Artigo

Brazilian agribusiness amid the turbulence provoked by Covid-19: a hope for the stock market?

Agronegócio brasileiro em meio à turbulência provocada pela Covid-19: uma esperança para o mercado de capitais?

Cassiana Bortoli cassianabortoli@gmail.com

Elisane Teresinha Brandt elisane_brandt@hotmail.com

Ivanildo Viana Moura ivm.bh.mg@gmail.com

Cláudio Marcelo Edwards Barros claudiomedwards@hotmail.com

Cassiana Bortoli cassianabortoli@gmail.com

Elisane Teresinha Brandt elisane_brandt@hotmail.com

Ivanildo Viana Moura ivm.bh.mg@gmail.com

Cláudio Marcelo Edwards Barros claudiomedwards@hotmail.com

Brazilian agribusiness amid the turbulence provoked by Covid-19: a hope for the stock market?

Enfoque: Reflexão Contábil, vol. 41, no. 3, pp. 157-175, 2022

Universidade Estadual de Maringá

Received: 12 November 2020

Revised document received: 08 February 2021

Accepted: 13 January 2021

ABSTRACT: This study aimed to investigate the effects of the COVID-19 crisis on the performance of the stocks of Brazilian agribusiness. Among the main activities of Brazilian agribusiness, grain production stands out worldwide. Thus, we selected the company SLC to represent this segment. And, from Thomson Reuters, we selected its peer companies: Ambev, JBS, BRF, Cosan Logística, Marfrig and São Martinho. We used the event study methodology and multivariate linear regression. The results showed that SLC performed well in the event window, while its peers experienced great volatility. The OLS regression confirmed that SLC was positively differentiated from other companies with daily trading in the period.

Keywords: COVID-19, Agribusiness, Financial Market, Stock Performance.

RESUMO: Este trabalho teve como objetivo investigar o efeito da crise do COVID-19 no desempenho das ações do agronegócio brasileiro. Entre as principais atividades do agronegócio brasileiro, a produção de grãos se destaca mundialmente. Assim, selecionamos a empresa SLC para representar esse segmento. E, a partir da Thomson Reuters, selecionamos as empresas pares: Ambev, JBS, BRF, Cosan Logística, Marfrig e São Martinho. Utilizamos a metodologia de estudo de eventos e regressão linear multivariável. Os resultados mostraram que a SLC obteve um bom desempenho na janela de evento, enquanto seus pares experimentaram de grandes volatilidades. A regressão OLS, confirmou que a SLC se diferenciou positivamente das demais empresas com cotação diária no período.

Palavras-chave: COVID-19, Agronegócio, Mercado Financeiro, Desempenho de Ações.

1 INTRODUCTION

In Brazil, according to the Ministry of Health (MINISTÉRIO DA SAÚDE, 2020), the first COVID-19 case was confirmed in February 26, 2020. In the same date, measures to contain the disease in the national territory were initiated. As a result, in different moments of the month of March, state governments have decreed a quarantine in their territories. That led to a greater impact in economy, which can be observed through its reflexes: the rise in the value of the dollar when compared to the Brazilian real, the increased unemployment rates, diminished industrial production, increased country risk, and projected GDP (Gross Domestic Product) drops. According to the note divulged by the Ministry of Economy (MINISTÉRIO DA ECONOMIA, 2020), the economic impact of coronavirus is directly related to the determination of social isolation, and can be decomposed in: i) immediate impact when faced with restrictions to the production and to consumption; ii) length of the recovery period; and iii) impact on the long-term trajectory of the economy. The impact was also observed in the diminution of formal employment, since, when part of the commerce in the country was closed, 1.1 million job opportunities were terminated during March and April, according to data from the CAGED (the General Records of Employed and Unemployed People) (G1, 2020c). In addition to the staggering unemployment numbers, data published by the IBGE (the Brazilian Institute of Geography and Statistics) indicate that the Brazilian GDP fell 1.5% in the first trimester of 2020, when compared to the last trimester of the previous year (IBGE, 2020).

Considering so many negative impacts of the international crisis provoked by COVID-19, the Brazilian trade balance was also impacted, but the agribusiness sector has been showing outstanding signs in the national economy. Brazil had a reduction of 27.1% in nearly all products of the commercial balance, with the exception of products from agribusiness, which presented an increase in their total balance. Additionally, when the sector is analyzed in isolation, a significant increase can be perceived in exportations, from 42.2% in 01/2019 to 55.8% in 04/2020, and a 16.7% reduction of importations, considering the same period (SISTEMA OCEPAR, 2020). This data reinforces the importance of the sector, both nationally and internationally.

Brazil is among the greatest producers of grains throughout the world, meaning that the international supply crisis can be seen as a great opportunity for the country to anticipate and/or increase its exportations (CEPEA, 2020). Brazil, a worldwide provider of commodities, lead the coalition of developing countries in the agricultural negotiations in the World Trade Organization (WTO), which contributes for its growth as an emerging economy (ANDRADE, 2016). This position is due to the expansion of the production scale of the technological restructuring, which made it possible for the Brazilian agribusiness to reach worldwide markets (HALL; MATOS; SILVESTRE; MARTIN, 2011; AMANOR; CHICHAVA, 2016; MUELLER; MUELLER, 2016). These factors lead the Brazilian agribusiness sector to positively sustain the trade balance with its exportations. In addition, as highlighted by Sui and Sun (2016), there is a belief that the demand of worldwide trade may positively impact in the performance of the companies of the main exporter countries. These authors also underline that globalization has been increasing the speed of the flux of internal trade, but developing countries have difficulties due to the strong interference of the exchange rates in the capital market.

Therefore, the advance of the agribusiness in Brazil is reported as the personification of the most progressive elements of a developing economy (IORIS, 2015; SCOONES; AMANOR; FAVARETO; QI, 2016), considering the use of agriculture as a promising strategy for development. Considering these factors, the large cultivable areas, the favorable climate, and the availability of water made Brazil into one of the main producers and exporters of agricultural commodities (MUELLER; MUELLER, 2016; SISTEMA OCEPAR, 2020). The increase in the exportation of agricultural products also reflects the capacity of Brazil of increasing its production in cultivable areas, with the technification of production systems, which strengthens the role of the country in world markets (PEREIRA; MARTHA JR; SANTANA; ALVES, 2012).

The expansion of Brazilian agribusiness started in the 2000s, when many companies perfected their main activities and expanded their production scale, becoming some of the largest agribusiness companies in the world (AMANOR; CHICHAVA, 2016). Among them, companies whose capital is traded in the stock markets stand out, such as SLC Agrícola SA, which is one of the largest agricultural Brazilian producers and commodity exporter, exporting products such as: soy, cotton, and corn. There are few other peer companies who work in the agricultural field in Brazil and trade their stocks in the stock market. They are: São Martinho S.A., BRF S.A., JBS S.A., Cosan S.A., Marfrig Global Foods S.A., and Ambev S.A. (as classified by Thomson Reuters). This setting favors an investigation of the resilience and magnitude of the Brazilian agribusiness, when considering contingent situations, which justifies this study, considering the relevance of the theme in the current context, that of a pandemic. The magnitude of the Brazilian agribusiness has been shown, as was its uniqueness when compared to other sectors which are suffering in the midst of this crisis. Considering that, this work aimed to investigate the effect of the crisis that was provoked by Covid-19 in the performance of the stocks of Brazilian agribusiness.

