Articles

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-CompartirIgual 4.0 Internacional.

Recepción: 18 Enero 2018

Aprobación: 22 Noviembre 2018

DOI: https://doi.org/10.5585/ijsm.v18i1.2616

Resumo:

Objetivo (obrigatório): O presente estudo tem por objetivo caracterizar os modelos de negócios sob a lógica das estruturas de governança discutidas na Economia dos Custos de Transação (ECT).

Método (obrigatório): A partir da revisão na literatura, foram identificados os principais elementos que compõem um modelo de negócios, que foram então combinados em um modelo gráfico com as principais características da Economia dos Custos de Transação (ECT) adotadas.

Originalidade/Relevância (obrigatório): Com base na fundamentação teórica sobre o assunto, foi identificada a forma com que os elementos de um modelo de negócios interagem entre si, sob a lógica da ECT.

Resultados (obrigatório): Os resultados apresentam as relações entre os componentes de um modelo de negócio e as principais características conceituais da ECT. Um modelo de negócio é suportado por elementos como as especificidades dos ativos, frequências e incertezas, estratégias de diferenciação, entre outros, definidos a partir da segmentação de clientes.

Contribuições teóricas/metodológicas (obrigatório): As principais contribuições estão relacionadas à complementaridade da literatura sobre modelos e negócios, em seus diferentes elementos, à luz da ECT de modo a caracterizar a competitividade de diferentes organizações, a partir de diferentes estratégias adotadas.

Contribuições sociais / para a gestão (opcional): Diferentes organizações, que já se pautam na redução dos custos transacionais, podem se utilizar dos elementos que caracterizam um modelo de negócio para se tornarem mais competitivas.

Palavras-chave: Competitividade Organizacional, Estratégia, Estrutura de Governança.

Abstract:

Objective of the study: The main objective of this study is to characterize business models under the logic of governance structures discussed as viewed in Transaction Cost Economics (TCE).

Method: We identified the main elements that make up a business model on the literature. The models were combined in a graphic model with the main characteristics of the Transaction Cost Economics (TCE).

Originality / Relevance: We have identified how the elements of a business model interact with each other from the perspective of TCE.

Main results: The results present the relationships among the components of a business model and the main conceptual characteristics of TCE. A business model is supported by elements such as asset specificities, frequencies and uncertainties, differentiation strategies, and others, all defined from customer segmentation.

Theoretical / methodological contributions: The main contributions are related to the advancement of literature on models and business, regarding its different elements, in the light of TCE. Thus, we hope to contribute with the characterization of competitiveness in different organizations which use different strategies.

Social / management contributions: Different kinds of organizations that already focus on the reduction of transactional costs can use the elements that characterize a business model in order to become more competitive.

Keywords: Organizational Competitiveness, Strategy, Governance Structure.

Resumen:

Objetivo: El presente estudio tiene como objetivo caracterizar los modelos de negocios bajo la lógica de las estructuras de gobernanza discutidas por la Economía de los Costos de Transacción (ECT).

Método: A partir de la revisión en la literatura, se identificaron los principales elementos que componen un modelo de negocio, que luego se combinaron con un modelo gráfico a las principales características de la Economía de los Costos de Transacción (ECT) adoptadas.

Originalidad / Relevancia: Con base en la fundamentación teórica sobre el asunto, se identificó la forma en que los elementos de un modelo de negocio se interrelacionan entre sí bajo la lógica de la ECT.

Resultados: Los resultados presentan las relaciones entre los componentes de un modelo de negocio y las principales características conceptuales de la ECT. Un modelo de negocio es soportado por elementos como las especificidades de los activos, frecuencias e incertidumbres, estrategias de diferenciación, entre otros definidos a partir de la segmentación de clientes.

Contribuciones teóricas / metodológicas: Las principales contribuciones están relacionadas con la complementariedad de la literatura sobre modelos y negocios, en sus diferentes elementos, a la luz de la ECT para caracterizar la competitividad de diferentes organizaciones a partir de diferentes estrategias adoptadas.

Contribuciones sociales / para la gestión: Diferentes organizaciones que ya se basan en la reducción de los costos transaccionales, pueden utilizarse en los elementos que caracterizan un modelo de negocio para llegar a ser más competitivos.

Palabras clave: Competitividad Organizacional, Estrategia Estructura de Gobernanza, Estrategia, Estrategia, Estructura de Gobernanza.

INTRODUCTION

Considering the need of companies to differentiate themselves from their competitors (Porter, 1996), business models become decisive elements in business strategies, seeing that they characterize all aspects of business in a holistic way and visualize all concepts of a management plan in a representation, as in the case of the Business Model Canvas (Osterwalder & Pigneur, 2010). As a result, business models enable us to mitigate weaknesses and to highlight the strengths that create value for an organization.

These values are obtained from the interaction between all elements involved in the business, such as suppliers, customers and distribution channels (GASSMANN et al., 2014; TEECE, 2010).

However, although the approach to business models is increasingly discussed in the literature, some gaps on the subject have yet to be fulfilled. Wirtz et al. (2016) point out, among the main gaps in the area, a better understanding of the interaction of the elements that make up a business model and the way in which these elements are represented.

Given the potential of business models, there is also a need to improve and exploit their possibilities (Maglio & Spohrer, 2013). In this regard, the Transaction Cost Economics (TCE) can be interpreted as a theoretical perspective capable of contributing to this improvement, since it presents the concept of governance structure and institutional core that defines the ways in which the transactions of the organizations are carried out, that are market, hierarchy or hybrid form. Either the market, the hybrid, or the hierarchical forms have advantages and disadvantages, and it is necessary to measure whether the benefits of a choice will outweigh the losses (Williamson, 2010).

