Artigos

Esta obra está bajo una Licencia Creative Commons Atribución 4.0 Internacional.

Recepción: 09 Abril 2023

Revisado: 31 Mayo 2023

Aprobación: 21 Agosto 2023

Publicación: 31 Agosto 2023

DOI: https://doi.org/10.16930/2237-7662202333851

Abstract: Implicit taxes reduce the pre-tax return rate due to investment tax preferences, contrasting with direct, explicit taxes paid to the government. This paper explores implicit taxes in Brazilian publicly traded firms within the differentiated Corporate Governance segments of [B]3 from 2011 to 2021. Using a focused methodology that tests two hypotheses, the study demonstrates that firms in these segments bear a higher implicit tax burden and have their explicit tax benefits supplanted by implicit ones. Results specifically reveal that companies in differentiated segments experience lower pre-tax investment returns than others, pointing to weakened tax management levels. This concise analysis underscores the complex relationship between implicit and explicit taxes and corporate governance practices, necessitating further research for comprehensive understanding.

Keywords: Corporate governance, Implicit taxes, Explicit taxes, Taxation.

1 INTRODUCTION

Due to the separation of ownership and management in companies, agency problems have arisen, leading to the emergence of good corporate governance practices. While the literature on corporate governance has focused on the correlation between such practices and enhanced company performance (Armstrong et al., 2015; Gomes, 2016; Silva et al., 2019; Pereira et al., 2021; Ribeiro & Souza, 2023; Tarighi et al, 2023), there's a notable gap concerning the relationship between corporate governance and implicit taxes.

Many studies, like Kovermann and Velte (2019), explore aspects of corporate governance such as management compensation, board composition, ownership structure, and auditing in relation to explicit taxes. However, the impact of implicit taxes remains largely unexamined. This paper seeks to fill this gap in the tax-accounting literature by investigating the existence of implicit taxes in publicly traded Brazilian companies, considering the moderating effects of corporate governance segments introduced by Brasil Bolsa Balcão - [B]³. The understanding of implicit taxes is vital as they contribute to a company's total tax burden, formed by both implicit and explicit taxes. Research must therefore integrate implicit taxes into analyses to avoid biased conclusions (Scholes et al., 2009). These taxes are conceptualized as lower pre-tax rates of return on investments that are tax-favored, calculated by comparing pre-tax rates of return on differently taxed assets (Scholes et al., 2009).

This study's practical contribution lies in analyzing the relationship between implicit taxes and corporate governance, focusing on the moderating effect that corporate governance has on implicit taxes. Such an analysis contributes socially by promoting more responsible tax practices and governance structures, thus enhancing corporate accountability. From an academic standpoint, this research fills an existing gap in both national and international literature, providing new insights into a relatively unexplored area.

Tests conducted using accounting data analyzed through quantile regression present evidence that companies in the differentiated Corporate Governance segments of [B]3 endure higher implicit taxes, with these taxes effectively neutralizing benefits from tax incentives. These findings have practical implications for corporate tax strategy and add novel dimensions to the field of tax-accounting literature.

The absence of evidence from studies examining the effect of implicit rates in the Brazilian capital market underscores the necessity of this research. While the lack of empirical evidence alone does not inherently necessitate new research, the investigation into the effect of governance on the relationship between ETR (GAAPETR) and the implicit rate (PTROE and ROE) holds profound significance. It is essential to recognize that implicit taxes play a significant role in financial decisions, investment behavior, and overall market dynamics (Da Silva, (2020).

The implications of this research extend beyond academia, offering valuable insights to policymakers, regulators, and corporate leaders in shaping tax policies, optimizing investment strategies, and strengthening governance practices. Understanding how governance influences the interaction between GAAPETR and implicit rates could lead to more efficient capital allocation, improved risk management, and heightened transparency in financial reporting. Therefore, this exploration is not merely a theoretical endeavor but has potential real-world applications that could foster more responsible and effective corporate governance and financial management in Brazil's evolving economic landscape.

This paper is structured into six parts: Following this introduction, the second part details the theoretical framework and hypothesis, the third part describes the sample selection and research design, the fourth part discusses the statistics, multivariate analysis, and results, the fifth part offers the conclusions, and the final part lists the references.

2 THEORETICAL FRAMEWORK AND HYPOTHESIS

2.1 Corporate Governance, Tax Avoidance, Implicit Taxes and Investment Returns

Rogers et al. (2008) comment that in the literature involving corporate governance, one of the hypotheses raised about the benefits of good corporate governance practices is that, by adopting them, companies have their cost of capital reduced and, consequently, their returns on investment are increased. Furthermore, the authors clarify that in Brazil, one of the primary efforts to create a healthy business environment through good corporate governance practices was undertaken by Bovespa in 2000, with the promotion of the Novo Mercado and the Special Corporate Governance Levels (Level 1 and Level 2). Based on these premises, Rogers et al. (2008) developed work to analyze whether companies trade shares in the Novo Mercado and Levels 1 and 2 of corporate governance have lower cost of capital and higher return on investment than companies in other segments.

