending.

Effect of DPRD Oversight Function on Quality of Education Sector Expenditure

The hypothesis test result shows that the DPRD's oversight function has a positive effect on the quality of education sector spending with a coefficient of determination of 0.50. This influence shows empirically that the better the DPRD’s oversight functions, the better the quality of local government spending. The oversight function of the DPRD starts at the ex-ante stage during the drafting of the APBD. The DPRD is involved in every stage of the planning of local government programs/activities, including education programs, by providing recommendations and insights for improvement to the regional government's budget proposal. The ex-post oversight function of the DPRD is exercised through the efforts of the DPRD by actively overseeing the implementation of the programs/activities, particularly in education, and in evaluating the implementation of these programs/activities. The essential roles of the DPRD in ex-ante and ex-post oversight are inseparable from the existence of a sufficient role of the supporting legislative structure, such as the commission, which includes the education commission and the parliament’s budget agency. The positive relationship between the dimensions of the DPRD's oversight function and the quality of education spending is manifested in, among other things, the timeliness of budget approval and the approval of local government's financial and accountability reports, including financial and accounting reports about education sector programs/activities. The result of this study is consentaneous with those by Stapenhurst (2011), who argued that legislature function in the budgeting process is a tool to control government activities in accordance with the necessity for activities approved by the people's representatives.

This study, however, discloses two aspects of the quality of education sector expenditure that still need to be improved by the local governments: budget proportion for capital expenditure and subvention allocations in the education sector. Both issues, if addressed properly through the oversight function of the DPRD, especially at the ex-ante stage during the APBD drafting processes, could resolve the inequitable distribution problems ofschool infrastructure and education personnel throughout the region while simultaneously providing equal opportunities to economically disadvantaged students to obtain a proper education.

Influence of Quality of Education Sector Expenditure on Educational PerformanceThe hypothesis test result indicates that the quality of education sector spending has a positive effect on educational performance with a coefficient of determination of 0.688. This result is in line with previous studies that explain a positive relationship between government spending and performance (Ebi and Ubi, 2017; Rajkumar and Swaroop, 2008; Wahaba et al.: 2018, pp. 32-65).

Particularly in the education sector, Wardhani et al. (2017) found that education sector expenditure improves the performance of education in the current year and for a few years going forward. This was mainly due to the timeliness of APBD approval and proper distribution of authorities in education services delivery between the central, provincial, and district or municipal governments. Those two aspects have helped local governments to increase the conformity of local government education programs/activities to be in line with national education service standards, particularly in the application of the curriculum, utilization of teaching materials, implementation of teaching methods, and in-classroom teaching sufficiency.

However, the result of testing this hypothesis also indicates the need for efforts to increase the allocation of capital expenditures in the education sector to support the fulfillment of minimum educational infrastructure standards, including equal distribution of the school infrastructure throughout the region, that is expected to improve the quality of the teaching process. This, in turn, helps students to increase their performance—i.e., an improvement on average national exam scores and student achievements at national and international levels.

Effect of Regional Heads’ Commitment to Educational Performance through Quality of Education Sector Expenditure

The test result of the fourth hypothesis shows that the commitment of regional heads has a positive effect with the total coefficient of determination of 0.546 percent on educational performance through the quality of education sector expenditure. This finding is consistent with previous studies by Andrews & Boyne (2010), Babatunde (2015), and Erlina & Muda (2017), which stated that the commitment of the regional head encourages the success of the program. Regional heads have a pivotal role in encouraging organizations to work harder and strive to achieve optimal performance.

Further analysis of respondents’ answers to the questionnaire indicates that regional heads have sufficiently delegated authority and responsibility to subordinates in the form of targets, including evaluating the performance achievements of teaching personnel. Moreover, regional heads have provided an adequate budget for the development of the capacity and competency of educational personnel, especially teachers. This policy improves the quality of the spending, as capacity development of teachers is a priority of the local government; it also improves the quality of teaching delivery, according to the teaching methods and materials stipulated in the national standard.

In addition, the commitment of regional heads to increase the quality of education sector expenditure is still constrained by the uneven distribution of teachers in every sub-district, which is caused by the limited availability of teachers and the reluctance of teachers to be positioned in certain remote areas. This issue has lowered educational performance, particularly in regions that have larger areas with limited access.

