Articles

This work is licensed under Creative Commons Attribution-NonCommercial 4.0 International.

Received: 02 December 2018

Accepted: 02 July 2019

Abstract: This paper serves as a double purpose in the context of local administrations’ information on line disclosure of Social Responsibility (SR). First, this study examines how levels of information dissemination of SR are evolving. Second, some fiscal, political, population, and socioeconomic factors were investigated as determinants of this information disclosed. A content analysis of the websites of the local government in a region of Spain was carried out. This region is the first which has a Corporate Social Responsibility Lay. Later, according to literature review, the authors propose a multiple linear regression model based on disclosure index scores calculated previously. On the one hand, the results show an increase in the amount of SR information disclosed between 2013 and 2016. On the other hand, the study concludes that larger municipalities with more resources, progressive party governments, and intense political competition present higher levels of information disclosure of social responsibility.

Keywords: Social Responsibility, Disclosure, Websites, Determinant factors.

Resumen: En el contexto de la divulgación de información sobre Responsabilidad Social (RS) por la Administración Local, este trabajo presenta un doble objetivo. En primer lugar, se examina cómo evolucionan los niveles de divulgación de información sobre RS. Para ello, se ha realizado un análisis de contenido de las páginas web de los gobiernos locales en una región de España, pionera en la aprobación de una Ley de Responsabilidad Social Coroporativa. En segundo lugar, se investigan algunos factores poblacionales, socio-económicos, fiscales y políticos determinantes de la divulgación de este tipo de información, planteando un modelo de regresión lineal múltiple en función de un índice de divulgación calculado previamente. Los resultados muestran, por un lado, un aumento en la cantidad de información divulgada entre los años 2013 y 2016. Por otro lado, los municipios de mayor tamaño, con mayores recursos, gobernados por partidos progresistas y con una alta competencia política, muestran mayores niveles de divulgación de información sobre RS.

Palabras clave: Responsabilidad Social, Divulgación de información, Páginas web, Factores determinantes.

1. Introduction

In recent years, companies and institutions have devoted significant effort, time, and financial resources to develop social responsibility (SR) policies. Companies’ responsible actions are geared towards legitimising the relevant market processes and improving the perceptions of shareholders, customers, employees, and other stakeholders (Server and Capó, 2009; Gallardo-Vázquez, Sánchez-Hernández, and Corchuelo-Martínez-Azúa, 2013; Asgary and Li, 2016). Companies also seek to benefit from the advantages that SR offers in terms of competitiveness (Porter and Kramer, 2006; Server and Capó, 2009; Gallardo-Vázquez et al., 2013; Schramm-Klein, Morschett, and Swoboda, 2015; Shahzad, Rutherford, and Sharfman, 2016). While SR has been linked mainly to businesses’ voluntary actions, more and more public institutions are concerned about engaging in socially responsible initiatives, aiming thereby to satisfy the needs of the relevant interest groups and, more specifically, citizens (García-Sánchez, Frías-Aceituno, and Rodríguez-Domínguez, 2013; López et al., 2018). As the public sector’s main interest group, citizens need more information to monitor public administration activities (McTavish and Pypper, 2007; Guillamón, Bastida, and Benito, 2011; Araujo and Tejedo, 2016; Meijer et al., 2018). As a result, public entities have decided to play a more active role in promoting sustainability and improving the information provided about these initiatives (Crane, Bastida, and Benito, 2008; Nevado-Gil, Gallardo-Vázquez, and Sánchez-Hernández, 2016).

The study population chosen for analysis in the present research was local governments since they represent the first level of citizen participation in public affairs, thus making municipalities’ information disclosure particularly important (Caamaño-Alegre, Lago-Peñas, Reyes-Santias, and Santiago-Boubeta, 2013). Being the public entities closest to citizens, these organisations serve as direct and immediate channels of participation in everyday affairs in citizens’ immediate localities (Navarro et al., 2010; Cueto et al., 2014). Local governments are in an advantageous position to know the information demands of the main stakeholders in SR, and municipalities tend to favour disclosure (Díaz, 2009). Notably, the commitment to sustainability that local authorities must communicate to the public could be due to the type of services they provide (Navarro et al., 2011), as well as the importance of these services in terms of local taxes (Guillamón et al., 2011).

A resource that administrations use to establish a direct relationship with citizens is information and communications technology (ICT). The term e-government is used to refer to the use of ICT in areas such as the provision of online services and citizen participation in political affairs and accountability (Heeks and Bailur, 2007; Pina et al., 2009). Through e-government, citizens can monitor administrations’ initiatives and the public services provided, which leads to a more responsible management of public resources. In this context – while taking into account the different possible applications of ICT in e-government – the present study focused on the most universal, well-known, and widely used technology: the Internet.

The disclosure of online information facilitates the interaction between citizens and administration, enhancing the communication with the user, at the same time that implies a greater social commitment (Sandoval et al., 2011; Bonsón et al., 2012; Gandía et al. Al., 2016). On the other hand, online disclosure will permit that information will be available to everyone, and it will eliminate time and space barriers, offering a better service to citizens (Frías et al., 2014; Cuadrado et al., 2014).

This research sought to serve a dual purpose. First, it investigates the online SR information provided by local governments and, more specifically, on websites in order to calculate an index of information disclosure and to track its evolution between 2013 and 2016. Second, some determinant factors of information disclosure levels were studied. This approach sought to contribute to the generation of knowledge about this area in the Extremadura region since the level of disclosure of socially responsible initiatives by local government is, thus far, a little discussed subject – despite its important impact on citizens. For this reason, authors such as Marcuccio and Steccolini (2005); Pina et al. (2007); and Mazzara et al. (2010) call for increased research in this field and encourage organisations to adopt sustainable behaviours, which motivated the study presented below.

To achieve the proposed objectives, a sample of 40 municipalities of the Autonomous Community of Extremadura was selected, consisting of those have more than 5,000 inhabitants. This region was chosen because the community approved the first law on corporate social responsibility (Government of Spain, 2010) in Spain, in December 2010, committing Extremadura to promoting the responsible behaviour of both companies and public institutions.

After this introduction, we first examine the previous academic literature on the determinants of information disclosure and discuss research hypotheses. Then we describe the methods used in the statistical treatment of the data supplied by the study sample, analyse the level of information provided by municipality websites, as well as their evolution over time, and identify those factors that have conditioned SR information disclosure. Finally, we detail and discuss the results, offering conclusions, implications, and suggestions for future research.

2. Determinants of online disclosure of sustainability information and research hypotheses

A review of the academic literature on information disclosure at the local level through websites revealed that most studies have focused primarily on economic and political determinants of voluntary financial information (Tejedo-Romero and Araújo, 2018). At the international level, we found research by Laswad et al. (2005); Pietrowsky and Van Ryzin (2007); Piotrowski and Bertelli (2010); Jorge et al. (2011); Ma and Wu (2011); Frías-Aceituno et al. (2013); Bunget et al. (2014); and Brusca et al. (2016), among others. Focusing on Spain, papers such as Cárcaba and García (2008), Serrano-Cinca et al. (2009a), Guillamón et al. (2011), Albalate del Sol (2013) and Alcaide and Rodríguez (2015) analyse voluntary information and financial disclosure by local governments. This review identified an increase in research that analyses the factors that lead to greater financial information disclosure by the public sector. Among other studies analysing these disclosure practices, both at the international and national level, we found research by Navarro et al. (2010); Navarro et al. (2011); Navarro et al. (2014); Frías-Aceituno et al. (2013); Nevado-Gil et al. (2013, 2016); García-Sánchez et al. (2013); Moura et al. (2014); and Alcaraz-Quiles et al. (2015).