The evidence indicated that companies in the differentiated segments (Novo Mercado, Level 1, and Level 2) have lower capital and return on investment costs than those in the other segments. For companies in the differentiated segments and those in the different segments, the cost of capital is higher than the return on investment, evidencing value destruction in both segments. However, value destruction is proportionally more remarkable in the companies of the other segments than those of differentiated segments (Rogers et al., 2008).

With the adoption of an alternative view on agency theory, Armstrong et al. (2015) state that tax avoidance is one of many risky investment opportunities available to management and that, similar to other investment decisions, unresolved agency problems can lead managers to select a different level of tax avoidance than shareholders would prefer, i.e., as with other agency problems, the various corporate governance mechanisms in place can mitigate agency problems concerning tax avoidance.

There are potential net positive benefits (e.g., cash savings) from engaging in tax avoidance up to some firm-specific optimum level. However, beyond this optimal point, the marginal cost of additional tax avoidance may exceed the marginal cost benefits. For example, suppose shareholders and managers have different tax avoidance preferences. In that case, governance mechanisms can influence managers' tax avoidance decisions to prevent or mitigate excessive and insufficient investment in tax avoidance (Armstrong et al., 2015).

In conducting their research, Armstrong et al. (2015) focused on the corporate governance mechanisms that they believed would be most closely related to tax decisions, i.e., they focused on financial sophistication and board independence, as more financially sophisticated boards would be more able to monitor their companies' tax positions. The authors argue that independent directors may not have sufficient firm-specific knowledge to affect the firm's tax policy. Still, they can draw on outside experience with the tax positions of other firms and therefore be more likely to influence tax planning activities. Independent advisors should recognize potential costs associated with extreme tax positions and attempt to mitigate extreme tax avoidance (Martinez, 2017).

The tests were performed using quantile regression since quantile regression allows the researcher to obtain evidence of the relationship between the independent variables and any specified quantile of the conditional distribution of the dependent variable of interest, which does not occur with ordinary least squares (OLS), which allows the researcher to obtain evidence only of the relationship between the independent variables and the conditional mean of the dependent variable of interest. Thus, it was conjectured that any relationship between tax avoidance and corporate governance (more financially savvy and more independent boards) would be most intense at the extreme points of tax avoidance (Armstrong et al., 2015).

Supported by these assumptions, we looked for evidence of a positive (negative) relationship between board sophistication and financial independence and tax avoidance at the left (right) end of the tax avoidance distribution. It also examined how two crucial corporate governance mechanisms (financial expertise and board independence) relate to tax avoidance. Financial expertise was intended to measure knowledge of the costs and benefits of tax avoidance, and board independence was designed to measure the ability and incentive of the board to monitor management's tax avoidance decisions. The results showed evidence that board sophistication and financial freedom show a positive (negative) relationship with tax avoidance at the left (right) end of the tax avoidance distribution, thus being consistent with the hypothesis that more sophisticated and more financially independent boards mitigate agency problems related to relatively extreme levels of tax aggressiveness (Agyei-Mensah, 2021). On the other hand, evidence was obtained that financial expertise and board independence have a positive relationship with tax avoidance for low levels of tax avoidance, which is consistent with underinvestment in tax avoidance in the absence of monitoring. There was also evidence that financial expertise and board independence have a negative relationship with tax avoidance for high levels of tax avoidance, which is also consistent with overinvestment in tax avoidance without monitoring (Armstrong et al., 2015).

To verify which tools are used by corporate governance to increase the performance of companies, Gomes (2016) developed research to examine whether companies seek to improve their performance by reducing the tax expenses levied on the profit since knowing how corporate governance will make decisions to mitigate the risks of tax management, and how it will contribute so that the benefits of tax management occur, will bring the understanding to shape corporate governance practices so that the company can achieve the main objective of shareholders (the increase in the market value of the company).

Gomes (2016) clarifies that the composition of the Board of Directors, the independence of its members, the segregation between the chairman and the chief executive officer, and the appropriate design of executive management compensation contracts are corporate governance features that can: (i) influence the increase of corporate performance by reducing tax expenses, (ii) avoid agency problems in situations where tax management enables managerial opportunism, and (iii) avoid the uncertainty of the benefits of tax management by minimizing the application of resources in risky tax management.

Based on the literature consulted, Gomes (2016) understood that it is possible that independent directors can provide helpful knowledge to the chief executive officer and the other executive directors to advise them to focus their efforts on tax management as a way to increase the overall performance of companies. With this, the author tested six hypotheses, highlighting the hypothesis that seeks to obtain evidence that companies in the differentiated corporate governance levels of [B]. (Level 1, Level 2, and Novo Mercado) are the ones with the best tax management. In conclusion, it was observed that companies in the differentiated levels of corporate governance presented worse tax management for ETR and better control for BTD (Gomes, 2016).

