COMPETITIVENESS OF THE MANUFACTURING SECTOR IN MEXICO, THE UNITED STATES AND CANADA 2006-2022: ADVANTAGES, DISADVANTAGES AND CURRENT TRENDS

COMPETITIVENESS OF THE MANUFACTURING SECTOR IN MEXICO, THE UNITED STATES AND CANADA 2006-2022: ADVANTAGES, DISADVANTAGES AND CURRENT TRENDS

Revista Científica "Visión de Futuro", vol. 29, núm. 1, pp. 22-38, 2025

Universidad Nacional de Misiones

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-CompartirIgual 2.5 Argentina.

Recepción: 21 Septiembre 2023

Aprobación: 28 Noviembre 2023

Abstract: This research seeks to analyze the competitiveness of the manufacturing sector in Mexico compared to the United States and Canada from 2006 to 2022 in the different industries that make it up to identify the advantages, disadvantages and trends. Official databases were consulted to correlate the information through statistics; specialists in the sector (Organization for Economic Cooperation and Development, Mexican Institute of Competitiveness, World Bank, Statistics Canada and the U.S. Bureau of Labor Statistics); reports and studies. The most productive sectors for Mexico compared to the United States and Canada are: food, beverages, tobacco, paper, non-metallic products and transport equipment. The least productive: leather and leather, furniture, textiles and automotive. And the stable ones: wood, metal products, machinery and basic metals. The main advantages: Nearshoring, geographical location, logistics and labor. The disadvantages for Mexico are: high dependence on the United States, disruption, technology transfer and inflation. And trends: wage increases, sustainability, turning suppliers into partners, new technologies (cloud, 5G and AI), redesigning work and work culture.

Keywords: Factory, Productivity, Trending, Mexico, United States, Canada.

INTRODUCTION

The reforms of the 1980s gave a boost to Mexico's development, prioritizing stability, eliminating trade protectionism, and reducing state intervention in the economy, according to Moreno Brid (2015).

These modified the productive structure due to the opening of markets to competition. NAFTA opened free trade, strengthening exports in the long term, leading to an increase in economic activity and employment. However, it has not been what was expected today; mainly in the manufacturing sector, which in Mexico is considered one of the engines of economic growth according to Carbajal, Suarez & Almonte (2017).

Mexico has now become a competitive country in terms of manufacturing, as it has large trade agreements with other countries. As well as other factors that benefit it. This research aims to address issues related to Mexico's competitiveness in relation to its USMCA trading partners (the United States and Canada) in a historical and comparative way. Along with this, a review of the advantages and disadvantages that Mexico has in manufacturing.

Camino Mogro (2017) comments that manufacturing worldwide has undergone many changes since the economic crisis of 2008 and because of this, studies on the subject became relevant as a tool to respond to public and business policies. In other words, new empirical models of competition and markets have emerged.

In order for a country to develop, it requires an industrial culture that involves skills, talents, market experiences, and economic factors according to Astikė (2022). Analyzing the issue of manufacturing will help to visualize those areas and factors that must be maintained, addressed, strengthened or reconsidered to continue with the level and that in the short and medium term can improve with respect to its business partners. A comparison of the main industries between the three countries is sought in order to understand and be able to land in a more objective way the situation of the manufacturing industry between them.

"The globalized scenario has posed many open challenges, especially in technology-related areas. Companies... they are subject to many complexities as they have to constantly update their technologies to gain a decisive advantage over their competitors" (Prabhu, Thangasamy & Abdullah, 2020, p. 39). Where being competitive includes: quality, delivery, cost, flexibility, know-how, customer focus and after-sales service.

Day by day, new forms of manufacturing are sought to be implemented at an accelerated pace and accessible. This is due to the new forms of consumption and demand from the markets; as well as the disruptive events that have impacted the world (the pandemic, lack of raw materials and energy, among others). This is where the manufacturing sector must look for the best strategies to solve, minimize or improve the situation.

DEVELOPMENT

Manufacturing

According to Camino Mogro (2017, p. 409) "the manufacturing sector is a strategic sector that is characterized by boosting the economy through mechanisms such as job creation, contributions and gross value added".

