Original article

Monetary policy and regional impacts: empirical evidence from the Brazilian states*

A política monetária e impactos regionais: evidência empírica para os estados brasileiros

Caio César de Azevedo caiocesarablsilva@gmail.com

Fernanda Faria Silva ferfaria@ufop.edu.br

Ivair Ramos Silva ivairest@gmail.com

Caio César de Azevedo caiocesarablsilva@gmail.com

Fernanda Faria Silva ferfaria@ufop.edu.br

Ivair Ramos Silva ivairest@gmail.com

Monetary policy and regional impacts: empirical evidence from the Brazilian states*

Economia e Sociedade, vol. 34, no. 3, e271273, 2025

Instituto de Economia da Universidade Estadual de Campinas; Publicações

Received: 18 January 2023

Accepted: 11 November 2024

Abstract:

This paper investigates the heterogeneous regional effects of monetary policy

across Brazilian states from 2004 to 2018. It introduces three new variables and

employs an alternative empirical technique to identify these regional effects.

Overall, the Northeast and North regions were the most significantly affected,

both positively and negatively; credit emerged as the most active regional

transmission mechanism, followed by interest rates and exchange rates. The paper

also highlights the importance of coordinating economic policies, particularly

monetary and fiscal policies, to address inequalities and economic disparities

in peripheral states.

JEL: R12, O23, R15.

Keywords: Regional finance, Regional economic policy, Regional economic disparities.

Resumo: Este artigo investiga os efeitos regionais heterogêneos da política monetária nos estados brasileiros de 2004 a 2018. Incluem-se três novas variáveis e uma técnica empírica alternativa para identificar os efeitos regionais é utilizada. De modo geral, as regiões Nordeste e Norte foram as mais afetadas, tanto positiva quanto negativamente; o crédito foi o mecanismo de transmissão regional mais ativo, seguido pelas taxas de juros e pelas taxas de câmbio. O artigo também destaca a importância da coordenação das políticas econômicas, especialmente das políticas monetária e fiscal, para enfrentar as desigualdades e disparidades econômicas nos estados periféricos.

Palavras-chave: Finanças regionais, Política econômica regional, Disparidades econômicas regionais.

1 Introduction

The literature on the effects of Regional Monetary Policy (RMP) began to emerge in the 1950s but gained prominence in research agendas from the 1990s onward, particularly following the implementation of the final phase of the European Monetary Union. This literature has examined RMP under various theoretical perspectives and regional scales. Previously, currency and financial variables were largely overlooked in these analyses due to the prevailing belief in money neutrality and its perceived inability to explain regional differences. However, the post-Keynesian literature has reinvigorated the debate on the role of money and the non-neutrality of money across time and space, significantly contributing to the analysis of the regional transmission of monetary policy and potentially affecting the persistence of regional inequalities (Dow; Rodríguez-Fuentes, 1997; Rodríguez-Fuentes; Dow, 2003; Rodríguez-Fuentes, 2006).

This article aims to advance the discussion on RMP in Brazil by making two main contributions: (i) incorporating three new variables (asset prices, regional fiscal components, and uncertainty); and (ii) applying an alternative empirical technique to identify regional effects. Specifically, this study analyses the regional transmission mechanisms of monetary policy and their impact on state-level economic activity and responses to national shocks. Considering the non-neutrality of money over time and space and the integration of new variables, this study hypothesizes improvements in the robustness and analysis of results within the regional empirical debate.

The remainder of this paper is organised as follows. Following this introduction, the first section provides a brief theoretical review of the post-Keynesian literature on the subject, focusing on the conceptualization of both structural and behavioural effects as coined by Dow and Rodríguez-Fuentes (1997) and updated by Rodríguez-Fuentes (2006). Section 2 presents a review of recent national empirical literature. Section 3 details the empirical analysis using the Vector Autoregression (VAR) model in levels for model estimation. Additionally, empirical measurements of regional responses by state are estimated using the Generalized Impulse Response Function (GIRF) for the period from January 2004 to December 2018. Finally, Section 4 discusses the results of these estimates and Section 5 concludes the paper.

2 Theoretical elements on Regional Monetary Policy in Brazil

In the international arena, the initial contributions on the effects of RMP began to emerge during the 1950s and 1970s. These contributions were discussed through various theoretical perspectives and applied to several countries and regions. The topic gained prominence in research agendas toward the end of the 1990s, particularly with the completion of the final phase of the Eurozone implementation (Dow; Rodríguez-Fuentes, 1997; Rodríguez-Fuentes; Dow, 2003; Rodríguez-Fuentes, 2006). In Brazil, however, this theme started to gain traction in research agendas in the early 2000s. This shift was marked by the consolidation of the initial phase of the Real Plan and the implementation of the macroeconomic tripod, which included generating fiscal surpluses, targeting inflation, and floating exchange rate1.

Building on Rodríguez-Fuentes (2006), this section presents the theoretical elements of the post-Keynesian approach to RMP, followed by a review of the Brazilian literature on regional monetary policy. This review addresses both structural and behavioural effects, with their definitions and implications discussed in the subsequent sections.

2.1 Aspects of post-Keynesian theory

The analysis of Regional Monetary Policy (RMP) can be understood through two distinct effects, as defined by Rodríguez-Fuentes (2006): structural effects and behavioural effects, within a post-Keynesian framework. Structural effects focus on examining whether regional responses to monetary policy, in terms of intensity and duration, exhibit symmetry across different regions. This strand of literature tests the transmission channels of monetary policy using real variables that characterise the regional economy’s structure (Carlino; DeFina, 1998; 1999).

If regional economic structures differ, the effects of monetary policy may vary across regions; otherwise, the responses would be the same. This perspective aligns with conventional economic orthodoxy, which often considers only structural factors in regional effects while ignoring or neglecting concepts such as uncertainty, the non-neutrality of money (in both the short and long term), the development of the banking system, and the liquidity preferences of the public and banks (Dow; Rodríguez-Fuentes, 1997; Rodríguez-Fuentes, 2006).

On the other hand, behavioural effects, as described by Rodríguez-Fuentes (2006), pertain to how economic and monetary conditions influence the financial behaviour of economic agents (including banks), thereby affecting economic activity beyond mere asymmetric shocks. In the (post-) Keynesian context, following authors such as Keynes ([1936]1985), Chick (1993a), and Amado (2000), a monetary economy of production is one in which money is non-neutral and affects economic agents’ decisions on investment, production, and capital accumulation in both the short and long term. There is non-probabilistic uncertainty and, being the time historical (irreversible), the liquidity preference as uncertainty about the future causes the economic agents (both the public - demand - and the banks - supply) to reassess their liquidity and profitability positions. This results in increased currency retention, deferred purchasing power, and inhibited investments and credit anticipation.

In examining central and peripheral regions (Dow, 1982), it is noted that economic agents at the regional level exhibit distinct liquidity preferences (Dow, 1987). This distinction is crucial for understanding the different patterns of financial concentration and wealth between central and peripheral regions, as well as the challenges of breaking the cycle of inequality, particularly in peripheral economies such as Brazil.

According to Dow (1982, p. 25-26), central regions are characterised “[...] by prosperity, which is expected to continue, active markets, and financial sophistication.” In contrast, peripheral regions are marked by “[...] a stagnating economy, thin markets, and a lesser degree of financial sophistication.” For example, central regions exhibit lower liquidity preferences but greater liquidity for regional assets due to their status as financial centers, access to financial instruments, high transaction volumes, and diverse markets characterized by financial sophistication. Peripheral regions, however, tend to exhibit higher liquidity preferences, with small businesses and financial institutions facing greater credit risks, weaker markets, and lower financial sophistication, leading to higher income variability and a preference for liquidity among agents (Dow, 1987).

Regarding banks, the stages of development of the banking system (Chick, 1986; 1993b) and their regional implications (Chick; Dow, 1988) are considered a gradual process that highlights the increasingly endogenous currency and demonstrates the importance of banks in the economy (Amado, 1998), affecting the effectiveness of monetary policy. Understanding national monetary policy and interpreting its effects on a regional level is therefore essential, given that economic agents operate within a monetary production economy.

2.2 Structural regional effects in the face of a unique monetary policy

The Brazilian regional studies on the impacts of monetary policy were more widespread in the 2000s. Bertanha and Haddad (2008) estimated the effects on economic activity across Brazilian states using a Spatial Structural VAR model, incorporating spatial econometrics techniques and concepts. Their findings indicate that the North and Northeast regions are more sensitive to positive monetary shocks, with notable disparities and spillovers, especially in credit accessibility.