The relevance of TCE within strategic management has been identified by Kenworthy and Verbeke (2015), that put TCE as the second most recurrent theory in the study of strategic management. The authors understand that this theory, initially applied in the economic sciences, has contributed in the field of strategic administration by incorporating perspectives previously absent, by incorporating previously non-existent perspectives, to deal with transaction costs. An example of this is the adoption of collaborative strategies, or strategic alliances.

According Wirtz et al. (2016), future research on the subject must correlate the interfaces of business models with concepts from other areas. Kenworthy and Verbeke (2015) corroborate this suggestion and argue that theories borrowed from other areas can be of great value for the development of fields that seek greater legitimacy, as is the case with the business model.

As noted by DaSilva and Trkman (2014), strategists need to choose not only the right combination of resources (according to the Resource-Based View), but also the most efficient transactions (according to TCE) at a certain moment, in order to overcome long-term competitors. The insertion of TCE would help explain the interactions between the elements that make up a business model.

Arend (2013) criticize the practical approaches that authors have given in analyzing the business model and its concepts, and ask for a change of perspective for a theoretical approach. For the authors, this transition will allow a more abstract analysis of the theme, and the genesis of new insights and questions.

In this sense, the present study is characterized as a theoretical essay that seeks to answer the following research question: how does the interaction and representation of the elements present in a business model occur from the TCE perspective? Thus, this research, when applied to strategic management, aims to insert governance decisions in business models, identifying the interaction and representation of the set of elements that constitute business models, from the perspective of TCE.

In this way, it is intended to contribute to the development of the business model literature by responding to the theoretical gap on the interaction and representation of the elements that make up a business model (WIRTZ et al., 2016), to explore new possibilities for this tool by highlighting TCE perspectives from the governance framework and providing a more streamlined understanding of the business model for organizations, as highlighted by Arend (2013).

BUSINESS MODELS

The literature attempts to explain the differences of business performance between organizations in different ways, either by analysing the company's internal politics, the peculiarity of activities and processes, or through alliances and external agreements, among others. However, there is a concept that also includes aspects such as strategy, innovation and a holistic view of the environment in which the organization is inserted.

These are the business models (Chesbrough, 2010; Casadesus-Masanell & Ricart, 2010).

Business models present a wide view of the organization, as they encompass all aspects that are responsible for generating value and creating competitive advantage, such as the threat of new entrants and opportunities for performance enhancement (Amit & Zott, 2008; Chesbrough, 2010).

However, the concept of business models still presents divergences among authors. For Shafer et al. (2005), business model is the representation of the main strategic choices that are applied to generate value for the organization. In contrast, Osterwalter et al. (2005) understand the business model as the structure that rules the transactions between the organization and its exchange partners. According to Brettel et al. (2012), these different definitions related to the business model are seen as an obstacle to the progress of the area.

According Casadesus-Masanell and Ricart (2010), business models aims to represent an organization's way of acting and how it creates value for its stakeholders. On the other hand, Teece (2010) says that the goal of a business model is to provide a structure that connects an organization's activities to market demands, relationship channels and value creation.

Trimi and Berbegal-Mirabent (2012) relate business model to what must be done in order to deliver value to the customer and to receive the feedback that will sustain the development of an organization. Amit and Zott (2001) describe it as the business model that establishes the structuring of every operationalization within an organization and thus generates value through the exploration of opportunities. According to Tikkanen et al. (2005), business model can be defined as a set of several components that, when related, create value for organization.

Although there is no unanimity about the concept that defines business models in the literature, the definitions of these authors converge in the sense of strategic coordination of the several elements that set the business of a company, in order to generate value and provide competitive advantages for the same. The present study adopts this perception to reach the definition of business models.

In order to facilitate the understanding on the subject, Casadesus-Masanell and Ricart (2010) compare a business model to a car, which is composed of several components. The authors defend the idea that each component individually can not make the vehicle run, being the interaction between the components that achieves the driver's primary goal, since it is from these interactions that the car works and thus creates value for its owner. In the same way, the components of a business model, when related, generate value for the organization, which in this example is analogous to the driver of the car.

Berends et al. (2016) understand that the business model works from the strategic interactions of its components. Thus, the failure of a business model can occur when one component adversely or conflictingly involves another component. For the authors, interactions among the components may be difficult to predict.

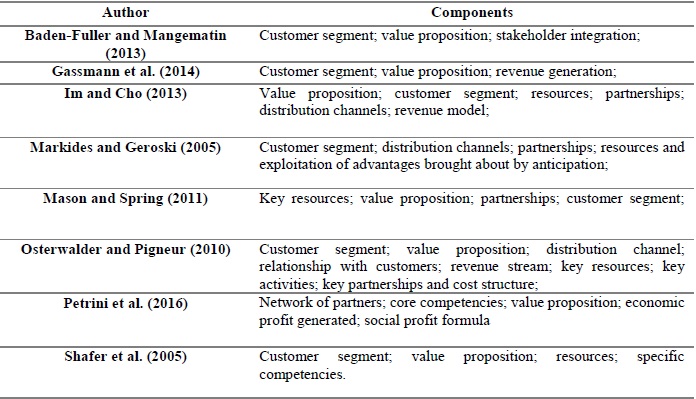

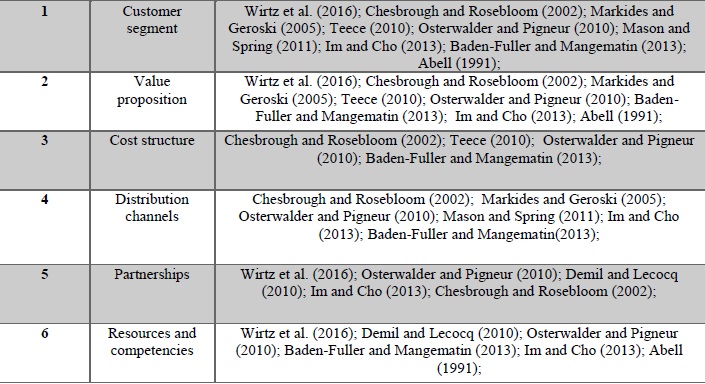

Like its concept, the components and form of graphical representation of the business models also vary among authors. Pereira and Caetano (2015), in order to propose a conceptual business model for airlines, identified 38 different components from four strategic chains cited in the literature from years 2005 to 2014. Table 1 below highlights the main elements identified by the authors to compose a business model using different studies.

