Article

Career choice intention and work engagement of the audit professional in the Brazilian context1

Intenção de escolha de carreira e engajamento no trabalho do profissional de auditoria no contexto brasileiro

Cristiane Krüger Cristiane.kruger@ufsm.br

Luis Felipe Dias Lopes lflopes67@gmail.com

Rafaelly Moraes dos Santos rafaelly.lrds@gmail.com

Ester Escalante Peiter esterpeiter21@gmail.com

Cristiane Krüger Cristiane.kruger@ufsm.br

Luis Felipe Dias Lopes lflopes67@gmail.com

Rafaelly Moraes dos Santos rafaelly.lrds@gmail.com

Ester Escalante Peiter esterpeiter21@gmail.com

Career choice intention and work engagement of the audit professional in the Brazilian context1

Enfoque: Reflexão Contábil, vol. 43, no. 2, pp. 14-39, 2024

Universidade Estadual de Maringá

Received: 21 March 2022

Revised document received: 02 September 2022

Accepted: 18 November 2022

ABSTRACT

Objective: This research analyzed the attitudinal, subjective norms, behavioral perception, and work engagement variables that determine the audit professional’s intention to choose to pursue the career.

Method: The methodology is quantitative, descriptive, and survey. Data were obtained through the application of a questionnaire with 312 audit professionals in Brazil. Data analysis included structural equation modeling.

Originality/Relevance: The theoretical gap lies in the relationship between the Theory of Planned Behavior and work engagement in audit professionals. In this way, the intention of deciding on a career does not consist only in choosing a specific branch within the accounting area, but also in the individual’s willingness and competence to implement their projects and in the future engagement to support it, which demonstrates the confidence of the search.

Results: The results revealed that audit professionals are happy to follow in this area, feel confident, believe in their professional capacity, and intend to grow in their careers in the coming years. Professionals have high levels of vigor, dedication, and concentration, and are highly engaged in their work. Personal attitudes, subjective norms, vigor, and dedication presented an explanatory power of 58% of the intention, concluding that the relationships between the scales are supported.

Theoretical contributions: The model for measuring the relationship between intention to choose a career and engagement at work was validated. The study fills a gap in the behavioral area, helping to understand the auditor's behavior.

Keywords: Auditing+ Professional behavior+ Theory of Planned Behavior+ Utrecht Work Engagement Scale+ Structural equation modelling.

RESUMO

Objetivo: Esta pesquisa analisou os antecedentes atitudinais, normas subjetivas, percepção comportamental e engajamento no trabalho que determinam a intenção do profissional de auditoria em escolher seguir na carreira.

Método: A metodologia é quantitativa, descritiva e de levantamento. Os dados foram obtidos por meio da aplicação de um questionário com 312 profissionais de auditoria no Brasil. A análise dos dados incluiu modelagem de equações estruturais.

Originalidade/Relevância: A lacuna teórica reside na relação entre a Teoria do Comportamento Planejado e o engajamento no trabalho em profissionais de auditoria. Deste modo, a intenção de decidir por uma carreira não consiste apenas na escolha de um ramo específico dentro da área contábil, mas também na disposição e competência do indivíduo para implementar seus projetos e no engajamento futuro para sustentação da mesma, o que demonstra a relevância da pesquisa.

Resultados: Os resultados revelaram que os profissionais de auditoria estão satisfeitos em continuar nesta área, sentem-se confiantes, acreditam na sua capacidade profissional e pretendem crescer na carreira nos próximos anos. Os profissionais têm altos níveis de vigor, dedicação e concentração, e são altamente engajados em seu trabalho. Atitudes pessoais, normas subjetivas, vigor e dedicação apresentaram poder explicativo de 58% da intenção, concluindo que as relações entre as escalas são sustentadas.

Contribuições teóricas: O modelo de mensuração da relação entre intenção de escolha de carreira e engajamento no trabalho em profissionais de auditoria foi validado. O estudo supriu uma lacuna na área comportamental, auxiliando no entendimento acerca do comportamento do auditor.

Palavras-chave: Auditoria, Comportamento profissional, Teoria do Comportamento Planejado, Escala de Engajamento no Trabalho de Utrecht, Modelagem de equações estruturais.

1 INTRODUCTION

The accounting profession is among the most requested and widespread professions in Brazil (Ribeiro, 2017). According to Iudícibus et al. (2019), accounting has a wide field of action, being one of the areas that provide the most opportunities for professionals. For the authors, the student who opted for a higher degree in accounting will have numerous alternatives. Among them, Attie (2018) cites auditing, which is a specialization in the accounting area and aims to test the efficiency and effectiveness of equity control by expressing an opinion on a given data.

The auditing profession has undergone significant changes over the years, both with the increase in legislation, technological advances, and with the demand for the conduct, engagement, and behavior on the part of auditors (Mercali & Costa, 2019; Mota & Martins, 2018). It is known that it is a relevant activity in the business world and that in the last five decades it has undergone a profound transformation in relation to the definition of its role (Camargo et al., 2013; Mendonça & Martins, 2016; Niyama et al., 2011). For these authors, professionals in the area are required to adapt their routines and dedication to the profession, such as giving up being with the family to fulfill a travel schedule, spending more hours a day to complete tests and procedures, and maintaining a routine of updating and continuing technical education.

Among the demands, benefits, and limitations of the profession, the subject must be clear about what his real intention is for an assertive choice of career to be followed (Santos & Almeida, 2018). According to the authors, career choice is understood as the individual’s ability to identify their interests within the profession and develop strategies to achieve established professional goals and objectives. Corroborating, Neves et al. (2013) consider the career to be the path taken by the individual through work experiences, development, and monitoring of goals that can influence, throughout life, their personal satisfaction.

In this sense, Santos and Almeida (2018) state that, in relation to the intention to choose a career, the individual takes into account several internal and external factors, this choice is linked to the degree of self-knowledge of the individual, the world, the work and, mainly, of his/her personal and professional reasons. This can be evidenced through the Theory of Planned Behavior (TPB), which characterizes human behavior as rational and predicts the individual’s intention, analyzing the relationship with the background of personal attitude, subjective norms, and perceived behavioral control (Ajzen, 1991), for example, for choosing a career (Santos et al., 2018).

The intention of deciding on a career for the audit professional does not only consist in choosing a specific branch within the accounting area but also in the subject’s willingness and competence to implement their projects and in the future engagement to support them (Santos and Almeida, 2018). In this sense, engagement can directly reflect on the quality and productivity of work, benefiting the organization and the professional, who are increasingly seeking self-development in their careers and involvement in pleasurable and self-fulfilling activities (Schaufeli et al., 2013).

Therefore, the research question is: do attitudinal, subjective norms, behavioral perception and engagement at work determines the audit professional’s intention to choose to pursue the career? To answer the raised issue, the objective is to analyze the antecedents attitudinal, subjective norms, behavioral perception and work engagement that determines the audit professional’s intention to choose to pursue the career. Specifically, it aims to: a) describe the profile of the surveyed audit professionals, and b) demonstrate the relationship between the dimensions of the career choice intention scales and audit professionals’ engagement in their work.

A similar study was carried out by Tetteh et al. (2022), who interviewed 75 undergraduate Accounting Sciences students from Ghana, seeking to understand whether these students would choose auditing as a career, through social cognitive career theory. These authors recommend considering other theories that can help uncover important personal and contextual factors in individuals' intention to follow the auditing profession. Ilias et al. (2022) also investigated factors that determine the intention of future Malaysian Accounting Science graduates to undertake professional certifications to pursue the field of auditing. In the research, the TPB was adopted, and the authors suggest that future research can analyze other determinants of intention, for example, the engagement. It is in these gaps that the present research is inserted, which uses the TPB, a theory consecrated in the area of intention, and the quantitative approach, to unveil determinants of the intention to pursue in the career in auditing, in the Brazilian context, considering professionals instead than students.

It should be noted that the TPB has already been adopted in different studies focused on the accounting area (Santos & Almeida, 2018; Santos, Moura & Almeida, 2018; Batista & Marçal, 2020; Zago Júnior et al., 2020), however, its application in measuring the intention to follow a professional career in auditing in the Brazilian context is scarce. Another relevant factor for the elaboration of this study, regarding social and behavioral aspects, refers to the use of TPB (Santos & Almeida, 2018). This theory has been shown to be useful to explain different types of behavioral intention, being used in research to analyze variables that affect the choice of ethical decisions, entrepreneurial behavior, and career choice (Krüger & Ramos, 2020; Santos et al., 2018), what substantiates the choice of this theory for this research.

As a justification for this research in auditing, Crepaldi and Crepaldi (2019) point out that research on the subject enriches the literature, contributing to the development of audit professionals. Also, as a result of the performance of the independent audit professional’s office, in analyzing the veracity of the financial statements disclosed by organizations, an expansion in the field of auditing in Brazil can be seen (Pacheco & Camilo, 2020). In this way, contributing to the existence of a more reliable scenario, in which the performance of audit professionals is essential for the progress of the financial, capital markets, and organizations in general. Therefore, the relevance of the auditing area demonstrates the need for research aimed at improving the role performed by these professionals (Niyama et al., 2011). Furthermore, the increase in auditors in Brazil is a motivation to investigate why individuals are more interested in auditing (Amorim et al., 2012).

A professional career in auditing remains attractive for many accounting graduates, due to factors such as incentives, professional training, professional recognition, social values, work environment and the job market (Ramdani et al., 2019). In this way, knowing the background of career choice can be useful for future professionals to be more prepared for the profession that awaits them.

