RURAL MICROCREDIT AND GENDER: FEMALE PARTICIPATION IN THE AGROAMIGO PROGRAM

MICROCRÉDITO RURAL E GÊNERO: PARTICIPAÇÃO FEMININA NO PROGRAMA AGROAMIGO

Dayane da Costa Oliveira ladyane27488@gmail.com

Luiz Alves da Silva Cruz Neto cruz_luiz@uvanet.br

Ezequiel Alves Lobo ezequiel_alves@uvanet.br

Dayane da Costa Oliveira ladyane27488@gmail.com

Luiz Alves da Silva Cruz Neto cruz_luiz@uvanet.br

Ezequiel Alves Lobo ezequiel_alves@uvanet.br

RURAL MICROCREDIT AND GENDER: FEMALE PARTICIPATION IN THE AGROAMIGO PROGRAM

Revista Pensamento Contemporâneo em Administração, vol. 19, núm. 3, pp. 1-16, 2025

Universidade Federal Fluminense

Recepción: 15 Agosto 2025

Aprobación: 05 Octubre 2025

Abstract: This research analyzed differences between men and women in access to rural microcredit, considering age, education, income, amounts contracted, frequency of operations and defaults. Based on data from 903 Agroamigo borrowers, it was found that women access credit at a younger age, with more schooling, lower default rates and higher amounts, although they contract less frequently. In short, the role of microcredit, especially Agroamigo Woman, in empowering rural women is clear. We therefore conclude that microcredit policies with a gender focus mainly strengthen women's financial autonomy.

Keywords: Rural microcredit, Gender, Agroamigo, Family Farming, Financial inclusion.

Resumo: A presente pesquisa analisou diferenças entre homens e mulheres no acesso ao microcrédito rural, considerando idade, escolaridade, renda, valores contratados, frequência de operações e inadimplência. Com base em dados de 903 tomadores(as) do Agroamigo, verificou-se que mulheres acessam crédito mais jovens, com maior escolaridade, menor inadimplência e valores mais altos, embora contratem com menor frequência. Em síntese, fica evidente o papel do microcrédito, especialmente do Agroamigo Mulher, no empoderamento feminino rural. Diante disso, conclui-se que políticas de microcrédito com enfoque de gênero fortalecem principalmente a autonomia financeira feminina.

Palavras-chave: Microcrédito Rural, Gênero, Agroamigo, Agricultura Familiar, Inclusão Financeira.

Introduction

Family farming plays a fundamental role in Brazil's economy and food security (Kffuri et al., 2025). Among the various programs aimed at strengthening this modality, Agroamigo stands out, an initiative of the Banco do Nordeste (BNB, the development bank for Brazil's Northeast region) that seeks to promote sustainable development and the financial inclusion of small farmers (Banco do Nordeste, 2023a).

According to Banco do Nordeste's report Family Farming and the Agroamigo Program 2024, female participation in the countryside is growing every year. Currently, around half of family farms are run by women, who also produce a wide variety of non-agricultural goods, helping to increase family income and achieve financial independence. According to data from the program (Banco do Nordeste, 2024), approximately 48.8% of clients are women. In the livestock sector, for example, more than 353,677 operations were contracted, of which 51.42% were led by female farmers.

These results converge with the process of female empowerment, which, according to Amartya Sen (2000), is one of the central aspects in the development trajectory of various countries. The strengthening of women's autonomy is directly linked to factors such as increased schooling, improved property conditions, more job opportunities and a more inclusive labor market. According to Sen (2000), women have expanded their status as agents, in other words, they have acquired greater freedom to make decisions they consider relevant, in line with their objectives, aspirations and commitments.

Women's role as agents of transformation represents an important mediator of economic and social change, the effects of which are closely associated with the main characteristics of development. Studies such as that by Tahim, Lobo and Sousa (2025) confirm the expressive and articulate participation of women as promoters of development and protagonists of domestic economic activities, even in the rural context.

In this scenario, Fernandes (2013) investigates the obstacles to gender inclusion in rural credit policies; Sousa, Almeida and Leitão (2017) analyze access to credit by an association of craftswomen in the municipality of Baixa Verde-PE; Cunha Júnior et al. (2022) explore the relationship between microcredit and female empowerment in the Crediamigo program in Ceará, although they do not address Agroamigo; Vázquez and Carámbula (2025) examine the gender perspective in the Rural Microcredit Program (PMR) in Uruguay; and Martiningo Filho (2025) discusses risk in microcredit programs considering variables such as gender, age and schooling.

Despite these contributions, there is still a gap in rural microcredit, especially with regard to the differences between women and men farmers who access this resource. With this in mind, the aim of this study is to comparatively analyze rural microcredit (Agroamigo) among female and male farmers served by the Banco do Nordeste branch in São Benedito-CE, checking for significant differences depending on the gender of the borrower. To this end, it is proposed to: i) characterize the socio-economic and demographic profile of the beneficiaries, taking into account gender, age, education and income; ii) compare the amounts contracted, frequency of operations and default rates between genders, identifying possible patterns; and iii) evaluate the performance of women in the use of credit, especially in terms of amounts contracted and defaults, in order to strengthen their financial autonomy and management capacity.

