Evaluate the use of farmlands encumbered with electric grid facilities: damage factors and solution approaches

Evaluación del uso de tierras de cultivo con instalaciones de la red eléctrica: factores de daño y enfoques de solución

Evaluate the use of farmlands encumbered with electric grid facilities: damage factors and solution approaches

Opción, vol. 34, no. 85-2, pp. 677-705, 2018

Universidad del Zulia

Received: 13 January 2018

Accepted: 22 March 2018

Abstract: This article presents solution approaches towards the effective use of farmlands encumbered with electric grid facilities. This problem is characterized not only by the difficulties in the process of land cultivation, but also by other damage factors affecting this process, as well as yields, tax and rent losses. The choice of methods for assessing the negative processes is regarded as one of the major problems when it comes to placing electric grid facilities. The use of economic tools in assessing damage and finding the most profitable way to use farmlands for placing and running electric grid facilities was substantiated.

Keywords: electric grid, facilities, suspension towers, farmland.

Resumen: Este artículo presenta enfoques de solución para el uso efectivo de tierras agrícolas con instalaciones de rejillas eléctricas. Este problema se caracteriza no solo por las dificultades en el proceso de cultivo de la tierra, sino también por otros factores de daño que afectan este proceso, así como por los rendimientos, las pérdidas de impuestos y rentas. La elección de métodos para evaluar los procesos negativos se considera uno de los principales problemas a la hora de ubicar las instalaciones de la red eléctrica. Se comprobó el uso de herramientas económicas para evaluar los daños y encontrar la forma más rentable de utilizar las tierras de cultivo para la instalación y el funcionamiento de las instalaciones de la red eléctrica.

Palabras clave: red eléctrica, instalaciones, torres de suspensión, tierras de cultivo.

1. INTRODUCTION

In difficult geopolitical environment, the Russian Federation will not develop without a proper infrastructure based on facilities ensuring the critical infrastructure activity. Electric grid facilities are exactly the type (Gans-Morse, 2017; Wegren, 2014). The ongoing changes in the legislation on the real estate provisions have not provided for a clear understanding of how to interpret the system of creating a right (Markus, 2015; Cook, 2013; Uzun and Shagaida, 2015). First and foremost, this is the case of linear facilities, including those that are considered in this paper – electric power transmission lines that are part of the electric grid facilities. This situation is typical for the most of the post-Soviet states (Prishchepovet al., 2013; Newell and Henry, 2016; Maksimova et al., 2017).

Technical accounting of linear facilities became logical and methodical-based only with the adoption of the Regulation on the State Technical Accounting and Technical Inventory of the Objects of the Town Development Activity in the Russian Federation, approved by Decree of the Government of the Russian Federation No. 921 (04.12.2000). Changes reflecting the uniqueness of linear facilities were introduced to the Rules of maintaining the Unified State Register of Rights to Real Estate and Transactions Therewith by the Decree of the Government of the Russian Federation No. 710 only in the end of 2006 (November 22, 2006). Currently, rights to line facilities are registered according to the Federal Law No. 218-FZ (The Federal Law of 13.07.2015 No. 218, 2015).

Legal land owners are interested in whether there is a risk of unexpected losses associated with the lack of information about encumbrances in the Unified State Register of Real Estate. In most cases, they are concerned about the infill construction on the territory of 1.0-3600 square meters (10 kV and 750 kV suspension towers, respectively) depending on facility’s design and material. Protected zones are established for all electric grid facilities, which width is set depending on the voltage level in accordance with RF Government Resolution No. 160 (RF Government Resolution of 24.02.2009 No. 160). It ranges from 2 to 40 meters on the other side of the outer power line. Information about the protected zone boundaries is being entered in the Real Estate Cadastre. In the future, cadastral documents are subject to the Regulations on Protection of Electrical Networks Placed on Land Parcels. As from the date of protected zone establishment, individuals allowed to agree their actions in protected zones are obliged to carry out them in accordance with the conditions ensuring the safety of electric grid facilities (RF Government Resolution of 24.02.2009 No. 160).

In the case of right holders, encumbrances on electric grid facilities do not simply impose certain obligations on the owner, but necessitates establishing economically viable relationships based on the interests of participants in them. We have considered and substantiated the issue of introducing correction factors in the process of calculating levy and rent. We have also provided propositions on how to calculate payment for a linear facility zone under the protection established on the territory with suspension towers, which are networked into a single site by the overhead power transmission lines (OHTL) (Lepekhin and Lepekhin, 2015), (Shurygin & Krasnova, 2017).

