European Regional Policy

This work is licensed under Creative Commons Attribution-NonCommercial 4.0 International.

Received: 24 November 2019

Accepted: 04 February 2021

DOI: https://doi.org/10.38191/iirr-jorr.21.008

Abstract:

The debate on cohesion policy has recently intensified due to the increasing tensions within the EU and requires constant inputs with regards to various instruments which are applied. In Poland, a unique mechanism for guarantee distribution was adopted – the guarantees are mainly distributed through NGOs (nonbanking organisations granting guarantees – NOGG).

Thus, the article aims to investigate the relationship between the level of regional development, the experience of nonbanking organisations granting guarantees and their performance which leads to observations and recommendations with regards to the functioning and assessment of guarantees as cohesion policy instruments. We have used panel regression for 156 observations covering 26 NOGG in Poland.

The results confirm that there exist positive associations between the level of regional development, NOGG size (measured with guarantee capital) and experience and some financial performance measures. We posit, that a prerequisite for the high performance of these organisations is to ensure that they have an adequate level of guarantee capital and experience. We call for future EU-wide comparative research allowing deeper understanding of various guarantee distribution mechanisms performance.

Keywords: nonbanking organisations, guarantees, performance, regional development, cohesion policy.

Resumen:

El debate sobre la política de cohesión se ha intensificado recientemente debido a las crecientes tensiones en el seno de la UE y requiere constantes aportaciones en relación con los distintos instrumentos que se aplican. En Polonia, se adoptó un mecanismo único para la distribución de garantías: las garantías se distribuyen principalmente a través de las ONG (organizaciones no bancarias que conceden garantías - NOGG).

Así pues, el artículo pretende investigar la relación entre el nivel de desarrollo regional, la experiencia de las organizaciones no bancarias que conceden garantías y su rendimiento, lo que da lugar a observaciones y recomendaciones con respecto al funcionamiento y la evaluación de las garantías como instrumentos de la política de cohesión. Hemos utilizado una regresión de panel para 156 observaciones que cubren 26 NOGG en Polonia.

Los resultados confirman que existen asociaciones positivas entre el nivel de desarrollo regional, el tamaño de la NOGG (medido con el capital de la garantía) y la experiencia y algunas medidas de rendimiento financiero. Afirmamos que un requisito previo para el alto rendimiento de estas organizaciones es asegurar que tengan un nivel adecuado de capital de garantía y experiencia. Pedimos que en el futuro se realicen investigaciones comparativas en toda la UE que permitan comprender mejor el rendimiento de los distintos mecanismos de distribución de garantías.

Palabras clave: organizaciones no bancarias, garantías, rendimiento, desarrollo regional, política de cohesión.

1. Introduction

Irrespective of the level of analysis (national, regional or sub-regional), space is characterised by economic inequalities, social disparities and diverse geographical conditions which exert negative impacts on development in economic, social as well as environmental dimensions (Mendez et al., 2019).

It leads to the need for correcting actions that public authorities undertake to minimise the existing disproportions and hence their negative effects. In the European Union, these actions are predominantly contained within the EU’s cohesion policy. Since its creation, the EU pursues a cohesion policy that aims to address excessive disparities as well as to ensure sustainable growth and enhance the competitiveness of all its regions and the EU as a whole. The cohesion policy plays a critical role in the process of creation of European identity and therefore for the long-term stability of European Union project (Royuela & López-Bazo, 2020). The European identity and the support for cohesion policy varies substantially between countries, regions and demographic groups (Charron & Bauhr, 2020). Citizens with lower education and income, and those living in the lagging behind regions of the EU are less likely to identify with Europe (Perucca, 2020). It is a topical issue in the times of Brexit and tensions due to a possible economic downturn during and after Covid-19 pandemics.

The cohesion policy embraces a variety of financial, organisational and legal instruments (Hooghe & Marks, 2019). Under the principle of subsidiarity, it complements national, regional policies. Pelkmans (2006, p. 44-60) distinguishes two primary criteria for evaluation of cohesion policies: efficiency and equity. The efficiency of cohesion policies has been measured by absorption capacity (Iatu & Alupului, 2011; Moreno, 2020) and by the ability to generate economic growth in the lagging areas (Gagliardi & Percoco, 2017). Efficiency of EU Cohesion Policy and spending with other factors as the trust in the EU institutions, and the level of corruption mostly affect citizens’ identification with EU (Brasili et al., 2020).

In this paper, we concentrate on the efficiency aspect, analysing the performance of organisations granting guarantees.

The European Council decided to reduce direct public aid and concentrate on horizontal policies and indirect support, also for small and medium enterprises, in Lisbon in 2000. Apart from awarding grants to small business, guarantee schemes are created in many countries nowadays to help small and medium-sized enterprises (SMEs) obtain bank loans and increase their creditworthiness. Under the 2014-2020 Financial Framework, cohesion policy funding is delivered through the European Regional Development Fund, the European Social Fund and the Cohesion Fund.

As Griffith-Jones & Fuzzo de Lima (2004) emphasise that guarantee schemes play an essential role as mechanisms for support of private investments in case when the investors’ trust is low. Such tools are particularly important in the times of economic downturn when the access to capital for SMEs becomes increasingly difficult. The guarantee schemes were developing at a particularly fast pace in the 21st century when the loan guarantee mechanisms turned out to be a remedy for the risk aversion of investors.

Our study concentrates on the functioning of guarantee schemes in Poland and contributes to the ongoing debate on cohesion policy functioning in several ways. Firstly, the enterprises’ structure in Poland is characterised by a large number of SMEs with modest financial resources that translates to hindered access to capital (Waniak-Michalak et al., 2018). Therefore, cohesion policy – including guarantee schemes – is critical for their operations and competitiveness improvement. Secondly, Poland is the greatest beneficiary of cohesion funds under the 2014-2020 Financial Framework. For this reason, the efficiency of these funds is particularly relevant. Thirdly, a unique mechanism for guarantee distribution is adopted in Poland – the guarantees are distributed through NGOs (called later nonbanking organisations granting guarantees – NOGG) created in the 1990s during the economic system transformation. Their efficiency and financial sustainability play a critical role in the current and future allocation of cohesion funds in the form of financial instruments such as guarantees.

The main aim of this article is to investigate the relationship between the level of regional development and experience of nonbanking organisations granting guarantees (NOGG) on the one hand and their performance on the other. The performance in NOGG (reflecting their quality of management) is evaluated in reference to two dimensions: efficiency (measured by the number of guarantees granted, the value of guarantees and the multiplier ratio) and financial sustainability (measured by revenues, costs, and default ratio).

-

data on nonbanking organisations granting guarantees in Polish regions was collected for the period between 2013 and 2018 to assess their experience and performance in both dimensions;

panel regression models were created to verify the existence of relationships between the analysed phenomena.

