Artigos

OPTIMIZING REGIONAL GOVERNMENT BUDGET ABSORPTION THROUGH PLANNING, HUMAN RESOURCES QUALITY, AND INFORMATION TECHNOLOGY SUPPORT

Putri Ayu Sholihat putriayusolihat1@gmail.com

Putri Ayu Sholihat putriayusolihat1@gmail.com

Yesi Mutia Basri yesimutiabasri@lecturer.unri.ac.id

Nasrizal Nasrizal nasrizal@lecturer.unri.ac.id

Yesi Mutia Basri yesimutiabasri@lecturer.unri.ac.id

Nasrizal Nasrizal nasrizal@lecturer.unri.ac.id

OPTIMIZING REGIONAL GOVERNMENT BUDGET ABSORPTION THROUGH PLANNING, HUMAN RESOURCES QUALITY, AND INFORMATION TECHNOLOGY SUPPORT

Revista Catarinense da Ciência Contábil, vol. 24, pp. 1-18, 2025

Conselho Regional de Contabilidade de Santa Catarina

Esta obra está bajo una Licencia Creative Commons Atribución 4.0 Internacional.

Recepción: 10 Mayo 2025

Revisado: 30 Julio 2025

Aprobación: 26 Agosto 2025

Publicación: 19 Septiembre 2025

Abstract: This research investigates the effects of budget planning and HR quality on budget absorption, considering the role of information technology as a moderator. The research was conducted across 32 Regional Apparatus Organizations (OPDs) in Kampar Regency using a census method, involving key stakeholders Including Budget Users, Finance Heads, Treasurers, and Technical Activity Executors. Data collection was conducted using structured questionnaires, followed by analysis through multiple linear regression and MRAThe results demonstrate that both effective budget planning and high-quality HR significantly enhance budget absorption. Furthermore, the utilization of information technology not only exerts a direct positive effect but also moderates and strengthens the influence of both planning and HR quality on budget absorption. The findings support integrating the Technology Acceptance Model (TAM) and the Unified Theory of Acceptance and Use of Technology (UTAUT) as a framework for public sector budgeting, emphasizing both behavioral and structural aspects of digital tool adoption. Theoretically, the study extends TAM and the Resource-Based View (RBV) by positioning information technology as a strategic enabler that enhances organizational performance. Practically, it provides actionable insights for regional governments to align planning, human capital, and digital transformation in pursuit of more accountable and effective fiscal management.

Keywords: Budget Planning, Human Resource Quality, Budget Absorption, Information Technology, TAM, UTAUT, Public Financial Management.

1 INTRODUCTION

Budget realization serves as an important indicator in assessing implementation performance, while also representing a fundamental component of financial accountability reported in the Government Agency Performance Accountability Report. According to the Regulation of the Minister of Finance (PMK) No. 158/PMK.02/2014, ministries and institutions are required to achieve a minimum budget absorption rate of 95 percent, which functions as the basis for granting rewards or imposing sanctions related to budget execution.

In Indonesia, the issue of low budget realization recurs nearly every year, affecting both ministries/agencies (K/L) and local governments, raising concerns about the effectiveness of public expenditure and delays in program implementation (World Bank, 2020). It affects the slow realization of the budget for the implementation of programs and activities stated in the budget implementation document (Hadiwijoyo & Anisa, 2019).

Budget absorption has a significant influence on driving economic growth (Mardiasmo, 2018). Each government institution is required to manage its spending effectively to maintain operational continuity and to facilitate the achievement of development objectives. One of the local governments that experienced the phenomenon of delayed budget absorption is Kampar Regency. As one of the oldest and strategically located regencies in Riau Province, Kampar serves as a critical administrative and economic hub in the region. However, this potential has not yet translated into optimal financial governance, as reflected in repeated underperformance in budget absorption. The budget and realization of the Kampar Regency Government for 2016-2021 can be seen on the following page:

| Year | Budget Ceiling(Rp) | Realization(Rp) | % |

| 2016 | 2,550,025,390,123 | 2,360,507,515,750 | 92.57% |

| 2017 | 2,421,154,921,809 | 2,232,826,396,846 | 92.22% |

| 2018 | 2,323,932,027,652 | 2,168,293,382,294 | 93.30% |

| 2019 | 2,891,698,863,104 | 2,551,135,143,694 | 88.22% |

| 2020 | 2,683,397,332,583 | 2,497,886,793,719 | 93.09% |

| 2021 | 2,647,390,998,717 | 2,462,013,633,916 | 92.99% |

The percentage of budget absorption indicates a low level of budget absorption, even though budget absorption is expected to reach at least 95 percent each year (PMK Number 158/PMK.02/2014). This persistent under-absorption not only reflects inefficiencies in internal administrative mechanisms but also undermines the region’s fiscal contribution to broader development outcomes.

This phenomenon occurs in ministries/institutions (K/L) or local governments, leading to disproportionate levels of budget absorption. The presence of a budget surplus (Silpa) that should be directed toward priority programs is frequently left unrealized, thereby undermining the effectiveness of fiscal policy in stimulating economic growth, delays in the implementation of government programs related to poverty alleviation, Postponements in executing economic and social stabilization programs, along with the year-end buildup of payment obligations, create inefficiencies and weaken government cash flow management.

The inability of government agencies to attain optimal budget absorption is often attributed to multiple determinants, particularly deficiencies in budget planning and the limited capacity of human resources. According to Mahmudi (2018), budget planning is the process of compiling work programs and activities supported by a budget in an organization. It is a systematic process in determining the appropriate budget that will be used as a basis for assessment by both public sector organizations and the government (Ramadhani & Setiawan, 2019). The budget planning stage is the key to successfully managing regional finances.