With some similarities in terms of conclusions, Fonseca and Medeiros (2011) analyze the regional effects of monetary policy on production and credit in Brazilian states employing a VAR model. They discover that contractionary monetary policy leads to a decline in industrial production across all states and Brazil as a whole, with variations in timing and intensity, thus corroborating the findings in the literature on differentiated impacts. The Northeast experiences the largest drop in production, followed by the Southeast and the South. Credit effects are more varied in the initial months following the interest rate shock, with the Southeast showing the most significant reduction in credit supply, followed by the Northeast and the South.

In another study, Silva (2014) investigates whether monetary and fiscal policy shocks have asymmetric effects on the economic activities of Brazilian regions, given their diverse productive structures, income levels, and financial development. Utilizing a Structural VAR model and defining four types of shocks (business cycle, monetary policy, government spending, and government revenue), the results suggest that there are no significant differences in regional responses to business cycle shocks. The response to business cycle shocks is smaller compared to monetary policy shocks and follows a distinct pattern in regional output. Finally, the author concludes that responses to monetary shocks are more symmetrical across regions, compared to a fiscal shock. However, the former shock affects the regions’ activity more in terms of production fluctuations than the latter, stressing that the authorities should observe those differences when implementing a new policy, whether fiscal or monetary.

Braatz and Moraes (2016) explore the regional effects and asymmetries of monetary policy by examining how Brazilian states respond to shocks in the basic interest rate. Using a VAR model, the results show that the southern states are less affected, whereas northern states experience stronger effects due to limited access to alternative sources of financing, low participation in international trade, and economic sector concentration. The authors also point out that, in terms of economic policy, the most affected regions should receive different treatments to mitigate the effects in time and space.

Braga (2017) examines the impacts of monetary policy on agricultural and industrial production sectors, as well as trade sales in the state of Pernambuco. Using a VAR model, the author observes divergent responses among sectors both in the short and long term. The results also point out that most sectors show negative effects, and that fewer sensitive responses can also be observed in others whose share of capital is lower when compared with those of capital intensity. By observing the channels of transmission of interest (via characteristics of the productive structure of the industries) and credit (via the size of the establishments in the industries and the ability to obtain resources in the financial market), using a cross-section regression, the results point to a statistical significance of the credit channel in the industrial sectors, while the interest rate is not significant in any estimated model.

Almeida Jr., Lima, and Paula (2020) advance the research area by examining asymmetries in monetary and exchange rate policy shocks from an Optimum Currency Area perspective for Brazilian states. They employ a Factor Augmented Vector Autoregressive model to identify shocks through signal restrictions. Their findings indicate that the shocks are not significant, and the causes could be because some states have little economic integration and difficulties in recovering from asymmetric shocks. In general, the authors find that in response to monetary policy innovations, states show symmetry in price responses and non-predictability in economic activity.

This section highlights the convergence of the reviewed literature with the conventional perspective, which identifies regional asymmetries through the economic structure of regions and empirically tests transmission channels, particularly interest and credit, aligning with the concept of structural effects.

2.3 Behavioural regional effects

Studies addressing the regional effects of monetary policy from a heterodox theoretical and empirical perspective are relatively scarce and recent. Silva (2011) contributes to this literature by analyzing the relationship between centrality patterns, liquidity preference, and asymmetries in the transmission of monetary shocks in Brazilian states and autonomous communities in Spain. This study incorporates econometric measurements of regional effects from national monetary policy, with a focus on the defined centrality patterns and regional categorization to examine asymmetric transmission of various shocks.

Building on the work of Rodríguez-Fuentes (2006), the author calculates regionalized interest rates to provide empirical evidence on the differential effects of a single monetary policy across regions. The findings indicate that peripheral states (characterized by a higher liquidity preference and less advanced banking development) are more significantly impacted by restrictive monetary policy shocks. This results in regionally higher interest rates, which in turn affect investment expectations and the performance of the financial system, particularly the banking sector. Conversely, states such as Minas Gerais, Rio de Janeiro, and São Paulo exhibit lower regional interest rates, reduced liquidity preference, and a more advanced level of banking system development.

In general, Silva (2011) demonstrates that an increase in the interest rate leads economic agents to invest in more profitable securities than in the productive sector; moreover, both behavioural and structural factors can influence the liquidity preference of agents on both the supply and demand sides. The study finds that a contractionary monetary shock would increase the agents’ liquidity preference through a drop in expectations; lower levels of financial sophistication are associated with greater liquidity preference. Furthermore, faced with this scenario, the limitation for the composition of the portfolio in the peripheral regions would be in the possibility of choosing assets that are less sensitive to monetary shocks. This highlights the importance of the spatial dimension in understanding differentiated regional responses to common monetary shocks.

Diniz (2017) explores the regional impacts of economic policy on the manufacturing sector, integrating the debate on deindustrialization. Utilizing a VAR model and principal component analysis, the author categorized the 27 Brazilian states into three spatial units (peripheral, intermediate, and central). The results corroborate the explanation that different degrees of development in the regions can accentuate the impacts of an economic policy, highlighting regional and sectoral disparities as they are not able to absorb the effects of a policy. Additionally, Diniz (2017) concludes that the lack of coordination between regional and industrial development policy, together with the macroeconomic one, stresses regional inequalities in the country and hinders regional recovery.

Concerning the monetary policy shock on credit supply in Brazilian regions, Dutra, Feijó and Bastos (2017) investigate whether the heterogeneous behaviour of banks at regional levels would be able to interfere in the supply of credit with different maturity dates. The authors demonstrate that there is an increase in liquidity preference in all Brazilian regions in response to a positive interest rate shock in the regional credit supply. Based on banks’ perceptions of the expected return (their profitability), they add that those institutions reduce the effectiveness of monetary policy, considering that the country adopts restrictive policies in this regard. In short, Dutra, Feijó and Bastos (2017) argue that these differentiated responses are attributable to the management behaviours of banks based on their location, affecting economic growth and regional inequality reduction.

One notable aspect is the importance attributed by the public and banks to regional credit, uncertainty, and liquidity preference, which are incorporated into the models or influence the interpretation of results, challenging arguments like money neutrality. As Rodríguez-Fuentes (2006) argues, even if it is not possible to fully measure the behavioral effects of agents for empirical purposes, the authors justify their choice of data series despite limitations. Their results provide alternative measurements that approximate these concepts, enabling a more accurate assessment of their impact on empirical simulations.

In conclusion, the evidence presented in this literature reinforces the argument for studying regional monetary policy effects within the theoretical framework of post-Keynesian economics. This focus, particularly relevant for Brazil, expands the scope of research and contributes to the literature by aligning with the concept of behavioural effects. Accordingly, this paper seeks to advance the field by introducing new variables for analysis and utilizing an alternative empirical technique to identify regional shocks.

3 Statistical modelling and data

The VAR model developed by Sims (1980) is utilized in this paper to analyze the data, a common approach for modeling monetary policy and its transmission mechanisms.The goal is to analyze the dynamic relationships between the variables, but not necessarily to be interpreted as causality or deterministic relationships between them. The estimation of possible contemporaneous effects between the endogenous variables is not intended as well. Furthermore, identifying the economic assumptions to explain the ordering of the variables would be controversial, which is one of the reasons pointed out by Pesaran and Shin (1998) while advocating the use of the traditional VAR. For these reasons, the traditional VAR is used instead of the structured VAR model in the present paper.

In a VAR model, the current value of each endogenous variable depends on its own lagged values as well as the lagged values of all other endogenous variables in the model. According to Bueno (2015) and Hamilton (1994), a generalization of the VAR model is obtained by adding g exogenous variables that affect the endogenous ones, as shown in the following equation:

Where:

Xt is a q n × 1 vector of endogenous variables, as in the previous equations;

Φ0 is a n × 1 matrix of fixed unknown intercepts;

Φi is a n × n matrix of fixed unknown coefficients of the endogenous variables in Xt - i;

G is a matrix of n × g coefficients;

Zt is a vector of g × 1 exogenous variables, which may include deterministic variables;

et is a vector of random disturbances that is not correlated with the regressors, being non-autocorrelated, but contemporaneously correlated with each other.

Enders (2014) explains that the VAR model aims to uncover the interrelationships between variables. Referring to the literature of Sims (1980) and Sims, Stock, and Watson (1990), Enders (2014) suggests that differencing series when they are not stationary could result in the loss of important information. Sims, Stock, and Watson (1990) demonstrate that least squares estimators remain asymptotically consistent even in the presence of a unit root, and that differencing or correcting for series cointegration is sometimes unnecessary.