We will be focused on mainly on studying the economic mechanism for establishing protection zones around power transmission lines, on developing the compensation measures for land users encumbered by legal peculiarities of a protected zone.

According to the Article 57 of the Land Code of the Russian Federation, losses resulted from limiting the rights of landholders, land users and land tenants are subject to full reimbursement. The damage compensation procedure is established by the Decree of the Government of the Russian Federation No. 262 (May 7, 2003). However, damage compensation claim made due to the protected zone establishment has been rejected according to the Decree of the Supreme Arbitration Court of the Russian Federation No. VAS- 18041/12 (January 21, 2013) (Zolotova, 2016).

Solution approaches towards the process of assessing compensation payments for the encumbrances imposed by the holder of the right to power transmission lines upon the land owned by a landholder are considered in regards to the economic tools (Vershinin et al., 2016).

The major difference between the US and Russian laws on servitudes is that in the US, servitudes can be adopted for the utility lines and systems. They can also be adopted in favor of both the real estate (utility lines and systems) and a specific legal entity (facility owner) (Gilbert, 2016; Menon et al., 2017).

At the same time, the process of imposing encumbrances on power and connection lines, pipelines, railways and other similar facilities is not legally binding in the US. Facility owners have the right to purchase land under them and in property and in rent (Hanstad, 2016).

In France, for example, lands with power lines on them are also classified as servitudes (Jepsen et al., 2015; Kaas et al., 2016).The Sweden experience is of particular interest, as there are servitudes for buildings (ledningsratt), providing for the obligation to impose encumbrances on pipelines, telecommunication and telephone lines, electric grids, etc. Sweden was the first country where servitudes transformed into specific property rights (Bostedt et al., 2015).

In order to solve these problems, we have to develop correction factors for determining the land tax, rent and easement payments. In this study, we have considered different types of economic damage resulting from business restrictions for land market participants, which should be used while developing damage reduction methods and methods for calculating levy and rent paid for the land with imposed encumbrances, for example – electric grid facility zones (Dinershtein & Aleeva, 2017).

2. RESULTS

In the Russian Federation, the greatest share of linear facilities is represented by power transmission lines (about 68%). Protection zones around the power transmission lines can be registered through (Murasheva and Lepekhin, 2014):

- 1.

1) Renting a part of the land parcel;

2) Easement;

3) Land seizure for the purpose of placing and running a facility.

If one is paying rent for a land parcel to establish a protected zone, both the farmer and the person owning the electric grid facility have their own benefits, as the owner of the electric grid facility undertakes to compensate the compulsory land taxes and lost profits from non-produced agricultural products on agricultural lands. In turn, he/she has the unimpeded access to own facility for repair and maintenance. The downside is that this rental payment paid to the owner of a land parcel entails an increase in electricity tariffs for other users.

There have been innovations in the regulation of leasing relations after the Federal Law No. 171-FZ "On Amendments to the Land Code of the Russian Federation and Certain Legislative Acts of the Russian Federation" entered into force on March 1, 2015:

- 1.

1. Recognizing public land lease agreements without tenders in case of granting to entities for placing facilities designed to provide electricity, heat, gas and water supply, water discharge, communications, oil pipelines, objects of federal, regional or local importance (Federal Law of 25.10.2001, No. 136-FZ).

2. Introducing land use provisions for land, which is wholly or partially located in the protected zone established around the linear facility: land lease agreements must provide for the conditions for access to the facility for representatives sent by the owner of a linear facility or representatives of the organization running the facility in order to provide its safety (Federal Law of 25.10.2001, No. 136-FZ).

3. Land lease agreements that are made for placing linear facilities are settled for a period of up to forty-nine years (Federal Law of 25.10.2001, No. 136-FZ).

4. Rental rates for public land, granted for placing facilities, according to the subparagraph 2 of paragraph 1 of the Article 49 of the Land Code of the Russian Federation (including certain linear facilities), may not exceed the rental rates fixed for relevant purposes that is realized on the federal land (Federal Law of 25.10.2001, No. 136-FZ).

According to the Resolution of the Government of the Russian Federation No. 582 "On the Basic Principles of Determining Rents in Case of Leasing State-owned or Municipal Land Parcels and the Rules for Determining Rental Rates, as well as the Procedure, Conditions and Deadlines for Making Lease Payments for Land Owned by the Russian Federation" (July 16, 2009), rental rates for land use are calculated by the formula:

Where:

Vcadastral. – specific index of cadastral value for the relevant types of land use, RUB per 1 square meter;

S – area of the land parcel or part thereof, which is the subject of a land lease agreement, square meters;

Vr.r. – rental rate, (in %);

CSEC – coefficient of socio-economic characteristics: categories of tenants, targeted land use in accordance with the land lease agreement, the social significance of the activity carried out by the tenant on this land parcel;

m – number of months when the rent was paid in the current year.

