Articles

Do financial constraints impact the technical efficiency of agricultural cooperatives? evidence from Brazil1

A restrição financeira afeta a eficiência técnica das cooperativas agrícolas? evidências para o Brasil

Vanessa Schaefer vahschaefer@gmail.com

João Paulo Augusto Eça joaopauloeca@outlook.com

Marcelo Botelho da Costa Moraes mbotelho@usp.br

Amaury José Rezende amauryj@usp.br

Vanessa Schaefer vahschaefer@gmail.com

João Paulo Augusto Eça joaopauloeca@outlook.com

Marcelo Botelho da Costa Moraes mbotelho@usp.br

Amaury José Rezende amauryj@usp.br

Do financial constraints impact the technical efficiency of agricultural cooperatives? evidence from Brazil1

Enfoque: Reflexão Contábil, vol. 40, no. 3, pp. 79-95, 2021

Departamento de Ciências Contábeis - Universidade Estadual de Maringá

Received: 28 January 2020

Revised document received: 01 April 2020

Accepted: 21 April 2020

ABSTRACT: Agricultural cooperatives have the main goals of meeting the economic, social and cultural needs of their members. Although they do not seek profits, they must be competitive since they compete with other cooperatives and companies in the market. In this sense, the search for technical efficiency to give cooperatives a better market position contrasts with the difficulty these organizations face in obtaining foreign capital to enable greater investments. There is little empirical evidence, however, of the relationship between financial constraints and technical efficiency in these organizations. According to theoretical assumptions, this relationship could be positive or negative. Thus, this paper analyzes the impact of financial constraints on the technical efficiency of Brazilian agricultural cooperatives. For this, we used two metrics to measure financial constraint and analyzed panel data on 68 Brazilian agricultural cooperatives for the 2005-2014 period. Despite the theoretical predictions, our main results suggest there is no evidence that financial constraints affect technical efficiency. This result can be explained by the characteristics attributed to Brazilian cooperatives, that is, the fact they deal with different commodities (multi-purpose) and do not have strong demand for investments (technology). This paper contributes to the literature both by providing new empirical evidence regarding the relationship between technical efficiency and financial constraints and by introducing a new metric for analyzing financial constraint in the context of cooperatives.

Keywords: financial constraints, technical efficiency, agricultural cooperatives.

RESUMO: As cooperativas têm como objetivo principal atender às necessidades econômicas, sociais e culturais de seus membros. Embora não visem lucro, é necessário que sejam competitivas tendo em vista que concorrem com outras cooperativas e empresas no mercado. Neste sentido, a busca por uma eficiência técnica que confira às cooperativas um melhor posicionamento de mercado contrasta com a dificuldade que essas organizações enfrentam para obter capital externo. Capital este potencialmente capaz de viabilizar maiores investimentos. Existem poucas evidências empíricas, no entanto, que verificaram se (e o quanto que) a restrição financeira pode impactar a eficiência técnica nessas organizações. Os pressupostos teóricos apontam que esta relação pode ser tanto positiva quanto negativa. Assim, este artigo tem como objetivo analisar o impacto da restrição financeira na eficiência técnica das cooperativas agropecuárias brasileiras. Para isso, foram usadas duas métricas para medir a restrição financeira e, posteriormente, estimou-se um painel de dados com 68 cooperativas agrícolas brasileiras para o período 2005-2014. Nossos principais resultados sugerem que não há evidências de que a restrição financeira afeta a eficiência técnica das cooperativas brasileiras. No geral, é possível que este resultado possa ser explicado pelas características atribuídas às cooperativas brasileiras, isto é, o fato de lidarem com diferentes commodities (multi-propósito) e de não apresentarem uma demanda robusta por investimentos (tecnologia). O presente artigo contribui para a literatura tanto ao fornecer novas evidências empíricas a respeito da relação entre eficiência técnica e restrição financeira quanto ao introduzir nova métrica para análise da restrição financeira dentro do contexto de cooperativas.

Palavras-chave: restrição financeira, eficiência técnica, cooperativas agropecuárias.

1 INTRODUCTION

Cooperatives are “people-centered enterprises owned, controlled and run by and for their members to realize their common economic, social, and cultural needs and aspirations” (INTERNATIONAL COOPERATIVE ALLIANCE, 2013). The main goal of cooperatives is not profit. Instead, they aim to meet members’ economic and social needs through the products and services they offer (BENOS et al., 2018). This makes cooperatives able to promote the integration of communities in the dominant economy, but in order to achieve this purpose, it is important to analyze their performance, as pointed out by Xaba, Marwa and Helm (2019).

However, cooperatives face competition from both companies and other cooperatives, offering product and services. Most prior findings provide evidence that cooperatives are less efficient than companies (GRASHUIS, 2018; BRANDONO, DETOTTO; VANNINI, 2019). This competition makes cooperatives search for external financing in order to invest in assets, increase efficiency and ensure market position (BIALOSKORSKI NETO, 2006, 2012)

In Europe and the United States, many cooperatives have changed their capital structure to bring external investors as a response to agricultural industrialization and competition (CHADDAD; COOK, 2004). In this new capital structure, they can obtain financial resources and make the investments required to maintain efficient operational structures (CHADDAD; COOK, 2004). In Brazil, however, cooperatives are legally forbidden from obtaining equity investments, leading to the question of how they make investments.

According to Rodrigues et al. (2018), the optimal agricultural cooperative capital structure is still an open question, especially those in the state of Paraná. The cooperatives need to use their own resources (payment for members’ shares and retained residuals) and those of creditors (lenders). This causes limitations on cooperatives’ ability to obtain financial resources in two ways.

First, the members do not have incentives to invest more in shares because of the “one-member, one-vote” democratic principle (HANSMANN, 1996; CHADDAD; ILIOPOULOS, 2013), as well as because the members’ share of returns is limited in 12% per year, according the Brazilian Cooperatives Law (COOK, 1995; MAIETTA; SENA, 2010). Therefore, it is common, mainly in the first years, for cooperatives to retain residuals to obtain resources (CHADDAD; COOK; HECKLEI, 2005; RODRIGUES et al., 2018).

Second, as shown by Chaddad, Cook and Hecklei (2005), Gonçalves, Braga and Ferreira (2012) and Li, Jacobs and Artz (2015), agricultural cooperatives are financially constrained. Their cost to obtain external financial resources is higher than for companies. This occur because of the vague ownership rights and the information asymmetry between cooperatives and creditors (CHADDAD; COOK; HECKLEI, 2005; GONÇALVES; BRAGA; FERREIRA, 2012; LI; JACOBS; ARTZ, 2015).