Despite its importance, recent international studies highlight persistent gaps between planning and actual execution in many developing countries. For instance, unrealistic projections, weak institutional coordination, and limited use of digital tools have been identified as key barriers to effective planning implementation (Schiavo-Campo, 2023; Oulasvirta & Rönkkö, 2023). Moreover, Valle-Cruz et al. (2020) emphasize that traditional planning mechanisms are often disconnected from real-time data and fail to adapt to dynamic fiscal conditions. These limitations are particularly pronounced in decentralized administrative settings, where local governments may lack the technical capacity or strategic alignment needed to translate plans into actual budget absorption (Purba, 2025). Therefore, empirical investigation is needed to explore how planning operates under such conditions and whether institutional and technological factors can help close the planning–execution gap.

Human resources also play a pivotal role in this process. Drawing on the Resource-Based View (RBV) framework (Barney, 1991), competent and accountable civil servants constitute valuable, rare, inimitable, and non-substitutable (VRIN) assets in achieving organizational goals. The quality of human capital, measured in terms of technical skills, integrity, and adaptability, significantly affects the efficiency and timeliness of budget execution. While empirical studies such as Imelda et al. (2022), Fitriyani et al. (2022), and Norawati et al. (2024) confirm the positive influence of HR quality on budget absorption, other research (e.g., Rifai et al., 2016) report insignificant effects, highlighting the need to consider additional contextual or enabling variables.

Although budget planning and HR quality have been widely studied, the findings remain mixed. For instance, Astuti and Fadjarenie (2024), Basri et al. (2021), and Hutagalung et al. (2024) found a significant positive effect on budget absorption, whereas Indriani (2016) and Rifai et al. (2016) reported contradictory results. This inconsistency may be attributed to differences in research context, administrative structure, digital infrastructure, and institutional capacity, Highlighting the need to explore moderating variables that may condition the strength of these relationships.

One such variable is the use of information technology. In recent years, the Indonesian government has accelerated the digitization of public services through the implementation of the Electronic-Based Government System (SPBE), as mandated by Government Regulation No. 12/2019. While digital platforms provide opportunities to enhance transparency, efficiency, and real-time monitoring, their effectiveness depends on several organizational factors, including digital literacy, infrastructure readiness, and user engagement (OECD, 2021).

In exploring the behavioral aspects of technology utilization, this research employs the Technology Acceptance Model (TAM) introduced by Davis (1989), which argues that perceived usefulness and perceived ease of use determine an individual’s intention to adopt a system. Nevertheless, the model’s emphasis on individual-level factors constrains its relevance in public sector bureaucracies, where decision-making is strongly shaped by organizational structures and social dynamic. Accordingly, this research adopts the Unified Theory of Acceptance and Use of Technology (UTAUT) formulated by Venkatesh et al. (2003), which advances the TAM framework by incorporating additional constructs, including social influence, facilitating conditions, and performance expectancy—elements that are particularly relevant in hierarchical, compliance-based institutions such as regional governments.

Despite mandates to utilize digital systems in public financial management, disparities in adoption and effectiveness persist across local governments. Variations in leadership support, technical training, and integration with legacy systems often hinder the full realization of the full potential of technology in improving fiscal outcomes. This study therefore aims to examine not only the direct effects of budget planning and HR quality on budget absorption but also to test whether information technology moderates these relationships.

By centering on Regional Apparatus Organizations (OPDs) within Kampar Regency, this study provides contributions of both theoretical significance and practical relevance. Theoretically, it enhances the understanding of UTAUT and RBV within the context of public sector budgeting and digital transformation. Practically, it provides evidence-based insights for regional policymakers on how to leverage technology and strengthen internal capabilities to achieve more effective, transparent, and accountable budget management.

2 REVIEW OF LITERATURE AND CONCEPTUAL FRAMEWORK

2.1 Budget Planning

Budget Planning and Budget AbsorptionBudget planning plays a crucial role in ensuring effective and timely fiscal execution within public institutions. Mahmudi (2018) emphasizes that sound planning requires accuracy, stakeholder involvement, and compliance with regulations. In the Indonesian context, Ministerial Regulation PMK No. 158/PMK.02/2014 underscores the strategic importance of planning quality in supporting optimal budget realization.

Previous studies have consistently found that effective planning significantly enhances budget absorption performance (Astuti & Fadjarenie, 2024; Marsontio et al., 2022; Basri et al., 2021). However, other research indicates that planning alone is not sufficient. Indriani (2016) and Rifai et al. (2016) observed that even well-structured plans may fail to materialize if there is poor coordination or gaps in technical implementation at the operational level.

Schiavo-Campo (2023) and Valle-Cruz et al. (2020) explain that many developing countries experience a persistent planning–execution gap due to overestimated forecasts and limited horizontal integration among government units. Therefore, adaptive, and data-driven planning approaches are considered essential for improving budget execution outcomes.

2.2 Human Resource Quality

As a critical strategic asset, human capital plays a central role in shaping organizational effectiveness. The Resource-Based View (RBV), articulated by Barney (1991), emphasizes that long-term competitive advantage emerges from resources that are valuable, unique, and difficult to replicate, with skilled employees exemplifying such characteristic. Empirical research in the public sector supports this notion. Fitriyani et al. (2022) and Imelda et al. (2022) demonstrated that the competence and experience of civil servants are critical in facilitating accurate and timely implementation of public budgets. The effectiveness of public programs depends not only on technical capabilities but also on leadership quality, compliance awareness, and decision-making autonomy.

Nonetheless, Rifai et al. (2016) argue that human resource quality alone does not ensure performance improvements. In the absence of systemic support, such as ongoing training, performance incentives, and enabling work environments, the potential impact of human capital may remain unrealized.

2.3 Information Technology

Digital transformation has increasingly shaped public administration practices worldwide. In Indonesia, the adoption of electronic-based government systems (SPBE) reflects a broader effort to modernize public financial management through digitalization. According to OECD (2021) and UNDESA (2022), information technology (IT) can significantly enhance transparency, accountability, and service efficiency when effectively implemented.