This research is also justified by the relevance of approaching engagement for professional practice, since engaged individuals are described as essential for organizational success and efficiency (Schaufeli et al., 2014). Therefore, measuring engagement can be as significant for professionals as for the organization in which these individuals work, while opening possibilities to identify strengths or promote actions that make people feel inspired and motivated at work (Freitas & Charão-Brito, 2016). Furthermore, engagement is one of the most studied topics in organizational science (Lee et al., 2019), but in auditing they are still rare. According to Lee et al. (2019), more research is needed to understand the concepts of engagement and investigate their relationship, due to the positive influences for organizations.

The present study presents theoretical contribution potential. So far, it has not been possible to identify in the literature a previous study that relates the intention to choose a career (TPB) and the engagement at work. This gap encourages the development of new studies in the behavioral area. Thus, there is a research gap, which can scientifically contribute to advances in the literature. That said, the theoretical foundation of the research is presented below.

2 THEORETICAL FOUNDATION

2.1 Auditing profession in Brazil

The advent of auditing in Brazil is related to the arrival of international independent auditing companies, as well as the arrival of branches and subsidiaries of foreign firms, financing of Brazilian companies through international entities, the growth of Brazilian companies and the need for decentralization and diversification. of its economic activities, evolution of the capital market (Creation of the Securities and Exchange Commission) and creation of auditing standards promulgated by the Central Bank of Brazil (Attie, 2018; Crepaldi & Crepaldi, 2019).

The function of the audit, in short, is to review the entire financial statement at the end of the company's fiscal year, issue audit reports and evaluate the entity’s internal control system, as well as it can identify errors and frauds during its audit process. analysis (Attie, 2018). Through the applicability of the audit, the types of ramifications of this accounting tool emerged, being external audit (independent) and internal audit (Crepaldi & Crepaldi, 2019). For these authors, both emerged in view of the information needs that the manager requires to postulate about his entity, whether through survey, study, procedures, operations, or financial statements.

Despite having different objectives, internal and external audit activities are often carried out simultaneously within organizations, the first complementing the second (Oliveira & Ciupak, 2017). According to the Federal Accounting Council (CFC, 2016), the independent audit comprises the set of technical procedures that aim to issue an opinion on the adequacy of the financial statements, in accordance with the Brazilian Accounting Standards and, as appropriate, the specific legislation. Meanwhile, internal audit is the independent evaluation activity within the company, to verify operations and issue a report on them, being considered a service provided to management (Almeida, 2019).

In this way, according to NBC PG 100 (R1) (CFC, 2019a), the title of accounting audit professional, to perform the audit activity and sign the reports, must have a degree in Accounting and be duly registered with the Regional Council of Accounting (CRC). It should be noted that the accounting technician is not qualified to perform this activity. Likewise, the auditor must participate in activities of the Continuing Education Programs, promoted by the CRC’s, developed with the aim of maintaining, updating, and expanding technical and professional knowledge and skills, as well as raising the social, moral, and ethical behavior of the accounting professionals, thus ensuring the maintenance of their registration with regulatory bodies (Almeida, 2019; CFC, 2017).

The auditor is the target of the most diverse criticisms towards society, regarding his conduct in the face of ethical dilemmas and moral virtues (Elias et al., 2014). In view of this, through NBC PG 100 (R1), the auditing profession requires obedience to professional ethical principles that fundamentally rely on independence, integrity, objectivity and efficiency, confidentiality, conduct, competence, and professional care (CFC, 2019a). For this, the performance of the auditor is managed by NBC PG 01 - Professional Code of Ethics of the Accountant, which presents how the professional's conduct should be and the consequences for those who inflict the code of ethics (CFC, 2019b).

The professional attitude of auditing is the combination of technical knowledge and professional education acquired through the constant study of new regulations and work tools, personal improvement and the experience acquired during the various works carried out (Attie, 2018). The auditor should seek to build and maintain an incorruptible reputation, founded on unassailable moral standards, because “the auditor’s signature on the audit report of the financial statements requires the exercise of a preventive attitude, by an individual with sufficient moral strength to be able to give reliability the same” (Attie, 2018, p. 6).

2.2 Theory of planned behavior

The Theory of Planned Behavior (TPB) was coined to unravel and predict human behavior in a specific context (Ajzen, 1991). TPB is a widely disseminated theoretical model, composed of factors that lead to the formation of a behavioral intention, proposed in 1991 by the social psychologist Icek Ajzen (Ajzen, 1991; 2015). This theory assumes that individuals consider the implications of their actions before deciding whether or not to behave in a certain way. Thus, the intention of determining behavior depends on three variables: personal attitudes, subjective norms and perception of behavioral control (Ajzen, 2015).

The three precedents of behavioral intentions are based on beliefs (behavioral, normative and control) that “represent the information he [the subject] has about the object. Specifically, a belief relates an object to some attribute” (Fishbein & Ajzen, 1975, p.12). This object can refer to people, groups, institutions, behaviors, and attributes, quality, consequence, characteristic, event (Moutinho & Roazi, 2010).

In BPD, a positive attitude, or personal attitude, predisposes the individual to perform the behavior, while a negative attitude can lead to the withdrawal of the behavior (Ajzen, 1991). Thus, attitudes help to have a stable idea of the reality in which individuals find themselves, protecting them from unpleasant situations (Ajzen, 1988). The subject’s attitude towards a behavior is a function of their beliefs and behavioral evaluations, that is, it is what the subject believes will happen as a result of the behavior and the evaluation of these consequences (Santos & Almeida, 2018).

Another component in the determination of behavioral intention is the subjective norm, or subjective norms in the plural, which reflects the perception of the opinion of other people about the execution or not of a certain behavior by the individual, in this way, “the more the person realizes that others who are important to her think that she should perform the behavior, the greater will be her intention to perform it” (Santos & Almeida, 2018, p. 44).

The third precedent of intention is the degree of perceived behavioral control or perceived behavioral control. For Ajzen (2002) the perception of control has proved to be an important predictor element, since it can act together with the intention, indirectly relating to the behavior, as well as acting without intentional mediation, directly relating to the behavior. Based on BPD, the intention to perform and the performance of the behavior itself are influenced by the perception of behavioral control (Ajzen, 1991). Being able to carry out an intention if the individual has resources and opportunities to carry out the action (Ajzen, 1991). Thus, for the author, when individuals believe that they have the resources and opportunities required and that the obstacles they may encounter are few and manageable, they trust their abilities to perform the behavior, presenting a high degree of perception of behavioral control.

Being influenced by the three components already explained (attitude, subjective norm, and perception of control), the behavioral intention construct is characterized as the purpose, will and determination that an individual has to perform a certain behavior (Ajzen, 1991). In other words, it can be understood as a summary of the motivation needed to perform a particular behavior, reflecting an individual's decision to follow a course of action, as well as an index of how much a person would be willing to try to perform a behavior (Fishben & Ajzen, 1975).

For Moutinho and Roazi (2010) behavioral intention is the variable that best predicts behavior, and this, in turn, will express the weighted choice between the various existing alternatives. In this perspective, intentions are considered a particular type of belief, in which the person is the object, and the attribute associated with it is always a behavior, and its result is a subjective probabilistic degree in which it best predicts the behavior (Ajzen & Fishbein, 1980).

The application of TPB allows dealing with the complexities of human social behavior, “incorporating central concepts of the social sciences and behavior, in a way that allows the prediction and understanding of specific behaviors in specific contexts” (Ajzen, 1991, p.206). In this way, it is useful to explain many types of behaviors, such as career choice (Santos & Almeida, 2018).

2.3 Engagement at work

The theme engagement at work originated in Work Psychology and in the management literature in the 1990s, following a general trend of studies on positive organizational behaviors (Schaufelli & Bakker, 2004). During this period, the main studies addressed the diseases developed by the exercise of work, such as stress and exhaustion. For Schaufelli and Bakker (2004) this highlights the aspects responsible for the development of a positive and effective environment at work, thus giving rise to the concept of engagement at work.

Engagement and disengagement at work are behaviors through which people bring or leave their selves during the performance of tasks (Siqueira et al., 2014). Engagement is defined by Schaufeli et al. (2002) as a mental and dispositional state of energetic investment, facing difficulties and directing the effort towards the work with which the individual identifies and feels immense pleasure in performing. Engagement at work, in turn, for Avigo et al. (2017) and Schaufeli et al. (2013), it can be understood as a positive mental state, which has a motivational character, and maintains a link to work activity, reflecting the individual's desire to contribute to the success of the organization.

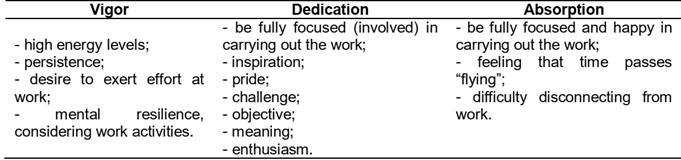

Work engagement is characterized by three dimensions: vigor, dedication, and absorption/concentration (Hansen et al., 2018; Schaufeli et al., 2002; Vazquez et al., 2015). There are discrepancies between authors regarding the terminology used for absorption, as is the case of Vazquez et al. (2015) who adapted and validated the Utrecht Work Engagement scale for the Brazilian context, choosing to use the term concentration, adopted in this study. Table 1 presents the components of engagement at work.