In this context, do financial constraints impact agricultural cooperatives’ performance and survival? Can financial constraints impact their efficiency? In the literature, there is no consensus about these questions. On the one hand, empirical evidence shows that the resource scarcity decreases investments in assets and technological innovation, so the production units become inefficient (DERCON, 1996). On the other hand, resource scarcity can encourage managers to create process that improve the use of resources and avoid waste (NICKELL; NICOLITSAS, 1999; MAIETTA; SENA, 2010). For example, Maietta and Senna (2010) found that financial constraints positively impact Italian wine cooperatives’ efficiency. The authors argued that the lack of external financial resources leads the members to reduce inefficiencies in the production process to decrease losses.

However, unlike Italian cooperatives, most Brazilian agricultural cooperatives have a varied product portfolio. The cooperatives diversify their portfolios to meet the needs of the members instead of improving their market position by reducing risks and taking advantage of market opportunities (GONÇALVES; BRAGA; FERREIRA, 2012). Besides that, Brazilian cooperatives are not legally allowed to obtain equity from external investors. This traditional structure increases the probability that they will be financially constrained (CHADDAD; COOK; HECKLEI, 2005; GONÇALVES; BRAGA; FERREIRA, 2012). Thus, here we investigate the following research question: How do financial constraints impact Brazilian agricultural cooperatives’ technical efficiency?

We conducted panel data analysis pertaining to 68 Brazilian agricultural cooperatives in the state of Paraná from 2005 to 2014. These are the latest data available in the Observatory of Cooperative Organizations (Observatório do Cooperativismo - OBSCOOP)2, provided by the Cooperatives Organization of Paraná (OCEPAR). The cooperative organizations in other Brazilian states do not provide financial information.

Paraná is located Brazil’s South region and it has large participation in the nation’s agriculture. It is responsible for 20% of the vegetable origin and animal feed production in Brazil (LAUERMANN et al., 2018). Nationwide, agriculture accounts for nearly 25% of gross domestic product (GDP) (Cooperatives Organization of Paraná, 2017), and agricultural cooperatives contribute 50% of the country’s agricultural GDP (BRAZILIAN AGRICULTURE MINISTRY, 2016). In Paraná, agricultural cooperatives are responsible for 56% of agricultural GDP (COOPERATIVES ORGANIZATION OF PARANÁ, 2015).

Our results show there is no evidence that financial constraints affect the technical efficiency of agricultural cooperatives in Paraná. This result proved robust to additional testing. We argue that the Brazilian context explains our results, especially, two points. First, most Brazilian cooperatives work with more than one type of commodity, requiring different operational structures, and consequently influencing technical efficiency (GUZMAN; ARCAS, 2008). Second, there may be no strong technological needs of Brazilian cooperatives. In view of a possible lack of greater demand for investments in technology, it is reasonable to question the ability of financial constraints to affect the technical efficiency of cooperatives. In other words, cooperatives have sufficient ability to structure their internal capital to finance their investments without compromising technical efficiency.

Finally, our paper contributes to the literature from both the methodological and empirical standpoints. First, we have developed a new metric to analyze the financial constraints of agricultural cooperatives. Second, we present empirical evidence on two important aspects in the cooperative context: external capital constraint and technical efficiency.

This paper is organized in five sections including this introduction. Section 2 discusses the theoretical background and the research hypothesis; Section 3 demonstrates the research methods; Section 4 presents and discusses the results; and Section 5 concludes.

2 THEORETICAL FRAMEWORK

A firm is financially constrained when, due to its difficulty of attracting external resources, its investments rely on internal cash generation (ALMEIDA; CAMPELLO; WEISBACH, 2004; KAPLAN; ZINGALES, 1997). Because of the lack of resources, Ottaviano and Souza (2017) argue that the financial constraints limit firms’ innovation, growth and performance.

The financial constraint phenomenon is a widespread market feature (AMBROZIO et al., 2016). It occurs because of information asymmetry. Financial intermediaries require high risk premiums to provide capital in situations where they do not know the risks underlying the business and the borrower’s management skills (Ambrozio et al., 2016). This problem is more intensive in agricultural cooperatives since their ownership rights are vague, so they have difficulties to obtain resources from their members and from financial intermediaries (CHADDAD; COOK; HECKLEI, 2005).

In the first case, when the members buy their shares, they acquire the right to vote in meetings by the democratic principle and receive the residuals based on patronage (HANSMANN, 1996; CHADDAD; ILIOPOULOS, 2013). However, they do not receive a return based on the share value, so they do not have incentive to buy more shares (MAIETTA; SENA, 2010). Cook (1995) called this the horizon problem.

Because of the horizon problem, some cooperatives, mainly in their early years, decide to retain the residuals as members’ shares (CHADDAD; COOK; HECKLEI, 2005). With the retained residuals, they have resources to invest in assets (CHADDAD; COOK; HECKLEI, 2005). When the cooperative transforms the residuals into members’ shares, it increases the value of its equity, which is generally considered a guarantee to obtain loans. However, since the members’ shares are redeemable, the cooperative becomes financially unstable, from the creditors’ point of view (CHADDAD; COOK; HECKLEI, 2005).

Therefore, cooperatives may have difficulties to obtaining external capital due to the following factors: i) the existence of redeemable shares (BIALOSKORSKI NETO, 2000; GONÇALVES; BRAGA; FERREIRA, 2012); ii) the Brazilian bankruptcy law does not apply to cooperatives, so creditors do not have any guarantee they will obtain partial recovery if the cooperative fails (BIALOSKORSKI NETO, 2000; GONÇALVES; BRAGA; FERREIRA, 2012); iii) the multiple members’ roles in the cooperative (suppliers, clients, owners and administrators) makes ownership rights dispersed, so it is difficult for creditors to monitor the cooperative’s performance (GONÇALVES; BRAGA; FERREIRA, 2012); and iv) non-professionalization of management, generating distrust of creditors in relation to the efficient management of resources (BIALOSKORSKI NETO, 2012).

In Paraná, Gonçalves et al. (2012) found that agricultural cooperatives are more financially constrained than agricultural companies. The authors argued that this result might be the effect of the lack of definition of property rights in cooperatives, posing additional risk for lenders and no return on investment from members’ standpoint. Therefore, cooperatives can be considered financially constrained for two reasons: lack of own capital and information asymmetry between the cooperative and creditors (CHADDAD; COOK; HECKLEI, 2005; GONÇALVES; BRAGA; FERREIRA, 2012; LI; JACOBS; ARTZ, 2015).

