Artigos

PERFORMANCE MEASUREMENT IN POLLUTING COMPANIES BELONGING TO ISE IN TERMS OF ENVIRONMENTAL, SOCIAL AND GOVERNANCE AND SUSTAINABLE DEVELOPMENT GOALS

Ana Mariella Bandeira anaufsm@gmail.com

Ana Mariella Bandeira anaufsm@gmail.com

Márcia ferraz Meneghel marciafmeneghel@gmail.com

Lucas Veiga Ávila lucas.avila@ufsm.br

Larissa Degenhart larissa.degenhart@ufsm.br

Diego Marques Cavalcante dieegomc@hotmail.com

Márcia ferraz Meneghel marciafmeneghel@gmail.com

Lucas Veiga Ávila lucas.avila@ufsm.br

Larissa Degenhart larissa.degenhart@ufsm.br

Diego Marques Cavalcante dieegomc@hotmail.com

PERFORMANCE MEASUREMENT IN POLLUTING COMPANIES BELONGING TO ISE IN TERMS OF ENVIRONMENTAL, SOCIAL AND GOVERNANCE AND SUSTAINABLE DEVELOPMENT GOALS

Revista Catarinense da Ciência Contábil, vol. 24, pp. 1-19, 2025

Conselho Regional de Contabilidade de Santa Catarina

Esta obra está bajo una Licencia Creative Commons Atribución 4.0 Internacional.

Recepción: 12 Mayo 2025

Revisado: 21 Julio 2025

Aprobación: 26 Agosto 2025

Publicación: 19 Septiembre 2025

Abstract: This study investigates the impact of Environmental, Social, and Governance (ESG) scores and the Sustainable Development Goals (SDGs) on the performance of Brazilian companies from highly polluting sectors listed on the Corporate Sustainability Index (ISE) of B3 – Brasil, Bolsa, Balcão, between 2016 and 2020. The research employs a mixed-method, descriptive, and documentary approach. Results reveal that ESG factors, when considered jointly, do not significantly contribute to the advancement of SDGs. However, when disaggregated, environmental, social, and governance dimensions exhibit positive and significant effects on SDG alignment. In contrast, market performance—measured by Tobin’s Q and Market-to-Book ratios—was positively and significantly influenced only by the aggregated ESG scores. No significant relationship was found between SDGs as a whole and market performance, but disaggregated analysis revealed that SDG 3 (Good Health and Well-Being) positively influenced both Tobin’s Q and Market-to-Book, while SDG 9 (Industry, Innovation, and Infrastructure) had a positive effect only on Market-to-Book. These findings offer theoretical contributions by highlighting the differentiated effects of ESG and SDGs on corporate performance in an emerging economic context. From a practical standpoint, the results support the development of more robust corporate sustainability strategies, assist investors identify value-adding ESG practices, and inform policymakers in designing more effective regulations that foster both internal improvements and external commitments to sustainable development.

Keywords: Sustainable Development Goals, Environmental Social and Governance, Performance, Sustainability.

1 INTRODUCTION

The Sustainable Development Goals (SDGs) are part of multilateral efforts that have guided the corporate context toward more sustainable and resilient pathways (Caiado et al., 2018). Thus, translating these global goals into actionable corporate engagement to address societal and environmental challenges (Muff et al., 2017) and assessing how companies measure, communicate and monitor their contributions to the SDGs is a challenge for the corporate sector (Khaled et al., 2021). Identifying companies' sustainable practices through environmental, social, and governance (ESG) scores (Tamimi and Sebastianelli, 2017) assists in meeting the SDGs and makes it possible to assess corporate sustainability performance (Khaled et al., 2021).

In this context, managing and investing in social responsibility through environmental, social and governance (ESG) criteria fosters sustainable performance, resilience and potential investment stability (Chen et al., 2021). Observation of ESG aspects should be considered by companies, as investors seek investments that provide social and environmental benefits (Chen et al., 2021; Mohammad and Wasiuzzzaman, 2021) and timely, reliable, consistent, and comparable ESG information is a factor in evaluating corporate behavior and ensuring corporate sustainability (Alsayegh et al., 2020).

Several studies have sought map the relationships between ESG issues, corporate sustainable performance, and the sustainable development goals (Khaled et al., 2021). Evidence highlights positive effects of environmental disclosure on corporate financial performance (Wang et al., 2020; Wang et al., 2021) as well as negative effects (Xia and Wang, 2020).

The theoretical gap motivating this research is the absence of studies that have looked at the variables of ESG scores, sustainable development goals, and performance in a joint theoretical configuration to explain market outcomes in a sample of Brazilian companies belonging to Brazil, Bolsa e Balcão (B3). It is assumed in this research that the conditions under which shareholders attribute relevance and value to sustainability information are linked to the increased performance of the organization, through ESG practices and incorporation of SDGs in business activities.

Regarding the study's innovation, it is worth noting that ESG practices and alignment with the SDGs can constitute a competitive advantage by enhancing the company’s market value and promoting social well-being. A consistent sustainability index serves as a reference for capital and credit markets, highlighting organizations that integrate socio-environmental risks into their management, which contributes to strengthening their image in society (Sobrosa Neto et al., 2020).

It should be noted that ESG practices, when aligned with the Sustainable Development Goals (notably SDG 8 - Decent Work and Economic Growth, 9 - Industry, Innovation and Infrastructure, 12 - Responsible Consumption and Production, and 13 - Climate Action), can constitute a significant competitive advantage. This integration not only contributes to the market valuation of companies, but also reinforces their commitment to sustainable development and collective well-being. Other ESG practices, also strategically aligned with the Sustainable Development Goals most relevant to the industrial sector - in particular SDG 9 (Industry, Innovation and Infrastructure), SDG 12 (Responsible Consumption and Production) and SDG 13 (Climate Action), represent and contribute to the generation of value in the market, while also mitigating environmental impacts.