As evidenced in Table 1, Vigor corresponds to high levels of energy and mental resilience at work. Dedication refers to being deeply involved and committed to work, experiencing a strong sense of meaning, enthusiasm, and challenge. And, Absorption indicates a high level of concentration, where time passes quickly while at work (Salanova et al., 2005).

For Cavalcante et al. (2014), it can be observed that the expression engagement refers to a positive motivational construct, qualified by absorption, dedication, and vigor, always related to work. This construct results in feelings of accomplishment that involve a positive cognitive state, manifesting a motivational and social nature (Cavalcante et al., 2014). Thus, engagement at work must be understood from its dimensions, which allow for independent identification and measurement, and which enables the verification of the psychological meaning of work (Fernandes et al., 2014).

The promotion of engagement at work modulates the direct effects of organizational resources on performance, well-being, and quality of life in general (Llorens et al., 2007), benefiting not only individuals, but also organizations, the that generates a competitive advantage for them (Llorens et al., 2007). It is a positive state that enables and facilitates the use of resources, which is closely linked to the development of the organization, stimulating positive organizational results and, thus, reducing negative results (Schaufeli et al., 2013). It is in this aspect that the TPB is inserted, through which it seeks to verify whether engagement is a determinant of intention. Next, the theoretical model is presented.

2.4 Theoretical model for intent and engagement

To support the subsequent discussions and conclusions, and seek to analyze the antecedents attitudinal, subjective norms, behavioral perception, and engagement in work that determines the intention of choosing the audit professional’s career, we discuss the different dimensions surveyed.

Attitude is characterized as positive or negative reactions to a certain behavior (Fishbein & Ajzen, 1975). So, the individual’s attitude refers to the personal influence on the behavior, being a function of his/her beliefs and behavioral assessments, which corresponds to the individual’s judgment to perform a certain behavior, admitting their favorability or not to the action (Moutinho & Roazi, 2010). Therefore, it is expected that the beliefs and behavioral assessments of audit professionals positively influence the intention to choose to pursue a career. Thus, the first research hypothesis is: H1 Personal attitudes influence the intention to choose a career.

Then, the dimension of subjective norms is inserted, which for Ajzen and Fishbein (1980) refers to the social pressure that can be exerted on the individual to perform or not some behavior. And is determined by the individual’s beliefs about expectations that other specific people, belonging to their environment, have about a certain behavior (Fishbein & Ajzen, 1975). Based on this, it is expected that the more audit professionals perceive those others, who are important to them, encourage them to perform certain behavior’s, such as choosing a career, the greater will be their intention to do so. In this sense, the second research hypothesis is: H2 Subjective norms influence the intention to choose a career.

The third hypothesis investigates the influence of behavioral control perception on intention. For Ajzen (1991), this dimension is TPB’s third variable and is defined as the resources and opportunities available to the individual, which facilitate the execution of a behavior with a high probability of success when performing the intended behavioral action. While for Santos et al. (2018), seeks to evidence the individual’s perception about the ease or difficulty of performing a certain behavior, which may inhibit or facilitate the subject’s behavior in the face of resources, information, and opportunities that occur during the execution of the behavior of interest. Thus, it is expected that the greater the perceived behavioral control, the greater the intention in choosing to pursue an auditing career. Therefore, the third hypothesis is: H3 Perception of behavioral control influences the intention to choose a career.

The fourth hypothesis investigates the influence of the vigor dimension on the intention to choose to pursue a career. For Schaufeli et al. (2014), vigor is related to high levels of energy and mental resilience in the workplace, the willingness to invest effort, and being persistent, even in difficult situations. In fact, vigor abstracts the state of vitality, motivation and energy of individuals, positively influencing the performance of professional tasks and negatively influencing absenteeism (Neuber et al., 2022). In this aspect, it is understood that engagement at work is a positive motivation at work that increases the vigor of employees (Bouckenooghe et al., 2022). In this sense, it is assumed that the greater the individual’s vigor level, the greater will be their intention to choose to pursue in the auditing career, formulating the fourth research hypothesis: H4 Vigor influences the intention to choose of the career.

The fifth hypothesis investigates the influence of dedication on the intention to choose a career. For Schaufeli et al. (2014), dedication is characterized as a strong sense of meaning, enthusiasm, inspiration, pride and challenge in the work environment, with the individual being deeply involved with what happens in daily work. For Akgunduz et al. (2022), being dedicated connotes inspiring enthusiasm about job responsibilities. Thus, it is assumed that the higher the individual's level of dedication, the greater his intention to choose to pursue an auditing career. Thus, the fifth hypothesis of the study is stated: H5 Dedication influences the intention to choose a career.

Finally, the sixth hypothesis tests the influence of concentration on intention. For Schaufeli et al. (2014), the concentration dimension is characterized by the individual being involved in a state of total concentration and happiness, immersed in the work environment, making time pass quickly and it is difficult to completely disconnect from work. Concentrating at work means being fully attentive, along with complete absorption and immersion with work (Hussain et al., 2022). Highly engaged employees become engrossed in their work (Alev, 2022). Thus, it is assumed that the higher the individual's concentration level, the greater his intention to choose to pursue an auditor career, formulating the sixth research hypothesis: H6 Concentration influences the intention to choose a career.

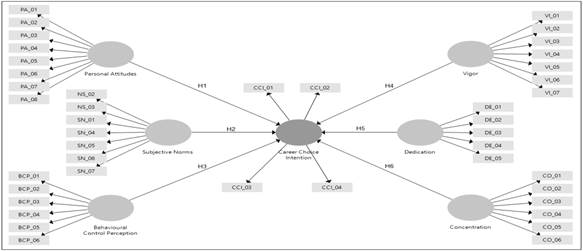

Figure 1 demonstrates the theoretical model with the research hypotheses, which seeks to analyze the relationship between the dimensions of the scales of intention to choose a career and work engagement for audit professionals in Brazil, considering the influence of different dimensions on the intention to choose a career.

Figure 1

Theoretical model for intention and engagement

Source: The authors.

3 METHODOLOGY

The population is composed of audit professionals, namely, independent auditors, internal auditors, assistants, trainees, among others working in Brazil. Focusing on the profession, it was decided to consider all professionals in this area, and it is not possible to reliably estimate the size of the population in Brazil. Therefore, to estimate the minimum sample size, the calculation established by Hair et al. (2009), which considers the minimum observation by variables to be 5:1. For this study, which contains 43 variables, a minimum sample of 215 respondents was estimated. After defining the sample, the questionnaire was elaborated using the Google Forms platform. The questionnaire was structured from the grouping of validated scales, by Santos et al. (2018) and Vazquez et al. (2015).

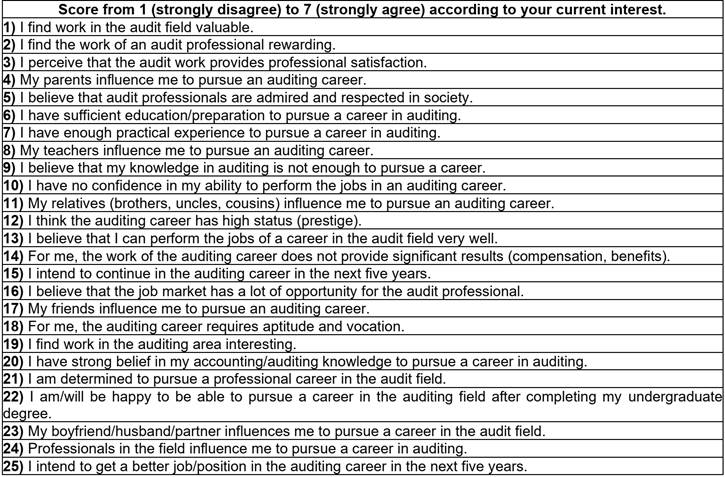

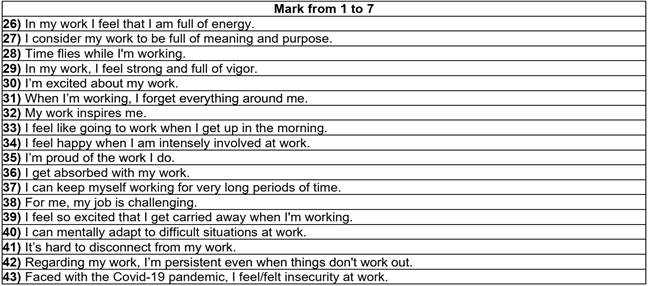

The instrument, considering the profile questions and the researched variables, consisted of a total of 53 closed questions distributed in three blocks (Appendix A). The first block was based on the study by Santos et al. (2018), which included questions related to TPB, adapted for choosing an auditing career. To measure the intention to choose the auditing career, 25 statements were used, distributed into four constructs: eight statements related to the Attitude construct, seven statements related to Subjective Norms, six statements related to Perceived Behavioral Control, and four assertions related to the Intent construct. In the instrument, the indicators were presented randomly between the dimensions, in addition, three questions (9, 10, and 14) were presented in a negative way to test the respondents’ attention to the answers, and their results were inverted for analysis.

The second block was based on the study by Vazquez et al. (2015), on the Utrecht Work Engagement Scale (UWES), and contained questions related to the level of engagement in the work of audit professionals. For this, the three dimensions of vigor, dedication, and concentration were taken into account. This block was composed of 18 assertions: seven related to the vigor dimension, five to the dedication, and six to concentration. It is worth noting that the last statement (In view of the Covid-19 pandemic, I feel/felt insecurity at work) was included by the researchers in view of the established pandemic. In the instrument, the indicators were presented randomly among the dimensions analyzed. It should be noted that there are no inverted (negative) items in this scale.

