Contabilidad de Gestión

Opportunity of robust research in Accounting: a literary analysis on performance indicators in the management of municipal governments

Oportunidad de investigaciones robustas en contabilidad: un análisis literario sobre evaluación de rendimiento en la gestión de los gobiernos municipals

Oportunidade de pesquisas robustas em contabilidade: uma análise literária sobre avaliação de desempenho na gestão dos governos municipais

Opportunity of robust research in Accounting: a literary analysis on performance indicators in the management of municipal governments

Contabilidad y Negocios, vol. 14, no. 28, pp. 126-142, 2019

Pontificia Universidad Católica del Perú

This work is licensed under Creative Commons Attribution-NonCommercial-NoDerivs 4.0 International.

Received: 27 July 2017

Accepted: 20 December 2018

Abstract: The study investigates gaps of potential research in accounting, about performance evaluation (PE) in public management, and analyze how the performance evaluation system (PES) contributes to the effectiveness of such management. The research was motivated by the dissemination of a set of PE recommendations for public management by the United Nations Commission (UNC) and ratified by the System of National Accounts (SNA) in 1993 and in 1995 by the European System of National Accounts (ESNA) and the Commission of the European Union (CEU). As well as the discussions in events and periodicals of public accounting on the subject in question. The method applied to achieve the objectives of this study was the search for key words in the Spell, Scopus and Web of Science databases from 1993 to 2016. The results reveal little or no research on PE with the application of performance indicators (PIs) in public management, and that diagnoses by PIs can contribute to the decision-making process by the public manager in bud- get execution and assist the oversight bodies in assessing the effectiveness of government. The study suggests potential opportunities for empirical research on PE in public management with the application of management techniques developed by management accounting practices, internal process reengineering, costs, budget and total quality.

Keywords: Performance evaluation, public administration, efficiency and effectiveness in public management.

Resumen: El estudio investiga lagunas de investigación potencial en contabilidad, sobre evaluación de desempeño (AD) en la gestión pública y analiza cómo el sistema de evaluación de desempeño (SAD) contribuye a la eficacia de dicha gestión. La investigación fue motivada por la diseminación de un conjunto de recomendaciones de AD para gestión pública por la Comisión de las Naciones Unidas (CNU) y ratificada por el Sistema de Cuentas Nacionales (SCN) en 1993 y 1995 por el Sistema Europeo de Cuentas Nacionales (SECN) Comisión de la Unión Europea (CUE). Así como las discusiones en eventos y periódicos de contabilidad pública sobre el asunto en cuestión. El método aplicado para alcanzar los objetivos de este estudio fue la búsqueda de palabras clave en las bases de datos Spell, Scopus y Web of Science de 1993 a 2016. Los resultados revelan poca o ninguna investigación sobre AD con la aplicación de indicadores de desempeño (IDs) en la gestión pública, y que los diagnósticos por IDs pueden contribuir al proceso de toma de decisión por el gestor público en la ejecución presupuestaria y auxiliar a los órganos de supervisión en la evaluación de la eficacia del gobierno. El estudio sugiere potenciales oportunidades de investigación empírica sobre AD en la gestión pública con la aplicación de técnicas de gestión desarrolladas por prácticas de contabilidad gerencial, reingeniería interna de procesos, costos, presupuesto y calidad total.

Palabras clave: evaluación de rendimiento, administracion publica, eficiencia y eficacia en la gestión pública.

Resumo: O estudo investiga lacunas de pesquisa potencial em contabilidade, sobre avaliação de desempenho (AD) na gestão pública, e analisa como o sistema de avaliação de desempenho (SAD) contribui para a eficácia de tal gestão. A pes- quisa foi motivada pela disseminação de um conjunto de recomendações de AD para gestão pública pela Comissão das Nações Unidas (CNU) e ratificada pelo Sistema de Contas Nacionais (SCN) em 1993 e em 1995 pelo Sistema Europeu de Contas Nacionais (SECN) e a Comissão da União Europeia (CUE). Assim como as discussões em eventos e periódicos de contabilidade pública sobre o assunto em questão. O método aplicado para alcançar os objetivos deste estudo foi a busca de palavras-chave nas bases de dados Spell, Scopus e Web of Science de 1993 a 2016. Os resultados revelam pouca ou nenhuma pesquisa sobre AD com a aplicação de indicadores de desempenho (IDs) em gestão pública, e que os diagnósticos por IDs podem contribuir para o processo de tomada de decisão pelo gestor público na execução orçamentária e auxiliar os órgãos de supervisão na avaliação da eficácia do governo. O estudo sugere oportunidades potenciais de pesquisa empírica sobre AD na gestão pública, com a aplicação de técnicas de gestão desenvolvidas por práticas de contabilidade gerencial, reengenharia de processos internos, custos, orçamento e qualidade total.

Palavras-chave: Avaliação de desempenho, Administração pública, Eficiência e Eficácia na gestão pública.

1. Introduction

Performance evaluation (PE) is a management tool, also used to measure the efficiency and effectiveness of organizations in competitive environments and is used assist managers in achieving and monitoring established goals (Petri, 2005). In addition, it is able to implement the organization’s strategic planning (Merchant, 2006; Fernandes, 2005; Van Bellen & Hans, 2005).

In the public sector, Smith (1989) affirms that PE is inserted in the relation between product or service offered to the population, coming from the budget execution that aims to reach social needs.