The development of this research is justified by the growing international and national interest of investors and corporate managers in ESG/CSR (Gillan et al., 2021; Mohammad and Wasiuzzaman, 2021) and by the fact that the ESG profile of companies is related to their market characteristics, leadership, ownership, risk, performance and company value (Gillan et al., 2021). Finally, the analysis of the direct relationship between sustainability and market performance enriches the debate on corporate sustainability, contributes to a better understanding of stakeholders' reactions to sustainability issues, and informs the design of strategies that promote increased investments in sustainable development.

2 THEORETICAL CONSTRUCTION AND RESEARCH HYPOTHESES 2.1 ESG scores, sustainable development goals, and market performance

ESG scores provide an assessment of sustainable actions at the company and product levels, whereas the SDGs extend this assessment to describe their environmental and social impacts (Consolandi et al., 2020). The literature highlights the challenge of linking ESG activities developed contribute to the achievement of the SDGs (Khaled et al., 2021), as ESG metrics lack uniformity (Consolandi et al., 2020). The SDGs create a high-level framework of environmental, social, and governance impacts, elucidating elements missing or implicit in widespread ESG standards and metrics, enabling the assessment of whether there are sustainable actions, and whether they generate positive or negative externalities (Consolandi et al., 2020).

Under these conditions, it is understood that achieving the Sustainable Development Goals (SDGs) helps address gaps in sustainable information, being positively influenced by ESG-oriented actions. Therefore, it is assumed that: H1: There is positive relationship between ESG scores and sustainable development goals. H1a: There is a positive relationship between environmental scores and sustainable development goals. H1b: There is positive relationship between social score and sustainable development goals. H1c: There is positive relationship between governance score and sustainable development objectives.

Market performance can be measured by Tobin's Q, which reflects the firm’s future performance that meets the expectations of its stakeholders (Mohammad and Wasiuzzzaman, 2021), and by Market to Book, which refers to firms' growth opportunities. Chowdhury and Quaddus (2021) point out that sustainability practices directly improve market performance through improved sustainability governance. Broadstock et al. (2021) suggests that companies with higher Market to Book ratios experience smaller declines in closing share value.

Among the environmental and social dimensions, Ng et al. (2020) suggest that corporate investments can reduce environmental degradation and enhance employee health and safety. Within corporate governance, studies indicate a positive contribution between governance and profitability, facilitating more efficient resource utilization (BUSCH et al., 2016). Velte's (2017) results in German companies indicated a positive impact of ESG practices on the accounting indicator ROA, and negative on the market indicator Tobin's Q.

In view of these conflicting findings, further insights into the effects of ESG scores on market performance are expected from the development of the second hypothesis, which posits the positive and significant influence of investment in environmental, social, and governance aspects on market performance. Thus, it is proposed: H2: There is positive relationship between ESG scores and market performance. H2a: There is positive relationship between environmental score and market performance. H2b: There is positive relationship between social score and market performance. H2c: There is positive relationship between governance score and market performance.

Sustainable actions enhance production efficiency, customer satisfaction, cost reduction, improved market reputation, awareness of sustainable growth, and reduction of carbon emission (Jensen and Berg, 2011; Porter and Kramer, 2018). At the disclosure level, the proper measurement of the sustainability process and its integration into corporate reporting brings benefits even for the entity's economic andfinancial performance (Brocket and Rezaee, 2012).

Jung et al. (2017) suggest that a company's corporate sustainability performance is positively associated with its financial performance, particularly in the information and communication technology sector. The reformulation of approaches and contributions to sustainable value generation is one of the effects of adopting and implementing SDGs in corporate actions (Izzo et al., 2020). Considering the context in which attention to sustainable development goals can provide greater corporate performance, the third hypothesis to be tested in this research assumes that: H3: There is a positive relationship between sustainable development goals and market performance.

3 METHODOLOGY

The methodology is characterized as descriptive, with data based on documentary sources and result analysis conducted using a mixed-method approach (Iglesias and Alfinito, 2006), with analysis of a five-year period (2016 to 2020). This period is justified by the fact that the Sustainable Development Goals (SDGs) were agreed upon in September 2015 by the global population (Muff et al., 2017), which provided companies with greater observation regarding the sustainable practices exercised.

The study population consisted of all Brazilian companies belonging to the B3 Corporate Sustainability Index (ISE), which totaled 39 companies. The sample was limited to companies in the segments considered most polluting based on Law 10.165 (2000), and that have ESG scores, excluding companies with incomplete data on the variables analyzed. Thus, the final number that meets these requirements was 20 companies, thus making up the study sample. In the years 2016 and 2017, 18 companies were considered, in 2018 19 companies were considered, and in the years 2019 and 2020, 20 companies presented all the data regarding ESG scores.

The independent variables in the study are the sustainable development goals and ESG scores. Market performance is considered the dependent variable of the model and is measured through Tobin's Q and Market to Book. However, to verify the effects of ESG performance (environmental, social, and governance) on the Sustainable Development Goals, the SDGs were considered as the dependent variable of the model and ESG performance as the independent variables.

Companies' compliance with the SDGs was assessed through a qualitative analysis of the activities carried out in relation to the 17 goals, as contained in the Sustainability Reports and Annual Reports of the selected companies, considering the presence of actions, policies, targets, or indicators clearly linked to each of the 17 SDGs. For each SDG, a binary compliance score was assigned: Value 1 (compliant): A value of 1 was assigned if they contributed explicitly with actions directly linked to the SDGs. Value 0 (non-compliant): A value of 0 was assigned when there was no clear mention of the content of the SDGs evaluated.

The evaluation was conducted individually by the researchers, with any discrepancies subsequently resolved through joint re-evaluation. The total number of SDGs achieved by each company in each year was used for aggregate analysis (Equation 3), while compliance with each SDG was used individually in the disaggregated analysis (Equation 4). A control variable was included in the model, represented by company size, a variable relevant to explaining market performance, according to prior evidence from Yoon and Chung (2018).

