Artículos

Competency and quality of financial reporting management of Blud hospitals in west Java Province

Calidad y competencia de gestión de informes financieros de los hospitales BLUD en la provincia de Java Occidental

R. PUSPITASARI puspita.dindha@gmail.com

W. YADIATI yadiati@gmail.com

S WINARNINGSIH srihadi.winarningsih@unpad.ac.id

IRIYADI d_iriyadi@yahoo.co.id

R. PUSPITASARI puspita.dindha@gmail.com

W. YADIATI yadiati@gmail.com

S WINARNINGSIH srihadi.winarningsih@unpad.ac.id

IRIYADI d_iriyadi@yahoo.co.id

Competency and quality of financial reporting management of Blud hospitals in west Java Province

Utopía y Praxis Latinoamericana, vol. 26, núm. Esp.3, pp. 37-46, 2021

Universidad del Zulia

Recepción: 26 Abril 2021

Aprobación: 30 Mayo 2021

Abstract: This study aims to empirically prove whether the competency of financial reporting managers positively affects the financial statements' quality and performance accountability. Data were collected from questionnaires and interviews conducted at a number of BLUD hospitals in West Java Province and analyzed using SEM-PLS. from the returned questionnaires of 96 respondents, and the results show that the competency of financial reporting managers has a direct positive effect on the quality of financial statements but has no effect on performance accountability. But, the quality has a positive effect on performance.

Keywords: Competency of financial reporting managers, quality of financial statements, performance accountability, hospitals..

Resumen: Este estudio tiene como objetivo probar empíricamente si la competencia de los gerentes de informes financieros afecta positivamente la calidad de los estados financieros y la responsabilidad del desempeño. Los datos se recopilaron a partir de cuestionarios y entrevistas realizados en varios hospitales BLUD en la provincia de Java Occidental y se analizaron mediante SEM-PLS. A partir de los cuestionarios devueltos por 96 encuestados, los resultados muestran que la competencia de los gerentes de informes financieros tiene un efecto positivo directo en la calidad de los estados financieros, pero no tiene ningún efecto en la responsabilidad del desempeño. Pero, a través de su calidad, tienen un efecto positivo en la responsabilidad del desempeño.

Palabras clave: Competencia, calidad, responsabilidad, hospitales.

INTRODUCTION

The designation of Regional hospitals as government institutions to become Regional Public Service Bodies (BLUD) aims to increase accountability and transparency in the health sector (Bakalikwira et al.; 2017, pp. 133-169). To be accountable for financial management and service activities, the BLUD prepares and serves financial statements from performance reports (Ballantine et al.: 1998, pp. 71-94). Financial statements include budget realization/operational reports (activity reports/surplus deficit reports), balance sheets, cash flow reports, financial report notes, and performance reports. Several empirical studies explain that quality financial statements are needed to create accountability in the public sector (Bartkus et al.: 2006, pp. 86-94). Financial statements, based on IAI (2012), are parts of the financial reporting process since they are the results (output) of processes of transactions or other events categorized based on their nature and function. The financial statements of Regional General Hospitals (RSUD) with BLUD status are prepared to provide information related to 1) Financial position, 2) Financial performance and, 3) Financial changes. But, until 2016, 409 of 668 new RSUDs (61.23%) had implemented the BLUD Financial Management Pattern (PPK) (Eeckloo et al.: 2004, pp. 1-15). This is due to the lack of understanding of the difference between the application of the Financial Accounting Standards (SAK) and the Government Accounting Standards (SAP). Besides, the inappropriate implementation process is also due to the lack of technical skills of financial managers for BLUD financial accounting and reporting (Beck: 20118, pp. 785-826). This then indicates that the competency of financial managers affects the quality of financial statements (Vainieri et al.: 2019, pp. 306- 325).