The results contribute to filling the research gap with regards to the evaluation of the efficiency and financial sustainability of NOGG. The findings indicate a positive relation between the level of regional development as measured by the Subnational Human Development Index (SHDI), costs and the revenues of NOGG. The research results also highlight that experience of NOGG is positively related to the number of guarantees issued. However, the most important factor influencing the efficiency and financial stability of the organisations granting guarantees is the capital of these organisations. We posit that as far as cohesion policy is concerned the support of already existing organisations is recommended to benefit from their experience, although support for the creation of new support institutions in lagging regions must not be overlooked. It is the public authorities’ responsibility to facilitate cooperation between organisations granting guarantees from different regions (i.e. in the form of consortia) to assist the transfers of knowledge between them.

The paper consists of five sections. Following the introduction, section 2 reviews literature on organisations granting guarantees covering their typology, highlighting some of the differences in the way in which the guarantee distribution channels are organised in various countries. It also introduces former research results and concludes with hypotheses development. Section 3 presents data and methodology, including variables, descriptive analysis and econometric strategy. The results of panel regression analysis aiming to find the relationship between the level of regional development as well as organisation granting guarantees experience and the efficiency of the organisations granting guarantees functioning in Poland are described and discussed in section 4. Finally, we provide a summary covering the key findings, limitations and new research trajectories in section 5.

The research is financed by the National Science Centre in Poland and is part of a project entitled “Financing the development of loan and guarantee funds” – grant number 2016/23/B/HS4/00348.

2. Literature review and hypothesis development

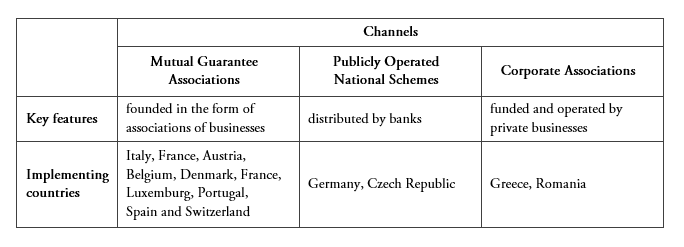

Beck et al. (2010) observed a significant variation in organisational features of credit guarantee schemes across and within countries on the global scale. They distinguished three main types of guarantee distribution channels following the criteria of their structure and ownership presented and described in Table 1.

Guarantee distribution channels classification by Beck, Klapper & Mendoza

Source: Prepared by the authors based on Beck, et al. (2010).

The guarantees in Poland are distributed either within Publicly Operated National Schemes or through Corporate Associations. However, there exists a major specificity insofar as the latter group is concerned – although some organisations granting guarantees operating in Poland are set up and run by business entities, there is also a significant group of Non-Governmental Organisations granting guarantees. This paper concentrates solely on the Corporate Association type of guarantee distribution (both business entities and non-governmental organisations).

According to the recent EC report (European Commission, 2018) the cohesion funds for guarantees within the 2014-2020 Financial Framework are allocated through Publicly Operated National Schemes and then distributed directly by banks. The situation is different in three countries: Italy, Malta and Poland, where chosen intermediaries manage the funds and grant guarantees (nonbanking organisations granting guarantees – NOGG).

Most organisations granting guarantees in Poland were created in the 1990s from the funds of financial support programs for SMEs as financially, but not organisationally, separate entities. These entities were initially run by foundations or public sector entities. Gradually they transformed into separate legal entities: foundations, associations, chambers of commerce and limited liability companies that do not operate for profit. According to the data of the National Association of Guarantee Funds, 44 nonbanking organisations granting guarantees were operating in Poland at the end of 2018. The total capitalisation of NOGG in 2018 was PLN 1.07 billion (about EUR 250 million). Some NOGG functioned within the National System of Services for Small and Medium-sized Enterprises, the mission of which is to support the development and promotion of entrepreneurship. These organisations offered consultancy for companies in the areas of innovation, environmental protection, financial management, energy management, the use of information technology, marketing and sales as well as credit guarantees. Until 2007, NOGG were mainly financed by money from the EU SOP ICE programme (Sectoral Operational Programme Improvement of the Competitiveness of Enterprises). In 2007, the task of financing the development of this type of financial tool was transferred to the local government level. Each region in Poland created its programmes for financing institutions or tools focusing on the development of entrepreneurship. In some regions, a few new NOGG were created (every guarantee organisation was created by a different founder and from different financial support programme) offering the services to the same recipients. In the researched period, some of them operated locally, regionally or nationally. NOGG in Poland typically aided SMEs functioning in the region preferred by them (usually the region where the NOGG are based).

NOGG which are subject to analysis are most frequently financed in their operations using public funding from the European Union (i.e. Cohesion Fund) and central, regional or local governments. At the same time, some of them use private sources of funding. The EU cohesion policy provided – within the 2007-2013 Financial Framework – support to final recipients in all Member States in the amount of EUR 4 billion. Guarantees were the second most important financial instrument after loans. Under the 2014-2020 Financial Framework, from which funds can be disbursed until the end of 2022, at the end of 2018, the value of operating programmes contribution to guarantees was EUR 1 billion (European Commission, 2018). The European Commission emphasised that during the 2021-2027 perspective grants should be efficiently complemented by financial instruments, which have a leverage effect and are closer to the market. In the new financial framework Member States will be able to transfer a part of their Cohesion Policy resources to the new, centrally managed InvestEU fund, to access co-guarantees provided by the EU budget.

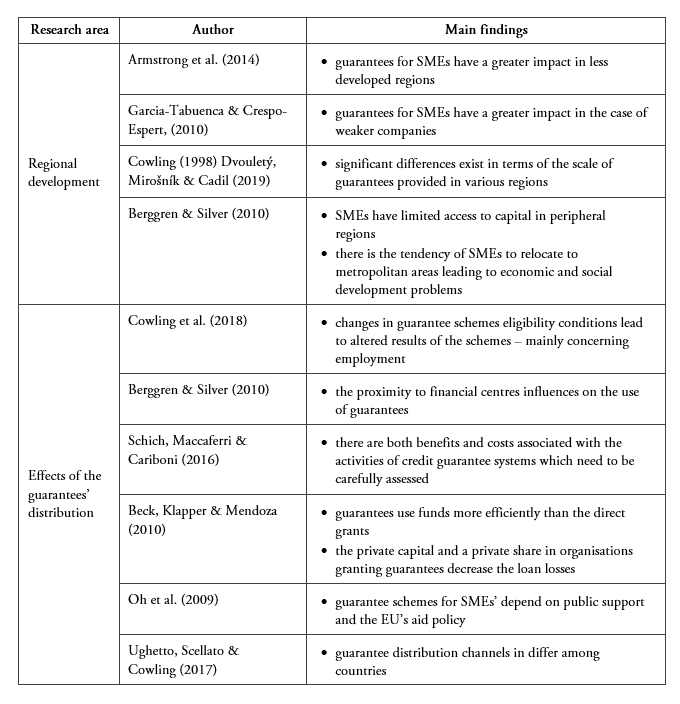

Analysing the business models of organisations granting guarantees in Poland the same generic types (direct and indirect relation of the borrower and the guarantor) may be identified with regards to how the guarantees are provided to beneficiaries as in other countries (Riding, Madill & Haines, 2007). The process of guarantee application differs: a borrower can apply for a guarantee in a bank (indirect relation) or in an institution that provides a guarantee (direct relation). In our research, we included all nonbanking organisations granting guarantees irrespective of their sources of financing or adopted business models. Below, in Table 2, we present a review of research results of guarantee schemes within the context of their performance and regional development.

