Artigos

Esta obra está bajo unaLicencia Creative Commons Atribución 4.0 Internacional.

Received: 13 January 2023

Revised: 22 May 2023

Accepted: 18 August 2023

Published: 12 September 2023

DOI: https://doi.org/2237-7662202333651

Abstract: Brazil is one of the emerging countries that has adopted the IFRS, and agribusiness plays a relevant role in the Brazilian economy, turning the country into an important player in the review and discussion process of international standards. The objective of this paper is to assess whether IAS 41 contributes to the enhancement of the quality of accounting information, given that the measure that was previously used was historical cost, with no changes in the future economic benefits being disclosured, resulting in low-quality information. To analyse agribusiness companies’ financial statements, five analysis sections were created: disclosure in the notes; value relevance; timeliness of fair value information on biological assets; earnings management; and experts’ opinion of the quality of the information on the biological assets. The results reveal that: there have been improvements in the compulsory disclosure required by IAS 41, but this disclosure is not yet suitable; variations in the fair value of biological assets are value-relevant, but not for bearer plants; the information on biological assets is not timely; there are signs of earnings management by companies with lower disclosure levels; analysts consider that non-financial information may be prepared more useful. No study was found in the literature that considered the combination of the level of disclosure of the notes to the financial statements, the value relevance, the timeliness of the fair value information, earnings management and analysts’ opinions.

Keywords: Biological assets, IAS 41, Accounting information quality, Fair value, Agribusiness.

1 INTRODUCTION

The relevance of this article derives from the strategic role of agribusiness for Brazil, which enhances its economic and social development. In this sense, the growth of agribusiness can favor the Brazilian economy as a result of its economic and social implications. Accordance to data from Confederação da Agricultura e Pecuária do Brasil - CNA (2023), Brazilian agribusiness is responsible for 24.8% of GDP. For this reason, government incentives work on different fronts, and one of these fronts is funding programmes to enhance companies’ productivity.

In view of the importance of the sector for the economy, the existence of alternative funding sources like the capital markets is healthy. Despite their immature nature when compared to other developed countries, the efforts made to grant small and medium-sized companies access to the market are noteworthy.

In this scenario, the important function of accounting, which is considered the language of business, should be highlighted, as it contributes to a reduction in the adverse selection problem. To reduce the information asymmetry between debtors and creditors, debtors’ financial statements should be relevant, understandable and useful for investment decision purposes. The accounting model that is currently adopted is based on the international model called the International Financial Reporting Standards – IFRS, which is considered a set of high-quality rules that can result in better information.

One of these standards is IAS 41 for Biological Assets and Agricultural Products, which focuses on the regulation of accounting practices in companies dealing with live animals and plants that go through some sort of biological transformation, together with agricultural production at the point of harvest[1]. Firms with such assets can play a relevant role in agribusiness.

IAS 41 resulted in significant changes in companies’ balance sheets, because before the convergence with the IFRS companies used to adopt cost as the basis for measuring their biological assets, which corresponds to the accumulation of expenses as the assets grow. To offer more timely information, IAS 41 strongly recommends fair value, because the financial statements can then disclose the expected economic gains (losses) due to the valuation (devaluation) of the asset, independently of its sale.

Some studies question this better information (Booth & Walker, 2003; Dvorakova, 2006; Herbohn, 2006; Williams & Wilmshurst, 2009; Fisher et al., 2010; Argilés, Garcia-Blandon & Monllau, 2011; Rech & Pereira, 2012; Baazaoui & Zaraï, 2019; Moutinho, 2022) because of the difficulty of estimating the fair value when there is no active market, and also due to use of non-observable data and low level of disclosure required by IAS 41. However, some studies found an improvement in the disclosure of accounting information associated with IAS 41 (Hsu et al., 2019; Souza & Shikida, 2021), highlighting the increase in Brazilian research (Oliveira & Nakao, 2021). Concerning this, agency theory puts forward the possibility of a mismatch between the targets of the agent and the principal, explained by the different incentives of the two parties. Thus, the manager can use the discretion given in the standard to focus on specific targets, producing low-quality financial statements.

In addition, the home country’s institutional characteristics, such as the development of the capital markets, the funding source, the political and legal system and the enforcement level, can influence the convergence process with the IFRS. Without enforcement mechanisms, it is improbable that convergence will truly take place, which contradicts the objective of the IFRS to provide financial information that is useful to investors. If the information is irrelevant, it will be of no use for investors that are interested in evaluating a company in the agribusiness sector, making efficient resource allocation more difficult.

In that context, the objective of this paper is to investigate whether IAS 41 contributes to the enhancement of the quality of accounting information, given that the historical cost does not disclose the future economic benefits, which results in low-quality information. Therefore, we observe the value-relevance and timeliness of the fair value variation of the biological assets net of the depletion expense (FV), and we consider whether there are signs of earnings management, given the greater subjectivity in the accounting of some biological assets. Finally, we analyse the level of compliance with the disclosure requirements in IAS 41. This study focuses on analyzing the quality of accounting information provided by IAS 41, together with its utility for stakeholders. We, therefore, investigate the disclosure quality of the information on biological assets and how investors and market analysts consider this information. To study investors’ perceptions, earnings quality models are used, while questionnaires were sent to analysts. No study was found in the literature that combined the level of disclosure in the notes to the financial statements, the value-relevance, the timeliness of the fair value, earnings management and analysts’ opinions. This range of approaches can provide further assistance in understanding the effects of IAS 41 and can support a discussion of the standard and possible changes to it, as happened recently concerning bearer plants[2]. Therefore, what distinguishes this study is precisely the exploration of further evidence, which can clarify the application of IAS 41 in the Brazilian economy.

Brazil is one of the emerging countries that has adopted the IFRS, and agribusiness plays a relevant role in the Brazilian economy, turning the country into an important player in the review and discussion process of international standards, including IAS 41. Thus, we hope to contribute to the review of the standard.

Furthermore, this research can bring contributions to companies, standard-setters, investors and stakeholders, who are interested in investigating and discussing the possible limitations associated with the standard, given the influence of institutional aspects and disincentives that difficult relevant disclosure. The importance of this study arises from the growth of agribusiness, which can be funded by the capital markets, with a range of positive effects for Brazil.

2 REFERENCE FRAMEWORK AND RESEARCH HYPOTHESES

When the IFRS was adopted, many studies were published around the world to analyze the consequences of its application. In addition, many studies specifically investigated the effects of a particular standard, such as IAS 41 on Agriculture.

IAS 41 applies to all companies with biological assets and agricultural produce at the point of harvest. Biological assets refer to all living animals and plants that are the origin of agricultural produce – which means any produce that is harvested from biological assets. Although the standards permit the use of two bases of measurement – fair value or historical cost – the use of the latter has become the exception (IFRS Foundation, 2021b).

Concerning fair value, IFRS 13 on Fair Value Measurement requires a company to use valuation techniques appropriate to the circumstances and for which sufficient data are available to measure the fair value, maximizing the use of relevant observable data and minimizing the use of non-observable data (IFRS Foundation, 2021a).

In this situation, the IAS 41 require a certain degree of judgement in addition to the responsible use of subjectivity in the application of accounting standards. In addition, according to IFRS 13, the availability of relevant information and the relative subjectivity of this information can influence the choice of the appropriate valuation technique. Nevertheless, without an active market, the manager can use non-observable data to price the asset, as in the case of the discounted cash flow, but this is not a desired scenario, according to IFRS 13 (IFRS Foundation, 2021a).

Hence, when a market value is unavailable for biological assets, the company should use the present value of the expected net cash flow, discounted at the current market rate. All the premises for the determination of the fair value should be disclosed.

In Brazil, before IAS 41, biological assets were measured at the lower between historical cost and market value, which gave a more objective and verifiable measuring basis. Nevertheless, the most common basis of measurement was the historical cost, which does not show the expected future benefits of the biological asset, resulting in poor-quality information. As a result of IAS 41, the biological assets are represented at their fair value, which can produce more relevant information. By allowing the use of the fair value when no observable data exist, the standard gives the manager the responsibility of using the discounted cash flow, by the elements that most adequately represent the expected future performance of the business, with the discount rate and the period of the benefits serving as relevant distinguishing factors. Hence, the manager can be more or less conservative in his projections – which by itself can influence the quality of the accounting information (Georgiou et al., 2021). Nevertheless, the historical cost method can reduce the quality of the financial information for biological assets that have a long life and high maturing and production values (Hsu et al., 2019). To give an example, companies in the paper and pulp sector have extensive forest growth areas that take many years to reach cutting age. Therefore, the fair value concept may be more suitable, despite the questions raised about its subjectivity.

Although accounting plays a fundamental role in addressing the information needs of external users, it is known that managers have an incentive not to disclose information that is coherent with the company’s equity situation, because of the agency theory (Jensen, & Meckling, 1976). The manager can use his discretionary power, given that there are accounting alternatives, to maximise his utility function to meet his preferences (Jensen & Meckling, 1994). Considering the company as a network of contracts, Watts and Zimmerman (1986) developed hypotheses to explain differences in accounting, due to distinct incentives among the parties.

In addition, we know that the implementation of GAAP is influenced by legal and institutional aspects (Soderstrom & Sun, 2007; Holthausen, 2009; Armstrong et al., 2010; Walker, 2010; Christensen et al., 2013). These studies reveal that accounting can be questionable in environments with low legal protection for investors, poorly developed capital market, weak institutional environment, and corporate governance practices that do not guarantee equal rights for all shareholders.

Brazil is classified as a code-law country, which provides less protection for investors, and in addition, it has a poorly developed capital market (La Porta et al., 1997). Furthermore, the Brazilian economy has a weak institutional environment (Anderson, 1999), with corporate governance practices that do not protect shareholders’ rights (Chong & Lopez-De-Silanes, 2012), representing a disincentive to foreign capital.