Financial reporting managers who are competent in financial accounting are valuable assets forgovernment agencies because they will have a great influence in the preparation of quality financial statements (Reinstein & Luecke: 20001, pp. 56-56). Previous studies find that the most basic problem in making financial statements is that the financial management parties do not have an educational background in accounting (Thomas et al.: 2008, pp. 122-141). Therefore, this causes an obstacle since the financial statement managers are not fully ready to prepare and serve financial statements so that the quality of financial statements does not meet the normative principles required by the Government Accounting Standards (SAP) (Tasi et al.: 2019, pp. 256-262). The variables in this study have been widely discussed (Greenwood et al.: 2017, pp. 831-855). However, there are still inconsistent results. Previous research emphasizes human resource competency variables in general that affect the quality of financial statements without discussion of their impact on accountability (Safkaur & Sagrim: 2019, pp. 29-41). Likewise, this also happens in the study that focuses more on SKPD (Regional Work Units). Therefore, this study is important to answer problems that occur at BLUD Hospitals and to test how many competencies of financial managers affect the quality of financial statements and performance accountability. This research is expected to provide academic contributions and recommendations to help to solve the problems in BLUD hospitals, especially in West Java Province.

LITERATURE REVIEW

Competency of Financial Reporting Manager

Human resource competency as a financial manager can be defined as the human ability to apply or use knowledge, skills, abilities, behavior, and personal characteristics related to the quality of the financial statements produced (Curtright et al.: 2000, pp. 58-68). In this study, human resource competencies refer to characteristics of human resources as financial managers in carrying out accounting tasks to produce quality financial statements (Ganyam & Ivungu: 2019, pp. 39-49). Besides, the relation between human resource competency and the quality of financial statements refers to the competency standards of accounting graduates set by IFAC (International Federations of Accountants), namely IES (International Education's Standards in IES 2, IES 3, and IES 4) including the dimensions of knowledge, skills, and attitude (Kaplan & Norton: 2001, pp. 87-104). Based on these dimensions, in managing good finances, experienced and quality human resources supported by a basic accounting education and training background are needed because they are able to implement accounting systems and understand accounting logic well (Duran et al.: 2019, pp. 199-220). Byincreasing the competency of human resources at the system, institutional, and individual levels supported by the application of an accounting system, it is expected that financial managers, especially accounting, are able to carry out accounting duties and functions properly, which ultimately leads to good governance (Cohen et al.: 2019, pp. 23-46).

Quality of Financial Statements

Financial statements are a product of financial reporting regulated in accounting standards, managerial policies and strengthened by supervision mechanisms (Calhoun et al.: 2008, pp. 123-143). In other words, the financial reporting process is not only for producing output in the form of financial statements (Brown: 2013, pp. 25-34) but also aims to produce and provide high-quality financial statements. Based on literature (Bracci et al.: 2015, pp. 37-64), in this study, the dimensions and indicators refer to the study results of operational measurement on the variable of financial reporting quality in the research of Iriyadi et al. (2018), which refers to the framework 2010 (IASB, 2010).In this study, 21 questionnaire questions adopted from Calhoun et al. (2008) were used to Measure each dimension of the qualitative characteristics of financial statements.

Accountability of Government Agency’s Performance

Thomas et al. (2008), in their research which refers to Inpres no. 7 of 1999, describes that "the performance accountability of government agencies is a manifestation of the obligations of a government agency to be accountable for the success in achieving the set goals and objectives through periodic accountability." Likewise, based on the description by Eeckloo et al. (2004) describe performance accountability of Government Agencies as a manifestation of the obligations of a Government agency that aims to be accountable for the successful implementation of the organization’s mission in achieving the goals and objectives set through periodic accountability. Several previous studies (Ballantine et al.: 1998, pp. 71-94) leads the Five dimensions of accountability, including transparency, liability, controllability, responsibility, and responsiveness, to become the basis and reference for measuring the performance accountability of Government Agencies in this research.