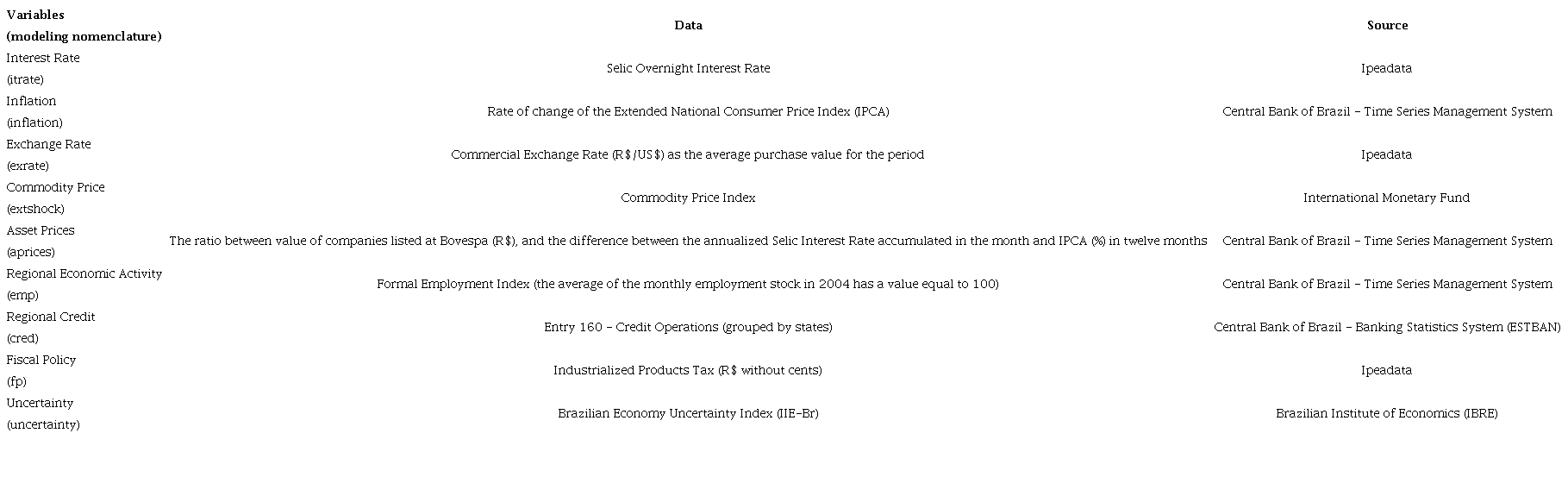

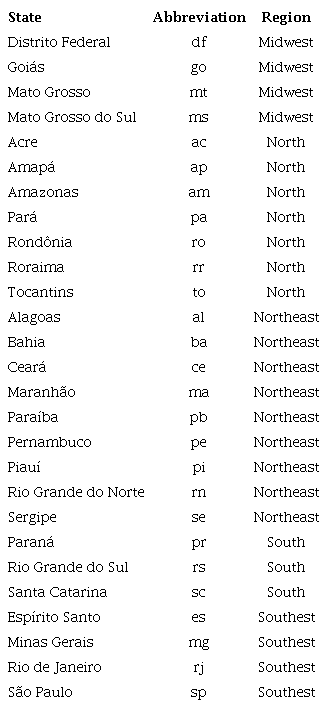

Given the availability of data on state economic activity, the analysis period spans from January 2004 to December 2018. The following variables were considered2: (i) Selic Overnight interest rate; (ii) rate of change of the Extended National Consumer Price Index (IPCA); (iii) commercial exchange rate, as the average purchase value for the period; (iv) commodity price index, to control external shocks in the Brazilian economy; (v) asset prices, using an approximation of the Tobin’s q by Montes and Machado (2014), to account for the impact of the stock market on investment; (vi) regional economic activity, measured by the formal employment index; (vii) regional credit, using Credit Operations (Entry 160) grouped by states; (viii) regional fiscal component, using the Industrialized Products Tax (IPI) series3 as an indirect monetary policy channel by Kaplan, Moll and Violante (2018); and (ix) uncertainty indicator, measured by the Economic Uncertainty Index - Brazil (IIE-Br), developed and extracted from the Brazilian Institute of Economics (IBRE, 2016b) of the Getúlio Vargas Foundation (FGV). The uncertainty indicator aims to assess whether uncertainty, in the post-Keynesian sense, can be validated in terms of economic effect, and to explore its dynamics across central and peripheral states. All variables, except for the commodity price index (iv), were included in the vector of endogenous variables.

Subsequently, the ADF and KPSS unit root tests were applied to assess the stationarity of the series in both levels and first differences. The stationarity of the series was also examined graphically. It is important to emphasize the choice to estimate the VAR model in levels, as the goal is to investigate the interrelationships between the variables rather than to perform forecasting4. Consequently, no differencing was applied to the series to achieve stationarity. Furthermore, to preserve the integrity of the data and avoid the loss of valuable information, the natural logarithm was not applied. Lastly, maintaining the original information, the state employment series will not be seasonally adjusted but will include 11 monthly dummies (February to December) in the estimates of each model to capture seasonality in the vector of exogenous variables.

Some authors argue that not establishing an ordering for the variables could impose restrictions on the estimated parameters, regardless of economic theory or researcher preference. Conversely, Pesaran and Shin (1998) developed the Generalized Impulse Response Function (GIRF) for linear models, where such an ordering is unnecessary, and the results are invariant to the order. Thus, the GIRF will be employed based on the arguments of Ewing (2003) to identify regional responses, as it is considered more robust compared to orthogonalized methods. The GIRF approach (i) does not require an explicit causal ordering of the variables, avoiding the use of different orthogonalization techniques that can produce varying responses depending on the technique; (ii) allows for better identification and interpretation of the initial effects of shocks on the model’s variables due to its non-orthogonal nature; and (iii) provides unique responses to impulses that incorporate the full pattern of historical correlations between shocks. This choice is also in line with the literature and Dutra, Feijó and Bastos (2017), contributing to the national debate on the topic5.

4 Results and discussion

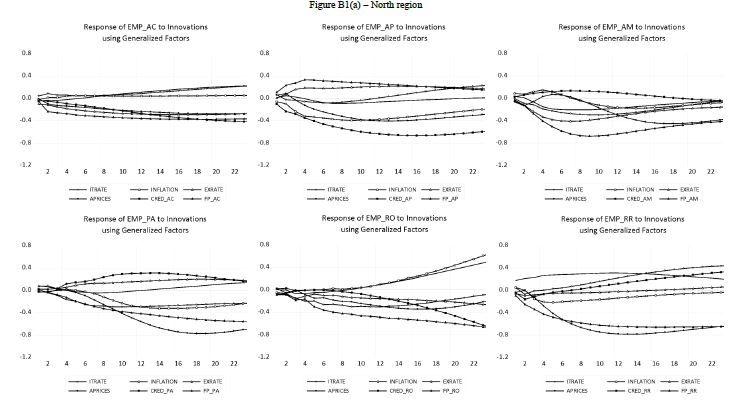

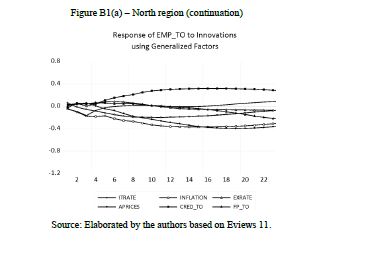

This section examines the regional responses of Brazilian states to changes in regional economic activity, as measured by the formal employment index, in response to impulses in monetary and fiscal variables, asset prices, and uncertainty. The structural and behavioural effects will be analyzed based on post-Keynesian literature for interpreting the results (see Appendix B). Results will be described and presented individually and by variable to facilitate state-level comparisons. The Generalized Impulse Response Functions (GIRFs) are standardized to one standard deviation.

It is important to note that the dynamics of the relationships between the variables in each model do not occur in isolation; however, for presentation and comparison purposes, they will be discussed in this manner. A comprehensive argument regarding regional responses will also be made based on the evidence found, even if this requires anticipating some results, which will be more thoroughly explored in the context of the respective shock. When using employment series as a variable of interest, it is crucial to recognize that the response timing may be delayed. Initial results are expected to be lower or constant, with the full effects becoming apparent in subsequent periods (Silva, 2011). This consideration supports and reinforces the choice of GIRF as an estimation method, particularly when observing low regional response intensities in the initial months (see Appendix B).

4.1 Differentiated transmission channels for a common economic policy

4.1.1 Interest rates

In line with much of the literature on RMP, interest rate effects on regional activity were primarily negative due to the contractionary monetary policy prevailing throughout most of the analyzed period, which broadly affected states in all regions. The greatest intensities were observed in states of regions with lower degrees of economic development such as the Northeast and North (Bertanha; Haddad, 2008), while the least negatively affected states are in the Southeast and South, which are more economically developed.