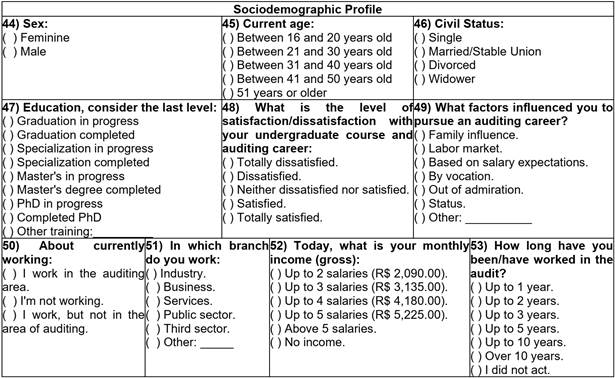

The instrument was answered by the respondents according to a 7-point Likert scale for blocks I and II, partially anchored, whose points for block I - Intention to choose a career were: 1 (strongly disagree), 2 (strongly disagree), 3 (somewhat disagree), 4 (neither disagree nor agree), 5 (somewhat agree), 6 (very much agree) and 7 (strongly agree). And in block II - Engagement in work, the scale points corresponded to: 1 (Never), 2 (Almost Never/A few times a year or less), 3 (Rarely/Once a month or less), 4 (Sometimes/ A few times a month), 5 (Often/Once a week), 6 (Very often/A few times a week) and 7 (Always/Every day). The third block included questions related to the profile of professionals. These questions aimed to obtain additional information, consisting of questions that lead to evidence of gender, age, marital status, education, length of experience in the auditing profession, participant’s income, and factors that influenced him to pursue a career audit trail.

Data collection was carried out from October 26th to November 23rd, 2020, through the social business network Linkedln, e-mails with auditing companies, and direct sending to professionals, as well as, by sending the instrument to the e-mails of the Unions of Accountants and from the website of the Instituto Brasileiro de Contabilidade - Ibracon. In the social network Linkedln, the profiles of professionals in the population were searched, in which the objective was to make a “connection”, to enable requests to participate in the research. At the end of the stipulated period, a total of 312 valid responses were obtained, which were considered for analysis in the research. After collection, tabulation was performed, followed by data analysis. The first step to proceed with the data analysis consisted of the elaboration of a database in an electronic spreadsheet.

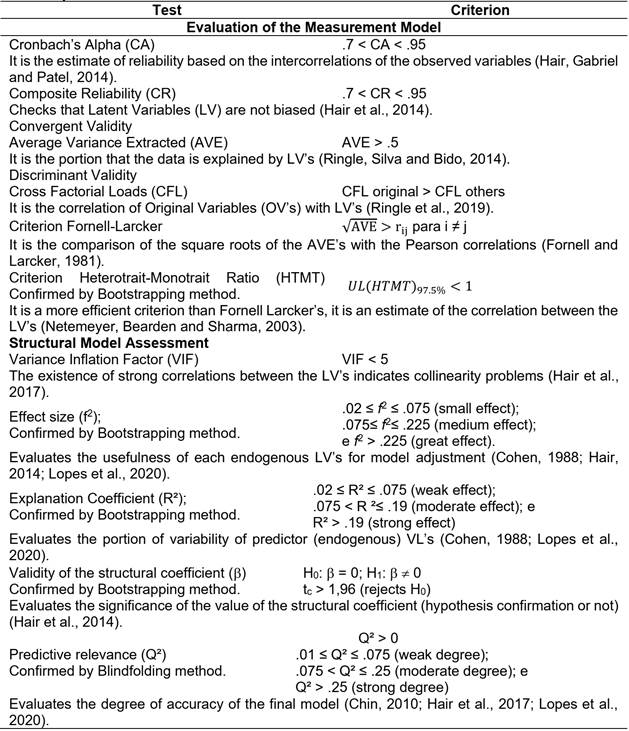

In the preparation phase, the data were sorted by dimension. Afterward, the analyses were started based on the specific objectives stipulated. Initially, the sample was characterized, presenting the profile of the surveyed audit professionals. This analysis took place from the profile identification block, through the frequencies of responses from professionals. Then, to measure the determinants of the intention to pursue a career in auditing, the Structural Equation Modeling (SEM) was used, according to the tests and criteria presented in Table 2.

Table 2

Systematic evaluation of PLS-SEM results.

Note: UL = Upper LimitSource: Elaborated by Lopes et al. (2020), adapted from Ringle, Silva and Bido (2014).

Table 2 addresses the criteria for systematic evaluation of the measurement model and structural model. Initially, to evaluate the measurement model, the convergent validity based on the AVE is analyzed. Then, internal consistency is observed through Cronbach’s Alpha (CA) and Composite Reliability (CR). Finally, the discriminant validity is analyzed by means of Crossed Factor Loadings (CFL), and the Fornell-Larcker and HTMT criteria.

Next, the evaluation of the structural model takes place through the evaluation of collinearity (VIF), the effect size (f2), the explanation coefficient (R2), the validity of the structural coefficient (β) and the predictive relevance (Q²).

4 ANALYSIS AND DISCUSSION OF RESULTS

4.1 Profile of audit professionals

Among the interviewees, in relation to gender, it is observed that the majority are men, approximately 56%, and 44% are women. This result can be supported by previous studies by Inda et al. (2013) and Tetteh et al. (2022) that signal gender inequality, pointing out that women often have lower self-efficacy beliefs than men when deciding on a numerical career, such as auditing. For age, the predominant age group was between 21 and 40 years old (95.19%), of these, 82.37% of professionals are up to 30 years old. For Santos et al. (2018) professionals are starting their careers in the auditing area at an earlier age. As for the marital status of respondents, 226 professionals (72.44%) are single, 80 (25.64%) are married or have a stable union and 6 (1.92%) are separated or divorced. In this aspect, the glass ceiling of the audit is emphasized, which has as a barrier the reconciliation between the personal and professional lives of its professionals, especially the high workload in periods of high demand and the need for constant travel (Cruz et al., 2018). What can justify the result obtained, preeminently men, young and single.

As for the level of education, it was observed that 214 (68.59%) answered that they had an ongoing or completed graduation. In the sample, no professional has a doctorate in progress or completed. This lack of interest in the doctorate was also verified by Bianchi et al. (2019) and Hoff et al. (2017), which demonstrates disaffection for this continuing academic education as a form of insertion or evolution in the labor market. Regarding satisfaction with the undergraduate course and the auditing career, it was observed that, of the 312 professionals surveyed, 177 (56.73%) declared they were “satisfied”, and 60 (19.23%) were “totally satisfied”, that is, most audit professionals evaluate their undergraduate and career courses positively.

As for the factors that motivated respondents to pursue an auditing career, 83% (259 professionals) reported that the “Labor market” was the main factor. Previous studies, which observed the auditing scenario in Brazil, showed that auditing is essential for the operation of business and has been increasingly requested by companies due to the development and expansion of markets (Amorim et al., 2012; Attie, 2018; Silva et al., 2017). These studies point to a rising market, with little expressiveness of auditors, which justifies the fact that the market was listed as the main factor that influenced respondents to pursue an auditing career. Other factors reported were “By admiration” and “By salary expectations”, selected 120 and 96 times, respectively. The answer options “By vocation” and “Status” were also selected, 61 and 51 times, in that order.

As for the economic and professional characteristics of the respondents, almost all responded that they were working, 311 professionals (99.68%). Of these, 304 (97.4%) work directly in the audit area and seven in another area, different from the audit area. When asked about the length of experience in the auditing area, it is observed that 222 professionals (71.15%) have worked for a maximum of 5 years. Of these, 68 and 64 professionals (21.79% and 20.51%) responded, respectively, that they work “from 3 to 5 years” and “from 1 to 2 years”. It is noticed that the length of work is heterogeneous, with the first five years of work standing out.

In addition, it was found that 82.37% of professionals are up to 30 years old and have been in the audit area for 5 years. Data suggest that auditing professionals are potentially starting their careers early, right after or even before graduation, which is supported by Santos et al. (2018). Respondents work professionally, concurrently, or not, in the following sectors: Services, 155 respondents (49.6%), Industry, 133 (42.6%) respondents, Commerce, 22 (.07%) respondents, Third Sector, 16 (.05%) respondents, Public Sector, 12 (.04%) respondents, and finally, 7 (.02%) professionals selected the option “Other”.

About monthly gross earnings, it was observed that 90 professionals (28.85%) had monthly gross earnings “Above 5 national minimum wages (5,225.00 BRL)”, corresponding to the largest stratum of the sample. Furthermore, 187 respondents receive R$ .01 up to 4 salaries, representing approximately 60% of the total sample. Of these, 84 (26.92%) have a monthly income of “Up to 3 salaries (3,135.00 BRL)” and 66 (21.15%) of “Up to 4 salaries (4,180.00 BRL)”. These numbers may be related to the main factors influencing the choice of an auditing career, as presented above.

After characterizing the profile of respondents, the structural model is analyzed below.

4.2 Structural model of career choice intention and work engagement

The exploratory phase measurement model, shown in Figure 2, was built from the theoretical model on career choice intention and work engagement.

Figure 2

Theoretical model career choice intention and work engagement.

Source: The authors.

