Impact of accounting choice of dividends on the company’s value: Initial evidences

O impacto da escolha contábil dos dividendos no valor das empresas: Evidencias iniciais

Mariana Titoto Marques marianatitoto@gmail.com

Bruno José Canassa bjcanassa@fearp.usp.br

William Aparecido Maciel da Silva w.aparecidomaciel@hotmail.com

Jéssica de Morais Lima jesslima24@gmail.com

Fabiano Guasti Lima fgl@usp.br

Flávia Zóboli Dalmácio flaviazd@usp.br

Mariana Titoto Marques marianatitoto@gmail.com

Bruno José Canassa bjcanassa@fearp.usp.br

William Aparecido Maciel da Silva w.aparecidomaciel@hotmail.com

Jéssica de Morais Lima jesslima24@gmail.com

Fabiano Guasti Lima fgl@usp.br

Flávia Zóboli Dalmácio flaviazd@usp.br

Impact of accounting choice of dividends on the company’s value: Initial evidences

Enfoque: Reflexão Contábil, vol. 38, no. 2, pp. 01-13, 2019

Universidade Estadual de Maringá

This work is licensed under Creative Commons Attribution 3.0 International.

Received: 22 February 2018

Accepted: 05 April 2018

Abstract: The theme "value" always draws attention in discussions because its concept is linked to a high subjectivity. There are many models that try to get to an asset or a company’s value, which in addition to dealing with the subjectivity of the term, also must deal with several projections. The model of free cash flow is quoted in the literature. This method is affected by the variation of working capital which is the difference between assets and liabilities that is considered operational, calculated by Fleuriet’s Model, but to classify as operational is up to the evaluator/analyst. There are many choices for those who prepare the accounting reports too, what is called in the literature as the accounting choices. Example of the accounting choices is the treatment of interest, dividend and interest on shareholders' equity. Thus, if any account is classified as operational, this could impact the calculation of working capital and maybe, the value of a firm. This study analyzed whether there is an impact on the value, calculated by the discounted cash flow method, resulting from the accounting choice of dividends. Starting from the company's cash flow approach, which is affected by working capital, the sample was made by 80 companies in the Bovespa New Market between 2011 and 2015. Based on tests of mean and sign differences, the results confirmed what was expected: the dividend affects the free cash flow calculation and, moreover, should affect the company’s value.

Keywords: Accounting choices, Business valuation, Working capital.

Resumo: O tema “valor” sempre chama atenção para discussões porque seu conceito está atrelado a uma alta subjetividade (PEDRO, 2014). Existem muitos modelos que tentam fazer chegar ao valor de um ativo ou uma empresa, que além de lidar com a subjetividade do termo, também precisam lidar com diversas projeções. O estudo analisou se existe um impacto no valor, calculado pelo método do fluxo de caixa descontado, decorrente da escolha contábil do dividendo. Usou-se a abordagem do fluxo de caixa da empresa, à qual é sofre efeito do capital de giro. Não há um consenso se os dividendos (recebidos e pagos) compõem esse cálculo, bem como sua classificação na Demonstração do Fluxo de Caixa. A amostra foi de 80 empresas do Novo Mercado da B3 entre os anos de 2011 e 2015. A partir de testes de diferenças de médias e de sinais, os resultados confirmaram o que era previsto: o dividendo afeta significativamente no valor de uma empresa.

Palavras-chave: Escolhas contábeis, Avaliação de empresas, Capital de giro.

1. INTRODUCTION

Discussions about corporate value permeate corporate finance literature over time. In this context, the process by which it is estimated the company’s value or any asset is called the valuation or valuation of companies (GALDI; TEIXEIRA; LOPES, 2008). This estimation, however, is not a simple task (MARTINS et al., 2001). Much of the difficulty is based on the subjectivity of the exercise, which deals with premises and projections, and can be influenced by the analyst's own bias (DAMODARAN, 2002). Another factor that makes this forecast even more challenging is the Brazilian institutional environment, which has very peculiar characteristics in comparison to more developed markets (CUNHA; MARTINS; ASSAF NETO, 2014).

Researchers have developed some valuation methods in the search of techniques for performing this assessment. Among many, the model of free cash flow is quoted in the literature as the most common (SOUTES et al., 2008). The assumption that guides this method says that the company’s value is configured as the sum of the projected values of free cash flows, brought to present value (DAMODARAN, 1997; BRIGHAM; GAPENSKI; EHRHARDT, 2001). The most common structure for the calculation of these cash flows is the companies’ cash flow, whose calculation is affected by the variation of working capital (DAMODARAN, 2002). Working capital is the difference between assets and liabilities that is considered operational, calculated by Fleuriet’s Model, to classify as operational is up to the evaluator/analyst.