From the perspective of budget administration, digital tools such as e-budgeting platforms, SIPD (Integrated Planning and Budgeting System), and e-Monev enhance data accuracy and decision tracking. Refitia (2025) and Aprina & Fitriasuri (2023) found that the effective use of IT systems contributes to improved fiscal outcomes by streamlining planning and reporting processes.

However, Andhika (2013) highlighted that resistance to change, low digital literacy, and inadequate infrastructure can undermine the potential benefits of technology. Thus, technology should not be viewed merely as a tool, but as an enabler that relies on organizational readiness and user engagement.

2.4 Theoretical Foundations: TAM, UTAUT, and RBV

Proposed by Davis (1989), the Technology Acceptance Model (TAM) posits that individuals are more likely to adopt a technology when they perceive it as useful and simple to use. Despite its roots in private-sector applications, TAM has gained wide acceptance in analyses of technology adoption across public sector organizations.

Venkatesh et al. (2003) expanded the TAM framework by developing the Unified Theory of Acceptance and Use of Technology (UTAUT), which combines factors including performance expectations, effort expectations, social influence, and enabling conditions. This model is particularly effective in explaining technology use within bureaucratic organizations.

In addition, the Resource-Based View (RBV) provides a theoretical foundation for understanding how internal capabilities—such as human capital—serve as core drivers of organizational performance. When integrated, TAM/UTAUT and RBV offer a comprehensive framework on how technology and human resources interact to influence public budgeting outcomes.

The reviewed literature confirms that budget planning, human resource quality, and information technology are key determinants of public sector budget absorption. While these variables have been studied individually, few studies have examined their interrelationships, particularly the moderating role of information technology in enhancing internal organizational capabilities.

To respond to this gap, this study investigates how planning, in combination with other factors, exerts its effects, HR quality, and IT utilization on budget absorption. In doing so, it contributes to both theory and practice by integrating TAM, UTAUT, and RBV to elucidate the dynamics of performance in local government budget execution.

2.5 Hypothesis Development

2.5.1 The Influence of Budget Planning on Budget Absorption

Budget planning functions as a strategic instrument in the allocation and utilization of public resources. Effective planning involves setting priorities, aligning programs with available budgets, and establishing implementation timelines that facilitate the timely execution of activities. According to Hadiwijoyo and Anisa (2019), inadequate planning practices, including the absence of a clear priority scale, often result in misalignment between budget allocations and actual implementation, which in turn hinders optimal budget absorption. When budget plans are underdeveloped or disconnected from operational programs, work execution suffers, and allocated funds may remain underutilized.

From a theoretical perspective, the normative approach in public finance (Ahmad & Jaelani, 2015) emphasizes that effective public spending begins with a well-defined policy plan. This approach highlights the importance of deliberate resource allocation to ensure that public expenditures generate maximum economic and social value. Planning is therefore not merely procedural, but central to achieving the outcomes envisioned in public service delivery.

Empirical evidence further supports this theoretical perspective. Several studies (Astuti & Fadjarenie, 2024; Basri et al., 2021; Hutagalung et al., 2024; Marsontio et al., 2022) consistently demonstrate a positive relationship between the quality of budget planning and the level of budget absorption. These findings indicate that when planning is participatory, timely, and aligned with institutional goals, it facilitates more effective and accountable budget execution.

H1: Budget planning exerts a positive and significant influence on budget absorption.

2.5.2 The Influence of Human Resource Quality on Budget Absorption

Human resources constitute a critical asset in any public organization, particularly in the management of regional finances. High-quality personnel—characterized by strong educational backgrounds, relevant training, technical competencies, and practical experience—are essential to ensure that financial procedures are implemented effectively and efficiently. According to Van Hiep (2021), the presence of qualified human resources enhances the professionalism and productivity of employees, enabling them to execute their duties in alignment with organizational objectives.

The importance of human resource quality is also supported by goal-setting theory, which emphasizes that the alignment of tasks with individual capabilities contributes to enhanced performance and the achievement of objectives . In the context of budget execution, skilled and competent personnel are more likely to understand budget mechanisms, comply with regulatory procedures, and make timely and accurate financial decisions—all of which facilitate higher levels of budget absorption.

Empirical studies corroboratethis theoretical linkage. Imelda et al. (2022), Fitriyani et al. (2022), and Norawati et al. (2024) found a significant positive relationship between human resource quality and the effectiveness of budget implementation in local government agencies. These findings indicate that without competent staff, budget absorption may be adversely affected due to delays, errors, or inefficiencies in execution.

H2: The quality of human resources has a positive and significant effect on budget absorption.

2.5.3 Budget Planning, Budget Absorption, and IT Moderation

The integration of information technology (IT) into public financial management has transformed budget planning practices . IT facilitates the systematic collection, processing, and reporting of financial data, allowing organizations to develop budgets that are more accurate, timely, and aligned with programmatic goals. By employing digital tools—such as e-budgeting platforms and integrated planning systems—budget planning can be streamlined, and the allocation of resources can be better monitored from formulation to realization and reporting stages.

Drawing on Davis’s (1989) TAM and Venkatesh et al.’s (2003) UTAUT, it is argued that perceptions regarding a system’s benefits and user-friendliness are central determinants of digital technology adoption within organizations. In the context of public sector budgeting, effective IT utilization can enhance decision-making quality, Minimizing procedural bottlenecks and enhancing transparency—both of which strengthen the role of budget planning as a key determinant of absorption performance.

Empirical studies have also demonstrated this moderating effect. Aprina and Fitriasuri (2023) found that IT utilization significantly strengthens the relationship between budget planning and budget absorption in regional apparatus organizations. Similarly, Refitia (2025) confirmed that organizations with higher levels of IT integration achieve more effective implementation of budget plans, resulting in improved budget realization.