In this context, IPSASB (2011) establishes six terms that must be pursued in the performance of the ser- vices offered to society: (i) the objectives, correspond to the results that the body wants to achieve, and these must be specific, measurable, availables at a value fair, relevant and with a deadline for their scope; (ii) inputs, are the financial and nonfinancial resources used to produce output; (iii) the exits, are the prod ucts or services offered to the society; (iv) the results, are the reflexes of the exit to society - the achievement of the goals (Gregory & Lonti, 2008; IPSASB, 2011); (v) efficiency indicators, are instruments to evaluate the relationship between inputs and outputs, through the allocation of the necessary minimum resources (IPSASB, 2011; Athanassopoulos, 2003); and (vi) effectiveness indicators, are the instruments used to evaluate the results from the relationship between inputs and outputs products or services offered to society (IPSASB, 2011).

For Neely, Mills, Gregory and Platts (1995) efficiency and effectiveness in the field of PE are elements used to evaluate the quality of services offered to the population and to quantify the outcome of governmental actions.

In this understanding, this study presents potential research gaps in accounting, regarding PE in public management. For this, it analyzes the literature from 1993 to 2016 in the Spell, Scopus and Web of Science databases, in order to diagnose PE studies in public management.

The study is justified by addressing an emerging issue, discussed in accounting events and journals, in the face of corruption practices involving the public sector (Carvalho, Moura & Neiva, 2015; Brito & Dias, 2015; Lima & Diniz, 2016), and for three distinct reasons: (i) dissemination of a set of performance measurement recommendations by the United Nations Commission (UNC) in 1993 (ratified by the National Accounts System - NAS in the same year, and by the European System of National Accounts

-

- ESNA and Commission of the European Union

-

- CEU in 1995); (ii) provide reflection among pub lic managers, academics, researchers and society on effective information of performance of the budgetary resources executed by local governments; (iii) for presenting that management reform plans were not reached with the 1995 Reform in Brazil.

The limitations of the study are related to not exhaust the state of the art and using three databases (Spell, Scopus and Web of Science) for data collection-although Silva et al (2014) affirm that these data- bases store a significant fraction of public accounting research.

The study is structured in four sections. The first section (1) is composed of motivational exposition, justifications and its limitations. In the second section (2.1 and 2.2), the evolution of public administration and the reflexes of economic globalization. In the third section (3) is the methodology applied to achieve the proposed objective. In the fourth section (4), are apresentation the results found. In the fifth section (5), are the discussions of the results. In the sixth and last section (6), the conclusion and suggestions for future studies

2. Theoretical flamework

2.1. Evolution of Public Administration

It is based on three models of management: the patrimonialist, the bureaucratic and the managerial, the latter, also known as New Public Management (NPM). The first began in the Middle Ages, with a strong predominance in the absolutist monarchist regime from the fifteenth to the eighteenth centuries. It was based on religious belief and seigniorial powers and had strong resistance in the separation of public goods from private ones (Secchi, 2009). This model aimed to serve the interests of the few and to ignore the basic purpose of the state - to protect public affairs (Kettl, 2006; Hood, 1995; Lane, 1993), understood that effectiveness was not important in management and practiced corruption and nepotism (Martins, 1997; Weber, 1999).

This practice was no different in Brazil during D. João VI’s government in the early nineteenth century, specifically in 1889. Gomes and Oliveira (2010) argue that fiscal resources aimed at the interests of the court - not to commune with the interests of the people. Had difficulties in distinguishing public and private assets between politician and public administrator. This difficulty was characteristic of this model.

The second model, classified as the first great administrative reform of the Modern State (Weber, 1999), was born of the need to separate what was public and private in the second half of the nineteenth century in European countries (Gomes & Oliveira, 2010). It also had the objective of combating nepotism and corruption, as well as guaranteeing the civil rights of society, despite authoritarianism by denying the right to vote to the poor (Martins, 1997).

In Brazil this model was instituted in 1930, with the purpose of counteracting conservatism fragmented by the power of rural export oligarchies (Pereira, 2011). But it also took the lead in the process of economic and social modernization and, consequently, intervened in the productive sector of goods and services and in social economic modernization (Gomes & Oliveira, 2010). It was obsolete due to the influence of external and internal factors from the oil crisis in the 1970s, when governments realized that instead of a bureaucratic, rigid and interventionist model, the creation of a managerial model should be created (Gomes & Oliveira, 2010).

In the 1970s and 1980s, the fragility of the bureaucratic model in maintaining and guaranteeing the social well-being of its citizens, as well as the control of technological innovations as a consequence of globalization, emerges (Weber, 1999). Hence the strengthening of discussions on the role of the state in social, political and economic aspects (Weber, 1999).

These discussions culminated in the rise of the managerial model, with the aim of making the admin istration of state services more effective (imperative of the globalization process), including citizen assistance, fiscal adjustment, and reducing the cost of the state machine (Dunleavy & Hood, 1994; Ferlie, Ash- burner, Fitzgerald & Pettigrew. 1999).

The third NPM model then emerges, initially in Great Britain, the United States, Australia, New Zealand and then gradually in Europe and Canada (Ormond, 1999), with the aim of filling the shortcomings of the bureaucratic model, social welfare and the efficiency of the public machine, as a consequence of the techinnovations of globalization (Pollit, 1996).

This model (NPM) became necessary due to the modernization of the state, which was politically absolutist and economically mercantilist, combating nepotism and corruption, and becoming politically unavoidable (Ibrahim, Kamal, Nor, Zubir, Normah & Jamaliah 2006; Pereira, 2011).

In Brazil, this managerial reform only occurred in 1995, in response to the challenges presented by the transformation of the Brazilian State into a Social State, after the democratic transition in 1985 - the result of a political pact that established the state to guarantee political and promote a better distribution of income in a society marked by excessive inequality (Pereira, 2011). This pact was ratified by the Federal Constitution of 1988 in the guarantee the universal right to health and education.