One of the immediate consequences of the restriction on capital is the increased cost of capital of cooperatives. According to Maietta and Sena (2010), this increase can influence performance by increasing production costs and, consequently, decreasing the profits and waste that each member receives at the end of the year.

In addition, financial constraints can affect investment capacity and efficiency (DERCON, 1996). Agricultural cooperatives need to invest in specific assets to store or benefit the members’ production (HENDRIKSE; VEERMAN, 2001), and without access to financial resources they may have difficulties in maintaining an efficient productive structure (CHADDAD; COOK; HECKLEI, 2005).

Porter and Scully (1987) classified economic efficiency into allocative, technical and scale. Technical efficiency means the firm’s ability to obtain the maximum output given a set of inputs; allocative efficiency means the firm’s ability to use its inputs in optimal proportions given their relative prices (SOUZA; BRAGA; FERREIRA, 2011); and scale efficiency involves the firm’s ability to choose the right level of output (SEXTOW; ISKOW, 1988). In this study, we consider the concept of efficiency as the level of performance that can be achieved by an economic unit according to its production possibilities (GUZMAN; ARCAS, 2008). Because of this, we analyzed technical efficiency. We argue that if the cooperatives are financially constrained, they need to use the resources available to achieve optimal output.

However, financial constraint may be a limiting factor to maximizing results (KOMICHA; OHLMER, 2007), because firms invest more in low-risk and low-productive assets than in high-risk and potentially high-productive assets (DERCON, 1996). In Brazil, Braga and Ferreira (2011) found that small cooperatives invest in short-term activities which are less risky and provide lower return because they do not have their own resources and also do not have access to credit. On the other hand, large cooperatives have more internal resources and have greater and cheaper access to external financing, so they invest in technology development to increase efficiency level (SOUZA; BRAGA; FERREIRA, 2011; RODRIGUES et al., 2018). In the long term, Li et al. (2015) explained that the credit restriction can have negative implications for the survival and growth of agricultural cooperatives.

Thus, based on the assumptions listed above, we argue that financially restricted cooperatives have more difficulties to acquire technology and sustain efficient asset structures than others that are not financially restricted. Thus, we formulated the following research hypothesis:

-

H1: Financial constraints negatively impact Brazilian agricultural cooperatives’ technical efficiency.

On the other hand, Maietta and Sena (2010) showed that financial constraints positively impact Italian wine cooperatives’ technical efficiency. The main argument for this result is that the financial constraint can act as an incentive for the members to apply the scarce resources more efficiently (NICKELL; NICOLITSAS, 1999). Nevertheless, Maietta and Sena (2010) concluded that the impact of financial constraint can be different for each type of cooperative. In Brazil, cooperatives adopt the traditional organizational form (without external investors) and have a diversified portfolio (not only a single product, such as wine). Because of this, we argue that the relationship between financial constraint and technical efficiency in Brazilian agricultural cooperatives might be different from the Italian context.

3 METHODOLOGY

This study analyzes the impact of financial constraints on agricultural cooperatives. First, we use data envelopment analysis (DEA) to measure the technical efficiency index of cooperatives. After that, we estimate an unbalanced panel data regression to identify the possible impact of financial constraint on technical efficiency.

Our initial sample contained 74 agricultural cooperatives from Paraná. We excluded cooperatives that did not have enough financial data to calculate all variables and those that showed negative equity. Thus, our final sample was composed of 68 cooperatives and 514 observations. We analyzed data from 2005 to 2014, obtained from OBSCOOP, which has a standard chart of financial accounts for all cooperatives. These data are the last complete data available from OBSCOOP. After 2014, cooperatives did not send more financial information, and before that, only cooperatives from Paraná sent information regularly for all years. The cooperatives from other states sent information only for some years, so we were not able to carry out panel data analysis with them.

The following subsections address the technique for measuring the technical efficiency of agricultural cooperatives, as well as other variables used in the model.

3.1 MEASUREMENT OF TECHNICAL EFFICIENCY

Data envelopment analysis (DEA) was developed by Charnes, Cooper and Rhodes (1978) and subsequently extended by Banker, Charnes and Cooper (1984). It is a nonparametric mathematical programming technique that aims to measure the efficiency relative of productive units, called decision making units (DMUs). The nonparametric technique assumes that the production function, which relates the output produced with the inputs consumed, is unknown (GUZMAN; ARCAS, 2008). According to Xaba et al. (2019), DEA is a widely used method to measure the efficiency of agricultural cooperatives.

In summary, through linear programming, DEA builds an efficient production frontier starting with selected inputs and outputs. Efficiency is determined by the distance of each DMU in relation of the efficient frontier (NEVES; BRAGA, 2015). Furthermore, DEA has a series of models with different interpretative forms. There are two models that stand out: the CRS (constant return to scale) model, or the CCR model, acronym of Charnes, Cooper and Rhodes (1978), which presupposes constant scale returns; and the VRS model (variable returns to scale), or BCC, developed by Banker, Charnes and Cooper (1984). The orientation can be to input or output (NEVES; BRAGA, 2015).

Like Neves and Braga (2015) and Soboh et al. (2012), we adopted a BCC model with output orientation, which seeks to maximize output with a given amount of inputs. Our DEA model considered the multipurpose characteristics of Brazilian agricultural cooperatives (NEVES; BRAGA, 2015), since to meet the needs of all cooperative members, they operate with more than one product type, as well as offer different kinds of service (BIALOSKORSKI NETO, 2012). We used the Stata software to measure the efficiency index.

Our BCC model was as follows:

Subject to:

Where yi is a vector (m × 1) of product quantities of the i-th DMU; xi is a vector (k × 1) of input quantities of the i-th DMU; Y is a matrix (n × m) of products of n DMUs; X is a matrix (n × k) of inputs of n DMUs; λ is a vector (n × 1) of weights; and φ is a scalar with values greater than or equal to 1, thus indicating the efficiency score of the DMUs. In this case, a value equal to 1 indicates the relative technical efficiency of the i-th DMU in relation to the others, and a value greater than 1 indicates relative technical inefficiency, while (φ -1) indicates the proportional increase in the products that the i-th DMU can obtain (keeping the amount of inputs constant). Last, we calculated 1/φ to obtain each DMU’s technical efficiency score, ranging from 0 to 1 (NEVES; BRAGA, 2015).

We selected inputs and outputs based on previous studies that analyzed technical efficiency of agricultural cooperatives and on accounting variables available in Brazilian cooperatives’ financial statements. We present these variables below:

Output (Y)

-

a) Gross revenue, measured by total revenues (SOUZA; BRAGA; FERREIRA, 2011; SOBOH; LANSINK; VAN DIJK, 2012; NEVES; BRAGA, 2015).