The manufacturing industry according to the North American Industrial Classification System, Mexico SCIAN 2013 cited by INEGI (2013):

This sector comprises economic units mainly engaged in the mechanical, physical or chemical transformation of materials or substances in order to obtain new products; mass assembly of manufactured parts and components; to the mass reconstruction of industrial, commercial, office and other machinery and equipment, and to the finishing of manufactured products by dyeing, heat treatment, plating and similar processes. This also includes the mixing of products to obtain different products, such as oils, lubricants, plastic resins and fertilizers. Transformation work can be done in places such as plants, factories, workshops, maquiladoras, or homes. These economic units generally use power-driven machines and manual equipment. (p.143)

For the NAICS Association (2022):

Establishments in the manufacturing sector are often described as plants, factories, or mills and use motor-driven machines and material handling equipment. However, establishments that transform materials or substances into new products by hand or at the worker's home and those that sell products made in the same premises from which they are sold, such as bakeries, confectionery shops and personalized tailors, may also be included in this sector. Manufacturing establishments may process materials, or they may contract with other establishments to process their materials for them. Both types of establishments are included in the manufacturing.

The manufacturing sector according to INEGI (2013) consists of: Food Manufacturing (NAICS 311), Beverage and Tobacco Products Manufacturing (NAICS 312), Textile Factories (NAICS 313), Textile Products Factories (NAICS 314), Apparel Manufacturing (NAICS 315), Leather and Related Products Manufacturing (NAICS 316), Wood Products Manufacturing (NAICS 321), Paper Manufacturing (NAICS 322), Printing and related support activities (NAICS 323), Petroleum and Coal Products Manufacturing (NAICS 324), Chemical Manufacturing (NAICS 325), Plastics and Rubber Products Manufacturing (NAICS 326), Non-Metallic Mineral Products Manufacturing (NAICS 327), Primary Metals Manufacturing (NAICS 331), Fabrication of Fabricated Metal Products (NAICS 332), Manufacture of Machinery (NAICS 333), Manufacture of Computer and Electronic Products (NAICS 334), Manufacture of Electrical, Electronic Equipment and Components (NAICS 335), Manufacture of Transportation Equipment (NAICS 336), Manufacture of Furniture and Related Products (NAICS 337), Miscellaneous Manufacturing (NAICS 339).

Competitiveness in Mexico

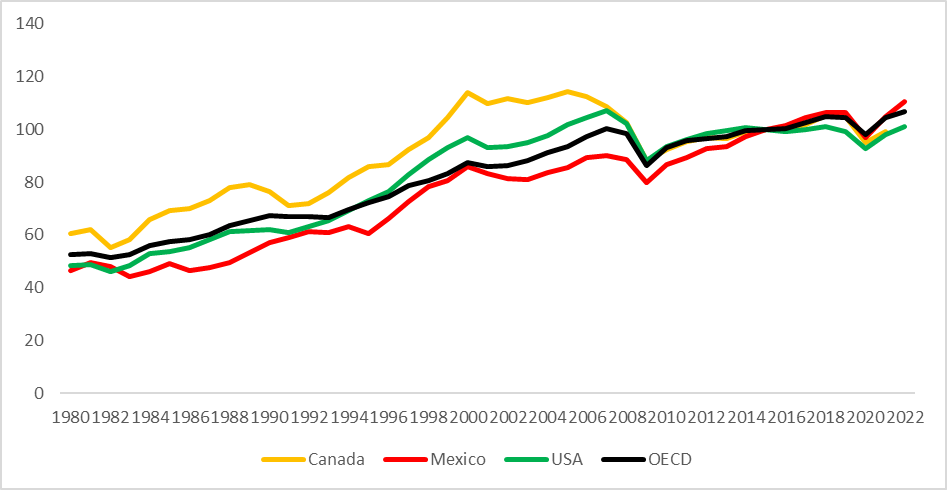

Competitiveness from the macroeconomic point of view is "the ability of companies to compete in the markets and, based on their success, gain market share, increase their profits and grow: generate value for shareholders and wealth for society" (Berumen & Palacios Sommer, 2011, pp.1-2). Mexico has played an important role in productive issues since its manufacturing sector has been growing in general terms, even reaching above-average levels. To give us an idea of the degree of competitiveness in Mexico's manufacturing sector vis-à-vis its USMCA trading partners and in relation to the OECD, Figure 1 shows the productivity index of the countries in question.