Coelho (2004) observes that management reform was not achieved with the 1995 Reform but contributed to discursive practices on the institutionalization of changes in Brazilian governments. An example of this is: (i) introduction of the notion of agencification in the public administration, granted to the greater public manager; (ii) intensification of administrative decentralization, different administrative arrangements; (iii) introduction of regulatory mechanisms, especially through the implementation of regulatory agencies for public services.

In this way, it is possible to classify the Brazilian public administration as a mixed one since it has difficulties in quickly solving societal problems. It has robust control systems, but it cannot inhibit the practice of corruption and nepotism. It applies a large amount of resources in large areas such as health and safety but cannot be effective in meeting social needs (Pereira, 2011).

2.2. Influence of Globalization, Social Democracy and Social Welfare in Public Management

This influence is perceptible in the managerial reform of the state, due to the market opening (globalization) and world-wide comprehension of capitalism. The State benefit from the results provided by an open and competitive market, takes social responsibilities more effectively (Klering, Porsse & Guadagnin, 2010).

Democracy was the political instrument that safeguarded civil rights against tyranny, and bureaucracy was the administrative instrument to combat nepotism and corruption, adopting principles of a professional public service and an impersonal, formal and rational administrative system (Andrews, Beynon & Mcdermott, 2015).

The managerial view on the role of public administration is to promote efficiency, reduce costs and achieve greater effectiveness in service delivery through the application of planning, organization and control tools, continuous training and motivational mechanism to the servers (Osborne & Gaebler, 1995).

A society will only be developed and democratic if it has an able or strong state - for this, it is necessary that, besides the legitimacy of its laws and its rulers, it counts on the competence of its public officials (servants). This is possible through continuous training (Andrews et al., 2015).

In Brazil, the first indications of social democracy occurred in 1985 through a democratic and popular political pact, which was legally consolidated through the Federal Constitution of 1988, by establishing a substantial increase in social public spending from 11% to 23% in the health (Pereira, 2011).

In this context, the bottleneck of Brazilian governments lies in the operational field, which depends on the competence of its employees - most of which correspond to political indications, without any knowledge of public management (Coelho, 2004).

As for the role of the citizen, they are expected to assist in making decisions about the laws or institutions of the country, or on specific issues regarding the use of public resources. As an example, greater participation in the construction of the planning for the period of government, with accompanying stance of control and measurement of the result (accountability) by its rulers (Dutra, 2003).

3. Method

The methodological technique applied in this study was the descriptive method, whose focus is on the description of the findings in the national and international literature, on research that deals with empirical and theoretical subjects on performance evaluation in public management from 1993 to 2016. The choice of period is harmonized with the dissemination of the UNC, NAS, ESNA and CEU, one of the justifications of this study.

To guide the study, the methodology was divided into three stages: in the first step the key words were structured in two axes. Axis 1, labeled performance evaluation, consists of the key words “indicators, public, management, administration, model government” with boolean “and” between each word. Axis 2, labeled “Efficiency in public management”, is com- posed of the key words “governance, government, agency, state, administration, public, efficient, effectiveness and gestion”, also composed of boolean “and” between each word.

Structured the two axes, a search was performed on the “Spell, Scopus and Web of Science” database, with period filter between 1993 and 2016.

In the second step, we identified 1,558 articles that were sent to the Endnot reference management software and then the prealignment identification with the proposed theme was performed. Subsequently, the articles were pre-aligned through their respective titles, discarding those that did not correspond. This action led to the elimination of 889 articles, aligned with other areas such as biology and health, with 669 articles remaining in the areas of economics, adminis tration and accounting.

This result was again passed through another prealignment filter, this time, based on the summary reading of each of the 669 articles. This action resulted in the elimination of 582 articles that were not aligned with the proposed research theme, leaving 87 articles specifically aligned with the title and abstract.

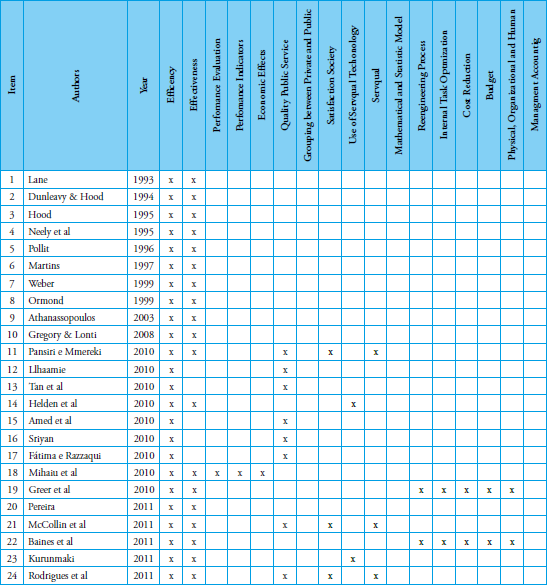

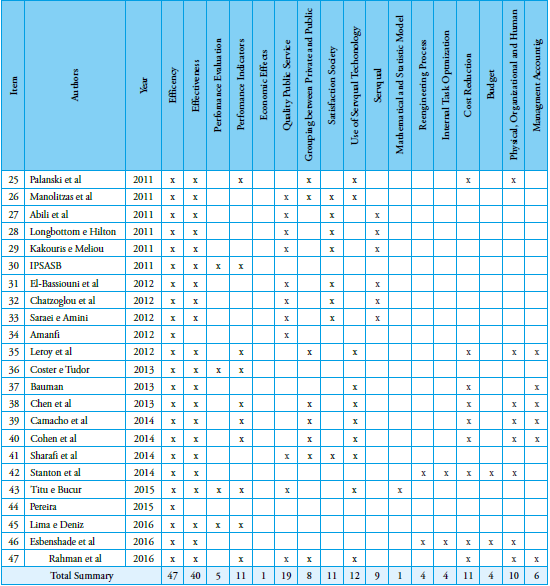

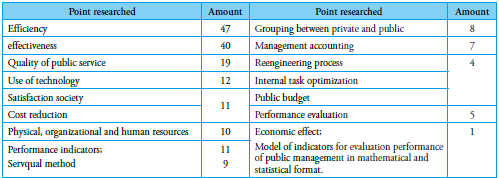

In the third and final step, after reading, analyzing and classifying the 87 articles, it was verified that there were only 47 articles totally aligned with the objective of this study. This final result was used as a research sample (see Table 1 in section 4).