H3: Information technology serves as a positive moderator in the association between budget planning and budget absorption.

2.5.4 Human Resource Quality and Budget Absorption: Evidence of Information Technology as a Moderator

Effective budget implementation is highly dependent on the quality of human resources, particularly in contexts where digital systems are integrated into financial management processes. Competent personnel with adequate digital literacy are better equipped to utilize information technology (IT) tools to streamline tasks, reduce errors, and ensure timely execution of financial procedures. As noted by Adhika et al. (2018) and Aditama & Widowati (2017), enhancing human resource capacity—especially regarding IT proficiency—supports more responsive and efficient budget absorption.

Aligned with this perspective, Government Regulation No. 12 of 2019 institutionalizes the integration of information technology in local governance, mandating the use of electronic-based mechanisms for regional financial management (Article 222). This regulatory framework underscores the importance of integrating IT systems not merely as tools, but as integral structures within which human resources operate.

The Technology Acceptance Model (TAM) and Unified Theory of Acceptance and Use of Technology (UTAUT) further reinforce that the effectiveness of technology depends not only on its availability but also on users’ ability and willingness to adopt it. In this sense, high-quality human resources are more likely to engage effectively with IT systems, thereby enhancing the efficiency and accuracy of budget processes.

Empirical research supports this interaction. Andhika (2013) and Adhika et al. (2018) found that IT utilization amplifies the positive impact of human resource competence on budget absorption, particularly in public sector organizations adopting digital systems.

H4: The utilization of information technology positively moderates the relationship between human resource quality and budget absorption.

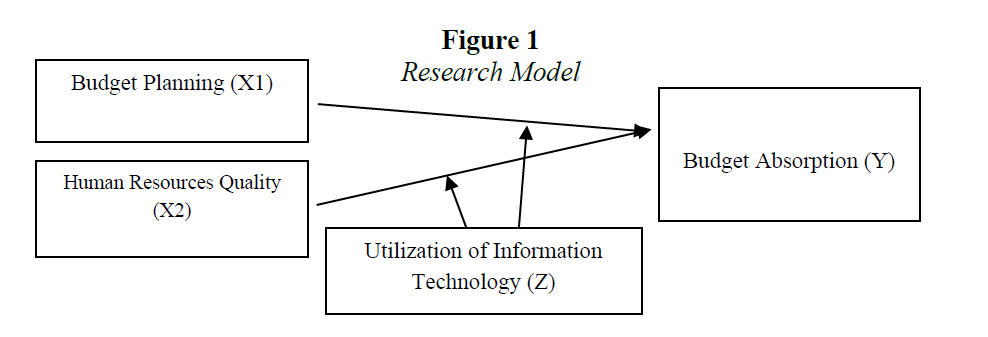

The following is a research model

Figure 1

Research Model

3 RESEARCH METHODS

The study applies a quantitative methodology through a survey-based design. The research population encompasses 32 Regional Apparatus Organizations (OPDs) in Kampar Regency, with saturated sampling employed to ensure that every unit of the population was represented in the sample. Participants comprise Budget Users/Authorized Budget Users, Heads of Finance, Treasurers, and Technical Activity Executors (PPTK) from each OPD.

The researcher distributed five questionnaires to each OPD, resulting in a total of 160 questionnaires across 32 Regional Apparatus Organizations. This approach aimed to capture diverse perspectives from key financial personnel responsible for budget execution.

This research employs quantitative primary data, obtained firsthand from respondents via structured questionnaires. The type of research conducted is descriptive and explanatory survey, designed to explain causal relationships among variables.

o ensure instrument validity, a pilot trial was administered to 15 respondents drawn from three OPDs before the primary data collection. This process was intended to verify the questionnaire’s clarity, ease of interpretation, and consistency, with pilot feedback serving as the basis for refining items and confirming validity.

3.1 Operational Variables

Budget absorption. Budget absorption refers to the extent to which allocated funds are utilized within a given period, typically assessed through budget realization at a specific point in time (budget realization)(Halim & Kusufi, 2014). Budget absorption is measured each year through budget absorption.

Budget planning involves the preparation of work programs and activities supported by an organization's budget (Mahmudi, 2018). It is assessed through several indicators, including alignment with organizational needs, compliance with regulations, minimization of administrative errors, clarity and ease of understanding, timeliness, and the degree of stakeholder participation.

The quality of human resources refers to the development of individuals through training and education programs aimed at enhancing professionalism and the skills required to optimally perform their duties and functions within an organization. It is measured using indicators such as skills, experience, competence, education, and training(Mocodompis, 2015).

Information technology involves the collection, processing, storage, and manipulation of data to produce high-quality information for decision-making purposes (Berisha-Shaqiri, 2014). The indicators measure the utilization of information technology: Having sufficient computers, Internet network, utilization of computer networks (LAN), Computerized accounting processes, Data processing using software, Integrated information systems, and Regular equipment maintenance schedules (Al-Hashimy et al., 2022)

3.2 Data Analysis Techniques

The analytical method employed consisted of multiple linear regression and moderation testing, carried out using SPSS version 24. The regression equation was developed to examine the proposed hypotheses, namely: (H1) the effect of budget planning on budget absorption, and (H2) the effect of human resource quality on budget absorption. Multiple regression analysis was employed, and the regression model applied in this study is expressed as follows:

Prior to executing the regression analysis, classical assumption testing was carried out, covering normality and multicollinearity diagnostics (using the VIF approach). These procedures were applied to confirm the model’s appropriateness for inferential analysis. Furthermore, the interaction effect was examined through Moderated Regression Analysis (MRA), which represents a specific form of multiple linear regression where the model incorporates interaction terms derived from the product of two or more independent variables (Ghozali, 2016). MRA is used for hypothesis testing 3 and 4

The MRA equation in this study is as follows:

H3 Y = α + β1X1 + ԑ

Y = α + β1X1 + β2Z1 + ԑ

Y = α + β1X1 + β2Z1 + β3X1*Z1 + ԑ

H4 Y = α + β1X2 + ԑ

Y = α + β1X2 + β2Z1 + ԑ

Y = α + β1X2 + β2Z1 + β3X2*Z1 + ԑ

Information :

Y = Budget Absorption

α = Constant

β1-β3 = Regression coefficient

X1 = Budget Planning

X2 = Quality of Human Resources

Z1 = Utilization of Information Technology

A significant β₃ coefficient in Model 3 indicates a moderating effect of information technology on the respective relationship. The increase in R² value from Model 2 to Model 3 is also used to assess the strength of the moderation effect (Ghozali, 2016).