Rural microcredit

Bank credit is a financial operation in which an institution grants a sum of money to an individual or company, with the obligation to repay this amount plus interest. It plays an important role in financial inclusion, enabling people and companies without access to large sums of money to carry out their projects and improve their quality of life. Consequently, it contributes to economic growth by stimulating consumption and investment (Silva, 2000).

Schumpeter (1997) pointed out that economic development is based on three factors: the innovative entrepreneur, technological innovations and bank credit. In the author's view, credit is the creation of purchasing power and is fundamental for development in a system of private property and division of labor. In this way, bank credit is an important source of funding for small businesses. Among the various lines of credit, microcredit stands out, understood as a set of financial services offered by institutions, aimed at the production and growth of entrepreneurs, with different advantages, such as lower interest rates, longer terms and no real guarantee (Greatti & Silva, 2020).

Microcredit is characterized by the granting of low-value loans to small informal entrepreneurs and micro-enterprises without access to the traditional financial system, mainly because they do not have real or formal guarantees to prove their income (Barone et al., 2002, p. 11). This type of credit is an essential tool for promoting social justice, offering, in addition to financing, business guidance, financial education, professional training, digital inclusion and sustainability of initiatives.

In Brazil, the first initiative to promote microcredit was the National Program for Oriented Productive Microcredit (PNMPO). This is a public policy aimed at encouraging the generation of work and income, supporting small entrepreneurs, young people and women heads of household, with the aim of improving living conditions and reducing social inequality. Created by Law No. 11.110/2005 and reformulated by Laws No. 13.636/2018 and No. 13.999/2020, the program is aimed at enterprises with revenues of up to R$ 360,000 per year. Microcredit, through the PNMPO, has opened up new business opportunities and fostered socioeconomic development and entrepreneurship, especially in disadvantaged areas.

According to Guedes et al. (2021), microcredit significantly improves the lives of families who use it for agricultural production. Rural microcredit, specifically, is aimed at small farmers and rural entrepreneurs, with the aim of providing resources to invest in their productive activities, improve living conditions and promote sustainable development in the countryside. It is offered by financial institutions, credit cooperatives and government programs, generally with more favorable interest rates and payment terms, with the aim of making it easier for small producers to access the necessary resources.

One of the main legal bases that regulates rural microcredit is the National Rural Credit System (SNCR), created by Law No. 4,595, of December 31, 1964, and by Law No. 4,829, of November 5, 1965, which institutionalized Rural Credit, previously carried out exclusively by Banco do Brasil. In order to adapt to the reality of national agriculture, important measures marked its trajectory, such as the increased participation of the BNDES in rural credit, through Finame Rural, the Joint Operations Program (POC) and the Direct Operations Program, as well as the creation of the National Program to Strengthen Family Farming (PRONAF), which will be discussed later.

According to the Central Bank of Brazil (2022), the sources of funds for rural credit can be classified into three groups, according to their origin: i) controlled resources, with rates set by the government, such as the Workers' Support Fund (FAT); ii) non-controlled resources, with free rates; and iii) funds and programs, which include the BNDES and the constitutional funds - the Constitutional Financing Fund for the Northeast (FNE), the Constitutional Financing Fund for the Midwest (FCO) and the Constitutional Financing Fund for the North (FNO).

The creation of the Constitutional Funds was aimed at providing stability to the sources of financing, guaranteeing sustainable investments. Banco do Nordeste do Brasil S.A. (BNB) played a crucial role in the creation of the FNE, forming a team at the Technical Office for Economic Studies of the Northeast (ETENE) in Brasilia to advise the Northeastern caucus from the start of the discussions (1989-1990) until the project was drawn up. Based on these studies, the FNE's initial programming was drawn up, consisting of 15 programs aimed at supporting innovation, productive diversification, water security, environmental conservation and human development (Banco do Nordeste, 2022).

According to its internal credit guidelines manual, the BNB provides microcredit and advice to micro-entrepreneurs who are not served by the traditional financial market, either because of the small size of their businesses or the lack of real guarantees.

The BNB operates two microcredit programs with funds from the FNE: the Urban Microfinance Program (CredAmigo) and the Rural Microfinance Program (Agroamigo). CredAmigo, launched in 1998, is considered the largest microcredit program in Latin America, aimed at low-income micro-entrepreneurs, ranging from formal and informal workers to micro and small businesses, with 986 service units, 292 bank branches and 468 CredAmigo service points (Banco do Nordeste, 2023b). Agroamigo, created in 2005, aims to improve the social and economic profile of family farmers, encouraging the development of productive agricultural and non-agricultural activities with an entrepreneurial character, and currently has 310 service units (Banco do Nordeste, 2023c).

BNB Agroamigo

Until the mid-1990s, financing for small producers was almost exclusively administered by the Special Credit Program for Agrarian Reform (PROCERA). This program had a specific and limited scope, as it only served beneficiaries of the Agrarian Reform (Castro, 2024).

In January 1994, the Food and Agriculture Organization of the United Nations (FAO) and the National Institute for Colonization and Agrarian Reform (INCRA) signed an agreement to carry out the UTF/BRA/036/BRA project, whose main objective was "to contribute to the elaboration of a new rural development strategy for Brazil" (FAO/INCRA, 1994, p. 1). Using data from the 1985 Agricultural Census of the Brazilian Institute of Geography and Statistics (IBGE), a socio-economic profile of Brazilian family farming was drawn up. According to Guanziroli et al. (2001), since then, family farmers have been characterized according to the social relations of production they develop, seeking to overcome the common practice in analyses on the subject of mistakenly associating family farming with small production, limiting it by area or production value.