2 THEORETICAL FRAMEWORK

In December 2019, the first case of COVID-19 was documented in the city of Wuhan (AYITTEY, F. K., et al, 2020). This is a viral disease that has been leading countries to impose a series of social distancing measures to contain its outbreak (NICOLA et al., 2020). As a result, the workforce in all economic sectors has diminished, which, in addition to affecting companies, generates the loss of jobs (NICOLA et al., 2020; SHARIF; ALOUI; YAROVAYA, 2020). Therefore, these measures raise the potential of the global pandemic to destroy means of survival, businesses, industries, and economies. In this context, the new coronavirus is likely to impact the economy of the world, bringing many countries into recession and, possibly, into economic depression (BARUA, 2020). As a result, there have been many uncertainties about the future economic conditions, and, consequently, consumption and investments, both national and international, have declined (OZILI; ARUN, 2020).

The COVID-19 crisis emerged as a worldwide disaster, which has been affecting profoundly the performance of the global economy and threatens the survival of companies throughout the world (WANG; HONG; LI; GAO, 2020). As a result, comparisons are being made to the 2008 financial crisis (SHARIF; ALOUI; YAROVAYA, 2020) and to the great depression from the 1930s, since the stock markets are having the worst declines in decades (IQBAL et al., 2020). This can be observed in the diminution of the market value of companies. The impact in global stock markets generated a loss of US $ 6 trillion from February 24 to February 28; the S&P 500 index lost more than US$ 5 trillion of its value in one week in the USA; the ten largest S&P 500 companies, combined, lost more than US $ 1.4 trillion (OZILI; ARUN, 2020). These circumstances show the macroeconomic impact that countries are experiencing due to the outbreak (BARUA, 2020). The effects can be summarized when divided in: primary sectors, including the extraction of raw materials; secondary sectors, which produce finished products; and tertiary sectors, which include all service provision sectors (NICOLA et al., 2020). Therefore, the impact of the crisis is felt in all economic sectors and, the isolation measures directly affect the GDP of each country from the principal economies, which are expected to lose approximately 2 percentage points in their annual growth rate (CHAKRABORTY; MAITY, 2020). Bloomberg Economists have predicted, through a modeling aimed at estimating the expected losses for different countries in the world, a probable drop of nearly 0.42% to the GDP of the world during the first trimester of the year (AYITTEY et al., 2020). Considering this, COVID-19 has been shown not only to have a disturbing effect on human life, but also to have the potential to provoke economic deceleration (CHAKRABORTY; MAITY, 2020).

Considering the setting of COVID-19, Nicola et al. (2020) observed that the worldwide outbreak impacted the primary, secondary, and tertiary sectors. And that the demand for food increased due to the panic of the population, who started stocking produce, contributing to the resilience of agriculture, which is part of the primary sector. Furthermore, many countries in the world need to import food, be it due to management, climate, or population conditions. Therefore, there are two strong indicators of worldwide agriculture which can lead investors to intuit the potential acceleration of Brazilian agribusiness, especially with regard to the production of grains: (1) the country has one of the greatest trade balances when it comes to this activity, and positively signals the growth projects of the agricultural production for the next years (EMBRAPA, 2020b); and (2) the government of some countries limited or restricted the exportation of foods, due to the insecurity generated by the pandemic and the consequent scarcity of foods (CADILLO-BENALCAZAR; RENNER; GIAMPIETRO, 2020). This fact is a reflex of the importance of the contribution of the country to diminish world hunger (PEREIRA et al., 2012; MUELLER; MUELLER, 2016).

Despite the growing importance of Brazilian agribusiness to placate the food needs of the world (EMBRAPA, 2020b) and of the capacity to increase the production per cultivable area in the next years, investors can produce volatility in the Brazilian stock market for companies from the sector. The uncertainties of the event have generated nervousness in the investors and, as a consequence, turbulence in the market, which is in accordance to the Contrast Hypothesis (TIEGEN; KEREN, 2003). The reactions of investors tend to produce abnormal positive returns (negative), followed by negative ones (positive). At the end of the event, Brazilian agribusiness is expected to have the ability to reap positive cumulative abnormal returns, despite the extremely volatile events produced by COVID-19. From this perspective, the economic importance and the political power of agribusiness should not be underestimated, since, throughout many decades, the sector was the center of the growth trajectory of Brazilian economy (SCOONES; AMANOR; FAVARETO; QI, 2016; EMBRAPA, 2020b). In addition, considering the current settings, it presents itself as a possible hope for the country, in the diminution of the negative economic impact caused by the COVID-19 crisis.

3 METHODOLOGY

To achieve our objective, we adopted the event studies methodology. To do so, the circuit break that took place in the B3 Brazilian stock exchange in March 18, 2020, was used as the event of interest. The date of the event was chosen due to the 10.26% drop in Ibovespa, as a consequence of the uncertainty provoked by COVID-19 in the Brazilian capital market. A window of 21 days was considered, formed by the last 10 days of trading floor open outcry before the event, and the 10 days that followed it, since the circuit break happened after a series of occurrences in the financial market and several containment measures announced after the date, such as: 03/11/2020, the World Health Organization (2020) announces the coronavirus pandemic; 03/16/2020 circuit breaker after announcements from the Federal Reserve (FED) and other central banks about measures regarding the size of the impact of the pandemic in the economy. From 03/17/2020 to 03/23/2020, many teaching institutions adhered to the suspension of in-person classes; from 03/17/2020 to 03/24/2020, the states Santa Catarina, Rio Grande do Sul, São Paulo and Rio de Janeiro declared a quarantine, and other states adhered to measures of social isolation and distancing; and in 03/30/2020, there were new rumors of a possible circuit breaker, due to the nervousness in the market. We have found indicators that the agribusiness sector, especially that of seeds, is developing well, despite the turbulent economic situation. As a result, the company SLC Agrícola AS, which is representative among Brazilian agricultural producers, was used to investigate the possible positive effects of COVID-19 for this activity in the Brazilian financial market, which is considered to be a developing market. We also seek to compare its performance with that of its peers. Table 1 shows the companies that were considered for the analysis.

The companies analyzed, presented in Table 1, have been classified as peers, in accordance to Refinitiv®. In this case, all the companies are understood to operate in the agribusiness field. However, it should be highlighted that there are intrasectoral differences, that is, despite offering activities that are related to the agribusiness, SLC Agrícola, for instance, operates in grain production, while companies such as JBS S.A., BRF S.A., Marfrig Global Foods S.A. operate in the production of meats, an activity which depends on the production of grains as the base for the feeding of the animals. As a result, all companies considered in Table 1 present, in some degree, a relationship of intrasectoral interdependence, even with distinct activities.

Note: This table shows the corporate name of the company, their appropriate codes of negotiation (outcry) in the Brazilian stock exchange, their classification according to their main sectoral activity, and a short description of the company and their operations. This information was acquired from Refinitiv®, and adapted. Source: Developed by the outhors.

As a parameter for the expected performance in the stock markets, we used the values of the Ibovespa (made up of a portfolio of companies from the Brazilian stock market), and, using it, we calculated the expected returns, the abnormal returns, the cumulative abnormal returns, as well as the T-test for the respective abnormal returns. To do so, a sample of 170 companies that presented daily quotations was considered. To evaluate the impact of the event, the abnormal return for the "i" company was measured, calculated by:

Where: ARit represents the abnormal return, Rit represents the actual return, and E (Rit) represents the normal or expected return for each t period. Finally, Xt is the information that conditions the normal performance model, obtained by the constant mean, which assumes a linear relation between the return of the market and the return of the title, using an estimation period of 252 days. A similar methodology was used by Barros, Lopes and Almeida (2019), with small variations such as the size of the estimation and event window, which are consistent with the triggers of the analyzed events.