Silva et al. (2019) conducted research aimed at investigating the moderating role of corporate governance quality in the investment-cash flow sensitivity of Brazilian companies listed on [B]., assuming that, in theory, companies with better corporate governance quality offer more robust protection to their investors, since good governance practices allow them to minimize the impacts of financial constraints. Furthermore, the researchers assume that these firms, in principle, have low or no investment cash flow sensitivity. On the other hand, firms with poorer corporate governance quality tend to have a higher potential for financial constraint, consequently increasing their investment-cash flow sensitivity. Thus, the hypothesis raised in the study was to investigate whether positive and significant investment cash flow sensitivity would be associated with worse corporate governance practices.

The findings revealed that firms with the worst corporate governance qualities have negative sensitivity of investment to cash flow; that is, they seek to increase their cash reserves when their cash flows increase since they are more financially constrained and present, as an effect, higher liquidity risk. In conclusion, it was emphasized that the adoption of better corporate governance practices could benefit firms by, on the one hand, decreasing financial constraints and increasing access to external sources of funding and, on the other hand, combating the entrenched behavior of managers/controlling shareholders through better internal controls, more transparency in information disclosure, and more effective monitoring on insiders(Silva et al., 2019).

Kovermann and Velte (2019), in an extensive systematic review of recent literature aimed at synthesizing research on the impact of corporate governance on tax avoidance, clarify that this literature shows that corporate governance is understood as the alignment between the interests of shareholders and managers, which makes it an essential factor in understanding corporate tax avoidance. Their analysis indicated that seven groups of corporate governance aspects primarily drive corporate tax avoidance: (1) incentive alignment between management and shareholders, (2) board composition, (3) ownership structure, (4) capital market pressure, (5) auditing, (6) enforcement and government relations, and (7) pressure from other stakeholders such as employees, customers, and the public.

Summarizing the research results, it was concluded that the effects of various corporate governance mechanisms on tax avoidancedepend on which each respective mechanism channels stakeholder interests. Therefore, corporate governance balances the conflicting interests of multiple stakeholders concerning tax avoidance, directing it to the optimal level for a given firm, which will offset the cost of paying taxes and eliminating them. Finally, the findings showed that corporate governance mechanisms, board independence, example, can increase tax avoidance and make firms more profitable but also limit tax avoidance to a level where the risks do not outweigh the benefits (Kovermann & Velte, 2019).

Supported by studies already conducted - where it was found that due to the high concentration of control, corporate governance practices no longer focus on reducing agency conflicts between shareholders and managers and start seeking to resolve disputes of interests between majority and minority shareholders - Martinez and Fonseca (2020), with a sample of companies listed in the [B]., conducted a study to verify: (i) if the level of control concentration of the companies influences tax aggressiveness, and (ii) if the corporate governance adopted by the companies mitigates the effect of the influence of control concentration on tax aggressiveness.

The authors developed the study based on the existing theory that with the adoption of good corporate governance practices, the fear of minority shareholders is reduced because there is greater transparency in the information disclosed and that, additionally, adherence to good corporate governance practices raises the level of monitoring by minority shareholders, thus creating obstacles for the development of activities related to the extraction of benefits for managers, and consequently no longer justifying the implementation of tax strategies that result in increased risks.

The results obtained with the tests performed offered evidence of a negative relationship between tax aggressiveness and the increase of shareholder control, suggesting, therefore, that the companies in the sample avoid tax aggressiveness practices because such practices could induce the investors of the existence of shareholder expropriation. On the other hand, when analyzing the adherence of the companies to the differentiated levels of corporate governance, the test results showed a positive relationship between tax aggressiveness and the increase of shareholder control, suggesting, therefore, that companies with good corporate governance practices benefit their cash flows with the approach of tax aggressiveness, demonstrating to investors the absence of risks of shareholder expropriation through tax aggressiveness. Thus, it was concluded that the tendency of companies with complete control to adopt a less fiscally aggressive posture is softened as these companies join the differentiated levels of corporate governance (Martinez & Fonseca, 2020).

Lin and Lin (2021) argue that corporate investment decisions are critical financial management decisions made by the board of directors. These decisions have long-term implications for the growth rate and earnings potential of the firm and are consequently irreversible and possess a high degree of risk. Ultimately, corporate investment decisions should increase the firm's value and maximize shareholder wealth.

As a mechanism available to shareholders, corporate governance can ensure that companies have adequate decision-making processes and controls. Thus, good corporate governance practices can lead to more effective monitoring by the board of directors and ensure that managers make investment decisions effectively. In this way, the board of directors should ensure that firms' investment decisions meet the objectives of maximizing firm value or shareholder wealth (Lin & Lin, 2021).

Based on a sample of Canadian firms from 2009 to 2012, the study was developed to examine how corporate governance affects firms' investment decisions empirically. The evidence revealed an inverse relationship between corporate governance and investment decisions, which suggests that corporate governance mechanisms can inhibit managers' opportunistic behavior and monitor managerial behavior regarding investment decisions. Thus, firms with good corporate governance practices may prevent managers from overinvesting (Lin & Lin, 2021).