According to most studies focusing on the dissemination of information online, population size is a basic factor that determines these practices (Ribeiro, 2007; Pilcher et al., 2008; Cárcaba and García, 2008; Ribeiro and Aibar, 2008; Serrano-Cinca et al., 2009a, 2009b; Joseph, 2010; Navarro et al., 2010; Ribeiro and Aibar, 2010; Jorge et al., 2011; García-Sánchez et al., 2013). Ahmed and Courtis (1999) confirm the significant and positive relationship between the level of disclosure and size, in a meta-analysis performed of 29 outreach studies. According to Ryan et al. (2002), size is positively associated with disclosure of annual reports in Australian local governments. Meanwhile, other authors in the literature reviewed, such as Larrán and Giner (2002), reached the same conclusion. Torres et al. (2005) argue that the publication of information on the internet has greater possibilities to be disclosed in the largest administrations that in the small. This may be because, as Guillamón et al. (2011) argue, the larger municipalities handle larger budgets, so, generally, they have more resources available to allocate to increase the disclosure of information. In addition, Navarro et al. (2010) justify this relationship on the grounds that large population municipalities have staff better qualified, which could encourage dissemination practices. However, based on their study of 55 large Spanish local governments, the cited authors concluded that the entities’ size does not explain the dissemination of SR information. The same conclusion was reached by Prado-Lorenzo et al. (2012) who, based on local Spanish government studies, found no significant relationship between population size and sustainable information disclosure. For García-Sánchez et al. (2013), large populations tend to demand more services and have a broader variety of stakeholders, requiring, among other things, more information on sustainability. In this cited study of 102 Spanish local governments, the results indicate that the organisations’ size has a positive impact on sustainability reporting. In general, it can be said that the previous literature argues the existence of a positive relationship between the size of the municipality and information disclosure (Cárcaba and García, 2008; García et al., 2013; Nevado and Gallardo, 2016). Therefore, in this study, the following hypothesis was proposed:

H1: A significant and positive relationship exists between entities’ size and their level of SR information disclosure.

Another factor that the literature suggests can influence information disclosure is the amount of public resources available (Serrano-Cinca et al., 2009a, 2009b; García-Sánchez et al., 2013). Laswad et al. (2005) and Serrano-Cinca et al. (2009a, 2009b) found a positive association between municipal wealth – measured by per capita income – and level of disclosure. Similarly, Navarro et al. (2010) assert that municipalities with higher incomes have more means to improve their information systems. However, the cited results provide no empirical evidence to link the volume of budgetary resources managed by local administrations and their level of information dissemination on the Internet. Guillamón et al. (2011) found evidence in a sample of the 100 largest Spanish municipalities that budgetary capacity, represented by total spending per capita, is positively related to levels of information disclosure. Along the same lines, García-Sánchez et al. (2013) argue that, the higher the level of public spending, the higher the levels of disclosure of sustainability. Based on these findings, the following hypothesis was developed:

H2: A significant and positive relationship exists between institutional capacity and levels of SR information disclosure.

Unemployment rates are also used in the literature as a possible factor explaining levels of disclosure. The higher their unemployment, the greater the municipalities’ social needs and, therefore, the greater the pressure on local governments to disseminate information (Navarro et al., 2010). Thus, Navarro et al. (2011) found a significant and positive relationship between unemployment rates and levels of information about sustainability in 17 Spanish regional governments. In contrast, authors such as Guillamón et al. (2011); Albalate del Sol (2013); and Caamaño-Alegre et al. (2013) report results indicating that municipalities with higher unemployment rates have lower levels of disclosure. Contrary to the above cited authors, García-Sánchez et al. (2013) were unable to confirm any impact of unemployment rates on the disclosure of sustainable practices information. Similarly, Nevado and Gallardo (2016) also did not find any type of impact of unemployment rates on the dissemination of information on sustainable practices. However, in times of crisis this negative relationship could have been like that, but there are recent studies that prove otherwise (Ortiz et al., 2018). Based on this literature, the following hypothesis was formulated:

H3: A significant and positive relationship exists between unemployment rates and levels of SR information disclosure.

Internet access is another factor the literature considers related to information disclosure (Caba Pérez et al., 2014; Pina et al., 2009; Alcaraz-Quiles et al., 2015; Saez-Martín et al., 2016). Access to broadband could generate an increase in demand for information that could lead to a wider dissemination of information. Debreceny et al. (2003) confirmed a positive relationship between these variables, while Caba Pérez et al. (2014) found no evidence for this relationship. Therefore, the following hypothesis was proposed:

H4: A significant and positive relationship exists between Internet access and levels of SR information disclosure.

In addition, public administrations are governed by politicians, and they try to attract more votes by meeting the demands of voters and other stakeholders in order to ensure reelection, so political ideas can be reflected in information disclosure (García et al., 2013). Therefore, the literature also considers factors such as political ideology, political competition, and electoral participation as determinants of the degree of disclosure (Cárcaba and García, 2008; Navarro etal., 2011; Jorge et al., 2011; Prado-Lorenzo et al., 2012; Albalate del Sol, 2013; Alcaraz-Quiles etal., 2015). Regarding political ideology, authors such as Navarro et al. (2010) and Jorge et al. (2011) show that the political orientation of ruling parties is not associated with levels of dissemination of SR information. However, Guillamón et al. (2011) confirmed that municipalities governed by progressive mayors disclose more information than do those governed by conservative mayors. García-Sánchez et al. (2013) also conclude that leftist governments disclose more information. In contrast, Prado-Lorenzo et al. (2012) research shows that parties with conservative tendencies increase their sustainable practices to attract more progressive voters.

Similarly, more political competition, based on the number of political parties participating in elections, can lead to greater information disclosure by government teams (Cárcaba and García, 2008). As political competition grows, the pressure on governing parties increases, which can be reflected in greater information disclosure that seeks to show citizens that these parties offer better services than opposition parties do. In the previous literature, some results, such as Laswad et al. (2005), reveal no statistically significant impact of this factor for New Zealand municipalities. However, authors such as Gandia and Archidona (2008), Navarro et al. (2011), and Prado-Lorenzo et al. (2012) show that levels of disclosure depend on political competition and, moreover, that this influence is positive.

Finally, voter turnout in municipal elections is also considered an indicator of information disclosure as electoral participation demonstrates citizens’ interest in government activities (Jorge et al., 2011; Albalate del Sol, 2013). A high voter turnout indicates that citizens have a greater interest in government initiatives (Esteller-Moré and Polo-Otero, 2008; Caamaño-Alegre et al., 2013). Authors such as Esteller-Moré and Polo-Otero (2008) report a positive relationship between electoral participation and fiscal transparency, which is considered an aspect of information dissemination. For Jorge et al. (2011), voter abstention also appears to be a positive determinant, while in Albalate del Sol’s (2013) research, this does not appear to be statistically significant. The resulting proposed hypotheses were:

H5: Political parties with a progressive ideology show higher levels of disclosure than parties with a conservative ideology do.