The dynamism of the business environment generates a demand for tools that allow simplifying the relationship between the organization and its diverse stakeholders. A good business model should systematize different concepts and be clear about what is being addressed, so that the several elements present could communicate in a single language and with a common goal.

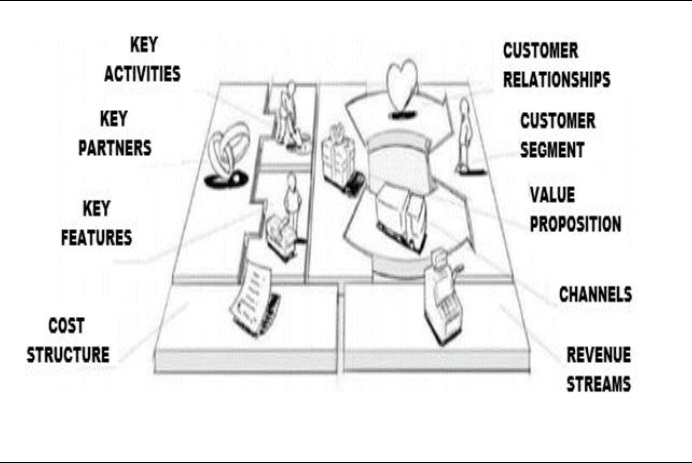

The Business Model Canvas, conceived by Osterwalder and Pigneur (2010), allows the company to identify failures and threats in its components through a self-reflection exercise, by establishing a relationship among nine components, which refer to four fields: product, customer, infrastructure and finance. In this model, all quadrants must be questioned and reviewed, and questions such as "How do I make a profit?", "Who is my client?", "What is value to my client?" and "How much does it cost to satisfy my client?" must be done constantly, in order to achieve the best possible performance using their answers.

The Business Model Canvas is composed of nine elements. The Customer Segment defines the niche of customers, whether individuals or companies, that the organization aims to serve. Value Proposition refers to the differential that justifies why consumers choose a company over its competitors. The Channels relate to how the organization will deliver value to its customer.

Customer Relationships describe the type of relationship that an organization seeks to establish with its customer segment. The Revenue Streams represent the financial gains obtained by the company from its segment of clients.

Key Features comprise the most important assets necessary to run a business model. The Key Activities consist of the most important actions that the company must undertake to create value for its customer. Key Partners are the network of suppliers and potential partners that will provide the organization's business model. The Cost Structure describes all the costs involved in the operation of a business model, whether fixed or variable. Figure 1 represents the nine elements that make up the Canvas model.

Figure 1

Business model Canvas

Bonazzi and Zilber (2014), adapted from Osterwalder and Pigneur (2010).

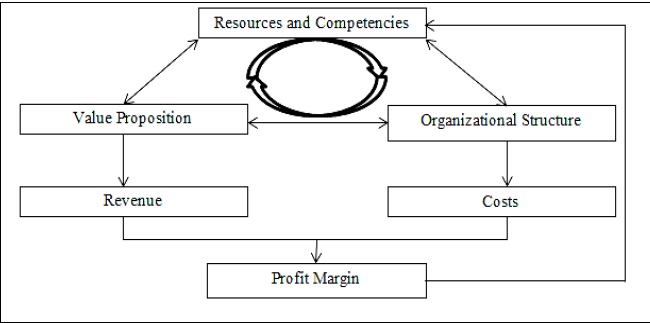

In the study proposed by Demil and Lecocq (2010), in order to explore the interaction between the components of the business model adopted by English professional football club Arsenal, the authors use the RCOV model, which is composed of three main components: resources and competencies, organizational structure and value proposition.

According to Figure 2, the "resources and competencies" component consists of the revenue sources, produced internally or acquired from the market, and the knowledge, skills and attitudes that accompany the individuals responsible for managing the resources of the organization. The skills of several individuals, combined, are capable of generating new products.

The element "organizational structure" comprises the relationships that the organization establishes with other players in order to guarantee the operation of its business. There are other elements inserted as well, such as the value chain, the processes involved in the activities and the company's relationship with its stakeholders.

The "value proposition" is an element that refers to the value offered by the organization by means of products and services, that is, the way in which it proposes to serve its stakeholders.

The value of this proposal covers the relationship between the organization and its stakeholders, and the resources used to support that relationship. It is important to note that, although portrayed in a completely different way from Business Model Canvas, the structure and purpose of the two models are the same: to generate value for their client. Figure 2 below highlights the components of the RCOV business model.

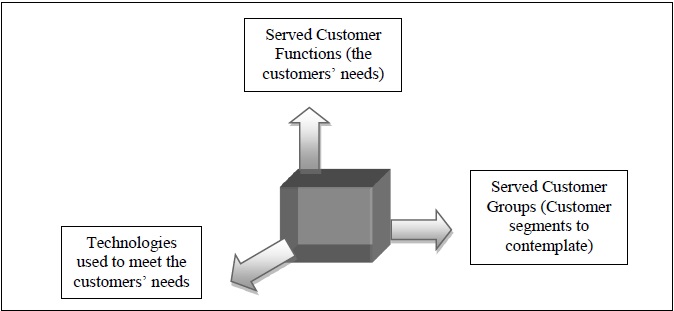

Abell's business model (1991), represented in Figure 3, also proposes a structured model in three dimensions, containing: served customer groups; served customer functions, and technologies used to meet those needs. This model emphasizes the customer over the organization itself, and explores what lies behind the final product, that is, the application of the resources needed to meet the demands of a particular segment of customers.