The cumulative abnormal return (CAR) is the measure of abnormal returns during the event window (T1; T2) around the day of the event t=0, where (T1; T2) = (-10; +10), calculated by:

Additionally, we carried out a regression analysis according to what follows:

In this model, i represents the companies within the sample. DUMMY represents the dummies regarding the analyzed company, since six models were regressed, which were SLC, the company that is the subject of this study, and its peers. The logarithmic variable SIZE indicates size, and variable PTB represents Price to Book, ROA represents returns on actives, and CASH corresponds to the cash value or equivalent. All data used in this study was extracted from the Refinitiv® database.

4 RESULT ANALYSIS AND DISCUSSION

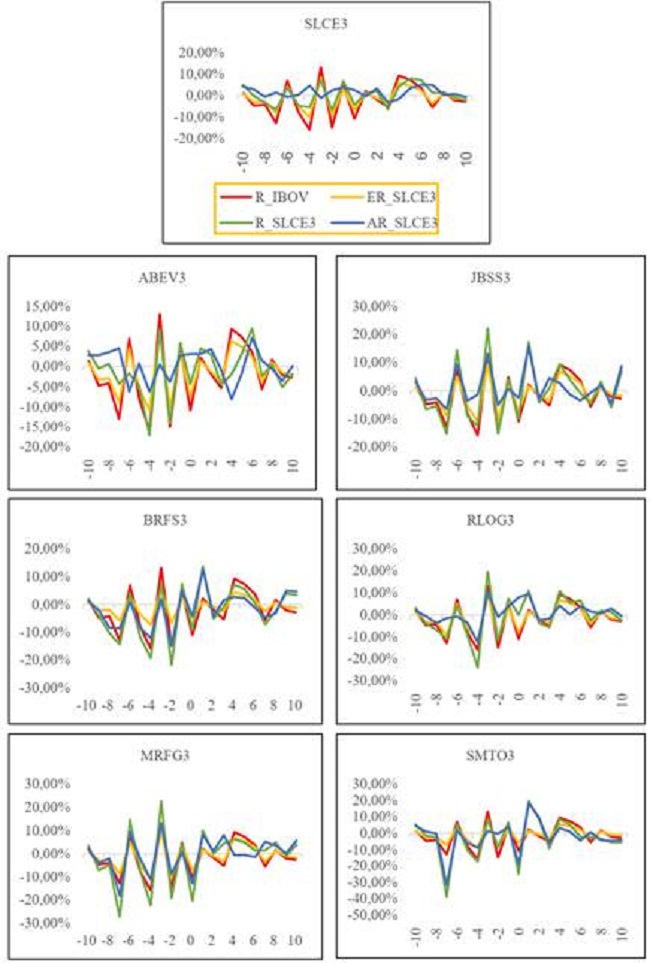

The technique of event studies basically works with a statistical analysis with regard to the performance of the company. Therefore, it becomes necessary to recognize the portion of systematic risk to which every company is exposed. To do so, an estimation window of 252 days from the effective return of the company and of Ibovespa. Based on this data, it is possible to find two other important elements: the value regarding the expected return and, consequently, that of the abnormal return. Understanding these concepts is necessary to explore the context of a new event that may influence them. As a result, Figure 1 suggests an analysis of the individual performance of companies of Brazilian agribusiness, obtained from the interpretation of the movement observed in each of the graphs shown.

It should be highlighted that the presentation of the caption of Figure 1 was inserted only in the graph of SLC, since the others share the same logic in the use of colors. Red represents the actual return from Ibovespa in the period, thus showing the same movements in all graphs of the figure, since it is the same event window. Yellow represents the expected return for each company, considering the general market movement and the respective systematic risk. The green represents the effective return, that is, the actual performance considering the reflexes of the reactions of their investors. Finally, blue represents the abnormal return, since it represents the difference between the expected return and the actual, real return. Furthermore, in a later moment (Table 2), a test in the difference of means, a T-test, was necessary, to validate the relevance of said difference, that is, to say whether there are statistically observable differences.

Figure 1

Individual performance of the Brazilian Agribusiness Companies.

Source: Developed by the outhors.

The Beta was calculated to find the systematic risk found for each company in the sample: SLC = 0.63; AMBEV = 0.68; JBS = 0.70; BRF = 0.46; Cosan = 0.72; Marfrig = 0.71; and São Martinho = 0.56. Systematic risks correspond to the system or market in which the company is inserted, and it is not possible to control them, since they depend on exogenous variables that cannot be manipulated. Each company will go through variations in their performance according to their degree of exposure to risk. The Beta of the company, indicates, therefore, the degree of exposure to this risk. Therefore, according to the degree of exposure, the company has conditions to estimate the return expectations, considering the risks that cannot be controlled by them. If all investors achieved perfect rationality and had the same level of information, they would interpret it equally, and, as a result, the effective return would be identical to the expected return at the moment an event takes place, in a way that the lines of the expected return (yellow) and the actual return (green) would overlap. Thus, it would not be possible to obtain positive or negative abnormal returns, since there would be no difference. Therefore, the blue line would be over the "0" axis.