In 1996, the federal government set up the National Program to Strengthen Family Farming (PRONAF), with the aim of providing credit lines for funding and investment for rural establishments classified as belonging to family farming. In its initial phase, the lack of differentiated criteria as to the income bracket of the beneficiaries for the granting of financing resulted in the concentration of resources among more structured rural producers with greater insertion in the market. In this way, PRONAF ended up reproducing the distribution pattern already observed in the National Rural Credit System, allocating most of the loans to the southern states of the country and making it difficult for farmers in situations of greater socio-economic vulnerability to access them (Maia & Pinto, 2015).

According to the report Family Farming and the Agroamigo Program (Agroamigo, 2023), Group B - made up of family farmers with a gross annual income of up to R$40, 000.00 and payment conditions suited to their profile - was included in PRONAF's financing lines in 1999, offering small amounts for investments in agricultural and non-agricultural activities in rural areas. Over time, it became clear that providing financial resources alone was not enough to improve the situation of family farmers. For this reason, the Federal Government developed various programs to support marketing, offer technical assistance, guarantee prices and provide agricultural insurance, promoting greater sustainability for the enterprises.

Agroamigo, created in 2005 by Banco do Nordeste, is one of these rural microcredit programs. It ensures the presence of a microcredit agent in rural communities, offering guided and monitored productive credit to family farmers, with the aim of improving their social and economic profile in the bank's area of operation. The program encourages the development of productive agricultural and non-agricultural activities of an entrepreneurial nature.

Between 2005 and 2023, the program served more than 370,397 clients in the state of Ceará, out of a total of 2,839,219 throughout Brazil, with contracted amounts of approximately R$ 702.5 million in Ceará, out of a national total of R$ 5.66 billion - second only to Bahia (Banco do Nordeste, 2023c). The Agroamigo unit at the São Benedito branch has 7,555 clients with active operations and a track record of more than R$ 224 million contracted by May 2025.

Women in Agriculture

The central role of command and decision-making on rural properties is still mostly exercised by men, and female autonomy is more frequent in productive activities that do not constitute the property's main source of income (Tahim; Lobo & Souza, 2025). Studies on the division of labor and management between men and women, especially in the context of family farming, show the invisibility of female participation in running farms (Carneiro, 2001; Brumer, 2004; Zorzi, 2008; Hernández, 2009). These analyses indicate that unequal roles are not the result of biological factors, but of social constructions that attribute male supremacy (Menasche & Belém, 1998; Spavanello et al., 2021).

The recognition of rural women workers, especially in the context of family farming, gained momentum with the mobilization of these workers themselves, organized in the Rural Women Workers Movement in the 1980s. This movement was responsible for important achievements, such as the right to rural retirement and maternity pay (Souza, 2017; Souza, 2021). Later, women were included as beneficiaries in the Agrarian Reform Program and, from the 2000s onwards, they were covered by the National Policy for Technical Assistance and Rural Extension (PNATER) and national rural credit policies, such as PRONAF.

According to Fernandes (2008, p. 20):

Credit is a way of giving economic autonomy and visibility to the activities carried out by women in and around the domestic space. Throughout history, these activities have remained on the margins of the productive system and the public sphere; they have been considered, from an economic point of view, unproductive. Having autonomy means exercising citizenship.

As a way of encouraging greater demand for credit by women, in 2001 the Federal Government launched an ordinance that established credit quotas for rural women within PRONAF, through which at least 30% of the resources in each Safra Plan would be earmarked for women (Brasil, 2001). Melo (2003) points out that despite this, women farmers did not demand these lines of credit because they did not know about them.

According to Fernandes (2008), in the 2003 Safra Plan, the government launched a specific credit line for women, called PRONAF woman, to remedy this issue and allow them to invest in the activity they wanted. As a result, credit is seen as an important ally in reducing the differences between men and women when it comes to managing and working on family farms (Zorzi, 2008; Hernandéz, 2009; Fernandes, 2008).

Agroamigo has some business strategies aimed at diversifying rural activities, classified as "Agroamigo Getting Better and Better", such as Agroamigo Woman, whose strategy is to prioritize assistance to women family farmers, with the aim of contributing to improving family income, women's financial autonomy and gender equity in rural areas (Banco do Nordeste, 2024).

Methodology

The methodology was structured in three main stages: characterization of the beneficiaries' socio-demographic and operational profile; statistical comparison between men and women in variables such as age, schooling, income, amounts contracted, frequency of operations and defaults; and inferential analysis to identify significant differences between the genders. Statistical tests such as the Student's t-test for continuous variables and the chi-square test of independence for categorical variables were used to ensure that the comparisons were robust.

Type of research

The research is characterized as a study with a quantitative approach and of a descriptive and gender comparative nature (Grant & Booth, 2009). According to Alford and Teater (2025), descriptive quantitative research consists of empirical research investigations whose main purpose is the delineation or analysis of the characteristics of facts or phenomena, the evaluation of programs, or the isolation of main or key variables.