Electric power enterprises are directly interested in establishing private easements legally, as it is allowed to register rights without making an agreement with the land owners. However, the process of establishing private easements involves the process of signing appropriate agreements with certain entities. Since power transmission lines are very long and often pass through the lands owned by many landholders and districts, easement registration procedure may take some time. As reaching a compromise with an owner is not always possible, a procedure is complicated by litigations.

Easement payments paid for public land parcels are regulated according to the paragraph 2 of the Article 39.25 of the Land Code of the RF (March 1, 2015). The procedure for determining them is established by the Government of the Russian Federation, the governments of the RF subjects and the local self-government bodies. Easement payments paid for federal land parcels are established in the RF Government Decree No. 1461 (December 23, 2014):

- 1.

1) 0.01 percent of a parcel’s cadastral value per year;

2) The difference between the market value of rights to the land parcel before and after establishing easement, calculated by an independent appraiser (if the land parcel is granted to third parties).

One is able not to register a part of a land parcel (easement) if the easement is established under an easement agreement, regarding a part of a public land parcel signed for a period up to 3 years. Easement covers the territory, which boundaries are fixed in accordance with the scheme of easement borders on the territory’s cadastral plan, attached to the easement agreement (par. 4, Article 39.25 of the LC RF).

The adequate value of \permanent easement payment is calculated as follows:

Where:

Vno res. – market value of the land without restrictions (easements);

Seasement – area of land parcel with established easement;

St – total land area;

Cd – coefficient that takes into account the degree of owner’s rights restriction.

In terms of an individual owning a land parcel, the easement is not a profitable, but an unprofitable measure. The owner of an electric grid facility will, naturally, have a number of advantages after establishing an easement, but we assume that the easement is not popular in practice.

There is also a third way of establishing a protected zone – land seizure. The legal framework for state-owned and municipal land seizure is provided for by the Chapter VII.1 of the Land Code of the Russian Federation.

Land seizure is a compulsory alienation of a land parcel from the right holder.

Its goal is to satisfy the state or municipal needs (there is no legal definition).

Seizure principles:

-

- Exclusivity (there are no other variants where to place the facility);

- Reimbursement (compensating market value and losses / providing land in return for the seized one);

- Reasonableness.

Land seizure conditions:

-

- Approving territorial planning documents and projects while building and re-building facilities of federal, regional and local importance;

- Making a decision to create or expand a protected natural area;

- International treaty;

- Subsoil use license;

- Making a decision to recognize the building as a failing one or as one that is/isn’trepairable (Federal Law of 25.10.2001, No. 136-FZ).

List of organizations eligible to file an application for land seizure:

- 1.

1) Subjects of natural monopoly;

2) Organizations authorized in accordance with regulatory legal acts of the Russian Federation and agreements (made with authorities)/organizations permitted (licensed) to carry out activities that involve land seizure in accordance with Article 49 of the Land Code of the RF;

3) Subsoil users, with whom the integrated territorial development agreements have been signed (Federal Law of 25.10.2001, No. 136-FZ).

In our opinion, general damage (Dg) to land users resulted from business restrictions imposed on zones provided for by special land use provisions can be measured by the following formula:

Where:

DD – direct damage;

ID – indirect damage;

LEP – loss of expected profit;

Cencum – encumbrance costs.

Direct damage (DD) can be measured by methods of compensation for direct damage, based on the cost standards for developing new lands instead of the seized ones approved by the RF Government Decree No. 77 of 28.01.93 with subsequent amendments.

In our opinion, indirect damage (ID) can be measured by the formula:

Where:

Pbefore – agricultural production in quantitative terms before the restrictions were imposed;

P – agricultural production in quantitative terms after the restrictions were imposed;

Ct – total costs of agricultural output restoration.

We suggest that the loss of expected profit (LEP) can be measured by the formula:

Where:

Ialter. – income from alternative (most effective) land use

Iactual – income from actual land use;

Аp – decrease in the market value of a land parcel.

Encumbrance costs (Cencum) can be measured by the formula:

Where:

Ci-th encum – i-th encumbrance costs.