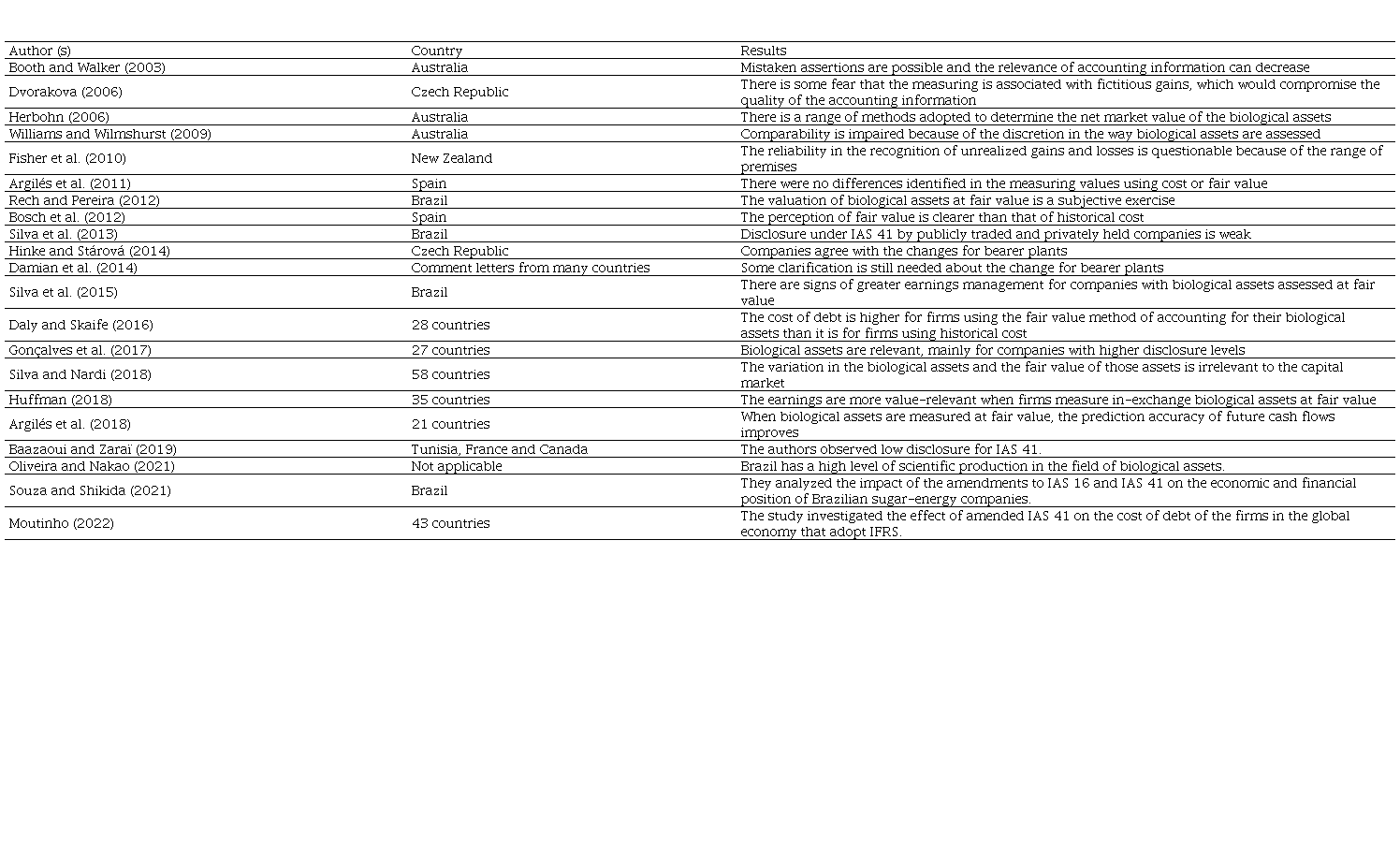

In that sense, the studies by Fisher et al. (2010), Argilés et al. (2011), Rech and Pereira (2012) and He et al. (2018) alert us to the subjectivity and the possibility of earnings management in the application of IAS 41. These and other studies have explored the financial reports, based on the change in the measuring base from the historical cost to the fair value. Some of these studies are displayed in table 1.

Source: developed by the authors.

The studies indicate that there is room for discussion on IAS 41, mainly arising from the use of fair value, the quality of disclosure and the recent changes for bearer plants.

Huffman (2018) analyzed 35 countries and concluded that the fair value of biological assets supplies information that is more useful for taking decisions. She found that earnings information is significantly more relevant when firms measure in-exchange biological assets at their fair value, but that book value and earnings information are significantly less relevant when firms measure in-use biological assets at their fair value. In addition, she provided evidence supporting the recent amendment for bearer plants. Moreover, Gonçalves et al. (2017) examined the value-relevance of fair value accounting for biological assets in 27 countries. Their results showed that biological assets are value-relevant, mainly for companies with higher disclosure levels. Surprisingly, the same results were obtained for bearer biological assets. Finally, Argilés et al. (2018) investigated the usefulness of the fair valuation of biological assets for cash flow prediction. They found that when biological assets are measured at fair value, the prediction accuracy of future cash flows improves as the ratio of biological assets to total assets increases. Nevertheless, the evidence is weaker for bearer plants.

The earlier studies present contradictory results, indicating that there is room to explore this research area. In addition, developing markets like Brazil are more likely to have a poor information environment that does not provide an adequate flow of information (Lopes & Alencar, 2010). In this context, and considering the results of Silva et al. (2013), the following research hypothesis can be presented:

H1: the disclosure of biological assets in Brazil following IAS 41 is weak.

Regarding the quality of accounting information in the capital market context, there is evidence that the value-relevance of accounting information has changed since the adoption of the IFRS (Barth et al., 2008; Chalmers et al., 2011). Specifically addressing IAS 41, the relevance of accounting information may have decreased (Booth & Walker, 2003; Dvorakova, 2006; Fisher et al., 2010) or increased (Gonçalves et al., 2017; Huffman, 2018).

Considering the opposing results for the relevance of biological assets, we will support the next hypothesis with results that show an increase in the relevance of accounting information after the adoption of the IFRS (Barth et al., 2008; Chalmers et al., 2011). Therefore, the second hypothesis is as follows:

H2: the variation in the fair value of biological assets (Income Statement) and the measurement of biological assets at fair value (Balance Sheet) are value-relevant in the capital market.

Regarding bearer plants, there are only a few studies about this group of biological assets (Damian et al., 2014; Hinke, & Stárová, 2014; Gonçalves et al., 2017). However, the amendment in the measurement for bearer plants motivated us to expect the accounting information to have less relevance. We should remember that bearer plants have been included in the scope of IAS 16 on Property, Plant and Equipment since January 2016, and now they are being measured at historical cost. The main incentive for withdrawing the measurement at fair value was that bearer plants are held for production rather than sale. Hence, they deserve the same measurement rules as property, plant and equipment. During our analysis period, 2008-2015, bearer plants were measured at fair value, and this was criticized by market analysts and other users of information (IFRS, 2019) because of the great uncertainty present in the calculation of the fair value. Thus, the hypothesis for bearer plants is:

H3: the variation in the fair value of bearer plants (Income Statement) and the measurement of bearer plants at fair value (Balance Sheet) are not value-relevant in the capital market context.

According to Barth (2018), one of the main concerns about fair value measurements is that, in the absence of market prices from a liquid market, fair value estimates have too much estimation error. However, the fair value may be closer to the economic value of the asset than is its historical cost. In addition, fair value can bring better information (Ball, 2006) because it implies more timely accounting information. In Brazil, there is evidence of low levels of earnings timeliness (Lopes, 2005).

Given that there are no studies addressing the timeliness of the fair value of biological assets, we composed our research hypothesis based on Lopes (2005) and on research that found some difficulty in measuring the fair value of biological assets properly (Dvorakova, 2006; Williams & Wilmshurst, 2009; Fisher et al., 2010; Silva et al., 2015).

H4: the variation in the fair value of biological assets (Income Statement) is not timely in the capital market.

The next two hypotheses concern earnings management. We know that financial statements depend on the incentives confronted by managers (Ball et al., 2000). In addition, Brazil is classified as a country with poor enforcement (La Porta et al., 1997; Anderson, 1999; Chong & Lopez-De-Silanes, 2012), which may favour higher earnings management (Burgstahler et al., 2006; Eilifsen et al., 2021). However, the adoption of the IFRS may reduce earnings management levels (Barth et al., 2008; Zéghal et al., 2011).

In the context of IAS 41, the studies of Fisher et al. (2010), Silva et al. (2015) and Silva et al. (2022) demonstrated the possibility of earnings management for companies that have biological assets, especially in the case of assets without an active market. There is still evidence of an inverse relationship between earnings management practices and companies’ disclosure levels (Lobo & Zhou, 2001; Jo, & Kim, 2007; He, 2020). Therefore, our first earnings management hypothesis is:

H5: companies with higher earnings management disclose less of the information required by IAS 41.

Bearer plants were measured at fair value in the study period. Given that there was no active market for them, other valuation techniques were applied, such as discounted cash flow. However, these valuation methods to measure fair value are based on unobservable data, which allows greater discretion in choosing the parameters and premises. This freedom can be exercised to increase the reported wealth of the owners of capital or to expropriate it (Watts & Zimmerman, 1990), depending on the incentives that influence managers’ actions. The application of discounted cash flow models can generate results of questionable reliability, because of the diversity of the premises, directly influencing the quality of the accounting information (Fisher et al., 2010) and leading to our second earnings management hypothesis:

H6: earnings management is higher for companies holding bearer plants.