Figure 1

Productivity Index of Trading Partners and the OECD

Note. Based on information from OECD (2023a). Calculation based on 2015 = 100%

As can be seen, at the OECD level, productivity in the manufacturing sector is on the rise and that, although the United States and Canada as powers mark this trend to the rest of the 43 countries of the organization, Mexico, being a developing country, shows accelerated growth to such a degree that at the end of 2022 it exceeded its partners and the average (OECD). This shows the degree of competitiveness that Mexico has in the manufacturing sector, becoming a great trading partner, a viable country to invest in and a good economic future.

Manufacturing is related to a country's level of productivity; In this case, the Ministry of Finance and Public Credit (2022) states that Mexico is one of the most competitive countries for productive investment because:

Strategic geographical position; competitiv

Strategic geographical position; competitive costs; young and highly qualified human capital; size and strength of its domestic market; macroeconomic and political stability; economic growth; capacity to produce advanced manufactures (high-tech products); open economy that, through its network of free trade agreements that guarantees access to international markets.

The International Competitiveness Index (ICI) conducted by the Mexican Institute for Competitiveness (2022a) measures the capacity of 43 economies (to generate, attract, and retain talent and investment). IMCO itself points out (2022a, p.4) that:

A competitive country is one that, beyond the possibilities it has thanks to its own resources and capacities, is attractive to talent and foreign investment, and is thus in a position to achieve greater productivity and generate well-being for its inhabitants.

The same Mexican Institute for Competitiveness (IMCO) (Moy, 2020) mentions in terms of competitiveness that:

Mexico would have characteristics that would place it as a country with enormous potential: a young population, a still growing labor force, a middle class that has grown gradually and will increasingly seek access to more variety and quality of goods and services, a tax burden that is not too heavy in comparative terms, an unbeatable geographical location to position itself as a logistics center. abundant land and bearable climates, among many others.

Productivity by industry

Moreno Brid (2015) states that a productive structure generates sustainable growth of the economy if production and exports are competitive in the dynamic global segments; growth in innovation and technology activities; and a high degree of interconnectivity throughout the chain adds value.

Manufacturing in Mexico, for example, mentions Carbajal, Suarez & Almonte (2017), is heterogeneous in its growth by region, which causes different results in productive activities.