H6: A significant and positive relationship exists between political competition and levels of SR information disclosure.

H7: A significant and negative relationship exists between levels of electoral participation and levels of SR information disclosure.

3. Empirical study

3.1. Sample selection, objectives, and methodology

Nevado-Gil et al. (2013) analysed the information disclosed about SR, between January and February 2013, by a sample of 40 Extremadura municipalities that represent 64.22% of the autonomous community’s total population. Municipalities with a population equal to or more than 5,000 people were chosen, based on a distinction made in Article 20 of Law 7/1985 of 2 April (Government of Spain, 1985) regulating local regimes according to municipalities’ organisation. In order to compare disclosure practices over time, the present study used the same sample of Extremadura municipalities’ information disclosure in January and February 2016. The Law makes an express mention of the Social Responsibility of the Autonomous Public Administration itself and its dependent public agencies, such as consuming, investing, contracting, employing and providing services entities. Likewise, having an Annual Report on Government Social Responsibility, which systematically includes the policies, measures, actions and actions developed by the different public agencies of its administration, makes the municipalities adopt the same behaviors. This regulation, innovative and pioneering in Spain and in the autonomous community, is one of the agreements included in the Social and Political Reform Pact for Extremadura, approved by the Assembly of Extremadura on April 22, 2010, which aimed to change the production model in the region to achieve sustainable development, based on values such as equal opportunities and social and territorial cohesion. The existence of this Pact and this Law, which are approved in 2010 and set out a very broad plan of actions for companies and institutions, encourages us to check whether the dissemination of social information in this autonomous community is really being undertaken.

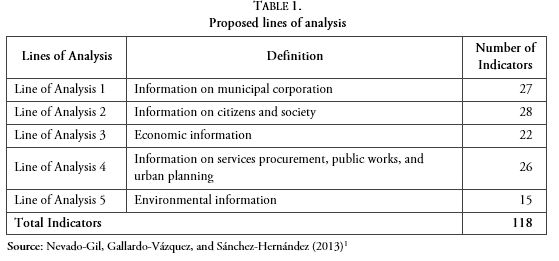

To achieve the research objectives, first, we did a temporal study by collecting data from the websites of Extremadura municipalities at two points in time (i.e. 2013 and 2016), to verify whether these institutions are involved in an evolving process that seeks to satisfy users’ expressed information needs. In addition, we checked if that evolution is occurring in all the aspects analysed of data collected with a questionnaire. To achieve this goal, content analysis was used, as has been done in numerous studies of this nature (Rodríguez et al., 2006, 2007; Pina et al., 2007; Navarro et al., 2010; Moneva and Martin, 2012; Nevado-Gil et al., 2013; Navarro et al., 2015). This technique allows the systematisation of qualitative information. Content analysis, according to Dumay and Cai (2015), is ‘a research technique designed to formulate, from certain data, reproducible and valid inferences that may apply to your context’. Data were collected with the aforementioned questionnaire, which had already been used in previous studies (Nevado-Gil et al., 2013, 2016), consisting of a total of 118 indicators divided into five lines of analysis (see Table 1).

Proposed lines of analysis

Source: Nevado-Gil, Gallardo-Vázquez, and Sánchez-Hernández (2013)1

The information gathered enabled the development of an index in order to analyse the degree of SR information disclosure on Extremadura municipalities’ websites. To apply this index, the criterion of the presence or absence of each indicator contained in the proposed questionnaire was considered and assigned the value of one if the indicator’s information was disclosed and zero otherwise. The use of indices to measure levels of information has been applied in numerous studies, including Gandia and Archidona (2008); Jorge et al. (2011); Navarro et al. (2010); Joseph and Taplin (2011); Moneva and Martin (2012); Beuren and Angonese (2015), and Navarro et al. (2015).

Second, once the disclosure index scores had been calculated, we analysed possible factors affecting the degree of dissemination of SR information. For this, we carried out a multiple linear regression of the disclosure index following the approach used by Laswad et al. (2005); Moura et al. (2014); Alcaraz-Quiles et al. (2015) and Garrido et al. (2019), among others. The estimation was done with the EViews software version 6.

3.2. Dependent variable: Index disclosure

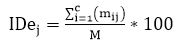

As noted above, the level of dissemination of SR information was measured with an index consisting of the score each municipality received through a process of review and analysis of municipality web pages. Before calculating the index scores – in order to analyse the level of disclosure by categories of information – a partial index was calculated for each of the lines of analysis into which the questionnaire was divided. These partial indices were determined by the ratio of the sum of the number of items identified on each website and the total number of items that made up each line of analysis. To express this in percentage, the scores were multiplied by 100:

[1]

[1]in which IDej= the partial index of information disclosure of line of analysis ‘e’ in the municipality ‘j’; mij = the number of items identified on the website; c = the total score obtained for each municipality in each line of analysis; M = the number of items that make up each line of analysis ‘e’; and e = each of the lines of analysis that make up the disclosure index. In the equation below, C = the line of analysis of each municipal corporation; S = the line of analysis of social information; O = the line of analysis of services and public works contracts; E = the line of analysis of economic information; and M = the line of analysis of environmental information.

The index of full SR disclosure by municipality was calculated with the following equation:

[2]

[2]Having no empirical evidence of the relative importance of the various partial indices that made up the overall index, the same weight was assigned to each of the dimensions or lines of analysis.

3.3. Explanatory variables

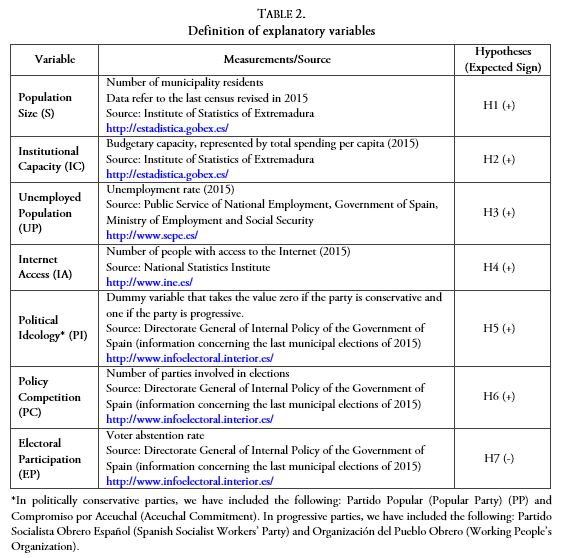

The results of the literature review guided the selection of the correct variables to include in the present study (Cárcaba and García, 2008; Pilcher et al., 2008; Serrano-Cinca et al., 2009a, 2009b; Guillamón et al., 2011; Jorge et al., 2011; Cruz et al., 2012; Esteller-Moré and Polo-Otero, 2012; García et al., 2013; Caamaño-Alegre et al., 2013; Albalate del Sol, 2013; Cuadrado, 2014; Alcaraz-Quiles et al., 2015). We thus considered the explanatory variables that are listed in Table 2.