In the research conducted, Rogers et al. (2008) obtained evidence that companies in the differentiated segments of corporate governance listed in the [B]3 (Novo Mercado, Level 1 and Level 2) have lower rates of return on investments than companies in other segments. On the other hand, Gomes (2016) obtained evidence that firms in the differentiated corporate governance segments listed on [B]3 (Novo Mercado, Level 1, and Level 2) had worse levels of tax management. Considering the interaction between these two findings, and that the implicit tax theory predicts that companies with lower pre-tax rates of return on investments have higher implicit taxes, and also considering that the tests will be conducted through quantile regression, where several points of the distribution (quantiles) will be analyzed, the following research hypothesis.

2.2 Hypotheses

The hypotheses can be detailed in this section:

2.2.1 Hypothesis on Corporate Governance and Implicit Taxes (H1)

The first research hypothesis related to the implicit taxes in differentiated corporate governance segments could be described as:

H1: In most quantiles, companies in the differentiated corporate governance segments (Novo Mercado, Nível 1, and Nível 2) listed on [B]3 have higher implicit taxes than companies in the other corporate governance segments listed on [B]3.

In the research conducted on implicit taxes, tests are conducted to find out what happens with the benefits obtained through tax incentives. In these cases, the relationship between the explicit tax rate and the post-tax return is analyzed to find out whether these benefits: (i) were retained by the firms (passed on to their shareholders), (ii) were not retained by the firms (passed on to the parties that the tax incentives were intended to benefit), or (iii) were eliminated by the implicit taxes.) To this end, the following research hypothesis is formulated.

2.2.2 Hypothesis on Benefit Retention from Tax Incentives (H2)

The second research hypothesis that deals with the retention of benefits obtained from using tax incentives within differentiated corporate governance segments can be detailed as:

H2: Companies in the differentiated corporate governance segments (Novo Mercado, Nível 1, and Nível 2) listed in [B]3 cannot retain the benefits obtained from using tax incentives, given the higher incidence of implicit taxes.

3 SAMPLE SELECTION AND RESEARCH DESIGN

The present research is exploratory since it was developed based on consultation of scientific articles. It is also descriptive since, based on the characteristics of a particular sample, it will establish the relationships among the variables that will be analyzed.

For the selection of the samples, data from the financial statements of Brazilian companies listed on the [B]., covering the period from 2011 to 2021, were used. The year 2011 was the first year chosen due to Brazilian companies' complete adoption of the IFRS standard (International Financial Reporting Standards). 2021 was selected as the last period because it was the previous year available in the database consulted.

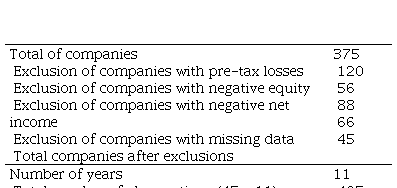

Using the COMDINHEIRO Platform, the companies that make up the samples were selected for the tests, already excluding the data capture of the financial companies, which is possible when using the COMDINHEIRO Platform. Companies with losses before taxes, companies with negative equity, companies with negative net income, and companies without data for the variables that will form the short and balanced panel were eliminated. Table 1 shows the process of formation and composition of the sample.

Process of Formation and Composition of the Sample

Source: Prepared by the authors.

Source: Prepared by the authors.

3.1 Research Project

Research seeking evidence of the presence of implicit taxes delves into the intricate relationship between the explicit tax rate and companies' pre-tax rate of return. Implicit taxes, as elaborated by Smith (2017), reflect the lower pre-tax returns on investments that are tax-favored, indicating a more nuanced interplay between taxation and financial decision-making. Drawing from Smith's extensive analysis, the current study adopts his models with certain adaptations for a contextualized exploration of the subject, recognizing that the topic addressed has not been explored to date. The econometric models of multiple linear regression to be employed are as follows:

GAAPETRi,t = β + β0 1 PTROE + βi,t 2 GCi,t + β. PTROEi,t xGCi,t + ∑β. CONTROLi,t (1)

GAAPETRi,t = β + β0 1 ROE + βi,t 2 GCi,t + β. ROEi,t xGCi,t + ∑β. CONTROLi,t (2)

In these models, the dependent variable measuring the tax rate (ETR) will be replaced by the Effective Tax Rate on Profit (GAAPETR) as defined by Hanlon and Heitzman (2010), reflecting the degree of a company's tax aggressiveness. Thus, a low GAAPETR rate means that a company realizes the reduction of its explicit tax burden on profit more intensively than companies with a higher GAAPETR rate.

The pre-tax rate of return (PTROE) variable, utilized by Smith (2017) to investigate implicit taxes, is calculated by dividing pre-tax accounting profit by equity. A negative relationship between PTROE and the explicit tax rate (GAAPETR) would indicate non-existence of implicit taxes, while a positive relationship would suggest their existence.

Similarly, the variable ROE (rate of return after taxes) is calculated by dividing net income by equity, with its relationship with GAAPETR further elucidating the complex nature of implicit taxes. According to Smith (2017), a negative relationship would suggest that firms retain benefits from tax incentives, while a positive relationship would imply that these benefits are not retained.