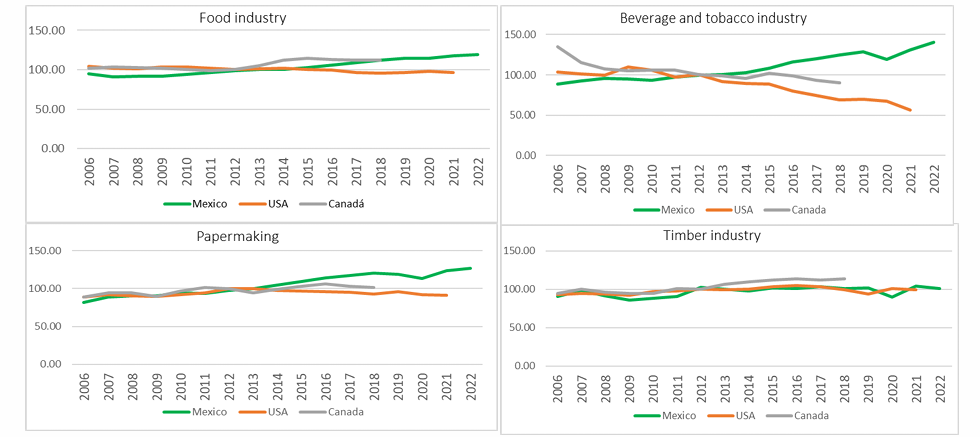

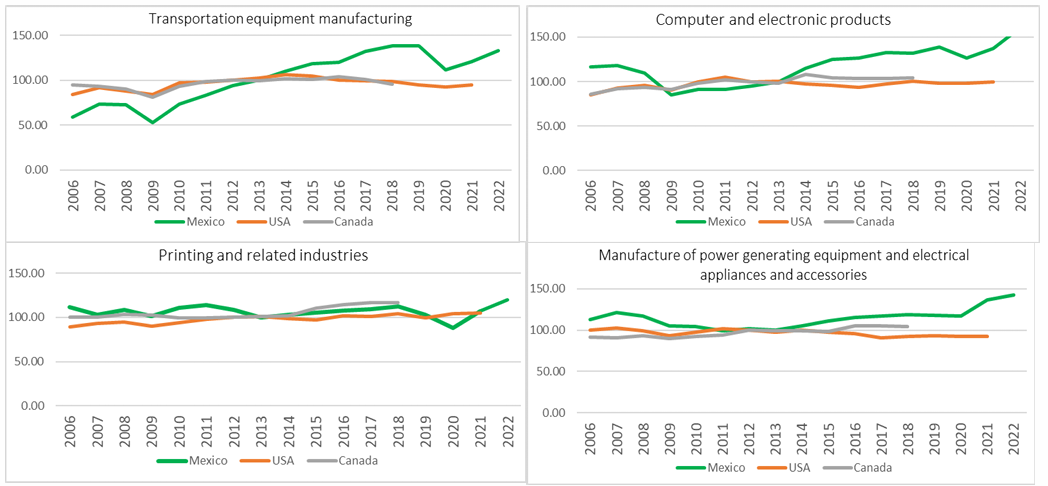

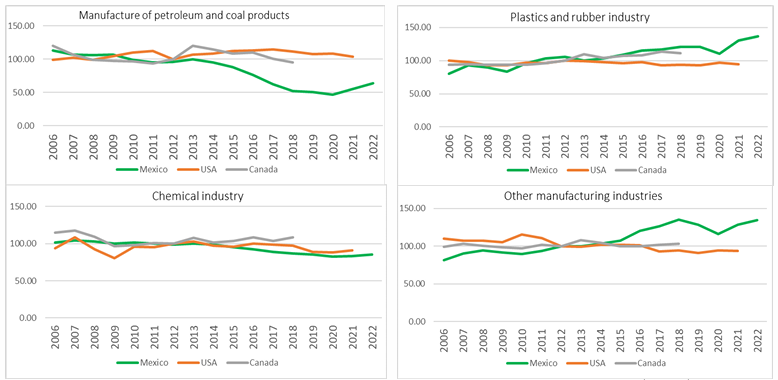

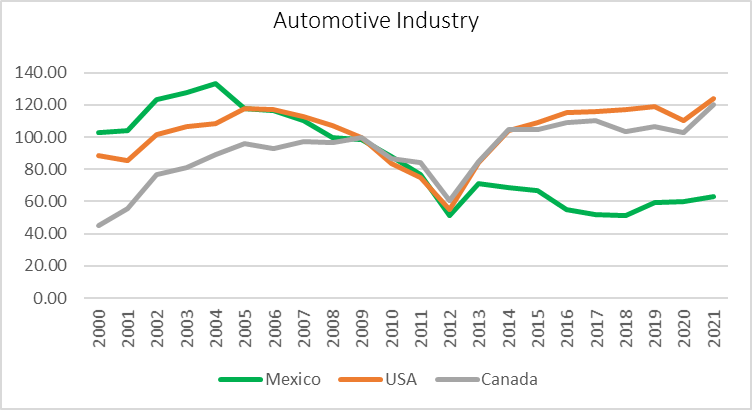

To begin with the analysis of how Mexico stands with respect to the United States and Canada; and by consulting various official databases, it is possible to clearly visualize the level of productivity that the three countries have for each industry. Canada only provides information up to 2018, even so, there is a trend that will help the analysis. This is shown in Figures 2 to 7 related to manufacturing industries.

Figure 2

Industry Comparison (Part 1)

Note. Based on information from the U.S. Bureau of Labor Statistics (2023); Statistics Canada (2022) and the Economic Information System (2023). The base for Mexico is 2013=100%, USA 2012=100% and Canada 2012=100%. Canada only has information up to 2018 and the USA up to 2021 on their official portals.

Figure 3

Industry Comparison (Part 2)

Note. Based on information from the U.S. Bureau of Labor Statistics (2023); Statistics Canada (2022) and the Economic Information System (2023). The base for Mexico is 2013=100%, USA 2012=100% and Canada 2012=100%. Canada only has information up to 2018 and the USA up to 2021 on their official portals.

Figure 4

Industry Comparison (Part 3)

Note. Based on information from the U.S. Bureau of Labor Statistics (2023); Statistics Canada (2022) and the Economic Information System (2023). The base for Mexico is 2013=100%, USA 2012=100% and Canada 2012=100%. Canada only has information up to 2018 and the USA up to 2021 on their official portals.