Thus, any restriction (encumbrance) reducing the value of real estate, imposed aside from the will of the right holder, is a restriction of property rights and should be reimbursed by:

-

- direct compensation according to the developed and approved methods;

- establishing the adjustment coefficient of land payments for land users using facilities located in the area of special land use regime;

- establishing the reduction factor to adjust land payments;

- setting fees for sanitary protection zones of industrial facilities;

- including certain environmental requirements into the land lease agreements regarding land parcels that are part of mining allotments, as well as sanctions for failure to comply with these requirements.

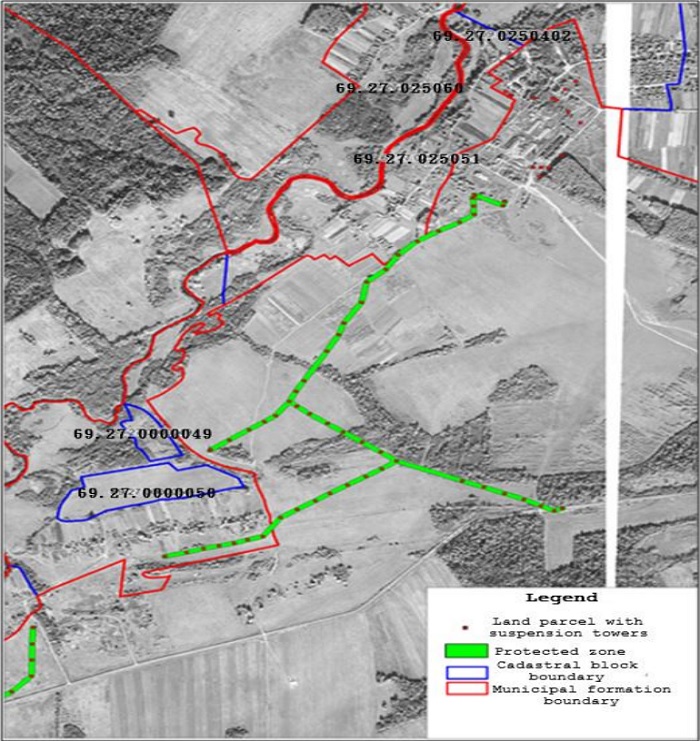

Consider the farmland located in the Zubtsovsky district of the Tver region, we have made calculations that can be made during the cadastral and monitoring works. The results have been analyzed and presented below. Figure 1 and Table 1 show the characteristics of land parcels and how they are related to the OHTL.

Figure 1

Protected zone and the farmland parcel with the suspension towers placed on it (Location Map Diagram)

| № | Area, m2 | Cadastral value, RUB | Length of the OHTLs, m | Protected zone area, m2 |

| 1 | 3 042 000 | 11 034 550.80 | 235 | 4700 |

| 2 | 478 000 | 1 668 315.60 | 440 | 8800 |

| 3 | 439 600 | 1 534 291.92 | 420 | 8400 |

| 4 | 160 000 | 558 432.00 | 170 | 3400 |

| 5 | 1 209 000 | 4 219 651.80 | 1240 | 24800 |

| 6 | 90 000 | 314 118.00 | 450 | 9000 |

| 7 | 71 000 | 247 804.20 | 185 | 3900 |

| 8 | 255 000 | 890 001.00 | 350 | 7000 |

| 9 | 314 000 | 1 095 922.80 | 475 | 9500 |

| 10 | 62 529 | 218 238.72 | 160 | 3200 |

| 11 | 83 511 | 291 470.09 | 300 | 6000 |

| 12 | 534 000 | 1 909 904.40 | 775 | 15500 |

| 13 | 209 000 | 747 509.40 | 145 | 2900 |

| 14 | 184 800 | 660 955.68 | 135 | 2700 |

| 15 | 190 000 | 679 554.00 | 310 | 6200 |

| 16 | 159 000 | 568 679.40 | 415 | 830 |

| 17 | 603 000 | 2 156 689.80 | 285 | 5700 |

| 18 | 446 209 | 1 796 705.16 | 775 | 15500 |

| 19 | 524 224 | 2 110 840.36 | 660 | 13200 |

| 20 | 71 250 | 286 895.25 | 330 | 6600 |

| 21 | 182 024 | 757 966.14 | 390 | 7800 |

| Total | 9308147.00 | 33748496.52 | 8645.00 | 165630.00 |

According to the Table 1, length of OHTL passing through the farmlands is 8645 m. The total area of protected zone is 165.630 m2.