3.4. Model specification

To carry out the contrast of the assumptions detailed in previous sections, multivariate regression techniques were used. Based on multiple linear regression, using the ordinary least squares method, the following model was estimated:

[3]

[3]In addition, an error term (Ɛ) was also incorporated, which includes the incidents of when the SR information disclosure index is not explained by the independent variables’ effects.

Definition of explanatory variables

*In politically conservative parties, we have included the following: Partido Popular (Popular Party) (PP) and Compromiso por Aceuchal (Aceuchal Commitment). In progressive parties, we have included the following: Partido Socialista Obrero Español (Spanish Socialist Workers’ Party) and Organización del Pueblo Obrero (Working People’s Organization).

4. Analysis of results and discussion

4.1. Evolution of disclosure information index

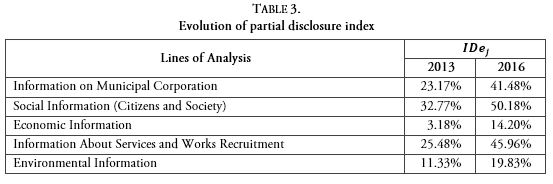

Table 3 shows the results of the partial indices of SR information disclosure and their evolution in the years considered.

Evolution of partial disclosure index

As can be seen, the results reveal a marked increase in the information provided by municipalities through their websites. If, in 2013, the SR information disclosure was quite low, in 2016, there was an increase in the amount of information disclosed. An important fact to note – as a possible reason for this dramatic increase – is the municipal elections held in 2015, which led to changes in government. These data were subsequently analysed to see if this increase may be due to political factors. Another possible reason for this increase in the information disclosed may be that in the public sector, there is greater awareness and conviction about sustainability. As we have already mentioned in this work, citizens are the main agent of interest and demand information and transparency in the performance of municipal management, therefore, increasingly, the administration is becoming aware of the need to improve and streamline the relationship between citizens and the Administration. For example, with the implementation of the e-Administration technology platform (e-Government portal) and its placement at the service of citizens, full and detailed information on social, economic and environmental issues is offered, while raising awareness to the citizen through social and environmental campaigns and allows them an active participation in decision making. On the other hand, the new regulations also affect that increase in the amount of information disclosed. In particular, we consider that one of the influential reasons in the high economic information offered by the local governments of our sample, in relation to previous studies, could be the approval of Law 19/2013, of December 9, of Transparency, Access to Public Information and Good Government2. This Law increases and reinforces transparency in public activity and recognizes the right to information to citizens. As can be seen in our study, the information that increases the most is related to economic aspects.

However, some municipalities still do not provide this type of information on the Internet, and, notably, the information in many cases has not been updated. This suggests that, at some point, municipalities decided to provide this information online, but, in subsequent years, they have shown no interest in updating it. In addition, it was also observed that the information provided in many cases is incomplete. Therefore, the Extremadura municipalities still have much to do to improve their information disclosure practices.

4.2. Determinant factors

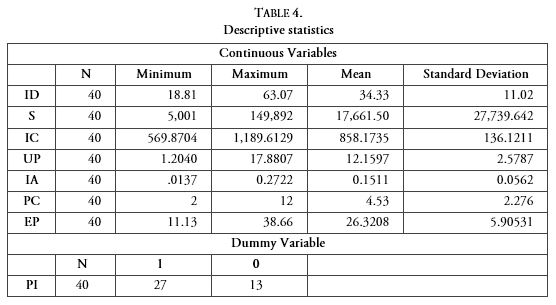

Descriptive analysis. Having analysed the evolution of the information disclosure index, we examined the factors that determine the relevant disclosure. To this end, we chose to use as a dependent variable the index values for the last year studied (i.e. 2016), since these contain the most current and complete information. Table 4 presents the descriptive statistics of mean, standard deviation, and maximum and minimum values. The continuous variables are presented first, and the dummy variable second. As can be seen from this table, the variables of population size (S) and institutional capacity (IC) have a remarkable degree of dispersion that reflects the diversity of resources among the municipalities studied. The other variables do not show a large dispersion. With respect to the dummy variable (PI), the statistics show that, according to the results of the last municipal elections in 2015, most municipalities are now governed by progressive parties (i.e. 27 municipalities).

Descriptive statistics

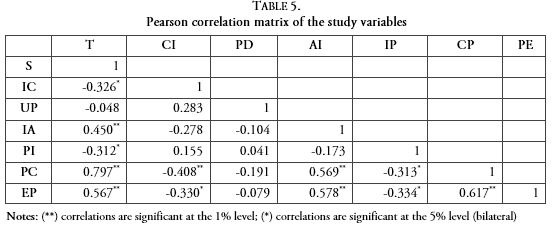

Univariate analysis. In order to check whether a correlation exists between the model variables, the Pearson correlation coefficient was applied (see Table 5), as this measures the overall degree of association between two random variables. The correlation matrix shows that most of the independent variables have a moderate or low correlation, except for a few variables that have a strong correlation. However, none of these correlations reached the value of 0.80 considered critical by Cooper and Schindler (2008) and Naser and Hassan (2013). Therefore, multicollinearity does not appear to be a problem in the model, so none of the variables considered for regression analysis had to be removed.

Pearson correlation matrix of the study variables

Notes: (**) correlations are significant at the 1% level; (*) correlations are significant at the 5% level (bilateral)

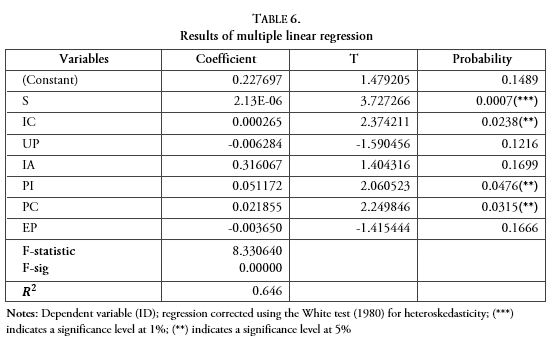

Multivariate analysis. Prior to regression analysis, we checked the basic assumptions of the general linear model and detected the presence of heteroskedasticity. To solve this problem and get more robust estimations of the regression coefficients, we used the White (1980) test to correct the regression and estimated the model using weighted least squares. The results obtained are presented in Table 6. The Importar imagen shows that the model has an explanatory power of 64.6%, a considerably higher percentage than for models dealing with cross-sectional data (Gujarati, 2009). Table 6 also shows the F-statistic (8.330640), which measures whether the independent variables included in the model, when considered together, influence the rate of SR information disclosure. Based on the value of the F-sig (0.0000), which is less than 0.01, we concluded that a confidence level of at least 99% exists that the proposed model explains the dependent variable.

Results of multiple linear regression

Notes: Dependent variable (ID); regression corrected using the White test (1980) for heteroskedasticity; (***) indicates a significance level at 1%; (**) indicates a significance level at 5%

Regarding the individual significance of each independent variable, as shown in Table IV, the variable representing population size (S) is shown to be extremely significant at a 99% confidence level (t-statistic = 3.72; probability = 0.0007). This variable is positively associated with the dependent variable (ID), as can be seen by the associated coefficient ( β1 = 2.13E-06). The first hypothesis (H1) is, therefore, confirmed, indicating that, the larger the size of the selected Extremadura municipalities, the higher their rate of SR information disclosure. These results are consistent with those of other authors, such as Larrán and Giner (2002); Ryan et al. (2002); Cárcaba and García (2008); and García-Sánchez et al. (2013).