Figure 5

Industry Comparison (Part 4)

Note. Based on information from the U.S. Bureau of Labor Statistics (2023); Statistics Canada (2022) and the Economic Information System (2023). The base for Mexico is 2013=100%, USA 2012=100% and Canada 2012=100%. Canada only has information up to 2018 and the USA up to 2021 on their official portals.

Figure 6

Industry Comparison (Part 5)

Note. Based on information from the U.S. Bureau of Labor Statistics (2023); Statistics Canada (2022) and the Economic Information System (2023). The base for Mexico is 2013=100%, USA 2012=100% and Canada 2012=100%. Canada only has information up to 2018 and the USA up to 2021 on their official portals.

Figure 7

Industry Comparison (Part 6)

Note. Based on information from the U.S. Bureau of Labor Statistics (2023); Statistics Canada (2022) and the Economic Information System (2023). The base for Mexico is 2013=100%, USA 2012=100% and Canada 2012=100%. Canada only has information up to 2018 and the USA up to 2021 on their official portals.

Summarizing the productive activities in Table 1, we can find how they have behaved historically.

| On the downside | Sharp | On the rise |

| Leather products, fur and substitute materials | Wood | Food |

| Furniture Manufacturing and Related Products | Fabricated metal products | Beverages and Tobacco |

| Apparel | Machinery and Equipment Manufacturing | Papermaking |

| Manufacture of textile inputs | Basic metals | Non-metallic mineral base products |

| Petroleum and coal products | Transportation Equipment Manufacturing | |

| Chemical industry | Computer and Electronic Products | |

| Automotive | Printing and Related Industries | |

| Power Generation and Electrical Appliances and Accessories | ||

| Plastic and Rubber Other Manufacturing Industries |

With this, we have evidence of Mexico's competitiveness vis-à-vis Canada and the United States, and that other industries still need to be strengthened. Although there are several industries that have been below the productive level of the other two countries; This level is not negligible in percentage terms.

Productive disadvantages in Mexico

Mexico's main risk is a high dependence on exports with the United States, a lack of skilled labor, and inflation that impacts supply and demand are what Bautista (2022) observes. Engen Capital (2022) also warns that if the United States falls back into recession, it will be negatively reflected in Mexico's sector.

With a similar opinion, Luis Manuel Hernández (president of Index) talks about the weakness of the U.S. economy for 2023 (it will grow 0.5% in 2023 and 1.6% for 2024), which means a disadvantage for Mexico; including a small growth of 1.9% in 2022 (Morales, 2023). Castro (2022b) comments that manufacturing is a major pillar of the Mexican economy, generating foreign exchange, employment and foreign investment, and that if it decreases because of inflation, the repercussions can be significant.

For Hernández Reyes (2015), another disadvantage in Mexico is the high costs compared to its trading partners (electricity, telecommunications and internet); as well as inadequate economic regulation in the country (monopolies).

In an interview with Mario Hernández, KPMG's INMEX leader in Mexico, with Castro (2022b), he said that:

The effects or risks of inflation in manufacturing companies located in Mexico is the decrease in the products that are manufactured. This is due to the fact that their prices increase and their demand falls, since people's purchasing power does not grow in the same proportion as inflation. This generates greater inflationary pressure, in addition to the rise in interest rates in both the United States and Mexico. It is expected and confident that interest rate increases, and supply chain improvements will stabilize prices and control inflation.

In the KPMG report (2022), Ricardo Delfín (Lead Partner of Clients and Market at KPMG in Mexico and Central America) mentions that:

After two years of pandemic, we have moved from a period of uncertainty to one of resilience. We will have to learn to coexist not only with the pandemic, but with scenarios of permanent disruption, either due to natural events or constant innovation. Organizations must find a way to operate, changing the concept of a new reality to that of a changing reality.

Kovtunenko, Kovtunenko Yu, Fomina, Kovalchuk, & Kovtunenko Yu (2022, p. 231) state that:

The war has also affected international manufacturing companies with the imposition of large-scale economic sanctions, which have restricted access to energy resources and thus raised the prices of materials, manufacturing, and as a result, the transportation of products around the world.