To conduct the data analysis, descriptive statistics of the variables, normality test, spearman correlation, and panel data regression were conducted. From the results found, a qualitative section was developed, presenting the companies' actions before the SDGs. A secondary analysis was carried out, showing which SDGs were more and less prioritized according to the sector in which they operate.

The equations considered for the study are presented below. Equation 1 aims to find the results to explain research hypothesis H1. Equation 2 refers to hypothesis H2, and equations 3 and 4 aim to provide support for hypothesis H3.

It should be noted that initially the impacts of the SDGs on market performance were checked jointly, by adding up the SDGs presented by the companies in their reports during the year (equation 3), and then the effects of the SDGs on performance individually (equation 4).

3.1 Limitations and future research

Despite the methodological rigor applied, this study has some limitations that should be noted. According to Mohammad and Wasiuzzzaman (2021), the adoption of the Sustainable Development Goals contributed to an increase in ESG-related disclosures, encouraging the voluntary reporting of non-financial information and promoting greater transparency.

However, the proportion of companies that mentioned the SDGs in their sustainability reports was limited in the first year of analysis of this study (2016), and it was not possible to identify clear mentions of the SDGs published in their Sustainability Reports, which may partially compromise the temporal comparability of the data in this first year of analysis. The Sustainable Development Goals were adopted in September 2015 and came into effect in January 2016, which may explain the lack of information in 2016 for some companies, given the recent formalization of the agenda at the time.

In addition, the binary approach to measuring SDG compliance may oversimplify the comprehensiveness of corporate actions, which may not accurately reflect the degree of effectiveness of the reported initiatives. This limitation is also related to the availability and standardization of information in corporate reports, which varied in detail across companies and years, which may compromise the classification and analysis of data.

It should also be noted that other relevant control variables were not incorporated into the model, such as sector of activity and specific governance characteristics, which may limit the explanatory power of the tested relationships, aspects that provide avenues for future research that integrate these elements.

4 ANALYSIS AND DISCUSSION OF THE RESULTS

Table 1 presents the results of the descriptive statistics of the variables.

| Variables | Mean | Standard Deviation | Minimum | Maximum |

| Q de Tobin (QT) | 0.93 | 1.00 | 0.12 | 7.97 |

| Market to Book (MTB) | 2.93 | 3.42 | -18.3 | 13.7 |

| Sustainable Development Goals (SDG) | 10.93 | 6.27 | 0.0 | 17.0 |

| Performance - ESG (ESG) | 65.55 | 13.92 | 14.48 | 84.59 |

| Environmental Performance (EP) | 66.62 | 17.09 | 4.59 | 94.25 |

| Social Performance (SP) | 70.73 | 17.29 | 4.66 | 96.50 |

| Governance Performance (GP) | 55.87 | 18.73 | 10.78 | 86.82 |

| Company Size (CS) | 7.42 | 0.519 | 6.03 | 8.99 |

The Market to Book (MTB) were positive as to the average (0.93 and 2.93), which reveals that there was, on average, an increase in market performance from the perspective of these indicators.

The dependent variables Tobin's QT and Market in ESG practices are associated with ethical investment promotion and improved capital market performance, contributing to higher stock returns and reducing portfolio risk. In other words, the better the ESG practices—especially in environmental, social, and governance goals—the higher the company's market value, reflected by a high Tobin's Q (Alpinar and Topak, 2024), in view of the companies' concern with investment It is observed, through the results shown in Table 1, a median propensity in some companies to meet the Sustainable Development Goals and the performance focused on ESG (environmental, social and governance). The dependent variables Tobin's QT and Market in ESG practices by the consequent ethical investment promoted and the improvement of performance in the capital market, managing and increasing stock returns and reducing portfolio risk.

Table 2 shows the results of the normality test for the variables analyzed in the proposed theoretical model.

| Variables | Kolmogorov-Smirnov | Shapiro-Wilk | ||||

| Statistic | df | Sig. | Statistic | df | Sig. | |

| Q de Tobin (QT) | 0.213 | 95 | 0.000 | 0.606 | 95 | 0.000 |

| Market to Book (MTB) | 0.214 | 95 | 0.000 | 0.728 | 95 | 0.000 |

| Sustainable Development Goals (SDG) | 0.245 | 95 | 0.000 | 0.802 | 95 | 0.000 |

| Performance - ESG (ESG) | 0.138 | 95 | 0.000 | 0.878 | 95 | 0.000 |

| Environmental Performance (EP) | 0.117 | 95 | 0.003 | 0.931 | 95 | 0.000 |

| Social Performance (SP) | 0.096 | 95 | 0.032 | 0.895 | 95 | 0.000 |

| Governance Performance (GP) | 0.161 | 95 | 0.000 | 0.932 | 95 | 0.000 |

| Company Size (CS) | 0.145 | 95 | 0.000 | 0.932 | 95 | 0.000 |

The results presented in Table 2 indicate that the data analyzed are not normal, since the Kolmogorov-Smirnov and Shapiro-Wilk tests were significant at the 5% level. Therefore, the Spearman correlation should be performed, to identify the existing correlation between the variables analyzed and possible multicollinearity problems (Fávero et al., 2009).