Finally, the last hypothesis is based on the responses to the IASB’s 2011 Agenda Consultation and the outreach performed by the IASB staff about the IAS 41 requirement for fair value information about bearer plants. When analysts were consulted about the additional disclosures, they showed a preference for receiving non-financial information about production rather than fair value information about bearer plants. Furthermore, analysts and other users eliminate the effects of changes in the fair values of bearer biological assets for two reasons: i) information about operating performance and cash flows is more relevant to their forecasting and analysis, and ii) there are concerns about the reliability of fair value measurements because such valuations involve significant management judgment, and have the potential for manipulation (He et al., 2018; IFRS, 2019; Goh et al., 2021). Thus, the last hypothesis is:

H7: analysts do not consider the information of IAS 41 to be useful in their forecasts.

3 SAMPLE AND METHOD

The sample consists of 33 publicly traded Brazilian companies, as listed in table 2.

Companies in the sample

Source: developed by the authors.Note. information collected from notes to the financial statements; *the company uses historical cost and fair value to measure biological assets; the "X" symbol means that the firm has Bearer plants.

All the companies have biological assets on their balance sheets between 2008 and 2015, which required the application of IAS 41. The table reveals that 22 of the companies have plants, three have animals, three have both plants and animals, and five do not give information about the nature of their biological assets in the notes to the financial statements.

In addition, as shown in table 2 there are 21 companies holding bearer plants, representing 64% of the total sample. Regarding the measurement bases, 22 of the companies use the fair value to evaluate their biological assets, four of the companies use fair value and historical cost, one of the companies uses historical cost, and six of the companies do not disclosure their measurement basis.

To analyse these companies’ financial statements, five analysis sections were created: i) disclosure in the notes to the financial statements; ii) value-relevance; iii) timeliness of fair value; iv) earnings management; and v) experts’ opinion on the disclosure of the biological asset. These sections are explained next.

3.1 Disclosure in the Notes to the Financial Statements

First, we analyzed the compliance of the notes to the financial statements with the requirements of IAS 41. We created a checklist based on the 22 disclosure items of IAS 41, and then we analyzed the notes to the financial statements for the period 2012-2014 for the companies in the sample. If the required information was present, a score of one was given, and on the contrary, zero. In general, the items checked were the disclosure of gains and losses, characteristics of the biological assets, fair value, risks and restrictions on biological assets, effects of changes, and maintenance of cost method. Thus, we reached evidence to analyze the level of disclosure of these companies with biological assets.

The checklist applied to assess the disclosure is displayed in Appendix 1. The results from this part of the analysis were used to assess research hypothesis 1.

3.2 Value-Relevance of Biological Assets

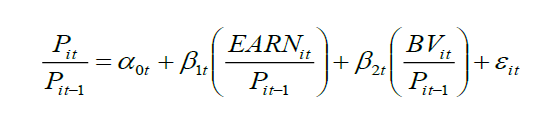

The second analysis section involves the application of value-relevance models. The basic specification used to assess the relevance of accounting information is based on Easton (1999)[3]:

(Eq. 1)

(Eq. 1)

where P corresponds to the stock price three (3) months after closing off the year; EARN corresponds to the earnings of company i in year t; BV is the book value of the equity of company i in year t; and Ɛ is the random error. The objective of dividing by the price at t-1 is to reduce scale problems, as suggested by Brown et al. (1999). The price-level regressions are explained next.

Accordingly to Easton (1999) at any point in time, the price reflects all returns since the company's inception, while book value represents all accounting measures of changes in value during the period. Book value will reflect the cumulative effect of accounting reporting lag – some of the value-relevant events observed by the market in early years will be included in accounting earnings of later years, but some will remain unrecovered in book value. The effect of this accounting reporting lag in the price-levels regression is similar to the effect in the returns regression.

However, current earnings reflect both a surprise to the market and a known component that the market had anticipated in an earlier period. In the return model, the known component is irrelevant in explaining current return and thus constitutes an error in the independent variable, biasing the slope coefficient on earnings toward zero. By contrast, the current stock price in the price model reflects the cumulative effect of earnings, and thus varies due to the surprise events and what the market already knows. Therefore, there is no errors-in-variables bias in price-model regressions. Intuitively, current earnings are uncorrelated with the information about future earnings contained in the current stock price, the dependent variable. Econometrically, the price model thus has an uncorrelated omitted variable, which reduces explanatory power, but the estimated slope coefficient is unbiased (Kothari & Zimmerman, 1995). There are studies that applied price-level regressions, such as Chen et al. (2020), Kwon and Wang (2020), Barth et al. (2021).

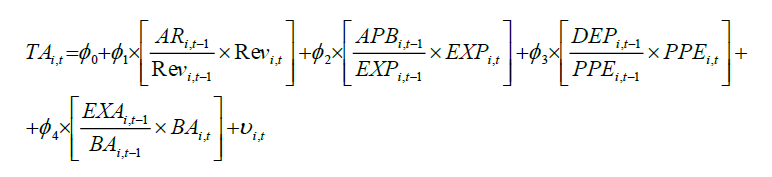

To analyze the value-relevance of the biological assets, we adjusted the original model. Among the accounts that compose the earning, we are interested in analyzing the variation in the fair value of the biological assets, because it was added to the financial statements after the adoption of IAS 41. Therefore, to observe the value-relevance of IAS 41, we isolated the fair value variation. In addition, the second variable of interest is the total value of the biological assets, which was also calculated by difference, according to the following model.

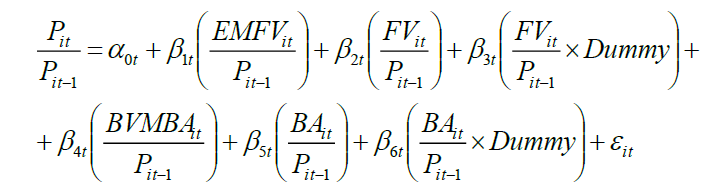

(Eq. 2)

(Eq. 2)

Where EMFV corresponds to the earnings minus the fair value variation of the biological assets[4] of the company i in year t, net of the depletion expense; FV corresponds to the fair value variation of the biological assets of the company i in year t, net of the depletion expense; BVMBA corresponds to the book value of equity minus the biological assets of the company i in year t; BA corresponds to the biological assets of the company i in year t; and Ɛ is the random error. The variables EARN and BV were decomposed, respectively, into EMFV and FV, and BVMBA and BA.

In this sense, the value-relevance of the information offered by IAS 41 can be investigated based on positive and statistically significant β2 and β5 coefficients. We used these results to assess research hypothesis 2.

This analysis should be complemented by the recent amendment[5] in IAS 41 Agriculture: bearer plants left the scope of IAS 41 and their accounting practice is now covered by IAS 16 on Property, Plant and Equipment.

The incentives for this amendment are explained by the criticism of measuring bearer plants at fair value, due to the use of future cash flow estimation models, which have some limitations and can produce an unreliable subjective estimate. In addition, there is no active market for bearer plants, except for agricultural production. To give an example, there is no active market for vineyards and rubber trees, but grapes and rubber have a market price.

Thus, the recent amendment for bearer plants offers an opportunity to study the value-relevance of this kind of asset. To analyze the accounting figures regarding bearer plants, the accounting earnings and the book value of the equity were again decomposed, and a dummy was added to indicate bearer plants, according to the following model.

(Eq. 3)

(Eq. 3)

Where Dummy is scored as 1 if the company has bearer plants and 0 if not; BVMBA corresponds to the book value of the equity minus the biological assets of the company i in year t; and Ɛ is the random error.

The value-relevance of bearer plants should be assessed through β2+β3 and β5+β6 for fair value and biological assets, respectively. According to research hypothesis 3, these should not be relevant in explaining the stock price behavior. Therefore, the coefficients for β3 and β6 are expected to be equal to zero.

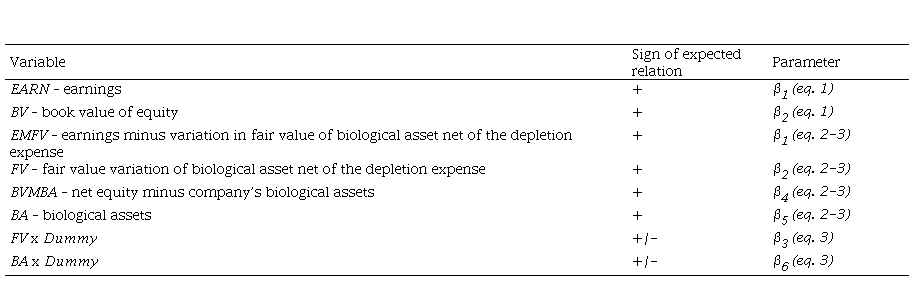

The expected signs are summarised in table 3.

Expected sign of variables

Source: developed by the authors.Note. Dummy scored 1 for companies with bearer plants and 0 if not.

3.3 Timeliness of Biological Assets

Another attribute that should be considered in the context of earnings quality is timeliness, which measures whether information is available for decision-makers in time to influence their decisions.

According to Easton (1999), price-based models are normally used to analyze the value-relevance of accounting information, while return models are applied to analyze timeliness. Return-based studies investigate the market’s response during a short period, and are intended to assess the role of accounting data in providing information that affects the investors’ perception of events that change the company value. In this case, the objective is to investigate the timeliness of the variation in the fair value of the biological assets, using the following model, which is based on Easton (1999):

(Eq. 4)

(Eq. 4)

where Ret indicates the stock return of company i in year t, estimated based on the continuous capitalisation method, which permits more robust results (Brooks, 2002). The profit variables are deflated by the price at t-1 with a view to reducing scale problems.

The timeliness model investigates the association between earnings and stock return. Accounting information is considered timely in the capital market when the stock return at time t reflects the earnings variation between t and t-1. Therefore, the information is considered timely when the coefficient β2 is statistically significant.