This nuanced understanding of implicit taxes, guided by Smith's foundational work (2017), underlines the importance of examining both explicit and implicit tax effects, especially in the context of corporate governance and the Brazilian market. By leveraging Smith's theoretical and empirical contributions, this study seeks to expand our comprehension of tax behavior and its broader implications for corporate strategy and governance.

The GC variable is a moderator dummy variable that will assume a value equal to one for the differentiated Corporate Governance segments of the [B]3 and zero for the others (Prado et al., 2014). A negative relationship between the dependent variable GAAPETR and the interaction between PTROE and GC (PTROExGC) suggests that firms in the differentiated Corporate Governance segments of [B]3 have lower implicit taxes than the other segments. On the other hand, a positive relationship between the dependent variable GAAPETR and the interaction between PTROE and GC (PTROExGC) suggests that firms in the differentiated Corporate Governance segments of [B]3 have higher implicit taxes than the other segments. A negative relationship between the dependent variable GAAPETR and the interaction between ROE and GC (ROExGC) suggests that firms in the differentiated Corporate Governance segments of [B]3 can retain the benefits of using tax incentives. On the other hand, a positive relationship between the dependent variable GAAPETR and the interaction between ROE and CG (ROExGC) suggests that companies in the differentiated Corporate Governance segments of [B]3 are unable to retain the benefits obtained from the use of tax incentives (Vieira & Faia, 2018).

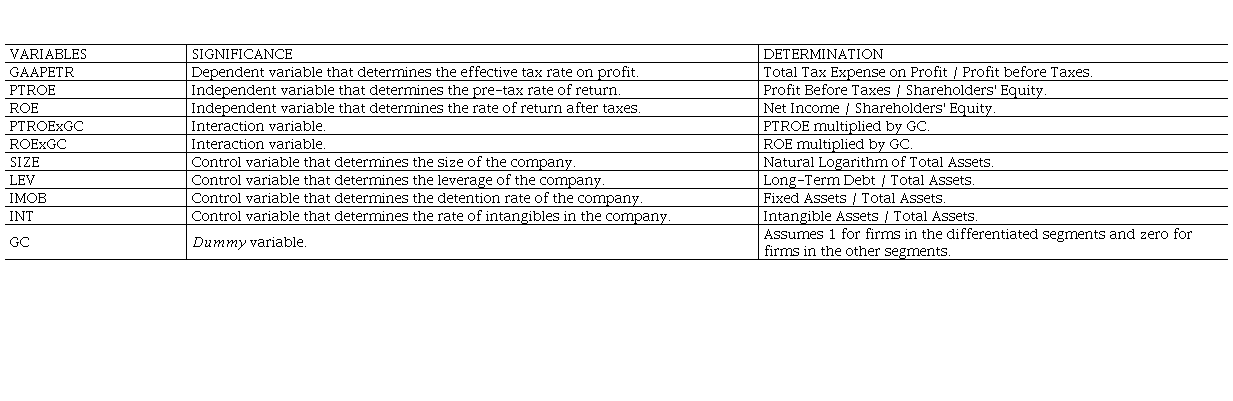

This paper will use the following control variables: SIZE, LEV, IMOB, and INT. The variable SIZE (size of firms) is calculated as the natural logarithm of total assets. LEV (leverage) is calculated by dividing long-term debt by total assets. The variable IMOB (companies' fixed assets ratio) is calculated by dividing total fixed assets by total assets. Finally, the variable INT (intangibles companies' rate) is calculated by dividing total intangible assets by total assets (Carvalho & Kalatzis, 2018). The summary and form of calculation of all variables used in the developed models are summarized in Table 2 below:

Calculations and Meanings of Model Variables

Source: Prepared by the authors.

4 ANALYSES OF RESULTS

After collecting the data using the COMDINHEIRO platform, a decision driven by the platform's reputation for comprehensive and reliable financial information, the data were treated in Excel to generate the variables and the respective short balanced panel. COMDINHEIRO was selected due to its extensive coverage of financial metrics and its widespread acceptance among researchers and practitioners in the field of finance. This platform provides access to detailed financial data essential for our analysis, making it a suitable choice for our research needs. Soon after the data preparation, the statistical tests were started in the R software, version 4.2.2, to perform robust analyses and validate the hypotheses.

4.1 Descriptive Statistics

After obtaining the data from the COMDINHEIRO platform, the EXCEL software was used to create and calculate the respective variables. Finally, the descriptive statistics results were obtained using the software R, version 4.2.2. Table 3 below presents the descriptive statistics for GAAPETR.

Descriptive Statistics of GAAPETR

Source: COMDINHEIRO Platform Table prepared by the authors

Analyzing the results of the descriptive statistics, it is observed that for taxes on income (GAAPETR) the average explicit tax rate of the companies in the differentiated Corporate Governance segments is lower than the average effective tax rate of the other Corporate Governance segments. In addition, it is also observed that in the first quartile, the median, and the third quartile, the average explicit tax rates of firms in the differentiated Corporate Governance segments are lower than the average explicit tax rates of the other segments, suggesting that across the distribution firms in the differentiated segments are using tax incentives more intensively than firms in the different Corporate Governance segments.