Managers are changing organizational thinking, overcoming uncertainty, and investing in building trust with staff to develop an action plan to restore staff competitiveness that will provide a solid foundation for the future in the current uncertainty.

Guevara (2020) indicates that if there is no focus on greater efficiency in supply, production and distribution processes in times of crisis, companies will go into decline. According to Castro (2022a), the economic recovery forces companies to seek to improve their production chains. However, one of the challenges that Mexico faces is the level of sophistication in value chains such as Asia (digital transformation). The efficiency of local suppliers must be improved according to customer demand. Policies that support companies to set up in the country (clear and robust procedures).

Morales (2023) comments on the report of the National Council of the Maquiladora and Export Manufacturing Industry (Index) in which it forecasts a slowdown between 3 and 5% for the manufacturing industry in Mexico. After falling 9.6% in 2020 (due to the COVID-19 pandemic), 2021 grew 8.6%.

Productive Advantages in Mexico

Guevara (2020) writes about how in 2020 55% of manufacturing companies have sought to redesign their supply chain, which would represent an acceleration in aspects such as the adoption of new tools and human talent, remote work programs for the supply of raw materials and inputs.

In the same KPMG document (2022), it notes that:

The so-called Fourth Industrial Revolution envisioned major changes in business models in the following years; However, the pandemic came to accelerate what was already an imminent fact. The collaboration models of human and business talent, distribution and sales channels, among others, are totally different and everything indicates that they will continue to reinvent themselves. Those who are better prepared and open to maintaining a business where innovation is a fundamental part of their model, will have greater opportunities to prevail and define the agendas of the market.

Morales (2023) writes about what Luis Manuel Hernández, president of the Index, said, who mentioned the advantage that Mexico has in 2023 with the relocation of parts of the production chain in the country from the United States and Asia. This is since there is already a stable supply chain, convenient tariffs and that small and medium-sized enterprises can be involved to replace certain imports (electronics, textiles and furniture, among others) from India, Vietnam, Indonesia and China. (Morales, 2023)

Castro (2022a) comments that nearshoring represents a great opportunity for Mexico's industry. In reports such as those of Bain & Company, Mexico could be the leader in North America in the manufacturing sector, mainly in transportation, mechanical and electrical devices, and machinery. It may lead to more U.S. and European companies arriving in the automotive, appliances, machinery, furniture, and plastics sectors. While the electrical/mechanical device industry and industrial machinery can come from the United States. This is mainly in the northern zone such as Nuevo León, Coahuila and Chihuahua; and in the Bajío such as Querétaro, Guanajuato, San Luis Potosí, Jalisco and Aguascalientes. (Castro, 2022a)

Bautista (2022) mentions that Mexico is one of the main manufacturing hubs worldwide (27% GDP, 90% of the exportable value and 4.3 million jobs). The country offers competitive advantages related to labor and production costs, good export programs, and the USMCA. The states that contribute the most to GDP are: Coahuila, Querétaro, Estado de México, Aguascalientes, Guanajuato, Puebla and San Luis Potosí.

Due to the Free Trade Agreement between Mexico, the United States and Canada (USMCA), Castro (2022a) mentions that some industries do not have taxes on their exports and delivery times are two to three days. This helps companies respond to market needs. Mexico has the capacity to deal with potential crises that disrupt the supply chain (e.g., the COVID-19 pandemic). The country can help transnational corporations reduce their time and improve their supply chains and reduce the carbon dioxide emissions they generate from their current logistics; There are also the cultural, political and social benefits of the country.

This is reflected in the fact that manufacturing firms interact with intermediaries, making the relationship more reliable and predictable through innovation and technology, according to Wang et al. (2023), by applying the theories of absorptive capacity and dynamic capacities. Manufacturing companies need to be mindful of the limitations of the linkages between them.

Hernández (2021) assures that the sector faces challenges with great resilience and that it is supported by flexible financing programs, as well as investment in innovation and technology. All this will help to face the challenges of the new reality and regain the confidence of investors.

Outlook and Trends for Manufacturing in Mexico

The Logistics World (2023) in a review of manufacturing trends in Mexico points out that the country is in a position to receive industries with a propensity to migrate from China and they are: appliances, computers and electronics, plastics and rubber, metalworking, manufacturing of transport equipment, furniture, electrical equipment, and medical equipment. And for this, Mexico needs to develop more industrial parks.