To analyze the timeliness of the fair value of the biological assets, the earnings were decomposed into earnings minus the variation in the fair value of the biological assets net of the depletion expense (EMFV) and the variation in the fair value of the biological assets net of the depletion expense (FV).

(Eq. 5)

(Eq. 5)

The earnings variables are deflated by the price at t-1, with a view to reducing scale problems. If the information is timely, the coefficient β4 needs to be statistically significant. The results were used to assess research hypothesis 4.

3.4 Earnings Management

Besides the value-relevance and timeliness of the fair value, the Conceptual Framework for Financial Reporting[6] requires that the accounting information should provide a faithful representation of the economic phenomena. It should therefore be complete, neutral and free from error, according to the Conceptual Framework.

To test whether the accounting information on biological assets is a faithful representation, one of the most used commonly used earnings management models in earnings management literature can be adopted: the model of Kang and Sivaramakrishnan (1995) - KS. According to Martinez (2001), this model provides the most efficient description of the accrual definition process. The KS model is based on the reasoning that total accruals are composed of discretionary and nondiscretionary items:

(Eq. 6)

(Eq. 6)

Where TA denotes total accruals; DA stands for discretionary accruals; and NDA denotes nondiscretionary accruals.

Therefore:

(Eq. 7)

(Eq. 7)

We calculated total accruals based on Healy (1985), Jones (1991) and Dechow et al. (1995), with an adjustment to consider the variation of the market value of biological assets, since total accruals do not necessarily represent an effect on cash flow. After calculating the total accruals, we computed the discretionary accruals based on the KS model adjusted according to Silva et al. (2015):

(Eq. 8)

(Eq. 8)

Where ARit-1, is the short-term accounts receivable; APBit-1 is net working capital without considering the accounts receivable of firm i in year t-1; EXPit-1 is the operating expense before depreciation and amortization of firm i in year t-1; EXPit is the operating expense before depreciation and amortization of firm i in year t; DEPit-1 is the depreciation and amortization expense of firm i in year t-1; EXAit-1 corresponds to the adjustment to fair value net of depletion expense of the biological assets of firm i in year t-1; and BAit denotes the biological assets of firm i in year t.

The adjustment proposed by Silva et al. (2015) is to consider the variation in the fair value net of the depreciation expense of biological assets, since the cash effect is not immediate. For a bearer plant with a long life cycle, many users of accounting information interested in predicting the company’s earnings may eliminate the variation in fair value because of the uncertainties in its calculation. As a result, the authors assume that there is a possibility of earnings management in the calculation of the variation in the fair value of biological assets, which justifies their occurrence in the adapted model of Kang and Sivaramakrishnan (1995).

3.4.1 Median tests

The first comparison was made between the discretionary accruals, which represent evidence of earnings management, and the disclosure score obtained from section 3.1 ‘Disclosure in the Notes to the Financial Statements’. Therefore, the companies were ranked according to their discretionary accruals. Next, the medians for the first and fourth quartiles were calculated. Then, we did the Mann-Whitney test to verify whether these medians are statistically different. According to Fávero et al. (2009), this is one of the most powerful non-parametric tests for two independent samples. The null hypothesis of the test affirms that there is no difference between the groups. The results were used to assess research hypothesis 5.

The second comparison was made between companies holding bearer plants and companies holding other biological assets. Therefore, the same test was used. The results were used to assess research hypothesis 6.

3.5 Analysts’ Opinion of the Quality of the Information on Biological Assets

In Brazil, over a period of less than ten years, the valuation of biological assets went through significant changes: initially valued at historical cost, they were then valued at fair value and, five years later, some of them returned to the historical cost. This whole process motivated a great amount of professional and academic discussion in Brazil and internationally.

Despite the benefits associated with the use of fair value, this measuring base may not be the most appropriate method for some biological assets. Market professionals and academic researchers raised questions about the compulsory use of fair value for all biological assets, as the expected economic benefit of these assets will be realised by their use, instead of their sale. In this context, IAS 41 established regulatory changes, determining that as from January 2016 these biological assets should again be measured based on their cost, being allocated as property, plant and equipment; thus, the intention was to reduce the subjectivity in the measuring of biological assets for which there was no intention to sell.

In this context, we investigated the opinion of information users, specifically those users with the technical knowledge to understand the accounting information, on the process and valuation of biological assets at fair value. In this regard, the role of market analysts is crucial, as they serve as intermediaries between the companies and the stakeholders. These professionals make predictions on companies’ future performance, to support investors’ decisions.

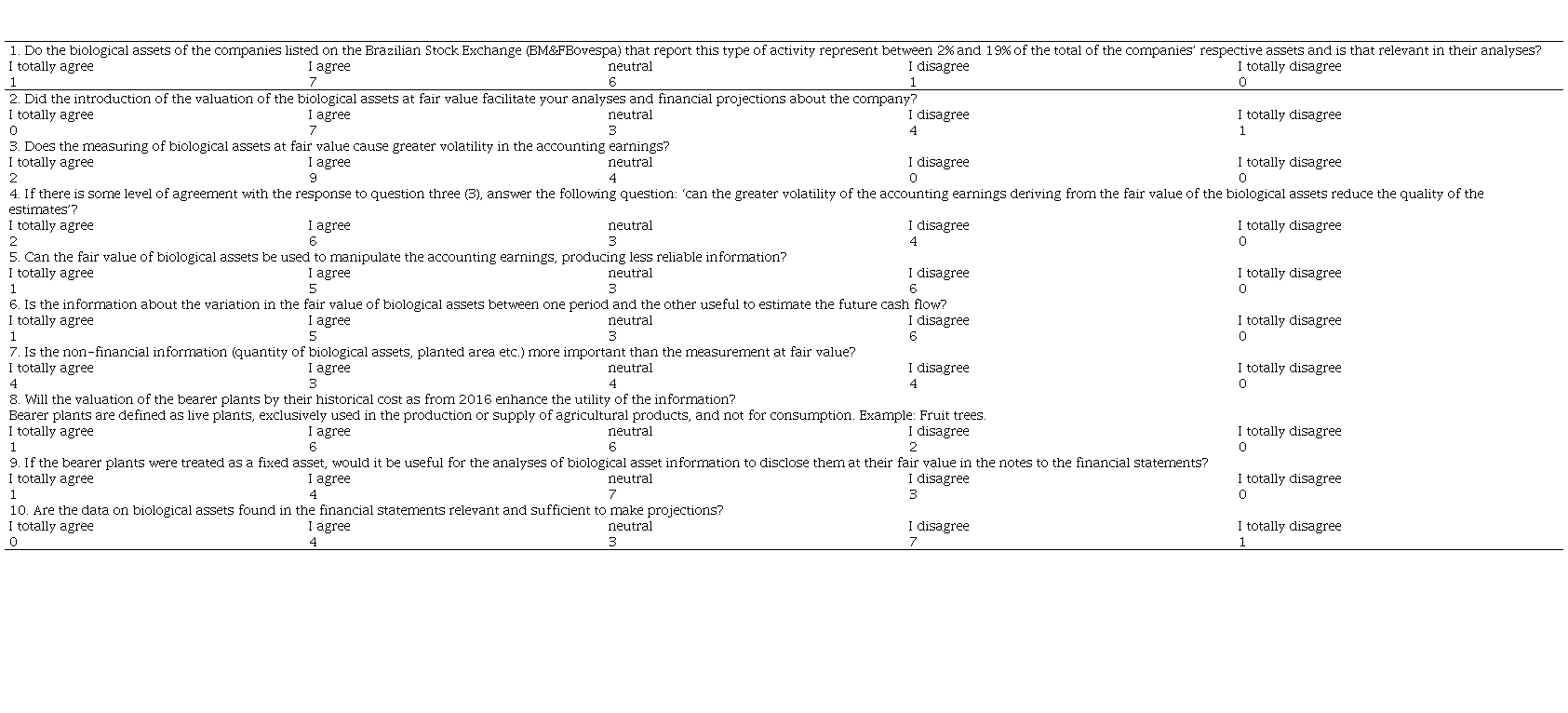

To put this phase into practice, we developed a Likert questionnaire to collect the market analysts’ answers to learn about their opinion regarding the disclosed information. Five options were provided, with scores of 5 points for the option ‘I totally agree’, 4 points for ‘I agree’, 3 points for ‘neutral’, 2 points for ‘I disagree’, and 1 point for ‘I totally disagree’.

We identified the analysts through the companies’ websites, under the section headed ‘Coverage of Analysts’, and, in addition, we searched for specialist email addresses. In total, 128 analysts were identified who covered companies with biological assets, and these analysts received the questionnaire by email address. Only 15 returned full answers, however, which is 9% of all the analysts who received the questionnaire.

The questionnaire used to assess the quality of accounting information is presented in Appendix 2. The results were used to assess research hypothesis 7.

3.6 Descriptive Statistics

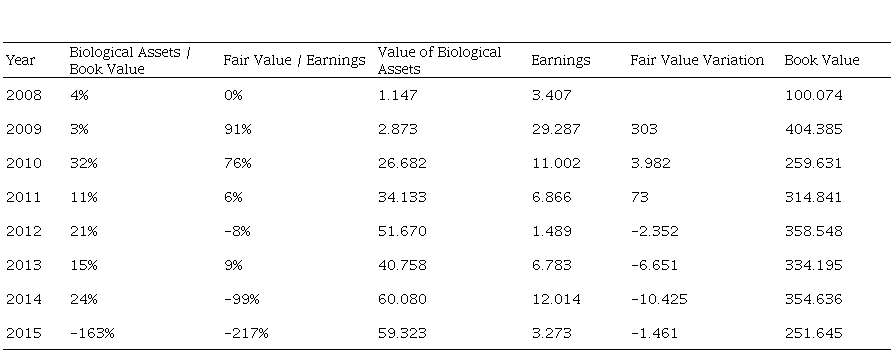

Descriptive statistics for the ratio of biological assets to book value, the ratio of fair value variation to earnings, the value of the biological assets, the earnings, the fair value variation and the book value are shown in table 4. All values represent the means of the total sample.