However, there are many choices for those who prepare the accounting reports. This judgment freedom to the authors in the accounting reports is called in the literature as the accounting choice (FIELDS; LYS; VINCENT, 2001). The accounting choices are part of the Accounting Positive Theory study’s objective, proposed by Watts and Zimmermann (1986). They derive economic variables and are therefore different from business to business. (WATTS, 1982). In this context, the Cash Flow Statement (CFS) is an example of a financial report that is affected by the accounting choices. According to CPC 03 – Cash Flow Statement, CFS aims to provide capability to the user in the process of analyzing the com pany's cash generation capacity, and it does so by dividing the cash into three types: Operational, financing and investment.

This classification, however, does not have a consensus for interest, dividend and interest on shareholders' equity. In the CFS, the Brazilian Committee still encourages some classifications, but provides the managers with the options of the accounting choice they deem most appropriate. Interest paid and received, dividends and interest on shareholders 'equity received can be classified as both operational cash flow and financing (interest paid) and investment (interest, dividends and interest on shareholders' equity received). On the other hand, dividends and interest on paid capital can be both financing and operational cash flows.

Therefore, since the accounting choices about dividends exist in the classification of CFS, it is plausible to think of a relation between these choices and the companies’ value. For example, if the dividends received are classified as operational activities in the CFS, this would imply that they should be classified as operational assets, which would affect the value of the working capital investment. In contrast, if they were investment activities, they would not be computed in the calculation. Consequently, the possibility of accounting choices would lead to a difference in the free cash flow and, therefore, in the value of the companies.

Galdi, Teixeira and Lopes (2008) compared the estimated company’s values by different models. The results suggest that the free cash flow model has more explanatory power than Ohlson's for the Brazilian market. Cunha, Martins and Assaf Neto (2014) evaluated projections of economic and financial performance of several Brazilian companies. They concluded that there are significant differences between the projected and realized in the company’s evaluating process. Cardoso, Martinez and Teixeira (2014) found the relationship between free cash flow and the propensity to results management through manipulation of discretionary accruals, finding a positive relation, corroborating with previous studies.

In this way, it is possible to observe the existence of a theoretical gap, if there is an impact of the dividends choices on the company’s value. Thus, the objective of this paper is to answer the following research question: does the accounting dividends choice, allowed in the Cash Flow Statement, influence the Brazilian companies’ value? For that reason, the main contribution of this study is directed to the analysts. This group formulates its ratings from a method, which has inputs as variables and assumptions. From a combination of this information comes in the output represented by the free cash flow, basis measurement of the company’s value. Consequently, the discovery of a new variable that can impact in free cash flow measurement should affect the company’s value, which implies that analysts should be cautious in the selection of inputs so the forecast is closer to the real company’s value, namely seeking greater accuracy.

2. RELATED LITERATURE

2.1 VALUATION

The concept of value has always been the subject of classical discussions. However, there is no consensus on its definition because it is linked to the subjectivity of the subject (PEDRO, 2014). In accounting, the process of assigning value to an objective is called measurement (HENDRIKSEN; VAN BREDA, 1999). However, achieving accuracy of value is not an easy task because, in addition to the abstraction of the term in question, accounting is not an exact science and is therefore affected by several judgments (ALMEIDA; HAJJ, 1997). Moreover, the amount of subjectivity is what provides the existence of markets where buyers and sellers transact assets because it binds different values to those objects.

In the markets’ environment, assets are traded in many ways and in different situations, such as mergers and acquisitions’ process, scission and privatizations. In these circumstances, which usually have high competitiveness, it commonly becomes necessary to estimate values of these objects, or even companies from a method that is titled valuation (GALDI; TEIXEIRA; LOPES, 2008) and it has been a theme widely studied in the literature (SANTOS; CUNHA, 2015). However, whatever the purpose of the evaluation, the evaluator's goal is always the search for the so-called intrinsic value (CUNHA; MARTINS; ASSAF NETO, 2014).

This intrinsic value (or fair) can be defined as the amount that would be tied to an asset by an expert, with access to all information available at the time, using a perfect model assessment (DAMODARAN, 2007). The market reality, however, is imperfect, being supported mainly by the assumptions of the Agency Theory and the semi-strong form of Efficient Market Hypotheses, which admit the existence of the problem of informational asymmetry (SCOTT, 2008). Moreover, there is no perfect valuation model since fair value is subjective and it is closely linked to the company’s projection to generate future benefits (SOUTES et al., 2008), and the expectations of growth and risk associated with the result of cash flows (ASSAF NETO, 2008).