Next, the results of the spearman correlation between the variables analyzed in the research are presented in Table 3.

| Variáveis | QT | MTB | SDG | ESG | EP | SP | GP | CS |

| Q de Tobin (QT) | 1 | 0.566** | -0.043 | 0.023 | -0.080 | 0.049 | 0.037 | -0.429** |

| Market to Book (MTB) | 1 | -0.197 | 0.032 | -0.052 | 0.084 | -0.028 | -0.290** | |

| Sustainable Development Goals (SDG) | 1 | 0.123 | 0.206* | 0.052 | 0.079 | 0.312** | ||

| Performance - ESG (ESG) | 1 | 0.705** | 0.700** | 0.559** | 0.064 | |||

| Environmental Performance (EP) | 1 | 0.419** | 0.078 | 0.222* | ||||

| Social Performance (SP) | 1 | 0.354** | 0.024 | |||||

| Governance Performance (GP) | 1 | -0.094 | ||||||

| Company Size (CS) | 1 |

The results indicate that Tobin's Q is positively and significantly associated with Market-to-Book at the 1% significance level, and negatively and significantly associated withcompany size, indicating that the larger the company size, the higher its market performance. The SDGs were positively and significantly related to environmental performance at the 5% level and to company size at the 1% level, suggesting that larger companies are more concerned with meeting the SDGs and consequently demonstrate better environmental performance, thereby seeking to mitigate the environmental impacts of their activities.

ESG performance is positively significantly associated at the 1% level of with all dimensions: environmental, social and governance. However, environmental performance relates positively and significantly only with social performance and company size, which reveals that larger companies have better environmental and social scores. Regarding social performance, it is positively and significantly related only to governance performance.

These correlation results indicate that the independent variables of the model (SDG and ESG) tend not to show effects on the market performance (Tobin's Q and Market to Book) of the analyzed companies. However, this finding was further examined through panel data regression applied to the sample under investigation.

4.1 Analysis of the relationship between ESG scores and sustainable development goals

Regarding equation 1, the panel data regression model used was POLS, since the Breusch-Pagan LM test and Chow's F-test were not significant at the 5% level. Table 4 presents the results of equation 1, which aims to identify the effects of ESG scores on SDG.

| Variables | POLS | |

| Coefficient | Sig. | |

| Constant (SDG) | 8.06 | 0.00* |

| ESG Performance | -1.52 | 0.01** |

| Environmental Performance (EP) | 0.69 | 0.00* |

| Social Performance (SP) | 0.50 | 0.02** |

| Governance Performance (GP) | 0.37 | 0.01** |

| Company Size (CS) | 2.91 | 0.02** |

| R2 | 0.11 | |

| Adjusted R2 | 0.07 | |

| F Test | 0.02** | |

| Breusch Pagan | Sig X² 0.21 | |

| Chow test | Sig. F 0.23 | |

| Hausman test | Sig. X² 0.14 | |

| Number of observations | 95 | |

Although evidence in the literature suggests that the adoption of the Sustainable Development Goals increases ESG disclosures, enhances transparency, and potentially reduces information asymmetry by providing investors with relevant information for decision-making (Mohammad and Wasiuzzzaman, 2021), the finding of the first hypothesis suggests otherwise, not proving representative for the companies in the sample.

Although the adoption of ESG best practices increased significantly over the years covered by this study, the evidence suggests that higher ESG scores tend to decrease the activities in front of the SDGs.The result found in this research can be attributed to the fact that the lack of correlation between the scores makes it difficult to measure the impact of ESG practices on the achievement of the goals (Khaled et al., 2021). Based on these findings, the first research hypothesis investigated H1: There is a positive relationship between ESG scores and sustainable development goals.

Despite the non-confirmation of the relationship between ESG scores (total score) and the SDGs, it was found that there is an effect of the specific performances: environmental, social and governance, as they showed a positive and significant relationship at the 1% and 5% levels with the SDGs, since the coefficient obtained was positive and significant. This finding indicates that companies that adopt a more responsible business conduct, present a better performance (Mohammad and Wasiuzzzaman, 2021). Such evidence also indicates that higher levels of environmental, social and governance practices contribute more effectively to companies’ alignment with the SDGs.

Previous evidence suggests that companies should balance social, environmental, and economic sustainability practices to reduce the risks of non-compliance with sustainability standards (Chowdhury and Quaddus, 2021). The findings of this study alsoindicate that companies that are more effective in sustainability are those that balance their environmental, social, and economic practices, maximizing their alignment with global sustainability goals. In this context, the following research hypotheses are confirmed: H1a: Is there a positive relationship between environmental scores and sustainable development goals? H1b: Is there a positive relationship between social scores and sustainable development goals? H1c: Is there a positive relationship between governance scores and sustainable development goals?

The control variable, company size also showed positive and significant effects on the SDGs, reinforcing that larger companies are more engaged in meeting the SDGs, because the higher the level of purpose of this company, the higher the global goals consolidated in its organizational culture.

4.2 Analysis of the relationship between ESG scores and market performance

For equations 2 (Table 5) and 3 (Table 6), the random effects panel data regression model was employed, since the Breusch-Pagan LM test was significant at the 5% level and the Hausman test was not statistically significant. The results of the effects of ESG disclosures of companies belonging to the ISE on market performance (Tobin's Q and Market to Book) are shown in Table 5.

| Variables | Random Effects | Random Effects | ||

| Coefficient | Sig. | Coefficient | Sig. | |

| Constant (Tobin's Q) | 8.21 | 0.00* | - | - |

| Constant (Market to Book) | - | - | 15.48 | 0.00* |

| ESG Performance | 0.11 | 0.06*** | 0.88 | 0.00* |

| Environmental Performance (EP) | -0.03 | 0.19 | -0.39 | 0.00* |

| Social Performance (SP) | -0.04 | 0.06*** | -0.27 | 0.02** |

| Governance Performance (GP) | -0.02 | 0.07*** | -0.21 | 0.01*** |

| Company Size (CS) | -1.05 | 0.00* | -1.71 | 0.03** |

| R2 Overal | 0.05 | 0.10 | ||

| F Test | 0.00* | 0.00* | ||

| Breusch Pagan | Sig X² 0.00* | Sig X² 0.00* | ||

| Chow test | Sig. F 0.00* | Sig. F 0.00* | ||

| Hausman test | Sig. X² 0.40 | Sig. X² 0.86 | ||

| Number of observations | 95 | 95 | ||

The findings indicate that overall ESG performance positively and significantly influences market performance, as measured by Tobin’s Q, at a 10% significance level. This evidence has relevant practical implications, as investment in ESG aspects not only enhances firms’ market performance but also enables investors to make decisions that consider not only financial aspects but also broader market performance (Mohammad & Wasiuzzaman, 2021). Therefore, it is possible to infer a positive reaction from shareholders and investors when a company demonstrates commitment to ESG practices, which may, in turn, positively affect its reputation (Nirino et al., 2021).