4 RESEARCH RESULTS

Out of the 160 questionnaires distributed to respondents across 32 Regional Apparatus Organizations (OPDs) in Kampar Regency, 128 were completed and deemed valid for analysis. This represents a response rate of 80%, which is considered acceptable for survey-based research in public administration (Sekaran & Bougie, 2016).

4.1 Test Results Descriptive Statistics

The results of the descriptive statistical test can be seen in the following Table 2.

| N | Min | Max | Mean | Std. Deviation | |

| BudgetAbsorption (Y) | 128 | 2 | 5 | 4.08 | 0.66 |

| Budget Planning (X1) | 128 | 2 | 5 | 4.10 | 0.70 |

| Human Resources Quality (X2) | 128 | 2 | 5 | 4.01 | 0.54 |

| Utilization of IT (Z) | 128 | 3 | 5 | 4.13 | 0.57 |

4.2 Validity and Reliability Test Results

4.2.1 Budget Absorption Data Validity Test Results (Y)

Budget absorption in this study consists of 7 statement items. Table 3 shows the results of the budget absorption validity test.

| Statement Items | r |

| Budget Absorption (Y) | 0.319-0.499 |

| Budget Planning (X1) | 0.279-0.666 |

| Human Resources Quality (X2) | 0.366-0.583 |

| Utilization of IT (Z) | 0.355-0.636 |

Table 3 indicates that all statement items associated with the indicators surpass the threshold value of 0.1736 (r-table). This finding demonstrates that each indicator of the information technology utilization variable meets the statistical validity criteria and is therefore appropriate for use in the study.

4.3 Data Reliability Test Results

The purpose of the reliability test is to evaluate the stability and consistency of a measurement instrument, specifically to determine whether it produces consistent results when applied multiple times under varying conditions. This assessment employs the Cronbach’s alpha method to gauge the degree of trustworthiness of the instrument. Measurement results are considered consistent if the instrument yields similar outcomes when administered two or more times under the same conditions.

| Variables | Standard | Cronbach's Alpha |

| Absorption (Y) | 0.60 | 0.722 |

| Planning (X1) | 0.60 | 0.774 |

| Human Resources Quality (X2) | 0.60 | 0.834 |

| Utilization of IT (Z) | 0.60 | 0.791 |

As presented in Table 4, the Cronbach’s alpha coefficients for the instruments measuring budget absorption (Y), budget planning (X1), human resource quality (X2), and information technology utilization (Z) all exceed 0.60, indicating that these instruments are reliable.

4.4 Results of Normality Test

To ensure compliance with one of the classical linear regression assumptions, a normality test was performed to examine whether the regression residuals follow a normal distribution. The Kolmogorov–Smirnov (K–S) method was utilized for this purpose. Based on the Kolmogorov–Smirnov test results presented the Asymptotic Significance (2-tailed) value was 0.200, which is greater than the standard significance threshold of 0.05. This result indicates that the residuals do not deviate significantly from a normal distribution.

4.5 Results of Multicollinearity Test

Based on the multicollinearity test results, Budget Planning (X1) has a Tolerance of 0.465 and a VIF of 2.148, while Human Resources (X2) has a Tolerance of 0.344 and a VIF of 2.906. Since all Tolerance values are above 0.10 and VIF values are below 10, it can be concluded that multicollinearity is not present, and both independent variables can be reliably used in the regression analysis.

4.6 Hypothesis Testing Results

Table 5 displays the findings from the multiple linear regression test.

| Model | Unstandardized Coefficients | t | Sig. | ||

| B | Std. Error | ||||

| 1 | (Constant) | .328 | 1,421 | .231 | .818 |

| Budget Planning (X1) | .279 | .047 | 5.874 | .000 | |

| Human Resources Quality (X2) | .177 | .050 | 3.529 | .001 | |

According to the multiple linear regression results presented in Table 5, the hypothesis tests can be interpreted as follows: The effect of budget planning (X1) on budget absorption (Y) yields a t-value of 5.874, which exceeds the critical t-value of 1.979, with a p-value of 0.000 (<0.05). Given the positive t-value, Ho1 is rejected and Ha1 is accepted, indicating that budget planning has a significant and positive impact on budget absorption.

The regression results for the effect of HR quality (X2) on budget absorption (Y) provide a t-value of 3.529; this value is greater than the t table 1.979 with a P-value of 0.001 <0.05. The t value is positive. So Ho is rejected, and Ha is accepted, meaning that HR quality positively and significantly affects budget absorption.