In order to get closer to this intrinsic value, to be able to represent in a balanced way the company’s potentialities and perspectives, these evaluations use quantitative methods and models based on assumptions and behavioral hypotheses (PEREZ; FAMA, 2003). Thus, finance literature has developed various valuation methods such as the pricing model of Black and Scholes options (1973); adjusted present value (APV), proposed by Myers (1974); The Ohlson model (1995); free cash flow and its variations, defended by Damodaran (1997), among others. Free cash flow is quoted in the literature as one of the most used in business valuation (SOUTES et al., 2008).

2.1.1 Free cash flow

According to this methodology, the company’s value is determined by the sum of present and future benefits’ streams, discounted at a rate that reflects the opportunity cost and the risks associated with the investment (CUNHA; MARTINS; ASSAF NETO, 2014). Therefore, the method consists in bringing the sum of the cash flows to the present value over a period in which it can be estimated with reasonable certainty, discounted at a rate that reflects the risk. In addition, the company’s present value of the residual value or perpetuity is added, which are the flows not covered by the projection, discounted by the difference between the rate of risk and the rate that these flows are expected to grow. In short, the model can be defined as the equation (1):

equation (1)

equation (1)In which, t = the useful life of the asset; FCFF t = operational cash flow in the period t; r = discount rate reflecting the risk inherent in the estimated cash flow; g = growth rate of operational cash flow. Thus, the great difficulty of this method lies in accurately and timely forecasting of relevant variables such as operational cash flow, the horizon of this flows’ projections, the perpetuity value and discount rate of cash flows (PEREZ; FAMA, 2003).

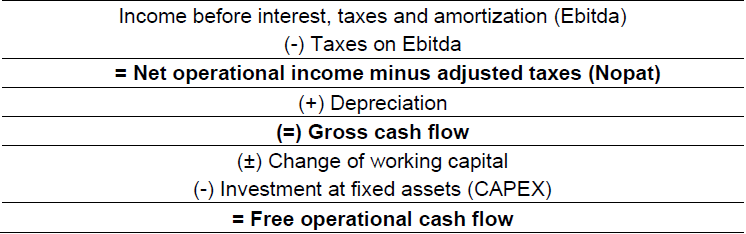

Also, operational cash flow can be estimated from several perspectives: the company, the shareholders and dividends, thus allowing different information, in view of the objectives of its various users (SANTOS; CUNHA, 2015). For the purpose of this paper, we considered the company's cash flow approach, which is the most common among companies’ appraisal reports. However, it should be noted that in situations of consistency of the assumptions used, the results obtained by different models are the same (GALDI; TEIXEIRA; LOPES, 2008). The calculation of the company's cash flow can be explained in Chart 1.

EBITDA is earnings before interest, taxes and amortization and can be obtained from the Income Statements (IS). The depreciation corresponds to the depreciation expense of the period, which is usually available in the IS. CAPEX is the amount of money spent on acquiring (or introducing improvements) capital goods from a particular company. The change in working capital is the variation in working capital between the year considered and the previous one, with the difference between current assets and current liabilities, calculated by Fleuriet’s model (Dynamic Working Capital Model).

Chart 1

Calculation of the company’s free cash flow

Elaborated by the authors.

According to Ambrozini, Matias e Pimenta Júnior (2014), in this model, the current assets and current liabilities on the companies’ Balance Sheet are reclassified into two sub-groups according to its operational cycle, in order to differentiate the accounts according to the time each takes to perform its rotation or turnover. Simplifying, Fleuriet’s Model (2003) proposes a reorganization of the assets accounts into operational or cyclical (it is constantly renewed in the normal course of the business operations), and financial or erratic (usually it arise from administrative decisions or negotiates, unrelated to production and sales activities). In this sense, it is up to the analyst to classify such accounts in the most appropriate way to best reflect the company’s reality, with so, their choices will affect the working capital calculation and therefore, its value.

2.2 ACCOUNTING CHOICES

The Accounting Positive Theory, proposed by Watts and Zimmermann (1986), seeks to explain and predict the choices of accounting practices (recognition, measurement and disclosure) as well as the effects on the cash flows caused by these choices. From Firm's Contractual Theory, the company is seen as a nexus of formal or informal contracts among its various users and which are inevitably incomplete (MILGROOM; ROBERTS, 1992). This incompleteness in the contracts allows the parties to act differently from the agreement, since the information available is not the same for both parties of the relationship (JENSEN; MECKLING, 1976).

In this environment surrounded by conflicts of interest, Watts and Zimmermann (1986) start from the premise that individuals act in their own interests, seeking to maximize their well-being. In this sense, individuals should prefer certain practices that benefit their interests (IUDÍCIBUS; LOPES, 2004). Thus, it is necessary to identify what role accounting plays in the contractual and organizational arrangements and how the arrangements change from company to company, because it is through these provisions that the accounting choices exists (CABELLO; PEREIRA, 2015).