These findings validate the second hypothesis investigated in this research, confirming that ESG scores are positively related to market performance as measured by Tobin's Q. H2: There is a positive relationship between ESG scores and market performance.

Although a substantial portion of the literature shows positive effects of ESG practices collectively on market performance (Velte, 2017; Mohammad & Wasiuzzaman, 2021), the findings of this study suggest that, when considered individually , these practices may not be perceived by the market as value-generating, as evidenced by negative coefficients.

Previous studies during periods of corporate crises indicate that the effects of ESG practices on financial performance are not always entirely positive (Saygili et al., 2021), presenting divergent and inconclusive results, which prevents a consensus on this relationship. Consistent with this perspective, the individual analysis of social and governance performance, along with Tobin’s Q, revealed statistical significance at the 10% level, but with negative coefficients. Environmental performance showed no relationship with Tobin’s Q, as its coefficient was negative and not statistically significant.

The results partially align with Degenhart et al. (2020), who observed that initiatives targeting internal stakeholders, as well as environmental actions, were not determinants of market performance. According to the authors, externally oriented actions were more effective in explaining the strong performance of Brazilian companies. This suggests that the market may respond more significantly to practices that generate perceived external value, related to social and reputational perceptions of the firm. However, in this study, even external practices did not exhibit significant effects on performance.

The results also align with Saygili, Arslan, and Birkan (2021), who observed a negative effect of environmental disclosures on the financial performance of Turkish companies. Additionally, Nirino et al. (2021) indicate that the ESG-performance relationship can become complex, as other secondary factors must be considered to fully understand this relationship and its impacts.

In this context, Ng et al. (2020) argue that financial development, as a driver of ESG practices, requires adequate government-led monitoring and governance systems to ensure its effectiveness and sustainability. This is relevant for interpreting the findings of this study, as the lack of significance of individual ESG pillars may reflect structural limitations in how these practices are implemented and perceived by stakeholders.

Regarding the environmental dimension, Khaled et al. (2021) suggest that financial development promotes environmental performance by providing additional financing sources for expansion, technological improvements, and income growth through economic development. For the social dimension, there is evidence that economic growth moderates the relationship between financial and social performance by expanding economic, social, and employment opportunities (Khaled et al., 2021). In the governance domain, studies indicate that greater financial development implies better access to external and long-term financing (Ho & Njindan Iyke, 2017), and that an adequate governance structure can positively contribute to firm profitability (Ng et al., 2020). However, such benefits may not manifest when these pillars are analyzed individually, underscoring the importance of an integrated ESG performance approach.

Evidence in the literature indicates that environmental preservation initiatives are not always effective in enhancing market performance (Degenhart et al., 2020), corroborating this study’s findings, which show that for the companies and period analyzed, when measuring Tobin’s Q from the market value/total assets perspective, environmental, social, and governance indicators considered individually did not generate positive impacts capable of enhancing market performance.

Given the context and the results presented, the following hypotheses are rejected: H2a: There is a positive relationship between environmental score and market performance. H2b: There is a positive relationship between social score and market performance. H2c: There is a positive relationship between governance score and market performance.

Regarding the relationship between ESG scores and market performance measured by Market-to-Book, the results indicate that ESG performance positively and significantly influenced market performance at the 1% level. These findings indicate that ESG performance, when considering the complete set of environmental, social, and governance variables, has a positive impact on market performance as measured by Market-to-Book, which considers both the market value and book value of equity.

This result allows managers to renew their business philosophy by paying more attention to social and environmental issues, given their positive impact on performance (Degenhart et al., 2020), as measured by the book and market value of equity. In this context, the hypothesis is confirmed: H2: There is a positive relationship between ESG scores and market performance (Market-to-Book).

Although environmental, social, and governance performances were statistically significant at the 1%, 5%, and 10% levels, respectively, their coefficients were negative, indicating that, individually, they were not associated with market performance as measured by Market-to-Book. This suggests that when considered in isolation, environmental, social, and governance indicators did not produce positive impacts capable of enhancing market performance from the Market-to-Book perspective. Such evidence suggests that higher levels of environmental, social, and governance performance, when analyzed individually, tend to reduce the growth opportunities of organizations — a finding that contrasts withthe prevailing literature.

The relationship between ESG practices and financial performance may be influenced by various contextual factors, including industry type, the nature of ESG-related risks, and the degree of transparency in disclosures. When the market does not fully recognize the value of the positive externalities generated by ESG practices, or when there is skepticism about the materiality of the disclosed initiatives, the impact on market value may be neutral or even negative (Broadstock et al., 2021).

Velte (2017) concluded that total ESG scores do not exert a positive impact on market-based performance (Tobin’s Q). Mohammad and Wasiuzzaman (2021) highlight that while environmental and social practices contribute to increasing a company’s market value in the long run, they require investments that may negatively affect this variable in the short term.

In a study of 26 Turkish companies, Çetin, Akarsu & Öztürk (2024) found a negative effect in the relationship between ESG performance and market value, indicating that isolated sustainability practices did not generate positive impacts on value perception by the financial market.

Therefore, the following hypotheses are rejected: H2a: There is a positive relationship between environmental score and market performance. H2b: There is a positive relationship between social score and market performance. H2c: There is a positive relationship between governance score and market performance.

The control variable, firm size, exhibited a negative and significant effect on both Tobin’s Q and Market-to-Book. This result suggests that, although this variable is generally considered relevant in explaining market performance (Yoon & Chung, 2018), for the companies in the selected sample, firm size did not indicate positive or differential effects that could lead to higher levels of market performance.