Inputs (X)

-

a) Operating expenses (NEVES; BRAGA, 2015).

-

b) Fixed assets, measured by total fixed assets of the current year (NEVES; BRAGA, 2015).

3.2 PANEL DATA REGRESSION

After measuring technical efficiency of cooperatives with DEA, we estimated panel regressions. Thus, the dependent, independent and control variables included in the model are presented below.

3.2.1. Dependent variable - technical efficiency (ef_tec)

As shown in 3.1 item, we calculated the technical efficiency variable through DEA (BCC model) for each cooperative in each year.

3.2.2. Independent variable - financial constraint

A firm is financially constrained when it cannot raise external credit with satisfactory cost to invest, and thus must depend on internal resources (investment-cash flow sensitivity) (ALMEIDA; CAMPELLO; WEISBACH, 2004; ONGORE; KUSA, 2013). There are some difficulties to define good criteria to classify a firm as constrained or not constraint (DEMONIER; ALMEIDA; BORTOLON, 2015). Therefore, we adopted two different methods to identify financial constraint.

3.2.2.1 Financial constraint 1 (fin_con_1)

For first method, we considered that small cooperatives are less known and thus have greater difficulty obtain financial resources from creditors. Therefore, cooperative size (log of total assets) was our proxy for financial constraint. We ranked all cooperatives from the sample, for each year, according to total assets. Based on Hadlock and Pierce (2010), Behr, Norden and Noth (2013) and Ambrozio et al. (2017), cooperatives positioned in the last (first) four deciles were considered restricted (unrestricted). Thus, fin_con_1 is a dummy variable that assumes value 1 if a cooperative is financially constrained and 0 otherwise.

3.2.2.2 Financial constraint 2 (fin_con_2)

For the second method, we considered a cooperative to be constrained when meeting two criteria: i) negative or zero variation of investment in property, plant and equipment; and ii) negative or zero variation of percentage of remaining shares available to the members (M). Table 1 presents the criteria and formula for each item.

Source: developed by the authors.

Net residuals represent the outcome of the cooperative, that is, all revenues minus all expenses. Residuals available to members express a value that the cooperative makes available to members for distribution, after deduction of legal and bylaw reserves (legal reserve, technical reserve and other reserves, generally allocated to investments) and allocation of the residuals to members’ shares. Cooperatives usually retain residuals use as capital when facing financial frictions (RUSSEL; BRIGGEMAN; FEATHERSTONE, 2018). Therefore, in the first criterion, a zero or negative variation of percentage of residuals allocated to members could indicate that the cooperative is retaining residuals for future investments. In other words, if the ratio between the money distributed to members and the net residuals increases, this may indicate that the cooperative does not need financial resources and can distribute them. This argument resembles the logic of dividend distribution of companies (FAZZARI, HURBARD; PETERSON, 1988; DEMONIER; ALMEIDA; BORTOLON, 2015), since firms avoid distributing money when there are investment needs.

In the second criterion, zero or negative variation of fixed assets indicates that cooperatives avoid investing with internal resources (CLEARY, 1999; DEMONIER; ALMEIDA; BORTOLON, 2015). Both variations (criteria 1 and 2) show that since cooperatives do not have easy access to credit, they do not invest in fixed assets and retain part of their outcome to ensure financial resources for future or unforeseen investment opportunities. Thus, we considered that a cooperative is financially constrained if it meets both criteria. We measured it by a dummy variable, fin_const_2, which assumes value 1 if the cooperative is financially constrained and 0 otherwise.

3.2.3. Control Variables

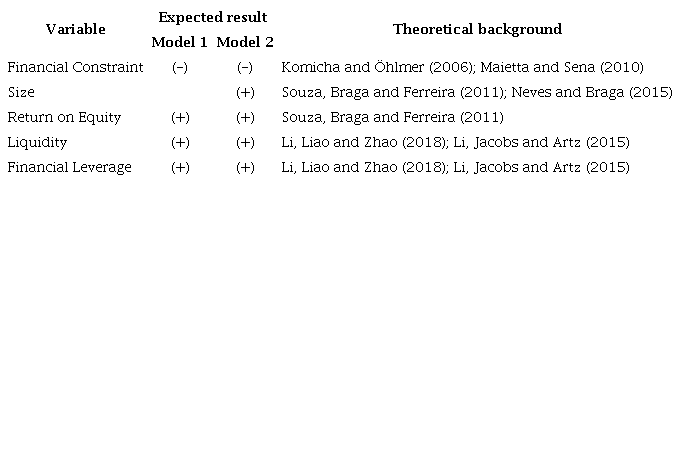

In order to control others factors that could affect technical efficiency, we inserted in the model the following control variables: i) size (size); ii) return on equity (ROE); iii) liquidity (liq); and iv) financial leverage (lev). Table 2 shows all variables, calculation formula and theoretical background.

Source: developed by the authors. Note: † Variable used only in Equation 3, together with the variable fin_const_2.

We introduced the size variable to capture the impact of resource contribution on cooperative efficiency (SOUZA et al., 2011; NEVES; BRAGA, 2015). We introduced ROE because Souza et al. (2011) found it was significant to separate cooperatives between efficient and inefficient ones. We decided to control for liquidity because high liquidity rates can stimulate productivity and consequently efficiency (LI; LIAO; ZHAO, 2018). Lastly, leverage also could reflect credit access of cooperatives (LI; LIAO; ZHAO, 2018) and, in general, leveraged firms tend to be more efficient and productive in their use of assets (LI; JACOBS; ARTZ, 2015; LI; LIAO; ZHAO, 2018).

We highlight that a profitability index, like return on equity, should be interpreted carefully. In general, cooperatives do not aim to maximize profit (LONDERO et al., 2018). However, profit can be considered an important resource, and it could indicate the level of effort of cooperatives to obtain financial resources (CARVALHO; BIALOSKORSKI NETO, 2008).

We used two models to measure the impact of financial constraints on technical efficiency of cooperatives:

In equation 2, financial constraint is measure by cooperative size, so the control variable size does not appear in the model. In equation 3, we measured financial constraint by the two criteria of Table 1, so we inserted size as a control. Table 3 reports all variables and expected signs.

Source: developed by the authors.