The different practices or accounting choices exist because it is impossible or impracticable to eliminate this flexibility (FIELDS, LYS; VINCENT, 2001). Accounting choice is a decision that influences the outcome of the accounting system in a very specific way, and the choices may vary among companies. This variation derives from the handling of the accounting, more precisely, from the void of the rules, the criteria chosen by the managers and the different accounting practices that can be taken (CABELLO; PEREIRA, 2015).

In addition, imposing an accounting standard that can deliver a language of disclosure that meets the needs of all firms in all markets is difficult because markets may be different (FIELDS, LYS; VINCENT, 2001). Moreover, not always the uniformity of accounting policies will portray faithfully the economic reality of all businesses, because they work with different operations, have different capital structures and are aimed at different users. Thus, a single imposed standard can negatively impact the quality of the information disclosed (HAIL; LEUZ; WYSOCKI, 2009).

The accounting choices are reenforced with the International Financial Reporting Standards (IFRS). These reporting standards are elaborated by the International Accounting Standards Board (IASB), which is responsible for promoting the convergence of the accounting standards among the countries (LEMES; SILVA, 2007). The IFRS provides a greater judgement of the administrators in the implementation of the standards (HAIL; LEUZ; WYSOCKI, 2009). One exemple is the flexibility in the classification treatment of some accounts in the Cash Flow Statement (CFS), mandatory in Brazil, for most companies in the Stock Market, after Law 11.638/2007. On the other hand, for some regulated sectors like energy and finance, CFS was already mandatory, also, some companies voluntarily reported their CFS (SALOTTI; YAMAMOTO, 2008).

2.2.1 Accounting choices in Cash Flow Statements

The Cash Flow Statement (CFS) is an accounting statement that should provide information so that its users can identify the entity's ability to generate cash and cash equivalents, as well as the needs for using those cash flows. Their preparation and disclosure rules are regulated by CPC 03, which is in line with its corresponding international standard, IAS 07 - Statement of Cash Flows. In terms of presentation, the CFS should present the cash flow for the period classified by three types of activities: operational, investment and financing, which are defined as:

Operational activities are the entity's main revenue generating activities and other activities that are neither investment nor financing. Investment activities are those relating to the acquisition and sale of long-term assets and other investments not included in cash equivalents. Financing activities are those that result in changes in the size and composition of the entity's own capital and third-party capital (IAS, 2007).

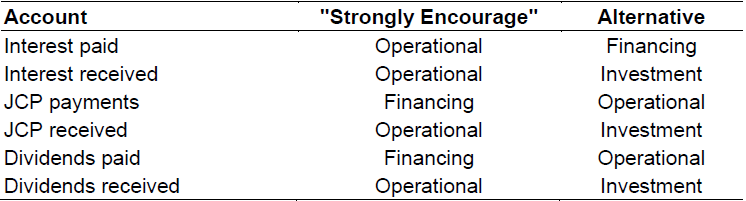

Also, paragraph 11 of CPC 03 lists: "An entity shall present cash flows from operational activities, investments and financing activities in the way that is most appropriate to their business”. Based on this concept, the standard exposes the possibility of accounting choices, which is clearly evidenced in paragraphs 33, 34 and 34A of CPC 03. The account of interest paid and received; Interest on capital paid and received and dividends paid and received do not have a classification consensus. However, it should be noted that the CPC "strongly encourages" certain classifications and requires disclosure in an explanatory note if the entity deems it not to be the most appropriate. Chart 2 summarizes the possibilities and recommendations.

In relation to the account of interests paid, it can be classified as operational because it enters into the determination of net profit or loss, or as financing because it may be a cost of obtaining financial resources. Interest, dividends and interest on equity received can be classified as operational also because they enter the determination of net income or loss, or as an investment, because it may be returns on investments. Finally, dividends and interest on equity paid can be classified as financing because it can be financial or operational costs to assist users in determining the entity's ability to pay dividends and interest on shareholders' equity using the operational cash flows.

Chart 2

Accounting choices in CFS

Elaborated by the authors.

2.3 PREVIOUS STUDIES

Galdi, Teixeira and Lopes (2008) compared the differences between the company’s values estimated by the discounted cash flow model and Ohlson's model (1995). The researchers used the methodology of comparing the estimates made by analysts using the discounted cash flow method and estimates of the companies’ value recalculated from the information contained in the analysts' reports by the Ohlson’s model. The findings indicated the existence of statistically significant differences for the estimated value of the companies by these methods, in addition to suggesting that the discounted cash flow model has more explanatory power than Ohlson’s.