4.3 Analysis of the relationship between Sustainable Development Goals and market performance

With a view to meeting the study's hypothesis H3, the effects of the SDGs jointly on market performance were verified and the results are presented in Table 6.

| Variables | Random Effects | Random Effects | ||

| Coefficient | Sig. | Coefficient | Sig. | |

| Constant (Tobin's Q) | 7.48 | 0.000* | - | - |

| Constant (Market to Book) | - | - | 11.90 | 0.03** |

| Object. Sustainable Development Goals (SDG) | -0.00 | 0.888 | -0.038 | 0.46 |

| Company Size (CS) | -0.85 | 0.000* | -1.12 | 0.12 |

| R2 Overal | 0.07 | 0.02 | ||

| F Test | 0.00* | 0.00* | ||

| Breusch Pagan | Sig X² 0.00* | Sig X² 0.01** | ||

| Chow test | Sig. F 0.00* | Sig. F 0.00* | ||

| Hausman test | Sig. X² 0.91 | Sig. X² 0.42 | ||

| Number of observations | 95 | 95 | ||

The total number of SDGs implemented by companies did not significantly impact market performance, both measured by Tobin's Q and Market to Book, as the obtained coefficient was negative and without statistical significance. Although corporate sustainability is key to achieving comparative advantage by corporations (Sharma and Gupta, 2020), the set of SDGs considered in this research does not contribute directly to increasing the levels of market performance of the companies in the sample studied.

Overall , this finding may suggest that the sustainability strategies of companies are not being incorporated into the corporate strategy, since it should not be considered only as a limiter of irresponsible damages that affect the company's reputation (Nirino et al., 2021). Also, that the effective advancement of the SDGs and sustainable development requires that the relationships between the SDGs need to be identified and addressed by companies, as well as their connections between the goals focused on social, community, welfare and climate (Fonseca et al., 2020).

In contrast to this finding, Ng et al. (2020) conducted a study on the mapping of SDGs with sustainability practices reflected by ESG scores, using market-to-book as one of the control variables, concluded that profitable and larger companies are more likely to exhibit better sustainability performance. Based on the negative and non-significant result found in the relationship between SDGs and market performance, hypothesis H3 was rejected: There is a positive relationship between sustainable development goals and market performance.

Furthermore, it was verified which SDGs individually impact the market performance of the analyzed ISE companies, as shown in Table 7.

| Variables | Fixed Effects | Fixed Effects | ||

| Coefficient | Sig. | Coefficient | Sig. | |

| Constant (Tobin's Q) | 5.57 | 0.00* | - | - |

| Constant (Market to Book) | - | - | 3.47 | 0.00* |

| SDG 1 | 0.21 | 0.45 | -0.85 | 0.54 |

| SDG 2 | -0.17 | 0.46 | 1.13 | 0.31 |

| SDG 3 | 0.58 | 0.08*** | 5.87 | 0.00* |

| SDG 4 | 0.06 | 0.80 | 0.85 | 0.50 |

| SDG 5 | -0.15 | 0.56 | -2.29 | 0.07*** |

| SDG 6 | -0.44 | 0.20 | -2.01 | 0.22 |

| SDG 7 | 0.02 | 0.94 | -2.51 | 0.10 |

| SDG 8 | -0.34 | 0.53 | -3.04 | 0.23 |

| SDG 9 | -0.12 | 0.77 | 3.38 | 0.09*** |

| SDG 10 | -0.00 | 0.98 | -0.66 | 0.63 |

| SDG 11 | 0.16 | 0.51 | 1.29 | 0.30 |

| SDG 12 | 0.01 | 0.98 | -5.64 | 0.07*** |

| SDG 13 | 0.38 | 0.52 | 1.20 | 0.67 |

| SDG 14 | -0.02 | 0.90 | 0.67 | 0.51 |

| SDG 15 | -0.39 | 0.41 | 0.81 | 0.73 |

| SDG 16 | 0.32 | 0.32 | 0.59 | 0.69 |

| SDG 17 | -0.16 | 0.46 | 1.06 | 0.34 |

| Company Size (CS) | -0.63 | 0.00* | -0.30 | 0.75 |

| R2 Within | 0.40 | 0.37 | ||

| F Test | 0.00* | 0.00* | ||

| Breusch Pagan | Sig X² 0.04** | Sig X² 0.06 | ||

| Chow Test | Sig. F 0.00* | Sig. F 0.02** | ||

| Hausman test | Sig. X² 0.00* | Sig. X² 0.09 | ||

| Number of observations | 95 | 95 | ||

In the model that considers the market performance measured by Tobin's Q, only SDG 3 was significantly related to Tobin's Q at the 10% significance level, indicating that some SDGs are being prioritized more in the corporate sector than others (Khaled et l., 2021). Thus, the greater the initiatives focused on SDG 3 (ensuring access to quality health care and promoting well-being for all), the greater the future market performance of ISE companies tends to be. The companies in the sample analyzed, from different B3 segments, demonstrated that they connect SDG 3 at the core of their business model. Thus, the following hypothesis is confirmed: H3: There is a positive relationship between sustainable development goals (SDG 3) and market performance (Tobin's Q).

The SDG 3 and SDG 9 (building resilient infrastructure, promoting inclusiveness, sustainability, and fostering innovation) were found to be related to Market to Book at the 1% and 10% significance levels, respectively. This finding corroborates with the result of the study by Allen et al. (2020) that identified good performance in targets related to good health (SDG 3) and better in targets related to infrastructure and innovation (SDG 9) when considering official SDG indicators in Australia. Thus, the following hypotheses are confirmed: H3: There is positive relationship between sustainable development goals (SDG 3) and market performance (Market to Book) and There is positive relationship between sustainable development goals (SDG 9) and market performance (Market to Book).