The impacts of interest rate shocks support the notion of differential incidence and suggest that regions with higher liquidity preferences, referred to here as peripheral, were the most affected due to lower levels of banking development. These findings emphasize that peripheral states experienced more intense reactions to restrictive monetary policy shocks, reflecting their economic fragility. Such intensity influences investment expectations and the performance of the banking (and broader financial) system in these regions, impeding economic growth and exacerbating disparities and instabilities relative to the central regions (Dow, 1987; Rodríguez-Fuentes, 2006; Silva, 2011; Diniz, 2017).

The states of Acre and Roraima (North) and Alagoas and Bahia (Northeast) showed positive employment impacts following the shock, as detailed in Appendix B. These effects might stem from sectoral characteristics, such as industries less sensitive or slower to react to interest rate changes, or from the expansion of the Brazilian economy, which boosted formal job creation until around 2013, mitigating the effects of monetary policy. Alternatively, these positive impacts could be linked to a shift in economic policy conservatism associated with the New Macroeconomic Matrix (NMM), which led to a period of declining Selic rates (2011-2013). Although still high, this decline might have stimulated regional economies through reduced credit costs6, for example, addressing both external and internal economic challenges while using interest rates as the primary monetary policy tool for inflation control (Nassif, 2015; Barbosa Filho, 2018).

With the onset of macroeconomic adjustments in 2015, the scenario shifted to one of policy exhaustion, deteriorating public accounts, reduced consumption and investment, sharp declines in commodity prices and international trade, and a political and institutional crisis, driven by a combination of internal and external factors. This period is also associated with the Brazilian economy’s expansion, driven by increased income transfers to low-income individuals and the elderly, wage adjustments for workers and civil service sectors, and favorable international economic conditions7. In early 2016, a new external shock, caused by another drop in commodity prices, contributed negatively to the country (Barbosa Filho, 2018; Lélis; Cunha; Linck, 2019; Villaverde; Rego, 2019). This scenario may have further hindered positive employment outcomes, particularly penalizing peripheral states with the reversal of interest rate declines, leading to levels surpassing those experienced during the international financial crisis.

It can be argued that using interest rates as the primary monetary policy instrument has revealed heterogeneous responses in terms of intensity and duration across Brazilian states, with the most severe reactions occurring in peripheral areas. The actions of the Central Bank of Brazil have had detrimental effects on the development of these peripheral regions, with contractionary effects anticipated due to the Inflation Targeting Regime (ITR) and persistently high interest rates for most of the evaluated period (until May 2017). This underscores the importance of understanding the structural and behavioural dynamics of state economies for the formulation and implementation of effective policies, especially in avoiding the perpetuation of economic disparities that further disadvantage peripheral states.

4.1.2 Inflation

The impacts of inflation were predominantly negative on regional activity, as detailed in Appendix B. According to Modenesi and Ferrari Filho (2011), Brazilian inflationary dynamics do not exhibit a strong relationship with domestic economic activity. Instead, the factors influencing these dynamics are associated with cyclical issues, costs (eg.: commodity prices), and structural factors, due to the inflationary inertia and historical roots of the Brazilian economy, rendering it a phenomenon influenced by both demand and supply. Barbosa Filho (2015) explains that even after the adoption of the floating exchange rate regime in 1999, monetary policy remains significantly affected by the high correlation between exchange rate fluctuations and inflation control, necessitating increased interest rates in response to exchange rate hikes.

The positive outcomes observed in states within peripheral regions align with the findings from the interest rate shock analysis, considering both external and internal conjunctural conditions. The tendency for interest rates to decline, including efforts by the NMM, despite remaining high, may have yielded beneficial effects in Acre and Alagoas, mitigating the negative impacts of interest rates in these states. Recognizing interest rates as the primary monetary policy instrument in Brazil, and their regional effects, combined with an appreciating exchange rate for most of the period, may have impaired the competitiveness and production of the national tradable goods industry. However, the exchange rate also contributed to inflation control (Nassif, 2015; Diniz, 2017; Villaverde; Rego, 2019). Furthermore, the positive impact of rising commodity prices, which benefited primarily exporting states, might have created a “buffering effect,” as noted by Stockl, Moreira, and Giuberti (2017, p. 178), by allowing these states to pass on cost increases to final goods.

This understanding is related to the market structure of regional economies, which affects firms’ financial costs and their ability to transfer these costs to prices. Central regions are more likely to be oligopolistic, whereas peripheral regions are more competitive. The former have greater capacity to pass on cost variations to prices, while the latter, due to their market structure, are less able to do so, making them more vulnerable and negatively impacted (Chick; Dow, 1988; Amado, 1998). Consequently, the industrial pattern and configuration reinforce the dominance of central regions over peripheral ones, as regional behaviour is influenced by the actions of the “headquarters agency” (Figueiredo; Crocco, 2012, p. 498), given the banking concentration within Brazil’s national financial system, where branch agencies are located in peripheral regions and headquarters in central ones. Consequently, they would be held hostage by the economic cycles for their availability of regional credit, due to the liquidity preference in the central regions.

In general, the results seem to reveal that the states of central regions, specifically the Southeast and the South, possess more developed institutional and economic frameworks to absorb and mitigate the negative effects of inflation. This is evident through structural and behavioural factors linked to their industrial and banking sectors, which demonstrate higher levels of economic and financial development, reduced uncertainty, and lower liquidity preferences. Thus, the Central Bank of Brazil’s national-level inflation control measures demonstrated adverse and asymmetric regional effects, particularly affecting less economically developed states in peripheral regions.

4.1.3 Exchange rate

The exchange rate effects were also largely negative on regional activity, with the states of the Northeast and North being the most affected (see Appendix B). The causes of inflation are both supply and demand related. There is a high correlation between the exchange rate and inflation, even after the adoption of the floating exchange rate regime; since the exchange rate continues to play a significant role in controlling inflation (Modenesi; Ferrari Filho, 2011; Barbosa Filho, 2015). The shock in costs caused by rising commodity prices, which occurred during the studied period, had notable effects on the Brazilian economy. This shock influenced the exchange rate and, consequently, affected employment in various states.

Periods of exchange rate appreciation combined with high interest rates tend to discourage production and weaken the competitiveness of the domestic tradable goods sector. These conditions also impact the productive structure and the balance of payments, particularly through the export basket, which stimulates imports despite benefiting from international prices (Nassif, 2015; Diniz, 2017; Stockl; Moreira; Giuberti, 2017). Even though there were periods of currency devaluation and declines in commodity prices (such as in September 2008 during the international financial crisis), the predominant combination of exchange rate appreciation and rising commodity prices appears to have had a greater relative impact during this period compared to the reverse scenario.

Villaverde and Rego (2019) explain that the commodity boom, which began in 2004 and continued until 2011, led to higher prices for primary goods like soy and iron ore, resulting in increased dollar flows to the Brazilian economy. Despite exchange rate appreciation, exporters of these commodities were significantly favored and did not experience negative profit pressures from exchange rate fluctuations8. From 2014 onward, the country experienced a downturn compared to the expansionary years of 2004-2013. Commodity prices began to decline sharply between mid-2014 and mid-2016, while the global economy and trade were also slowing down (Barbosa Filho, 2018; Lélis; Cunha; Linck, 2019).

In addition to sharp exchange rate devaluations, Brazil experienced post-financial crisis policy exhaustion, which led to deteriorating public accounts and reduced consumption and investment. As argued by the authors, Brazil’s regressive specialization and extensive financial opening, resulting from deindustrialization and reliance on international trade in natural resources, left it vulnerable to financial cycles and commodity price fluctuations. This context reinforces the country’s fragility and highlights the need to interpret both conjunctural and structural factors, both domestic and external, to understand the dynamics of the Brazilian economy.

For such reasons, the combination of these results suggests that states with a significant export profile, such as Bahia and Pará, experienced attenuated negative effects due to the export effect, similar to states in the Southeast and South regions (Silva, 2011), as shown in Appendix B. Conversely, states with a heavy reliance on imports or those predominantly importers, indicating their dependence on central regions, such as those in the Northeast and North, were more negatively impacted. This highlighThis supports the viewts the disincentives to production and the loss of competitiveness faced by these states in the domestic market.