Cunha, Martins and Assaf Neto (2014) evaluated projections of economic and financial performance of Brazilian companies between 2002 and 2008 in 58 samples from various sectors of the national economy. The authors performed means tests on paired samples to evaluate if the projections were adherent over time. They concluded that, apparently, there are significant differences between projected and realized in the companies valuation process, especially in relation to some values’ conductor as, operational expenses, indebtedness, growth rates and reinvestment, which are inputs of the free cash flows model.

Cardoso, Martinez and Teixeira (2014) found the relationship between free cash flow and the propensity to manage results through handling of discretionary accruals for companies with low growth prospects. The database consisted of companies listed on BMF & Bovespa between 2008 and 2012, in a total of 111 observations. The authors concluded that, as in the developed financial markets, there is a positive relationship between the amount of free cash flow and discretionary accumulations in Brazil, corroborating with previous studies.

Santos and Cunha (2015) analyzed whether in appraisal reports with purpose of OPA, the relationship between the company’s appraisal and the company’s contractor appraisal causes bias in the fair value per share in relation to the share price. The period studied comprised the years 2002 to 2013, with a total of 106 reports and the methodology used was the means test. As a result, there is a bias in the evaluation process, especially in situations where the evaluation contractor is the evaluated company.

It is possible to observe that the literature on company’s valuation seems to be focused on the comparison between different models, the adherence of projections and the cash flow from a skewed perspective and results management. On the other hand, research on accounting choices is directed towards studying the different practices and the benefits and costs that determine these choices (BERSTER; COLLIN; LYS, 2012). In this way, there seems to be a gap in the state of the art about the possible impact that accounting choices have on the companies’ values. Thus, this paper has the potential to contribute to literature, filling the gap.

The present study aims to fill this gap and find out if there is any impact, due to the dividends accounting choices, on the companies’ value. As mentioned above, the manager has freedom in the accounts classification, interest, equity’s interest and dividends (received and paid), while elaborating the CFS. In addition, there is also the flexibility exposed in the Dynamic Working Capital Model, in which they choose the accounts that composes the calculation.

Thus, if any account is classified as operational, this could impact the calculation of working capital, which is the difference between current operational assets and current operational liabilities. For example, the classification of dividends paid as operational activity in the CFS implies that this account (dividends payable) should be considered as current operational liabilities in the calculation of working capital. The opposite is also true: if it is classified as an activity of financing it should not be computed in working capital. This difference in value of working capital, therefore cause a difference in the calculation of free cash flow and consequently on the companies’ value. In this context, the paper proposes to test the following hypothesis:

H1: The accounting choice of dividends generates a significant difference in the means of companies’ value.

3. METHODOLOGY

3.1 DATA AND SAMPLE

For the sample of the survey, we considered 80 Brazilian publicly traded companies that are listed in the BMF & Bovespa, which, since March 2017, is called B3. Financial institutions were excluded because they have different rules, and therefore do not allow comparability. In addition, regulatory issues differentiate the way dividends are distributed to this group. The financial statements used were non-consolidated (individual). These criteria is justified by the existence of received dividends only in this type of statement, since dividends received from subsidiaries are eliminated in the consolidation process from the financial statements. The information was taken from Economática. The study period was from 2011 to 2015. The time window selection is because IFRS was fully adopted only in 2010, although the CFS was mandatory since 2008.

Considering the structure to calculate Free Cash Flow, previously discussed in Chart 1, the variable EBITDA was taken from Economática®. For the calculation of income tax, the rate considered was 34 % which corresponds to the sum of income tax (15%), additional income tax (10%) and social contribution (9%). The EBITDA minus the tax originates the NOPAT. Then, each company’s depreciation expense, which was available in the Income Statement for the Year (DRE) and collected in Economática®, was added, which generates the Gross Cash Flow. From it was deducted the CAPEX, available in Economática® and the variation (positive or negative) of Working Capital, arriving at the Free Cash Flow.

It should be pointed out that, for analysis, two company's cash flows were calculated: the first one (FOCF1) does not take into account the dividends as an operational account, and therefore does not compute the working capital calculation. Subsequently, (FOCF2) was calculated, in which dividends, both received and paid, were considered as operating. Thus, they were added to the Working Capital (WC) calculation. As the WC implies in the variation between operating assets, deducted from operating liabilities, the dividend’s balances accounts that were included in the Balance Sheet were added to the WC.

3.2 STATISTICAL TREATMENT

The first step was to verify the normality of the distribution, the mean and the variance of the data. The most commonly used tests to verify univariate normality are the Kolmogorov-Smirnov (KS) and Shapiro-Wilk (SW) tests.