NOGG provide guarantees for banks taking into account the risk of insolvency of the company requesting the loan (Sanneris, 2015). As NOGG help the entrepreneur to complete the formalities associated with obtaining the credit, organise additional trainings, and also take the responsibility of monitoring the borrower, the cost of the loan can be lower than in other conditions (Garcia-Tabuenca & Crespo-Espert, 2010; Zecchini & Ventura, 2009). However, the growing importance of tender guarantees, export guarantees and contract enforcement guarantees is observed in some countries (Waniak-Michalak et al., 2020).

Some authors emphasise that guarantees as financial instruments bring several benefits to economic development. The guarantees, provided mostly within schemes financed by public funds, enable the value of small business loans to be increased by up to 100% (Cowling et al., 2018). Bradshaw (2002) argues that the consequences of the support may include an increase in the number of employees and the decrease in the SME’s default rate. Moreover, the guarantee schemes can enhance SMEs financial position and increase the value of their assets (D’Ignazio & Menon, 2013). However, if companies using guarantees are on the brink of bankruptcy and the loans are necessary simply for survival on the market, the loan will not allow further investment or enhancement. In this way, the cost of the support may outweigh the benefits (Schich et al., 2016).

As the money invested in guarantee schemes is the basis for multiple loans – a relatively small capital used for offering guarantees allows support of credit applications for much higher amounts – the guarantee schemes have a significant advantage over other forms of support. It boils down to the fact that they offer much higher multiplier effects – relative to the funds involved in them – than in case of other forms of support and allows for involving also private capital on a much broader scale, leading to the effects of additionality (Beck et al., 2010).

Research results on the activity of organisations granting guarantees

Source: Prepared by the authors.

Most previous studies on the guarantee fund functioning concentrated on analysing the impact of guarantees on companies, predominantly on SMEs – Cowling (1998), Berggren & Silver (2010), Schich, Maccaferri & Cariboni (2016), Dvouletý, Mirošník & Cadil (2019). There is, however, a considerable research gap with regards to the factors which influence the organisations granting guarantees or schemes and their performance (in financial efficiency and financial sustainability dimensions). Our study aims to fill this gap.

The study conducted by Armstrong et al. (2014), shows that major government intervention in the small firm credit market yields significantly better results in markets (regions) that are less financially developed. We intend to verify whether this observation holds for the organisations granting guarantees performance. Hence, we set the following hypothesis: (1) there exists a negative relationship between the level of regional development and performance of nonbanking organisations granting guarantees in Poland.

Zhou et al. (2015) found a positive association between organisational learning dimensions and firm performance. Sivill et al. (2013) also stress that that organisational performance improves with experience. Therefore, we formulated the second hypothesis: (2) there exists a positive relationship between organisational experience and performance of nonbanking organisations granting guarantees in Poland.

3. Data and methodology

In our study, we gathered the data on nonbanking organisations granting guarantees (NOGG) for SMEs in Polish regions for the period between 2013 and 2018 (e.g. all the organisations that submitted their financial statements to the National Registry in Poland for those years) to assess their experience and performance. The data was provided by the Polish Association of Guarantee Funds.

Performance is a broad and multifaceted concept (Kaplan & Norton, 1996; Richard et al., 2009). Traditionally performance of financial institutions is perceived through the lens of the return from invested capital and risk associated with the lending policy (Froot & Stein, 1998). In the case of NOGG, which are analysed in the article, the criteria for performance assessment need to go beyond the return and risk in order to better reflect the types and objectives of these organisations.

The first consideration that needs to be taken into account is that the organisations granting guarantees and loans in Poland are mostly not-for-profit entities. What is more, they operate using differing combinations of private and public financing. In that respect, the performance of these institutions should be evaluated mainly in two dimensions: efficiency and financial sustainability.

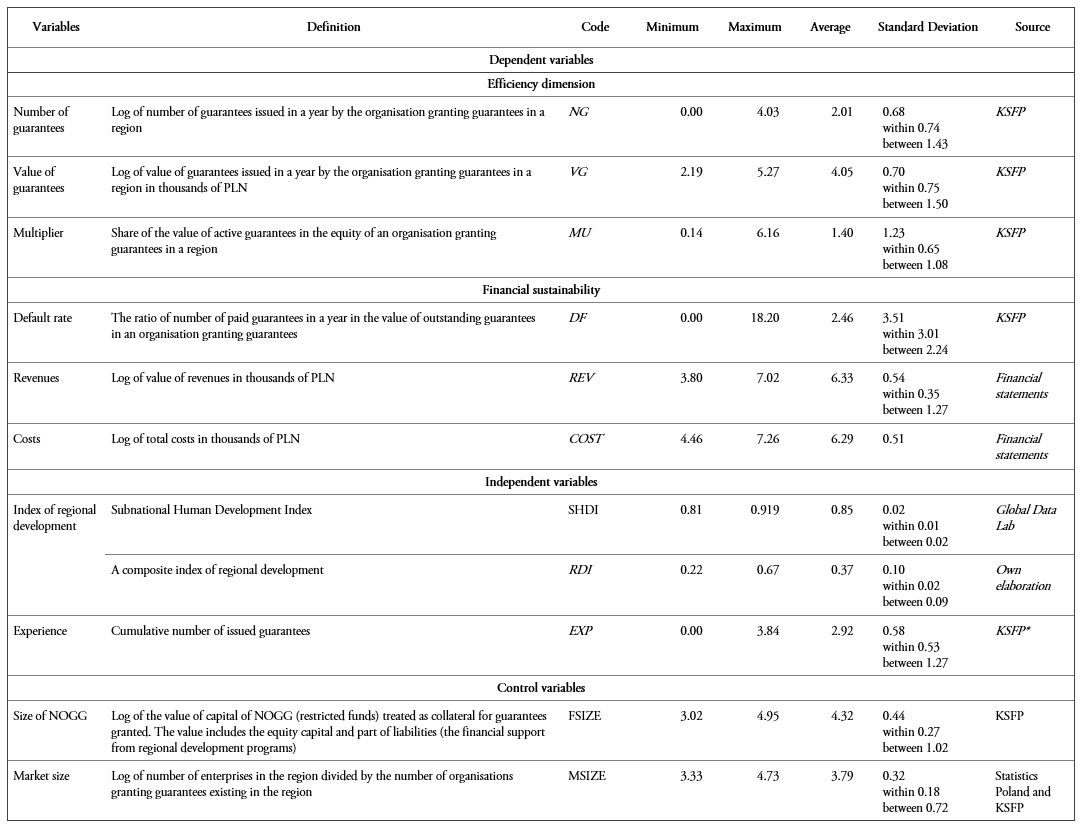

In the efficiency dimension of performance, NOGG are expected to contribute towards public policy objectives achievement (European Commission, 2006) taking into consideration cost, organisation and process relative to the output and the price of the service. This translates into an ability of the organisation granting guarantees or scheme to meet the demand. The measurement of NOGG’s efficiency was prepared using the following measures: the number of guarantees granted (NG), the value of guarantees (VG) and the share of the value of active guarantees in the equity – the equity multiplier (MU).