Research Hypothesis

Competency is the basic capital of human resources in an organization to achieve the goals or objectives of the organization, which is measured based on the educational background of financial managers. Several studies explain that the competency of financial managers has a positive effect on the quality of financial statements. Thus, the hypothesis is

H1: The competency of a financial manager has a positive effect on the quality of financial statements Likewise, the competency of financial managers has an important role in increasing the performanceaccountability of government agencies. Several previous studies indicate that the competency of financial managers has a positive effect on the accountability of government agencies. Thus, the hypothesis is

H2: The competency of financial managers has a positive effect on performance accountability.

Competency is the basic capital of human resources in an organization to achieve the goals or objectives of the organization, which is measured based on the educational background of financial managers (Pandey, 2014). Several studies show that the competency of financial managers has a positive effect on the quality of financial statements. Likewise, competency has an important role in increasing the performance accountability of government agencies. Several previous studies show that the competency of financial managers has a positive influence on the accountability of government agencies. Thus, the hypothesis of this study is

H3: The competency of a financial manager has a positive effect on the quality of financial statements on performance accountability.

METHODOLOGY

The target population in this study is 44 BLUD hospitals of 51 RSUDs in (Ganyam & Ivungu: 2019, pp. 39- 49). The units observed in this study were the head of the finance/accounting division, the head of the finance/accounting sub-division, and the accounting staff. The primary data were collected through questionnaires consisting of closed questions provided with a column for opinions/comments, while open questions were delivered through face-to-face interviews to obtain real facts and information. The data were analyzed using instruments adapted from previous researchers.

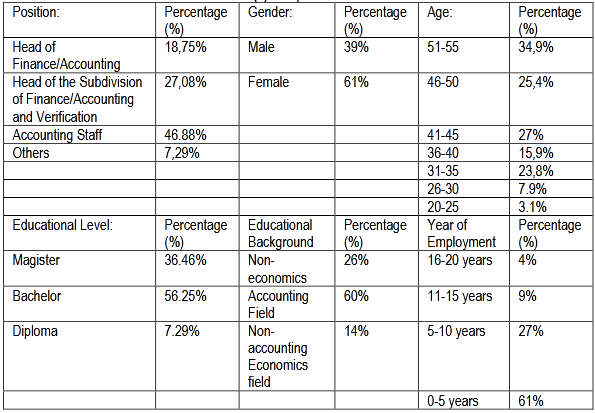

Respondent Profile

In this study, the data were collected from96 respondents from a number of BLUD hospitals in West Java Province. The profiles of respondents in this study were divided into position, gender, age, educational level, educational background, and year of employment for the position at BLUD hospital. The description of the demographic profile of the respondents is as follows:

RESULTS

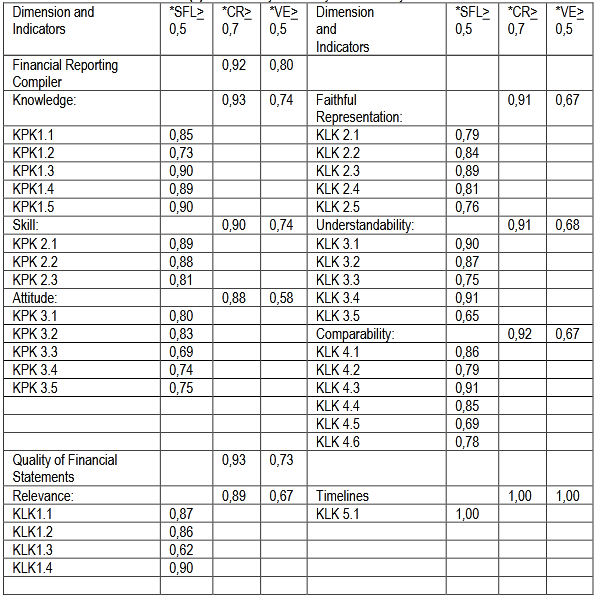

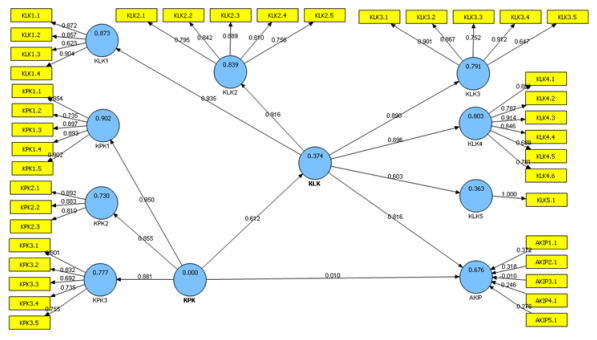

Table 2 shows that all values of standardized factor loading are ≥ 0.50, meaning that all indicators are valid. Likewise, the reliability of the measurement model is shown by the value of CR ≥ 0.70 and VE ≥ 0.50. Therefore, it can be concluded that all dimensions and indicators of the variables of the competency of financial managers and the quality of financial statements are valid and reliable in this study.

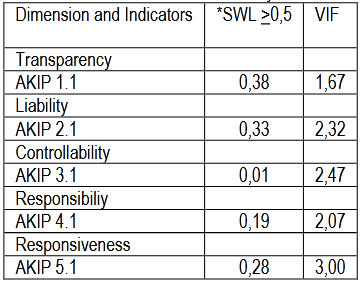

The variable of BLUD hospital performance accountability in this study has a formative model so that it is different from other latent variables. Furthermore, the results of the measurement model testing for each dimension and indicator of this variable are presented in Table 3. This indicates that based on the measurement model testing, all dimensions/indicators are valid and reliable.

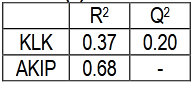

Coefficient of Determination (R2) and Predictive Relevance (Q2) Test

Table 4 shows that the R2value of the variable of financial statements quality (KLK) is 0.37, meaning that the influence of financial management commitment to the quality of financial statements is 37%, while the 63% is influenced by other variables not observed in this study. The influence of the competency of financial managers on the performance accountability of BLUD Hospital is 68%, and the 32% is influenced by other variables. Table 4 also shows that the Q2 value for the endogenous latent variable of financial statements quality is 0.20 (Q2> 0), so it is predictive relevance. However, the performance accountability variable does not have a Q2 value because it is a formative latent variable.

Structural Model Test

Hasil pengujian statistik terhadap pengukuran model struktural menghasilkan persamaan Statistical test on the structural model measurements forms the following equation:

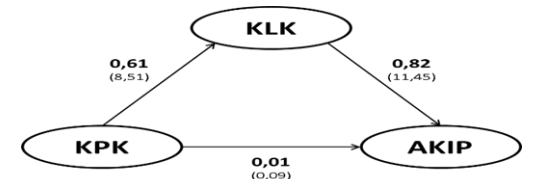

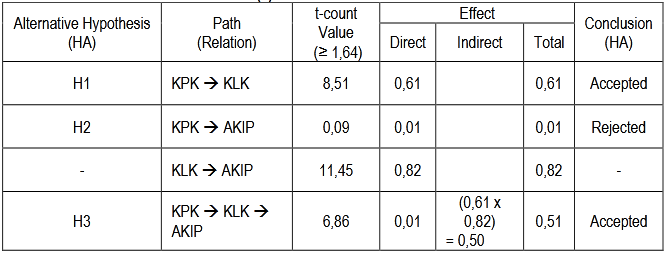

η_1= 0,61*ξ_1+0,63

η_2= 0,01*ξ_1+ 0,82*η_1+ 0,32

Keterangan:

ξ_1: Latent variable (dimension) of competency of financial reporting managers

η_1: Latent variable (dimension) of financial statement quality

η_2: Latent variable (dimension) of the performance accountability of government agencies γ: Path coefficients between exogenous latent variables and endogenous latent variables β: Path coefficient between two endogenous latent variables

ζ: Measurement error in endogenous latent variables

The following is the SEM model with path coefficient and t-count showing the results of hypothesis testing and the value of the causal relationship between the research variables.