Per Fávero et al. (2009), if the data having normal distribution, the most common is to use the parametric Student t test to compare two independent means: the means of the values of Brazilian companies considering or not the accounting choice of dividends. However, if the normality of data distribution is not met, a non-parametric test (BICKEL; DOKSUM, 1977) should be used, one of the most common being the signal test. The null hypothesis of these parametric and non-parametric tests asserts that there was no significant difference between the groups compared. In this way, the means or values are expected to be different, thus rejecting the null hypothesis. The tests were conducted in Stata 14® software. The steps are outlined in Appendix A.

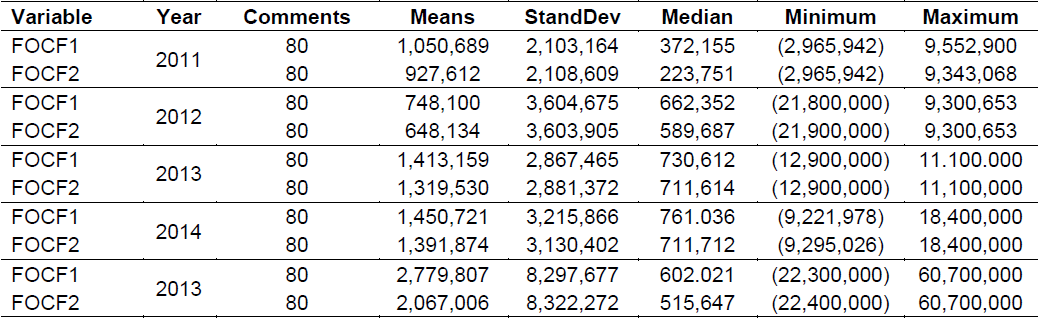

Table 1 presents a descriptive statistic of the operational cash flows according to each accounting choice.

For each year, there is a small difference between the means of the groups of each cash flow, indicating the possibility of a difference arising from the accounting choice. In each choice, too, the standard deviation of cash flows is high, which can be explained by the heterogeneity of firm sizes in the sample - larger firms tend to have numbers more expressive than smaller companies. The same point can be seen in the minimum and maximum values found. Due to sample heterogeneity, the median becomes important because it points out the value that separates the groups of the largest from the group of the lowest values. It is observed, then, means values expressively smaller than the average ones, fruits of the great variation of sizes found in the sample.

survey data using Stata 14.

4. RESULTS

The next sections present the tests performed and their respective results. First, tests of normality between the two possible cash flows are presented in line with each accounting choice. Then, the mean and median tests to verify the statistical difference arising from the accounting choices.

4.1 TEST OF VARIABLES’ NORMALITY

The heterogeneity of companies in the sample indicated the possibility of absence of normality in the variables of interest in this study - something also seen by the descriptive statistics. Therefore, the Shapiro-Wilk test was performed to verify the existence or not of normality in the variables representative of the cash flows. The Shapiro-Wilk test presents as null hypothesis the distribution being normal (SNEDECOR; COCHRAN, 1989) and was considered an alpha of 0.05. Table 2 presents the result for the Shapiro-Wilk test.

The results for the Shapiro-Wilk test indicate that both variables do not present normality in their distribution (p-value < 0.05). This result points to the preference for the use of non-parametric statistical inference techniques, since traditional techniques use inference around mean values that may not be representative in this sample. This justifies the use of a median test in the analysis used in this research.

survey data using Stata 14 software.

4.2 TESTING MEANS DIFFERENCE AND SIGNAL TESTING

For the hypothesis test, mean and median difference tests were performed between both cash flows arising from each accounting choice. In the case of this study, paired groups were considered. A paired group is one that, with all others controlled, presents as the only difference one treatment to be investigated - in this case, accounting choice (SNEDECOR; COCHRAN, 1989). The possibility of a test using paired groups has a main benefit of further approximation to the true effect of the change that took place thanks to a phenomenon, since the other possible determinants must be controlled (SNEDECOR; COCHRAN, 1989).

Even with the Shapiro-Wilk test indicating that the distribution is not normal, a median test, a non-parametrical test, was performed as preliminary analysis of the hypothesis to be tested. The results for this test difference between means are shown in Table 3, considering alpha = 0.05.

The p-value of 0.0000 indicates that the null hypothesis of equality between the means may be rejected. Therefore, the accounting choice interferes with the mean values of the possible cash flows.

survey data using the software Stata 14.

This result is in accordance with what was theorized: the classification of dividends as operational activities in the CFS, and later in the calculation of working capital, affects the basis for the calculation and hence the company’s value. This suggests that analysts should consider this variable (accounting choice of dividends), when performing their projections.