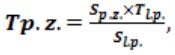

Table 2 shows that the total amount of tax imposed on the protected zones of land parcels, through which the OHTL pass, is RUB 1.817.52. This amount was calculated by multiplying two variables: protected zone area and the land tax rate. The tax rate was adopted in accordance with the Tax Code of the Russian Federation, Part 2, Section X, Chapter 31 and the Decision of the Municipal Council of Deputies No. 121 of November 27, 2015 ("Urban Settlement – Zubtsov town", Tver Region). One, who calculated this tax, can conclude that the owner of a land parcel suffers losses, since this amount is not compensated and his is paying not less then before.

We have used the following formula to calculate the tax imposed on the protected zone:

Where: Tp.z. – tax imposed on the protected zone;

Sp.z.– Protected zone area;

Tl.p.– tax imposed on the land parcel; Sl.p.– land parcel area.

Tax calculations are presented in Table 2.

| № | Land tax, RUB | Protected zone area, m2 | Land parcel area, m2 | Tax imposed on the protected zone, RUB |

| 1 | 33103.65 | 4700 | 3042000 | 51.15 |

| 2 | 5004.947 | 8800 | 478 000 | 92.14 |

| 3 | 4602.876 | 8400 | 439 600 | 87.95 |

| 4 | 1675.296 | 3400 | 160 000 | 35.60 |

| 5 | 12658.96 | 24800 | 1209000 | 259.67 |

| 6 | 942.354 | 9000 | 90 000 | 94.24 |

| 7 | 743.4126 | 3900 | 71 000 | 40.84 |

| 8 | 2670.003 | 7000 | 255 000 | 73.29 |

| 9 | 3287.768 | 9500 | 314 000 | 99.47 |

| 10 | 654.7162 | 3200 | 62 529 | 33.51 |

| 11 | 874.4103 | 6000 | 83 511 | 62.82 |

| 12 | 5729.713 | 15500 | 534 000 | 166.31 |

| 13 | 2242.528 | 2900 | 209 000 | 31.12 |

| 14 | 1982.867 | 2700 | 184 800 | 28.97 |

| 15 | 2038.662 | 6200 | 190 000 | 66.52 |

| 16 | 1706.038 | 830 | 159 000 | 8.91 |

| 17 | 6470.069 | 5700 | 603 000 | 61.16 |

| 18 | 5390.115 | 15500 | 446 209 | 187.24 |

| 19 | 6332.521 | 13200 | 524 224 | 159.45 |

| 20 | 860.6858 | 6600 | 71 250 | 79.73 |

| 21 | 2273.898 | 7800 | 182 024 | 97.44 |

| Total | 101245.49 | 165630.00 | 9308147.00 | 1817.52 |

Let us measure the share of protected zone of the total land area.

Its arithmetic mean value is:

М = 71.62/21 = 3.4

We have calculated the arithmetic mean, which reflects the average share of the protected zone as part of the farmland. Let us accept that statistical universe is homogeneous and this value corresponds to the entire studied area.

We propose to apply this value as a reduction factor when calculating the compulsory land tax imposed on individuals owning land parcels.

Since the average share of protected zone with electric grid facilities is 0.034, we propose to calculate the land tax considering a decrease in the total payment amount by 3.4%.

We have calculated the amount of imposed land tax in the case of 21 land owners and found put that the municipal budget receives RUB 101.245.5 annually. However, land use data are limited by the protection zones around the electric grid facilities. Thus, we assume it is fair to introduce a reduction factor for land users.

Since the share of protected zones with electric grid facilities placed in them is 0.034 on average of the total land area, we assume it is fair to calculate this coefficient in order to lower the tax rate (Table 3).

In calculating the values of a reduction factor, we have got a value that amounted to approximately RUB 3.442.3. Land tax is a constant value and is included in the constant business costs. In other words, it does not depend on the output volume. Hence, constant costs of land users are reduced.

| № | Land parcel area, m2 | Cadastral value of land parcel, RUB | Tax, RUB | Reduction factor | Reduction factor value, RUB |