4. Presentation of results

Table 1 describes the results found in the literature during the period investigated with their respective discussions in the section five.

Lane (1993) and Hood (1995) found in their studies that local governments seek a management model capable of interacting with political actions in achieving social welfare and economic development.

Martins (1997) and Secchi (2009) affirm that this search is present in patrimonialist, bureaucratic and NPM models.

Some countries rely on the NPM model to improve the final product offered to citizens and address management deficiencies within local governments (Dunleavy & Hood, 1994; Pollit, 1996; Ormond, 1999). For Martins (1997) and Weber (1999) this model is capable of walking and adapting to the technological requirements evidenced and demanded by globalization.

Harmonizing the reflexes of globalization and the practices of social democracy to achieve the social well-being of the citizen are the great challenges of local governments. For this, they understand Pansiri and Mmereki (2010); Ilhaamie (2010) that performance evaluation systems (PES) are strongly aligned to achieve these challenges.

The PES in public management contributes to the improvement and maintenance of public service quality and better management of resources collected (Tan, Wang, Lam & Chee, 2010). For this reason, it is necessary that the local government, with the help and maintenance of legislator and oversight bodies, provide operational conditions for the adoption of APED measures in the management of local governments (Pereira, 2011).

Helden, Aardema, Bogt and Groot, (2010) argue that strong criticism of the inefficiency and ineffectiveness of the public sector over budget execution since the last two decades requires a review of the applied management model.

Amed, Usman, Shaukat, Ahmet and Iqbal, (2010) and Sriyam (2010) assert that public service quality is increasingly important for the achievement of society’s learning, especially in underdeveloped and developing countries (Tan et al., 2010).

Source: survey data

Opportunity of robust research in Accounting: a literary analysis on performance indicators in the management of municipal governments

Source: survey data

Fatima and Razzaque (2010) affirm that this quality has a strong influence in the competitive highlight, including even for re-election of government. It is the fundamental basis for the achievement of social satisfaction and is linked to the agility, empathy, guarantee, receptivity and reliability of society (Mihaiu, Opreana & Pompiliu, 2010).

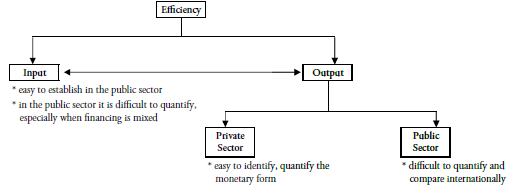

Mihaiu et al., (2010) still state that the effectiveness of public service quality, the final product of the state to society, is established by the relation between the effects of inputs and outputs of products or services offered to society (see Figure 1)

The difficulty attributed by Mihaiu et al., (2010), shown in Figure 1, is related to direct and immediate economic benefit in the public sector. As an example, if a school is built in a peripheral region of extreme poverty, the efforts involved in this investment can easily be identified (costs incurred for construction, such as material, wages, etc.). But how are benefits identified in this case? Can we identify direct economic benefits?

Cases where only social benefits are found, it will be difficult to quantify financially. Therefore, in conclusion, we can say that the economic efficiency of this investment is zero, from the definition of efficiency (Pansiri & Mmereki, 2010; Greer, & Stuart, 2010).

Mccollin, Ograjensek, Go and Ahlemeyer (2011); Baines, Charlesworth, Turner and O´neill (2011) affirm that the tools of managerial accounting are capable of assisting in the application of a PES, mainly in relation to the cost reduction with responsibility.

Kurunmaki, Lapsley and miller (2011); Rodrigues, Barkur, Varambally and Motlagh (2011) believe that management accounting is an instrument capable of modernizing and reforming public management (Palanski & Mmereki, 2011) along with application of transparency, credibility, competence, integrity and reliability.

Figure 1.

Determining the efficiency indicator

Source: Mihaiu et al., (2010)

For Manolitzas, Yannacopoulos, Tsotsolas and Drosos (2011); Abili, Thani, Morkhtarian and Raschidi (2011); Longbottom and Hilton (2011), public managers should use the information generated by accounting in their operational and strategic decisions, especially with regard to the use of PE indicators, when in execution budgetary resources.

Kakouris and Meliou (2011) used the Servqual instrument to measure the satisfaction of society regarding the quality of the services offered by the local government. This technique was also applied by El-Bassiouni et al., (2012) and Chatzoglou et al (2012), and both studies concluded that citizens’ expectations in the areas of intangibility, reliability and safety are low and that there is a lack of transparent communication between public managers and society. This instrument is extensively used in the literature to collect primary data (Sarei & Amini, 2012; Amanfi, 2012; Leroy, Palanski & Simons (2012).

Coster and Tudor (2013), establish characteristics for PE in public management corresponding to six input and output variables, as shown in Figure 2.

Figure 2.

Terms for performance evaluation

Source: Adapted from Coster and Tudor (2013).