Figure 2 presents the path model with the respective hypotheses, showing the relationships between the dimensions proposed by the original authors. The collected data were tested following the steps proposed by Ringle et al. (2014) and Hair et al. (2017). We began by analyzing the AVE. The variables PA_07 (( = .181), PA_06 (( = .413), SN_02 (( = .448), SN_03 (( = .526) and VI_07 (( = -.169) were excluded from the initial model because they presented low factor loadings.

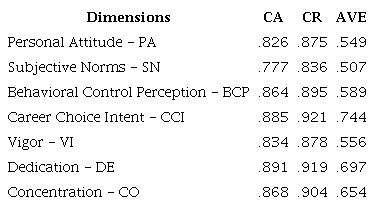

After the exclusions, Table 3 shows the results for Cronbach’s Alpha, Composite Reliability and AVE.

Source: The authors.

We can see in Table 3 the results of the model evaluation, with AVE being all values above .50, showing the convergent validity and reflecting the general amount of variance of the indicators explained by the constructs (Ringle et al., 2014). In addition to the AVE coefficients, it appears that the internal consistency values are adequate, as, according to Hair et al. (2014), present a Cronbach’s Alpha above .7. It is also observed the Composite Reliability values that assess whether the indicator adequately measured the constructs, and for this measure Hair et al. (2014) suggest that values above .8 and .9 are considered satisfactory. Therefore, it appears that this criterion was met.

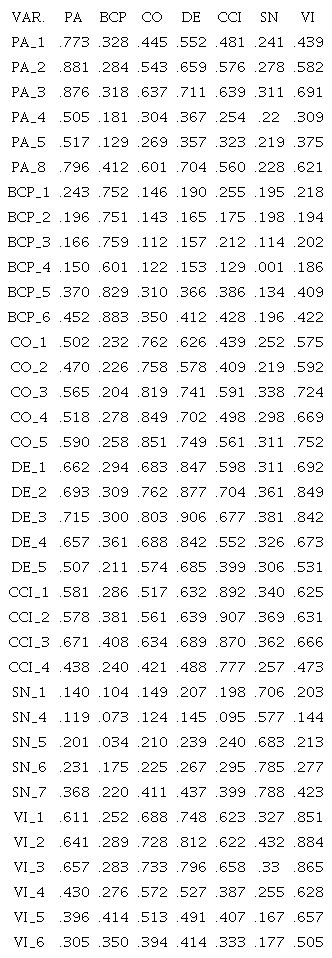

Table 4 presents the values of the crossed factor loadings for the observed and latent variables (dimensions).

Source: The authors.

From Table 4, the variables had higher factor loadings with the original dimensions (latent variables). For Chin (1998) this indicates that there is discriminant validity.

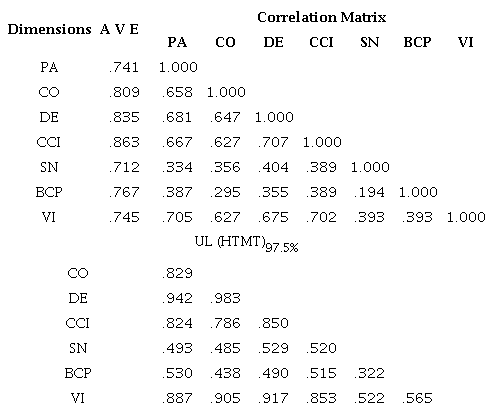

Table 5 presents the validity indicators based on the Fornell-Larker and HTMT criteria confirmed by the bootstrapping method for 5,000 subsamples. In this validity, the square roots of the AVE’s values of each dimension are compared with the correlations between the dimensions (Fornell & Larcker, 1981) and the matrix generated by the HTMT’s is analyzed.

Source: The authors.

For the discriminant validity shown in Table 5, using the Fornell-Larker test, the square roots of the AVE’s were greater than the correlations between the dimensions, meeting the established criteria (Fornell & Larcker, 1981).

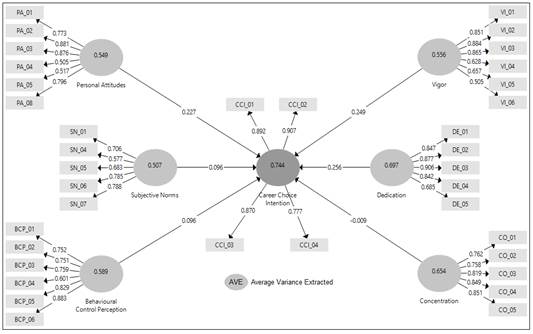

In addition, the HTMT test was performed, which is a more efficient criterion than the other tests (Hair et al., 2017). The HTMT is a true estimate of the correlations between dimensions (Netemeyer et al., 2003). Based on Henseler et al. (2015), UL values (HTMT) 95% < 1,0 indicate that the model has discriminant validity. Figure 3 presents the confirmatory model.

Figure 3 summarizes the results obtained and illustrates the values of the model’s internal coefficients, values of the model’s external loads and values of the AVE.

Figure 3

Confirmatory structural model for career choice behavior

Source: The authors.

After validating the model, the next step sought to assess the predictive capacity and the relationships between the constructs proposed in the model. The evaluation of the structural model is a systematic approach, which according to Hair et al. (2017), can be measured by: collinearity analysis (VIF), the significance level of R2, effect size f2, evaluation of significance and relevance of structural model betas (Student’s t-test), and finally, by evaluation of predictive relevance Q2 (blindfolding method).

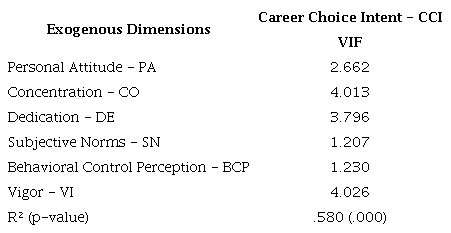

Table 6 presents the VIF, which indicates whether there is a potential collinearity problem in the model and the significance level of the R2.

Source: The authors.

From Table 6, all VIF values are less than 5, given the absence of strong correlations between the dimensions, therefore collinearity is not a major problem (Hair et al., 2017). On the other hand, the variance explained by the model’s explanation coefficient (R²) is 58% for the predictive dimension “Career Choice Intention”.

Subsequently, in Table 7, the values of f², path coefficient (β) and the value of Q² for the evaluation of the structural coefficients are shown.

Note. a Research hypothesis. S.D. = Standard Deviation. Source: The authors.

The quality of the model (Table 7) is evaluated using the Cohen indicator; thus, the size of the effect (f2) considers how useful the dimension is for the adjustment of the model (Cohen, 1988, Hair et al., 2014, Lopes et al., 2020). Based on these authors (see Table 2), the effects were not significant (p > .05), indicating a lack of statistical evidence. However, this does not preclude the possibility of a relationship between the dimensions, thereby confirming the proposed hypotheses.

In the other relationships, the effects are considered null in view of the non-significance found (p > .05). To better understand the relationships between the dimensions of the scales of intention to choose a career and engagement in the work of the surveyed audit professionals, it is important to discuss the relationships between the constructs and confirm the hypotheses raised. Table 7 summarizes the relationships between the constructs, as well as the path coefficients (β) and their significance.

The significance of the structural model coefficients (β’s) are considered based on the model’s relationships, dealing with the correlations with the establishment of the null hypothesis (H0), with β = 0 and the proposed hypotheses must be rejected when p < .05, that is, the path coefficient is different from zero (Ringle et al., 2014) (Table 7). The values of the path coefficients (β’s) suggest the direction and strength of the relationship between the variables in the model. The direction demonstrates whether the relationship between the two variables is directly proportional or inversely proportional. Strength is observed by the t indicator calculated in the analysis of the statistical significance of structural relationships (Hair et al., 2014).

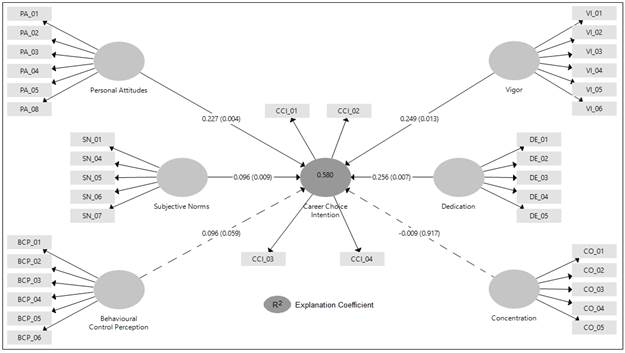

As shown in Table 7, the variables, with an acceptable situation, showed positive path coefficient values (β), directly proportional to the CCI. It appears that t values are statistically significant, above 1.96, for the path coefficients, indicating significance for almost all proposed relationships, except for hypothesis H6, CO → CCI, which obtained a value below 1.96. As well as H3, BCP → CCI, due to the non-significance found (p > .05). It is worth noting that among the dimensions of engagement at work, dedication was the one that presented the greatest explanatory power for the intention to choose to follow a professional career. Thus, it can be inferred that the variables of attitude (PA), subjective norm (SN), vigor (VI) and dedication (DE) are positive, directly proportional, and significant predictors of the intention to choose a career (CCI) in auditing.