Financial sustainability dimension of the performance of NOGG stems from the idea of their self-financing. Financial sustainability is negatively affected by the wrongly granted guarantees, lack of money needed to grant new guarantees, inability to cover the costs of functioning. This translates into the capacity of the organisations to cover their expenses with revenues and their liquidity. The assessment was done using the following measures: revenues (REV) and costs (COST). We also used the default rate (DF) as the measure of financial sustainability. We posit that the value of lost guarantees (paid guarantees) influence significantly financial stabilisation of NOGG.

The diversity of theoretical approaches to the concept of regional development means that there exist numerous ways of measuring the development of territories. The discourse on the notion of regional development recognises the need for flexibility and adapting one's approach to defining development and identifying its core determinants depending on the specificity of a given territory – its history, geography, developmental aspirations and strategies, existing institutions and available resources. There exists no universal approach to managing development which would suit every municipality or region independently of its overall context (Pike, Rodrigues-Pose & Tomaney, 2014). Rural development is but one example of possible ambiguities in terms of meaning which a change of context may introduce (Torre & Wallet, 2015). One of the most widely used regional development measures is HDI.

We used the Subnational Human Development Index (SHDI) as the measure of regional development. The SHDI is the geometric mean of the subnational values of three dimensions: education, health and standard of living. The indicators in the SHDI Database are scaled in such a way that their population weighted averages equal their national values in the official UNDP-HDI database.

List of variables

* KSFP= National Association of Guarantee Funds (Krajowe Stowarzyszenie Funduszy Poręczeniowych).

Source: Prepared by the authors.Experience is one of the key determinants of the performance of organisations granting guarantees. The experience results from the company's activities. Research on the learning curve indicates that performance improves with experience (Sivill et al., 2013). Experience can be measured in terms of the cumulative number of tasks carried out (Argote & Miron-Spektor, 2011). We note that one of the criteria used in tenders for selecting financial intermediaries in regional development programmes is the number of instruments granted in previous years. For the purposes of our study, we, therefore, used the cumulative number of guarantees as the measure of the experience of NOGG.

As control variables, we include the organisation’s size (measured by a Log of capital of organisations granting guarantees) and market size (measured by Log of the relation of number of enterprises in the region and the number of NOGG existing in the region). The capital of NOGG (that serves as collateral for the guarantees provided) affects both the value and number of guarantees and can be treated as the measure of the size of these organisations. Thus, NOGG with smaller capital resources may perform worse than other organisations, despite operating in the same region. At the same time, the number of enterprises (potential clients) per the nonbanking organisation granting guarantees in the region may influence the number and value of the guarantees provided, and thus also other stability and efficiency indicators (such as revenues, costs). We name the measure the market size. Table 3 outlines the description of variables.

The descriptive analysis of used variables leads to a conclusion that NOGG in Poland reached a low level of losses (default rate) – below 3% – between 2013 and 2018. It means that for the majority of borrowers, the difficulties in obtaining financing without additional collateral resulted from an overly prudent risk assessment by banks1. We have also found a high variation in the number and value of guarantees granted. Despite the average level of few thousands of guarantees, their number in case of leading organisations granting guarantees reached 11 thousand (in 2018). Such differentiation in the number and value of guarantees granted between 2018 and other years result from the fact that disbursement of funds from the 2014-2020 financial perspective only started towards the end of 2017 due to the delays related to the preparation of Regional Operating Programmes. Previously, the organisations granting guarantees used the capital raised from fees from entrepreneurs and funding within the 2007-2013 Financial Framework. Moreover, the implementation of programmes co-financed from the EU funds made it possible to adapt preferential conditions for entrepreneurs (e.g. reducing commissions for granting guarantees) that may have affected the demand for financial instruments. Moreover, greater availability of grants for entrepreneurs leads to an increased demand for additional financing (own contributions) and thus collaterals (like guarantees).

Analysing the efficiency measures it may be observed that the number of issued guarantees (NG) and value of guarantees (VG) are related to the capital of organisations granting guarantees while showing no noticeable relation to the regional development level. It is the basic collateral for the instruments granted and on this basis, banks decide to accept the collateral which is the guarantee of the organisation granting guarantees.

4. Econometrics strategy

We conducted a panel regression analysis for financial and non-financial data on organisations granting guarantees and regional development indices. The sample covered 26 nonbanking organisations granting guarantees. Data for a six-year period was collected leading to a total of 156 observations. With this in mind we formed the separate models (regressions) for seven various performance measures used as depended variables, in the general following form:

[1]

[1]Here,

Yit is the depended variable of NOGGs’ performance; SHDI, EXP are independent variables; MSIZE, FSIZE are control variables; dti-time effect; βi are coefficients; 𝜀it is error.

We changed the general form of equation only for equity multiplier. In this equation, we excluded MSIZE as the control variable, as it was strongly correlated with equity multiplier (which is calculated as the value of guarantees divided by the capital).

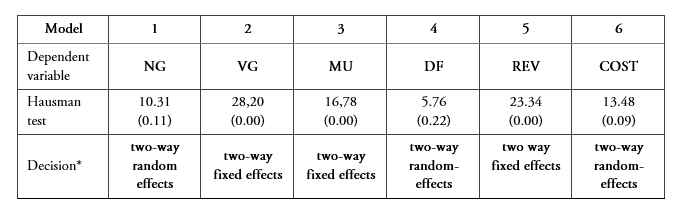

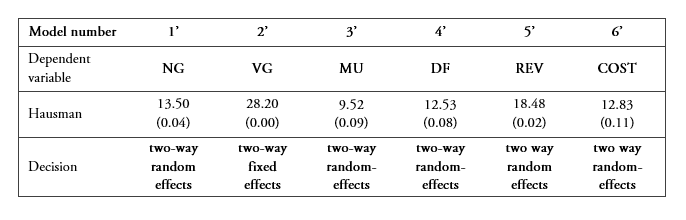

At the first stage, we used Hausman test to distinguish between fixed effects and random effects specifications (Arellano 2003, pp. 11-13). When the null hypothesis was true, we chose random effect specification as more efficient GLS estimator. We included in every model time effects in order to control for global aspects associated to the business cycle. The results of the above analysis are presented in table 4.