Descriptive Statistics

Source: developed by the authors.Note. the information was collected from notes of the financial statements. Amounts expressed in thousands of BRL (Brazilian Real).

The increase in biological assets can be explained in two ways. First, the full IFRS adoption started in Brazil in 2010, which explains the huge growth in 2010, because IAS 41 allows the fair value option for biological assets. Before the IFRS was adopted, the Brazil GAAP required only the historical cost for biological assets, which explains the large effect in 2010. Second, the average Brazilian GDP for the period 2008-2015 was 2.3%, which may explain why there is more investment by Brazilian companies, including companies with biological assets.

Regarding the ratio of biological assets to book value, there is an average increase over the period 2008-2014, consistent with the previous analysis. The figure of -163% for one year can be explained exclusively by the figures for Biosev, which presented negative equity because of accumulated losses from previous years.

The ratio of the fair value variation to earnings decreased on average over the period 2008-2015. To understand this reduction, we can analyse earnings and the fair value variation. The earnings are decreasing, on average, over the period studied, except for 2010, which corresponds to the initial IFRS adoption. There is empirical evidence that the first-time adoption of the IFRS implies increased net income (Fifield et al., 2011). On the other hand, the fair value variation shows a larger decrease, with negative values from 2012 to 2015 due to fair value losses for the analysed biological assets. We would like to highlight that the use of the fair value variation for biological assets began in 2010, and the 2009 income statement was released as required by IFRS 1 on First-time Adoption of International Financial Reporting Standards – see table 4. Finally, the ratio of the fair value variation to earnings of -217% for 2015 is explained by the figures for Celul Irani, which disclosed low earnings and a large and negative fair value variation.

4 ANALYSIS OF RESULTS

4.1 Disclosure in the Notes to the Financial Statements

The results show some shortfalls in the disclosure of the requirements of IAS 41, in line with Silva et al. (2013). We found a good disclosure for the first subgroup ‘Disclosure of gains and losses’. In 2014, 26 of the companies observed (87%) presented gains or losses in the value of their biological assets. As regards the subgroup ‘Characteristics of biological assets’, the weakest disclosure refers to the non-financial estimates of physical quantities. This information can be relevant for many analysts who cover these companies. Section 4.5 ‘Analysts’ Opinion of the Quality of Information on the Biological Assets’ will further illustrate the importance of this information.

The disclosure in the subgroup ‘Fair value’ also indicates a lack of information about the agricultural products harvested, as 33% of the companies disclosed information on this item in 2014, against an even worse result in 2012 of 7%. This result shows that the companies have not disclosed this information in accordance with IAS 41. The subgroup ‘Effect of changes’ reveals the composition of the reconciliation between the initial and final balances of the periods under analysis. The disclosure for this subgroup was not adequate[7] either. The best results for 2014 within this subgroup were for changes in the book value of the biological assets (73%), gain or loss deriving from the change in the fair value minus the sales expense (70%), and increases due to purchases (50%).

The final subgroup shows that disclosure for measuring at cost is extremely low – see “Maintenance of cost method” in Appendix 1. Although the disclosure for some items is weak, based on the results reported, the level of disclosure in the notes to the financial statements has improved from when we compare our results with Silva et al. (2013).

4.2 Value Relevance of Biological Assets

The coefficients were estimated using panel data, which is the most suitable method for testing the dynamics of changing relationships among variables (Fávero, 2013), and permits the size of the research sample to be expanded by crossing the dimensions of time and space or the individuals.

In short, the specification tests indicated fixed effects, and the residual analysis presented heteroscedasticity and self-correlation problems. The results are shown in table 5. In addition, a multicollinearity problem was verified through the Variance Inflation Factor (VIF) in model 3, and the exclusion of the Biological Assets (BA) variable allowed the correction of the problem.

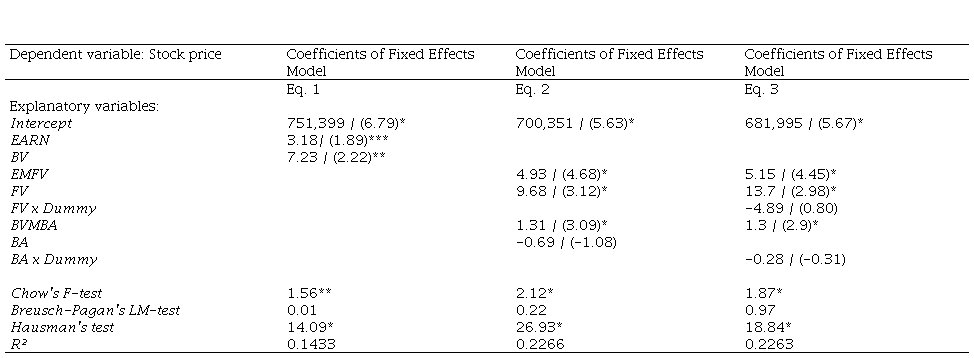

Value relevance models

Source: developed by the authors.Note. * 0.01; ** 0.05; *** 0.10 is the significance level. The coefficients were multiplied by 1 million to facilitate the presentation. Dummy is scored one (1) for companies with bearer plants and zero (0) for others; BVMBA corresponds to the book value of equity minus its biological assets; BA corresponds to the biological assets of company i in year t. The coefficients that are considered statistically significant are also significant in the economic sense.

Model 1 reveals relevant information for decision purposes, as the variables EARN and BV are statistically significant. However, the statistical significance of earnings is weak, consistent with studies concerning the value-relevance of accounting information in Brazil (Lopes, 2005). According to Lopes (2005), book values are expected to be relevant because of their implications for liquidity and debt covenants. Model 2, adopted to analyze the biological assets, shows that the accounting earnings without the effect of the fair value of the biological assets (EMFV) and the fair value variation (FV) are relevant for decision-making purposes, or, in other words, that the decomposition of the earnings can be more useful for investors than the earnings of the first model. In addition, the signs are positive and in accordance with table 3. The book value of equity without the effect of the biological assets (BVMBA) is value-relevant, while the biological assets variable (BA) is not statistically significant. These results, when compared to those for model 1, indicate that investors use the book value of equity without considering the effect of the biological assets.

One explanation for this relates to the doubts and uncertainties about the financial position of biological assets. To give an example, the companies Fibria and Klabin have extensive areas of growing forest, which will take many years to reach maturity. However, other variables beyond the management’s control can influence the expectations of the generation of cash flow by the biological assets, and consequently of the company value.

On the other hand, the fair value variation of the biological assets indicates value-relevant information, in view of the results for FV in model 2. This variation should reflect the future economic benefits, determined by the change measured for significant physical attributes. IAS 41 requires that attributes accepted in the market, for example, age or quality, are used for measuring fair value. IAS 41, paragraph 15, establishes that ‘an entity selects the attributes corresponding to the attributes used in the market as a basis for pricing’. This means that the simple growth of a biological asset can imply an increase in its market value, since growth is an attribute that analysts or investors take into account. This physical change is directly related to the calculation of the fair value variation, explaining the value-relevance of this information.

Nevertheless, this result cannot be extended to bearer plants, as the interaction between the bearer plants dummy and the variables FV and BA in model 3 is not statistically significant. This result does not allow us to assert that the information about bearer plants is value-relevant, supporting the opinion of market analysts who cover companies holding bearer plants (IFRS, 2019).

Therefore, this evidence confirms the market’s expectations about the effects of bearer plants on the value-relevance of accounting information. In that sense, the amendments in IAS 41 and IAS 16 can be useful for stakeholders, allowing access to higher-quality information while reducing the possibility of misleading or unreal information being produced. This result is in accordance with the studies by Gonçalves et al. (2017) and Huffman (2018).

4.2.1 Value-Relevance of Biological Assets: Additional Tests

We did some additional tests at this stage. Given that there are differences in corporate governance practices that affect shareholders’ rights (Chong & Lopez-De-Silanes, 2012), we believe that accounting practices can be used for opportunistic purposes rather than meeting the informational needs of stakeholders, as noted by Lopes and Walker (2012).

Therefore, we decided to work with the three levels of corporate governance existing in the Brazilian stock exchange. Brazilian companies may voluntarily participate in a particular corporate governance level after complying with the rules for that level. The characteristics of these three trading segments can be summarised as follows: i) Level 1 requires companies to adopt practices that favor better disclosure and access to information, by releasing more information than the minimum required by law, and maintaining more dispersed ownership, through a minimum free float of 25%; ii) Level 2 requires the company to comply with the Level 1 rules and other rules, such as the extension to all shareholders of common shares of the same rights as those obtained by the controllers upon the sale of control of the company, and the payment of at least 80% of this value to shareholders of preferred shares (tag-along rights), as well as the giving of voting rights to preferred shares; and iii) the Novo Mercado level has the same rules as Level 2 but only allows voting shares to be issued. Therefore, the Novo Mercado segment is the most rigorous in terms of governance, and Level 1 is the least rigorous.

We operationalize the models 1, 2 and 3 considering the different levels of corporate governance. A new variable was created, with four possible values: 1 for the traditional segment, which includes companies that do not participate in corporate governance levels; 2 for companies that adhere to Level 1 corporate governance; 3 for companies that participated in Level 2 corporate governance, and 4 for companies that have joined the Novo Mercado.

The next step was to repeat the tests; however, we did not find differences in relation to the previous results. Therefore, we decided not to report the results with the corporate governance variable.