Regarding institutional capacity (IC), we checked this using statistical measures (t-statistic = 2.37; probability = 0.0238) and found this variable is individually significant at a 95% confidence level and is positively associated with the dependent variable (ID) ( β2= 0.000265). This confirms the second hypothesis (H2). The present results coincide with those of previous studies (Laswad et al., 2005; Gandía and Archidona, 2008; Guillamón et al., 2011) in which higher levels of information disclosure have been observed in municipalities with more resources.

Regarding the political variables of ideology and political competition (PI and PC) – as was found in most previous studies (Gandía and Archidona, 2008; Guillamón et al., 2011; Navarro et al., 2011; Prado-Lorenzo et al., 2012; García et al., 2013) – a significant influence at a 95% confidence level was confirmed (t-statistic = 2.060523; probability = 0.0476 for PI and t-statistic = 2.249846; probability = 0.0315 for PC). The signs of the coefficients ( β5 = 0.051172 and β6= 0.021855, respectively) show a positive relationship with the level of SR information disclosure. These results confirm, therefore, the fifth and sixth hypotheses (H5 and H6), which indicate that municipalities governed by progressive parties and characterised by more intense political competition have higher levels of information disclosure.

The remaining variables (i.e. unemployed population, Internet access, and voter turnout) are not statistically significant in the model, so they have no effect on the dependent variable. This meant that the third, fourth, and seventh hypotheses (H3, H4, and H7) were rejected. A growing unemployed population, greater access to the Internet by municipalities’ citizens, and greater or lesser participation of citizens in municipal elections does not appear – according to the results for the present sample – to explain the behaviour of ruling parties in terms of information disclosure.

5. Conclusions, implications, limitations and future research

This research was conducted on a sample of the largest local authorities in Extremadura. The data collected revealed an increase in the amount of SR information disclosed between 2013 and 2016. This study also examined some determinants of the level of this information disclosure based on an analysis of these municipalities’ websites.

The results can be divided into two distinct areas. First, the evidence shows that the factors behind the rate of SR information disclosure are municipalities’ size, institutional capacity, political ideology of the ruling party, and political competition. Second, contrary to expectations, others factors do not explain the level of information disclosed, among which are a population with higher or lower unemployment rates, Internet access, and greater or lesser electoral participation. Given these results, municipalities can now refocus their practices and policies of SR information disclosure based on the factors that have or do not have an effect on levels of information disclosure.

In order to find a clear explanation that includes the main reason for the increase of information disclosed in 2016, we connected the present results with those of Nevado-Gil et al. (2016). In this previous research based on a review of municipalities’ websites between 2013 and 2015, no significant differences were found in the level of information disclosure. Given the change of government resulting from municipal elections in May 2015, the present research focused on the presence of political factors, revealing that these are the main cause of most levels of information disclosure. These two studies represent a continuity in the phenomena under study, allowing us to discover in the second study some progress compared to the previous study’s results. These results can also be explained with information dissemination theories. In the first place, we can say that, according to the Theory of Legitimacy, it is expected that politicians who want to participate in projects that require significant efforts when undertaking a public investment, will be interested in disseminating this information. Therefore, in election years, in municipal budgets, politicians will encourage the dissemination of information to obtain voter support. Second, the Theory of the Agency is related to the actions of politicians in relation to satisfying the needs of citizens. The rulers must be responsible for their actions and the problem of asymmetry of information is raised. When trying to reduce the problem of asymmetry in information what is achieved is to restore the confidence of the citizen in the politicians, something of vital importance in these moments (Garrido et al., 2019). Finally, the Theory of Stakeholders tries to explain how an entity adopts certain behaviors and issues external information to guarantee its survival. This theory is based on how interdependencies are managed by interest groups that are relevant to the organization. In this sense, interest groups with power are those on which the survival of the entity depends in terms of economic interests, above aspects of moral or legal legitimacy.

We conclude, therefore, that larger municipalities in Extremadura with more resources available, governed by progressive parties, and characterised by more intense political competition, will be more prone to disseminate SR information. At the same time, it appears that unemployment does not motivate governments of Extremadura municipalities to release SR information and neither does having citizens with increasing Internet access. Finally, citizens’ participation in elections does not appear to be decisive in Extremadura municipalities’ dissemination of SR information.

The above findings clearly have implications for various areas. In terms of academic contributions, some influential and nondecisive factors have been identified by measuring the levels of SR information disclosure for municipalities in Extremadura. This indicates that research can be done to help local administrations by observing which policies encourage and promote some factors and by seeking to eliminate the negative effects of other factors in order to prevent low levels of information disclosure. This can assist municipalities achieve clear public policies and strategies to cover to the maximum level possible citizens’ demands. These academic contributions undoubtedly are tied to implications for local governments, achieving a much sought after link between university and local government initiatives and covering an existing gap in previous research.

We would like to emphasize the importance of the online services implementation by the administration. It leads to transforming these organizations, improving efficiency and effectiveness in the internal government administration. At the same time, offering online public services leads to a more open context which improves the image of organizations, increases information transparency and enables citizens to increase their participation in making decisions.

Even if the results obtained for the proposed model are positive, the limitations of this study need to be mentioned. This research has some limiting aspects that restrict the results obtained and, therefore, reduce their usefulness when extrapolated to broader contexts of study. The first is the size of the sample. The municipalities were selected based on current theoretical interests, but a larger sample could yield different results and produce a greater or lesser number of verified hypotheses. The second limitation is that region and country effects must also be considered. In this case, all the municipalities analysed are in Extremadura, Spain. A consideration of entities belonging to other regions and even other countries could produce different results.

In response to these issues, possible future research could include studies with larger sample sizes, with municipalities belonging to other regions of Spain and local governments of other countries. Finally, although not derived from any limitation of the present study, we intend to continue this research by applying other current methodologies that can identify causal relationships between the variables studied and predict future behaviour in municipalities.

Finally, we can offer some recommendations to local governments, among which we rule out the following: an important factor is the direct and explicit commitment of the representative of the government team, in this case the Mayor, as well as the rest of the corporation, on the importance of sustainability, including priorities, strategies and initiatives that are going to be carried out, as well as communicating their successes and achievements in CSR in any of their social, economic and environmental spheres, to the stakeholders, through a strategic CSR plan that culminates with the preparation and publication of a CSR Report. It is also recommended to approve a Code of Good Governance for all political groups or managers and create a commission for reflection and debate with the participation of employees and interest groups.

In addition, you must dispense with information that may be misleading or that incites illegal behavior and thus maintain the quality and safety of the service offered. On the other hand, in order to guarantee and improve the provision of services, it must comply with the legal and regulatory requirements established in current regulations. You can also improve customer service by creating an office and a citizen information platform where municipal information services are offered, information on the city, document confirmation, appointment with councillors and technicians, immediate resolution procedures (registration of mopeds, collection of fines, receipt and delivery of lost objects, modifications of the registers, etc.) and also, establish procedures for the treatment of suggestions, complaints and claims of citizens, obtaining the maximum information about their needs and expectations, as well as the degree of satisfaction towards the services rendered. In this way, it will encourage citizen participation in municipal decisions and will gather opinions, proposals and conclusions that will help support the preparation of municipal budgets.