Data Source and Variables

The research was carried out using secondary data made available by the Banco do Nordeste São Benedito branch. The database was made up of a sample of 903 borrowers from the Agroamigo program, collected in May 2025 from clients with active registrations from 2004 to 2025, who have operations in force at the time of data collection, containing socio-demographic information on the borrowers, such as gender, level of education, age group and income, and variables that characterize the operations, such as the amount lent, recurrence and default.

Data analysis

Data analysis was conducted using descriptive and inferential statistical techniques to examine the profile of Agroamigo Program beneficiaries and assess possible differences between genders. Initially, a descriptive analysis of the sample was carried out to characterize continuous variables such as age, income, number of operations, amount contracted, amount in arrears and number of days in arrears. Subsequently, the Student's t-test was used to compare continuous variables. The Chi-Square test of independence was used for categorical variables. The assumptions of normality and homogeneity of variance were analyzed.

The data was analyzed using Microsoft Excel software, version 2019, which was used to tabulate and organize the data from the financial transaction records, calculate descriptive statistics such as mean, median, mode, standard deviation and variance, allowing for an initial characterization of the sample, construct graphs and tables to visualize the patterns and trends observed, and apply statistical tests such as Student's t-test for continuous variables and the Chi-square test of independence for categorical variables, using formulas and statistical supplements available on the platform. All ethical procedures were followed, guaranteeing the anonymity and confidentiality of the participants, since the intention of the research is not to identify the client, but to collect information on the profile of farmers who benefit from the Agroamigo program.

Results

Description of the sample

Table 1 shows the characteristics of the sample. Of the total number of holders, 49% were female and 51% male. The average age was 45.3 years, ranging from 19 to 88 years. As for level of education, 3% were illiterate, 8% literate, 38% had completed elementary school, 30% had incomplete elementary school, 12% had completed secondary school and 8% had incomplete secondary school, and only 1% of the sample had a degree. On average there were 5 loans per person, with a minimum of 1 and a maximum of 21, between 2004 and May 2025. The average amount taken out was R$8,786.30, with a minimum of R$117.32 and a maximum of R$30,000.00. As for the amount in arrears, the average is R$48.98, with a maximum of R$5,101.85. Finally, on average there are 23.8 days in arrears with a maximum of 3,380 days.

| Variable | N | Percentage | ||

| Gender | ||||

| Female | 439 | 49% | ||

| Male | 464 | 51% | ||

| Level of education | ||||

| Illiterate | 28 | 3% | ||

| Literate | 72 | 8% | ||

| Complete elementary school | 345 | 38% | ||

| Incomplete elementary school | 270 | 30% | ||

| High school completed | 112 | 12% | ||

| Incomplete high school | 70 | 8% | ||

| Graduated | 6 | 1% | ||

| Variable | Mean | Min. | Max. | |

| Age | 45,3 | 19 | 88 | |

| Income | R$ 1.570,93 | R$ 0,00 | R$ 8.150,42 | |

| Frequency of operation | 5 | 1 | 21 | |

| Contract value | R$ 8.786,30 | R$ 117,32 | R$ 30.000,00 | |

| Amount in arrears | R$ 48,98 | R$ 0,00 | R$ 5.101,85 | |

| Days in arrears | 23,8 | 0 | 3380 | |

| Source: Prepared by the authors (2025) |

Comparison between genders

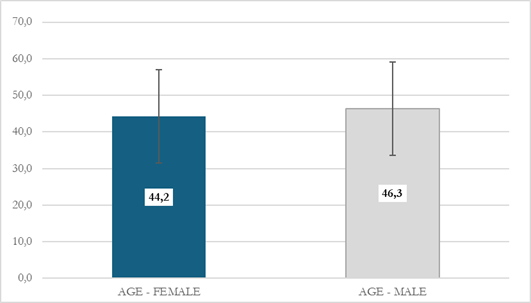

In order to see if there is a difference in the average age between men and women who obtain credit from Agroamigo, a T-test was carried out between the gender groups, as shown in Figure 1. The results obtained through the T-test showed different averages, statistically male borrowers have a higher average age (M = 46.3; SD = 12.71) than female borrowers (M = 44.2; SD = 12.57) (t (901) = -2.491, p = 0.012).

Figure 1 -

Average age of male and female borrowers of the Agroamigo program of the Agroamigo Program

Prepared by the authors (2025)

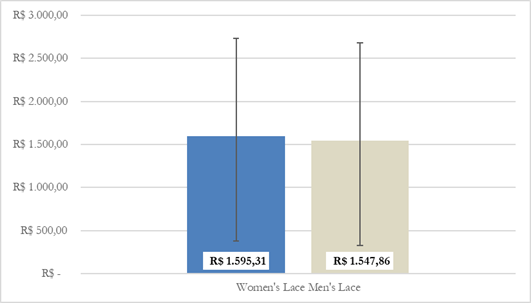

Similarly, an analysis was made of the income of borrowers segmented by gender, as shown in Figure 2. It was found that there is no significant difference between the average income of the genders, as shown by the t-test, statistically male borrowers have (M = R$1,547.86; SD = R$1,220.10) while female borrowers have (M = R$1,595.31; SD = R$1,133.25) (t (901) = 0.604, p = 0.545).