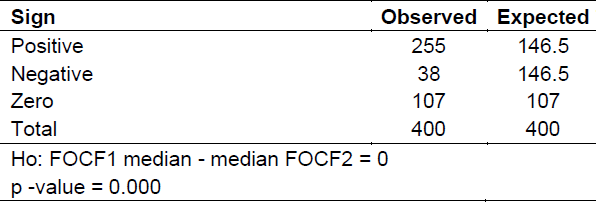

Finally, the test signals indicated by the absence of normality in the distribution of the sample was performed on the assumption that the difference between the matched sample values is zero. In other words, the sign test checks whether there was a difference between the values of paired samples caused by the difference in treatment (SNEDECOR; COCHRAN, 1989). It is important to remember that a nonparametric test no other claim on the distribution is carried out, which is its weakness - inference using average values tend to be more robust (SNEDECOR; COCHRAN, 1989). The results for the test of difference between medians are shown in Table 4, whereas a 0.05 alpha.

survey data using the software Stata 14.

The p-value of 0.000 rejects the null hypothesis that the medians of the variables did not present statistical difference. This corroborates the mean test performed previously and confirms the prediction made by the hypothesis: the presence of dividends in working capital calculation influences the company’s free cash flow measurement.

5. CONCLUSIONS

This study aimed to investigate the relationship between accounting choices concerning the classification of dividends as operational, investment (dividends received) or financing (paid dividends) in the Cash Flow Statementin the calculation of working capital from Fleuriet’s Model (2003). Per this model, what makes up the working capital is the difference between Current Operational Assets and Current Operational Liabilities; however, this is the evaluator/analyst’s decision.

The methodology considered only companies listed on the Bovespa's New Market segment, for the years 2011 to 2015. There were carried out median differences and signs tests that confirmed the hypothesis presented: the presence of dividends in the calculation of working capital affect the company’s free cash flow and therefore its value. The finding of this research implies that analysts should consider the dividend when making a judgment call of their inputs to the projection. Thus, it takes a careful analysis of the essence of dividends on the company that is being analyzed.

It is important to highlight that the results presented in this paper are initial evidence because of the basic methodology. For future research, it is suggested to extend the sample to all companies listed on the stock exchange, and the use of more sophisticated statistical technique, for example, use of panel data. It might be interesting to do an analysis of how the share price may be affected in this situation.

References

ALMEIDA, M. G. M.; HAJJ, Z. S. E Measurement and Asset Evaluation: a conceptual review and an approach to Goodwill and intellectual assets. Journals, Vol. 9, n. 16, p.66-83, 1997.

AMBROZINI, M. A.; MATIAS, A. B.; PIMENTA JÚNIOR, T. Análise Dinâmica de Capital de Giro segundo o Modelo Fleuriet: uma classificação das empresas brasileiras de capital aberto no período de 1996 a 2013. Contabilidade Vista & Revista, v.25, n.2, p. 15-37, 2014

ASSAF NETO, A. Corporate finance and value. In: .[Sl]: Editora Atlas, 2005. cap. Fashion model asset pricing and opportunity cost, p. 253-278.

Badertscher, B. A; COLLINS, D. W; LYS, T. Z. Discretionary accounting choices and the predictive ability of accruals with respect to future cash flows. Journal of Accounting and Economics, 53, p. 330-352, 2012.

BARTH, M. E; BEAVER, W.H; Landsman, W. R The relevance of the value relevance literature for financial accounting standard setting: another view. Journal of Accounting and Economics, v. 31, no. 1-3, p. 77-104, 2001.

BOWEN, R. M.; Burgstahler, D.; DALEY, L. A. The incremental information content of accrual versus cash flow. The Accounting Review, Vol. 62, no. 4, p.723-747, 1987.

BRIGHAM, E. F.; GAPENSKI, L.C.; EHRHARDT, M.C. Financial Management: Theory and Practice. São Paulo: Atlas, 2001.

CABELLO, O. G; PEREIRA, C. A. Effects of profit taxation practices in the effective tax rate (ETR):. An approach Theory of Financial Choices Advances in Scientific and Applied Accounting, v.8, n.3 p. 356-373, 2015.

CARDOSO, F. T.; MARTINEZ, A. L.; TEIXEIRA, A. J. C. Free cash flow and earnings management in Brazil: The negative side of financial slack. Global Journal of Management and Business Research, Vol. 14, n. 1, p. 84-96, 2014.

RABBIT, A. C. D.; GALDI, F. C.; LOPES, A. B. The determinants of earnings quality: the case of Brazilian public and private Firms. 2010. SSRN.

CPC. Committee of Accounting Pronouncements CPC 03 - Cash Flow Statement. Available in http://www.cpc.org.br.

COPELAND, T. Evaluation companies - Valuation: Calculating and Managing Value Enterprise. [Sl]: Pearson Education, Brazil, 2002.