Another good practice with this interest group could be the adoption of a commitment to reduce road accidents, analyzing and identifying the accident concentration sections, signaling and applying corrective measures in these sections and evaluating the effectiveness of the measures applied.

In terms of society and community, we propose respect and protection of the environment through an Environmental Action Plan that allows actions to be carried out in a sustainable manner aimed at improving the environment such as reducing polluting emissions, improving and conserving of the environmental quality of the Local Entity, the protection and conservation of the natural wealth of the territory, the optimization of the use of natural resources (water, energy or other resources), the reduction of the dependence on non-renewable resources and the promotion of of changes in habits and attitudes on the part of the population in the line of sustainability. Likewise, the possibility of achieving a commitment to energy efficiency and reducing light pollution from public lighting is proposed, establishing conditions to be met by new facilities in terms of efficiency such as replacing traditional street lighting with LED bulbs, analyzing and evaluating economically the corrective measures to be applied on efficient lighting, elaborating and approving new regulations in this matter and assigning an economic endowment for the fulfillment of these purposes, as well as the adoption of a commitment to adhere to the principles of the Agenda 21. Concerning sustainable mobility, we suggest encouraging the use of environmentally-friendly means of transport, as well as the incorporation of non-polluting means of transport.

References

Albalate del Sol, D. (2013). The institutional, economic and social determinants of local government transparency. Journal of Economic Policy Reform, 16(1), 90–107. https://doi.org/10.1080/17487870.2012.759422

Alcaide, M. L., & Rodríguez, B. M. P. (2015). Determining Factors of Transparency and Accountability in Local Governments: A Meta-Analytic Study. Lex Localis, 13(2), 129-160. https://doi.org/10.4335/13.2.129-160(2015)

Alcaraz-Quiles, F. J., Navarro-Galera, A., & Ortiz-Rodríguez, D. (2015). Factors determining online sustainability reporting by local governments. International Review of Administrative Sciences, 81(1), 79–109. https://doi.org/10.1177%2F0020852314541564

Ahmed, K., & Courtis, J. K. (1999). Associations between corporate characteristics and disclosure levels in annual reports: a meta-analysis. The British Accounting Review, 31(1), 35-61. http://dx.doi.org/10.1006/bare.1998.0082

Araujo, J. F. F. E. D., & Tejedo-Romero, F. (2016). Local government transparency index: Determinants of municipalities’ rankings. International Journal of Public Sector Management, 29(4), 327–347. http://dx.doi.org/10.1108/IJPSM-11-2015-0199

Asgary, N., & Li, G. (2016). Corporate Social Responsibility: Its Economic Impact and Link to the Bullwhip Effect. Journal of Business Ethics, 135(4), 665–681. http://dx.doi.org/10.1007/s10551-014-2492-1

Beuren, I. M., & Angonese, R. (2015). Instruments for Determining the Disclosure Index of Accounting Information. Revista Eletronica de Estrategia e Negocios – REEN, 8(1), 120–144. http://dx.doi.org/10.19177/reen.v8e12015120-144

Bonsón, E., Torres, L., Royo, S., & Flores, F. (2012). Local E-government 2.0: Social media and corporate transparency in municipalities. Government Information Quarterly, 29(2), 123–132. http://dx.doi.org/10.1016/j.giq.2011.10.001

Brusca, I., Manes Rossi, F., & Aversano, N. (2016). Online sustainability information in local governments in an austerity context: An empirical analysis in Italy and Spain. Online Information Review, 40(4), 497–514. https://doi.org/10.1108/OIR-05-2015-0161

Bunget, O. C., Blidisel, R. G., Feleaga, L., & Popa, I. E. (2014). Empirical Study of Intangible Assets in Romanian Municipalities. Ekonomie a Management, 17(3), 136–151. http://dx.doi.org/10.15240/tul/001/2014-3-011

Caamaño-Alegre, J., Lago-Peñas, S., Reyes-Santias, F., & Santiago-Boubeta, A. (2013). Budget transparency in local governments: An empirical analysis. Local Government Studies, 39(2), 182–207. https://doi.org/10.1080/03003930.2012.693075

Caba Pérez, C., Rodríguez Bolívar, M. P., & López Hernández, A. M. (2014). The Determinants of Government Financial Reports Online. Transylvanian Review of Administrative Sciences, 42, 5–32.

Cárcaba, A., & García, J. (2008). Determinantes de la Divulgación de Información Contable A través de Internet por Parte de los Gobiernos Locales. Revista Española de Financiación y Contabilidad, 37(137), 63–84. https://doi.org/10.1080/02102412.2008.10779639

Cooper, D. R., & Schindler, P. S. (2008). Business research methods (10th ed.). Boston: McGraw-Hill Irwin.

Crane, A., Bastida, F., & Benito, L. J. (2008). Corporate Social Responsibility: Readings and Cases in a Global Context, Abingdon, UK: Routledge.

Cruz, C. F., Ferreira, A. S., Silva, L. M., & Macedo, M. S. (2012). Transparência da Gestão Pública Municipal: Um Estudo a Partir dos Portais Eletrônicos dos Maiores Municípios Brasileiros. Revista de Administração Pública, 46(1), 153–76.

Cuadrado, B. B. (2014). The impact of functional decentralization and externalization on local government transparency. Government Information Quarterly, 31(2), 265–277. https://doi.org/10.1016/j.giq.2013.10.012

Cuadrado B, B., Frías Aceituno, J., & Martínez Ferrero, J. (2014). The role of media pressure on the disclosure of sustainability information by Local Governments. Online Information Review, 38(1), 114-135. https://doi.org/10.1108/OIR-12-2012-0232

Cueto, C. C., de la Cuesta, G. M., & Moneva, A. J. M. (2014). La Oferta Informativa Sobre Responsabilidad Social Corporativa en las Administraciones Locales Españolas. Revista Prisma Social, Revista de Ciencias Sociales, 12, 646–687.

Debreceny, R., Gray, G., & Rahman, I. (2003). The Determinants of Internet Financial Reporting. Journal of Accounting and Public Policy, 21(4-5), 371–394. https://doi.org/10.1016/S0278-4254(02)00067-4

Díaz, C. V. (2009). Transparencia de la Información Económico-Financiera A través del E-Gobierno o Gobierno Electrónico: Caso Español. Perspectivas, 24, 59–90.

Dumay, J., & Cai, L. (2015). Using content analysis as a research methodology for investigating intellectual capital disclosure: a critique. Journal of Intellectual Capital, 16(1), 121-155. https://doi.org/10.1108/JIC-04-2014-0043

Esteller-Moré, A., & Polo-Otero, J. (2008). Analysis of the Causes of Fiscal Transparency: Evidence from Catalonian Municipalities. Unpublished paper. University of Barcelona.