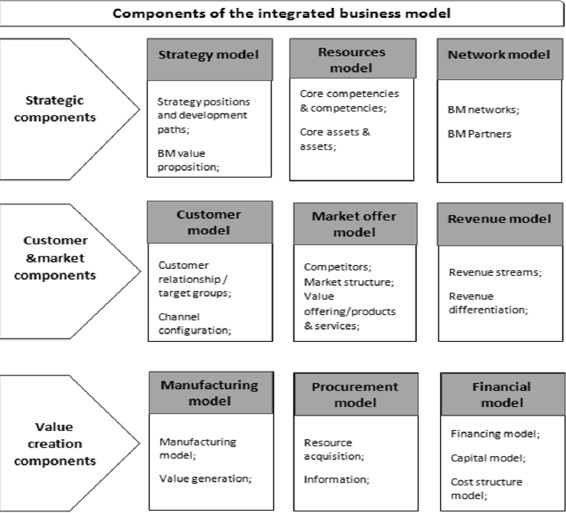

Wirtz et al. (2016) establish a business model composed of nine elements, as well as the Canvas model, divided into three groups: strategic components; market components and customers; and value creation components. The components that are part of the first group are: strategy, resources and competencies, and partnerships. The second group includes customers, market supply and revenue streams. The third group consists of value proposition, acquisition method and financing structure. The authors emphasize that, although the components are divided into groups, these components are related to each other. Figure 4 shows the model representation of Wirtz et al. (2016).

Wirtz et al. (2016) conducted a literature review and elected the nine elements of Figure 4 as those that they consider to be the essential elements in the composition of a business model. The authors treat the "strategy" component as central, a kind of guide that determines the organization's mission, vision and values. The component "acquisitions method" refers to the management of acquisitions in the production cycles and the relation of the producer to the buyer market. The "market supply" component, in its turn, takes into account the competitors and the market structure, for which the value proposition will be offered. The other components are treated by the authors in the same way as the others mentioned above.

However, the present study assumes that some of these elements are considered to be derived from others, such as the "strategy" component. The present study considers that the strategy does compose the business model, but implicitly. Wirtz et al. (2016) emphasize that, although they have chosen these nine elements for their business model, the heterogeneity of interpretations among authors is abundant in the literature. The authors contend that while there is a great deal of agreement with the "resources" element, the contradiction is great in relation to the elements "strategy", "recipes" and "purchases".

According to what has been presented above, it is noted that, in the view of the present study the literature registers different components of business models, according to the definitions of several authors on the subject. However, it may be noted that some components appear more frequently in this diversity of models, even though one or another author sometimes describes them differently. Table 2 below shows the six minimum components present in a business model, in the view of the present study, and the authors who cited them.

Components that characterize a business model

Survey data (2017)

The six components presented in Table 2 can be identified as Customer Segment, Value Proposition, Cost Structure, Distribution Channels, Partnerships, and Resources and Competencies. Although the literature cites other elements, this study understands that the six elements that are part of this categorization contain, in some way, those that are part of the categorization presented by the authors.

If on the one hand the business model is composed of different elements, on the other hand it is the way these elements interact that generates value for organization. This interaction can take place in different ways, such as hierarchical concentration, strong market presence or hybrid form. That said, TCE appears as a theoretical perspective capable of supporting this issue, and its fundamentals will be dealt within the next section.

TRANSACTION COST ECONOMICS

The characteristic of each component of a business model reflects a strategic choice made by the organization and that generates different consequences, as proposed by Casadesus-Masanell and Ricart (2010). According to the authors, the degree of integration between the components of the business model is a choice that the organization has to make, choosing, for example, whether to own a truck train or rent it.

Organizations are developed within an institutional environment that affects their activities through a series of regulations, either political, social, cultural or economic. Williamson (1985) analyses the relationship between organizations and TCE, evidencing how forms of governance structure vary according to the institutional environment in which they are embedded.

According the author, the governance structure is the institutional core in which the transactions are carried out and that influences the generation of value inside the organization.

The first author to discuss this subject was Coase (1937), who questioned the reason for the existence of firms. In his study, the author criticizes the classic economic system, which considers that relations are controlled automatically by the market and the factors of production are controlled by price mechanisms. The author argues that this point of view cannot be generalized, while he points out that firms establish themselves not only with the ideal of production, but also to reduce market costs, called transaction costs.

Subsequently, Williamson (1985) continued the Coase theory, defining transaction costs as those costs related to contracting. In addition, three different forms of governance structure adopted by the organizations were established: market, hybrid or hierarchy. Organizations, through the form of governance structure adopted, manage to control transaction costs, interfering with their increase or reduction.

The market is determined by prices, to which the involved parts have no dependency relationship and transactions occur separately, without the need for a new exchange. The hierarchical form is represented by the vertical relations, with incorporation of the transactions by the same organization, and presents a strong managerial control and a weak external incentive. The hybrid form, in its turn, is characterized by absence of activities incorporation and presence of an additional control that does not exist in market relations, and the relations are governed by contracts (Williamson, 1985; North, 1990).