Implicit taxes are conceptualized as lower pre-tax rates of return on investments in tax-favored assets (Scholes et al., 2009). In the GAAPETR descriptive statistics, it is observed that the pre-tax rates of return (PTROE) of the differentiated segments are lower than the pre-tax rates of return (PTROE) of the other segments across the distribution (mean, median, first quartile, and third quartile). These results suggest that firms in the differentiated segments bear higher implicit taxes than others.

In the case of after-tax returns (ROE), the literature on implicit taxes informs us that the ROE analysis aims to verify whether companies can retain the benefits obtained through tax incentives. Thus, an analysis of ROE within the scope of descriptive statistics is not appropriate.

4.2 Multivariate Quantile Regression Analysis

Supported by what Armstrong et al. (2015) explain, the use of Ordinary Least Squares (OLS) describes only the conditional mean relationship of the dependent variable with the independent variables. Essentially, OLS focuses on estimating the mean of the dependent variable given certain independent variables, thereby providing a snapshot of the central location of the distribution. However, this approach can be limiting in several ways, especially for our research, where understanding the full distribution is essential.

1. Capturing the Entire Distribution. OLS's limitation in capturing only the mean effect could lead to an incomplete or even misleading understanding of the underlying relationships in our data. Quantile regression, on the other hand, allows us to investigate the relationship between the dependent and independent variables at different quantiles of the distribution. This ensures that we are not only focusing on the central location but exploring how the relationship behaves across the entire spectrum of the distribution.

2. Robustness to Outliers. Unlike OLS, quantile regression is not as sensitive to outliers. By examining different quantiles, it provides a more robust view of the relationships in the presence of extreme values or non-normal distribution. This robustness is particularly beneficial in our study, given the potential complexity and diversity of corporate tax structures and governance.

3. Understanding Heterogeneous Effects. Quantile regression can reveal heterogeneous effects that might be obscured when only looking at the mean relationship. In the context of our study, where interactions between the effective tax rate and other factors may differ across the distribution, this is an invaluable insight.

4. Tailoring to the Research Question. Lastly, the specific focus on implicit taxes and the complexity of the relationship between corporate governance and tax structures necessitates a more nuanced analysis. Quantile regression fits well with our research objectives, offering a more detailed and nuanced understanding of the relationships at various points in the distribution.

Thus, in this paper, the analysis will be conducted using quantile regression, which offers a richer and more comprehensive examination of the underlying relationships in our data. It allows us to move beyond the limitations of OLS and provides insights that are more aligned with the complexities and nuances of our research focus.

By choosing this approach, we are better positioned to uncover meaningful insights into the relationship between the effective tax rate and the models' interactions in this paper, insights that might otherwise be missed by solely focusing on the central location of the distribution.

After collecting the data in the COMDINHEIRO Platform, they were treated in Excel to generate the variables and the respective short and balanced panel. Soon after this treatment, the statistical tests were started in the R software, version 4.2.2.

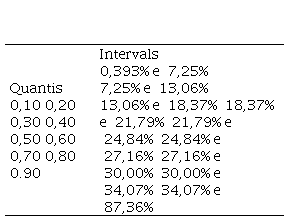

In the quantile regression run, the quantiles listed in the following table were tested, in which the ranges of explicit tax rates for each quantile considered are also shown.

Ranges of the GAAPETRs for each quantile

Source: COMDINHEIRO Platform Table prepared by the authors

4.2.1 Multivariate analysis of the PTROExGC interaction

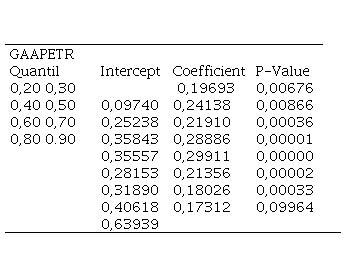

The following table presents the quantile regression results concerning the tests performed for the interaction between pre-tax rate of return (PTROE) and corporate governance (CG), which assumes a value equal to 1 for companies in the differentiated segments and zero for companies in the other segments. Therefore, only the results of the quantiles in which the interactions were statistically significant are presented.

Results of the interactions

Source: COMDINHEIRO Platform Table prepared by the authors

The displayed table shows that for taxes on profit (GAAPETR), the quantile 0.10 did not present a result with statistical significance, suggesting that the implicit taxes are not statistically different among the segments studied at this point of the distribution. However, for the other quantiles, the results show a positive and significant relationship between the explicit tax rate and the interactions at the 1% level (for the quantiles 0.20, 0.30, 0.40, 0.50, 0.60, 0.70, and 0.80) and the 10% level for the quantile 0.90. These results suggest that companies in the differentiated corporate governance segments (Novo Mercado, Nível 1, and Nível 2) have higher implicit taxes than companies in the other segments, which corroborates what was predicted in our first hypothesis.