Figure 2 -

Average income among male and female borrowers of the Agroamigo Program

Prepared by the authors (2025)

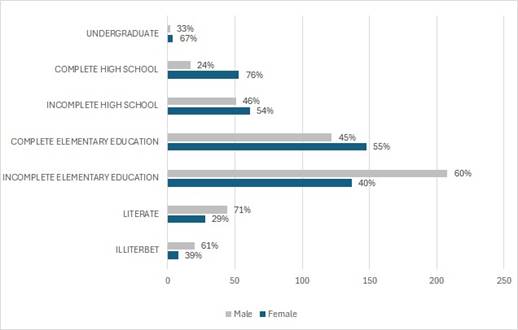

In order to identify whether there is a difference in educational level between male and female borrowers, a chi-square test of independence was carried out (2x2). A significant association was found between educational level and gender (2(6) = 45.23, p < 0.001). Figure 3 shows a higher proportion of women with complete higher education, complete secondary education and complete primary education, showing that women are more likely to have higher levels of education than men.

Figure 3 -

Proportion of borrowers' educational level by gender (male and female) in the Agroamigo Program

Prepared by the authors (2025)

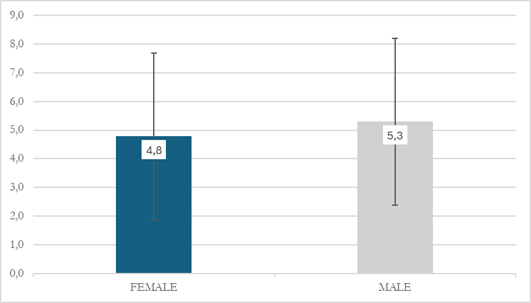

Figure 4 shows the results of the analysis carried out to see if there are differences in the number of contracts between the genders. With regard to the number of credit operations, the result shows that the average number of contracts differs significantly between genders, statistically (t (895) = -2.453, p = 0.014). Male borrowers hire more often (M = 5.3; SD = 3.329) than females (M =4.8; SD =2.904).

Figure 4-

Average number of contracts between male and female borrowers of the Agroamigo Program

Prepared by the authors (2025)

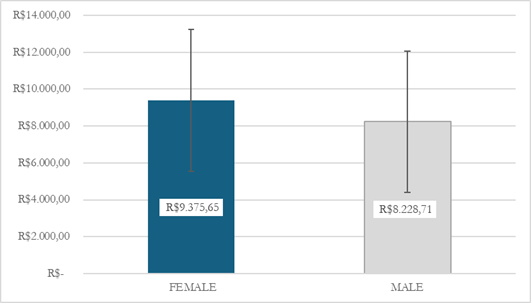

The average amount contracted between the genders was also analyzed, as shown in Figure 5. The average contract value is significantly different between men and women (t (883) = 4.255, p =2.310), the average contract value for men (M= R$8,228.71; SD= R$3,842.42) is significantly lower than for women (M= R$9,375.65; SD= R$4,214.69). Thus, women obtain a larger amount of credit compared to men.

Figure 5-

Average amount contracted between male and female beneficiaries of the Agroamigo Program

Prepared by the authors (2025)

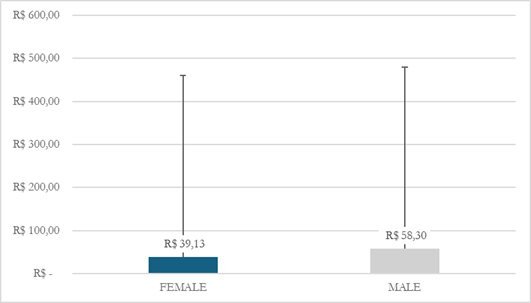

The average amount in arrears between men and women was statistically compared, as shown in Figure 6. The result was that there was no significant difference between the average value of arrears between men and women (t (901) = -0.758, p = 0.448). The average amount in arrears for men was R$58.30 (SD= R$421.61) and for women it was R$39.13 (SD= R$328.73).

Figure 6-

Average amount in arrears by gender, male and female, in the Agroamigo Program.

Prepared by the authors (2025)

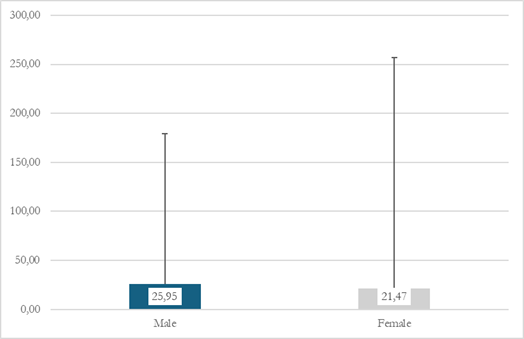

Finally, the number of days in arrears was compared between genders, as shown in Figure 7. The results showed that males have a slightly higher average number of days in arrears (M = 26.0; SD = 153.29) than females (M = 21.5; SD = 235.47). However, the difference was not statistically significant (t (901) = -0.340, p = 0.733).