Hausman test statistics for models with independent variable SHDI

p values in parentheses

*99% confidence level was assumed

Source: Prepared by the authors.Additionally, we decided to construct an alternative measure of regional development and use it to test our hypotheses. In an attempt to measure regional development levels, some authors emphasise technological progress (defined as knowledge development, accumulation and diffusion) and the regions’ ability to develop new technologies and/or to assimilate the existing ones (de Groot, Nijkamp & Acs, 2001; de Dominicis, Florax & de Groot, 2013), the geographical mobility of investors (Miguelez et al., 2010), knowledge transfer mechanisms and knowledge transfer agents (Simonen & McCann, 2010), universities and commercialisation of university research (Bergman, 2010), migrations and their impact on labour markets (Rodriguez-Pose & Tselios, 2010). Others point out human capital, knowledge and creativity (Nijkampet al., 2010) or knowledge infrastructure, human capital, talent, knowledge generation, protection and accumulation (Karlsson & Johansson, 2012), leading to the overarching concept of territorial capital, as defined by Camagni & Capello (2013).

The approach to measuring the level of regional development which is assumed in this paper uses a selection of approaches mentioned above. Three dimensions of development have been identified: socio-economic, spatial (relating to transport infrastructure and the natural environment) as well as institutional.

We created a simple composite measure of territorial units’ development levels, one which could be easily adjusted to the availability of data sets and provide flexibility in extending the analysis also to lower levels of territorial division (districts, municipalities) if need be. Following an overview of available indicators and the correlations between them (to avoid redundancy), we decided to use six indicators. Three indicators are chosen to reflect the socio-economic dimension of development and one indicator each for infrastructural, environmental and institutional dimensions.

Data on the following indicators for all 16 Polish regions were collected for the period between 2013 and 20182:

-

Socio-economic:

-

value of fixed assets per capita in a region (a stimulant);

-

registered unemployment rate (a destimulant);

-

average monthly disposable income per capita (a stimulant);

-

-

Infrastructural:

-

expressways and highways per 1,000 square kilometres (a stimulant);

-

-

Environmental:

-

share of protected areas in a total area of the region (a stimulant);

-

-

Institutional:

-

the number of public benefit organisations per 1,000 inhabitants (a stimulant).

-

To combine these indicators into a single measure of regions’ development levels three approaches were considered: the taxonomic development standard method, the standardised sums method and the unitarised sums method. The results presented below are based on the taxonomic development standard method which was calculated in a four-step process.

Step 1. The variables were standardised:

[2]

[2]for stimulants of development and

[3]

[3]for destimulants of development, where:

-

xij – represents the initial value of the diagnostic variable for the ith region and the jth partial indicator of development;

zij – represents the standardised value of the diagnostic variable for the ith region and the jth partial indicator of development;

σj – represents the standard deviation for the jth partial indicator of development;

Step 2. The development standard (4) ( ) and the development anti-standard ( ) are set.

Step 3. The Euclidean distance of each region from the set development standard ( ) is determined:

[5]

[5]Step 4. The regional Development Index (RDI) is determined as:

(6) , where is the Euclidean distance between the development standard ( ) and the development anti-standard ( ).

The RDI was developed specifically for this paper and may be flexibly scaled down and applied to territorial units at different levels of administrative division (regional, district, municipal), a feature which is not available when using a well-established development index such as the Subnational Human Development Index (SHDI).

5. Results and discussion

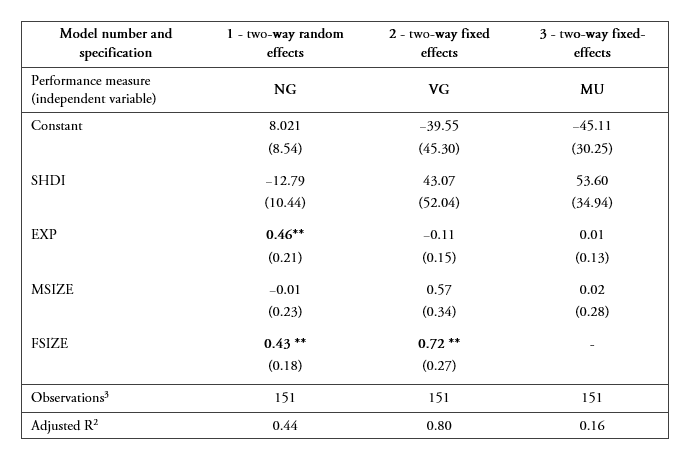

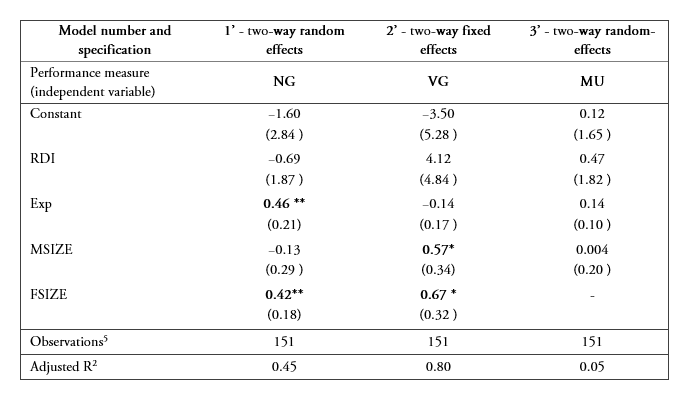

The outcomes of the panel data regression analysis specifications are presented in Table 5 and Table 6. Table 5 shows the results of three models in the efficiency dimension. The study does not confirm the existence of the relation between performance (efficiency dimension) and the level of regional development. It is an unexpected result. We decided to check it using measure of regional development developed by us (RDI).

Panel regression analysis in efficiency dimension (robust HAC errors)

Robust standard errors in parentheses

*** p<0.01. ** p<0.05. * p<0.1

Source: Prepared by the authors.

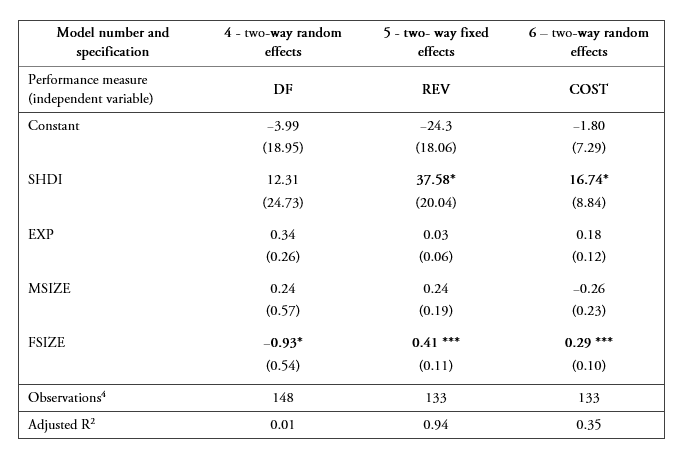

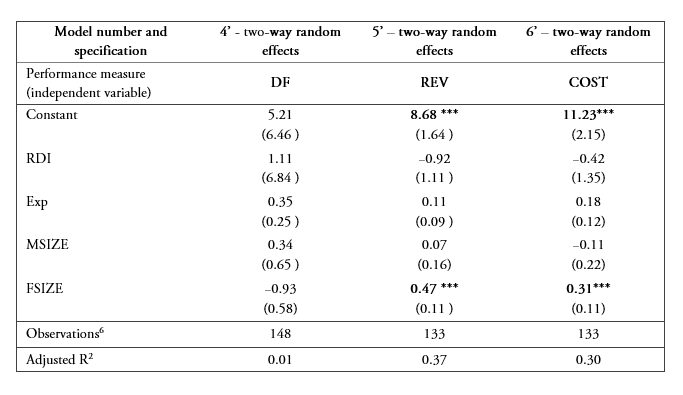

Panel regression analysis in financial sustainability dimension (robust HAC errors)

Robust standard errors in parentheses

*** p<0.01. ** p<0.05. * p<0.1

1model with fixed effects

Source: Prepared by the authors.There is a positive association between the size of organisation granting guarantees and both the number of guarantees as well as the value of guarantees. It leads us to the conclusion that in order to conduct efficient cohesion policy with the use of guarantees big and experienced NOGG should be preferred. None of the dependent and control variables proved to be statistically significant in the case of equity multiplier.