These variables are described as:

-

Objectives are the results that the body wants to achieve (IPSASB, 2011), and therefore must be specific, measurable, available at fair and relevant value (Gregory & Lonti, 2008);

-

Inputs are the financial and non-financial resources of an entity, used to achieve the stated goals (IPSASB, 2011) and the basis for measuring government performance (Hood, 1995);

-

Outputs are products or services, including transfers between entities, executed by an entity as delivery of its objectives (IPSASB, 2011);

-

Results are the exit effects for society, as well as the achievement of the goals established by the entity (Gregory & Lonti, 2008; IPSASB, 2011);

-

Efficiency indicators are measures of the relation- ship between inputs and outputs through the imposition of quality services with the minimum resources necessary to provide the service or product (Athanassopoulos, 2003; IPSASB, 2011);

-

Effectivenes indicators are the measures of relation between outputs and results (IPSASB, 2011). Comparing efficiency and effectiveness, Neely et al., (1995) establish that performance measurement is a set of matrices used to quantify and evaluate managers’ actions.

For Bauman (2013); Chen, Cumming, Hou and Lee (2013), new management techniques can improve the costing measurement of government actions. Rahman, Everett and Neu (2016) suggest a set of seven elements: (i) leadership; (ii) management of accounting information; (iii) resource management; (iv) community and customer focus; (v) stakeholder partnership management; (vi) performance management; and (vii) results of the provision of services. These elements are responsible for the composition of the perception index of corruption.

Camacho, María and Campa (2014); Cohen, Cornett, Marcus and Tehranian (2014) state that these elements, along with ethical professional practices, are present in NPM. With this, it is possible to investigate the causes that prevent the adoption of NPM by the managers elected by the people.

Sharafi, Jurisch, Ikas, Wolf and Krcmar (2014) affirm that the process of grouping between private and public initiative in the development of social processes, contribute to the improvement of public services, and, consequently, greater efficiency and effective- ness in governmental management. Both will benefit through the cost-benefit method. Thus, services will be offered with more quality, a determining factor for the performance of any organization (Stanton, Ballar- die, Bartram, Bamber & Sohal, 2014).

Titu and Bucur (2015) with the purpose of measuring the quality of services in the local public administration, developed a model with 12 indicators through regression and likert scale.

The use of budget performance indicators, for example, aims to demonstrate the relative participation of budget results, government savings generation capacity, current spending capacity and current and capital budget results (Lima & Diniz, 2016).

Esbenshade, Vidal, Fascilla and Mariko (2016) affirm that the reengineering process is increasingly used to restructure work in the public sector, especially in reducing costs, optimizing internal tasks, budgeting, manipulating physical, organizational and human resources, in order to efficiency and effectiveness, since it prioritizes the capacity of the worker (public servant), the quality of the public service and the bud-getary pressures.

Rahman et al., (2016) argue that performance measurement through indicators is necessary to measure the effectiveness of public management, and that accounting needs to break down legality barriers with respect to its use in support of local government exec utive branch decisions.

5. Results and Discussion

Considering the satisfaction of the citizen conditioned the quality of the service offered by the government in a timely manner, listed by Fatima and Razzaque (2010), influence on the maintenance or change of manager in election time in democratic countries, the question is pertinent: why governments democratic countries that want re-election do not pursue this satisfaction through the provision of quality services?

The effectiveness shown by Mihaiu (2010) is related to the results obtained by performance indicators related to economic and social effects. Acknowledg- ing, even, that this relationship is apparently simple, but the practice often goes the other way, because identifying and measuring the inflows and outflows in the public sector is often a difficult operation, as shown in Figure 1.

As for the technique Servqual listed by Kakouris and Meliou (2011), El-Bassiouni et al., (2012), Chatzoglou et al., (2012), Sarei and Amini (2012), Amanfi (2012) and Leroy et al., (2012), to measure the satis faction of the population, since this same satisfaction is a reflection of the quality of the services offered by the local governments, it is pertinent to investigate in the underdeveloped countries the reliability and security of the citizen towards its ruler.

The facts listed by Pereira (2011), Coster and Tudor (2013) make clear that PE is imperative public man- agement, under penalty of inefficiency of services offered to the population. Therefore, it is a necessity that must be practiced by all public agencies, effec tively and transparently.

Source: Research Data.

Table 2 shows the central themes addressed in the studies found in the literature during the period investigated. In it, it is possible to observe that the concentration of research on PE in public management is in the measurement of efficiency and effectiveness. However, they are embryonic studies on theoretical methods because there is no adherence in case studies.

Research on a model of PE with the application of mathematical and statistical methods, economic effects of public management methods, budget analy sis of public management practices, reengineering processes and optimization of internal tasks, such as improving efficiency in public management, ratify the low interest by researchers in developing studies with these proposals. This provokes reflection on the low interest of researches in these areas. However, it is a challenge for future empirical research.

The study also found, with regard to public manage ment, that there is little research regarding the model of statistical and mathematical indicators, reengineering process and budget (Titu & Bucur, 2015; Sharafi et al., 2014; Stanton et al., 2014; Baines et al., 1994; Greer et al., 2010).

However, on efficiency and effectiveness (see Table 1) there is increased interest in the researchers in this approach (Tan et al., 2010; Rahman et al., 2016).

In view of the above, two questions for reflection on the low empirical publication in the evaluation of public management through PEs are listed: (i) what are the difficulties of the literature in developing studies that use statistical models, reengineering processes and budget to evaluate government performance local? (ii) are there difficulties in accessing data generated by local governments? If yes, which ones?

Regarding the economic repercussions due to the inefficiency of public management, only one study was found, but with a qualitative focus. As well, in the same proportion, on models of performance evaluation indicators involving logarithm, exponential, logic, swot analysis and balanced scorecard. With this same look, studies involving metrics of managerial account ing to evaluate the performance, also registered low publication of empirical studies (see Table 1).