4.7 Determination Coefficient Results

The model yields an adjusted R² of 0.760, meaning that 76% of the changes in budget absorption are attributable to budget planning, human resource quality, and organizational commitment, and 24% to other factors. The findings of the moderated regression analysis are presented in Table 6:

| Model | Unstandardized Coefficients | t | Sig. | ||

| B | Std. Error | ||||

| 1 | (Constant) | 13,663 | 5,806 | 2.353 | .020 |

| Budget Planning (X1) | .782 | .149 | 5.257 | .000 | |

| IT Utilization) | .784 | .180 | 4.345 | .000 | |

| X1.Z | .011 | .004 | 2.553 | .012 | |

Based on the regression model, the coefficient b2 is 0.00 (>0.05, not significant), while b3 is 0.012 (<0.05, significant). These results indicate that information technology functions as a quasi-moderator, acting simultaneously as a moderating and an independent variable. As shown in Table 5, the p-value for the interaction between budget planning and information technology (X1*Z) is 0.012 (<0.05), supporting H4. This demonstrates that the interaction between budget planning and information technology significantly influences budget absorption (Y), and the positive β implies that the use of information technology amplifies the relationship between budget planning and budget absorption

4.8 Hypothesis Test Results 5

The outcomes of the regression analysis incorporating a moderating variable are summarized in Table 7:

| Model | Unstandardized Coefficients | t | Sig. | ||

| B | Std. Error | ||||

| 1 | (Constant) | 11,711 | 3.390 | 3.455 | .001 |

| Human Resources Quality (X2) | .205 | .103 | 1.989 | .049 | |

| IT Utilization (Z) | .092 | .119 | .773 | .441 | |

| X2.Z | .006 | .003 | 2.022 | .045 | |

Based on the regression model, the coefficient b2 is 0.441 (>0.05, not significant), while b3 is 0.045 (<0.05, significant). These results suggest that information technology functions as a pure moderator, meaning it solely serves as a moderating variable. As presented in Table 5, the p-value for the interaction between human resource quality and information technology utilization (X2*Z) is 0.045 (<0.05), supporting H5. This indicates that the interaction between HR quality and information technology significantly affects budget absorption (Y). Furthermore, the positive β coefficient shows that information technology enhances the effect of HR quality on budget absorption.

5 DISCUSSION

5.1 The Effect of Budget Planning on Budget Absorption

The hypothesis testing results indicate that budget planning exerts a significant positive influence on budget absorption within the Regional Apparatus Organizations (OPDs) of Kampar Regency. This suggests that well-structured, participatory, and timely planning facilitates more efficient program implementation, resulting in increased budget utilization. Additionally, descriptive analysis reveals that planning practices across most OPDs have attained a relatively advanced level of maturity.

This finding is consistent with Heniwati (2023) who emphasize that effective planning determines the success of budget execution, serving as the foundation for all financial operations. In normative public finance theory, planning ensures efficient resource allocation that is aligned with institutional goals and public interest.

Moreover, these results are consistent with studies conducted by Astuti & Fadjarenie (2024), Basri et al. (2021), Hutagalung et al. (2024), and Marsontio et al. (2022). However, it is worth noting that Indriani (2016) reported insignificant results in a different context. Such discrepancies may be attributed to contextual variables, including the administrative discipline of local agencies, leadership commitment, and institutional capacity. This reinforces the need for a more nuanced understanding of how non-technical dimensions, such as political will or inter-agency coordination, shape budget performance.

5.2 The Effect of Human Resource Quality on Budget Absorption

The second hypothesis is also supported: the quality of human resources positively affects budget absorption. In Kampar Regency, skilled and experienced personnel appear to contribute significantly to the efficient execution of financial programs. As emphasized by the Resource-Based View (Barney, 1991), human capital is a strategic asset whose value lies in being valuable, rare, inimitable, and non-substitutable (VRIN).

This result is consistent with the findings of Imelda et al. (2022), Fitriyani et al. (2022), and Norawati et al. (2024), who all affirm that qualified civil servants enhance organizational capacity in public budgeting. However, a contradictory finding by Rifai et al. (2016) suggests that in contexts where bureaucratic procedures dominate or accountability is weak, HR competence alone may not ead to improved budget absorption. This implies that capacity must be matched with enabling systems and incentives to produce meaningful fiscal impact.

5.3 The Moderating Role of Information Technology on the Effect of Budget Planning

The third hypothesis reveals that information technology utilization strengthens the effect of budget planning on budget absorption. This underscores the enabling role of digital systems in enhancing the accuracy, speed, and traceability of financial planning. When supported by robust IT infrastructure, planning becomes more data-driven, facilitating the early detection of inefficiencies and the prompt reallocation of resources.

These findings are consistent with the Technology Acceptance Model (Davis, 1989), which asserts that perceived usefulness and ease of use play a critical role in shaping the intention to adopt a system. This conclusion is further supported by empirical evidence from Aprina & Fitriasuri (2023) and Refitia (2025), who reported that the integration of information technology improves planning effectiveness.

The contribution of this study lies in its empirical validation of IT as a moderating variable rather than a direct predictor, which is relatively underexplored in the context of local government budgeting. This represents a theoretical extension of TAM and provides new insight into the design of digital governance systems, particularly within subnational administrations.

5.4 The Moderating Role of Information Technology on the Effect of Human Resource Quality

Likewise, the fourth hypothesis demonstrates that information technology serves as a moderating factor in the relationship between human resource quality and budget absorption. This indicates that skilled personnel, when equipped with sufficient digital resources, are able to carry out budget implementation tasks more effectively and precisely.

This interaction supports the assertion in TAM and UTAUT (Venkatesh et al., 2003) that technological facilitation enhances individual performance. It also aligns with the findings of Andhika (2013) and Adhika et al. (2018), who emphasize that the interplay between digital competence and HR capability is essential in modern public sector finance.

Nonetheless, it is crucial to recognize that such synergies may not emerge in agencies with low digital literacy or underdeveloped IT systems. This limitation calls for future research to explore institutional digital readiness as a condition for maximizing the benefits of human capital in public budgeting.

This research adds to the existing literature by providing empirical evidence of information technology’s moderating role on two primary organizational factors influencing budget absorption: budget planning and human resource quality. While previous research has often examined these variables in isolation, this study presents a more integrated framework that better reflects the interconnected dynamics of digital-era public management.