4.3 Timeliness of Biological Assets

The specification tests here indicated fixed effects. After the specification and diagnostic tests, the results are displayed in table 6.

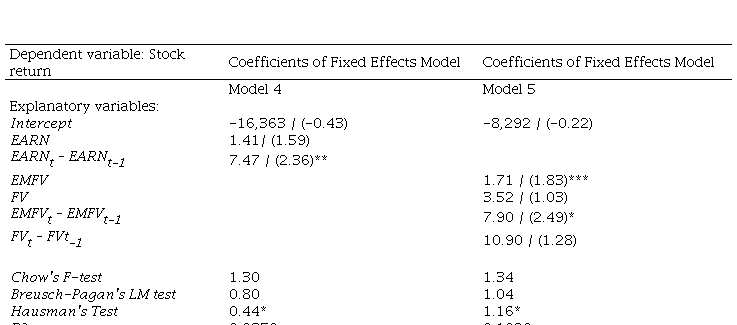

Timeliness models

Source: developed by the authors.Note. * 0.01; ** 0.05; *** 0.10 is the significance level. The coefficients were multiplied by 1 million to simplify the presentation. Ret indicates the stock return of company i in t, estimated based on the continuous capitalization method, permitting more robust results (Brooks, 2002). The earning variables are deflated by the price at t-1, to reduce scale problems.

The baseline model indicates that the accounting information, represented by the earnings, is timely, as the estimated coefficient for the variable (EARNt – EARNt-1) is statistically significant. In line with the Conceptual Framework, this means that information is available for decision-makers in time to be able to influence their decisions. Nevertheless, the adjusted model for the fair value variation of biological assets reveals the absence of timeliness. This result shows that the investors are not sensitive to the fair value variations of biological assets.

However, the disclosure of quarterly financial statements or market analysts’ predictions, based on different information sources, contributes to an anticipation of the fair value variation in the biological assets, which could explain this result.

Finally, the argument that the Brazilian capital market is not efficient also contribute to the explanation for this result: in this scenario, it can take some time for information to influence the behavior of investors. Therefore, a one-period lag was adopted for the earnings variable. After unreported additional tests, no changes were observed in the findings.

4.4 Earnings Management Analysis

4.4.1 Median test involving disclosure level between ‘high and low management’ subgroups

The results of the first test are displayed in table 7.

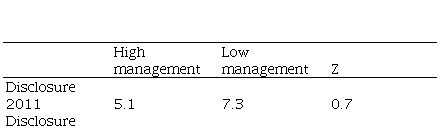

Median test for variation in disclosure between the subgroups ‘high earnings management’ and ‘low earnings management’

Source: developed by the authors.Note. * 0.01; ** 0.05; *** 0.10 is the significance level. The disclosure variables are obtained based on the checklist in section 3.1 ‘Disclosure in the notes to the financial statements’. The discretionary accruals, a proxy for earnings management, were estimated by the KS model; high discretionary accruals indicate the use of earnings management practices to produce accounting information that does not correspond to the company’s economic and financial reality.

The subgroups of companies with high and low earnings management present different median levels of disclosure, but the differences are only statistically significant for 2013 and 2014. This evidence is coherent with the hypothesis that companies with a low earnings management level tend to have better disclosure – that is, they have more transparent notes to the financial statements. In other words, companies that are more compliant with the disclosure requirements of IAS 41 and, therefore, that are more transparent, have lower earnings management.

These results cannot be extended to 2011 and 2012, indicating that the quality of the companies’ notes to their financial statements is the same for the two subgroups (companies with high and companies with low earnings management). The years 2010, 2011 and 2012 present very close and low disclosure scores, which is coherent with a learning period in the initial adoption of the IFRS (including IAS 41 for biological assets). For this reason, we believe that the learning effect may have influenced the application of the standards, reducing the quality of the financial reports.

4.4.2 Median test involving bearer plants

The results for the second test can be observed in table 8.

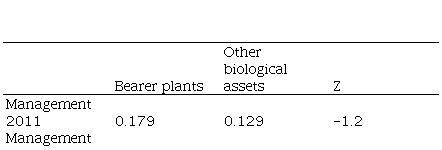

Median test for the variation in earnings management between the subgroups ‘bearer plants’ and ‘other biological assets’

Source: developed by the authors.Note. * 0.01; ** 0.05; *** 0.10 is the significance level.

The results show that there is no significant difference between the subgroups analyzed, going against the expectation of higher earnings management by companies with bearer plants. This expectation is based on some international studies that have investigated the application of IAS 41 regarding biological assets and agricultural products and have observed limitations arising from the use of the standard and the possibility of earnings management practices due to the lack of objective orientations (Herbohn, 2006; Pires & Rodrigues, 2008; Williams & Wilmshurst, 2009; Fisher et al., 2010).

The criticism of the subjectivity in the application of the fair value measure targets some particular biological assets, specifically those assets that are not grown for sale and that require a high dose of subjectivity in their measurement, such as bearer plants. The fair value of these biological assets, for which there is no active market, is measured using the discounted cash flow method, which can produce questionable outcomes because of the range of premises adopted.

In this study, we found empirical evidence of earnings management in the financial statement disclosures of companies holding biological assets. This result can be useful for standard-setters interested in assessing the earnings management and its implications for the quality of the financial statements. Nevertheless, no empirical evidence was found to support practices of earnings management for companies holding bearer plants.

4.5 Analysts’ Opinion of the Quality of the Information on Biological Assets

In short, for a considerable number of the respondents, the answers showed general agreement. Hence, these professionals were familiar with the relevance of biological assets, with their measurement at fair value, with the variation in the value between one period and another, with the impact on asset volatility and with the revised treatment of bearer plants.

Nevertheless, some respondents did not agree with the relevance of biological assets, and believed that they could not influence the valuation of the earnings, suggesting a lack of trust in the definition of fair value or a lack of knowledge of how it is used.

In short, there is no consensus in the analysts’ opinions, and nor is there a significant preponderance between the groups. This and other factors can explain the analysts’ preference for non-financial information on the fair value, and their search for other sources of information besides the financial statements. In addition, there is slight agreement on the lower quality of the information, the possibility of earnings management and the easy estimation of cash flow, indicating a clear division in the perception of the market analysts. Concerning bearer plants, some degree of agreement is observed for the valuation at historical cost. Despite the small number of respondents, the result is coherent with the other parts of this paper.

4.6 Synthesis of Findings

The findings can be summarised in table 9.

Synthesis of findings

Source: developed by the authors.

Appendix 1 shows the checklist that was used, based on the disclosure items of IAS 41. Despite observing an improvement in the disclosure of information about biological assets through the notes to the financial statements, plenty of room remains for improvement in the disclosures, such as the non-financial estimates of physical quantities, which are required by analysts. In addition, section 4.1 above shows that in most of the subgroups of the IAS 41 checklist there is poor disclosure, and this is not satisfactory. In general, the results allow us to conclude that the disclosure of accounting information following IAS 41 could improve, which supports research hypothesis 1: ‘the disclosure of biological assets in Brazil following IAS 41 is weak’.

The results for section 4.2 permit the partial acceptance of research hypothesis 2 as, although the variation in fair value is relevant for decision-making purposes, biological assets are not relevant – see table 5, model 2. Regarding bearer plants, the results from table 5 model 3 allow us to accept research hypothesis 3 and to conclude that ‘the variation in the fair value of bearer plants (Income Statement) and the measurement of bearer plants at fair value (Balance Sheet) are not relevant in the capital market context’.

Section 4.3 provides evidence that financial information is not timely, supporting the acceptance of H.: ‘the variation in the fair value of biological assets (Income Statement) is not timely in the capital market context’ – see table 6. The quarterly reports that anticipate much of the annual variation in the fair value can particularly explain this non-timeliness. Further, we found an association between earnings management and disclosure in 2013 and 2014, letting us accept H.: ‘companies with higher earnings management disclose less of the information required by IAS 41’ – see section 4.4 and table 7. On the other hand, we did not find evidence of any difference in earnings management between companies holding bearer plants and companies holding other kinds of biological asset. Therefore, we cannot accept H., and we conclude that earnings management is the same for all the companies in the sample – see section 4.4 and table 8.

Finally, the submission of the questionnaire to analysts was intended to assess market analysts’ need for information, with a view to presenting solutions to reduce the information asymmetry. However, the number of answers was small, which implies the need for a broader base of analysts able to answer the questionnaire in future studies. Anyway, the 15 analysts who responded to the questionnaire signalled the need to improve disclosure aspects, which implies more debate about IAS 41. Thus, we accept H.: ‘analysts do not consider the information of IAS 41 to be useful in their forecasts’.

Hence, for accounting to play its role in reducing information asymmetry, minimising conflicts of interest and contributing to a more suitable allocation of resources in the capital market, further discussions on IAS 41 should be encouraged, with a view to responding to accounts users’ information needs. To give some examples, should the standard provide more objective orientations on the accounting criteria, reducing the space for earnings management? What is the actual benefit of measuring bearer plants at historical cost? What information is valued by analysts and investors? This and other aspects could be further discussed in the academic sphere, and with companies, regulators and stakeholders.

5 CONCLUSIONS

Accounting standards naturally evolve in accordance with information users’ needs. In Brazil, after the adoption of the IFRS, a small number of companies started to adopt IAS 41, a standard focused on biological assets and agricultural products. IAS 41 required that Brazilian companies make greater use of fair value measurements in their balance sheets, besides other changes. Based on these changes and given possible mismatches between the interests of the agent and principal, founded on the agency theory, we raised the question of whether the quality of the financial information required by IAS 41 has increased.

In this sense, the reduction in the information asymmetry is noteworthy, and could encourage greater funding of agribusiness through the capital markets, with several positive effects on the economy, such as higher exports, more jobs and other economic and social implications. Because of the importance of the sector for the economy, the existence of alternative funding sources like the capital market is healthy.