The culture of the Brazilian public organization can be considered a patrimonial inheritance and, despite the changes that have taken place in the country, nepotism, favoritism, corruption and clientelism are still persistent cultural characteristics in society, with respect to the State and also to the organization of Public administration.

Therefore, inserting PE models used by the private sector, without any pertinent adaptations, with the expectation of immediate success, is largely a mere scientific illusion.

The state is not measured by what it has, but by what it is. This leads to the culture of its people, in the use of public apparatus, both ethically and culturally. Inserting an PAS is a long and arduous walk (Pereira, 2011).

6. Final considerations

The study presents potential opportunities for accounting research, mainly empirical (including case studies and experiments), with regard to PE in pu lic management. These are gaps that have not been explored in the literature until now (see Table 1).

As for PAS contribution to achieving efficacy in pub lic management, Titu and Bucur (2015) affirm that once the results of local government management actions are evaluated through mathematical and sta tistical models, with the application of quantitative or qualitative PEs, there will be elements of performance comparison. And so, governments will also have as a goal the alignment of these results with their political actions, which will certainly be harmonized with the political and social commitments necessary to society. As a reflection, will improvement in the quality of the public service to the population, since it is the mea- surement thermometer of satisfaction of well-being, objective greater of the whole government.

Finally, the study concludes that there is little empirical research on actual outcomes through PA indicators in public management, and that there are probably no studies on local government decision-making based on accounting information. And that the application of concepts of reengineering in the public management would help in the optimization of execution of the internal tasks, and consequently, the elimination of rework and aggregation of similar tasks.

The study also suggests that the constitution and application of PA indicator models to assess public management in developing countries is the biggest challenge because of the lack of knowledge of democratically elected managers by the people.

This study contributes to knowledge construction by presenting information capable of provoking reflectionon performance measurement in public management,as well as fostering future research, such as: (i) performance evaluation and its economic impact on public management; (ii) evaluation of performance in public management in partner ship with the private sector;(iii) performance indicators model; (iv) contributions of reengineering processes for efficiency and effectivenessin public management.

References

Abili, K., Thani, F.N., Mokhtarian, F., Rashidi, M.M. (2011). Assessing quality gap of university services. Asian Journal on Quality, 12(2), 167-175. https://doi.org/10.1108/15982681111158724

Amanfi Jr, B. (2012). Service Quality and Customer Satisfaction in Public Sector Organizations: A Case Study of the Commission on Human Rights and Administrative Justice. A Thesis Submitted to the Institute of Distance Learning, Kwame Nkrumah University of Science and Technology in Partial Fulfillment of the Requirements for the Degree of Commonwealth Executive Masters In Business Administration.

Amed, M. M. N., Usman, A., Shaukat, M., Ahmed, N., & Iqbal, H. (2010). Impact of Service Quality on Customer Satisfaction: Emperical Evidence from the Telecom-sector of Pakistan. Interdisciplinary Journal of Contemporary Research in Business, 12, April.

Andrews, Rhys, Beynon, M. J., Mcdermott, A. M. (2015). Organizational capability in the public sector: a configurational approach. Journal of Public Administration Research and Theory, p. muv005. https://doi. org/10.1093/jopart/muv005

Athanassopoulos, A. D. (2003). Using frontier efficiency models as a tool to re-engineer networks of public sec- tor branches: An application

Baines, D., Charlesworth, S., Turner, D. & O’neill, L. (2011). Lean social care and worker identity: the role of outcomes, supervision and mission. Critical Social Policy, 34(4), 433-453. https://doi.org/10.1177/0261018314538799

Bauman, D. C. (2013). Leadership and the three faces of integrity. The Leadership Quarterly, 24(3), 414-426. https://doi.org/10.1016/j.leaqua.2013.01.005

Brito, H.S., & Dias, R. R. (2015). O comportamento da receita pública Municipal: um estudo de caso no município de Parnaíba/PI. Revista de Gestão e Contabilidade da UFPI, 3(1), 130-146. https://doi.org/10.26694/2358.1735.2016.v3ed13466

Camacho-M., María. D. M. & Campa, D. (2014). Integrity of Financial Information as a Determinant of the Outcome of a Bankruptcy Procedure. International Review of Law and Economics, 37, 76-85. https://doi.org/10.1016/j.irle.2013.07.007

Carvalho, J. J., Moura, N. S., Neiva, W. D. (2015). Receita pública municipal: um estudo sobre o comportamento das receitas próprias e de transferência no município de Picos/ PI. Recuperado de http://www.faculdadersa.com.br/Arquivos /downloads /semana_cientifica/

Chatzoglou, P., Chatzoudes, D., Vraimaki, E. & Diamantidis, A. (2013). Service quality in the public sector: the case of the Citizen’s Service Centers (CSCs) of Greece. International Journal of Productivity and Performance Management, 62(6), 583-605 https://doi.org/10.1108/IJPPM-12-2012-0140

Chen, J., Cumming, D., HOU, W. & LEE, E. (2013). Executive integrity, audit opinion, and fraud in Chinese listed firms. Emerging Markets Review, 15, 72-91. https://doi.org/10.1016/j.ememar.2012.12.003

Coelho, M. Q. (2004). Indicadores de performance para projetos sociais: a perspectiva dos stakeholders. Alcance, Biguaçu, 11(3), 423-444.