| 1 | 3 042 000 | 11 034 550.80 | 33103.65 | 0.034 | 1125.5 |

| 2 | 478 000 | 1 668 315.60 | 5004.95 | 0.034 | 170.2 |

| 3 | 439 600 | 1 534 291.92 | 4602.8 | 0.034 | 156.5 |

| 4 | 160 000 | 558 432.00 | 1675.30 | 0.034 | 57.0 |

| 5 | 1 209 000 | 4 219 651.80 | 12658.96 | 0.034 | 430.4 |

| 6 | 90 000 | 314 118.00 | 942.35 | 0.034 | 32.0 |

| 7 | 71 000 | 247 804.20 | 743.4 | 0.034 | 25.3 |

| 8 | 255 000 | 890 001.00 | 2670.00 | 0.034 | 90.8 |

| 9 | 314 000 | 1 095 922.80 | 3287.7 | 0.034 | 111.8 |

| 10 | 62 529 | 218 238.72 | 654.72 | 0.034 | 22.3 |

| 11 | 83 511 | 291 470.09 | 874.41 | 0.034 | 29.7 |

| 12 | 534 000 | 1 909 904.40 | 5729.71 | 0.034 | 194.8 |

| 13 | 209 000 | 747 509.40 | 2242.53 | 0.034 | 76.2 |

| 14 | 184 800 | 660 955.68 | 1982.867 | 0.034 | 67.4 |

| 15 | 190 000 | 679 554.00 | 2038.66 | 0.034 | 69.3 |

| 16 | 159 000 | 568 679.40 | 1706.04 | 0.034 | 58.0 |

| 17 | 603 000 | 2 156 689.80 | 6470.07 | 0.034 | 220.0 |

| 18 | 446 209 | 1 796 705.16 | 5390.115 | 0.034 | 183.3 |

| 19 | 524 224 | 2 110 840.36 | 6332.52 | 0.034 | 215.3 |

| 20 | 71 250 | 286 895.25 | 860.68 | 0.034 | 29.3 |

| 21 | 182 024 | 757 966.14 | 2273.90 | 0.034 | 77.3 |

| Total | 4986147 | - | 101245.5 | - | 3442.4 |

There is also a second positive aspect of applying this coefficient – it will be positive for land users, as it will partly cover the expected profit lost due to the restrictions imposed on the farmland use.

It is advisable to determine the amount of expected profits lost as the farmland was encumbered with protection zones around the electric grid facilities.

We have determined that the lost profit of land owners growing potatoes with an average yield of 17 tons per hectare on the territory encumbered with protected zone will be RUB 2.435.477.

3. DISCUSSION

Let us calculate the lost profit on the territory encumbered with a protection zone around the electric grid facilities. The decrease in the amount of land taxes paid can be called insignificant – about RUB 3.442.34 (21 parcels). At the same time, it is required to determine how the farm/production profitability has changed after the tax liability had decreased (Table 4).

Thus, we have determined that the process of introducing a reduction factor of land tax will have a positive effect on farmers on whose land the electric grid facilities are placed. Despite a slight decrease in tax liability, the average farm/production profitability can grow from 7.5% to 11.3%, namely – almost by half. This statement is based on the fact that the share of protected zones may be different and depends on the farmer’s land parcel area (legal advice service "Народный СоветникЪ" – ER).

| № | Land parcel area without the protected zone, ha | Yield capacity, tons per ha | Gross output, tons | Potential gross income, RUB | Gross cost, RUB | Profitability | Profitability with a reduction factor | Dynamics |