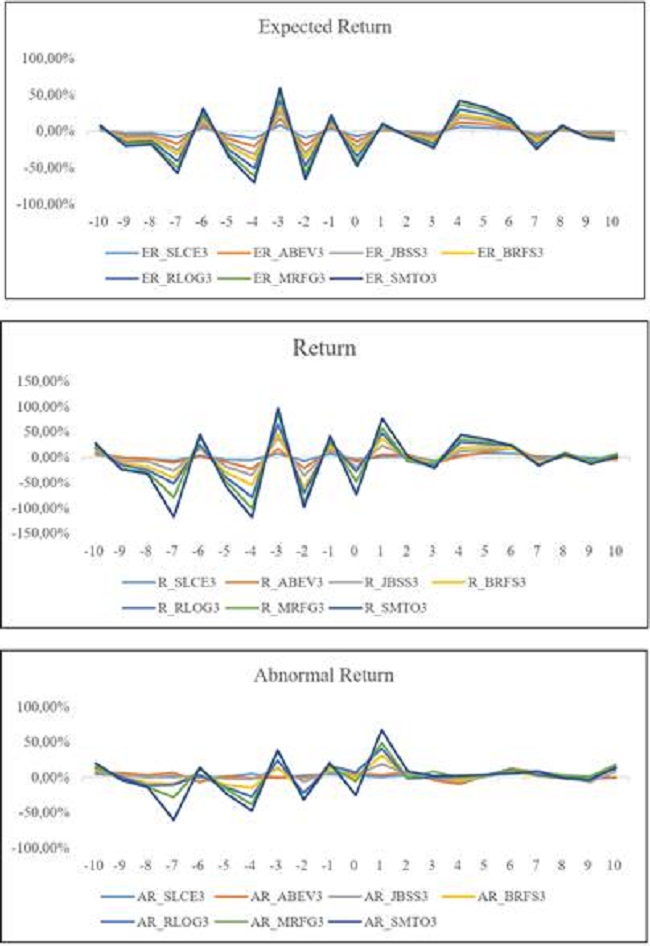

The scientific community recognizes that the levels of rationality and the access to the entirety of available information are different between investors and can affect the capacity of individual interpretation. Therefore, the decision can be delayed or anticipated, depending on the degree of exposure to the uncertainty. This is why this study considers an event window including previous and later days to the date of the event. Considering the SLC as the example for the analysis and considering that this is the most interesting company for this study, it is possible carry out some expressively useful observations. First, the visual movement of the yellow line is, approximately, half of the movement observed in the red line. When the beta information from the company is observed, we consider that the movement is, actually, of 63% of the market movement, reflecting the risk estimation in the return expected by the company. Therefore, the company does not expect to overcome the mean of returns offered by the market. It also does not wish to reach the levels of mean losses presented in the market. Furthermore, it is possible to interpret that, the higher the betas, the lower the volatility attributed to the company, which demonstrates higher stability in normal market conditions. Secondly, the green line seems to show that, when the market declined (red line), the company did not lose as much as expected (yellow line). However, in moments in which there were favorable movements (above the "0" axis), the green line is close to the expected return (yellow line), between the expected return and the market return (red line), sometimes overcoming the expected return. During both drops and gains, when discrepancies were observed between expected return and actual returns, the company shows to have a potential positive statistical significance. Lastly, and complementing the analyses above, the blue line traces a path that is very close to the "0" axis and, when a larger distance is observed, it is shown to be superior to the axis, reinforcing the idea that few dates obtain positive abnormal returns. The description of this analysis makes it possible to perform others, similar to the other companies included in the sample. However, as a product of analysis, when the blue line of the graphs of peer companies is briefly observed, it can be noted that the distance from the "0" axis is bigger, both in the up and in the downside, showing high volatility and the possibility of significant positive and negative abnormal returns throughout the window of events. To complement the analysis and provide a brief visual analysis that allows us to compare the performance of the agribusiness companies listed in the Brazilian stock exchange, Figure 2 was elaborated.

In addition to the calculation carried out to find out the AR and the CAR, the consistency of the abnormal return for SLC and its peers was found using the T-test, and the values are presented in Table 2.

Figure 2

Comparative performance of the Brazilian Agribusiness Companies.

Source: Developed by the outhors.

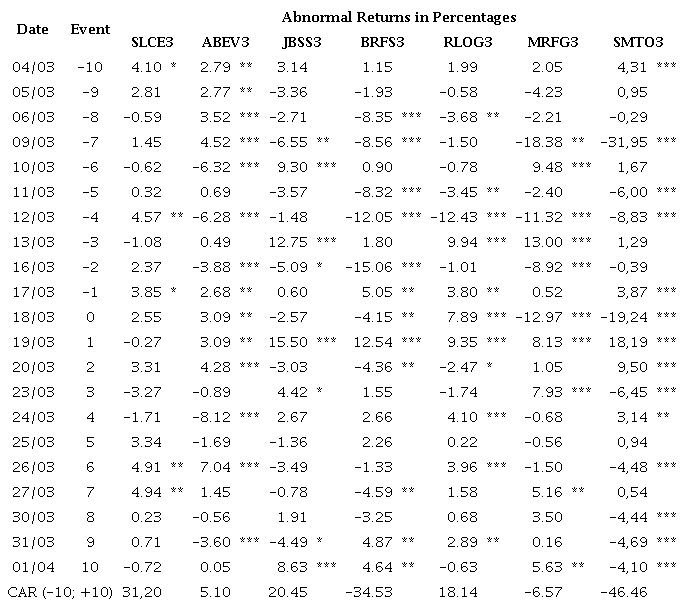

Note: Table 2 shows the abnormal returns in percentages of the event window (-10 to +10). T-test was calculated with regard to the abnormal return, and we replaced the results whose values were ≥ 2.27, ≥ 1.96 and ≥ 1.64, which denote a statistical significance with a level of 1%, 5%, and 10%, represented by a superposition of asterisks: ***, **, *, respectively. Source: Developed by the authors.

Table 2 shows that the agribusiness sector had positive and/or negative abnormal returns around the dates of the event, which shows the volatility of the sector when faced with the uncertainty provoked by COVID-19. Still, the reaction of investors can be noted with greater intensity in the SLC S.A. peers, since this company had a significant abnormal return in 5 out of the 21 dates, and these returns were positive, meaning that they reached a 31.20% cumulative abnormal return in the period. The stocks of SLC did not significantly lose market value in any day of the event window, and only their upticks were relevant. Additionally, it can be noted that, when Ibovespa dropped, SLC did not do so as much. However, when Ibovespa emerged, SLC had superior and expressive highs. This behavior was not observed in its peer companies, which denotes a bit of indifference, that is, transmits an idea that SLC was nearly untouched by the volatility pressure of the dates surrounding the selected date (the day zero) of this study. As a result, investors who had their stocks in their portfolios perceived it as an extremely protective active. In 03/04, when SLC presented a positive abnormal return (AR: 4.10%; Sig. 10%), the Central Bank of the USA announced a small diminution in the interest rates, to mitigate the impact of coronavirus. This decision softens the worldwide economic pressure, especially for emerging and developing countries, such as Brazil. That is why investors that have the USA in their eyesight and economies that make up the group of the seven most industrialized countries in the world (the G7) can exploit the possibility of investing in more attractive economies. With this regard, Brazilian agribusiness, especially in the field of grains, has been attracting the attention of the globe, since it is the third largest exporter, the second largest soy producer, and the first in the world's commercial balance. The sector is even responsible for the elevation of the Brazilian commercial balance amidst the economic crisis generated by COVID-19 (CEPEA, 2020; EMBRAPA, 2020a; SISTEMA OCEPAR, 2020). These results evidence the good moment SLC and the grain sector are going through, as it traverses the turbulence of the stock exchange "unscathed", and, when it was under stress, showed optimist investors, such as in its 4.57% abnormal return (Sig.: 5%) in the very date the pandemic was declared 03/12 (WORLD HEALTH ORGANIZATION, 2020). It stands out that the activity of producing grains is already carried out in social isolation, meaning that work in the fields did not stop, since the activity is seen as indispensable.

Cosan Logística S.A. is considered to be a peer company in the agribusiness, despite being a railway company, because of the items it transports. The company operates with stretches of the national railroad network that are considered to be the agribusiness exportation passageway, which mainly carry: corn, soy, sugar, soy bran, and diesel, in this order of relevance, defined according to the amount of tons of each that are transported. Furthermore, in 2019, the Brazilian government ceded new segments of the railroad network to the company Rumo, part of the Cosan group, which will be used, especially, to transport cargo that originates from agriculture, for up to 30 years of operation, at some points (PPI, 2020). In Brazil, the federal government cedes the rights to explore the railroad network to private enterprises, so that companies expressively invest in the maintenance and expansion of the railroad network. However, despite the territory extension, the railroad network is still small, which delays the development of the agribusiness sector. Therefore, the disposal of the harvest has been taking place, especially, through road transportation, which leads to high costs, delays in the delivery of produce, a greater risk of losing the goods being transported, and a greater amount of gas emissions, being a superior environmental passive when compared to railway transportation. Since 2019, the Brazilian government has been increasing railway concessions. However, since there are few railway transportation companies, there is no competition, and the impact is little in the cost of agricultural products, though it generates benefits in other aspects. Despite the evident need of improving the segment, we have found that, in general, Brazil had no serious problems in the distribution of commodities to the ports, guaranteeing exportation. Therefore, the increase in exportations leads to greater expectations with regard to the use of the railways, and the expansions expected for the next years are welcomed by the agribusiness sector, generating a shared good performance between the agribusiness and railway transportation sectors, which can be observed by the abnormal return of 18.14% of the company in the period.