Esteller-Moré, A., & Polo-Otero, J. (2012). Fiscal Transparency: Why Does Your Local Government Respond?. Public Management Review, 14(8), 1153–1173. https://doi.org/10.1080/14719037.2012.657839

Frías-Aceituno, J. V. F., da Conceição Marques, M., & Ariza, L. R. (2013). Divulgación de información sostenible: ¿Se adapta a las expectativas de la sociedad? Revista de Contabilidad, 16(2), 147–158. https://doi.org/10.1016/j.rcsar.2013.07.004

Frías-Aceituno, J. V. F., García-Sánchez, I. M., & Rodríguez Domínguez, L. (2014). Electronic administration styles and their determinants. Evidence from Spanish Local Governments. Transylvanian Review of Administrative Sciences, 10(41), 90-108.

Gallardo-Vázquez, D., Sánchez-Hernández, M. I., & Corchuelo-Martínez-Azúa, M. B. (2013). Validación de un Instrumento de Medida Para la Relación Entre la Orientación a la Responsabilidad Social Corporativa y Otras Variables Estratégicas de la Empresa. Revista de Contabilidad, 16(1), 11–23. https://doi.org/10.1016/S1138-4891(13)70002-5

Gandía, J. L., & Archidona, M. C. (2008). Determinants of Website Information by Spanish City Councils. Online Information Review, 32(1), 35–57. https://doi.org/10.1108/14684520810865976

Gandía, J. L., Marrahí, L., & Huguet, D. (2016). Digital transparency and Web 2.0 in Spanish city councils. Government Information Quarterly, 33(1), 28-39. https://doi.org/10.1016/j.giq.2015.12.004

García-Sánchez, I. M., Frías-Aceituno, J. V., & Rodríguez-Domínguez, L. (2013). Determinants of corporate social disclosure in Spanish local governments. Journal of Cleaner Production, 39, 60–72. https://doi.org/10.1016/j.jclepro.2012.08.037

Garrido-Rodríguez, J. C., López-Hernández, A. M., & Zafra-Gómez, J. L. (2019). The impact of explanatory factors on a bidimensional model of transparency in Spanish local government. Government Information Quarterly, 36(1), 154-165. https://doi.org/10.1016/j.giq.2018.10.010

Global Reporting Initiative (GRI) (2005). Sector Supplement for Public Agencies, Amsterdam: Global Reporting Initiative.

Global Reporting Initiative (GRI) (2010). Reporting in Government Agencies. Amsterdam: Global Reporting Initiative.

Government of Spain (1985). Ley 7/1985, de 2 de Abril, Reguladora de las Bases del Régimen Local. Boletín Oficial del Estado, 80, 8945–8964.

Government of Spain (2010). Ley 15/2010, de 9 de Diciembre, de Responsabilidad Social Empresarial en Extremadura. Boletín Oficial del Estado, 314, 107269–107283.

Guillamón, M. D., Bastida, F., & Benito, B. (2011). The determinants of local government’s financial transparency. Local Government Studies, 37(4), 391–406. https://doi.org/10.1080/03003930.2011.588704

Gujarati, D. N. (2009). Basic Econometrics, New York: Tata McGraw-Hill Education.

Heeks, R., & Bailur, S. (2007). Analyzing E-Governement Research: Perspectives, Philosophies, Theories, Methods, and Practice. Government Information Quarterly, 7, 114–197. https://doi.org/10.1016/j.giq.2006.06.005

Jorge, S., Moura, P., Pattaro, A., & Lourenço, R. (2011). Local government financial transparency in Portugal and Italy: A comparative exploratory study on its determinants. In Proceedings from CIGAR 2011: The Thirteenth Biennial CIGAR Conference, Bridging Public Sector and Non-Profit Sector Accounting (pp. 9–10).

Joseph, C. (2010). Content Analysis of Sustainability Reporting on Malaysian Local Authority Websites. Journal of Administrative Science, 7(1), 101–25.

Joseph, C., & Taplin, R. (2011). The Measurement of Sustainability Disclosure: Abundance Versus Occurrence. Accounting Forum, 35(1), 19–31. https://doi.org/10.1016/j.accfor.2010.11.002

Larrán, M., & Giner, B. (2002). The Use of the Internet for Corporate Reporting by Spanish Companies. The International Journal of Digital Accounting Research, 2(3), 53–82.

Laswad, F., Fisher, R., & Oyelere, P. (2005). Determinants of voluntary Internet financial reporting by local government authorities. Journal of Accounting and Public Policy, 24(2), 101–121. https://doi.org/10.1016/j.jaccpubpol.2004.12.006

López-López, V., Iglesias-Antelo, S., Vázquez-Sanmartín, A., Connolly, R., & Bannister, F. (2018). e-Government, Transparency & Reputation: An Empirical Study of Spanish. Local Government. Information Systems Management, 35(4), 276-293. https://doi.org/10.1080/10580530.2018.1503792

Ma, L., & Wu, J. (2011). What Drives Fiscal Transparency? Evidence From Provincial Governments in China. Paper presented at the 1st Global Conference on Transparency Research, Rutgers University-Newark, NJ, 2011 May.

Marcuccio, M., & Steccolini, I. (2005). Social and Environmental Reporting in Local Governments: A New Italian Fashion?. Public Management Review, 7, 155–176. https://doi.org/10.1080/14719030500090444

Mazzara, L., Sangiorgi, D., & Siboni, B. (2010). Public Strategic Plans in Italian Local Governments: A Sustainability Development Focus. Public Management Review, 12(4), 493–509. https://doi.org/10.1080/14719037.2010.496264

McTavish, D., & Pyper, R. (2007). Monitoring the public appointments process in the UK. Public Management Review, 9(1), 145–153. https://doi.org/10.1080/14719030601181290

Meijer, A., ’t Hart, P., & Worthy, B. (2018). Assessing government transparency: an interpretive framework. Administration & Society, 50(4), 501-526. https://doi.org/10.1177%2F0095399715598341

Moneva, J., & Martin, E. (2012). Universidad y Desarrollo Sostenible: Análisis de la Rendición de Cuentas de las Universidades Públicas Desde un Enfoque de Responsabilidad Social. Revista Iberoamericana de Contabilidad de Gestión, 10(19), 1–18.

Moura, A., Ribeiro, V., & Monteiro, S. (2014). Divulgação de informação na Internet sobre responsabilidade aocial – Evidência empírica nos municípios Portugueses. XXIV Jornadas Luso-Espanholas de Gestão Científica. February, Leiria (Portugal).

Naser, K., & Hassan, Y. (2013). Determinants of corporate social responsibility reporting: Evidence from an emerging economy. Journal of Contemporary Issues in Business Research, 2(3), 56–74.

Navarro, A., Alcaraz, F. J., & Ortiz, D. (2010). La divulgación de información sobre responsabilidad corporativa en administraciones públicas: Un estudio empírico en gobiernos locales. Revista de Contabilidad, 13(2), 285–314. https://doi.org/10.1016/S1138-4891(10)70019-4

Navarro, A., Ortiz, D., Alcaraz, F. J., & Zafra, J. L. (2011). La divulgación de información sobre sostenibilidad en los gobiernos regionales y sus factores influyentes: El caso de España (Unpublished paper). The Sixteenth AECA Conference, Granada, Spain.