Theoretically, this research expands the application of TAM/UTAUT and RBV frameworks to the study of fiscal performance at the subnational level. By framing human capital and digital infrastructure as interdependent resources, the study deepens our understanding of how these elements jointly affect budget absorption. Empirically, it stands out by situating the analysis within the real-world administrative context of Kampar Regency, where digital maturity and institutional capacity vary considerably.

Building on these theoretical and empirical foundations, the proposed model offers a new "subsidy" for public administration by integrating digital technology into the traditional performance management framework of local government budgeting. Rather than treating IT as a stand-alone input, the model emphasizes its role as an enabling factor that enhances the effectiveness of planning and human resources. It provides evidence-based justification for policymakers to invest not only in technical IT systems but also in human capital development and strategic planning reforms.

For local governments, this implies that digital transformation efforts must go beyond mere system procurement. Effective implementation requires comprehensive capacity building, change management, and continuous performance evaluation. In this context , the model serves not only as a diagnostic tool to identify performance gaps but also as a strategic roadmap for improving budget execution and advancing smart governance practices.

6 CONCLUSION

This research sought to investigate the impact of budget planning and human resource quality on budget absorption, while also exploring the moderating effect of information technology within local government institutions. The results indicate that effective budget planning significantly improves budget absorption, implying that structured and timely planning facilitates more efficient budget implementation. Additionally, the quality of human resources was found to positively affect budget absorption, highlighting the importance of employee competencies—including skills, experience, and training—in ensuring effective public financial management.

In addition, the study provides empirical evidence that information technology strengthens the effects of both budget planning and human resource quality on budget absorption. These findings confirm the role of IT not only as a support system but also as a strategic enabler that amplifies institutional capacity. When the aid of digital tools, planning becomes more data-driven, and personnel are better equipped to execute financial responsibilities effectively.

Theoretically, this study extends the Technology Acceptance Model (TAM) and the Resource-Based View (RBV) by positioning information technology as a moderating mechanism that enhances organizational performance in public budgeting. It further contributes to the literature on digital governance by presenting an integrated model that reflects the interdependence between planning, human capital, and IT systems.

Practically, the findings provide actionable insights for policymakers and local governments. To enhance budget absorption, public institutions should not only invest in planning capacity and human resource development but also prioritize the strategic adoption and integration of information technology. This includes building digital literacy, improving system infrastructure, and aligning IT use with performance targets.

This study is not without limitations. First, data were collected using self-administered questionnaires without triangulation through interviews or document analysis, which may introduce common method bias. Second, the research was conducted exclusively within the OPDs of Kampar Regency, which limits the generalizability of findings to other local governments or administrative contexts.

Future research is encouraged to adopt a mixed-method approach, combining quantitative and qualitative techniques to provide a more comprehensive understanding of budget absorption dynamics. In addition, expanding the sample to include multiple regions or comparative case studies would enhance the robustness and generalizability of the model. Ensuring higher response rates and more closely monitoring the data collection process may also improve the quality of empirical insights.

REFERENCES

Adhika, V. N. M., Gede, W. M., Dwija, P. I. A., & Dharma, S. I. (2018). The effect of information technology Usage on the relationship between budget planning, human resources competency, and budgetary implementation at State University in Bali, Indonesia. Russian Journal of Agricultural and Socio-Economic Sciences, 79(7), 182–194. https://doi.org/10.18551/rjoas.2018-07.20

Aditama, P. B., & Widowati, N. (2017). Analisis Kinerja Organisasi Pada Kantor Kecamatan Blora. Journal of Public Policy and Management Review, 6(2), 283–295. https://doi.org/10.14710/jppmr.v6i2.15994

Ahmad, A., & Jaelani, A. (2015). Kemampuan Spasial: Apa dan Bagaimana Cara Meningkatkannya? Jurnal Pendidikan Nusantara Indonesia, 1(1), 1–13.

Al-Hashimy, H. N. H., Said, I., Yusof, N., & Ismail, R. (2022). Evaluating the impact of computerized accounting information system on the economic performance of construction companies in Iraq. Informatica, 46(7). https://doi.org/10.31449/inf.v46i7.3920

Andhika, F. P. (2013). Pengaruh Kepemimpinan dan Inovasi terhadap Kualitas Kinerja organisasi. Journal of Chemical Information and Modeling, 53(9), 1689–1699. https://www.academia.edu/35593723/Pengaruh_Kepemimpinan_dan_Inovasi_Terhadap_Kualitas_Kinerja_Organisasi

Aprina, A., & Fitriasuri, F. (2023). The Effect Of Budget Planning, Administrative Recording, Utilization Of Information Technology, Human Resources And Organizational Commitment On The Absolute Of The State Budget In The Ministry Of Finance In South Sumatra Province. Jurnal Ekonomi, 12(04), 182–190. https://ejournal.seaninstitute.or.id/index.php/Ekonomi/article/view/2753

Astuti, E. Y., & Fadjarenie, R. A. (2024). The influence of budget planning, human resource competence, and budget implementation on budget absorption performance. JPPI (Jurnal Penelitian Pendidikan Indonesia), 10(3), 248–262. https://doi.org/10.29210/020244062

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120.

Basri, Y. M., Gusnardi, G., & Yasni, H. (2021). Government budget absorption: A study on the reallocation and refocus of the COVID-19 budget. JIA (Jurnal Ilmiah Akuntansi), 6(2), 317–337. https://doi.org/10.23887/jia.v6i2.38747

Berisha-Shaqiri, A. (2014). Management information system and decision-making. Academic Journal of Interdisciplinary Studies, 3(2). https://ojs.unhz.eu/index.php/ijir/article/view/184

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 319–340.