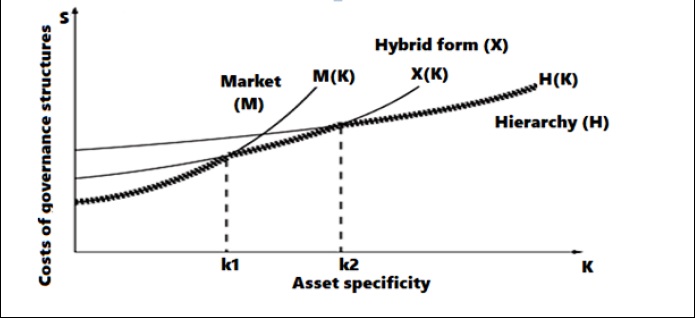

TCE explains the magnitude of transaction costs through three factors: frequency, uncertainty, and asset specificity. Frequency is related to the regularity with which the transactions occur, so that, in a high frequency scenario, the incorporation of these activities by the organization is more advantageous, because it allows the reduction of interaction costs. The uncertainty refers to the damages caused by possible changes in a relationship between customer and supplier, so that the greater the uncertainty, the greater the transaction cost. Asset specificity, in its turn, is considered the main characteristic of TCE and it approaches the autonomy that the company has over an asset, independently of its relationship with customers and suppliers (Williamson, 1985). This relationship can be seen in Figure 5 below.

Figure 5

Cost of governance structure as a function of asset specificity

Cabral (2004)

In his review of theory of the firm, analysing the contractual complexity, Williamson (1985) concludes that if the assets that are part of the relationship between company and outsourced parties are generic, the market can meet that demand. However, the greater the specificity of the asset, the greater will be the dependence of third parties, that is, the greater the risk that the market would be unable to meet its needs.

Investments supported by specific assets pose a great risk, because their replacement would probably bring about variations in results. As an example, one can cite the dependence that an organization has developed by an individual, a human asset, who through his knowledge and experience has become a fundamental part of an organization. Therefore, if there were no specificity in assets, there would be no reason to choose the hierarchy, since another individual, with the same adjectives, would be easily found in the market.

In addition to the three factors mentioned above (frequency, uncertainty and asset specificity), the organization has to deal with problems related to bounded rationality and opportunism in exchange relations. "Opportunism" addresses the fact that economic agents pursue their own interests. This assumption resembles what is addressed in the Agency Theory, where some agents have more information than others and thus seek to take advantage of that situation (KATO; MARGARIDO, 2000).

Bounded rationality, however, is a presupposition that contributes to TCE, and seeks to understand the fact that economic agents make complex decisions surrounded by incomplete contracts, since the dynamics of the environment and other aspects of the situation are unknown. Contingencies hinder contracts, so agents omit some clauses in the contract in order to reduce costs. The degree of credibility of the agents involved is a factor that contributes to reducing uncertainties and increasing the confidence to consolidate contracts and transactions with the market (KATO; MARGARIDO, 2000; WILLIAMSON, 2010).

It is not advisable, however, to examine the issue of "doing" and "buying" taking into account only the characteristics and assumptions of transaction costs. Factors such as the quality of the products and services provided may also influence the search for competitive advantages, and should be considered (Coles & Hesterly, 1998).

Each governance structure (market, hierarchy or hybrid form) presents advantages and disadvantages, and divides opinion among authors.

Venkatesan (1992) criticizes the hierarchical form and says that companies should not invest resources in activities that do not add value to clients. Silva et al. (2009) also criticize the hierarchical form, since they understand that the choice for this type of strategy entails high maintenance costs in different sectors, including in times of crisis.

Chesbrough (2003) demonstrates that the isolation, from the hierarchical form, harms the organization, since exchanging experiences between different organizations, in an environment that demands immediate responses to new customer requirements, is crucial and important.

According to the author, a closed organization, that is, that does not communicate with external agents, loses opportunities to explore new ideas and new markets. In this way, approaches such as Open Innovation, which consists of a set of interconnected companies in order to offer something new to the consumer, add performance to the value chain.

In opposition, Serio and Sampaio (2001) disagree and understand that the outsourcing of activities can lead to the absence of essential skills for organization. Williamson (1991) points out that the hierarchical form provides greater security and reduces the degree of uncertainty mainly in relation to the supply of inputs, since it is the very organization that supplies the chain. Among the uncertainties are: unpredictable environmental events that affect the activities of agents linked to the productive chain, such as droughts and floods; errors of demand projections; failures in the supply of inputs, among others.

In the comparison between the different structures of governance, Monteverde and Teece (1982) argue that the hierarchical form would be more appropriate for sectors that seek to differentiate products and services in the market, while the market form would be more suitable for sectors that compete for costs, such as commodities. Williamson (2010) points out that all forms of governance have advantages and disadvantages in their structure and one must know how to extract the strengths of the adopted form.

Therefore, the hybrid form shows itself as an interesting alternative, since it presents characteristics of the other two and is supported by contracts that provide certain security for the companies in the transactions.

For Kumar et al. (2015), the success of a business starts from a perspective where competitive advantage is based on the organization itself, to another that is focused within an ecosystem where the products and processes of a company affect one or more ecosystems. There is a tendency for organizations to begin to develop their activities within a set of interconnected organizations in order to deliver better results to consumers.

Business ecosystems are composed of a set of interconnected nodes, occupied by one or more companies that participate since production, made up of downstream players, such as suppliers of raw material, and upstream players, inserted in the phase of consumption and post-consumption, such as valuation companies. For Kumar et al. (2015), some factors lead to the transition of individualized enterprises to ecosystems, such as the possibility of allocating tasks, reducing costs and the contribution of external entities that aggregate in the operational part.

CHARACTERIZATION OF A BUSINESS MODEL

Authors such as Osterwalder and Pigneur (2010), Demil and Lecoq (2010), Abell (1991) and Wirtz et al. (2016), proposes their business models, describes the elements that make up each model, but they do not make it clear if these models can be applied to any type of organization and do not indicate how these elements interact. The proposal of this research differs in this sense, since it seeks to identify the way in which the elements that make up a business model are related, and represent a business model that can be used by any and every type of organization.