Figure 7 -

Average number of days in arrears by gender, male and female, among Agroamigo Program borrowers

Prepared by the authors (2025)

Discussion

The research analyzed data from the Agroamigo program, highlighting significant differences in credit access profiles between male and female farmers. A relevant finding is that women, on average, access credit at younger ages (44 years) compared to men (46 years), which indicates a growing female protagonism among new generations in agriculture. This aspect is notable, as emphasized by Spavanello et al. (2021), who point out that until 2010, women’s participation in Brazilian rural areas was composed predominantly of older women, according to IBGE data.

The fact that women seek credit at younger ages than men suggests a certain level of independence from them, evidencing their active role in productive and economic activities that ensure household sustenance. Nevertheless, the effort and work of these women often remain invisible, as highlighted by Tahim, Lobo, and Sousa (2025).

The results also showed that women present higher educational levels (Figure 3), a factor that may contribute to more efficient resource management and more assertive productive decisions. Higher education tends to broaden the capacity for planning and organizing productive activities, favoring access to higher credit amounts and lower default rates, while also fostering financial autonomy and earlier productive inclusion. In this perspective, Sen (2000) argues that the strengthening of women’s empowerment is directly related to the level of education. Despite this, Melo (2003) observed that, initially, many female farmers did not demand specific credit lines, such as PRONAF Mulher, due to lack of knowledge. This scenario, however, has been changing over the past two decades, partly thanks to Agroamigo Mulher, created to position women as protagonists in credit access, minimizing barriers pointed out by Fernandes (2013).

In this sense, the study by Tahim, Lobo, and Sousa (2025) identified that women working in agriculture have been increasing their level of education, considering that, in the past, rural activities occupied most of their time. Furthermore, there is evidence of a cultural factor that historically attributed greater importance to work over education. However, the sample analyzed in this study demonstrates that women have advanced significantly in this regard, even reaching higher education and showing greater educational representativeness.

The research data indicate that women contract, on average, higher credit amounts (R$ 9,375.65) than men (R$ 8,228.71), although they carry out fewer operations (4.8 vs. 5.3). This evolution is significant, considering that the Agroamigo Mulher line was implemented only in 2013, after the program was created. Still, female performance is superior, with an average default of R$ 39.13, compared to R$ 58.30 among men, suggesting greater robustness and better structuring of projects led by women, as well as greater commitment to financial return. These results indicate that the objectives advocated by Fernandes (2008) for credit aimed at women are being achieved by Agroamigo, contributing to reducing inequalities in management and work in family farms, as also observed in other programs.

The literature supports these findings. Cunha Júnior et al. (2022), when studying the Crediamigo program in Ceará, aimed at industry, trade, and service entrepreneurs, found that, even starting from less favorable initial conditions, female borrowers presented proportionally greater impacts than men, with an average increase of 31.1% in Operating Profit, 9.4% in Non-Operating Revenues, and 34.5% in Payment Capacity.

More specifically, Guedes et al. (2021), in a broad study, investigated the effect of rural microcredit on the agricultural production value of northeastern municipalities served by the Agroamigo Program, considering 1,791 municipalities between 2003 and 2015. It was found that 43% of operations carried out over 12 years were destined for women, which demonstrates the achievement of one of the program’s central objectives: to promote women’s productive inclusion.

Along the same lines, Martiningo Filho (2025) analyzed credit risk in a major regional Brazilian bank, a leader in microcredit. The study considered a random sample of 10,000 operations conducted in 2022 and revealed relevant data: 65% of borrowers were women, and the variables age, marital status, and gender significantly differentiated groups of defaulters and non-defaulters. Moreover, significant differences were observed in the average number of compliant male and female borrowers, indicating that women perform better in repayment. Although there was no robust statistical confirmation regarding significance, the results pointed to important indications, such as a lower average overdue amount among women and a higher number of overdue days among men.

However, in the international context, this female protagonism in credit access is not always predominant. As shown in the systematic review by Nascimento, Marques, and Rego (2023), in territories where serious socioeconomic problems and cultural gender barriers persist, microcredit often does not constitute an effective tool for the development of female entrepreneurship, falling short of expectations in terms of contracting, poverty reduction, and women’s autonomy.

In the Latin American context, Vázquez and Carámbula (2025) analyzed, from a gender perspective, a rural microcredit program in Uruguay, similar to Agroamigo in Brazil, concluding that men still remain the main beneficiaries of productive microcredit initiatives.

In Brazil, however, progress has been observed in this regard, as evidenced by the findings of this study and other research, such as Fernandes (2008, 2013), Guedes et al. (2021), Cunha Júnior et al. (2022), Martiningo Filho (2025), and the studies by Tahim, Lobo, and Sousa (2025), which, although not directly focused on microcredit, point to greater organization and participation of women in the rural productive context.

In summary, rural microcredit plays a central role by highlighting the protagonism of credit policies in promoting women’s autonomy and economic visibility (Fernandes, 2008). Moreover, it contributes to increased confidence, as well as the expansion of communication and relationships between women and other social actors, as emphasized by Spanevello et al. (2021).

Final considerations

The present study analyzed the profile of male and female beneficiaries of the Agroamigo Program in the municipality of São Benedito-CE, between 2004 and 2025, highlighting differences in access and behavior regarding the use of productive rural credit. The results showed that women access credit at younger ages, present higher educational levels, contract higher amounts, and register lower average default rates compared to men. Such evidence points to a growing female protagonism in rural areas, marked by greater financial autonomy, productive organization, and management capacity.