| 1 | 303.7 | 17 | 5163.41 | 42185060 | 39241916 | 1.075 | 1.113 | 1.035 |

| 2 | 46.9 | 17 | 797.64 | 6516719 | 6062064 | 1.075 | 1.113 | 1.035 |

| 3 | 43.1 | 17 | 733.04 | 5988937 | 5571104 | 1.075 | 1.113 | 1.035 |

| 4 | 15.7 | 17 | 266.22 | 2175017 | 2023272 | 1.075 | 1.113 | 1.035 |

| 5 | 118.4 | 17 | 2013.14 | 16447354 | 15299864 | 1.075 | 1.113 | 1.035 |

| 6 | 8.1 | 17 | 137.70 | 1125009 | 1046520 | 1.075 | 1.113 | 1.035 |

| 7 | 6.7 | 17 | 114.07 | 931951,9 | 866932 | 1.075 | 1.113 | 1.035 |

| 8 | 24.8 | 17 | 421.60 | 3444472 | 3204160 | 1.075 | 1.113 | 1.035 |

| 9 | 30.5 | 17 | 517.65 | 4229201 | 3934140 | 1.075 | 1.113 | 1.035 |

| 10 | 5.9 | 17 | 100.86 | 824026,2 | 766536 | 1.075 | 1.113 | 1.035 |

| 11 | 7.8 | 17 | 131.77 | 1076561 | 1001452 | 1.075 | 1.113 | 1.035 |

| 12 | 51.9 | 17 | 881.45 | 7201447 | 6699020 | 1.075 | 1.113 | 1.035 |

| 13 | 20.6 | 17 | 350.37 | 2862523 | 2662812 | 1.075 | 1.113 | 1.035 |

| 14 | 18.2 | 17 | 309.57 | 2529187 | 2352732 | 1.075 | 1.113 | 1.035 |

| 15 | 18.4 | 17 | 312.46 | 2552798 | 2374696 | 1.075 | 1.113 | 1.035 |

| 16 | 15.8 | 17 | 268.89 | 2196831 | 2043564 | 1.075 | 1.113 | 1.035 |

| 17 | 59.7 | 17 | 1015.41 | 8295900 | 7717116 | 1.075 | 1.113 | 1.035 |

| 18 | 43.1 | 17 | 732.20 | 5982074 | 5564720 | 1.075 | 1.113 | 1.035 |

| 19 | 51.1 | 17 | 868.74 | 7097606 | 6602424 | 1.075 | 1.113 | 1.035 |

| 20 | 6.5 | 17 | 109.90 | 897883 | 835240 | 1.075 | 1.113 | 1.035 |

| 21 | 17.4 | 17 | 296.18 | 2419791 | 2250968 | 1.075 | 1.113 | 1.035 |

| Total | 914.3 | - | 15542.28 | 126980346 | 118121252 | - | - | - |

The farmer will be able to increase own average profit while reducing the tax burden and maintaining the same sale cost. As a result, income tax payments to the regional and federal budgets will increase, value-added tax payments will also increase (in the case of general taxation regime), as well as other types of payments (in the case of a simplified tax system).

4. CONCLUSIONS

According to established rules, protected zones are prohibited for building and re-building installations, for loading and unloading operations, planting and cutting trees and bushes, arranging passages for vehicles and mechanisms that are over 4 meters above the road surface. In addition, protected zones of power transmission lines are prohibited for keeping petroleum, oil and lubricants, arranging landfills, building fire and carrying out other actions that can disrupt and damage the electrical networks.

Protected zones of power transmission lines are prohibited for placing cargo, pouring acid, alkaline and salt solutions, excavating at a depth of more than 0.3 m and ground shaping with bulldozers, excavators and other digging machines.

The right of the owner of the electric grid facility to unimpeded access to his/her facility should be secured.

In the course of the research, we have studied a significant number of agricultural enterprises and measured the arithmetic mean reflecting the average share of protected zone of the farmland (within one district).

As a result, we suggest using values reflecting the shares of land with power transmission lines passing through it as a reduction factor when calculating the compulsory land tax. For example, since the average share of protected zones with electric grid facilities placed in them is 0.034, we propose to calculate the land tax considering a decrease in the total payment amount by 3.4% (data is correct for the Zubtsovsky District of the Tver Region).

Land tax is a constant value and is included in the constant business costs. In other words, it does not depend on the output volume.

There is also a second positive aspect of applying this coefficient – it will be positive for land users, as it will partly cover the expected profit lost due to the restrictions imposed on the farmland use.

Thirdly, we should note the potential possibility of changing farm/production profitability after applying a reduction factor of the land tax payment (constant costs). It is expected that an increase in farm/production profitability will entail the possibility of reinvesting profits back into the business, upgrading plants, creating additional jobs, and fulfilling economic and social obligations in the region.

Our proposition to use a reduction factor actually stands for introducing a concept of "dynamic" taxation, which is new and allows building a flexible system of compulsory payments based on the payer’s solvency, his/her actual tax base and the balance of private and public interests.

Reduction factor can be applied not only to the land tax, although it is the simplest one to apply. It can regulate the profit tax, unified agricultural tax, tax paid under the simplified tax system. Multiplying factor can be used while calculating the depreciation amount for movable and immovable property. Dynamic taxation can become an encouragement tool for farmers, owners of electric grid facilities and product users.

REFERENCES

BOSTEDT, G., WIDMARK, C., ANDERSSON, M., & SANDSTORM, C. 2015. Measuring transaction costs for pastoralists in multiple land use situations: reindeer husbandry in Northern Sweden. University of Wisconsin Press. Vol. 91 No 4: 704-722. United States.

COOK, L. 2013. Post-communist welfare states: Reform politics in Russia and Eastern Europe. New York: Cornell University Press. United States.

DINERSHTEIN, P., ALEEVA, E. 2017. Myself when young or growing pains by Daphne du Maurier. Astra Salvensis, Review of history and culture, No10, p. 103-108. Romania.

Federal Law of 25.10.2001, No. 136-FZ. 2015. The Land Code of the Russian Federation. The Russian Federation Laws. Moscow: Eksmo Publishing House. Russia.