Cohen, L. J., Cornett, M. M., Marcus, A. J & Tehranian, H. (2014). Bank learnings management and tail risk during the financial crisis. Journal of Money, Credit and Banking, 46(1), 171-197. https://doi.org/10.1111/ jmcb.12101

Coster, A. L. & Tudor, A. T. (2013). Service Performance- Between Measurement and Information in the Public Sector. Lumen International Conference Logos Universality Mentality Education Novelty. de Janeiro, 2004

Dunleavy, P. & Hood, C. (1994). From Old Public Administration to New Public Management. Public Money & Management. https://doi.org/10.1080/09540969409387823

Dutra, A. (2003). Metodologia para avaliar e aperfeiçoar o desempenho organizacional: incorporando a dimensão integrativa à MCDA construtivista-sistê- mico-sinergética. Tese (Doutorado em Engenharia de Produção) - Programa de Pós-Graduação em Engenharia de Produção da Universidade Federal de Santa Catarina, Florianópolis, Santa Catarina, Brasil.

El-Bassiouni, M.Y., Madi, M., Zoubeidi, T. & Hassan, M.Y. (2012). Developing customer satisfaction indices using servqual sampling surveys: a case study of Al-Ain municipality inspectors, Journal of Economic and Administrative Sciences, 28(2), 98-108. https:// doi.org/10.1108/10264111211248394

Esbenshade, J., Vidal, M., Fascilla, G. & Mariko, O. (2016). Customer-driven management models for choiceless clientele? Business process reengineering in a California welfare agency. Work, Employment and Society, 30(1), 77- 96 https://doi.org/10.1177/0950017015604109

Fátima, J. K. & Razzaque, M. A. (2010). Understanding the Role of Service Quality, Customer Involvement and Rapport on Overall Satisfaction in Bangladesh Banking Service

Ferlie, E., Ashburner, L., Fitzgerald, L. & Pettigrew, A. (1996). The new public management in action. Oxford: Oxford University Press https://doi.org/10.1093/acprof:oso/9780198289029.001.0001

Fernandes, B. H. R. (2005). Rastreando os direcionadores da performance organizacional: uma proposta metodológica. Cadernos EBAPE.BR, Rio de Janeiro, 3(1), 1-17. https://doi.org/10.1590/S1679-39512005000100005

Gomes, M. L. S. & Oliveira, F. C. (2010). Modelos organizacionais de administração pública: um estudo dos aspectos da realidade cearense na estrutura de referência das reformas do Estado. Revista de Ciências da Administração, Florianópolis, 12(28), 105-126. https:// doi.org/10.5007/2175-8077.2010v12n28p105

Greer I, G. & Stuart, M. (2010). Beyond national ‘varieties’: public-service contracting in comparative perspective. In I. Cunningham and P. James (eds.), Voluntary Organizations and Public Service Delivery (pp. 153-167). London: Routledge.

Gregory, R. & Lonti, Z. (2008). Chasing shadows? Performance measurement of policy advice in New Zealand government departments. Public Administration, 86(3), 837-856. https://doi.org/10.1111/j.1467-9299.2008.00737.x

Helden, G. J. V., Aardema, H., Bogt, H. J. T. & Groot,T.L.C.M. (2010). Knowledge creation for practices in public sector management accounting by consultants and academics: Preliminary findings and directions for future research. Management Accounting Research, 21, 83-94. https://doi.org/10.1016/j.mar.2010.02.008

Hood, C. (1995). The «new public management» in the 1980s: variations on a theme. Accounting, Organizations and Society, 20(2/3), 93-109. https://doi.org/10.1016/0361-3682(93)E0001-W

Ibrahim, K. A. R., Nor A. Ab. R., Zubir A. C., Normah, O. & Jamaliah, S. (2006). Management Accounting Best Practices Award for Improving Corruption in Public Sector Agencies. Science Direct.

Ilhaamie, A. G. A. (2010). Service Quality in Malaysia Public Service: Some Findings, International. Journal of Trade, Economics and Finance. 1(1). https://doi.org/10.7763/IJTEF.2010.V1.8

IPSASB (2011). Consultation Paper Reporting Service Performance Information.

Kakouris, A. P. & Meliou, E. (2011). New public management: promote the public sector modernization through service quality. Current experiences and future challenges. Public Organization Review, 11(4), 351-369.

Kettl, D. F. (2006). A revolução global: reforma da administração do setor público. In Pereira, Luís Carlos Bresser; Spink, Peter Kevin (Orgs.), Reforma do Estado e Administração Pública Gerencial. Rio de Janeiro: FGV.

Klering, L. R., Porsse, M. C. S. & Guadagnin, L. A. (2010). Novos caminhos da administração pública brasileira, Análise, Porto Alegre, 21(1), 4-17, jan./jun.

Kurunmaki, L. L. & Miller, P. B. (2011). Guest editorial: Accounting within and beyond the state. Management Accounting Research, 22, 5. https://doi.org/10.1016/j.mar.2010.11.003

Lane, J. E. (1993). The public sector: concepts, models and approaches. London: Sage.

Leroy, H., Palanski, M. E. & Simons, T. (2012). Authentic leadership and behavioral integrity as drivers of follower commitment and performance. Journal of Business Ethics, 107(3), 255-264. https://doi.org/ 10.1007/s10551-011-1036-1

Lima, S. C. & Diniz, J. A. (2016). Contabilidade pública: análise financeira governamental. São Paulo: Atlas.

Longbottom, D. & Hilton, J. (2011). Service improvement: lessons from the UK financial services sector. International Journal of Quality and Service Sciences, 3(1), 39-59. https://doi.org/10.1108/17566691111115072

Manolitzas, P., Yannacopoulos, D., Tsotsolas, N. & Drosos, D. (2011). Evaluating the Public Sector in Greece: The case of Citizens’ Service Centers. European Conference on Information Management and Evaluation. Reading: Academic Conferences International Limi- ted. September.

Martins, H. F. (1997). Ética do Patrimonialismo e a Modernização da Administração Pública Brasileira. In Motta, Fernando C. Prestes; Caldas, Miguel P., Cultu- ra organizacional e cultura brasileira. São Paulo: Atlas.