The investors of Ambev S.A. were intensely nervous during the event window, leading the company to present negative and positive abnormal returns in 14 out of the 21 days analyzed (9 events with positive abnormal returns and 5 with negative abnormal returns). In the peak of national nervousness with the new coronavirus, the company became aware of the high demand of alcohol gel (used to clean the hands and prevent infection), and announced, in 03/17/2020, the production of 1.2 million of alcohol gel units, which were destined for donation to public hospitals, Federal Universities, and private individuals. This attitude may have influenced the positive reaction of the market for the four consecutive days of the announcement (17, 18, 19 and 20 of March), since it was a widely addressed subject in the national media, in addition to being publicized in the website of the company (AMBEV, 2020). In 03/24, the company had a negative balance with regard to its performance in the stock market. However, at the end of the same day, it announced a partnership with two other companies to provide 100 new beds to a municipal hospital (AMBEV, 2020). The negative reaction did not take place in the 25th, and was not significant in the 26th, presenting a positive abnormal return (T-test: 5.18; Sig.: 1%). In general, despite the turbulent period, Ambev had a positive abnormal performance of 5.10%. There were no declines in the price of grains and sugar cane in the period (despite the fall in the oil price, which could increase the offer of ethanol, since it is transposed from biofuel production). The opposite happened: prices rose. However, this result does not show the growth of the company, but the fact that it declined less than expected for the period, considering the systematic risk of the situation in which it is inserted (Market Beta: 0.68). The beer segment has been facing difficulties since the 2015 crisis, and its performance has been reflecting on the financial market through the devaluing of the company stocks.

Another company that depends on sugar cane as raw material, and which was considered in our sample, is São Martinho S.A. However, the event window was quite turbulent for this company, for, essentially, two reasons: (1) oil prices dropped, which directly impacts the price of fuel, meaning that it is not economically viable to fuel vehicles with ethanol, since it becomes more expensive than fuels that are produced using oil; and (2) fuel is less consumed due to isolation measures that started after the date of the event (03/18), since many companies started to operate in home-office and people started to use transportation only in cases of extreme need. The price of oil barrels reached US$ 25.22 in the first half of the month of March, due to a dispute, in the market, between Russia and Saudi Arabia, with regard to the commodity. As a result, the mean price was US$ 55.70, the lowest price in the last 18 years. In 03/19, oil prices were booming, since the USA announced that it would get involved in the commercial dispute, a relief for companies that produce ethanol, due to the return of the competition with the fossil fuel. However, the hopes of recovery were shattered fast, at the beginning of the next week (03/23), when educational institutions in the country adhered to the suspension of the school calendars or to carry them out in remote activities, while many companies adopted home-office practices to reduce the flow of people and, consequently, diminished fuel consumption (G1, 2020a). Therefore, during the harvest of sugar cane, many companies in this industry prioritized the production of sugar and its by-products as opposed to ethanol. However, some companies cannot convert in such a manner, due to the structure of their factories, and to the fact that these products are aimed at different markets. As a result, the increase in the production of sugar led to a greater offer of the product and to a possible diminution in prices. That is because this item has a place in the international market, in which anticipated supply purchases are taking place due to COVID-19. In this context, the company presented returns that are much lower than the expected by the investors in the period, as expressed in a negative cumulative abnormal return of 46.46%.

The segment of meats and meat-products is represented by three publicly traded companies: JBS S.A., BRF S.A., and Marfrig Global Foods S.A. As a result, this is the agriculture segment with the most representation in the Brazilian exchange. Despite acting in the same segment, these companies did not have similar performances at the end of the period. BRF and Marfrig, which attempted to merge in 2019 (G1, 2020b), presented negative abnormal returns of 24.53% and 6.57%, respectively, in the event window analyzed. JBS, on the other hand, had a positive abnormal performance of 20.45%. JBS stands out when compared to the other companies in the segment because it recently signed a contract with a Chinese company which may lead to a turnover of R$ 3 billion per year. China increased its importation of animal protein supplies, because, in addition to the COVID-19 crisis, the country is also facing consequences from the African swine flu, which made it necessary to sacrifice the herd not to further disseminate the disease (Istoé, 2020). Brazil, a country with sanitary surveillance protocols and successive investments in technology, has been increasing quality, traceability, and safety of food products, even attending additional quality demands from clients in the external market. Thus, although the financial crisis provoked by COVID-19 is expected to reduce the purchasing power of the population, leading to a decline in the consumption of animal protein products in Brazil, JBS can redirect part of its production to other markets. In the meantime, BRF faces a crisis in its management and successive losses, which led them to sell units in Argentine, one of which, incidentally, was sold to Marfrig. The latter, in turn, had to give up one of its main shares to maintain its finances stable (G1, 2020b). This recent setting, therefore, led JBS to have an advantage and to have conditions to attend to external demands.

Considering Figures 1 and 2 and Table 2, in general, we can say that the greatest differences observed were between the expected and real returns for the SLC peer companies. For these companies, it was possible to observe the volatility of the signs of abnormal returns during this period, that is, their contrast. Consequently, this can be analyzed from a behavioral perspective, since a contrasting volatility, generated by the tension of the event, can be perceived throughout the days of the event window. Soon, each new information about the event is interpreted and used to reflect the intensity of the emotion generated. Therefore, the abnormal return can be understood as a negative or positive surprise with regard to the expectations of the investors. Cognitive psychology, on the other hand, measures the expectancies using the concept of probability. Tiegen and Keren (2003) discuss the differences between probability and surprise, since the first is related to the moment before decision making, while the latter is related to the moment immediately after it, in addition to the cognitive and behavioral perspective. For these authors, a greater surprise can take place when there is a low probability, and the opposite is also true. It also stands out that the surprise may not be only associated to a low probability, but also to opposed signs to the expected ones, which are more likely in the event. In the context of this study, it can be said that the contrast between the expected and actual returns can provoke new reactions that reflect on the market value of the company, to correct previous information. Therefore, due to the magnitude of the event, this study admitted that positive abnormal returns (negative) would take place, followed by negative abnormal returns (positive). However, due to the capacity of Brazilian agribusiness, there was a belief in positive cumulative abnormal returns. These expectancies made sense for 4 out of the 7 companies analyzed. In the absence of statistically significant contrasts for the SLC company, the expectancy that the company would appear safe in the market with regard to grain activities was reiterated.