To do so, six elements needed to characterize a business model were extracted from the literature review. These elements are: Resources and Competencies, Cost Structure, Partnerships, Distribution Channels, Value Proposition and Customer Segment.

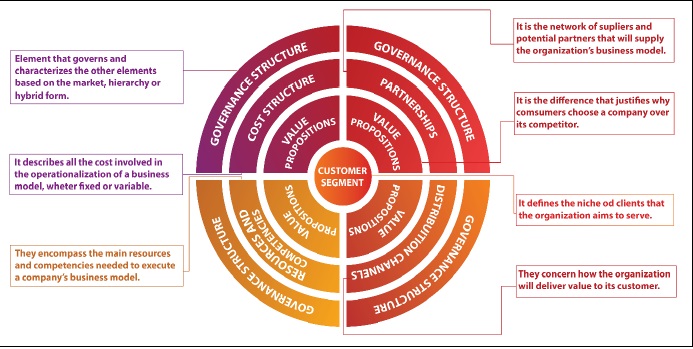

However, in pointing the TCE concepts in the characterization of a business model, this study understands that strategic relations encompass not only these six elements, but also the adopted governance structure, whether hierarchical, market or hybrid. Thus, it is understood that, among the six elements present in Table 3 of this study, there is a seventh element, which is the "governance structure" of the organization - the element that controls the business operation and characterizes the interactions between the other elements.

In this sense, the "governance structure" element involves how the elements "partnerships", "distribution channels", "cost structure" and "resources and competencies" interact to create a "value proposition" that serves a certain "customer segment". Thus, the present study understands that these four have particular governance structures, according to the TCE logic.

It is important to note that the "governance structure" component, extracted from TCE, differs from the "Organizational Structure" component, presented in the RCOV model and also present in other business models. The former establishes itself as something intangible, that characterizes relations between the other components, as market, hierarchy or hybrid, and the latter refers to a set of players that are part of the value chain of an organization.

The graphical representation of a business model allows to simplify the discussion about a certain subject. The literature presents different types of representations about business models: diagram, as in the model of Osterwalder and Pigneur (2010); flowTable, as seen in the model of Demil and Lecoq (2010), among others.

According to Carvalho (2005), the development of a graphic model consists of four stages: the first is the identification of each element in sequence, giving an idea of the progression of events; the second consists of the positioning of the identified elements; the third is the illustration of the relations that make up such a model; finally, the fourth step is the creation of a structure capable of identifying each element.

Wirtz et al. (2016) point out that one of the areas that should be explored in the theoretical development of business model is the design, that refers to the way in which the elements of the business model are represented. Thus, the present study aims to contribute to this gap evidenced by Wirtz et al. (2016) to facilitate the understanding of the interactions between the seven elements proposed here. The representation of the elements that make up the business model developed in this study can be identified in Figure 6 below.

Figure 6

Representation of the proposed business model

Survey data (2017)

The representation of the business model proposed in Figure 6 complies with the steps established by Carvalho (2005), although it has been adapted to a circular form. In this model, the Governance Structure is established in the first or outermost layer and involves the other four elements inserted in the second layer: Resources and Competencies, Cost Structure, Partnerships and Distribution Channels.

The elements of the second layer, when related, generate a value proposition for the organization, as presented in the third layer of the representation of Figure 6. The central layer, in its turn, is where the Segment of Customers is established, of which the organization will deliver your value proposition.

It is like an industry that produces haute couture clothing and that has machines and skilled personnel (resources and skills) in order to make its products; must pay for production inputs, such as fabrics, buttons and electricity; receives advice from a specialized company in fashion trends (partnerships); and uses the internet and direct selling to sell their clothes (distribution channels). When interacting, these four elements end up defining the value proposition of the company (third layer) to be delivered to its customers (fourth layer).

The four elements in the second layer may have different Governance Structures, so that in an organization the Resources and Competencies may be hierarchical, while the Structure of Costs presents a hybrid form or is supported by the market. According to this characterization, the same element may present more than one governance structure. An example of this can be illustrated by an organization that produces part of the needed resources for its production and purchases another part, either by contract or via the market.

The definition of governance structure, elements, resources and competences, cost structure, distribution channels and partnerships is influenced by the characteristics of TCE: asset specificity, frequency and uncertainty. The exception is the element of partnerships, which concerns the relationships between different entities. In this element does not apply the hierarchy structure, only the hybrid and market structures.

According to the competitive strategy adopted by the company, the elements present in the second layer show a certain strategy of governance. The differentiation strategy, for example, is based on the creation of products or services that differ from their competitors (Porter, 1985). According to TCE characteristics and assumptions, companies that opt for this type of strategy tend to use a higher degree of hierarchy in their governance structure.

Imagine that a company needs a material that a limited number of companies can supply, where a possible exchange of suppliers would entail damage to the production process. In this case, the tendency is for the company to verticalize its production line so as not to be influenced by certain unforeseen events of third parties, especially if it is inserted in an environment of high uncertainty. The same understanding can be applied to the other elements, such as cost structure, distribution channels and partnerships, the latter with the qualifications already mentioned above. According to this understanding, the following proposition is formulated: (1) when the organization's competitive strategy is based on differentiation, it is more likely that the organization's business model uses a higher degree of hierarchy (vertical integration) in its governance structure.

On the other hand, a company whose competitive strategy is based on cost leadership tends to offer products with low added value, and seeks to be competitive in reducing its costs and maximizing its sales. This type of company usually uses common resources in the market, that is, of low specificity, whose eventual change from one supplier to another could not change the company's production process. Therefore, the market structure could be the cheapest option, especially if it is inserted in an environment of low uncertainty. In this sense, the following proposition is formulated: (2) when the organization's competitive strategy is based on cost leadership, it is more likely that the organization's business model uses a greater degree of market transactions in its governance structure.