After this step, the results obtained in correspondence with the theory were examined. Based on Fishbein and Ajzen (1975), for H1 the results were significant (β1 = .227, tc = 2.901, p = .004), that is, attitude significantly and positively influences the intention to choose to pursue a career audit professional, accepting the first hypothesis. It is noteworthy that the respondents do not perceive extrinsic factors, such as the perception that the auditing career requires aptitude and vocation, and career opportunities in the labor market, as significant influencers on the attitude of following an auditing career. These indicators did not prove to be valid in the factor analysis process, presenting low factor loadings and, therefore, they were not validated in the confirmatory model. A different result was found by Ilias et al. (2022), they found that in accounting students in Malaysia, personal attitudes were not determinant for the intention to choose a career in auditing.

H2 includes the dimension of subjective norms, noting that it is defined as the perceived social pressure to perform or not a behavior (Fishbein and Ajzen, 1975). In this sense, the results were significant (β2 = .096; tc = 2.607; p = .009), corroborating this statement, that is, the evaluation of the perceptions of reference individuals, who are people who exert influence over the researched, affect their intentions. It is noteworthy that professionals in the auditing area, in front of parents, partners, friends and other family members (who showed moderate and low influence) showed greater influence on the professionals surveyed. Ilias et al. (2022), in research with undergraduate students in accounting, also found the construct of subjective norms as a determinant of intention. In their research, the authors concluded that it is possible for friends and teachers to encourage students to become auditors. Rosnidah et al. (2018), in research with accounting students, also found that the undergraduates’ choices for the accounting course are based on the expectations of their family members accompanied by teachers, friends, advisors/consultants and other students.

It is noteworthy about the findings of H2, that in the confirmatory model, factors such as the influence of professors and the admiration and respect of auditing professionals by society were not considered significant in the choice to pursue an auditing career. This is because these indicators did not prove to be valid in the factor analysis process, presenting low factor loadings and, therefore, they are not validated in the structural equation procedure.

H3 considered the perception of behavioral control, which is defined as the perceived ease or difficulty in performing the behavior (Ajzen, 2002). The third hypothesis (H3) sought to verify whether the perception of behavioral control significantly and positively influences the career choice intention of audit professionals. From Table 7, it is inferred that the results were not statistically relevant, as the p-value significance level was greater than 0.05 (β3= .096; tc = 1.910; p = .056), which does not corroborate this affirmation. For the professionals analyzed, the model cannot show that training, experience, knowledge and ability to exercise an auditing career significantly influence their intentions to choose to pursue an auditing career. A distinct result was found by Ilias et al. (2022), who found that the perception of behavioral control impacts the intention of future accounting graduates to pursue an auditing career. Haninda and Elfita (2022) also found that perceived behavioral control positively affects auditors' ethical behavioral intention, differently from what was found for intention to pursue a career.

Then, H4 deals with the vigor dimension, which is related to high levels of energy and mental resilience in the work environment, willingness to invest effort and being persistent, even in difficult situations (Schaufeli et al., 2014). The fourth hypothesis (H4) sought to verify whether vigor influences the career choice intention of audit professionals. The results were significant (β4= .249; tc = 2.417; p = .013), corroborating this statement, in other words, the individual’s level of vigor significantly and positively influences audit professionals, affecting their intentions. Vigor refers to an employee's energy, determination, and consistent investment of effort in their work (Dhanpat et al., 2021). Therefore, the higher the professional's level of vigor, the greater the intention to choose and remain in the auditing career (Fishbein and Ajzen, 1975; Vazquez et al., 2015). It is worth noting, in relation to the findings of H4, that statement 43, VI_07, included by the researchers in light of the established COVID-19 pandemic, had a low factor loading, not being valid in the factor analysis process and, therefore, is not validated in the structural model.

In H5, the predictor factor was dedication, which is characterized by a strong sense of meaning, enthusiasm, inspiration, pride, and challenge in the workplace (Schaufeli et al., 2014). The fifth hypothesis (H5) sought to verify whether dedication influences the career choice intention of audit professionals. The results were positive and significant (β5 = .256; tc = 2.6350; p = .007), corroborating this statement, thus, the individual's level of dedication influences audit professionals, affecting their intentions. Dedication is based on an individual's sense of importance in relation to their work (Bakker, 2017). Therefore, the greater the level of dedication, the greater will be their intention to choose a career in auditing (Fishbein and Ajzen, 1975; Vazquez et al., 2015).

Finally, H6 included the concentration dimension, which is characterized by the individual being involved in a state of total concentration and happiness, immersed in the work environment, making time pass quickly and it is difficult to completely disconnect from work (Schaufeli et al. al., 2014). The sixth hypothesis (H6) sought to verify whether concentration influences the career choice intention of audit professionals. The results obtained were not statistically relevant, as the significance level of the p value was greater than 0.05 and the strength observed by the t indicator was less than 1.96 (β6= -.009; tc = .106; p = .917), being unsupported. Concentration implies that employees have high levels of focus and immersion at work, while relaxing or taking a break is uncommon (Bakker, 2017). Thus, the structural model did not show that the level of concentration significantly influences the intention to choose a career for the professionals analyzed.

That said, Figure 4 demonstrates the final path model of the relationships between the dimensions of intention career choice and engagement at work.

Figure 4

Final model for career choice intention and work engagement.

Source: The authors.

The degree of accuracy of the final model was evaluated (Figure 4). According to Lopes et al. (2020), the Q2 values estimated by the blindfolding process represent a measure of how well the path model can predict the originally observed values.

Table 8 shows the values of the blindfolding measure and predictive relevance (Q2) for the career choice intention and job engagement model.

Note: *SOS = Sum of Observed Squares; **SSE = Sum of Squares of Errors. Source: The authors.

Table 8 was analyzed based on Chin (1998) and Hair et al. (2017). According on these authors, the following criteria for Q2 assessment were considered in Table 2. In the present model, it was found that there is a strong predictive validity, as the Q² has a value greater than zero (Q² = .416), that is, the model can be considered relevant. At the end of the stages proposed by Hair et al. (2017) and Ringle et al. (2014), the results are interpreted to achieve the objective of evaluating the relationships between the career choice intention scales of Santos et al. (2018) and the UWES by Vazquez et al. (2015), using the structural equation model.

The measurement model presented internal consistency measures: satisfactory Cronbach’s Alpha and Composite Reliability coefficients. The convergent validity (AVE’s) indicated the model’s convergence, with all constructs presenting AVE’s above 0.5. For analysis of discriminant validity, the HTMT criterion was used, calculated by the bootstrapping procedure, in which values lower than 1 were obtained for the relationships between the constructs. The structural model was then evaluated, with the identification of collinearity through the VIF indicator, which presented values below 5, indicating that the collinearity reached critical levels, not presenting problems for the estimation of the model.

The calculation of the coefficient of determination of R2 (a measure of the predictive capacity of the model) was also applied, obtaining consistent results for the predictive capacity. The evaluation of f2 showed both small and large effect sizes. Finally, by performing the blindfolding procedure, the predictive validity measure Q2 was calculated, which assesses the accuracy of the adjusted model, obtaining values greater than zero, identifying the relevance of the model of intention to choose a career and work engagement.

Thus, according to the indicators used, it can be inferred that the relationships between the dimensions of the Career Intention Scale and the dimensions of the Work Engagement Scale are supported. Therefore, the conclusion is presented below.

5 CONCLUSION

For the audit profession, the intention to decide on a career does not only consist in choosing a field of activity within the accounting area but also in the engagement to maintain it, considering that engagement can reflect on the quality and productivity of the work. Therefore, in this study, the question was: do attitudinal, subjective norms, behavioral perception, and engagement at work determine the audit professional’s intention to choose the career? For this, a questionnaire was applied to audit professionals in Brazil, comprising validated scales on the intention to choose a career and engagement at work.

Initially, the profile of the surveyed audit professionals was described. In general, the sample surveyed is composed of men, between 21 and 30 years of age, single, with an undergraduate degree, and who consider themselves satisfied with the undergraduate course and auditing career. As for the economic and professional characterization, most are working in the auditing area, have three to five years of experience in the respective profession, and have a gross monthly income above five national minimum wages. The job market was the main factor that motivated them to pursue a career in auditing.

Then, structural equation modelling was developed to demonstrate the determinants of the intention to choose a career. In modelling, the attitude dimension proved to be a positive influence on the intention to choose the career of audit professionals. Thus, the intrinsic factors of these professionals proved to be determinants of the intention to choose and maintain a professional career in auditing, supporting the first hypothesis developed. However, these professionals do not perceive extrinsic factors as influencing factors, such as the perception that the auditing career requires aptitude and vocation and career opportunities in the labor market.

As for the subjective norms, the results were significant and positive, accepting the second research hypothesis. Therefore, the professionals’ reference people, who influence their decisions, affect their intentions to choose a career. However, it is worth noting that the professionals in the auditing area proved to be people of reference for those surveyed. As for the perception of behavioral control, the results obtained were not statistically relevant, and the third hypothesis was not supported. Thus, for auditing professionals, there was no relationship between the sufficiency of preparation, practical experience, knowledge, and ability to exercise the auditing career as determinants for the intention to pursue an auditing career.

When analyzing the vigor dimension, the results were significant, supporting the fourth hypothesis. Thus, the individual’s level of vigor exerts a positive influence on his intention to choose a career. Likewise, for dedication, the results were significant, accepting the fifth research hypothesis. In this sense, the dedication of the audit professional proved to be a positive determinant of their career ambitions. While for the concentration dimension, the results were not statistically significant, the sixth research hypothesis was rejected. For the professionals surveyed, concentration was not shown to have the potential to predict the intention to pursue a career in auditing.