In our study 33 Brazilian companies holding biological assets were investigated in five analysis sections: i) disclosure in the notes to the financial statements; ii) value relevance; iii) timeliness of information on the fair value; iv) earnings management; and v) analysts’ opinions of the quality of information on the biological assets.

The results for these five sections permit a partial acceptance of the research hypothesis, that is, that IAS 41 makes a reasonable contribution to the production of high-quality information in Brazilian companies’ financial statements. Overall, improvements can be observed in the disclosure of information on biological assets in the notes to the financial statements, offering relevant information for decision purposes, despite evidence that the financial information is not timely, and that there is earnings management associated with poor disclosure. Finally, analysts point to the need to improve certain disclosure aspects, which implies that more time must be spent discussing IAS 41.

Hence, for accounting to play its role in reducing information asymmetry, minimizing conflicts of interest and contributing to the more appropriate allocation of resources in the capital market, further discussion on IAS 41 should be encouraged, in order to respond to accounting users’ information needs.

Future studies could use three-monthly data to reduce the data spread. In addition, other models for the quality of accounting information could be applied to enhance the robustness of the results. In addition, because of the small number of respondents, a broader base of market analysts able to answer the questionnaire is recommended. Finally, more comprehensive results would be obtained from studies comparing countries that adopt the IFRS, with a view to explaining qualitative differences in the financial information.

REFERENCES

Anderson, C. W. (1999). Financial Contracting under Extreme Uncertainty: An Analysis of Brazilian Corporate Debentures. Journal of Financial Economics, 51(1), 45-84. https://doi.org/10.1016/S0304-405X(98)00043-9

Argilés, J. M, Garcia-Blandon, J., & Monllau, T. (2011). Fair Value Versus Historical Cost-Based Valuation for Biological Assets: Predictability of Financial Information.. Revista de Contabilidad – Spanish Accounting Review, 14(2), 87-113. https://doi.org/10.1016/S1138-4891(11)70029-2

Argilés, J. M., Miarons, M., Blandon, J. G., Benavente, C., & Ravenda, D. (2018). Usefulness of Fair Value Accounting of Biological Assets for Cash Flows Prediction. Spanish Journal of Finance and Accounting,47(2), 157-180. https://doi.org/10.1080/02102412.2017.1389549

Armstrong, C. S., Barth, M. E., Jagolinzer, A. D., & Riedl, E. J. (2010). Market Reaction to the Adoption of IFRS in Europe. Accounting Review, 85(1), 31-61. https://doi.org/10.2308/accr.2010.85.1.31

Baazaoui, H. & Zaraï, M. A. (2019). The Effect of Firm Characteristics on the Disclosure of IAS/IFRS Information: The Cases of Tunisia, France and Canada. International Business and Accounting Research Journal, 3(2), 124-153. http://dx.doi.org/10.15294/ibarj.v3i2.67

Ball, R. (2006). International Financial Reporting Standards (IFRS): Pros and Cons for Investors. Accounting and Business Research, International Accounting Policy Forum, 5-27. https://doi.org/10.1080/00014788.2006.9730040

Ball, R., Kothari, S. P., & Robin, A. (2000). The Effect of Institutional Factors on the Properties of Accounting Earnings. Journal of Accounting and Economics, 29(1), 1-51. https://doi.org/10.1016/S0165-4101(00)00012-4

Barth, M. (2018). The Future of Financial Reporting: Insights from Research. ABACUS, 54(1), 1-13. https://doi.org/10.1111/abac.12124

Barth, M., Landsman, W.R., & Lang, M. H. (2008). International Accounting Standards and Accounting Quality. Journal of Accounting Research, 46(3), 467-98. https://doi.org/10.1111/j.1475-679X.2008.00287.x

Barth, M. E., Li, K., & McClure, C. G. (2021). Evolution in value relevance of accounting information. Working paper, Stanford University, https://ssrn.com/abstract=2933197

Booth, B., & Walker, R. G. (2003). Valuation of SGARAs in the Wine Industry: Time for Sober Reflection. Australian Accounting Review, 13(3), 52-60. https://doi.org/10.1111/j.1835-2561.2001.tb00171.x

Bosch, J. M. A., Aliberch, A. S., & Blandón, J. G. (2012). A Comparative Study of Difficulties in Accounting Preparation and Judgment in Agriculture using Fair Value and Historical Cost for Biological Assets Valuation. Revista de Contabilidad, 15(1), 109-42. https://doi.org/10.1016/S1138-4891(12)70040-7

Brooks, C. (2002). Introductory Econometrics for Finance. Cambridge University Press, Cambridge.

Brown, S., Lo, K., & Lys, T. (1999). Use of R2 in Accounting Research: Measuring Changes in Value Relevance over the Last Four Decades. Journal of Accounting and Economics, 28(2), 83-115. https://doi.org/10.1016/S0165-4101(99)00023-3

Burgstahler, D. C., Hail, L., & Leuz, C. (2006). The Importance of Reporting Incentives: Earnings Management in European Private and Public Firms. Accounting Review, 81(5), 883-1016. https://doi.org/10.2308/accr.2006.81.5.983

Chalmers, K., Clinch, G., & Godfrey, J. M. (2011). Change in Value Relevance of Accounting Information upon IFRS Adoption: Evidence from Australia. Australian Journal of Management, 36(2), 151-173. https://doi.org/10.1177/0312896211404571

Chen, B., Kurt, A. C., & Wang, I. G. (2020). Accounting comparability and the value relevance of earnings and book value. Journal of Corporate Accounting & Finance, 31(4), 82-98. https://doi.org/10.1002/jcaf.22459

Chong, A., & Lopez-De-Silanes, F. (2012). Corporate Governance in Latin America. Research Department Working Paper Series. Washington: Inter-American Development Bank, 2007. Available at: https://pdfs.semanticscholar.org/7d05/e407a17e5ebe6d2903769035b5aeb5c0aee1.pdf, accessed 29 August 2019.

Christensen, H. B., Hail, L., & Leuz, C. (2013). Mandatory IFRS Reporting and Changes in Enforcement. Journal of Accounting and Economics, 56(3), 147-177. https://doi.org/10.1016/j.jacceco.2013.10.007

Confederação da Agricultura e Pecuária do Brasil - CNA (2023). Após Alcançar Patamar Recorde em 2021, PIB do Agronegócio Recua 4,22% em 2022. Available at: https://www.cepea.esalq.usp.br/upload/kceditor/files/PIB-DO-AGRONEGOCIO-2022.17MAR2023(1).pdf.

Daly, A., & Skaife, H. A. (2016). Accounting for Biological Assets and the Cost of Debt. Journal of International Accounting Research, 15(2), 31-47. https://doi.org/10.2308/jiar-51335

Damian, M. I., Manoiua, S. M., Bonaci, C. G., & Strouhal, J. (2014). Bearer Plants: Stakeholders’ View on the Appropriate Measurement Model. Accounting and Management Information Systems, 13(4), 719-738.

Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting Earnings Management. The Accounting Review, 70(2), 193-225. https://www.jstor.org/stable/248303

Dvorakova, D. (2006). Application of Fair Value Measurement Model in IAS 41 – Relation between Fair Value Measurement Model and Income Statement Structure, European Financial and Accounting Journal, 1(2), 49-70.

Easton, P. D. (1999). Security Returns and the Value Relevance of Accounting Data. Accounting Horizons, 13(4), 399-412. https://doi.org/10.2308/acch.1999.13.4.399

Eilifsen, A., Hamilton, E. L., & Messier Jr., W. F. (2021). The importance of quantifying uncertainty: Examining the effects of quantitative sensitivity analysis and audit materiality disclosures on investors’ judgments and decisions. Accounting, Organizations and Society, 90, 101169. https://doi.org/10.1016/j.aos.2020.101169

Fávero, L. P. L. (2013). Panel data in accounting and finance: theory and application. BBR - Brazilian Business Review, 10(1), 131-156. https://doi.org/10.15728/bbr.2013.10.1.6

Fávero, L. P., Silva, F. L., Belfiore, P., & Chan, B. (2009). Análise de Dados: modelagem multivariada para tomada de decisões [Data Analysis: Multivariate Modeling for Decision Making], Elsevier, Rio de Janeiro.

Fifield, S., Finningham, G., Fox, A., Power, D., & Veneziani, M. (2011). A Cross-country Analysis of IFRS Reconciliation Statements. Journal of Applied Accounting Research, 12, (1), 26-42. https://doi.org/10.1108/09675421111130595

Fisher, R., Mortensen, T., & Webber, D. (2010). Fair Value Accounting in the Agricultural Sector: An Analysis of Financial Statement Preparers’ Perceptions Before and After the Introduction of IAS 41 Agriculture. In: Accounting & Finance Association of Australia and New Zealand – AFAANZ, 2010, Christchurch, New Zealand. Available at: http://www.afaanz.org/openconf/2010/modules/request.php?module=oc_program&act ion=view.php&id=57, accessed 25 January 2012.