On the other hand, SDG 5 (gender equality and women's empowerment) and SDG 12 (ensuring sustainable consumption and production patterns) negatively influence Market to Book. Both statistical significances of these relationships were at 10%. In contrast, a study by Allen et al. (2020) found that performance is better with respect to SDG 5 in Australia when official indicators are used. With respect to SDG 12, there is evidence that companies with a high level of engagement with sustainability are less likely to advance results management practices to misrepresent company performance to serve stakeholders (Grimaldi et al., 2020). Thus, the following hypotheses are rejected: H3: There is positive relationship between sustainable development goals (SDG 5) and market performance (Market to Book) and There is positive relationship between sustainable development goals (SDG 12) and market performance (Market to Book).

4.4 Companies' actions regarding the SDGs

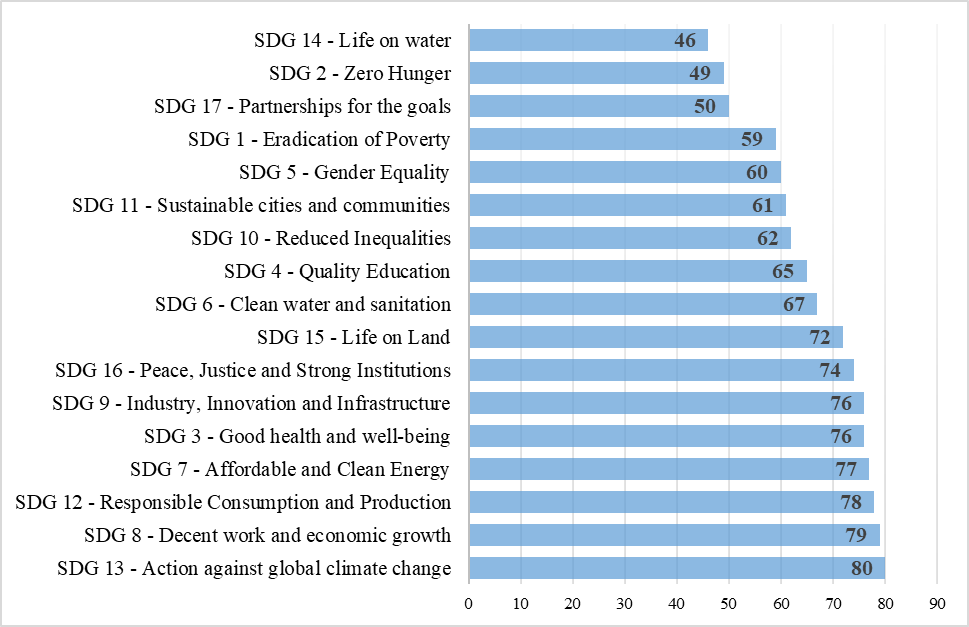

In order to help understand how sustainable practices at the organizational level contribute to the achievement of global goals, the SDGs prioritized by Brazilian companies from the most polluting segments were identified, as shown in Figure 1.

Figure 1

Most and least prioritized sustainable development goals by sector

Source: authors.

The results indicate a significant prioritization of sustainable actions aligned with SDG 13 (Climate Action) by the highly polluting Brazilian sector, reflecting a increased sensitivity among companies toward safer environmental practices. This reinforces the view that investors consider the fulfillment of the SDGs as a mechanism for identifying potential risks (Consolandi et al., 2020).

A strong commitment to sustainable actions was also observed in relation to SDG 8 (Decent Work and Economic Growth), suggesting that companies are striving to balance environmental and social agendas. This may also indicate a preference for goals that align more closely with economic objectives, such as job and income generation. However, according to Mair et al. (2019), such prioritization may lead to tensions between social and environmental goals, as efforts to mitigate ecological crises may compromise social objectives. One possible reason is that in developing countries, economic growth and local job creation still largely depend on the demands of developed countries (Alsamawi et al., 2014). This implies that the social benefits achieved locally may be linked to global production chains that exert environmental pressure in other regions, thus creating an imbalance among the SDGs.

On the other hand, SDG 14 (Life Below Water) was the least prioritized by the most polluting Brazilian sectors, highlighting a concerning gap in the country, given that Brazil possesses vast freshwater and marine resources. This finding may be explained by the fact that, although in developing countries like Brazil, activities such as small-scale fishing contribute to nutrition, food security, sustainable livelihoods, and poverty reduction, there is still a need for public policies and corporate strategies to ensure the implementation of this SDG (Landin, 2020).

It is important to emphasize that the achievement of the Sustainable Development Goals acknowledges the fundamental role that the private sector can play in realizing these goals (Van Der Waal et al., 2021). However, the research results revealed that, in the context of highly polluting sectors, SDG 14 was perceived as less material—particularly by companies not directly dependent on marine resources.

Segment-specific SDG analyses are relevant for investors who use such information to support the definition of specific and long-term investment strategies and the allocation of resources that enable the simultaneous return of sustainability and profit (Mair et al., 2019). In this sense, the integration of the SDGs into corporate strategies also represents a competitive advantage that enhances the value generated by companies.

5 CONCLUSIONS

This paper aimed to investigate the impacts of Environmental, Social, and Governance (ESG) scores and the Sustainable Development Goals (SDGs) on the performance of Brazilian companies from sectors considered highly polluting, listed in the Corporate Sustainability Index (ISE) of B3 – Brasil, Bolsa, Balcão – during the period from 2016 to 2020. The study sought to contribute to the existing literature and research on the topic by measuring the market performance of companies included in the ISE in relation to ESG and SDG practices.

Both theoretical and practical contributions are highlighted. As a theoretical and scientific contribution, the study presents the results of the relationship between SDGs and the market performance of Brazilian companies listed in the ISE, fostering discussions on the impact of this variable on market performance. Among the theoretical implications, the study examines the combined influence of ESG and SDG variables within an emerging market context, such as Brazil.