Thus, it was found that the dimensions of vigor and dedication are presented as determinants of intention, demonstrating greater strength among the observed relationships, confirming the theoretical relationship between the scales. Therefore, the general objective of analyzing the antecedents attitudinal, subjective norms, behavioral perception, and engagement in the work that determine the intention to choose the audit professional’s career was achieved. It was concluded that the relationships between the dimensions of the career choice intention scale and the dimensions of the work engagement scales are supported. It is worth noting that in the modelling the dimensions attitude, subjective norms, vigor, and dedication presented an explanatory power of 58% of the intention to choose the career of audit professionals.

The study presents practical and theoretical contributions, as it was not identified in the scientific literature, until the end of 2021, any study that contemplated simultaneously the two themes researched here, which reinforces the original character of the present research. Thus, this study filled this gap in the behavioral area, helping to understand the auditor’s behavior. Additionally, this study encourages the use of Social Psychology theories in accounting and contributes to the dissemination of the adoption of structural equation modelling as a means for data analysis.

As limitations of the research, the questionnaire adopted is mentioned, which, to a certain extent, restricts the validity of the results, as there may be other variables that influence the intention to choose a career, as well as other variables that determine engagement at work, which were not considered. Another limiting factor refers to the scarcity of studies focused on work engagement in the audit area. Finally, the difficulty of reliably estimating the size of the population surveyed is reported, namely, independent auditors, internal auditors, assistants, among other audit professionals working in Brazil.

The results found here, although specific to Brazilian audit professionals, can be analyzed, compared, and inspire new research in other contexts, which may contribute and encourage the development of studies focused on behavior. For future research, the adoption of different means for data collection is suggested, as well as the consideration of different variables for analysis, such as aspects related to culture or professional training.

REFERENCES:

Ajzen, I. (2002). Perceived behavioral control, self‐efficacy, locus of control, and the theory of planned behavior. Journal of Applied Social Psychology, 32(1), p.665-683.

Ajzen, I. (1991). The Theory of Planned Behavior. Organizational Behavior and Human Decision Processes, 50(2), p. 179-211.

Ajzen, I. (2015). The theory of planned behavior is alive and well, and not ready to retire: a commentary on Sniehotta, Presseau, and Araújo-Soares. Health Psychology Review, 9(2), p.131-137.

Ajzen, I. & Fishbein, M. (1980). Understanding Attitudes and Predicting Social Behavior, Prentice Hall, Nova Jersey.

Akgunduz, Y., Bardakoglu, O., & Kizilcalioglu, G. (2022). Happiness, job stress, job dedication and perceived organizational support: a mediating model. Journal of Hospitality and Tourism Insights. p.2514-9792. 10.1108/JHTI-07-2021-0189.

Alev, S. (2022). The mediating role of psychological well-being in the relationship between the psychological contract and professional engagement. Psihologija, 55(3), p.227-244

Almeida, M. C. (2019). Auditoria: abordagem moderna e completa. 9. ed. São Paulo: Atlas.

Amorim, E. N. C., Vicente, E. F. R., Will, A. R., & Silva, F. A. (2012). O mercado de auditoria no Brasil: um retrato considerando a percepção das firmas de auditoria. Revista Catarinense da Ciência Contábil, 11(32), p.73-97.

Attie, W. (2018). Auditoria: conceitos e aplicações. 7th ed., Atlas, São Paulo, SP.

Avigo, R. O., Caldeira, L. B., Melo, D. C., & João, I. S. (2017). Funcionário público engajado no trabalho? Uma análise do engajamento de profissionais da tecnologia da informação do serviço público federal. Anais doXLIEncontro da ANPAD. São Paulo.

Bakker, A. B. (2017). Strategic and proactive approaches to work engagement. Organizational Dynamics, 46(2), p.67-75. https://doi.org/10.1016/j.orgdyn.2017.04.002

Batista, T. C., & Marçal, R. R. (2020). Teoria do Comportamento Planejado e contabilidade: um estudo sobre a validade da teoria diante da opção pela carreira acadêmica contábil. Brazilian Journal of Management & Innovation, 8(1).

Bianchi, M., Werlang, J. D., Venturini, L. dal B., & Machado, V. N. (2019). Percepção dos discentes do curso de Ciências Contábeis e da Especialização em Perícia e Auditoria acerca do ensino e do mercado de trabalho em Auditoria. Revista Ambiente Contábil, 11(2), p.266-285.

Bouckenooghe, D., De Clercq, D., Naseer, S., & Syed, F. (2022). A curvilinear relationship between work engagement and job performance: the roles of feedback-seeking behavior and personal resources. Journal of Business and Psychology, 37(2), 353-368. https://doi.org/10.1007/s10869-021-09750-7

Camargo, R. C. C. P., Camargo, R. V. W., Dutra, M. H., & Alberton, L. (2013). A percepção dos auditados em relação às competências comportamentais dos auditores independentes: um estudo empírico na Região da Grande Florianópolis/SC. Revista de Contabilidade e Organizações, 7(18), p.37-47.

Cavalcante, M. M., Siqueira, M. M. M., & Kuniyoshi, M. S. (2014). Engajamento no trabalho, bem-estar no trabalho e capital psicológico: um estudo com profissionais da área de gestão de pessoas. Revista Pensamento & Realidade, São Bernardo do Campo, 29(4), p.44-45.

Chin, W. W. (1998). The partial least squares approach for structural equation modeling in Marcoulides, G. A.(Ed.), Modern Mothods for Business Research, Lawrence Erlbaum Associates, London, p.295-336.

Cohen, J. (1988). Statistical Power Analysis for the Behavioral Sciences. 2nd ed., Psychology Press, Nova York, NY.

Conselho Federal de Contabilidade. (2019b). NBC PG 01: Código de ética profissional do contador. Brasília, CFC, 2019a. Disponível em: <https://www1.cfc.org.br/sisweb/SRE/docs/NBCPG01.pdf>

Conselho Federal de Contabilidade. (2019a). NBC PG 100 (R1): Cumprimento do código, dos princípios fundamentais e da estrutura conceitual. Brasília: CFC. Recuperado de: https://www1.cfc.org.br/sisweb/SRE/docs/NBCPG100(R1).pdf

Conselho Federal de Contabilidade. (2017). NBC PG 12 (R3): Educação profissional continuada. Brasília: CFC . Recuperado de: https://www1.cfc.org.br/sisweb/SRE/docs/NBCPG12(R3).pdf

Conselho Federal de Contabilidade. (2016). NBC TA 200 (R1): Objetivos gerais do auditor independente e a condução da auditoria em conformidade com normas de auditoria. Brasília: CFC . Recuperado de: https://www2.cfc.org.br/sisweb/sre/detalhes_sre.aspx?Codigo=2016/NBCTA200(R1)

Crepaldi, S. A., & Crepaldi, G. S. (2019). Auditoria contábil: teoria e prática. 11th ed., Atlas, São Paulo, SP .

Cruz, N. G., Lima, G. H, Durso, S. D., & Cunha, J. V. (2018). Desigualdade de Gênero em Empresas de Auditoria Externa. Contabilidade, Gestão e Governança, 21(1), p.142-159. https://doi.org/10.51341/1984-3925_2018v21n1a8

Dhanpat, N., Danguru, D. L., Fetile, O., Kekana, K., Mathetha, K. N., Nhlabathi, S. F., & Ruiters, E. (2021). Self-management strategies of graduate employees to enhance work engagement. SA Journal of Industrial Psychology, 47(1), p.1-12. https://dx.doi.org/10.4102/sajip.v47i0.1857

Elias, A. L. de O., Mansano, R. S., & Campanhol, E. M. (2014). Questões éticas na auditoria independente: a auditoria da empresa Arthur Andersen na empresa Enron. Diálogos em Contabilidade: teoria e prática, 1(2), jan./dez.

Fernandes, C. M., Siqueira, M. M. M., & Vieira, A. M. (2014). Impacto da percepção de suporte organizacional sobre o comprometimento organizacional afetivo: o papel moderador da liderança. Revista Pensamento Contemporâneo em Administração, Rio de Janeiro, 8(4), p.140-162.

Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention and behavior: an introduction to theory and research. Addison-Wesley, Reading, MA.

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error, Journal of Marketing Research, 18(1), p.39-50.

Freitas, L. A. V. de, & Charão-Brito, L. (2016). Engajamento no trabalho: um estudo em profissionais multidisciplinares de saúde em um município da região sul. Revista CESUMAR Ciências Humanas e Sociais Aplicadas, 21(2), p.407-419.

Hair, J. F., Black, W. C., Babin, B., Anderson, R. E., & Tathan, R. L. (2009). Multivariate Data Analysis. 6th ed., International Thomson Business Press, Índia.

Hair, J. F., Gabriel, M. L. D. S., & Patel, V. K. (2014). Modelagem de Equações Estruturais Baseada em Covariância com o AMOS: Orientações sobre a sua aplicação como uma Ferramenta de Pesquisa de Marketing, Revista Brasileira de Marketing, 13(2), p.44-55.

Hair, J. F., Hult, G. T. M., Ringle, C., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM), Sage Publications, Los Angeles, LA.

Haninda, S. H., & Elfita, R. A. (2022) The Moderating Role of Religiosity on Ethical Behavioral Intention: Planned Behavioral Theory Approach. Business and Finance Journal, 7(1). p. 93-104. https://doi.org/10.33086/bfj.v7i1.2372

Hansen, R., Fabricio, A., Lopes, L. F. D., & Rotili, L. B. (2018). Inteligência Emocional e Engajamento no Ambiente de Trabalho: Estudo Empírico a partir de Trabalhadores Gaúchos. Revista Gestão Organizacional, 11(1), jan./abr.

Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling, J. Acad. Mark. Sci., 43, p.115-135.

Hoff, J., Alberton, L., & Camargo, R. de C. C. P. (2017). A visão da academia e do mercado de trabalho sobre o ensino da auditoria, Revista de Educação e Pesquisa em Contabilidade, 11(1), p.52-68.

Hussain, K., Ahmed, I., & Aamir, M. (2022). Ethical Leadership and Auditor’s Underreporting of Audit Time: Mediating Role of Work Engagement. Review of Applied Management and Social Sciences, 5(2), 231-242. https://doi.org/10.47067/ramss.v5i2.231

Ilias, A., Baidi, N., Ghani, E. K., & Rahman, R. A. (2022). Factors Driving the Intention to Pursue Internal Auditing Certification and Career among Future Graduates in Malaysia. Universal Journal of Accounting and Finance, 10(2), p.549-558. DOI: 10.13189/ujaf.2022.100219.

Inda, M., Rodriquez, C., & Pena, J. V. (2013). Gender differences in applying social cognitive career theory in engineering students. Journal of Vocational Behaviour, 83(3), p. 346-355. https://doi.org/10.1016/j.jvb.2013.06.010

Iudícibus, S. de, Martins, E., Kanitz, S. C., Ramos, A. de T., Castilho, E., Benatti, L., et al. (2019). Contabilidade introdutória. 12th ed., Atlas, São Paulo, SP .

Krüger, C., & Ramos, L. F. (2020). Comportamento empreendedor, a partir de características comportamentais e da intenção empreendedora, Revista de Empreendedorismo e Gestão de Pequenas Empresas, 9(4), p.556-583.

Lee, Y., Kwon, K., Kim, W., & Cho, D.(2016). Work Engagement and Career: Proposing Research Agendas Through a Review of Literature. Human Resource Development Review, 15(1), p.29-54. https://doi.org/10.1177/1534484316628356

Llorens, S., Schaufeli, W., Bakker, A., & Salanova, M. (2007). Does a positive gain spiral of resources efficacy beliefs and engagement exist? Computers in Human Behavior, 23(1), p.825-841. https://doi.org/10.1016/j.chb.2004.11.012.

Lopes L. F. D., Chaves, B. M., Fabrício, A., Porto, A., Almeida, D. M., Obregon, S. L., Lima, M. P., Silva W. V., Camargo, M. E., Veiga, C. P., Moura, G. L., Silva, L. S. C. V., Costa, V. M. F. (2020). Analysis of Well-Being and Anxiety among University Students. International Journal of Environmental Research and Public Health. 17(11), p. 3874. https://doi.org/10.3390/ijerph17113874

Mendonça, S. L., Martins, V. F. (2016). Decidi ser auditor: Um recorte de auditores e ex-alunos de uma instituição federal de ensino superior, Revista de Auditoria, Governança e Contabilidade, 4(13), p. 173-192.

Mercali, G. D., & Costa, S. G. (2019). Antecedentes do engajamento no trabalho dos docentes de ensino superior no Brasil, Revista de Administração Mackenzie, 20(1), p.1-28.

Mota, R., & Martins, V. F. (2018). Novo relatório do auditor independente: uma análise dos principais assuntos de auditoria evidenciados nas empresas do setor aéreo brasileiro, Revista de Auditoria, Governança e Contabilidade, 6(25), p. 65-84.

Moutinho, K., & Roazzi, A. (2010). As teorias de ação racional e de ação planejada: relações entre intenções e comportamentos, Avaliação Psicológica, 9(2), p.279-287.

Netemeyer, R. G., Bearden, W. O., & Sharma, S. (2003). Scaling procedures: issues and applications. Sage Publications, Thousand Oaks, CA.

Neuber, L., Englitz, C., Schulte, N., Forthmann, B., & Holling, H. (2022) How work engagement relates to performance and absenteeism: a meta-analysis, European Journal of Work and Organizational Psychology, 31(2), 292-315, https://doi.org/10.1080/1359432X.2021.1953989

Neves, M. M., Trevisan, L. N., & João, B. N. (2013). Carreira proteana: revisão teórica e análise bibliométrica, Revista Psicologia Organizações e Trabalho, 13(2), p.217-232.

Niyama, J. K., Costa, F. M., Dantas, J. A., & Borges, E. F. (2011). Evolução da regulação da auditoria independente no Brasil: análise crítica, a partir da teoria da regulação, Advances in Scientific and Applied Accounting, 4(2), p.127-161.

Oliveira, F. A., & Ciupak, C. (2017). Auditoria interna e externa em que elas se Complementam. (Aperfeiçoamento/Especialização em Auditoria e Controladoria Empresarial). Universidade Federal de Mato Grosso, Mato Grosso.

Pacheco, E., & Camilo, S. O. (2020). Competências essenciais requeridas na contratação de auditores profissionais em início da carreira, Revista de Auditoria, Governança e Contabilidade, 8(32), p.117-131.

Ramdani, M.; Arumbarkah, A., & Lestari, I.(2019). The Perception of Auditor Career From University Students Perspective. JEMA: Jurnal Ilmiah Bidang Akuntansi dan Manajemen. 16(1), p.104-116. http://dx.doi.org/10.31106/jema.v16i1.1908

Ribeiro, O. M. (2017). Contabilidade básica. 30th ed., Saraiva, São Paulo, SP.

Ringle, C. M., Silva, D., & Bido, D. S. (2014). Modelagem de equações estruturais com utilização do SmartPLS, Revista Brasileira de Marketing, 13(2), p.56-73.

Rosnidah, I., Johari, R. J., Sulistyowati, W. A., Siddiq, D. M., Setiawan, A. (2018). Students’ Intention in Pursuing Accounting Study: Theory of Planned Behaviour Perspective. Advanced Science Letters, 24(12), p.9475-9478. https://doi.org/10.1166/asl.2018.12301

Salanova, M.; Agut, S.; Peiró, J. M. (2005). Linking organizational resources and work engagement to employee performance and customer loyalty: the mediation of service climate. Journal of applied Psychology, 90(6), p.1217-1227. https://doi.org/10.1037/0021-9010.90.6.1217.

Santos, E. A., & Almeida, L. B. (2018). Seguir ou não carreira na área de contabilidade: um estudo sob o enfoque da Teoria do Comportamento Planejado, Revista de Contabilidade e Finanças da USP, 29(76), p.114-128.

Santos, E. A., Moura, I. V., & Almeida, L. B. (2018). Intenção dos Alunos em seguir carreira na Área de Contabilidade sob a Perspectiva da teoria do Comportamento Planejado, Revista de Educação e Pesquisa em Contabilidade, Brasília, 12(1), p.66-82.

Schaufeli, W. B., Dijkstra, P., & Vazquez, A. C. (2013). Engajamento no trabalho. São Paulo, SP: Casa do Psicólogo.

Schaufeli, W. B., Salanova, M., González-Romá, V. & Bakker, A. B. (2002). The measurement of engagement and burnout: a two-sample confirmatory factor analytic approach. Journal of Happiness Studies, 3, p.71-92.

Schaufeli, W. B, Truss, C., Delbridge, R., Alfes, K., Shantz, A., & Soane, E. (2014). What is engagement? Employee engagement in theory and practice, Routledge, UK.

Silva, M. C. da, Martins, V. F, & Rocha, V. A. da. (2017). A profissão de Auditor: Como está a motivação dos discentes de ciências contábeis para seguir esta carreira? Revista de Auditoria, Governança e Contabilidade, 4(17), p.154-174.

Siqueira, M. M. M., Martins, M. C. F., Orengo, V., & Souza, W. (2014). Engajamento no trabalho. In: Siqueira, M. M. M. (Org.). Novas Medidas do Comportamento Organizacional. Ferramentas de Diagnóstico e Gestão. Porto Alegre: Artmed, p.147-154.

Tetteh, L.A., Agyenim-Boateng, C., Kwarteng, A., Muda, P., & Sunu, P. (2022). Utilizing the social cognitive career theory in understanding students’ choice in selecting auditing as a career: evidence from Ghana. Journal of Applied Accounting Research, 23(3), p.715-737. https://doi.org/10.1108/JAAR-03-2021-0079

Vazquez, A. C. S., Magnan, E. dos S., Pacico, J. C., Hutz, C. S. & Schaufeli, W. B. (2015). Adaptation and validation of the Brazilian version of the Utrecht Work Engagement Scale, Psico-USF, 20(2), p.207-217.

Vergara, S. C. (2015). Métodos de pesquisa em Administração. 6th ed., Atlas, São Paulo, SP .

Zago Júnior, S. C., Barbosa, A., & Pavão, J. A. (2020). Ser ou não ser um estudante do curso de Ciências Contábeis, eis a questão: um estudo à luz da Teoria o Comportamento Planejado. Revista Contabilidade e Controladoria, Curitiba, 11(2), p.96-107. http://dx.doi.org/10.5380/rcc.v11i2.70999

Appendix A

Research Instrument Block I - Career choice intention

Indicate your degree of agreement with the statements, using the following: the number 1 [one] indicates that you TOTALLY DISAGREE, while the number 7 [seven] indicates that you TOTALLY AGREE.

Please mark only one alternative per question and be sure to answer none!

The following statements are related to your interest in pursuing a professional career in the auditing area.