Navarro, A., de los Ríos, A., Ruiz, M., & Tirado, V. P. (2014). Transparency of Sustainability Information in Local Governments: English-Speaking and Nordic Cross-Country Analysis. Journal of Cleaner Production, 64, 495–504. https://doi.org/10.1016/j.jclepro.2013.07.038

Navarro, A., Tirado Valencia, P., Ruiz Lozano, M., & de los Ríos Berjillos, A. (2015). Divulgación de información sobre responsabilidad social de los gobiernos locales europeos: El caso de los países nórdicos. Gestión y Política Pública, 24(1), 229–270.

Nevado Gil, M. T., Gallardo Vázquez, D., & Sánchez Hernández, M. I. (2013). La administración local y su implicación en la creación de una cultura socialmente responsable. Revista Prisma Social, Revista de Ciencias Sociales, 10, 64–118.

Nevado Gil, M. T., Gallardo Vázquez, D., & Sánchez Hernández, M. I. (2016). Análisis del grado de divulgación de información sobre responsabilidad social en las webs de los principales municipios extremeños. Auditoría Pública, 67, 77–92.

Nevado Gil, M. T., & Gallardo Vázquez, D. (2016). Información sobre Responsabilidad Social contenida en las páginas webs de los ayuntamientos. Estudio en la región del Alentejo. Revista Española de Documentación Científica, 39(4), 150. https://doi.org/10.3989/redc.2016.4.1353

Ortiz-Rodríguez, D., Navarro-Galera, A., & Alcaraz-Quiles, F. J. (2018). The influence of administrative culture on sustainability transparency in European Local Governments. Administration & Society, 50(4), 555-594. https://doi.org/10.1177%2F0095399715616838

Pilcher, R., Ross, T., & Joseph, C. (2008). Sustainability Reporting on Local Authority Websites Within an Institutional Theory Framework. Paper presented at the 7th Australian Conference for Social and Environmental Accounting Research, 510–531. Adelaide, South Australia: Center for Accounting Governance and Sustainability, 2008 December.

Pina, V., Torres, L., & Acerete, B. (2007). Are ICTs Promoting Governements’ Accountability? A Comparative Analysis of E-Governance Developments in 19 OECD Countries. Critical Perspectives on Accounting, 18(5), 583–602. https://doi.org/10.1016/j.cpa.2006.01.012

Pina, V., Torres, L., & Royo, S. (2009). E-Government Evolution in EU Local Governments: A Comparative Perspective. Online Information Review, 33(6), 1137–1168. https://doi.org/10.1108/14684520911011052

Piotrowski, S. J., & Van Ryzin, G. G. (2007). Citizen attitudes toward transparency in local government. The American Review of Public Administration, 37(3), 306–323. https://doi.org/10.1177%2F0275074006296777

Piotrowski, S. J., & Bertelli, A. (2010). Measuring Municipal Transparency. Paper presented at the 14th IRSPM Conference. Bern, Switzerland, 2010 April.

Porter, M., & Kramer, M. (2006). Estrategia y Sociedad. Harvard Business Review, 84(12), 42–56.

Prado-Lorenzo, J. M., García-Sánchez, I. M., & Cuadrado-Ballesteros, B. (2012). Sustainable cities: Do political factors determine the quality of life? Journal of Cleaner Production, 21(1), 34–44. https://doi.org/10.1016/j.jclepro.2011.08.021

Ribeiro, V. P. L. (2007). A Divulgação de Informação Ambiental nas Autarquias Locais Portuguesas. In Conocimiento, Innovación y Emprendedores: Camino al Futuro, (p. 71). Logroño, Spain: Universidad de La Rioja.

Ribeiro, V. P. L., & Aibar, C. G. (2008). Convergencia entre la Gestión Medioambiental Pública y Privada en el Ámbito de las Autarquías Locales. Revista Digital del Instituto Internacional de Costos, 2, 13–39.

Ribeiro, V. P. L., & Aibar, C. G. (2010). Determinants of Environmental Accounting Practices in Local Entities: Evidence from Portugal. Social Responsibility Journal, 6(3), 404–419. https://doi.org/10.1108/17471111011064771

Rodríguez, M. P., Caba, M. C., & López, A. (2006). Cultural Contexts and Governmental Digital Reporting. International Review of Administrative Sciences, 72(2), 269–290. https://doi.org/10.1177%2F0020852306064614

Rodríguez, M. P., Caba, M. C., & López, A. (2007). E-Government and Public Financial Reporting – The Case of Spanish Regional Governments. American Review of Public Administration, 37(2), 142–177. https://doi.org/10.1177%2F0275074006293193

Ryan, C., Stanley, T., & Nelson, M. (2002). Accountability Disclosures by Queensland Local Government Councils: 1997–1999. Financial Accountability and Management, 183, 261–289. https://doi.org/10.1111/1468-0408.00153

Saez-Martin, A., Caba-Perez, C., & Lopez-Hernandez, A. (2016). Freedom of information in local government: rhetoric or reality?. Local Government Studies, 1(29), 245-273. https://doi.org/10.1080/03003930.2016.1269757

Sandoval-Almazán, R., Gil-García, J. R., Luna-Reyes, L. F., Luna, D. E., & Díaz-Murillo, G. (2011). The use of Web 2.0 on Mexican state websites: A three-year assessment. Electronic Journal of E-government, 9(2), 107-121.

Schramm-Klein, H., Morschett, D., & Swoboda, B. (2015). Retailer Corporate Social Responsibility. International Journal of Retail and Distribution Management, 43(4/5), 403.

Serrano-Cinca, C., Rueda-Tomás, M., & Portillo-Tarragona, P. (2009). Factors influencing e-disclosure in local public administrations. Environment and Planning C: Government and Policy, 27(2), 355–378. https://doi.org/10.1068%2Fc07116r

Serrano-Cinca, C., Rueda-Tomás, M., & Portillo-Tarragona, P. (2009b). Determinants of E-Government Extension. Online Information Review, 33(3), 476–498. https://doi.org/10.1108/14684520910969916

Server, R. J. I., & Capó, J. V. (2009). La Responsabilidad Social Empresarial en un Contexto de Crisis. Repercusión en las Sociedades Cooperativas. CIRIEC-España, Revista de Economía Pública, Social y Cooperativa, 65, 7–31.

Shahzad, A. M., Rutherford, M. A., & Sharfman, M. P. (2016). Stakeholder‐Centric Governance and Corporate Social Performance: A Cross‐National Study. Corporate Social Responsibility and Environmental Management, 23(2), 100–112. https://doi.org/10.1002/csr.1368

Tejedo-Romero, F., & de Araujo, J. F. F. E. (2018). Determinants of local governments’ transparency in times of crisis: evidence from municipality-level panel data. Administration & society, 50(4), 527-554. https://doi.org/10.1177%2F0095399715607288

Torres L., Pina V., & Acerete B. (2005). E-government developments on delivering public services among EU cities. Government Information Quarterly, 22 (2), 217-238. http://dx.doi.org/10.1016/j.giq.2005.02.004

White, H. (1980). A Heteroskedasticity-Consistent Covariance Matrix Estimator and Direct Test for Heteroskedasticity. Econometrica, 48, 817–838. http://dx.doi.org/10.2307/1912934

Notes

Additional information

JEL classification: H83; H89; M14

Corresponding author: tnevado@unex.es