Figure 1. SEM Model with Path Coefficient and t-count value

Figure 2.SEM Model Smart-PLSOutput

DISCUSSION

Educational background in accounting is important for financial reporting managers to improve the quality of financial statements. In this study, the majority of the respondents (60%) have an accounting educational background. The results of hypothesis testing in table 5 show that the competency of financial managers has a positive effect on the quality of the BLUD Hospital financial statements. This supports several studies which state that the competency of financial managers has a positive effect on the quality of financial statements (Ballantine et al.: 1998, pp. 71-94). Furthermore, the results of the descriptive analysis show that the variable of financial managers’ competency is good, with an average score of 3.50. This is shown by some findings that financial managers understand a clear role and function in financial management, understand accounting procedures and processes, understand the main duties as a financial manager, are able to compile and present balance sheets, cash flow reports, statement of changes in equity, and financial statement notes, and has performed roles and responsibilities as a financial manager. The next hypothesis testing shows that the competency of financial managers has no positive effect on the performance accountability of BLUD hospitals. This finding is in contrast with research (Duran et al.: 2019, pp. 199-220) which shows that competence has a positive effect on the performance accountability of government agencies. It is not easy for financial managers to face intervention from superiors that violate the rules, thus causing the fact that the performance of the financial management unit is not clearly disclosed. A respondent from one of the BLUD Hospitals also stated that as the financial person in charge manager, he had actually carried out 100% but not including all forms of reporting that had to be accounted for by the RSUD to those concerned. However, this result is in line with Calhoun et al. (2008), which state that competency has no positive effect on accountability. On the other hand, the competency of financial managers shows a positive effect on the performance accountability of BLUD hospitals through the quality of financial statements. This finding confirms researches from (Reinstein & Luecke: 20001, pp. 56-56) which shows that the competency of financial managers has a positive effect on the quality of financial statements. Likewise, competency has an important role in increasing the accountability of the performance of government agencies (Calhoun et al.: 2008, pp. 123-143). this is mainly affected by the indicators of the dimensions of knowledge and attitude that show a good average value of 3.59 and 3.52, respectively.

CONCLUSION

The results of the study indicate that the competency of financial managers has a positive effect on the quality of financial statements, which positively affects the performance accountability of BLUD hospitals. This proves that quality financial statements are needed to create public-sector accountability better the quality of financial statements, the better the performance accountability. In this study, the accounting competency of financial managers was assumed to affect the quality of financial statements. The results then prove that the competency of financial reporting managers has a positive effect on the quality of financial statements but has no positive effect on the performance accountability of BLUD hospitals. However, the competency of financial reporting managers through the quality of financial statements has an indirect positive effect on the performance accountability of BLUD hospitals in West Java. It is affected by several factors such as indicators of the dimensions of financial manager’s competency, which show a good average score. This study suggests that to create quality financial statements and improvement on performance accountability at BLUD hospitals, financial managers need the motivation to update and upgrade their supporting skills to increase their competency as financial managers. It is also important to conduct training activities with materials designed to support competency as a financial manager.

BIODATA

R. PUSPITASARI: Ratih Puspitasari is currently a doctoral student of accounting at the Faculty of Economic and Business, Padjajaran University, Indonesia. Her main research interests are Economics and Accounting.

W. YADIATI: Winwin Yadiati is a lecturer the Faculty of Economic and Business, Padjajaran University, Indonesia.

S. WINARNINGSIH: Srihadi Winarningsih is a lecturer of Accounting Department at the Padjadjaran University. Her research interests include Auditing, Internal Auditing, and Bussiness Ethics.

IRIYADI: Iriyadi is the Head of Research and Community Service (Accounting) at institute of business and informatics kesatuan, Bogor Indonesia. His main research interest is accounting.

BIBLIOGRAPHY

BAKALIKWIRA, L, BANANUKA, J, KAAWAASE KIGONGO, T, MUSIMENTA, D & MUKYALA, V (2017).“Accountability in the public health care systems: A developing economy perspective”. Cogent Business & Management, 4(1), pp. 133-169.

BALLANTINE, J, BRIGNALL, S & MODELL, S (1998). “Performance measurement and management in public health services: a comparison of UK and Swedish practice”. Management Accounting Research, 9(1), pp. 71-94.