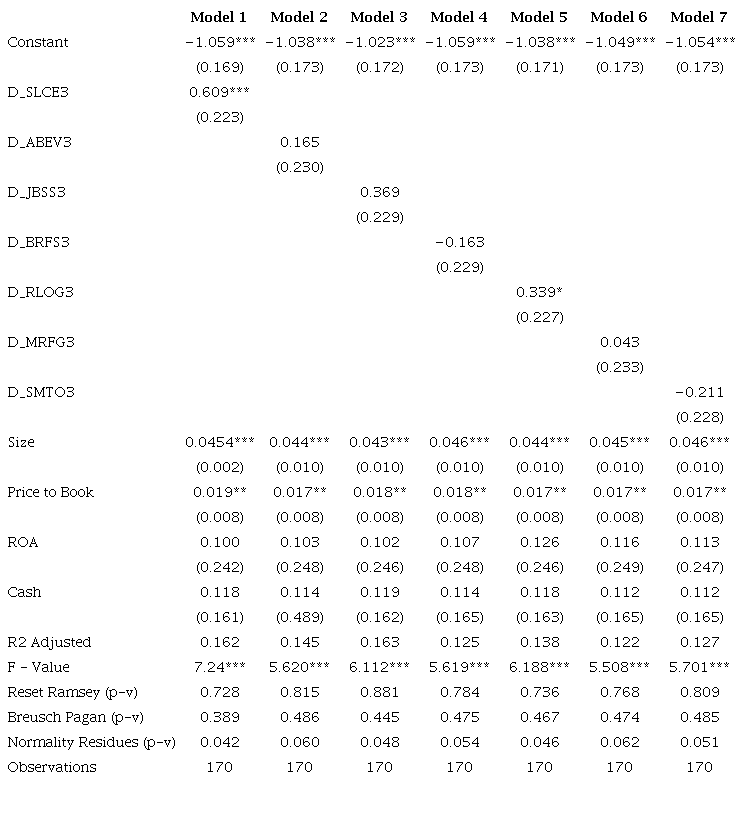

These analyses, based on the event study (Table 2), reinforce some interpretations carried out in the observations describing the graphs presented in Figures 1 and 2. Furthermore, in this occasion, they were based on the statistical evidence of the abnormal returns and of the relations between theory and the discussion of the events that took place. Aiming to provide a more robust analysis, other 7 OLS linear regressions were carried out (one for each agribusiness company), considering CAR (-10; +10) as their dependent variable, and the agribusiness company as an independent variable. This can be seen in Table 3.

Note: Table 3 shows the results for OLS linear regressions for a sample of 170 companies. The models considered the CAR (-10 to +10) as their dependent variable in the 03/18/2020 event, and the agribusiness companies as their independent variables. Each regression model took into consideration one company, considering 1 for the specific company and 0 for the other 169 companies in the sample. For the seven models, we used 4 control variables related to the end of the period before the event, the year 2019. They were: Size: natural logarithm of the total value of actives; Price to Book - market value divided by book value, per share; ROA - net income divided by total value of actives, multiplied by 100; and Cash - cash value and equivalent values divided by the total value of actives. The insertion of these control variables allows us to observe the consistency of the significance for the expected relation, making the model more robust. Null hypothesis of Ramsey's Reset Test: the original regression was specified correctly. Null hypotheses of the Breusch-Pagan Test: absence of heteroscedasticity. Null hypotheses of the Test of the Normality of Residuals: the error has a normal distribution. The superposition of asterisks (***, **, *) denotes a statistical significance with a level of 1%, 5%, and 10%, respectively. Additionally, below each coefficient, the respective standard error can be found. Source: Developed by the outhors.

The results of the multivariable linear regression tests presented in Table 3 were in accordance to the interpretations carried out from the event study, showing that the analyses were consistent. In general, the results of model 1, destined to the differentiate SLC agrícola from the other companies, confirm that it had a positive performance (Coef.: 0,609; Sig.: < 1%), different from that of the other companies that are part of the sample (169 other ones) in the period of 21 days, considered for the event windows. In addition to the SLC, Cosan Logística S.A. also presented signs of a positive statistical difference (Coef.: 0,339; Sig.: < 10%) in the performance of the financial market for the period being analyzed. However, this difference was of little significance when compared to SLC. The signs of a positive performance for Cosan Logística may be associated to the harvest and the grains, since the period analyzed included an intense moment of soy harvest outlet (2019/2020) and the importations increased (SISTEMA OCEPAR, 2020).

By adding the variables control, size, ROA, price to book, and cash were added, we guaranteed that our results would be more rigorous. Still, the control of these variables in the regression test made it possible for us to make further interpretations: (1) the size of the company is positively and significantly related to the CAR, indicating that larger companies had positive CARs and smaller companies had negative CARs; and (2) the index of company value has a positive and significant relation with the CAR, indicating that the largest the market value of the company with regard to its book value, the largest the CAR, and vice-versa. Also, we expected to obtain: (3) a positive relation between ROA and CAR, considering that the good performance of the activity of the company may reflect on a higher return that that expected; and (4) a positive relation between the cash availability of a company and its CAR, considering that it would have a better capacity to withstand the financial problems that the pandemic could bring to them. However, these two final hypotheses were not significant. The results did not vary from one model to the next, since the only change from one to the other was the agribusiness company that was considered as independent variable. It stands out that these variables are useful to calibrate the models tested, meaning that this is not the focus of the discussion. Therefore, we focused our efforts in the understanding of the positive relation of the control of the SLC company with regard to cumulative abnormal returns.

During the period of turbulence generated by COVID-19, the behavior of SLC investors was different than that of the investors of most other companies in the stock market, and even from the investors of peer companies in the sector. It These results are consistent with the setting of Brazilian agribusiness, since the country is one of the largest grain producers in the world (CEPEA, 2020) stands out that agriculture, in the form of grain production, occupies only 7% of the national territory (VIEIRA FILHO, 2019). According to Embrapa (2017) most countries use from 20% to 30% of their space to agriculture. Simultaneously, there is a discussion in Brazil to diminish the area destined to livestock, which is around 19%, to increase about 8% the area destined to agriculture (SENADO, 2020). This expectation will duplicate the area used to cultivate grains, diminishing the area for livestock (since genetic improvements make it possible to shorten the production cycle and, as a result, the space allows for an increased production in the next years). This intensification of crops makes it possible to expand the production of grains without the deforestation of native vegetation (SENADO, 2020).

Considering the importance of the Brazilian grain activity for the world and its capacity for growth both through the expansion of the area that can be cultivated and of the use of technologies in the agricultural system, it becomes possible to understand the behavior of SLC investors, since there are future expectations for the activity of the company. Another factor that contributes to increase further the optimism of these investors is that Brazilian agriculture has been in a period of record production. An estimation from the Systematic Survey of Agricultural Production (LSPA), carried out by the Brazilian Institute of Geography and Statistics - IBGE (2020), indicated that the harvest in 2020 is likely to reach 247 million tons, 2.3% more than in 2019 (Apud GOVERNO DO BRASIL, 2020). Coupled with this favorable environment, the needs generated by the pandemic increased the strength of the results in this sector, especially in the grain activities, leading to an increase/anticipation in exportations (SISTEMA OCEPAR, 2020). Also, the expansion of the exportation of these products with the world commerce came into fruition because the sector is prepared, with regard to the use of technologies and to the fact that quality standards of interested countries have been met. Therefore, the pandemic may have contributed to further intensify the use of technologies in agriculture, in addition to the potential anticipation of future negotiations. These may be the reasons why the investors felt safe and optimistic during these days of great turbulence in the stock exchange. As a result, the SLC company stood, if not unscathed, with positive reflexes in the period analyzed, with regard to the stock market.