Companies that opt for strategies based on the formation of relationship networks tend to adopt a business model supported by contracts. Here the company does not verticalize its production, but also does not buy at random in the market. In this format, transactions are backed by contracts that provide certain guarantees to the parties involved. In this way, the following proposition is formulated: (3) when the organization's competitive strategy is based on the formation of networks, it is more likely that the organization's business model uses a greater degree of hybrid arrangements in its governance structure.

Therefore, it is possible to visualize the influence of the governance structure, as one of the elements present in the business model, according the representation of Figure 6. This research can contribute with the literature of the area, as it discusses how the components of a model are related, and how this relationship is represented in a graphical model, both theoretical gaps evidenced by Wirtz et al. (2016). In addition, it demonstrates the governance structure, originating from TCE, as one of its elements, and presents three propositions that relate the business model to TCE.

FINAL CONSIDERATIONS

Organizations are within an increasingly dynamic and competitive environment. In this context, understanding how different players can influence the organizational environment, and how these relationships are established, is critical to creating value in a company. In this sense, the contributions generated from this study can contribute to progress in the area of business model. This study sought to evidence the decisions the governance decisions in the business models. First, it was identified in the literature the interaction between the elements that characterize a business model and the representation of them, in order to collaborate with previous studies on the subject (WIRTZ et al., 2016).

The elements considered as those that compose a business model, identified by means of theoretical revision, were: segment of clients, represented in the central layer; proposal of value, present in the third layer; resources and skills; cost structure; partnerships and distribution channels, the four located in the second layer. However, by highlighting the assumptions and principles of TCE in this discussion, a seventh element was included, which governs all others, and it is the governance structure (first layer).

These elements, when related, result in the Value Proposition delivered by the organization, in the third layer, to meet the needs of its Customer Segment, element located in the fourth layer, or central layer. Based on this theoretical foundation, a graphic representation of business model was proposed, in a circular format, divided into four layers.

The analysis of the governance structure of the four elements present in the second layer generated three propositions:

a) When the organization's competitive strategy is based on differentiation, it is more likely that the organization's business model uses a higher degree of hierarchy (vertical integration) in its governance structure.

b) When the organization's competitive strategy is based on cost leadership, the organization's business model is more likely to use a greater degree of market-based transactions in its governance structure.

c) When the organization's competitive strategy is based on the formation of networks, it is more likely that the organization's business model uses a greater degree of hybrid arrangements in its governance structure.

From the results obtained, it can be concluded that this study can help in the development of the business model literature in two ways: (1) proposing and representing the way in which the elements that make up a business model interact, understood as a barrier to the evolution of the area, as evidenced by Wirtz et al. (2016); (2) evidencing new perspectives, supported by TCE, a theory widely used in strategic management, also suggested by Wirtz et al. (2016) and Kenworthy and Verbeke (2015). In addition, the representation of these elements, proposed in four layers, differs from those models reviewed in the current literature, for detailing and reorganizing how each element relates to each other and the result of those relations.

It should be emphasized that the proposal of this study is not to introduce a new business model, but to synthesize it, through the analysis of existing models. Thus, business models could be shown as a more accessible tool, through a differentiated approach, to be explored in further theoretical and empirical studies, as suggested by Arend (2013). For future studies, it is suggested the practical application of the business model proposed here, in order to test its effectiveness and empirical validation.

REFERENCES

Abell, D. (1991). Definição do negócio: ponto de partida do planejamento estratégico. São Paulo: Atlas.

Achtenhagen, L., Melin, L., & Naldi, L. (2013). Dynamics of Business Models – Strategizing, Critical Capabilities and Activities for Sustained Value Creation. Long Range Planning, 46 (6), 427-442.

Amit, R., & Zott, C. (2008). The fit between product market strategy and business model: implications for firm performance. Strategic Management Journal, 29(1), 1-26.

Amit, R., & Zott, C. (2010). Business model design: an activity system perspective. Long Range Planning, 43(2-3), 216-226.

Amit, R., & Zott, C. (2001). Value creation in E-business. Strategic Management Journal, 22(6-7), 493–520.

Arend, R. (2013). The business model: Present and future-beyond a skeumorph. Strategic Organization, 11(4), 390-402

Baden-Fuller, C., & Mangematin, V. (2013). Business Models: a Challenging Agenda. Cass Business School. Strategic Organization, 11(4), 418-427.

Berends, H., Smits, A., Reymen, I., & Podoynitsyna, K. (2016). Learning while (re)configuring: Business model innovation processes in established firms. Strategic Organization, 14(3), 181-219.

Bonazzi, F. L. Z., & Zilber, M. A. (2014). Inovação e Modelo de Negócio: um estudo de caso sobre a integração do Funil de Inovação e o Modelo Canvas . Revista Brasileira de Gestão de Negócios, 16(53), 616-637.

Brettel, M., Strese, S., & Flatten, T. C. (2012). Improving the performance of business models with relationship marketing efforts – An entrepreneurial perspective. European Management Journal, 30(2), 85-98.

Cabral, S. (2004). Analisando a reconfiguração da cadeia de produção de pneus no Brasil pela economia dos custos de transação. Gestão & Produção, 11(3), 373-384.

Carvalho, J. M. (2005). Graphical representation of transaction arrangements. Organizações Rurais & Agroindustriais, 7(2), 188-198.

Casadesus-Masanell, R., & Ricart, J. E. (2010). From Strategy to Business Models and onto Tactics. Long Range Planning, 43(2-3), 195-215.

Chesbrough, H. W. (2010). Business model innovation: Opportunities and barriers. Long Range Planning, 43(2-3), 354-363.

Chesbrough, H. W. (2003). The era of open innovation. Mit Sloan Management Review, 44(3), 34-41.