4 ANALYSIS AND DISCUSSION OF RESULTS

4.1 SUMMARY STATISTICS

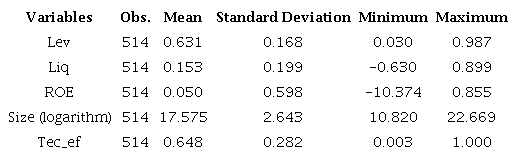

The sample is composed by 68 agricultural cooperatives from Paraná, representing around 83% of all the cooperatives in the state (OCEPAR, 2018). These cooperatives had 67,792 employees and 145,495 members in 2014 (OCEPAR, 2018). They operated with cereals, livestock, manufactured products, milk, horticulture, agricultural inputs, services and others. Table 4 reports the mean, standard deviation, minimum and maximum of the sample. The large dispersion around the mean shows that the cooperatives in the sample were heterogeneous in capital structure and performance.

Source: developed by the authors.

Cooperatives in the sample had, on average, technical efficiency of 64.8%, indicating inefficiency of 35.2%. There was a big difference in technical efficiency level between cooperatives, since the minimum and maximum indexes are 0.003 and 1.0. This result corresponds to prior findings (68.9%) by Souza et al. (2011) in relation to agricultural cooperatives from Paraná. However, Italian wine cooperatives were found to have a technical efficiency level of around 92.0% (MAIETTA; SENNA, 2010), and Italian fishery cooperatives’ score was 88% (MADAU; PURESI; FULINA, 2018). A possible explanation for this difference between the Brazilian and the Italian context may be the number of commodities traded by the cooperatives (single-purpose x multi-purpose)

In a democratic organization, when the heterogeneity of the membership increases, the efficiency of the decision making process decreases (BIJMAN; HENDRIKSE; VEERMAN, 2000).

The cooperatives had average financial leverage of 63.10%. This means that in general, external resources financed 63.10% of assets. Nevertheless, some cooperatives had just 3% financial leverage, while others had 98.7%. This result shows that cooperatives adopt different kinds of capital structure strategies.

Likewise, the liquidity variable has a high standard deviation, and a minimum value of -0,630 and maximum of 0,899. Some cooperatives were relatively large (22.66) and had good profitability (0.855), while others were smaller (10.82) and some had a loss on equity (-10.374). These finding suggests that the cooperatives analyzed during the study period were heterogeneous in their financial and economic strategies. There was variety in the kind of products the cooperatives operated with, so they required different agroindustrial systems, and consequently adopted different investment strategies.

4.2 RESULTS

Before running the panel data analysis, we verified the model’s adequacy in some tests for ordinary least squares (OLS) regression. Table 5 presents the results of the multicollinearity test.

Source: developed by the authors.

The results in Table 5 indicate absence of multicollinearity in the data, that is, all the values were smaller than 10. After that, we tested sample homoscedasticity by the Breusch-Pagan test. Based on this test, we rejected the null hypothesis of constant variance (p-value=0.0055). This means that our data were heteroscedastic so we needed employ the most robust model.

We estimated three robust regression models: fixed effect (FE), random effect (RE) and generalized least squares (GLS). We used the Chow test, Breusch-Pagan LM test and Hausman test to find the most appropriate estimation model for analysis. First, the Chow test rejected the null hypothesis (p-value=0.000), so the fixed effects was more adequate than the GLS estimate. Second, the Breusch-Pagan test reject the null hypothesis (Prob>-chibar2=0.0000), so the random effects model was more adequate for the analysis than the GLS estimate. Finally, the Hausmann test rejected the null hypothesis (Prob>chi2=0.000), so the fixed effects model more suitable than the random effects estimation model.

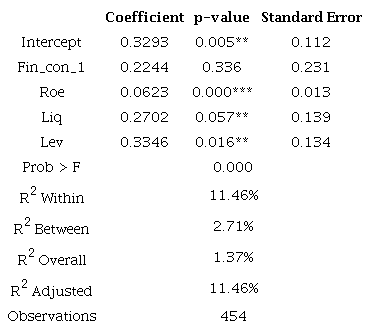

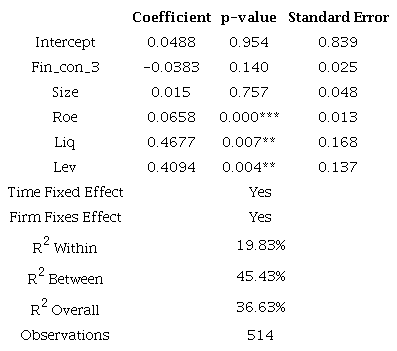

Table 6 reports the results from the robust fixed-effect regression estimated in the first model (Equation 1). We used fin_const_1 as independent variable. The smaller cooperatives were considered financially constrained (positioned in the last four deciles of total assets (logarithmic).

Source: developed by the authors. Note: Significance levels: *** 1%, ** 5%, * 10%.

When using fin_con_1 as explanatory variable, we lost 60 observations3. The results in Table 6 suggest that there is no empirical evidence that the financial constraint explains the variation in technical efficiency for the sample cooperatives. In Model 1, all control variables were positive and statistically significant related to the tec_ef variable.

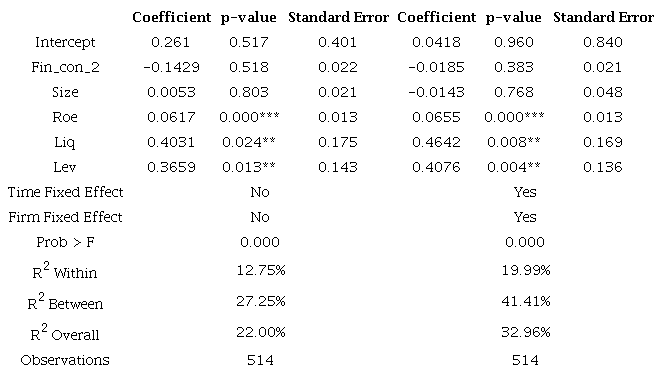

For Model 2, to give greater robustness to the study, we estimated a new regression considering another financial constraint proxy. We also opted to control firm and time fixed effects (testparm - Prob > F = 0.000) in order to eliminate bias caused by unobservable variables that change over time but are constant over entities. Table 7 presents the results.

Source: developed by the authors. Note: Significance levels:*** 1%,** 5%,* 10%.

The number of observations in Model 2 was more than in Model 1 because we used the variable fin_con_2 as a proxy for financial constraint. The results were very similar to those presented in Model 1, that is, there was no statistically significant relationship between financial constraint and technical efficiency. Roe, Lev and Liq presented statistically significant relationships with technical efficiency while size did not.