Even though the exchange rate has been used to control inflation in a sense of “buffering effect” and using interest as the main instrument of monetary policy, when realising its regional effects, it is evident that this combination of instruments to combat inflation in the moulds of the ITR has had detrimental effects on Brazilian states, with an emphasis on the least developed ones. Consistent with the inflation analysis described herein, the market configuration and banking system of both the centre (oligopolistic and “headquarters agencies”) and the peripheries (competitive and branch agencies) underscore the vulnerabilities of these locations. They are not only subject to economic cycles and dependence on central regions but also affected by the performance of national monetary policy and external sector dynamics, resulting in differentiated impacts on states in terms of regional structure and behaviour.

4.1.4 Asset prices

The impacts of the asset price channel on employment, represented by a measure of Tobin’s q, exhibited only two response patterns, both showing generalized negative effects on regional activity (see Appendix B). The first pattern observed included representation from all regions, with the smallest regional negative responses. Notably, this pattern includes all states from the Midwest and South regions. In the second pattern, states in the Northeast, North, and Southeast generally displayed negative responses between the fifth and eighth periods, in contrast to the positive responses observed in earlier periods. In terms of intensity, within the group of the most affected states, those in the Northeast and North were particularly notable.

Industrial concentration can result from banking concentration, as peripheral regions often host industrial branches linked to national bank branches. This setup demonstrates an advantage for national banks over regional ones, leading to the transfer of reserves to central regions and reinforcing national banking concentration. Consequently, financial availability in peripheral regions could be compromised relative to central regions, reinforcing the dominance of the center over the periphery (Chick; Dow, 1988; Amado, 1998). Additionally, while peripheral regions might capture positive spillover effects from policies implemented in central regions (Silva, 2011; Diniz, 2017), these effects are less pronounced due to their structural and behavioural characteristics, which make them more susceptible to the impacts of contractionary policies. Due to this dynamic, the centrality characteristic can mitigate the effects of monetary policy, contributing, once again, to maintaining the dominance of the centre over the periphery by affecting the liquidity preference of the agents of that region, perpetuating the regional economic inequalities among them (Dow, 1987).

Peripheral regions often face greater uncertainty, instability, and fragility, along with lower levels of economic and financial development. Monetary policy can influence the composition of savers’ portfolios through behavioural effects. Investors may favor safer and more liquid assets, leading to a migration of financial resources to central regions, which offer greater security, liquidity, and asset diversification. This scenario tends to increase asset values in central regions. Given Brazil’s predominantly national financial system, regional agencies are influenced by the liquidity preference of central agencies, which allocate resources to less uncertain regions (Chick; Dow, 1988; Rodríguez-Fuentes, 2006; Figueiredo; Crocco, 2012).

The “functional distance”9, to central regions can cause less developed or peripheral regions to increase their liquidity preference, negatively impacting local credit. As a consequence, the agencies of the central regions would determine the form of asset allocation, being passed on to their branches, diverting them to the more developed regions. The peripheral regions act as intermediaries in financial allocation, sustaining low levels of economic development, high uncertainty, and limited local credit (Cavalcante; Crocco; Jayme Jr., 2006).

The states most negatively affected were those farther from the financial center, characterized by greater distances, lower levels of development, higher uncertainty, and liquidity preference, such as those in the Northeast and North regions (see Appendix B). Thus, considering the cost of local capital as a locational decision factor for firms, central regions in a national financial system could reinforce their dominance relative to peripheral regions, perpetuating regional financial inequalities through asset concentration and displacement, which impacts local credit and investment and hinders growth and development (Amado, 1998; Figueiredo; Crocco, 2012).

In the sense of seeking to incorporate the interrelations of this shock with the previous ones, especially interest and exchange rates, it is possible to raise the hypothesis that for the period studied, the combination of the effects of the commodity boom, the exchange rate appreciation, the high levels of interest rate and, as a consequence, the entry of foreign capital into the country, leading to speculative behaviour in the Brazilian capital market, particularly in shareholder capital seeking short-term gains from interest rate differentials, which reinforces regional disparities and hinders growth and development in peripheral regions (Nassif, 2015).

This hypothesis gains theoretical support when considering that, following the Lehman Brothers’ bankruptcy, global investors exhibited heightened risk aversion, leading to a broad flight to quality and significant devaluation of the national currency (Freitas, 2009). In response, the Brazilian government raised interest rates, reversing earlier reductions made as an anti-cyclical measure during the financial crisis (Barbosa Filho, 2018). By not regulating capital flows, a measure that could prevent speculative capital entry and support long-term financing for productive investments, the market did not contribute to job creation and economic development. Even if the spillover effect were small (or perhaps negative) for peripheral regions, the general results indicate the (non) capacity of this channel to generate jobs for the period considered, having little effect on the “real side” of the economy when perceiving the very discreet and non-permanent positive regional responses.

4.1.5 Regional credit

The impacts of regional credit on employment have produced varying results across states, both positive and negative, as detailed in Appendix B. Among the states showing the highest positive magnitudes, only those in the Northeast and North regions were identified. In terms of the negative intensities, the greatest effects were seen in the North and Southeast of Brazil. From 2014 onwards, a decline in the volume of state credit can be observed, explained by reduced credit concessions, such as the expansion of disbursements by the Brazilian Development Bank (BNDES) and the increase in reserve requirements (Diniz, 2017; Barbosa Filho, 2018).

Greater credit instability in peripheral regions can be attributed to both structural factors, such as less economic diversification and development, greater dependence on economic cycles, product growth rates, and expectations (Rodríguez-Fuentes, 2006), and behavioral factors, including the development of the banking system and the liquidity preference of banks and the public, which influence the supply and demand for credit (Dow and Rodríguez-Fuentes, 1997). Consequently, these regions may exhibit more unstable credit availability patterns compared to central regions, with credit contracting during economic downturns and expanding during periods of growth, reflecting their higher dependence on economic cycles (Chick; Dow, 1988).

Brazil’s bank-based financial development model may exacerbate these conditions. As previously discussed in relation to asset prices, the Brazilian financial system’s structure could reinforce this scenario. The dependence of peripheral region bank branches on the behaviour of central branches may sustain low levels of economic development by reducing credit availability in times of high uncertainty (Cavalcante; Crocco; Jayme Jr., 2006; Figueiredo; Crocco, 2012).

The lower intensities observed in the states of central regions may be associated with higher levels of banking development, causing them to carry out off-balance-sheet operations by means of the management of liabilities due to financial innovations; thus, credit expansion would be carried out through credit derivatives and new over-the-counter securities, making operations more profitable (Chick, 1993b; Farhi; Prates, 2018). Hence, there would be a competitive advantage for these banks, compared to those based in peripheral regions, in their ability to create credit due to bank development.

In this context, while the direct control of the economy’s money stock by monetary authorities may be constrained by banks’ balance sheet management and financial innovations, this does not imply that monetary policy is ineffective. Prudential regulation and banking supervision are crucial for addressing the liquidity preferences of banks and borrowers. Such measures can influence behavioural factors and thus enhance the effectiveness of monetary policy in achieving economic stability (Dow; Rodríguez-Fuentes, 1997; Rodríguez-Fuentes, 2006).

Supporting this argument and considering the international financial crisis, Freitas (2009) explains that Minsky’s hypothesis of financial fragility is reinforced, increasing economic instability in this scenario. To mitigate these effects, regulations could be imposed on bank indebtedness levels, credit quality, and composition. However, as financial innovations increase, the complexity of the financial system and the relationships between creditors and debtors also evolve, underscoring the need to rethink monetary policy concepts (Chick, 1993b; Rodríguez-Fuentes, 2006; Farhi; Prates, 2018).

Since the analysis period covers most of the post-crisis period, the negative effects of an expansion of credit in the peripheral regions, beyond the high interest rates, the negative effects of inflation, and the appreciated exchange rate, in the existence of an even higher level of uncertainty in these locations due to the external situation, highlight the need for economic policy coordination (Sicsú, 2001). The interaction between these results and fiscal policy (discussed later) reveals a scenario that reinforces the fragility of peripheral regions compared to central ones. This affects agent expectations, inhibits and postpones investments, and results in a greater liquidity preference among the public and regional banks, reducing loan expansion during high uncertainty (Chick; Dow, 1988; Amado, 1998).

Emphasizing the importance of assessing the combined effects of shocks and their interrelationships, as previous highlighted in the interest rate shock, employment in states in peripheral regions that have benefited from credit expansion policies may be linked to the previously used argument of constant reductions in the Selic rate, making it possible to expand in these states by reducing their cost. However, this reasoning does not apply uniformly across all states, reinforcing the need for policymakers to understand regional dynamics. Accordingly, because of the heterogeneity of results within the same region, either due to factors linked to structure or behaviour, the performance of monetary policy in this case, in coordination with other policies, should mitigate the negative effects on peripheral regions but also observe the specific characteristics of each state. Additionally, actions should focus on addressing regional economic inequalities and creating mechanisms to protect these regions, especially during crises and periods of high uncertainty.