5 CONCLUSIONS

This study investigated the effect of the COVID-19 crisis in the performance of the stocks of Brazilian agribusiness companies. The agricultural sector has a wide variety of activities, and most of them are developed by private individuals and/or corporations that use their own capital and bank loans as a way to finance them. Therefore, there are few publicly traded Brazilian companies that belong to this sector. We consider SLC Agrícola S.A. to be the main company in the analysis, since it operates with grain production, the most expressive agricultural activity in the country. Considering this definition, we selected and considered for analysis the peer companies of SLC Agrícola S.A.: Ambev S.A., JBS S.A.; BRF S.A.; Cosan Logística S.A.; Marfrig Global Foods S.A., and São Martinho S.A. Therefore, considering the current setting (the pandemic, the restrictions of food exportations from some countries, the scarcity of foods in others, the surfacing of sanitary problems that allow for the emergence of diseases that impair and/or impede the consumption of foods) and the expressive increase in the exportation of agricultural products, positive reflexes were expected in the stock market performance of the sector, especially in the activity of grains.

Although the other companies analyzed were considered peers to SLC, each one has a very specific activity. Therefore, they have different behaviors in the financial market. It can be reaffirmed, as a result, that investors, despite of the nervousness caused by COVID-19, are capable of recognizing and evaluating the value of the company according to the intensity that the turbulence provoked by the event can affect current and future performances. Although positive and/or negative abnormal returns were found for the agribusiness sector in the dates investigated, showing that there is a volatility of the sector with regard to this uncertain event, it was possible to observe that the nervousness of the investors was more intensely noted in the peers of SLC Agrícola S.A. than in the company itself. This can be noticed because the company had a significant abnormal return in 5 out of the 21 dates, and these returns were positive, meaning that they reached a 31.20% cumulative abnormal return in the period. It stands out that, after a multivariable linear regression test was carried out, controlling the companies selected and considering a sample of 170 companies with a daily quotation in the Brazilian stock market, we were able to find a positive difference in the performance of SLC Agrícola, as opposed to the results of their six peer companies, which did not show significant results, that is, they did not have a different stock performance than that of the companies from other sectors in the event window.

The good performance of SLC Agrícola S.A. during the pandemic of the new coronavirus may be a result of evaluations of future expectations for the sector. Considering the current performance of the activity, there is an expectancy that the effects of the pandemic in the national economy will be mitigated, and that the capital markets will have a good performance in the next years. Therefore, the grain-related activities in Brazilian agribusiness have an important role in global commodity spheres, contributing for the country to stand out as an emerging economy (AGROLINK, 2019). Brazilian agribusiness must be given more visibility, since, according to the findings of this study, its companies presented a good performance, remained stable, and/or took advantage of the moment to expand the development of their activities, in spite of the financial crises and difficulties provoked by the pandemic. These findings reiterate the importance of the activities of Brazilian agribusiness for national and international economy, considering the positive abnormal returns, and the participation of these companies and of this activity in the GDP of the country.

The results of this research contribute to increase the knowledge about Brazilian agribusiness and the perspectives it has, since our analyses included the results of statistical tests and descriptive analyses associated with current news about the events, all of which was discussed from both theoretical and practical points of view. This allowed us to cross pieces of information to obtain a better capacity for analysis and discussion of results. These evidences encourage further studies to be carried out by providing evidence about the participation of agriculture in a developing country. Therefore, new studies are suggested that can compare the Brazilian agribusiness sector with that of other emerging countries. It is also highly relevant to map the technification of production systems and government incentives to agriculture, as well as their influence in the performance of the sector over time.

REFERENCES

AGROLINK. Brasil: país emergente e agronegócio de primeiro mundo? 2019. Availabre in: Availabre in: https://www.agrolink.com.br/noticias/brasil--pais-emergente-e-agronegocio-de-primeiro-mundo-_419816.html. Access in: June 12, 2020.

AMANOR, K. S.; CHICHAVA, S. South-South Cooperation, Agribusiness, and African Agricultural Development: Brazil and China in Ghana and Mozambique. World Development, v. 81, p. 13-23, 2016. Availabre in: https://doi.org/10.1016/j.worlddev.2015.11.021

AMBEV. Juntos à distância. 2020. Availabre in: Availabre in: https://www.ambev.com.br/juntosadistancia. Access in: May 25, 2020.

ANDRADE, D. ‘Export or die’: the rise of Brazil as an agribusiness powerhouse. Third World Thematics: A TWQ Journal, v. 1, n. 5, p. 653-672, 2016. Availabre in: https://doi.org/10.1080/23802014.2016.1353889

AYITTEY, F. K., et al. Economic impacts of Wuhan 2019‐nCoV on China and the world. Journal of Medical Virology, v. 92, n. 5, p. 473-475, 2020. Availabre in: https://onlinelibrary.wiley.com/doi/full/10.1002/jmv.25706.

BARROS, C. M. E.; LOPES, I. F.; ALMEIDA, L. B. Efeito Contágio da operação carne fraca sobre o valor das ações dos principais players do mercado de proteínas do Brasil e do México. Enfoque: Reflexão Contábil, v. 38, n. 1, p. 105 - 122, 2019. Availabre in: https://doi.org/10.4025/enfoque.v38i1.39966

BARUA, S. Understanding Coronanomics: The economic implications of the coronavirus (COVID-19) pandemic. SSRN Electronic Journal, 2020. Availabre in: http://dx.doi.org/10.2139/ssrn.3566477

CADILLO-BENALCAZAR, J. J.; RENNER; A.; GIAMPIETRO, M. A multiscale integrated analysis of the factors characterizing the sustainability of food systems in Europe. Journal of Environmental Management, v. 271, n. 1, p. 1 - 12, 2020.

CEPEA. Centro De Estudos Avançados Em Economia Aplicada. Especial/CEPEA: COVID-19 e agroalimentos: recalibrando expectativas. 2020. Availabre in: Availabre in: https://www.cepea.esalq.usp.br/br/releases/especial-cepea-covid-19-e-agroalimentos-recalibrando-expectativas.aspx. Access in: May 24, 2020.

CHAKRABORTY, I.; MAITY, P. COVID-19 outbreak: Migration, effects on society, global environment and prevention. Science of The Total Environment, v. 728, n. 1, p. 138882, 2020.

EMBRAPA. Lavouras são de apenas 7,6% do Brasil, segundo NASA. 2017. Availabre in: Availabre in: https://www.embrapa.br/busca-de-noticias/-/noticia/30972444/lavouras-sao-apenas-76-do-brasil-segundo-a-nasa. Access in: August 20, 2020.

EMBRAPA. Embrapa Soja. 2020a. Availabre in: Availabre in: https://www.embrapa.br/soja/cultivos/soja1/dados-economicos. Access in: May 26, 2020.

EMBRAPA. Trajetória da Agricultura Brasileira. 2020b. Availabre in: Availabre in: https://www.embrapa.br/visao/trajetoria-da-agricultura-brasileira. Access in: July 09, 2020.

G1. Preços do petróleo fecham em forte alta após três dias de queda. 2020a. Availabre in: Availabre in: https://g1.globo.com/economia/noticia/2020/03/19/precos-do-petroleo-operam-em-alta-apos-tres-dias-de-queda.ghtml. Access in: May 27, 2020.

G1. BRF e Marfrig desistem de fusão. 2020b. Availabre in: Availabre in: https://g1.globo.com/economia/noticia/2019/07/11/brf-e-marfrig-desistem-de-fusao.ghtml. Access in: May 27, 2020.