A positive relationship between the effective tax rate and the pre-tax rate of return indicates that as the tax rate on profit is reduced, the pre-tax rate of return is also reduced. From the results presented, it is seen that for the firms in the differentiated segments, a one-unit reduction in GAAPETR causes a reduction in the pre-tax rate of return of (i) 0.19693 units in the 0.20 quantile, (ii) 0.24138 units in the 0.30 quantile, (iii) 0.21910 units in the 0.40 quantile, (iv) 0.28886 units in the 0.50 quantile, (v) 0.29911 units in the 0.60 quantiles, (vi) 0.21356 units in the 0.70 quantiles, (vii) 0.18026 units in the 0.80 quantiles, and (viii) 0.17312 units in the 0.90 quantiles.

4.2.1 Multivariate Analysis of the ROExGC Interaction

The following table presents the results of the quantile regression concerning the tests performed about the interaction between the rate of return after taxes (ROE) and corporate governance (CG), which assumes a value equal to 1 for the companies in the differentiated segments and zero for the companies in the other segments. It should be noted that only the results of the quantiles in which the interactions presented statistical significance are shown.

Results of the interactions

Source: COMDINHEIRO Platform Table prepared by the authors

Source: COMDINHEIRO Platform

Table prepared by the authors

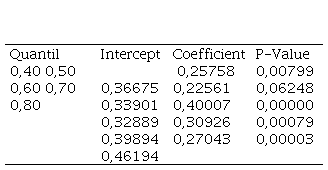

The table displayed shows that for taxes on profit (GAAPETR), the quantiles 0.10, 0.20, 0.30, and 0.90 did not show results with statistical significance, suggesting that at these points in the distribution, the implicit taxes are eliminating any benefit obtained from the use of tax incentives. However, for the remaining quantiles, the results show a positive and significant relationship between the explicit tax rate and the interactions at the 1% level (for the quantiles 0.40, 0.60, 0.70, and 0.80) and the 10% level for the 0.50 quantile (median). These results suggest that the benefits obtained from the use of tax incentives by companies in the differentiated corporate governance segments (Novo Mercado, Nível 1, and Nível 2) are not being retained by these companies but instead transferred to the parties that the tax incentives were intended to benefit, which corroborates the predictions of our second hypothesis.

A positive relationship between the effective tax rate and the after-tax rate of return indicates that as the tax rate on profit is reduced, the after-tax rate of return is also reduced. From the results presented, it is seen that for the firms in the differentiated segments, a one-unit reduction in GAAPETR causes a reduction in the after-tax rate of return of (i) 0.25758 units in the 0.40 quantile, (ii) 0.22561 units in the 0.50 quantile, (iii) 0.40007 units in the 0.60 quantiles, (iv) 0.30926 units in the 0.70 quantiles, and (v) 0.27043 units in the 0.80 quantiles.

Taken together, the results of the multivariate analysis suggest that companies in the differentiated Corporate Governance segments of the [B]3 (Novo Mercado, Nível 1, and Nível 2) bear a higher implicit tax burden than companies in the other Corporate Governance segments of the [B]3. Furthermore, the results also suggest that companies in the differentiated Corporate Governance segments of [B]3 (Novo Mercado, Nível 1, and Nível 2) are unable to retain (pass on to shareholders) the tax benefits obtained by reducing their explicit tax rates, i.e., the implicit taxes eliminate the benefits received by using the tax incentive.

The results obtained corroborate the hypotheses proposed in this work, as well as are in line with what was found by Rogers et al. (2008), who obtained evidence that companies of the differentiated segments of Corporate Governance listed in the [B]3 (Novo Mercado, Nível 1 and Nível 2) have lower rates of return on investments than companies in other segments. In addition, the results also find support in what was found in Gomes (2016) because the presence of implicit taxes in the companies of the differentiated Corporate Governance segments of [B]3 (Novo Mercado, Level 1 and Level 2) indicates the existence of weakened tax management levels.

5 CONCLUSIONS

According to the literature on implicit taxes, the total tax burden of a company is formed by the sum of implicit and explicit taxes. Therefore, tax-accounting research should strive to estimate and incorporate implicit taxes in its analyses, as failure to do so results in biased conclusions.

In the existing body of research focusing on corporate governance and taxes, the emphasis has predominantly been on explicit taxes. To the best of our knowledge, no studies have explored the relationship between corporate governance and implicit taxes. This paper has sought to bridge this gap, providing evidence of implicit taxes in Brazilian publicly traded companies within the specific Corporate Governance segments of B3 (Novo Mercado, Nível 1, and Nível 2).

Two key hypotheses were tested in this study. The first aimed to determine whether firms in differentiated segments have higher implicit taxes compared to other segments. The second sought evidence that explicit tax benefits are negated by implicit taxes in firms within these differentiated segments. The evidence supports both hypotheses, revealing that firms in differentiated segments indeed bear a higher implicit tax burden, and that the gains from explicit tax incentives are counterbalanced by implicit taxes. These findings align with existing corporate governance literature but also present new insights, particularly about the relationship between implicit taxes and corporate governance in Brazil.