Effect of DPRD Oversight Function on Educational Performance through Quality of Education Sector Expenditure

The test result of the fifth hypothesis indicates that DPRD's oversight function has a positive effect on educational performance through the quality of education sector expenditure with a coefficient of determination of 0.964. The test results for the direct influence of the DPRD's oversight function on educational performance only showed a magnitude of 0.520; however, the intervention of quality of education expenditure increased the indirect effect of DPRD's oversight function on educational performance by 0.444 (0.964 – 0.520). This shows that the influence of the DPRD is more intense if it engages comprehensively in determining the quality of the education expenditure budget in the ex-ante stage; actively and continuously scrutinizes budget execution activities in the ex-post stage, and provides insights and recommendations in the evaluation phase.

In the ex-ante stage, the role of DPRD's oversight to enhance educational performance through spending quality can still be increased through DPRD efforts to allocate more capital expenditure and subsidy to education. Increased capital spending is needed to provide adequate school facilities and infrastructure, while increased subsidy is expected to reduce the opportunity gap in obtaining an education, especially for underprivileged students.

This hypothesis result is in line with the research of Widajatun et al. (2020), which showed a positive relationship between the quality of council oversight and the performance of local governments. Other studies have also revealed that members of local parliament’s understanding of the management of regional budgets had a positive impact on the quality of DPRD supervision (Winarna & Murni, 2007, pp. 136-152).

CONCLUSION

The main result of this study highlights the large indirect influence of DPRD's oversight function on educational performance through the quality of education sector expenditure. Enhancing DPRD's oversight function throughout the budgeting cycle adds value to the quality of education sector spending and may simultaneously encourage better educational performance. This study also found a positive relationship between the commitment of regional heads and educational performance, both directly and indirectly, through the quality of education sector expenditure. Regional heads’ commitment is manifested in the form of delegating authority and responsibility to subordinates, conducting training programs to increase the capacity and competency of education personnel, establishing performance targets to teaching personnel, and evaluating the achievement of performance targets.

However, three areas require more attention from the local governments. Firstly, the allocation of teaching staff is not yet optimal and evenly distributed, especially in remote areas. Secondly, there is the unequal distribution of school infrastructure and facilities throughout the region due to a lower proportion of educational capital expenditure compared to other types of expenditure. Thirdly, the budget allocation for subsidies and assistance in education to increase equal opportunities, especially for underprivileged students, has not been sufficient to drive improvement in the attainment of performance indicators in the education sector.

Our research suggests strengthening the local legislative role at the ex-ante stage to determine the budget priority of education, particularly in terms of allocating more budget to capital expenditure and subsidy to underprivileged students. More allocation of capital expenditure for school infrastructure and more allocation for subsidies or assistance for poorer students are some of the critical efforts required to boost the quality of education sector spending. In the ex-post phase, educational performance could be improved through inherent oversight activities during the implementation of educational programs and activities.

We also encourage further research to identify other factors that influence the performance of education in Indonesia. Such research will broaden our understanding of obstacles to the escalation of the education sector performance in Indonesia, especially at the regional level.

BIODATA

I. YATUN: Isma Yatun is a board member of the Audit Board of the Republic of Indonesia. She is also a former member of the Indonesian House of Representatives on the commission in charge of education sector. She has experience in local government financial management. She is currently a doctoral candidate of Accounting in Universitas Padjadjaran

S. MULYANI: Sri Mulyani is a Rector in Universitas Singaperbangsa Karawang. She has experienced more than 25 years in the field of information systems and good governance for the private, public, and sharia sector. She actively writes and gives consultations to analyze and design applied information systems, good governance, sharia finance, and others. She is currently the National Council Member of the Institute of Indonesia Chartered Accountants

S. WINARNINGSIH: Srihadi Winarningsih is a lecturer in the Accounting Department, Economic and Business Faculty, Universitas Padjadjaran. She finished her doctoral program in business management, focused on accounting studies from Universitas Padjadjaran. She has a specialization in Auditing

C. SUKMADILAGA: Citra Sukmadilaga is a lecturer in the Accounting Department, Economic and Business Faculty, Universitas Padjadjaran. He finished his doctoral program in finance from University Putra Jaya Malaysia. He has a specialization in Accounting and Finance

BIBLIOGRAPHY

AL-AZHAR, A, RATNAWATI, V, & ADHA, W (2014). “Pengaruh akuntabilitas, ketidakpastian lingkungan, dan komitmen pimpinan terhadap penerapan transparansi pelaporan keuangan (studi empiris pada skpd kota dumai) (doctoral dissertation, riau university)”.Jom Fekon, 1(2), pp. 32-58.