4.1.6 Fiscal policy

The impacts of the regional fiscal component revealed that at least one state exhibited a positive response (excluding the Northeast region) and a negative response (excluding the South region). Among the states that experienced the most significant benefits from the shock, only those in the North and Midwest regions were identified. Conversely, the Northeast and North peripheral regions displayed notably greater negative magnitudes compared to the previous group and other shocks, as detailed in Appendix B.

In response to the 2008 financial crisis, the federal government implemented an expansionary fiscal policy (2008-2010) to stimulate aggregate demand and mitigate the crisis’s adverse effects. This was achieved through various measures, including temporary tax exemptions like the reduction of the IPI. Additional expansionary measures were introduced in income transfer programs (Bolsa Família), housing (Minha Casa, Minha Vida), infrastructure (Programa de Aceleração do Crescimento), and BNDES disbursements (Diniz, 2017; Barbosa Filho, 2018). Furthermore, the period saw a significant inflection in economic policy with the NMM, which strongly utilized fiscal policy by increasing public spending and investments (Barbosa Filho, 2017). Consequently, these countercyclical policies may have lessened the severe impacts on regional economies, particularly peripheral ones.

However, the Northeast and North peripheral regions, characterized by low levels of economic development, were the most adversely affected during this period. These regions experienced much higher negative intensities compared to other shocks, possibly reflecting fiscal deterioration due to the exhaustion of post-crisis policies and the fiscal adjustment implemented by the federal government in 2015 (Barbosa Filho, 2018), as mentioned before, which may have contributed to a worsening of results.

When observing the effects obtained here and comparing them with those of Silva (2014) and Diniz (2017), in addition to the differences in the variables and periods considered (which are sufficient to account for differences in the results), both demonstrate the dependence of peripheral regions on coordinated economic and industrial policies for local development and growth. These policies, in turn, would aim to settle disparities and dependence on the centre, especially in periods of crisis with different regional effects, requiring some type of mechanisms to protect these locations. Otherwise, the argument of greater sensitivities in peripheral regions to the fiscal policy shock is reinforced here, as well as that the type of fiscal policy to be implemented can accentuate regional disparities, contributing to their maintenance.

Sicsú (2001) argues for the necessity of coordinating economic policies, diverging from the orthodox view that subordinates monetary policy to fiscal policy since this could undermine its effectiveness because it is linked to inflation expectations. Diniz (2017) notes that if economic agents believe that policies aimed at reducing unemployment will lead to increased inflation, it will create instability in monetary policy performance. Therefore, Sicsú (2001) emphasizes the importance of ensuring that fiscal policy is viable, credible, and supported by clear objectives and adequate tools. This helps shape financial and entrepreneurial market behaviours in the desired direction and maintains a strong reputation among policymakers.

From a regional perspective, the argument is reinforced by the fact that the states most affected by employment reductions are in the Northeast and North regions, which have low levels of economic development and high uncertainty. These regions lack robust institutions and mechanisms to buffer against economic cycles and external fragility compared to the Southeast and South regions. Thus, the need to expand the concept of monetary policy is reiterated.

Additionally, enhancing elements of prudential regulation and banking supervision is crucial, particularly through direct state intervention in the financial system, to mitigate the economic impacts of contractionary shocks while considering regional specificities (Dow, 1982; Amado, 1998; Rodríguez-Fuentes, 2006). Furthermore, it is essential for both central and state governments to coordinate monetary and fiscal policies to promote and stimulate industrial policies in peripheral regions. This requires clear guidelines and careful, reputable, and prudent state action, as the state’s performance is perceived through “private logic,” which could exacerbate regional economic disparities between central and peripheral area (Amado, 1999; Sicsú, 2001).

4.1.7 Uncertainty

The impacts of the variable used to capture the effect of uncertainty on employment revealed heterogeneous results across states. There appears to be a certain “pattern” in the shape of the curves (U or V type, depending on the intensity of the shock), although there are variations in recovery times (see Appendix B). It is important to note that these data also reflect the effects of both external and internal adverse shocks, such as the international financial crisis (2007-2008), the slowdown in Chinese economic growth (2011), the national political scenario (2014), and the Brazilian economic recession (2015-2016).

Souza, Zabot, and Caetano (2019) emphasize the importance of uncertainty in interpreting and understanding economic dynamics, an area that remains underexplored. They argue that adverse shocks can diminish the effectiveness of economic policies aimed at recovery when these effects are pronounced during periods of high uncertainty. Supporting this view, Santos (2019) finds that the effectiveness of monetary policy on economic activity is greater during periods of lower uncertainty. Attempts to capture signs of uncertainty in the post-Keynesian sense reveal both agreement and disagreement. Since fundamental uncertainty cannot be estimated (Keynes, [1936]1985; Amado 2000; Rodríguez-Fuentes, 2006), there are mixed results.

Results consistent with this argument show that peripheral regions, specifically the Northeast, North, and Midwest, were the most negatively affected. When these results are compared with other shocks, the highest negative intensities are observed in these states across various shocks. These findings support the argument that these locations experience a higher level of uncertainty. Additionally, agreement is found in the observation of lower negative intensities in central regions (Southeast and South) across interest rate, exchange rate, and fiscal policy shocks. These results highlight and reinforce the heterogeneities and inequalities among states, indicating the dominance of central regions over peripheral ones.

However, some evidence does not support this argument, as states in the Northeast and North regions exhibited similar low negative responses as those in the South. Following this perspective, an increase in uncertainty was expected to generally reduce employment in states, with greater intensity in peripheral regions. Yet, results from some states in the Northeast, North, Midwest, and Southeast regions showed positive effects of this shock. Overall, this study evaluates the measurement as not being interesting in capturing uncertainty in the post-Keynesian sense. The agreement with some results supports this view, while the counterevidence does not necessarily refute the theory.

5 Conclusions

This article aims to analyze the mechanisms of regional transmission of monetary policy across Brazilian states, utilizing post-Keynesian literature to support the interpretation of the results. A significant contribution of this study is the inclusion of variables beyond those commonly used in the literature on RMP for Brazil. These additional variables include asset prices, the regional fiscal component, and uncertainty. Moreover, the measurement of regional responses was conducted using GIRF, which are still relatively underutilized in national studies. This approach offers the advantage of not imposing restrictions on the estimated parameters or requiring an ordering of the variables, thus yielding invariant results with respect to their order.

The findings align with both Brazilian and international literature that highlights asymmetries in regional responses. These asymmetries are evident both in isolation and when evaluated collectively, with a particular emphasis on states considered peripheral, such as those in the Northeast and North regions, in contrast to Southeast and South regions. This observation addresses empirical questions about differentiated impacts on states from a common national shock. The results for the evaluated period sustain Brazil’s role as vulnerable to economic cycles, a situation exacerbated by external shocks due to financial and trade openness. This vulnerability is particularly severe in peripheral regions. Recent political and institutional crises have also contributed to these outcomes.

It can be argued that the Central Bank of Brazil’s strategy to control inflation, within the framework of the Inflation Targeting Regime (ITR), predominantly focused on high interest rates and an appreciated exchange rate. This strategy has had a detrimental effect on the growth and development of states, particularly those in peripheral regions. In this context, short-term gains from interest rate differentials between countries indicate that the Brazilian stock market needs improvement to make a more substantial contribution to the country’s economic development and growth.

The performance of monetary policy through credit, aimed at stimulating demand to mitigate impacts, revealed an uneven effect across states. This disparity is attributed to varying stages of regional development within the banking system and the overall configuration of the Brazilian financial system. Fiscal policy, utilizing tax measures, demonstrated relevance but also revealed significant disparities in its effects, particularly in peripheral states. These results highlight the need for coordinated economic policies that consider regional specificities to stimulate development in less developed areas. Evidence of uncertainty further supports the post-Keynesian argument of differing liquidity preferences across regions. Although uncertainty has had negative effects in Brazilian states, the lowest magnitudes were observed in central regions, while peripheral states experienced higher magnitudes.

Regarding the persistence and duration of shocks impacting regional product during the analyzed period, as represented by state employment, credit emerged as the most prominent monetary variable. This was followed by interest rates, inflation, and exchange rates, which could be classified as intermediate variables, with asset prices being the least prominent. For the fiscal variable, signs of a prolonged recovery suggest the presence of long-term effects, potentially linked to the persistent impacts of the NMM adopted during the period.