GANS-MORSE, J. 2017. Demand for Law and the Security of Property Rights: The Case of Post-Soviet Russia. American Political Science Review. Vol. 111 No 2: 338-359. United States.

GILBERT, J. 2016. Indigenous Peoples' Land Rights under International Law. https://brill.com/view/title/13810. Date of consultation: 01/30/2018. Netherlands.

HANSTAD, T. 2016. Land rights: Intangible assets bring tangible benefits. Appropriate Technology. Vol. 43 No2: 42. In http://skoll.org/2016/03/17/land-rights-intangible-assets-bringtangible-benefits/. United States.

JEPSEN, M., KUEMMERLE, T., MÜLLER, D., ERB, K., VERBURG, P., HABERL, H., & BJÖRN, I. 2015. Transitions in European land-management regimes between 1800 and 2010. Land Use Policy. Vol. 49: 53-64. Netherlands.

KAAS, L., PINTUS, P., & RAY, S. 2016. Land collateral and labor market dynamics in France. European Economic Review. Vol. 84: 202-218.Netherlands.

Legal advice service "НародныйСоветникЪ". 2017. Establishing protection zone boundaries around the power transmission lines. http://sovetnik.consultant.ru/. Russia.

LEPEKHIN, P., and LEPEKHIN, P. 2015. Features of the legal regulation of linear electric grid facilities. Tula: Tula State University. pp: 3-9. Http: //www/elibrary.ru/. Russia.

MAKSIMOVA, T., BONDARENKO, N., & ZHDANOVA, O. 2017. Transformation of farms in the agrarian economy of the Russian federation in the modern conditions. Academy of Strategic Management Journal. p: 16. UK.

MARKUS, S. 2015. Property, Predation, and Protection: Piranha Capitalism in Russia and Ukraine. Cambridge, Cambridge University Press.UK.

MENON, N., RODGERS, Y., & KENNEDY, A. 2017. Land Reform and Welfare in Vietnam: Why Gender of the LandRights Holder Matters. Journal of International Development. Vol. 229 No 4: 454-472. United States.

MURASHEVA, A. and LEPEKHIN, P. 2014. Optimizing the use of agricultural land. Modern Scientific Bulletin [Sovremenny ynauchnyy vestnik]. Scientific and Practical Journal, Series: Ecology, Geography and Geology, Agriculture. Vol. 32 No 228: 11-17.Republic of Belarus.

NEWELL, J. & HENRY, L. 2016. The state of environmental protection in the Russian Federation: a review of the postSoviet era. Eurasian Geography and Economics. Vol. 57 No 6: 779-801.Russia.

PRISHCHEPOV, A., MULLER, D., DUBININ, M., BAUMANN, M., and RADELOFF, V. 2013. Determinants of agricultural land abandonment in post-Soviet European Russia. Land use policy. Vol. 30 No 1: 873-884. Netherlands.

RF Government Resolution of 24.02.2009 No. 160. 2013. On the Procedure for Establishing and Using Protection Zones around Electric Grid Facilities and the Special Conditions for Using Land Plots Located within such Zones (Amended on 26.08.2013).

SHURYGIN, V., KRASNOVA, L. 2017. The peculiarities of pedagogical projects implementation for identification and development of giftedness in children. Astra Salvensis - review of history and culture, No 10: 47-54. Romania.

The Federal Law of 13.07.2015, No. 218.2015. On State Registration of Real Estate. Garant–legal information data base. The Russian Federation Laws. Moscow: Eksmo Publishing House. Russia.

UZUN, V., and SHAGAIDA, N. 2015. The Mechanisms and the Results of the Agrarian Reform in Post-Soviet Russia. In https://ideas.repec.org/p/rnp/wpaper/mak15n6.html. Data consultation: 10/12/2017.

VERSHININ, V., MURASHEVA, A., SHIROKOVA, V., KHUTOROVA, A., SHAPOVALOVA, D., and TARBAEV, V. 2016. The Solutions of the Agricultural Land Use Monitoring Problems. International journal of environmental & Science education. Vol. 11 No 12: 5058-5069.Russia

WERGREN, S. 2014. Land reform in Russia: Institutional design and behavioral responses.https://yalebooks.yale.edu/book/9780300150971/land -reform-russia. Data Consultation: 09/15/2017. Russia.

ZOLOTOVA, O. 2016. Legal regulation of land protection zones: basic issues of judicial practice. Branches of Law. Analytical Portal: http: //xn----7sbbaj7auwnffhk.xn--p1ai/article / 18748. Data Consultation: 02/20/2018. Russia.