Table 6 shows the results of three models in the financial stability dimension. We found that only revenues (REV) and costs (COST) show a statistically significant positive relation with the level of regional development (measured by SHDI). The possible explanation is that in more developed regions NOGG grant more tender guarantees or export and contract performance guarantees which influences positively revenues of these organisations. As the previous research proved, in 2018, the NOGG in Poland most often guaranteed leasing, commercial and tender liabilities. They accounted for 70% of the number of all guarantees in 2018 (Waniak-Michalak et al., 2020). Guarantees granted within regional development programs usually do not bring additional revenues to NOGG, because fees for this kind of guarantees are very low or non-existent. However, they are able to generate more revenues from consulting and advisory operations. At the same time, the operating costs of guarantee organizations may be higher in more developed regions due to higher administrative costs (employee salaries).

We observe a positive relation between the organisation’s size (FSIZE), revenues and costs (COST). The possible explanation is that size and scale of operations of more experienced organisations require higher expenses and provide higher revenues.

The higher rate of guarantees paid out in small funds results from low diversification of the guarantee portfolio. Such funds may provide fewer guarantees and thus expose themselves to greater risk of unpaid loans.

Summarising, we did not confirm the first hypothesis that (1) there exists a negative relationship between the level of regional development and performance of organisations granting guarantees in Poland. In contrast, in case of two performance measures – revenues and costs we found their positive relation with regional development.

We confirm the hypothesis that (2) there exists a positive relationship between organisational experience and performance of organisations granting guarantees in Poland in case of one financial performance measure – number of guarantees.

We come to conclusions as Beck, Klapper & Mendoza (2010) formulated that the most important factor influencing financial is the experience and size of NOGG. Having successfully operated, more experienced NOGG are more likely to secure government funding as they have greater expertise at handling complex governmental procedures. Such additional financing may also help to improve the indicators such as number of guarantees.

In case of control variables, the variable that proved to be statistically significant is the size of NOGG.

As a robustness check for our results we use another measure – RDI to form similar regression models:

[7]

[7]Here,

Yit is the depended variable of NOGGs’ performance; RDI, EXP are independent variables; MSIZE, FSIZE are control variables; dti - time effect; βi are coefficients; 𝜀it is error.

Hausman statistics are presented in the table 7. The results of panel regression prepared as robustness checks are presented in Table 8 and Table 9.

Hausman test statistics for models with RDI as independent variable

p values in parentheses

*99% confidence level was assumed

Source: Prepared by the authors.In the efficiency dimension the replacement of SHDI with RDI did not change the results. We observed only lack of significance of size of NOGG for DF, however the sign of the coefficient stays the same. The results presented in Tables 8-9 show the robustness of our models.

Panel regression analysis in efficiency dimension (robust HAC errors)

Robust standard errors in parentheses

*** p<0.01. ** p<0.05. * p<0.1

Source: Prepared by the authors.

Panel regression analysis in financial sustainability dimension (robust HAC errors)

Robust standard errors in parentheses

*** p<0.01. ** p<0.05. * p<0.1

Source: Prepared by the authors.6. Conclusions

The results that the paper presents contribute to the research on the functioning of cohesion policy instruments, the importance of which is deemed to increase in the aftermath of the coronavirus pandemic. We focused our attention on guarantees as one of many available cohesion policy instruments. Guarantees have the advantage over other SME support forms within cohesion policy in that, they create a very high multiplier effect and are very effective in closing the equity gap. Specifically, the paper discusses the issue of relations between the level of regional development as well as the experience and the performance of non-banking organisations granting guarantees (NOGG) as reflected by their financial efficiency and financial sustainability.

The research was conducted for the NOGG which were active in Poland between 2013 and 2018. The choice of Poland is justified by the fact that it is characterised by a high share of small and medium enterprises in the total number of firms, in employment as well as in value-added creation in comparison with other OECD countries (OECD, 2018). What is more, the SMEs in Poland face significant challenges in terms of access to capital due to historical determinants resulting in a shorter period of capital accumulation and inferior level of development of financial sector institutions in comparison with Western European countries. Finally, there exists a unique system for supporting small and medium-sized enterprises created in Poland – it is based on organisations which provide support for entrepreneurs from specified regions and which remain independent of the government even though they use public funds.

The organisation of guarantee funds distribution in Poland leads to several advantages which may be considered for implementation also in other EU countries. First of all, the regional nature of most NOGG allows them to adjust their offer to the regional specificity and requirements of business organisations based in the same region. Secondly, the fact that these organisations granting guarantees operate as NGOs increases the probability that the resources which are involved therein will be used entirely for achieving regional development objectives in line with the cohesion policy requirements, as profit maximisation is not their ultimate goal.

Given the specificity of guarantee distribution channels used in Poland, the dimensions of financial efficiency and financial sustainability of these organisations appear as even more important and relevant, hence becoming the main subject of analyses and insights presented in this paper. It is, however, a markedly different situation from these in most EU countries. It highlights a new trajectory for further research on efficiency and sustainability of other forms of guarantee distribution channels.

Our research results indicate interregional differences in terms of financial efficiency and financial sustainability of NOGG which were changing over time. The results confirm that there exists a positive relationship between the level of regional development and the financial sustainability measures of NOGG– revenues and costs. The possible explanation is that in more developed regions grant more tender guarantees or export and contract performance guarantees which influences positively revenues of these organisations. Moreover, size and scale of operations of more experienced organisations require higher expenses and provide higher revenues.

The research results also highlight the importance of the experience of NOGG for selected measures of financial efficiency and financial sustainability – positive relationships were noted between the experience of NOGG and number of guarantees. The results confirm the expectation expressed in the second hypothesis that greater experience (related with a better reputation and higher expertise) at handling complex governmental procedures as well as accompanying economies of scale in case of older support institutions lead to more efficient usage of support funding.

Insofar as the cohesion policy is concerned the main recommendation stemming from our results is that the policy of supporting SMEs should concentrate on existing NOGG which should be nurtured and supported to maximise the benefits of their experience. In case of lagging regions where no well-established NOGG operate, they need to be set up, even though the creation of new NOGG bears the risk of reducing the efficiency of the entire system of support for SMEs, at least in the short-term perspective as less experienced NOGG are characterised by lower financial efficiency and financial sustainability. In such a scenario the public authorities need to take responsibility for creating a framework for cooperation between NOGG from different regions (i.e. in the form of consortia) to facilitate the transfers of knowledge.