Fitriyani, F., Nofianti, N., & Oktaviani, L. (2022). Budget Absorption: on The Interaction of Organizational Commitment, Budget Planning and Quality of Human Resources of The OPD in Serang City. Journal of Applied Business, Taxation and Economics Research, 1(4), 416–426. https://doi.org/10.54408/jabter.v1i4.85

Ghozali, I. (2016). Aplikasi Analisis Multivariat dengan Program IBM SPSS 23 (Edisi VIII). Semarang: Badan Penerbit Universitas Diponegoro.

Hadiwijoyo, S. S., & Anisa, F. D. (2019). Sistem Perencanaan dan Penganggaran Pemerintah Daerah. Rajawali Press.

Halim, A., & Kusufi, M. S. (2014). Akuntansi Sektor Publik. Salemba Empat.

Heniwati, E. (2023). Budget Absorption Phenomena: Evidence from Education Quality Assurance Institutions. Oblik i Finansi, 100, 101–110. 10.33146/2307-9878-2023-2(100)-101-110

Hutagalung, M. A., Nurbaiti, N., Lubis, A. W., Nurlaila, N., & Inayah, N. (2024). The Influence Of Budget Planning And Budget Implementation On The Level Of Budget Absorption. International Journal Of Economics Social And Technology, 3(4), 99–110. https://doi.org/10.59086/ijest.v3i4.362

Imelda, I., Fachrudin, F., Satriawan, B., Wibisono, C., & Khaddafi, M. (2022). The influence of human resources competency, budgeting politics and procurement of goods and services on budget absorption by budget implementation as a moderating variable in the government of Riau Islands. International Journal of Social Science, Educational, Economics, Agriculture Research and Technology, 1(12), 849–862. http://dx.doi.org/10.54443/ijset.v1i12.91

Indriani, T. (2016). Analisis faktor-faktor yang mempengaruhi rendahnya tingkat penyerapan anggaran belanja daerah. Universitas Pendidikan Indonesia.

Mahmudi. (2018). Akuntansi sektor publik. UII Press.

Mardiasmo. (2018). Akuntansi Sektor Publik. Andi Offset.

Marsontio, O., Basri, Y. M., & Ratnawaty, V. (2022). Keterlambatan Penyerapan Anggaran: Peran Komitmen Organisasi Sebagai Moderasi. Jurnal Akuntansi Dan Ekonomika, 12(1), 12–22. https://doi.org/10.37859/jae.v12i1.3505

Mocodompis, H. (2015). Pengaruh Kualitas Sumber Daya Manusia Aparatur terhadap Peningkatan Kinerja di Badan Kepegawaian Daerah Kabupatenbolaang Mongondow Utara. Politico: Jurnal Ilmu Politik, 2(6), 1108. https://www.neliti.com/publications/1108/pengaruh-kualitas-sumber-daya-manusia-aparatur-terhadap-peningkatan-kinerja-di-b

Norawati, S., Seprinaldi, S., & Rahmawati, R. (2024). Analysis of Budget Participation and Human Resource Competency and its Influence on Budget Absorption with Organizational Commitment as a Moderating Variable. Dinasti International Journal of Economics, Finance & Accounting (DIJEFA), 4(6). https://doi.org/10.38035/dijefa.v4i6.2249

OECD. (2021). Digital government in Indonesia: Strengthening the institutional and governance framework. OECD Publishing.

Oulasvirta, L., & Rönkkö, J. (2023). Public financial management: Budgeting, accountability and auditing. In Finnish Public Administration: Nordic Public Space and Agency (pp. 111–126). Cham: Springer International Publishing. https://doi.org/10.1007/978-3-031-34862-4_7

Purba, I. B. A. H. (2025). Enhancing budget policy alignment: Insights from local government practices. World Journal of Advanced Research and Reviews, 25(1), 019–023. https://doi.org/10.30574/wjarr.2025.25.1.4053

Ramadhani, R., & Setiawan, M. A. (2019). Pengaruh regulasi, politik anggaran, perencanaan anggaran, sumber daya manusia dan pengadaan barang/ jasa terhadap penyerapan anggaran belanja pada opd provinsi sumatera barat. Jurnal Eksplorasi Akuntansi, 1(2), 710–726. https://doi.org/10.24036/jea.v1i2.104

Refitia, T. O. (2025). Pengaruh Kualitas Sumber Daya Manusia, Teknologi Informasi, Dan Sistem Akuntansi Manajemen Terhadap Kinerja Manajerial Dengan Ketidakpastian Lingkungan Sebagai Variabel Moderasi (Survei Pada Badan Pengelolaan Keuangan Dan Aset Daerah (BPKAD) Kota Bandar L. UIN Raden Intan Lampung.

Rifai, A., Inapty, B. A., & Pancawati, S. M. (2016). Analisis Faktor-faktor yang Mempengaruhi Keterlambatan Daya Serap Anggaran (Studi Empiris pad SKPD Pemprov NTB). Jurnal Ilmiah Akuntansi Dan Bisnis, 11(1), 1–10. http://dx.doi.org/10.24843/JIAB.2016.v11.i01.p01

Schiavo-Campo, S. (2023). Public administration: the basics. Routledge.

Sekaran, U., & Bougie, R. (2016). Research Methods for Business: A Skill-Building Approach (7th ed.). Wiley.

Valle-Cruz, D., Gil-Garcia, J. R., & Fernandez-Cortez, V. (2020, June). Towards smarter public budgeting? Understanding the potential of artificial intelligence techniques to support decision making in government. In Proceedings of the 21st Annual International Conference on Digital Government Research (pp. 232-242).

Van Hiep, N. (2021). High quality human resources development. Journal of the University of Shanghai for Science and Technology, 23(1), 3818–3830. http://dx.doi.org/10.51201/jusst12546

Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425–478. https://www.jstor.org/stable/30036540

World Bank. (2020). Indonesia public expenditure review: Spending for better results. The World Bank.

Información adicional

redalyc-journal-id: 4775