BARTKUS, B, GLASSMAN, M & MCAFEE, B (2006). “Mission statement quality and financial performance”.European Management Journal, 24(1), pp. 86-94.

BECK, A, W (2018). “Opportunistic financial reporting around municipal bond issues”. Review of Accounting Studies, 23(3), pp. 785-826.

BORITZ, J. E., EFENDI, J., & LIM, J. H. (2018). The impact of senior management competencies on the voluntary adoption of an innovative technology. Journal of Information Systems, 32(2), 25-46.

BRACCI, E, STECCOLINI, I, HUMPHREY, C, MOLL, J, HEALD, D & HODGES, R (2015). “Will “austerity” be acritical juncture in European public sector financial reporting?”. Accounting, Auditing & Accountability Journal, 12, pp. 37-64.

BROWN, A, M (2013). “Nursing Accounting Competencies Related to HIV in a Papua New Guinea Context”. Journal of the Association of Nurses in AIDS Care, 24(5), pp. 25-34.

CALHOUN, J, G, DOLLETT, L, SINIORIS, M, E, WAINIO, J, A, BUTLER, P, W, GRIFFITH, J, R & WARDEN, G, L(2008). “Development of an interprofessional competency model for healthcare leadership”. Journal of healthcare management, 53(6), pp. 123-143.

COHEN, S, BISOGNO, M & MALKOGIANNI, I (2019). “Earnings management in local governments: The role of political factors”. Journal of Applied Accounting Research, 1, pp. 23-46.

CURTRIGHT, J, W, STOLP-SMITH, S, C & EDELL, E, S (2000). “Strategic performance management: development of a performance measurement system at the Mayo Clinic”. Journal of Healthcare Management, 45(1), pp. 58-68.

DURAN, A, CHANTURIDZE, T, GHEORGHE, A & MORENO, A (2019). “Assessment of public hospital governance in Romania: lessons from 10 case studies”. International journal of health policy and management, 8(4), pp. 199- 220.

EECKLOO, K, VAN HERCK, G, VAN HULLE, C & VLEUGELS, A (2004). “From Corporate Governance To Hospital Governance.: Authority, transparency and accountability of Belgian non-profit hospitals’ board and management”. Health Policy, 68(1), pp. 1-15.

GANYAM, A, I & IVUNGU, J, A (2019). “Effect of accounting information system on financial performance of firms: Areview of literature”. Journal of Business and Management, 21(5), pp. 39-49.

GREENWOOD, M, J, BAYLIS, R, M & TAO, L (2017). “Regulatory incentives and financial reporting quality in public healthcare organisations”. Accounting and Business Research, 47(7), pp. 831-855.

KAPLAN, R, S & NORTON, D, P (2001). “Transforming the balanced scorecard from performance measurement tostrategic management: Part 1”. Accounting horizons, 15(1), pp. 87-104.

REINSTEIN, A & LUECKE, R, W (2001). “AICPA Standard can help improve committee performance”. Healthcare Financial Management, 55(8), pp. 56-56.

SAFKAUR, O & SAGRIM, Y (2019). “Impact of Human Resources Development on Organizational Financial Performance and Its Impact on Good Government Governance. International Journal of Economics and Financial Issues, 9(5), pp. 29-41.

TASI, M, C, KESWANI, A & BOZIC, K, J (2019). “Does physician leadership affect hospital quality, operational efficiency, and financial performance?”. Health Care Management Review, 44(3), pp. 256-262.

THOMAS, J, COLLINS, A, COLLINS, D, HERRIN, D, DAFFERNER, D & GABRIEL, J (2008). “The language ofbusiness: a key nurse executive competency”. Nursing Economics, 26(2), pp. 122-141.

VAINIERI, M, FERRE, F, GIACOMELLI, G & NUTI, S (2019). “Explaining performance in health care: How and whentop management competencies make the difference”. Health care management review, 44(4), pp. 306-325.