In addition, uncertainty showed lasting and permanent effects, with few instances of dissipation. This supports the post-Keynesian argument of non-neutrality of money in time and space, reinforcing the importance of credit for regional development and highlighting the need for policymakers to coordinate fiscal (and monetary) policy effectively. Clear and transparent implementation is crucial, given the enduring effects of economic policy uncertainty on states.

The study also demonstrated that uncertainty, liquidity preference, and banking development are crucial in explaining the asymmetries of shocks. The configuration of the national financial system and regional market structures has contributed to maintaining disparities and regional heterogeneities among states. If coordinated policies (monetary, fiscal, industrial, foreign exchange) aimed at reducing economic inequalities, particularly in peripheral regions, are not implemented, these disparities may persist, jeopardizing regional development and national stability, especially during times of high uncertainty.

The incorporation of behavioural factors enriched the interpretation of regional effects, leading to a more robust understanding of regional dynamics and validating the article’s empirical hypothesis. It was shown that the primary mechanisms of monetary transmission in terms of incidence and propagation for the evaluated period were credit (most relevant), followed by interest rates and exchange rates. At the empirical level, the results revealed asymmetric regional effects of monetary policy in Brazil, concerning signs, intensities, and durations. At the theoretical level, the evidence supports the robustness of post-Keynesian literature, confirming its richness in interpretation by considering both structural and behavioural factors in analyzing regional impacts of a common economic policy.

References

ALMEIDA JR., L. C. de; LIMA, E. C. R.; PAULA, L. F. de. Assimetrias nas respostas dosestados brasileiros aos choques na política monetária e no câmbio: uma análise utilizando um modelo FAVAR. Nova Economia, Belo Horizonte, v. 30, n. 1, p. 143-175, 2020. Disponível em: https://revistas.face.ufmg.br/index.php/novaeconomia/article/view/4643.

AMADO, A. M. Limites monetários ao crescimento: Keynes e a não-neutralidade da moeda. Ensaios FEE, Porto Alegre, v. 21, n. 1, p. 44-81, 2000. Disponível em: https://revistas.fee.tche.br/index.php/ensaios/article/view/1960.

AMADO, A. M. Moeda, financiamento, sistema financeiro e trajetórias de desenvolvimento regional desigual: a perspectiva pós-keynesiana. Revista de Economia Política, São Paulo, v. 18, n. 1, p. 76-89, jan./mar. 1998. Disponível em: https://centrodeeconomiapolitica.org.br/rep/index.php/journal/article/view/1123.

AMADO, A. M. Moeda, sistema financeiro e trajetórias de desenvolvimento regional desiguais. In: LIMA, G. T.; SICSÚ, J.; PAULA, L. F. de (Org.). Macroeconomia moderna: Keynes e a economia contemporânea. Rio de Janeiro: Campus, 1999. cap. 9, p. 208-224.

BARBOSA FILHO, F. H. A crise econômica de 2014/2017. Estudos Avançados, São Paulo, v. 31, n. 89, p. 51-60, abr. 2017. Disponível em: http://www.revistas.usp.br/eav/article/view/132416.

BARBOSA FILHO, N. O desafio macroeconômico de 2015-2018. Revista de Economia Política, São Paulo, v. 35, n. 3, p. 406-426, jul./set. 2015. Disponível em: https://centrodeeconomiapolitica.org.br/rep/index.php/journal/article/view/231.

BARBOSA FILHO, N. H. Revisionismo histórico e ideologia: as diferentes fases da política econômica dos governos do PT. Brazilian Keynesian Review, [s. l.], v. 4, n. 1, p. 102-115, 2018. Disponível em: https://braziliankeynesianreview.org/BKR/article/view/160.

BERTANHA, M.; HADDAD, E. A. Efeitos regionais da política monetária no Brasil: impactos e transbordamentos espaciais. Revista Brasileira de Economia, Rio de Janeiro, v. 62, n. 1, p. 3-29, jan./mar. 2008. Disponível em: http://bibliotecadigital.fgv.br/ojs/index.php/rbe/article/view/1018.

BRAATZ, J.; MORAES, G. I. de. Impactos regionais assimétricos da política monetária no Brasil: uma abordagem com o método VAR para o período 2002-11. Ensaios FEE, Porto Alegre, v. 37, n. 2, p. 367-398, set. 2016. Disponível em: https://revistas.dee.spgg.rs.gov.br/index.php/ensaios/article/view/3138.

BRAGA, C. F. A. Impactos da política monetária sobre os diferentes setores industriais do Estado de Pernambuco. 2017. 53f. Dissertação (Mestrado em Administração e Desenvolvimento Rural)-Departamento de Administração, Universidade Federal Rural de Pernambuco, Recife, 2017. Disponível em: http://www.tede2.ufrpe.br:8080/tede2/handle/tede2/7180.

BUENO, R. L. S. Econometria de séries temporais. 2. ed. rev. atual. São Paulo: Cengage Learning, 2015. 341p.

CARLINO, G.; DEFINA, R. The differential regional effects of monetary policy. The Review of Economics and Statistics, [s. l.], v. 80, n. 4, p. 572-587, nov. 1998a. Disponível em: https://www.jstor.org/stable/2646839?seq=1.

CARLINO, G.; DEFINA, R. The differential regional effects of monetary policy: evidence from the U.S. states. Journal of Regional Science, Malden, v. 39, n. 2, p. 339-358, 1999a. Disponível em: https://onlinelibrary.wiley.com/doi/abs/10.1111/1467-9787.00137.

CAVALCANTE, A. T. M.; CROCCO, M.; JAYME JR., F. G. Preferência pela liquidez, sistema bancário e disponibilidade de crédito regional. In: CROCCO, M.; JAYME JR., F. G. (Org.). Moeda e território: uma interpretação da dinâmica regional brasileira. Belo Horizonte: Autêntica, 2006. p. 295-315.

CHICK, V. Macroeconomia após Keynes: um reexame da teoria geral. Rio de Janeiro: Forense Universitária, 1993a. 416p.

CHICK, V. The evolution of the banking system and the theory of monetary policy. In: FROWEN, S. F. (Org.). Monetary theory and monetary policy: new tracks for the 1990s. London: Palgrave Macmillan, 1993b. cap. 4, p. 79-92.

CHICK, V. The evolution of the banking system and the theory of saving, investment and interest. Économies et Sociétés. Monnaie et Production, v. 20, n. 3, p. 111-126, Aug./Sept. 1986.

CHICK, V.; DOW, S. C. A post-Keynesian perspective on the relation between banking and regional development. In: ARESTIS, P.; SKOURAS, T.; KITROMILIDES, Y. (Ed.). Thames papers in political economy. London: Thames Polytechnic, 1988. p. 1-23. Disponível em: http://hdl.handle.net/1893/22686.

DINIZ, G. F. C. A região importa? A indústria de transformação brasileira frente à política econômica de 2004 a 2015. 2017. 292f. Tese (Doutorado em Economia)-Centro de Desenvolvimento e Planejamento Regional, Faculdade de Ciências Econômicas, Universidade Federal de Minas Gerais, Belo Horizonte, 2017. Disponível em: http://hdl.handle.net/1843/32043.

DOW, S. C. Money and regional development. Studies in Political Economy, [s. l.], v. 23, n. 1, p. 73-94, 1987. Disponível em: https://www.tandfonline.com/doi/abs/10.1080/19187033.1987.11675566.

DOW, S. C. The regional composition of the money multiplier process. Scottish Journal of Political Economy, [s. l.], v. 29, n. 1, p. 22-44, Feb. 1982. Disponível em: https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1467-9485.1982.tb00434.x.

DOW, S. C.; RODRÍGUEZ-FUENTES, C. J. Regional finance: a survey. Regional Studies, [s. l.], v. 31, n. 9, p. 903-920, 1997. Disponível em: https://www.tandfonline.com/doi/abs/10.1080/00343409750130029.

DUTRA, L. D.; FEIJÓ, C. A. V.; BASTOS, J. C. A. Impacto de choques de política monetária sobre a oferta de crédito regional: uma análise econométrica a partir da metodologia VAR para o Brasil nos anos 2000. Brazilian Keynesian Review, [s. l.], v. 3, n. 1, p. 48-74, 2017. Disponível em: https://www.braziliankeynesianreview.org/BKR/article/view/94.

ENDERS, W. Applied econometric time series. 4. ed. New York: John Wiley & Sons, 2014. 485p.

EWING, B. T. The response of the default risk premium to macroeconomic shocks. The Quarterly Review of Economics and Finance, [s. l.], v. 43, n. 2, p. 261-272, 2003. Disponível em: https://www.sciencedirect.com/science/article/abs/pii/S1062976902001473.