4.3 SENSITIVITY ANALYSIS

In order to give greater robustness to our previous results, we performed sensitivity test. First, we considered as financially constrained those cooperatives classified as constrained in at least one year from 2004 to 2014 by using the fin_con_2 method. We argue that if a cooperative is financially constrained in one year, probably it will be in others. Second, we performed a regression by controlling the time and fixed effects of time (Prob> F = 0.000). Table 8 reports the sensitivity test results.

Source: developed by the authors. Note: Significance levels:*** 1%, ** 5%, * 10%.

The results in Table 8 corroborate those presented in the previous subsection. The financial constraint and cooperative size did not present a statistically significant relationship with technical efficiency while the control variables presented positive relationships. In summary, our investigation indicates that financial constraint of the cooperatives did not seem to be a determining factor to explain technical efficiency, which does not correspond to prior findings by Maietta and Senna (2010) in relation to Italian wine cooperatives, by Madau, Furesi and Pulina (2018) in relation to Italian fishery cooperatives, and by Skevas and Grashuis (2020) in relation to American grain marketing cooperatives. The first authors found that financial constraint was negatively related with technical efficient, the second showed that bigger cooperatives were more efficient than smaller ones, and the last found that the impact of membership size on technical efficiency was negative and decreased with increasing size. Therefore, our results suggest that, unlike in other countries, in Brazil, specifically in Paraná cooperatives, there is no empirical evidence that the financial constraints of agricultural cooperatives impact the technical efficiency level.

We argue that the Brazilian context explains our results, especially in two points. First, Brazilian agricultural cooperatives are generally multipurpose and trade with more than one type of commodity. In the Italian studies, the cooperatives operated only with wine (MAIETTA; SENNA, 2010) and fish (MADAU; FURESI; PULINA, 2018). This distinction requires different operational structures, and consequently can influence the technical efficiency (GUZMAN; ARCAS, 2008). Since members work with different products in the cooperative and they participate in the decision-making process, there may be disagreements about how to allocate resources in the operational structure. Thus, this heterogeneity of preferences influences the cooperative’s investment behavior (COOK, 2018). In Brazilian agricultural cooperatives, we cannot conclusively argue that the efficient allocation of resources is related to credit restrictions. So, it is necessary to perform additional analyses about this aspect. However, due to lack of data we cannot expand this point.

Second, cooperatives typically do not look to invest in innovation, so they invest less in technology than conventional firms (MAIETTA; SENA, 2010). In 2014, for instance, while 1,206 companies used the tax benefit in Brazilian law to encourage innovation, just four cooperatives did so (CALZOLAIO; MEDINA; FORGIARINI, 2018). Therefore, since there are no strong technological necessities in cooperatives, restricted credit access would not cause severe loss of investment opportunities. In this way, cooperatives would not lose efficiency when facing failure to satisfy immediate investment opportunities. Actually, cooperatives would have more time to structure their internal capital to finance their investments without compromising technical efficiency.

Finally, analysis of the control variables indicated that greater the return on equity, liquidity and financial leverage were associated with higher technical efficiency. Similar results are found by Souza, Braga and Ferreira (2001) when studying Brazilian agricultural cooperatives. They found by cluster analysis that return on equity and the average payment period (debt structure) explained the classification of cooperatives as efficient or not. These results suggest that the use of internal or external resources may have mixed effects on technical efficiency. Li, Liao and Zhao (2018), for example, found that in Chinese companies, the internal and outside financing increase firms’ productivity. If a firm has credit access, the internal financing effect tends to be low, but if the cash flow is not enough, the credit access is important for firms’ productivity (LI; LIAO; ZHAO, 2018).

5 CONCLUSIONS

In our knowledge, there is little empirical evidence about the financial constraint effect on efficiency of agricultural cooperatives. In this study, we aim to contribute to the literature by providing empirical results from Brazilian multipurpose agricultural cooperatives. Our aim was to verify the relationship between financial constraint and technical efficiency. The panel data analysis showed absence of a relationship between the financial constraint and technical efficiency in the two estimated models and in the sensitivity analysis. According to these results, we cannot affirm that financial constraint decreases or increases cooperatives’ technical efficiency score.

Our study contributes to the literature in two ways. First, our results demonstrate that the problem of financial constraint faced by cooperatives might not be a factor that greatly influences their efficiency. Although the literature indicates that financial friction is a problem faced by agricultural cooperatives, in Brazil, specifically in the state of Paraná, this may not impair their operational performance. Second, in methodological aspects, we contribute with a new method to identify financial constraint in agricultural cooperatives. This model was adapted from Demonier, Almeida and Bortolon (2015) and considered the specificities of cooperative dynamics.

5.1 LIMITATIONS AND FUTURE RESEARCH AGENDA

While our study sheds light on technical efficiency of cooperatives, it is possible that these cooperatives adopt strategies and management structures that meet the economic and social needs of their members, but decrease the technical efficiency (SOBOH et al., 2009). Or, on the other hand, these strategies may contribute to efficiency by maintaining the members’ commitment to the cooperatives. This is an open question. Thus, we encourage future analysis about this aspect. Nowadays, the measurement of these effects is still limited by lack of financial data (BENOS et al., 2018). Therefore, we recommend future qualitative analysis such as case studies or surveys with questionnaires and interviews in order to provide more insights into cooperatives’ financial behavior and strategy.

Furthermore, the small size of our sample is a limiting factor. This happened because some cooperatives did not disclose their financial information in the period studied, or when they did, the data were sparse. For further studies, we recommend increasing the sample size to cover cooperatives from other Brazilian states and/or countries.

Finally, if there is no evidence that financial constraint impacts agricultural cooperatives’ efficiency, does it impact other variables? Are there other variables explaining the technical efficiency of cooperatives? Our results and explanations suggest some possible answers. The control variables suggest possibility of mixed effects between financial sources (internal and external) and efficiency. Most of the Brazilian cooperatives investigated traded various commodities, which could affect the technical efficiency score. So, additional analyses are needed concerning this aspect. However, due to lack of data we could expand this point. For future studies, we encourage addressing these questions.