These findings corroborate the literature that identifies microcredit as an instrument of productive inclusion and gender inequality reduction (Fernandes, 2008; Guedes et al., 2021; Cunha Júnior et al., 2022). At the same time, they reinforce the importance of specific policies, such as Agroamigo Mulher, in overcoming the historical barriers to credit access faced by female farmers (Melo, 2003; Fernandes, 2013).

However, the study also revealed that women still carry out, on average, fewer credit operations than men, which may indicate specific challenges in maintaining continuity of contracting. This result suggests that, although advances are visible, cultural and structural factors may still persist, limiting the full female protagonism in rural areas in some regions. This aligns with the international literature that points to persistent inequalities (Nascimento; Marques; Rego, 2023; Vázquez; Carámbula, 2025).

Thus, it can be concluded that Agroamigo has played a relevant role in promoting the autonomy of rural women, strengthening their productive inclusion, and contributing to greater economic visibility of women’s work. Nevertheless, to expand positive impacts, it is recommended to strengthen other credit lines specifically aimed at female farmers, combined with technical training and incentives for women’s permanence in productive management processes, in order to promote greater integration.

From an academic perspective, this study contributes by evidencing, through a solid empirical basis, gender differences in access to rural microcredit and by seeking to associate these differences with other relevant aspects. As a limitation, it is worth noting the exclusive use of secondary data, which prevented a deeper analysis of the subjective factors influencing women’s decision-making.

Future studies may include interviews and qualitative analyses to complement the findings, as well as expand the scope of investigation to other cities or even states in Brazil, depending on data availability. In addition, further research may deepen comparative analysis across different territories and longitudinally assess the impacts of credit on income, autonomy, and well-being of female farmers.

References

Alford, S., & Teater, B. (2025). Quantitative research. In M. Alston, P. Buykx, W. Foote, & D. Betts (Eds.), Handbook of Research Methods in Social Work (pp. 156–171). Edward Elgar Publishing. https://doi.org/10.4337/9781035310173.00023

Agroamigo. (2023). Relatório: Agricultura familiar e programa agroamigo 2023. https://www.bnb.gov.br/documents/45735/6192659/Relat%C3%B3rio+da+Agricultura+Familiar+e+do+Agroamigo+-+2023.pdf/ed388911-ce27-15f5-0421-158387c10a95?version=2.0&t=1715710804082.

Banco do Nordeste do Brasil. (2022). 70 anos de contribuição para o desenvolvimento regional. A. S. Valente Junior, M. O. Alves, & C. R. C. dos Santos (Orgs.). https://www.bnb.gov.br/s482-dspace/handle/123456789/1255

Banco do Nordeste do Brasil. (2023a). CrediAmigo 25 anos: a trajetória do programa de microcrédito urbano do Banco do Nordeste. M. C. G. F. de Sousa, M. R. B. Melo, J. M. da Cunha Júnior, et al. (Orgs.). https://www.bnb.gov.br/crediamigo

Banco do Nordeste do Brasil. (2023b). Relatório 2023: programas de microfinanças do Banco do Nordeste. https://www.bnb.gov.br/agroamigo/relatorios-e-resultados

Banco do Nordeste do Brasil. (2023c). Relatório anual de crédito rural 2023. https://www.bnb.gov.br/relatorios-credito-rural

Banco do Nordeste do Brasil. (2024). Agricultura Familiar e Programa Agroamigo: relatório 2024. https://www.bnb.gov.br/agroamigo/relatorios-e-resultados

Barone, F. M., L., Dantas, V. P. F., & Rezende, V. (2002). Introdução ao microcrédito. Conselho da Comunidade Solidária. https://www.bcb.gov.br/content/publicacoes/outras_pub_alfa/microcredito.pdf

Brumer, A. (2004). Gênero e agricultura: a situação da mulher na agricultura do Rio Grande do Sul. Revista Estudos Feministas, 12(1), 205–227.

Carneiro, M. J. (2001). Herança e gênero entre agricultores familiares. Revista Estudos Feministas, 9(2), 22–55.

Castro, C. N. (2024). Agricultura familiar no Brasil, na América Latina e no Caribe: institucionalidade, características e desafios. In Agricultura familiar no Brasil, na América Latina e no Caribe (Cap. 4). Instituto de Pesquisa Econômica Aplicada (Ipea). http://dx.doi.org/10.38116/978-65-5635-074-5/capitulo4

Cunha Júnior, J. M. A., et al. (2022, maio). Microcrédito e empoderamento feminino: o caso do crediamigo no Ceará. Artigos ETENE, 3(1).

Food and Agriculture Organization of the United Nations. (1994). *Projeto UTF/BRA/036/BRA: estratégia de desenvolvimento rural para o Brasil*. FAO/INCRA.

Fernandes, S. A. (2008). Gênero e políticas de crédito: o Pronaf-Mulher em Santa Catarina [Dissertação de mestrado, Universidade Federal de Santa Catarina]. Repositório Institucional da UFSC.

Fernandes, S. A. (2013). Entraves para inclusão de gênero nas políticas de crédito no meio rural. Revista Grifos, 22(34/35), 157–175.