CUNHA, M. F.; MARTINS, E. ASSAF NETO, A. Evaluation of companies in Brazil by discounted cash flow: empirical evidence from the point of view of value drivers in the public offerings of shares. Journal of Management - RAUSP, v. 49, no. 2, p. 251-266, 2014.

DAMODARAN, A. Investment Rating: tools and techniques for determining the value of any asset. Rio de Janeiro: Qualimark 1997.

______. Corporate Finance Applied - User'sGuide. Porto Alegre: Bookman, 2002.

FÁVERO, L. P. L. et al. Data analysis: multivariate modeling for decision making. Sao Paulo: Campus, 2009.

FIELDS, T. D.; LYS, T. Z.; VINCENT, L. Empirical research on acconting choice. Journal of Accounting and Economics, v. 31, no.1, p. 255-307, 2001.

FLEURIET, M.; KEHDY, R.; BLANC, G. The Fleuriet model - the financial dynamics of companies. 5. ed. Rio de Janeiro: Elsevier, 2003.

GALDI, F. C.; TEIXEIRA, A. J. C.; LOPES, A. B. Empirical analysis of valuation models in the Brazilian environment: discounted cash flow versus Ohlson model (RIV). Journal of Accounting and Finance, vol. 19, n. 47, p. 31-43, 2008.

GRAHAM, J. R.; HARVEY, C. R. How CFOs make capital budgeting and capital structure Decisions. Journal of Applied Corporate Finance, Vol. 15, no. 1, p. 8-23, 2002.

HAIL, L.; LEUZ, C.; WYSOCKI, P. D. Global Accounting Convergence and the Potential Adoption of IFRS by the United States: An Analysis of Economic and Policy Factors. Http://ssrn.com/abstract=13573312009.

HENDRIKSEN, E. S.; VAN BREDA, M. F. Accounting Theory. 5th ed., São Paulo, Atlas, 550, 1999.

HUNG, M.; SUBRAMANYAM, K. R. Financial statement effects of Adopting international accounting standards: The case of Germany. Review of Accounting Studies, vol.12, p. 623-657, 2007.

IUDÍCIBUS, S.; LOPES, A. B. Advanced theory of accounting. São Paulo: Atlas, 2004.

JENSEN, M.; MECKLING, W. Theory of the firm: managerial behavior, agency costs, and capital structure. Journal of Financial Economics, vol. 3, no. 4, p. 305-360, 1976.

RUDDERS, S.; SILVA, M. G. A. The experience of Brazilian companies in the adoption of IFRS. Accounting and Vista Magazine, vol. 18, n. 3, p. 37-58, 2007.

MARTINS, E. et al. Companies Evaluation: accounting measurement of the economic. São Paulo: Atlas, 2001.

MILGROM, P.; ROBERTS, J. Economics, organization and management. New Jersey, NJ: Prentice Hall, 1992.

OHLSON, J. Earnings, book values and dividends in equity valuation. Contemporary Accounting Research, vol. 11, p. 661-687, 1995.

SALOTTI, B.; YAMAMOTO, M. M. Divulgação voluntária da demonstração dos fluxos de caixa no mercado de capitais Brasileiro. Revista Contabilidade & Finanças, v. 19, n. 48, p. 37-49, 2008.

SANTOS, T. B. D.; CUNHA, M. F. Evaluation companies: an analysis from the perspective of "evaluation bias" in the public offer of awards of shares. Management magazine, Finance and Accounting, vol. 5, n. 3, p. 61-74, 2015.

SANVICENTE, A. Z. The Awards Relevance by Sovereign Risk and Foreign Exchange Risk in Using the CAPM for Estimation of Cost of Capital Enterprises. [Sl], 2008.

SOUTES, D O.; MARTINS, E.; SCHVIRCK, E.; MACHADO, M. R. Evaluation methods used by investment professionals. Accounting, Management and Governance, vol. 11, n. 1-2, p.1-17, 2008.

PEDRO, A. P. Ethics, moral, axiology and values: Confusions and ambiguities around a common concept. Kriterion: Journal of Philosophy, vol. 55, n. 130, p. 483-498, 2014.

PEREZ, M. M.; FAMA, R. Methods of business valuation and balance determination. Research Notebook Administration, v. 10, No. 4, p. 47-59, 2003.

SCOTT, W. R. Financial Accounting Theory. Pearson Education Canada Inc, 2008.

SNEDECOR, G. W.; COCHRAN, W. G. Statistical Methods. 8th ed. Ames, Iowa: Iowa State University Press, 1989.

WATTS, R. L. Accounting choice theory and market-based research in accounting. British Accounting Review. Rochester, v. 24, p. 235-267, 1992.

WATTS, R. L.; ZIMMERMAN, J. L. Positive accounting theory. NJ: Prentice-Hall, Englewood Cliffs, 1986.