REFERENCES

ALMEIDA, H.; CAMPELLO, M.; WEISBACH, M. S. The cash flow sensitivity of cash. The Journal of Finance, v. 59, n. 4, p. 1777-1804, 2004. doi:10.1111/j.1540- 6261.2004.00679.x

AMBROZIO, A.H.P.; FALEIROS, J.P.; LAGE DE SOUSA, F.L.; SANT’ANNA, A. Credit scarcity in developing countries: an empirical investigation using Brazilian firm-level data. EconomiA, v. 18, n. 1, p. 73-87, 2017. doi: 10.1016/j. econ.2016.12.001

BANKER, R. D.; CHARNES, A.; COOPER, W. Some Models for Estimating Technical and Scale Inefficiencies in Data Envelopment Analysis. Management Science, v. 30, p. 1078-1092, 1984. doi: 10.1287/mnsc.30.9.1078

BEHR, L.; NORDEN, F.; NOTH, F. Financial constraints of private firms and bank lending behavior. Journal of Banking and Finance, v. 37, n. 9, pp. 3472-3485, 2013. doi: 10.1016/j.jbankfin.2013.05.018

BENOS, T.; KALOGERAS, N.; WETZELS, M.; RUYTER, K.; PENNINGS, J. M. E. Harnessing a “Currency Matrix” for Performance Measurement in Cooperatives : A Multi-Phased Study. Sustainability (Switzerland), v. 10, n. 12, p. 1-40, 2018.

BIALOSKORSKI NETO, S. Aspectos Econômicos das Cooperativas. Belo Horizonte: Editora Mandamentos, 2006

BIALOSKORSKI NETO, S. Economia e Gestão de Organizações Cooperativas. 2a ed. São Paulo: Atlas, 2012.

BIALOSKORSKI NETO, S. Ambiente institucional e estratégias de empreendimentos cooperativos. Paper presente at Workshop Internacional de tendências do cooperativismo. Ribeirão Preto - SP, p. 7-24, 2000.

BRANDANO, M. G.; DETOTTO, C.; VANNINI, M. Comparative efficiency of agricultural cooperatives and conventional firms in a sample of quase twin companies. Annals of Public and Cooperative Economics, v. 90, n. 1, p. 53-76, 2019.

BIJMAN, J.; HENDRIKSE, G. W. J.; VEERMAN, C. P. A marketing co-operative as a system of attributes: A case study of VTN / The Greenery International BV. In: Chain Management in Agribusiness and the Food Industry; Proceedings of the Fourth International Conference, 0, Anais...2000.

BRAZILIAN AGRICULTURE MINISTRY. Cooperativismo e Associativismo no Brasil, 2016. Available from: http://www.agricultura.gov.br/assuntos/cooperativismo-associativismo/cooperativismo-brasil

CALZOLAIO, A. E.; MEDINA, H.; FORGIARINI, D. Gestão do Incentivo Fiscal à Inovação em Cooperativas/Management of the tax incentives for innovation by cooperatives. Paper presented at VI Simpósio de Ciência do Agronegócio. Porto Alegre - RS, 2018.

CARVALHO, F. L.; BIALOSKORSKI NETO, S. Indicadores de avaliação de desempenho econômico em cooperativas agropecuárias: um estudo em cooperativas paulistas. Organizações Rurais & Agroindustriais, v. 10, n. 3, p. 420-437, 2008.

CHADDAD, F. R.; COOK, M. L. Understanding new cooperative models: An ownership-control rights typology. Review of Agricultural Economics, v. 26, n. 3, p. 348-360, 2004.

CHADDAD, F. R.; COOK, M. L.; HECKELEI, T. Testing for the presence of financial constraints in US agricultural cooperatives: an investment behaviour approach. Journal of Agricultural Economics, v. 56, n. 3, p. 385-397, 2005. doi: 10.1111/j.1477-9552.2005.00027.x

CHADDAD, F. R.; ILIOPOULOS, C. Control Rights, Governance, and the Costs of Ownership in Agricultural Cooperatives. Agribusiness, v. 29, n. 1, p. 3-22, 2013.

CHARNES, A.; COOPER, W.W.; RHODES, E. Measuring the efficiency of decision-making units. European Journal of Operational Research, 2, p. 429-444, 1978.

CLEARY, S. The relationship between firm investment and financial status. The Journal of Finance , v. 54, n. 2, p. 234-270, 1999. doi: 10.1016/0377-2217(78)90138-8

COOK, M. L. The Future of U.S. Agricultural Cooperatives: A Neo-Institutional Approach. American Journal of Agricultural Economics , v. 77, n. 5, p. 1153-1159, 1995.

COOPERATIVES ORGANIZATION OF PARANÁ. IBGE II: Agropecuária puxa o PIB de 2017, 2017. Available from: http://www.paranacooperativo.coop.br/ppc/index.php/sistema-ocepar/comunicacao/2011-12-07-11-06-29/ultimas-noticias/115843-ibge-ii-agropecuaria-puxa-o-pib-de-2017)

COOPERATIVES ORGANIZATION OF PARANÁ. Cooperativismo Paranaense: Desenvolvimento Sustentável no Campo e Na Cidade, 2015. Available from: http://www.paranacooperativo.coop.br/ppc/images/Comunicacao/2016/folders/Folder_cooperativismo_portugues.pdf

COOPERATIVES ORGANIZATION OF PARANÁ. Cenários do Cooperativismo, 2018. Avaible from http://www.paranacooperativo.coop.br/ppc/images/Comunicacao/2019/download/cenarios_cooperativismo/ramo_agropecuario_fechamento_2018_publico.pdf

DEMONIER, G. B.; ALMEIDA, J. E. F. de; BORTOLON, P. M. O impacto das restrições financeiras na prática do conservadorismo contábil. Revista Brasileira de Gestão de Negócios, v. 17, n. 57, p. 1264-1278, 2015.

DERCON, S. Risk, crop choice and savings: evidence from Tanzania. Economic Development and Cultural Change, v. 44, n. 3, p. 485-513, 1996. doi: 10.1086/452229

FÁVERO, L. P.; BELFIORE, P.; TAKAMATSU, R. T.; SUZART, J. Métodos quantitativos com Stata. Rio de Janeiro: Elselvier, p. 131-142, 2014.

FAZZARI, S., R. G. HUBBARD, AND B. PETERSEN. Financing Constraints and Corporate Investment,. Brooking Papers on Economic Activity 1, 141-195, 1988.

GONÇALVES, R. M. L.; BRAGA, M. J.; FERREIRA, M. A. M. Restrições Financeiras em Cooperativas Agropecuárias Brasileiras. Brasília. Revista Economia, v. 13, p. 647-670, 2012.

GUJARATI, D. N.; PORTER, D. C. Econometria Básica-5. McGrawl-Hill, 2011.

GUZMAN, I.; ARCAS, N. The usefulness of accounting information in the measurement of technical efficiency agricultural cooperatives. Annals of Public and Cooperative Economics , v. 79, n. 1, p. 107-131, 2008.

HADLOCK, C.; PIERCE, J. New evidence on measuring financial constraints: moving beyond the KZ index. Review of Financial Studies, v. 23, p. 1909-1940, 2010. doi: 10.1093/ rfs/hhq009

HANSMANN, H. The ownership of enterprise. London: Harvard University Press, 1996.