Grant, M. J., & Booth, A. (2009). A typology of reviews: an analysis of 14 review types and associated methodologies. Health Information & Libraries Journal, 26(2), 91–108. https://doi.org/10.1111/j.1471-1842.2009.00848.x

Greatti, L., & Silva, A. C. (2020). As inovações do microcrédito e sua importância para o microempreendedorismo. Revista de Empreendedorismo e Inovação Sustentáveis, 5(1), 65–84.

Guedes, I. A., et al. (2021). Efeitos do microcrédito rural sobre a produção agropecuária na região Nordeste. Revista de Economia e Sociologia Rural, 59(1), e210774. https://doi.org/10.1590/1806-9479.2021.210774

Guanziroli, C. E., Romeiro, A., Buainain, A. M., Di Sabbato, A., & Bittencourt, G. (2001). Agricultura familiar e reforma agrária no século XXI. Editora Garamond.

Hernández, C. O. (2009). Política de crédito rural com perspectiva de gênero: um meio de "empoderamento" para as mulheres rurais? [Tese de doutorado, Universidade Federal do Rio Grande do Sul]. Lume Repositório Digital UFRGS.

Kffuri, C., et al. (2025). New family farmers in Bahia, Brazil: analysis of the key factors influencing crop choice. *Ethnoscientia-Brazilian Journal of Ethnobiology and Ethnoecology, 10*(1), 44–66. http://dx.doi.org/10.18542/ethnoscientia.v10i1.13995

Maia, G. B. D. S., & Pinto, A. de R. (2015). Agroamigo: uma análise de sua importância no desempenho do Pronaf B. Revista Econômica do Nordeste, 46(Suplemento Especial), 9–20.

Martiningo Filho, A. (2025). Risco de crédito em programas de microcrédito: o papel das variáveis de gênero, idade e escolaridade. Redeca, Revista Eletrônica do Departamento de Ciências Contábeis, 12, e70181.

Melo, L. (2003). Relações de gênero na agricultura familiar: o caso do Pronaf em Afogados da Ingazeira - PE [Tese de doutorado, Universidade Federal de Pernambuco]. Repositório Digital UFPE.

Menasche, R., & Belém, R. C. (1998). Gênero e agricultura familiar: trabalho e vida na produção de leite do sul do Brasil. Raízes, 17(17), 135–142.

Movimento de Mulheres Trabalhadoras Rurais. (2020). Memórias da luta: 40 anos de conquistas.

Ministério do Desenvolvimento Agrário. (2001, 15 de junho). Portaria nº 196, de 14 de junho de 2001. Estabelece cotas de crédito para mulheres rurais no âmbito do PRONAF. Diário Oficial da União, Seção 1, p. 3. https://www.in.gov.br/.

Nascimento, M., Marques, C., & Rego, C. (2023). Microcrédito e empreendedorismo feminino: experiências em diferentes contextos socioterritoriais. Revista de Gestão e Secretariado, 14(7), 11457-11482.

Sant'anna, A. A., Borça Júnior, G. R., & Araújo, P. Q. (2009). Mercado de crédito no Brasil: evolução recente e o papel do BNDES (2004-2008). Revista do BNDES, 16(31), 41–59.

Schumpeter, J. A. (1997). Teoria do desenvolvimento econômico: uma investigação sobre lucros, capital, crédito, juro e o ciclo econômico (M. S. Possas, Trad.). Nova Cultural. (Trabalho original publicado em 1911).

Spanevello, R. M., Fagundes, C. C., Matte, A., & Boscardin, M. (2021). Contribuições do acesso ao crédito rural: uma análise entre mulheres no norte do Rio Grande do Sul. Revista Grifos, 30(51), 212-235.

Sen, A. K. (2000). Desenvolvimento como liberdade (L. T. Motta, Trad.). Companhia das Letras.

Silva, J. P. (2000). Gestão e análise de risco de crédito (3a ed.). Atlas.

Sousa, G. M. B., Almeida, M. G. A. A., & Leitão, M. R. F. A. (2017). Gênero e acesso ao crédito rural na Associação Municipal Mulher Flor do Campo em Pernambuco. Extensão Rural, 24(4), 31–47.

Souza, M. J. (2018). Lutas e conquistas das mulheres rurais no Brasil (2a ed.). Expressão Popular.

Souza, M. P., & Oliveira, J. R. (2021). Microcrédito como instrumento de inclusão financeira. Revista de Economia Contemporânea, 15(2), 45–67.

Tahim, E. F., Lobo, E. A., & Sousa, F. I. (2025). Atuação das mulheres no Arranjo Produtivo Local de Pingo D’Água-Ceará. Revista Econômica do Nordeste, 56(1), 140–159.

Vázquez, L., & Carámbula, M. (2025). Paridad en el acceso, desigual en el uso. Análisis desde una perspectiva de género del Programa de Microcrédito Rural (PMR) en Uruguay. Cuadernos de Economía Crítica, 11(21), 13–37.

Zorzi, A. (2008). Uma análise crítica da noção de empoderamento com base no acesso das agricultoras ao Pronaf-Mulher em Ijuí-RS [Dissertação de mestrado, Universidade Federal do Rio Grande do Sul]. Lume Repositório Digital UFRGS.

Información adicional

redalyc-journal-id: 4417