ANDREWS, R, & BOYNE, G, A (2010). “Capacity, leadership, and organizational performance: testing the black box model of public management”. Public administration review, 70(3), pp. 443-454.

BABATUNDE, S, A, ONODUGO, V, A, & DANDAGO, K, I (2015). “The effects of leadership quality on public expenditure management: evidence from lagos state treasury under akinwunmi ambode as accountant general”. International Journal of Business, Economics and Law, 6(1), pp. 125-141.

BALAJ, D, & LANI, L (2017). “The impact of public expenditure on economic growth of Kosovo”. Acta Universitatis Danubius. Œconomica, 13(5), pp. 452-471.

CHAPMAN, D, W, & ADAMS, D, K (2002). “The quality of education: dimensions and strategies. hong kong: asiandevelopment bank. International Journal of Business, Economics and Law, 12(1), pp. 75-96.

DIYANAYATI, K, & WENINGTYASTUTI, R (2018). “The local government commitment on the implementation of social welfare”. Journal Penelitian Kesejahteraan Sosial, 16(2), pp. 173-184.

ERLINA, A, S, & MUDA, I (2017). “Antecedents of budget quality empirical evidence from provincial government inIndonesia”. International Journal of Economic Research, 14(12), pp. 301-312.

HASIBUAN, A (2017). “Kebijakan Pemerintah Daerah Dalam Peningkatan Kualitas Pendidikan Di Provinsi Sumatera Utara”. International Journal of Business, Economics and Law, 10, pp. 125-146.

JOHARI, R, J, ALAM, M, M, & SAID, J (2018). “Assessment of management commitment in Malaysian public sector”.Cogent Business & Management, 5(1), pp. 146-175.

NASUTION, M, K, & SURBAKTI, A, H, (2020). “Trends, patterns, and the relationship of computer-based nationalexamination of high school science students”. In Journal of Physics: Conference Series, 14(1), pp. 35-55.

PELIZZO, R, & STAPENHURST, R (2004). “Tools for legislative oversight: an empirical investigation”. The WorldBank, 12(3), pp. 21-48.

ROSSER, A (2018). “Beyond access: making indonesia’s education system work”. International Journal of Business,Economics and Law, 13, pp. 123-141.

SCHLEICHER, A (2019). “PISA 2018: insights and interpretations”. OECD Publishing, 25(1), pp. 35-65.

STAPENHURST, F, C (2011). “Legislative oversight and curbing corruption: presidentialism and parliamentarianismrevisited”. International Journal of Business, Economics and Law, 6(2), pp. 54-75.

WAHAB, A, A, O, A, KEFELI, Z, & HASHIM, N (2018). “Investigating the dynamic effect of healthcare expenditure and education expenditure on economic growth in organisation of islamic countries (oic). International Journal of Business, Economics and Law, 3, pp. 32-65.

WAHYUNI, S, JUANDA, B, & FAHMI, I (2017). “Kualitas belanja daerah dan hubungannya dengan kinerjapembangunan di provinsi banten. Journal Ekonomi dan Kebijakan Pembangunan, 6(2), pp. 16-31.

WARDHANI, R, ROSSIETA, H, & MARTANI, D (2017). “Good governance and the impact of government spending on performance of local government in Indonesia”. International Journal of Public Sector Performance Management, 3(1), pp. 77-102.

WIDAJATUN, V, W, & KRISTIASTUTI, F (2020). “The effect of regional financial supervision, accountability and transparency of regional financial management on local government performance”. Budapest International Research and Critics Institute (BIRCI-Journal): Humanities and Social Sciences, 3(4), pp. 296-320.

WINARNA, J, & MURNI, S (2007). “Pengaruh personal background, political background dan pengetahuan dewan tentang anggaran terhadap peran DPRD dalam pengawasan keuangan daerah (Studi Kasus Di Karesidenan Surakarta dan Daerah Istimewa Yogyakarta Tahun 2006)”. Journal Bisnis Dan Akuntansi, 9(2), pp. 136-152.

WULANDARI, D, & MURTIANTO, Y, H (2017). “Structural equation modeling sebagai materi untuk pengembangan modul mata kuliah komputasi statistik”. Journal Ilmiah Teknosains, 3(1), pp. 45-65.