HENDRIKSE, G. W.; VEERMAN, C. P. Marketing cooperatives and financial structure: a transaction costs economics analysis. Agricultural Economics, v. 26, n. 3, p. 205-216, 2011. doi: 10.1111/j.1574-0862.2001.tb00064.x

INTERNATIONAL COOPERATIVE ALLIANCE. Plano de ação para uma década cooperativa, 2013. Available from: https://www.ica.coop/sites/default/files/publication-files/blueprint-for-a-co-operative-decade-portuguese-1267863829.blueprint-for-a-co-operative-decade-portuguese

KAPLAN, S.N.; ZINGALES, L. Do investment-cash flow sensitivities provide useful measures of financing constraints? Q. J. Econ. v. 112, p. 169-215, 1997.

KOMICHA, H. H.; OHLMER, B. Influence of Credit Constraint on Technical Efficiency of Farm Households in Southeastern Ethiopia. International Conference on African Development. Center for African Development Policy Research, v. 125, n. 125, p. 1-29, 2007.

LAUERMANN, G. J.; MOREIRA, V. R.; SOUZA, A; PICCOLI, P. G. R. Do Cooperatives with Better Economic-Financial Indicators also have Better Socioeconomic Performance? VOLUNTAS: International Journal of Voluntary and Nonprofit Organizations, p. 1-12, 2018. Disponível em: <http://link.springer.com/10.1007/s11266-018-0036-5>.

LI, Y. A.; LIAO, W.; ZHAO, C. C. Credit constraints and firm productivity: Microeconomic evidence from China. Research in International Business and Finance, v. 45, p. 134-149, 2018. doi: 10.1016/j.ribaf.2017.07.142

LI, Z.; JACOBS, K. L.; ARTZ, G. M. The cooperative capital constraint revisited. Agricultural Finance Review, v. 75, n. 2, p. 253-266, 2015.

LONDERO, P. R.; FIGUEIRA, L. M.; STANZANI, L. M. L.; MARTINS, E. Inflationary distortions in cooperatives. BASE-Revista de Administração e Contabilidade da Unisinos, v. 15, n. 3, p. 161-177, 2018. doi: 10.4013/base.2018.153.01

MADAU, Fabio A.; FURESI, Roberto; PULINA, Pietro. The technical efficiency in Sardinian fisheries cooperatives. Marine Policy, v. 95, p. 111-116, 2018.

MAIETTA, O. W.; SENA, V. Financial constraints and technical efficiency: Some empirical evidence for Italian producers’ cooperatives. Annals of Public and Cooperative Economics , v. 81, n. 1, p. 21-38, 2010.

NEVES, M. D. C. R.; BRAGA, M. J. Eficiência financeira e operacional em cooperativas participantes do programa de capitalização de cooperativas agropecuárias (PROCAP-AGRO). Organizações Rurais & Agroindustriais , v. 17, n. 3, 2015.

NICKELL, S.; NICOLITSAS, D. How does financial pressure affect firms. European Economic Review, v. 43, n. 8, p. 1435-1457, 1999.

ONGORE, V.O.; KUSA. G.B. Determinants of Financial Performance of Commercial Banks in Kenya. International Journal of Economics and Financial Issues, v. 3, n. 1, p. 237-252, 2013.

OTTAVIANO, G. I.; SOUSA, F. L. Relaxing credit constraints in emerging economies: The impact of public loans on the performance of brazilian manufacturers. International Economics. V. 154, p. 23-47, 2017. doi: 10.1016/j.inteco.2017.11.002

PORTER, P. K.; SCULLY, G. W. Economic efficiency in cooperatives. The Journal of law and economics, v. 30, n. 2, p. 489-512, 1987.

RODRIGUES, J. A.; LAUERMANN, G. J.; MOREIRA, V. R.; FERRARESI, A. A.; SOUZA, A. Estrutura de Capital e Peculiaridades Regionais nas Cooperativas Agropecuárias do Paraná-Brasil. Revista de Economia e Sociologia Rural, v. 56, n. 2, p. 213-224, 2018. doi: 10.1590/1234-56781806-94790560202

RUSSELL, L. A.; BRIGGEMAN, B. C.; FEATHERSTONE, A. M. Financial leverage and agency costs in agricultural cooperatives. Agricultural Finance Review, v. 77, n. 2, p. 312-323, 2017. doi: 10.1108/AFR-09-2016-0074

SEXTON, R. J.; ISKOW, J. Factors critical to the success or failure of emerging agricultural cooperatives (Vol. 88, No. 3). Davis: Division of Agriculture and Natural Resources, University of California, 1988.

SKEVAS, Theodoros; GRASHUIS, Jasper. Technical efficiency and spatial spillovers: Evidence from grain marketing cooperatives in the US Midwest. Agribusiness, v. 36, n. 1, p. 111-126, 2020.

SOBOH, R.; GIESEN, A. O. L. G.; DIIK, G. V. Performance Measurement of the Agricultural Marketing Cooperatives: The Gap between Theory and Practice. Review of Agricultural Economics , v. 31, n. 3, p. 446-469, 2009. Disponível em: <https://academic.oup.com/aepp/article-lookup/doi/10.1111/j.1467-9353.2009.01448.x>.

SOBOH, R.; LANSINK, A. O.; VAN DIJK, G. Efficiency of cooperatives and investor owned firms revisited. Journal of Agricultural Economics , v. 63, n. 1, p. 142-157, 2012.

SOUZA, Uemerson Rodrigues de; BRAGA, Marcelo José; FERREIRA, Marco Aurélio Marques. Fatores associados à eficiência técnica e de escala das cooperativas agropecuárias paranaenses. Rev. Econ. Sociol. Rural, Brasília , v. 49, n. 3, p. 573-597, Sept. 2011. Available from <Available from http://www.scielo.br/scielo.php?script=sci_arttext&pid=S0103-20032011000300003&lng=en&nrm=iso>. access on 13 Dec. 2019. Doi: 10.1590/S0103-20032011000300003.

XABA, Sharon Thembi; MARWA, Nyankomo; MATHUR-HELM, Babita. Efficiency evaluation of agricultural cooperatives in Mpumalanga. African Journal of Economic and Management Studies, v. 11, n.1, p. 51-62, 2019.

Notes

Author notes

Endereço dos Autores: Avenida Bandeirantes, 3900 Bairro Monte Alegre Ribeirão Preto, SP - Brasil CEP: 14040-905