G1. Com pandemia do coronavírus, Brasil fecha 1,1 milhão de vagas de trabalho entre março e abril. 2020c. Availabre in: Availabre in: https://g1.globo.com/economia/noticia/2020/05/27/coronavirus-brasil-fecha-860-mil-empregos-formais-no-pior-mes-de-abril-em-29-anos.ghtml. Access in: May 27, 2020.

GOVERNO DO BRASIL. IBGE prevê novo recorde na safra de 2020. 2020. Availabre in: Availabre in: https://www.gov.br/pt-br/noticias/agricultura-e-pecuaria/2020/05/ibge-preve-safra-novo-recorde-na-safra-em-2020#:~:text=A%20safra%20nacional%20de%20gr%C3%A3os,Geografia%20e%20Estat%C3% ADstica%20(IBGE). Access in: August 21, 2020.

HALL, J.; MATOS, S.; SILVESTRE, B.; MARTIN, M. Managing technological and social uncertainties of innovation: the evolution of Brazilian energy and agriculture. Technological Forecasting and Social Change, v. 78, n. 7, p. 1147-1157, 2011. Availabre in: https://doi.org/10.1016/j.techfore.2011.02.005

IBGE. Com impacto do coronavírus, PIB encolhe 1,5% no primeiro trimestre. 2020. Availabre in: Availabre in: https://agenciadenoticias.ibge.gov.br/agencia-noticias/2012-agencia-de-noticias/noticias/27838-com-impacto-do-coronavirus-pib-encolhe-1-5-no-primeiro-trimestre. Access in: July 20, 2020.

IORIS, A. A. Cracking the nut of agribusiness and global food insecurity: In search of a critical agenda of research. Geoforum, v. 63, n. 1, p. 1-4, 2015. Availabre in: https://doi.org/10.1016/j.geoforum.2015.05.004

IQBAL, N., et al. Nexus between COVID-19, temperature and exchange rate in Wuhan City: New findings from Partial and Multiple Wavelet Coherence. Science of The Total Environment, v. 729, p. 138916, 2020.

ISTOÉ. Importação chinesa de carne cresce 69,6% no 1º bimestre de 2020. 2020. Availabre in: Availabre in: https://istoe.com.br/importacao-chinesa-de-carne-cresce-696-no-1o-bimestre-de-2020/. Access in: May 27, 2020.

MINISTÉRIO DA ECONOMIA. Nota Informativa - Impactos Econômicos da COVID-19. 2020. Availabre in: Availabre in: https://www.gov.br/economia/pt-br/centrais-de-conteudo/publicacoes/notas-informativas/2020/nota-impactos-economicos-da-covid-19.pdf/view. Access in: May 27, 2020.

MINISTÉRIO DA SAÚDE. Brasil confirma primeiro caso da doença. 2020. Availabre in: Availabre in: https://www.gov.br/saude/pt-br/assuntos/noticias/brasil-confirma-primeiro-caso-de-novo-coronavirus. Access in: April 05, 2020.

MOREIRA, R. V.; KURESKI, R.; VEIGA, C. P. Assessment of the economic structure of Brazilian agribusiness. The Scientific World Journal, v.1, n. 1, p. 1 - 10, 2016. Availabre in: https://doi.org/10.1155/2016/7517806

MUELLER, B.; MUELLER, C. The political economy of the Brazilian model of agricultural development: Institutions versus sectoral policy. The quarterly review of economics and finance, v. 62, n. 1, p. 12-20, 2016. Availabre in: https://doi.org/10.1016/j.qref.2016.07.012

NICOLA, M. et al. The Socio-Economic Implications of the Coronavirus Pandemic (COVID-19): A Review. International Journal of Surgery, v. 78, n. 1, p. 185 - 193, 2020. Availabre in: https://doi.org/10.1016/j.ijsu.2020.04.018

OZILI, P. K.; ARUN, T. Spillover of COVID-19: impact on the Global Economy. SSRN Eletronic Journal. 2020. Availabre in: http://dx.doi.org/10.2139/ssrn.3562570

PEREIRA, P. A. A.; MARTHA JR., G. B.; SANTANA, C. A.; ALVES, E. The development of Brazilian agriculture: future technological challenges and opportunities. Agriculture & Food Security, v. 1, n. 4, p. 1-12, 2012. Availabre in: https://doi.org/10.1186/2048-7010-1-4

PPI - Programa de Parcerias de Investimentos. Projetos: Rumo Malha Paulista SA. 2020. Availabre in: Availabre in: https://www.ppi.gov.br/rumo-malha-paulista-sa. Access in: May 27, 2020.

SENADO. Em Discussão. 2020. Availabre in: Availabre in: https://www.senado.gov.br/noticias/ Jornal/emdiscussao/codigo-florestal/senado-oferece-um-projeto-equilibrado-para-o-novo-codigo-florestal-brasileiro/pecuaria-com-maior-maior-produtividade-dobraria-area-plantada.aspx. Access in: August 20, 2020.

SCOONES, I.; AMANOR, K.; FAVARETO, A.; QI, G. A new politics of development cooperation? Chinese and Brazilian engagements in African agriculture. World Development, v. 81, n. 1, p. 1-12, 2016. Availabre in: https://doi.org/10.1016/j.worlddev.2015.11.020

SHARIF, A.; ALOUI, C.; YAROVAYA, L. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis, v. 70, n. 1, p. 101496, 2020. Availabre in: https://doi.org/10.1016/j.irfa.2020.101496

SISTEMA OCEPAR. Mercado internacional: Exportações do agro superam os U$$ 10 bilhões em abril. 2020. Availabre in: Availabre in: http://www.paranacooperativo.coop.br/ppc/index.php/sistema-ocepar/comunicacao/2011-12-07-11-06-29/ultimas-noticias/127891-mercado-internacional-exportacoes-do-agro-superam-os-us-10-bilhoes-em-abril. Access in: May 24, 2020.

SUI, L.; SUN, L. Spillover effects between exchange rates and stock prices: Evidence from BRICS around the recent global financial crisis. Research in Internatonal Business and Finance, v. 36, n. 1, p. 459 - 471, 2016. Availabre in: https://doi.org/10.1016/j.ribaf.2015.10.011

TIEGEN, K. H.; KEREN, G. Surprises: low probalities or high contrasts? Cognition, v. 87, n. 1, p. 55 - 71, 2003. Availabre in: https://doi.org/10.1016/s0010-0277(02)00201-9

VIEIRA FILHO, J. E. R. Diagnóstico e desafios da agricultura brasileira. Rio de Janeiro: IPEA. 2019. Availabre in: Availabre in: https://www.ipea.gov.br/portal/index.php?option=com_content&view=article&id=35200&Itemid=444. Access in: July 25, 2020.

WORLD HEALTH ORGANIZATION. There is a curret outbreak of Coronavirus (Covid-19) disease. 2020. Availabre in: Availabre in: https://www.who.int/health-topics/coronavirus/coronavirus#tab=tab_1. Access in:May 26, 2020.

WANG, Y.; HONG, A.; LI, X.; GAO, J. Marketing innovations during a global crisis: A study of China firms’ response to COVID-19. Journal of Business Research, v. 116, n. 1, p. 214 - 220, 2020.Availabre in: https://doi.org/10.1016/j.jbusres.2020.05.029

Author notes

Endereço dos Autores: Av. Prefeito Lothário Meissner, 632, Jardim Botânico, Curitiba - PR - Brasil. 82590-300