FARHI, M.; PRATES, D. M. A crise financeira e a evolução do sistema bancário. Brasília: IPEA, 2018. p. 3-28. (Texto para Discussão, n. 2431). Disponível em: https://www.ipea.gov.br/portal/index.php?option=com_content&view=article&id=34419.

FIGUEIREDO, A. T. L.; CROCCO, M. A. A moeda como um fator interferente na escolha locacional das empresas. Revista de Economia Contemporânea, Rio de Janeiro, v. 16, n. 3, p. 487-508, set./dez. 2012. Disponível em: https://revistas.ufrj.br/index.php/rec/article/view/24200.

FONSECA, M. W. da; MEDEIROS, M. L. Impactos regionais da política monetária no Brasil pós-regime de metas de inflação. Ensaios FEE, Porto Alegre, v. 32, n. 2, p. 515-552, nov. 2011. Disponível em: https://revistas.fee.tche.br/index.php/ensaios/article/view/2290.

FREITAS, M. C. P. de. Os efeitos da crise global no Brasil: aversão ao risco e preferência pela liquidez no mercado de crédito. Estudos Avançados, São Paulo, v. 23, n. 66, p. 125-145, jan. 2009. Disponível em: http://www.revistas.usp.br/eav/article/view/10415.

HAMILTON, J. D. Time series analysis. Princeton, New Jersey: Princeton University Press, 1994. 799p

KAPLAN, G.; MOLL, B.; VIOLANTE, G. L. Monetary policy according to HANK. American Economic Review, [s. l.], v. 108, n. 3, p. 697-743, Mar. 2018. Disponível em: https://www.aeaweb.org/articles?id=10.1257/aer.20160042.

KEYNES, J. M. A teoria geral do emprego, do juro e da moeda: inflação e deflação. 2. ed. São Paulo: Nova Cultural, 1985. 333p.

LÉLIS, M. T. C.; CUNHA, A. M.; LINCK, P. O choque nos preços das commodities e a economia brasileira nos anos 2000. Revista de Economia Política, São Paulo, v. 39, n. 3, p. 427-448, jul./set. 2019. Disponível em: https://centrodeeconomiapolitica.org.br/rep/index.php/journal/article/view/42.

MODENESI, A. M.; FERRARI FILHO, F. Choque de oferta, indexação e política monetária: breves considerações sobre a aceleração inflacionária recente. Revista Economia & Tecnologia, Curitiba, v. 7, n. 3, p. 1-9, jul./set. 2011. Disponível em: https://revistas.ufpr.br/ret/article/view/26607. Acesso em: 25 jun. 2020.

MONTES, G. C.; MACHADO, C. C. Efeitos da credibilidade e da reputação sobre a taxa Selic e a transmissão da política monetária para o investimento agregado pelo canal dos preços dos ativos. Pesquisa e Planejamento Econômico, Rio de Janeiro, v. 44, n. 2, p. 241-287, ago. 2014. Disponível em: http://repositorio.ipea.gov.br/handle/11058/3314.

NASSIF, A. As armadilhas do tripé da política macroeconômica brasileira. Revista de Economia Política, São Paulo, v. 35, n. 3, p. 426-443, jul./set. 2015. Disponível em: https://centrodeeconomiapolitica.org.br/rep/index.php/journal/article/view/232.

PESARAN, H. H.; SHIN, Y. Generalized impulse response analysis in linear multivariate models. Economic Letters, [s. l.], v. 58, n. 1, p. 17-29, Jan. 1998. Disponível em: https://www.sciencedirect.com/science/article/abs/pii/S0165176597002140. Acesso em: 27 ago. 2020.

RODRÍGUEZ-FUENTES, C. J.; DOW, S. EMU and the regional impact of monetary policy. Regional Studies, [s. l.], v. 37, n. 9, p. 969-980, Dec. 2003. Disponível em: https://www.tandfonline.com/doi/abs/10.1080/0034340032000143959.

RODRÍGUEZ-FUENTES, C. J. Regional monetary policy. Abingdon: Routledge, 2006. 180p.

RODRÍGUEZ-FUENTES, C. J.; PADRÓN-MARRERO, D. Industry effects of monetary policy in Spain. Regional Studies, [s. l.], v. 42, n. 3, p. 375-384, Apr. 2008. Disponível em: https://doi.org/10.1080/00343400701291583.

SANTOS, F. R. Incerteza econômica e eficácia da política monetária no Brasil. 2019. 74f. Dissertação (Mestrado em Economia)-Faculdade de Economia, Universidade Federal de Juiz de Fora, Juiz de Fora, 2019. Disponível em: https://repositorio.ufjf.br/jspui/handle/ufjf/9991.

SICSÚ, J. Credible monetary policy: post Keynesian Approach. Journal of Post Keynesian Economics, [s. l.], v. 23, n. 4, p. 669-687, 2001. Disponível em: https://www.tandfonline.com/doi/abs/10.1080/01603477.2001.11490305.

SILVA, F. F. Centralidade e impactos regionais de política monetária: um estudo dos casos brasileiros e espanhol. 2011. 293f. Tese (Doutorado em Economia)-Centro de Desenvolvimento e Planejamento Regional, Faculdade de Ciências Econômicas, Universidade Federal de Minas Gerais, Belo Horizonte, 2011. Disponível em: http://hdl.handle.net/1843/AMSA-8ULRUG.

SILVA, I. E. M. The differential regional effects of monetary and fiscal policies in Brazil. In: ENCONTRO NACIONAL DE ECONOMIA, 42., 2014, Natal. Anais do 42° Associação Nacional dos Centros de Pós-Graduação em Economia, 2014. Área 4: Macroeconomia, Economia Monetária e Finanças, p. 1-19. Disponível em: https://en.anpec.org.br/previous-editions.php?r=encontro-2014. Acesso em: 9 abr. 2025.

SIMS, C. A. Macroeconomics and Reality. Econometrica, [S. l.], v. 48, n. 1, p. 1-48, jan. 1980. Disponível em: https://www.jstor.org/stable/1912017?seq=1. Acesso em: 9 abr. 2025.

SIMS, C. A.; STOCK, J. H.; WATSON, M. W. Inference in linear time series models with some unit roots. Econometrica, [S. l.], v. 58, n. 1, p. 113-144, jan. 1990. Disponível em: https://www.jstor.org/stable/2938337?seq=1. Acesso em: 9 abr. 2025.

STOCKL, M.; MOREIRA, R. R.; GIUBERTI, A. C. O impacto das commodities sobre a dinâmica da inflação no Brasil e o papel amortecedor do câmbio: evidências para o CRB Index e Índice de Commodities Brasil. Nova Economia, Belo Horizonte, v. 27, n. 1, p. 173-207, jun. 2017. Disponível em: https://revistas.face.ufmg.br/index.php/novaeconomia/article/view/2945. Acesso em: 9 abr. 2025.

VILLAVERDE, J.; REGO, J. M. O novo desenvolvimentismo e o desafio de 2019: superar a estagnação estrutural da economia brasileira. Revista de Economia Política, São Paulo, v. 39, n. 1, p. 108-127, jan./mar. 2019. Disponível em: https://rep.org.br/rep/index.php/journal/article/view/28. Acesso em: 9 abr. 2025.

Appendix A. Data and source

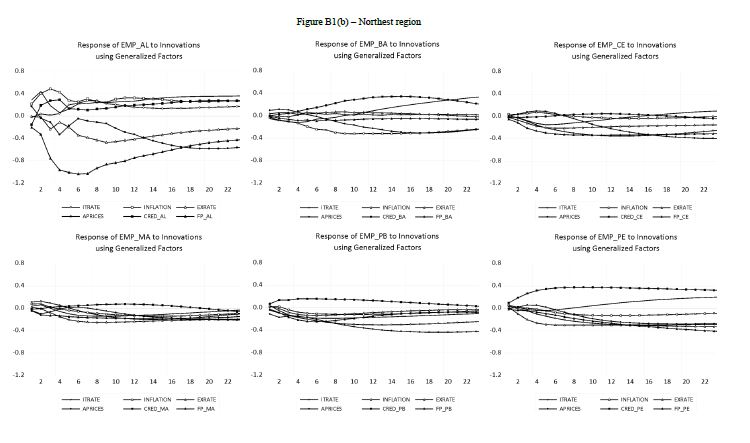

Appendix B. Generalized impulse response functions of Brazilian states

Figure B1

Generalized Impulse Response Functions of Brazilian States (GIRFs)

Notes

Author notes