Shahzad, Rehman, & Zafar (2022, p.10) comment that "organizations should provide favorable working conditions and encourage employees to acquire more advanced skills, specialized business operations (supply chain integration, innovation, and technology transfer) through education and training."

Siemens Digital Industries Software Vice President of Industrial Strategy Dale Tutt (2022), the trend for 2023 will be: "supply chain disruption, sustainability, staff turnover, and unexpected new challenges." So, for Tutt (2022), "additive manufacturing, artificial intelligence and machine learning (AI/ML), cloud and software-as-a-service, the industrial metaverse, IT/OT fusion, model-based systems engineering (MBSE) and what underlies it" must be adopted.

The Deloitte report (2023) analyzes the strength of the U.S. industry in 2022 that it took advantage of when it came out of the pandemic, exceeding expectations compared to the previous two years, however, they are experiencing problems related to inflation, economic uncertainty, and human talent. To address the above, strategies are sought such as: Maintaining momentum on investments in technologies that help manufacturing and pivot quickly; protecting long-term profitability that refers to the implementation of digital capabilities in the value chain to ensure profitability; and expanding advanced manufacturing capabilities related to robotics, automation, artificial intelligence, and machine learning capabilities.

"Accumulated technological capacity can make it easier for manufacturing firms to assimilate and combine the technological or market knowledge accessed for exploratory or exploitative service innovation" (Wang et al, 2023, p. 10). And for Skare and Soriano (2021, p. 230) "the level of globalization is associated with a lower barrier to digital technology adoption, as local firms put pressure on the government and local markets to reduce barriers to technology transfers."

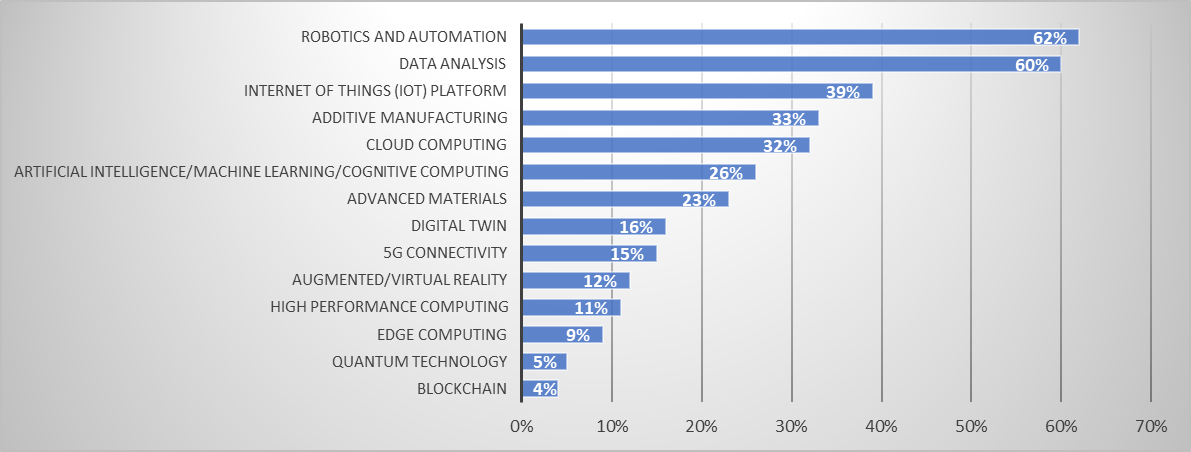

To support these strategies, Doloitte (2023) surveyed 100 U.S. executives on the type of technologies they consider necessary to increase operational efficiency over the next 12 months (Figure 8).

Figure 8

Technologies to be strengthened by 2023

Note. Taken and translated from Doleitte (2023, p.4).

As noted, U.S. executives are focusing more on robotics, automation, and data analytics. This should be the trend in Mexico and Canada as far as possible according to their capabilities. In other words, here we have what should be the trend that should be followed in the sector, taking the United States as a benchmark and economic power.

Regarding human talent, in the Deloitte report (2023), there is a need for changing human talent related to supply chain constraints, for which strategies such as: salary increases (although historically the base salary is high); upskilling and reskilling related to improving advanced technical and digital skills (skilled workers are scarce in the manufacturing industry); diversity, equity, and inclusion (DEI) strategy; and flexible work arrangements related to seeking the redesign of work and work culture.