Mccollin, C., Ograjensˇek, I., Go¨B, R. & Ahlemeyer-S. A. (2011). Servqual and the process improvement challen ge. Quality and Reliability Engineering International, 27(5), 705-718. https://doi.org/10.1002/qre.1234

Merchant, K. A. (2006). Measuring general managers’ performances: Market, accounting and combination-of- -measures systems. Accouting, Auditing & Accountability Journal, 19(6), 893-917. https:// doi.org/10.1108/09513570610709917

Mihaiu, D. M., Opreana, A. & Pompiliu, C. M. (2010). Efficiency, Effectiveness and Performance of the Public Sector. Romanian Journal of Economic Forecasting. April.

Neely, A., Mills, J., Gregory, M., & Platts, K. (1995), Performance measurement system design - A literature review and research. https://doi.org/10.1108/01443579510083622

Ormond, D. & Löffler, E. (1999). A nova gerência pública. RSP - Revista do Serviço Público. 50(2), 66-96.

Osborne, D. & Gaebler, T. (1995). Reinventando o governo. 6. ed. Brasília: MH Comunicação.

Palanski, M. E., Kahai, S. S. & Yammarino, F. J. (2011). Team virtues and performance: An examination of transparency, behavioral integrity, and trust. Journal of Business Ethics. 99(2), 201-216. https://doi.org/10.1007/s10551-010-0650-7

Pansiri, J. & Mmereki, R. N. (2010). Using the servqual model to evaluate the impact of public service reforms in the provision of primary health care in Botswana. Journal of African Business, 11(2), 219-234. https:// doi.org/10.1080/15228916.2010.509005

Pereira, L. C. B. (2011). Reforma gerencial do Estado, teoria política e ensino da administração pública. RGPP, 1(2), 1-6.

Pereira, R. M. (2015). Análise do sistema de controle inter- no no Brasil: objetivos, importância e barreiras para sua implantação. Revista Contemporânea de Contabilidade. ed. Setembro.

Petri, S. M. (2005). Modelo para apoiar a avaliação das abordagens de gestão de desempenho e sugerir aper- feiçoamentos: sob a ótica construtivista. 2005. 236f. Tese (Doutorado em Engenharia de Produção) - Programa de Pós-Graduação em Engenharia de Produção da Universidade Federal de Santa Catarina, Florianópolis/SP, Brasil.

Pollitt, C. (1996). Antistatist Reforms and the New Admi nistrative Directions: Public Administration in the United Kingdom. Public Administration Review, 56, 81-108. https://doi.org/10.2307/3110058

Rahaman, A. S., Everett, J. & Neu, D. (2016). Accounting and the privatization of water services in developing countries. Accounting, Auditing & Accountability Journal, 20(5), 637-670.

Rodrigues, L. L. R., Barkur, G., Varambally, K. V. M. & Motlagh, F. G. (2011). Comparison of Servqual and Servperf metrics: an empirical study. The TQM Journal, 23(6), 629-643. https://doi.org/10.1108/17542731111175248

Saraei, S. & Amini, A. M. (2012). A study of service quality in rural ICT renters of Iran by Servqual. Telecommunications Policy, 36(7), 571-578. https://doi.org/10.1016/j.telpol.2012.03.002

Secchi, L. (2009). Modelos organizacionais e reformas da administração pública. RSP - Revista de Administração Pública, 43. Rio de Janeiro: Fundação Getúlio Vargas. https://doi.org/10.1590/S0034- 76122009000200004

Sharafi, A., Jurisch, M., Ikas, C., Wolf, P. & Krcmar, H. (2014). Bundling Processes between Private and Public Organizations: A Qualitative Study. Information Resources Management Journal (IRMJ). https:// doi.org/10.4018/978-1-4666-3616-3.ch007

Silva, G. C., Nascimento, G. C. R. & Ferreira, C. D. (2014). Transparência na prestação de contas da administração pública municipal na internet: um estudo de caso no Estado de Goiás. V Congresso UFSC de Contabilida- de e Finanças & Iniciação Científica em Contabilidade. Maio/2014 - Florianópolis/SC.

Smith, P. (1989). Dynamic aspects of local authority expen diture decisionn. Fin. Acctab. Mangmt, 5, 1-18 https:// doi.org/10.1111/j.1468-0408.1989.tb00305.x

Sriyam, A. (2010). Customer Satisfaction towards Service Quality of Front Office Staff at the Hotel. Bangkok: Graduate School, Srinakharinwirot University.

Stanton, P. G. R., Ballardie, R., Bartram, T., Bamber, G. J. & Sohal, A. (2014). Implementing lean management/ Six Sigma in hospitals: beyond empowerment or work intensification? The International Journal of Human Resource Management, 25(21), 2926-40. https://doi.org/10.1080/09585192.2014.963138

Tan, B., Wang, C., Lam, C. H., Ooi, K. & Chee, Y. F. (2010). Assessing the link between service quality dimensions and knowledge sharing: Student Perspective. African Journal of Business Management, 4(6), 1014-1022.

Titu, M. A. & Bucur, A. (2015). Models for quality analysis of services in the local public Administration. Sprin- ger Science+Business Media Dordrecht 27 February. Trabalhos%202015/Receita_publica_municipal_ um_estudo_sobre_o_comportamento_das_recei- tas_proprias_e_de_transferencia_no_municipio_de_ Picos_Pi.pdf. Acesso: setembro, 2017.

Van, B. E. & Hans, M. (2005). Indicadores de sustentabili- dade: uma análise comparativa. Rio de Janeiro: FGV.

Weber, M. (1999). Economia e sociedade. Brasília: Editora da UnB, 1.