However, the study's limitations must be acknowledged. Firstly, the results are confined to the specific sample of companies studied, making broad generalizations infeasible. Secondly, the necessity to exclude a significant amount of data reduced the number of observations, possibly affecting the robustness of the findings. Thus, the suggestion for future research is to expand this study, focusing particularly on obtaining evidence concerning the relationship between implicit taxes and the corporate control structure.

In returning to the objective and hypotheses that guided this study, it becomes clear that this research not only advances our understanding of the interplay between explicit and implicit taxes but also sheds light on areas where further investigation is needed. The findings correspond to some existing literature, yet they differ in significant ways, especially in exploring new grounds within the context of Brazilian corporate governance.

The implications of understanding the total tax burden on companies reach beyond academic interest. Corporate strategists, investors, policymakers, and tax authorities can greatly benefit from these insights. It enhances tax planning, fosters more informed investment decisions, and may influence tax policy development. This understanding also contributes to improving the conclusions of information users by offering a comprehensive perspective on tax burdens, affecting various corporate decisions.

In conclusion, the intersection between implicit tax and corporate governance proves to be intricate and multifaceted. Full comprehension of how these factors interact requires further investigation, considering variables like ownership structure, board characteristics, tax haven activity, and corporate governance approach. A more profound understanding of this relationship is pivotal for both tax authorities and corporations striving to bolster internal control and governance while ensuring compliance with tax obligations. The insights gained from this study signify a meaningful step in this direction, promising a rich avenue for future research and practical applications.

REFERENCES

Agyei-Mensah, B. K. (2021). The impact of board characteristics on corporate investment decisions: an empirical study. Corporate Governance: The international journal of business in society, 21(4), 569-586.

Armstrong, C. S., Blouin, J. L., Jagolinzer, A. D., & Larcker, D. F. (2015). Corporate governance, incentives, and tax avoidance. Journal of Accounting and Economics, 60(1), 1-17.

Carvalho, F. L. de, & Kalatzis, A. E. G. (2018). Earnings quality, investment decisions, and financial constraint. Revista Brasileira de Gestão de Negócios, 20, 573-598.

Da Silva, R. (2020). Planejamento tributário e tributos implícitos: uma análise no nível corporativo. Anais do Encontro da ANPAD – EnANPAD, Evento On-Line, 44.

Gomes, A. P. M. (2016). Características da governança corporativa como estímulo à gestão fiscal. Revista Contabilidade & Finanças, (27), 149-168.

Kovermann, J., & Velte, P. (2019). The impact of corporate governance on corporate tax avoidance—A literature review. Journal of International Accounting, Auditing and Taxation, 36.

Lin, D., & Lin, L. (2021). An Examination of the Impact of Corporate Governance on Corporate Investment Decisions. International Journal of Business & Management Studies, 2(10).

Martinez, A. L. (2017). Agressividade Tributária: Um Survey da Literatura. Revista de Educação e Pesquisa em Contabilidade (REPeC), 11.

Martinez, A. L., & Fonseca, N. M. (2020). A influência da estrutura de controle na agressividade tributária corporativa. Enfoque: Reflexão Contábil, 39(2), 153-163.

Pereira, R., Marcilio, B., Guercio, M., Takimoto, T., & Fialho, F. (2021, novembro). ESG: Uma revisão integrativa. ENGEMA 2021. XXIII Encontro Internacional sobre Gestão Empresarial e Meio Ambiente - FEA/USP, São Paulo.

Prado, P. H. M., Korelo, J. C., & Da Silva, D. M. L. (2014). Análise de mediação, moderação e processos condicionais. Revista Brasileira de Marketing, 13(4), 04-24.

Ribeiro, J. E. & Souza, A. A. (2023). Impact of Corporate Governance on Financial Performance: Evidences in the Brazilian Stock Market. Revista Contabilidade, Gestão e Governança, 26 (1), 63-91.

Rogers, P., Securato, J. R., & de Sousa Ribeiro, K. C. (2008). Governança corporativa, custo de capital e retorno do investimento no Brasil. REGE Revista de Gestão, 15(1), 61-77.

Scholes, M. S., Wolfson, M. A., Erickson, M., Maydew, E. L., & Shevlin, T. (2009). Taxes and business strategy: a planning approach (4a ed.). Prentice Hall.

Silva, B. A. D. O., Caixe, D. F., & Krauter, E. (2019). Governança corporativa e sensibilidade investimento-fluxo de caixa no Brasil. Brazilian Review of Finance, 17(2), 72-86.

Smith, H. E. (2017). Implicit taxes in imperfect markets. (Ph.D. Dissertation, University of Tennessee, Tennessee, Estados Unidos).

Tarighi, H., Hosseiny, Z. N., Akbari, M., & Mohammadhosseini, E. (2023). The Moderating Effect of the COVID-19 Pandemic on the Relation between Corporate Governance and Firm Performance. Journal of Risk and Financial Management, 16(7), Artigo 7.

Vieira, V. A., & Faia, V. D. S. (2018). Efeitos moderadores duplos e triplos na análise de regressão. Revista de Administração UFSM, 11(4), 961-979.