The supply chain has been strongly affected in its disruption, increasing uncertainty and to mitigate its effect, as revealed by the executives surveyed for Doleitte (2023), they will be: partnering suppliers to improve the supply chain; diversify suppliers to mitigate risk; increase local capacity to reduce bottlenecks and logistics; and implement digital technologies to increase the visibility of the supply network (control and organization).

Of the next two points, Doleitte (2023) mentions that the transformation of the industry into smart factories must continue to have a holistic approach and remain competitive in the future through connectivity with the cloud, edge computing, and 5G, among others. And finally, in terms of sustainability, the environmental, social and governance (ESG) landscape must be considered, such as: waste management, increasing the diversity of suppliers, building smart buildings and electrifying industrial fleets.

Taking into account the data and information presented in this sector, we can list the advantages and disadvantages that Mexico has over its trading partners Canada and the United States, which are shown in Table 2.

| Advantages | Disadvantages |

| Currency Generation | High dependence on exports to the United States |

| Constant foreign investment | Lack of highly skilled labor (new technologies and AI) |

| Labor Required | Domestic inflation (rising prices and low demand) |

| Business Resilience | Inflation in the USA (interest rate hike) |

| Flexible and convenient financing programs | Possible recession in the USA |

| Nearshoring | Permanent disruption (pandemic, war, energy, etc.) |

| Logistics and geography (location and communication routes) | Changing collaboration models (based on market demand) |

| Reduction of carbon dioxide (smaller distance from the target market) | Poor attractiveness and efficiency of suppliers |

| Taxes (low or no) | Match the level of sophistication of the value chain of other countries (Asia and China) |

| Delivery times (2 to 3 days) | Technology transfer (zero in the USMCA) |

| Clear and robust policies | Little investment in new technologies (AI and 5G) |

| Proximity to the target market (North America and Latin America) | Little use of robotics and automation in general |

| Sustainability over time | Information and data (information collection and generation, data analysis, and specialized software) |

| Established and Updated Trade Agreements (USMCA) | Low wages |

| Cost and Availability of Supplies (Low and Fast) | Too many hours worked |

CONCLUSION

"Consumer preferences are often unpredictable in markets for goods and services" (Astikė, 2022, p. 229). In Mexico, there has been low growth in production and low growth in employment, which together result in minimal market growth; Above all, because productive activity has not responded to the economically active population. (Carbajal Suárez & Almonte, 2017)

For Mexico, there are factors that cannot be controlled, they are external and are driven by the economy and development in other countries. Being partners and part of the same region does not ensure that these factors will align to generate equal or favorable conditions in the short and medium term.

Mexico has historically had technological, political, and economic lags; This has meant that the country has had to accelerate and adjust its productive, political and economic environment to become a competitive partner in the manufacturing industry and with the potential to continue growing and improving.

Mexico's geographical location makes the rest of the world see it as a strategic point in economic terms. Its tariff policies and treaties make it a country with great economic benefits to settle in. And there is rapid adaptation to the conditions of production, technology and a trained and intellectual workforce.

Conditions in the manufacturing sector in Mexico, as well as in Canada and the United States, may change due to supply chain disruption, as happened in the United States in 2022. Inflation is skyrocketing due to economic issues worldwide, where the United States is the benchmark for other countries because it is one of the largest consumers in the world along with China. If these large countries are affected by inflation, it is sure to have an impact on the rest of the world.

Arshi & Burns (2019) state that innovation helps organizations develop in global markets and optimize their structures. To this end, "the acquisition of knowledge, information and learning must be a strategic imperative, without which know-how and the development of new skills will become a challenge" (p. 43). In Mexico, we must continue to work on the basis of trends, agreements and improve labor and technological conditions that accelerate productive, economic and competitive growth in the country. The many specialists in the sector consulted here call this resilience, which would be the capacity of the country and companies to overcome current and future regional and global circumstances.

A strengthening and dynamization of the manufacturing sector in Mexico are expected for the coming years, accompanied by its trading partners, since the new scenarios require collaborative work with a view to becoming a regional power in terms of production and trade.

Información adicional

redalyc-journal-id: 3579