Chesbrough, H. W., & Rosenbloom, R. S. (2002). The role of business model in capturing value form innovation: evidence from Xerox Corporation’s technology spin-off companies. Industrial and Corporate Change, 11(3), 529-555.

Coase, R. (1937). The nature of the firm.Economica, 4(16), 386-405.

Coles, J. W., & Hesterly, W. S. (1998). Transaction costs, quality, and economies of scale: examining contracting choices in the hospital industry. Journal of Corporate Finance, 4(4), 321-345.

DaSilva, C. M., & Trkman, P. (2014). Business model: what it is and what it is not. Long Range Planning, 47(6), 379-389.

Demil, B.; Lecocq, X. (2010). Business Model Evolution: in search of dynamic consistency. Long Range Planning, 43(2-3), 227-246.

Gassmann, O. G., Frankenberger, K. & Csik, M. (2014). The St. Gallen Business Model Navigator.Working Paper of University of St. Gallen.

Gil, A. C. (2008). Métodos e técnicas de pesquisa social. 6 ed. São Paulo: Atlas.

Im, K., & Cho, H. (2013). A systematic approach for developing a new business model using morphological analysis and integrated fuzzy approach. Expert Systems with Applications, 40(11), 4463–4477.

Kato, H. T., & Margarido, M. A. (2000). Economia dos custos de transação (ECT): análise do conflito das bananas. Revista de Administração, São Paulo, 35(4), 13-21.

Kenworthy, T., & Verbeke, A. (2015). The future of strategic management research: Assessing the quality of theory borrowing. European Management Journal, 33, 179-190.

Kumar, P., Dass, M., & Kumar, S. (2015). From competitive advantage to nodal advantage: Ecosystem structure and the new five forces that affect prosperity. Business Horizons, 58(4), 469-481.

Lambert, S., & Davidson, R. (2013). Applications of the business model in studies of enterprise success, innovation and classification: An analysis of empirical research from 1996 to 2010. European Management Journal, 31(6),668-681.

Maglio, P. P., & Spohrer, J. (2013). A service science perspective on business model innovation. Industrial Marketing Management, 42(5), 655-670.

Markides, C., & Geroski, P. (2005). Fast Second: how smart companies bypass radical innovation to enter and dominate new markets. Jossey-Bass, San Francisco.

Mason, K., & Spring, M. (2011). The sites and practices of business models. Industrial Marketing Management, 40(6), 1032-1041.

Monteverde, K., & Teece, D. J. (1982). Suppliers witching costs and vertical integration in the automobile industry. The Bell Journal of Economics, 13(1), 206-213.

North, D. (1990). A transactions cost theory of politics. Journal of Theoretical Politics, 2(4), 355-367.

Osterwalder, A., & Pigneur, Y. (2010). Business model generation: A handbook for visionaries, game changers, and challengers. New Jersey: John Wiley & Sons.

Osterwalder, A., Pigneur, Y., & Tucci, C. L. (2005). Clarifying business models: Origins, present and future of the concept. Communications of the Association for Information Systems, 15, 2-40.

Pereira, B. A., & Caetano, M. (2015). A conceptual business model framework applied to air transport. Journal of Air Transport Management, 44-45, 70-76.

Petrini, M., Scherer, P., & Back, L. (2016). Modelo de negócios com impacto social. Revista de Administração de Empresas, 56(2), 209-225.

Porter, M. E. (1985). Competitive advantage: creating and sustaining superior performance. New York: Free Press, Collier Macmillan.

Porter, M. E. (1996). What is strategy? Harvard Business Review, 74(6), 61-78.

Raupp, F. Metodologia da pesquisa aplicável às Ciências Sociais. In: Beuren, I. (2006). Como elaborar trabalhos monográficos em Contabilidade: teoria e prática. 3 ed. São Paulo: Atlas.

Serio, L. C., & Sampaio, M. (2001). Projeto da cadeia de suprimento: uma visão dinâmica da decisão fazer versus comprar. Revista de Administração de Empresas, 41(1), 54-66.

Sorescu, A., Frambach, R., Singh, J., & Bridges, C. (2011). Innovations in retail business models. Journal of Retailing, 87, S3-S16.

Shafer, S. M., Smith, H. J., & Linder, J. C. (2005). The power of business models. Business Horizons, 48(3), 99-207.

Silva, V. L. S., Rodrigues, F., Sannomya, J., Peres, L., & Corvacho, T. (2009). Integração vertical como estratégia de apropriação de valor: um estudo exploratório no canal de distribuição de produtos agrícolas. Revista Gestão e Produção, 16(1), 44-53.

Teece, D. J. (2010). Business models, business strategy and innovation. Long Range Planning, 43(2-3), 172–194.

Tikkanen, H., Lamberg, J., Parvinen, P., & Kallunki, J. (2005). Managerial cognition, action and the business model of the firm. Management Decision, 43(6), 789-809.

Trimi, S.; Berbegal-Mirabent, J. (2012). Business model innovation in entrepreneurship. International Entrepreneurship and Management Journal, 8(4), 449-465.

Venkatesan, R. (1992). Strategic sourcing: to make or not to make. Harvard Business Review, 70(6), 98-107.

Williamson, O. E. (1991). Strategizing, economizing and economic organization. Strategic Management Journal, 12, 75-94.

Williamson, O. E. (1985). The Economic Institutions of Capitalism. New York: The FreePress.

Williamson, O. E. (2010). Transaction Cost Economics: The Natural Progression. Journal of Retailing, 86(3), 215–226.

Wirtz, B., Pistoia, A., Ullrich, S., & Gottel, V. (2016). Business Models: Origin, Development and Future Research Perspectives. Long Range Planning, 49, 36-54.

Zott, C., Amit, R., & Massa, L. (2010). The business model: theoretical roots, recent developments, and future research. IESE Business Scholl-University of Navarra.