Our analysis shows that evaluators of EU intervention should not compare the results of guarantee schemes in different countries and regions without consideration of other factors, as the regional development or the experience of the network or institutions providing the support for SMEs. Comparing organisations granting guarantees operating in different countries directly may lead to misinterpretations and ultimately to incorrect conclusions and recommendations. We find also the size of NOGG measured by its capital as the most important factor influencing their performance. We posit, that a prerequisite for the high performance of the NOGG is to ensure that they have an adequate level of guarantee capital. Without this, it is not possible to achieve a high capital multiplier and leverage effect (a relation of the private resources involved in the support provided).

The article also has some limitations that need to be addressed. First of all, the article concentrates on one instrument of cohesion policy only, whereas its implementation needs to integrate a much broader spectrum of instruments (i.e. loans and grants). Further research on other cohesion policy instruments is required. Another limitation of our research lies in the fact that other determinants, then we considered in our study, may affect financial efficiency and sustainability of NOGG. Other determinants which may be examined in future research embrace: top manager characteristics including their experience, age and education (cf.Flanigan et al. 2017), a number of existing partnerships with banks and other institutions. public authorities (cf. Waniak-Michalak 2017) or measures of spatial and social proximity (cf.Capello & Caragliu 2018). The third limitation which ought to be mentioned relates to the fact that the paper is based on an analysis of NOGG functioning in one country. Inclusion of a broader representation of EU countries with their specificity of guarantee distribution channels in future research will allow for a deeper understanding of their performance.

References

Arellano, M. (2003). Panel data econometrics. Oxford University Press.

Argote, L., & Miron-Spector, E. (2011). Organizational Learning: From Experience to Knowledge. Organization Science, 22(5), 1123-1137. https://doi.org/10.1287/orsc.1100.0621

Armstrong, C., Craig, B., Jackson, W. E., & Thomson, J. B. (2014). The Moderating Influence of Financial Market Development on the Relationship between Loan Guarantees for SMEs and Local Market Employment Rates. Journal of Small Business Management, 52(1), 126-140. https://doi.org/10.1111/jsbm.12036

Baltagi, B. (2013). Econometric analysis of panel data. John Wiley & Sons.

Beck, T., Klapper, L. F., & Mendoza, J. C. (2010). The typology of partial credit guarantees funds around the world. Journal of Financial Stability, 6(4), 10–25. https://doi.org/10.1016/j.jfs.2008.12.003

Berggren, B., & Silver, L. (2010). Financing entrepreneurship in different regions: The failure to decentralise financing to regional centres in Sweden. Journal of Small Business and Enterprise Development, 17(2), 230-246. https://doi.org/10.1108/14626001011041238

Bergman, E. (2010). Knowledge links between European universities and firms: a review. Papers in Regional Science, 89(2), 311-333. https://doi.org/10.1111/j.1435-5957.2010.00310.x

Bradshaw, T. K. (2002). The contribution of small business loan guarantees to economic development. Economic Development Quarterly, 16(4), 360-369. https://doi.org/10.1177/089124202237199

Brasili, C., Calia, P., & Monasterolo, I. (2020). Profiling identification with Europe and the EU project in the European regions. Investigaciones Regionales - Journal of Regional Research, 46(1), 71-91.

Camagni, R., & Capello, R. (2013). Regional competitiveness and territorial capital: a conceptual approach and empirical evidence from the European Union. Regional Studies, 47(9), 1383-1402. https://doi.org/10.1080/00343404.2012.681640

Capello, R., & Caragliu, A. (2018). Proximities and the intensity of scientific relations: synergies and nonlinearities. International Regional Science Review, 41(1), 7-44. https://doi.org/10.1177%2F0160017615626985

Charron, N., & Bauhr, M. (2020). Do Citizens Support EU Cohesion Policy? Measuring European support for redistribution within the EU and its correlates. Investigaciones Regionales - Journal of Regional Research, 46(1), 11-26.

Cowling, M., Robson, P., Stone, I., & Allinson, G. (2018). Loan guarantee schemes in the UK: the natural experiment of the enterprise finance guarantee and the 5 year rule. Applied Economics, 50(20), 2210-2218. https://doi.org/10.1080/00036846.2017.1392004

d’Ignazio, A., & Menon, C. (2013). The Causal Effect of Credit Guarantees for SMEs: Evidence from Italy. Bank of Italy Temi di Discussione (Working Paper), 900, 1-42. https://doi.org/10.2139/ssrn.2259586

de Groot, H., Nijkamp, P., & Acs, Z. (2001). Knowledge spill-overs. innovation and regional development. Papers in Regional Science, 80, 249-253.

De Dominicis, L., Florax, R. J., & de Groot, H. L. (2013). Regional clusters of innovative activity in Europe: are social capital and geographical proximity key determinants?. Applied Economics, 45(17), 2325-2335. https://doi.org/10.1080/00036846.2012.663474

Dvouletý, O., Mirošník, K., & Cadil, J. (2019). Do Firms Supported by Credit Guarantee Schemes Report Better Financial Results 2 Years After the End of Intervention? The BE Journal of Economic Analysis & Policy, 10(1), 1-20. https://doi.org/0.1515/bejeap-2018-0057

EBI & EBCI Vienna Initiative (2014). Credit Guarantee Schemes for SME lending in Central. Eastern and South-Eastern Europe. http://www.eib.org/infocentre/publications/all/viwg-credit-guarantee-schemes-report.htm

European Commission (2006). Guarantees and mutual guarantees. Best Report. http://ec.europa.eu/DocsRoom/documents/3343/attachments/1/translations/en/renditions/pdf

European Commission (2018). Financial Instruments under the European Structural and Investment Funds. https://ec.europa.eu/regional_policy/sources/thefunds/fin_inst/pdf/summary_data_fi_1420_2018.pdf

Flanigan, R., Bishop, J., Brachle, B., & Winn, B. (2017). Leadership and Small Firm Financial Performance: The Moderating Effects of Demographic Characteristics. Creighton Journal of Interdisciplinary Leadership, 3(1), 2-19. http://dx.doi.org/10.17062/CJIL.v3i1.54

Froot, K. A., & Stein, J. C. (1998). Risk Management, Capital Budgeting, and Capital Structure Policy for Financial Institutions: An Integrated Approach. Journal of Financial Economics, 47(1), 55–82.

Garcia-Tabuenca, A., & Crespo-Espert, J. J. (2010). Credit guarantees and SME efficiency. Small Business Economics, 35, 113-128. https://doi.org/10.1007/s11187-008-9148-4

Gagliardi, L., & Percoco, M. (2017). The impact of European CP in urban and rural regions. Regional Studies, 51(6), 857-868. https://doi.org/10.1080/00343404.2016.1179384

Griffith-Jones, S., & Fuzzo de Lima, A. T. (2004). Alternative Loan Guarantee Mechanisms and Project Finance for Infrastructure in Developing Countries. University of Sussex.