Georgiou, O., Mantzari, E., & Mundy, J. (2021). Problematising the decision-usefulness of fair values: empirical evidence from UK financial analysts. Accounting and Business Research, 51(4), p.307-346. https://doi.org/10.1080/00014788.2020.1814687

Goh, C., Lim, C. Y., Ng, J., Pan, G., & Yong, K. O. (2021). Trust in Fair Value Accounting: Evidence from the Field. Journal of International Accounting Research, v.20, n.3, p.21-42. https://doi.org/10.2308/JIAR-2021-034

Gonçalves, R., Patrícia, L., & Craig, R. (2017). Value-Relevance of Biological Assets under IFRS. Journal of International Accounting, Auditing and Taxation, 29, 118-126. https://doi.org/10.1016/j.intaccaudtax.2017.10.001

He, L. (2020). Discount rate behaviour in fair value reporting. Journal of Behavioral and Experimental Finance, 28, 100386. https://doi.org/10.1016/j.jbef.2020.100386

He, Y. L., Wright, S., & Evans, E. (2018). Is fair value information relevant to investment decision making: Evidence from the Australian agricultural sector? Australian Journal of Management, 43(4), 1-20. https://doi.org/10.1177/0312896218765236

Healy, P. M. (1985). The effect of bonus schemes of accounting decisions. Journal of Accounting and Economics, 7(1-3), 85-107. https://doi.org/10.1016/0165-4101(85)90029-1

Herbohn, K. (2006). Accounting for SGARAs: A Stocktake of Accounting Practice before Compliance with AASB 141 Agriculture. Australian Accounting Review, 16(39), 62-76. https://doi.org/10.1111/j.1835-2561.2006.tb00361.x

Hinke, J., & Stárová, M. (2014). The Fair Value Model for the Measurement of Biological Assets and Agricultural Produce in the Czech Republic. Procedia Economics and Finance, 12, 213-220. https://doi.org/10.1016/S2212-5671(14)00338-4

Holthausen, R. W. (2009). Accounting Standards, Financial Reporting Outcomes and Enforcement. Journal of Accounting Research, 47(2), 447-458. https://www.jstor.org/stable/25548027

Hsu, A. W., Liu, S., Sami, H. & Wan, T. (2019). IAS 41 and stock price informativeness. Asia-Pacific Journal of Accounting & Economics, 26(1-2), 64-89. https://doi.org/10.1080/16081625.2019.1545928

Huffman, A. (2018). Matching Measurement to Asset Use: Evidence from IAS 41. Review of Accounting Studies, 24(4), 1274-1314.

International Financial Reporting Standards (IFRS). Exposure Draft ED/2013/8. Agriculture: Bearer Plants Proposed Amendments to IAS 16 and IAS 41. http://kjs.mof.gov.cn/zhengwuxinxi/gongzuotongzhi/201307/P020130719334708700118

IFRS Foundation. (2021a). International Financial Reporting Standard 13 Fair Value Measurement. London E14 4HD, UK. https://www.ifrs.org/issued-standards/list-of-standards/ifrs-13-fair-value-measurement/#standard

IFRS Foundation. (2021b). International Accounting Standard 41 Agriculture. London E14 4HD, UK. https://www.ifrs.org/issued-standards/list-of-standards/ias-41-agriculture/#standard

Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics, 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

Jensen, M., & Meckling, W. H. (1994). The Nature of Man, Journal of Applied Corporate Finance, 7(2), 4-19. https://doi.org/10.1111/j.1745-6622.1994.tb00401.x

Jo, H., & Kim, Y. (2007). Disclosure frequency and earnings management. Journal of Financial Economics, 84(2), 561-590. https://doi.org/10.1016/j.jfineco.2006.03.007

Jones, J. J. (1991). Earnings management during import relief investigations. Journal of Accounting Research, 29(2), 193-228. https://doi.org/10.2307/2491047

Kang, S., & Sivaramakrishnan, K. (1995), Issues in Testing Earnings Management and an Instrumental Variable Approach. Journal of Accounting Research, 33(2), 353-367. https://doi.org/10.2307/2491492

Kothari, S. P., & Zimmerman, J. L. (1995). Price and return models. Journal of Accounting and Economics, 20(2), 155-192. https://doi.org/10.1016/0165-4101(95)00399-4

Kwon, S. H., & G. Wang. (2020). The change in the value relevance of accounting information after mergers and acquisitions: Evidence from the adoption of SFAS 141(R). Accounting & Finance, 60(3), 2717-57. https://doi.org/10.1111/acfi.12411

La Porta, R., Lopez-De-Silanes, F., Shleifer, A., & Vishny, R. (1997). Legal Determinants of External Finance. Journal of Finance, 52(3), 1131-1150. https://doi.org/10.1111/j.1540-6261.1997.tb02727.x

Lobo, G. J., & Zhou, J. (2001). Disclosure quality and earnings management. Asia-Pacific Journal of Accounting & Economics, 8(1), 1-20. https://doi.org/10.1080/16081625.2001.10510584

Lopes, A. B. (2005). Financial Accounting in Brazil: An Empirical Examination. Latin American Business Review, 6(4), 45-68. https://doi.org/10.1300/J140v06n04_03

Lopes, A. B., & Alencar, R. C. (2010). Disclosure and Cost of Equity Capital in Emerging Markets: The Brazilian Case. The International Journal of Accounting, 45(4), 443-464. https://doi.org/10.1016/j.intacc.2010.09.003

Lopes, A. B., & Walker, M. (2012). Asset Revaluations, Future Firm Performance and Firm Level Corporate Governance Arrangements: New Evidence from Brazil. British Accounting Review, 44(2), 53-67. https://doi.org/10.1016/j.bar.2012.03.007

Martinez, A. L. (2001). Gerenciamento dos resultados contábeis: estudo empírico das companhias abertas brasileiras [Earnings Management: An Empirical Study of Brazilian Public Companies]. (Doctoral Dissertation in Accountancy, University of Sao Paulo).

Moutinho, R. A. (2022). Association between accounting for biological assets and the cost of debt for the firms in the global economy: impact of theimplementation of amended IAS 41 (Masters Dissertation, Universidade de São Paulo). Repositório USP. https://doi.org/10.11606/D.96.2022.tde-28112022-173324

Oliveira, D. L. & Nakao, S. H. (2021). O que temos de pesquisa sobre ‘mensuração de ativos biológicos’ em 20 anos da IAS 41 – Agriculture? Custos e @gronegócio on line, 17(4), 256-298. http://www.custoseagronegocioonline.com.br/numero4v17/OK%2014%20ativos.pdf

Pires, A. M. M., & Rodrigues, F. J. P. A. (2008). Necessidade de adaptar e ajustar a Ias 41 ao sector agrícola português [The Need to Adapt and Adjust IAS 41 to the Portuguese Agriculture Sector]. Revista Universo Contábil, 4(1), 126-140. http://dx.doi.org/10.4270/ruc.20084

Rech, I. J., & Pereira, I. V. (2012). Valor justo: análise dos métodos de mensuração aplicáveis aos ativos biológicos de natureza fixa [Fair Value: An Analysis of Measurement Methods Applicable to Fixed Biological Assets]. Custos e @gronegócio online, 8(2), 131-57. http://www.custoseagronegocioonline.com.br/numero2v8/valor.pdf

Silva, R. L. M., Figueira, L. M., Pereira, L. T. O. A., & Ribeiro, M. S. (2013). CPC 29: Uma Análise dos Requisitos de Divulgação entre Empresa de Capital Aberto e Fechado do Setor de Agronegócios [CPC 29: An Analysis of the Requirements for Disclosure between Private and Public Firms in the Agribusiness Sector]. Sociedade, Contabilidade e Gestão, 8(1), 26-49. https://doi.org/10.21446/scg_ufrj.v8i1.13281

Silva, R. L. M., Nardi, P. C. C., & Ribeiro, M. S. (2015). Earnings Management and Valuation of Biological Assets. Brazilian Business Review, 12(4), 1-27. https://doi.org/10.15728/bbr.2015.12.4.1

Silva, R. L. M., & Nardi, P. C. C. (2018). The (in) Difference between Historical Cost and Fair Value for Biological Assets: A Cross-Country Study. Annual Meeting of the American Accounting Association, 2018, Washington, DC.

Silva, R. L. M., Nardi, P. C. C., Mendes, G. S., & Oliveira, D. de L. (2022). Dissecando a mensuração da cana-de-açúcar a valor justo: buscando melhorias na informação contábil. Custos e @gronegócio online, 18(1), 187-211. http://www.custoseagronegocioonline.com.br/numero1v18/OK%209%20cana.pdf

Souza, M P. R., & Shikida, P. R. A. (2021). Impact of Amendments to IAS 16 and IAS 41 on the Economic-Financial Position of Brazilian Sugar-Energy Companies. Journal of Accounting, Management and Governance, 24(1), 92-108. http://dx.doi.org/10.51341/1984-3925_2021v24n1a6

Soderstrom, N. S., & Sun, K. J. (2007). IFRS Adoption and Accounting Quality: A Review. European Accounting Review, 16(4), 675-702. https://doi.org/10.1080/09638180701706732

Walker, M. (2010). Accounting for Varieties of Capitalism: The Case Against a Single Set of Global Accounting Standards. British Accounting Review, 42(3), 137-152. https://doi.org/10.1016/j.bar.2010.04.003

Watts, R. L., & Zimmerman, J . L. (1986). Positive Accounting Theory. Prentice-Hall, New Jersey.

Watts, R. L., & Zimmerman, J. L. (1990). Positive Accounting Theory: A Ten Year Perspective. The Accounting Review, 65(1), 131-56. https://www.jstor.org/stable/247880

Williams, B. R., & Wilmshurst, T. (2009). The Achievability of Sustainable Reporting Practices in Agriculture, Corporate Social Responsibility and Environmental Management, 16(3), 155-166. https://doi.org/10.1002/csr.190

Zéghal, D., Chtourou, S., & Sellami, Y. M. (2011). An Analysis of the Effect of Mandatory Adoption of IAS/IFRS on Earnings Management, Journal of International Accounting. Auditing and Taxation, 20(2), 61-72. https://doi.org/10.1016/j.intaccaudtax.2011.06.001

APPENDIX 1

Checklist based on the disclosure items of IAS 41

Source: developed by the authors.

APPENDIX 2

Questions used in the questionnaire, and analysts’ answers

Source: developed by the authors.

Notes