Hooghe, L., & Marks, G. (2019). Grand theories of European integration in the twenty-first century. Journal of European Public Policy, 26(8), 1113-1133. https://doi.org/10.1080/13501763.2019.1569711

Iatu, C., & Alupului, C. (2011). SF absorption in Romania: Factor analysis of NUTS 3 level. Transformations in Business & Economies, 11, 612-630.

Kaplan, R. S., & Norton, D. P. (1996). The Balanced Scorecard: Translating Strategy into Action. Harvard Business Press.

Karlsson, C., & Johansson, B. (2012). Knowledge. Creativity and Regional Development. In C. Karlsson, B. Johansson & R. R. Stough (Eds.), The Regional Economics of Knowledge and Talent. Edward Elgar Publishing.

Klagge, B., & Martin, R. (2005). Decentralised versus centralised financial systems: is there a case for local capital markets?. Journal of Economic Geography, 5(4), 387-421.

Lee, N., & Brown, R. (2016). Innovation. SMEs and the liability of distance: the demand and supply of bank funding in UK peripheral regions. Journal of Economic Geography, 17(1), 233-260. https://doi.org/10.1093/jeg/lbw011

Martin, R., Berndt, C., Klagge, B., & Sunley, P. (2005). Spatial proximity effects and regional equity gaps in the venture capital market: evidence from Germany and the United Kingdom. Environment and Planning, 37(7), 1207-1231.

Mendez, C., Bachtler, J., & McMaster, I. (2019). The Agenda for Cohesion Policy in 2019-2024: Key Issues for the REGI Committee. European Parliament.

Miguelez, E., Moreno, R., & Surinach, J. (2010). Investors on the move: tracing investors’ mobility and its spatial distribution. Papers in Regional Science, 89(2), 251-274.

Moreno, R. (2020). EU cohesion policy performance: regional variation in the effectiveness of the management of the structural funds. Investigaciones Regionales - Journal of Regional Research,46(1), 27-50.

Nijkamp, P., Stimson, R., & van Hemert, P. (2010). Human capital as knowledge resource for regional development. Journal of Economic and Social Geography, 101(5), 491-493. https://doi.org/10.1111/j.1467-9663.2010.00635.x

Oh, I., Lee, J-D., Heshmati, A., & Choi, G-G. (2009). Evaluation of credit guarantee policy using propensity score matching. Small Business Economics, 33, 335-351. https://doi.org/10.1007/s11187-008-9102-5

OECD (2018). Entrepreneurship at a Glance Highlights 2018. OECD Publishing.

Pelkmans, J. (2006). European Integration. Methods and Economic Analysis. Financial Times Prentice Hall.

Perucca, G. (2020). When Country Matters More than Europe: What Implications for the Future of the EU?. Investigaciones Regionales - Journal of Regional Research, 46 (1), 93-109.

Pike, A., Rodriguez-Pose, A., & Tomaney, J. (2014). Local and regional development in the Global North and South. Progress in Development Studies, 14(1), 21-30.

Richard, P. J., Devinney, T. M., Yip, G. S., & Johnson, G. (2009). Measuring Organizational Performance: Towards Methodological Best Practice. Journal of Management, 35(3), 718–804. https://doi.org/10.1177/0149206308330560

Riding, A., Madill, J., & Haines, G. (2007). Incrementality of SME Loan Guarantees. Small Business Economics, 29, 47-61. https://doi.org/10.1007/s11187-005-4411-4

Rodriguez-Pose, A., & Tselios, V. (2010). Returns to migration. education and externalities in the European Union. Papers in Regional Science, 89(2), 411-435. https://doi.org/10.1111/j.1435-5957.2010.00297.x

Royuela, V., & López-Bazo, E. (2020). Understanding the process of creation of European identity – the role of Cohesion Policy. Investigaciones Regionales - Journal of Regional Research, 46(1), 51-70.

Sanneris, G. (2015). Support of SME's in Italy: Case of Confidi. Experience and Perspectives of Evolution. St. Petersburg State Polytechnical University Journal. Economics, 228(5), 7-19. https://doi.org/10.5862/JE.228.1

Schich, S., Maccaferri, S., & Cariboni, J. (2016). Un moment opportun pour l’évaluation des coûts et bénéfices des garanties de crédit et la relance des politiques de soutien aux PME [A timely moment for assessing the costs and benefits of credit guarantees and relaunching SME support policies]. Revue d'économie financière.123, 279-296. https://doi.org/10.3917/ecofi.123.0279

Simonen, J., & McCann, P. (2010). Knowledge transfers and innovation: the role of labour markets and R&D cooperation between agents and institutions. Papers in Regional Science, 89(2), 295-309. https://doi.org/10.1111/j.1435-5957.2010.00299.x

Sivill, L., Manninen, J., Hippinen, I., & Ahtila, P. (2013). Success factors of energy management in energy‐intensive industries: Development priority of energy performance measurement. International Journal of Energy Research, 37, 936-951. https://doi.org/10.1002/er.2898

Torre, A., & Wallet, F. (2015). Towards new paths for regional and territorial development in rural areas. European Planning Studies, 23(4), 650-677. https://doi.org/10.1080/09654313.2014.945812

Ughetto, E., Scellato, G., & Cowling, M. (2017). Cost of capital and public loan guarantees to small firms. Small Business Economics, 49, 319-337. https://doi.org/10.1007/s11187-017-9845-y

Waniak-Michalak, H. (2016). Success factors of loan and guarantee funds supporting SMEs in Poland. Proceedings of ICEM 2016 Smart and Efficient Economy: Preparation for the Future Innovative Economy. https://ssrn.com/abstract=2942372

Waniak-Michalak, H., Michalak, J., & Turala, M. (2020). Loan and guarantee funds. Development. Performance. Stability. University of Lodz Press.

Waniak-Michalak, H., Michalak, J., & Gheribi, E. (2018). The Sources of Financing for SMES in Poland. Management and Education, XIV, 15-21.

Zecchini, S., & Ventura, M. (2009). The impact of public guarantees on credit to SMEs. Small Business Economics,32, 191–206. https://doi.org/10.1007/s11187-007-9077-7

Zhou, W., Hu, H. & Shi, X. (2015). Does organizational learning lead to higher firm performance? An investigation of Chinese listing companies. The Learning Organization, 22(5), 271-288. https://doi.org/10.1108/TLO-10-2012-0061

Glossary

NGOs: non-governmental organisations

NOGG: nonbanking organisations granting guarantees

SHDI: Subnational Human Development Index

EC: European Commission

SMEs: small and medium-sized enterprises

EU: European Union

Notes

Additional information

JEL Classification: G23; L31; L84; O16.

Corresponding author: maciej.turala@uni.lodz.pl

Acknowledgments: The research is financed by the National Science Centre in Poland and is part of a project entitled “Financing the development of loan and guarantee funds” – grant number 2016/23/B/HS4/00348.