In terms of practical implications and contributions, the study allows for the identification of different ways to measure market performance and assess how sustainable strategies contribute to improved performance outcomes. Furthermore, it provides a foundation for regulatory policymakers to develop more robust legislation, which may lead to greater organizational commitment to internal, external, and environmental concerns (Degenhart et al., 2020).

From a managerial perspective, decisions based on ESG practices create a favorable environment to helps prevent actions that could harm the company's reputation and consequently impair performance (Nirino et al., 2021). Moreover, it aims to increase awareness of the relevant value of the SDGs, influencing the evolution also of sustainability reporting (Van Der Waal et al., 2020), suggesting a change by organizations towards achieving the Sustainable Development Goals (Fonseca et al., 2020).

Among the limitations of this study, it should be noted that in 2016, although companies released sustainability reports, there was no reference to the Sustainable Development Goals. As opportunities for future research, it is recommended to incorporate additional control variables, such as market of operation, aspects of corporate governance structure, specific characteristics of the company or mediating variables in the relationships studied, which may help explain variations in performance and other observed relationships.

REFERENCES

Allen, C., Reid, M., Thwaites, J., Glover, Rod., & Kestin, T. (2020). Assessing national progress and priorities for the Sustainable Development Goals (SDGs): experience from Australia. Sustainability Science, 15, 521–538. https://doi.org/10.1007/s11625-019-00711-x

Akpınar, H. İ., & Topak, M. S. (2024). The Effect of ESG (Environmental, Social And Governance) Scores on Company Performance: Evidence from the Manufacturing Industry in Turkey. EKOIST Journal of Econometrics and Statistics, (41), 109–117. https://doi.org/10.26650/ekoist.2024.41.1540173

Alsayegh, M. F., Abdul Rahman, R., & Homayoun, S. (2020). Corporate Economic, Environmental, and Social Sustainability Performance Transformation through ESG Disclosure. Sustainability, 12(9), 3910. https://doi.org/10.3390/su12093910

Alsamawi, J. Murray, & M. Lenzen. (2014). The employment footprints of nations. Journal Industrial Ecology, 18, 59–70. https://doi.org/10.1111/jiec.12104

Brasil, Bolsa e Balcão. (2021). Índice de Sustentabilidade Empresarial ISE (B3). https://www.b3.com.br/pt_br/market-data-e-indices/indices/indices-de-sustentabilidade/indice-de-sustentabilidade-empresarial-ise-b3.htm

Broadstock, David C., Chan, K., Cheng, L. T. W., & Wang, X. W. (2021). The Role of ESG Performance During Times of Financial Crisis: Evidence from COVID-19 in China. Finance research letters, 38, 101716. https://doi.org/10.1016/j.frl.2020.101716

Brockett, A., Rezaee, Z. (2012). Corporate sustainability: integrating performance and reporting. John Wiley and Sons, Hoboken, NJ, USA.

Busch, T., Bauer, R., & Orlitzky, M. (2016). Sustainable development and financial markets: old paths and new avenues. Business and Society, 55(3), 303–329. https://doi.org/10.1177/0007650315570701

Caiado, R. G. G. C., Filho, W. L., Quelhas, O. L. G., Nascimento, D. L. M., & Ávila, L. V. (2018). A literature-based review on potentials and constraints in the implementation of the sustainable development goals. Journal of Cleaner Production, 198, 1276–1288. https://doi.org/10.1016/j.jclepro.2018.07.102

Çetin, F. A., Öztürk, S., & Akarsu, O. N. (2024). The Effect of ESG Data of Companies on Financial Performance: A Panel Data Analysis on The BIST Sustainability Index. Sosyoekonomi, 32(61), 125–146.

Chen, L., Zhang, L., Huang, J., Xiao, H., & Zhou, Z. (2021). Social Responsibility portfolio optimization incorporating ESG criteria. Journal of Management Science and Engineering, 6(1), 75–85. https://doi.org/10.1016/j.jmse.2021.02.005

Consolandi, C., Phadke, H., Hawley, J., & Eccles, R. G. (2020). Material ESG Outcomes and SDG Externalities: Evaluating the Health Care Sector’s Contribution to the SDGs. Organization & environment, 33(4), 511–533. https://doi.org/10.1177/1086026619899795

Chowdhury, M. H., & Quaddus, M. A. (2021). Supply chain sustainability practices and governance for mitigating sustainability risk and improving market performance: A Dynamic capability Perspective. Journal of Cleaner Production, 123521. https://doi.org/10.1016/j.jclepro.2020.123521

Degenhart, L., Giordani, M. da S., Halberstadt, I. A., Soares, C. S., & Zonatto, V. C. da S. (2020). Corporate social responsibility and the market performance of Brazilian companies. Revista de Administração da UFSM, 13, 1373–1391.

Fávero, L. P., Belfiore, P., Silva, F. L. da, & Chan, B L. (2009). Análise de Dados: modelagem multivariada para tomada de decisões. Elsevier.

Fonseca, L. M., Domingues, J. P., & Dima, A. M. (2020). Mapping the Sustainable Development Goals Relationships. Sustainability, 12, 01–15. https://doi.org/10.3390/su12083359

Gillan, S. L., Koch, A. & Starks, L. T. (2021). Firms and social responsibility: A review of ESG and CSR research in corporate finance. Journal of Corporate Finance, 66, 1–16. https://doi.org/10.1016/j.jcorpfin.2021.101889

Grimaldi, F., Caragnano, A., Zito, M., & Mariani, M. (2020). Sustainability Engagement and Earnings Management: The Italian Context. Sustainability, 12(12), 4881. https://doi.org/10.3390/su12124881

Ho, S. Y., & Njindan Iyke, B. (2017). Determinants of stock market development: A review of the literature. Studies in Economics and Finance,34(1), 143–164. https://doi.org/10.1108/SEF-05-2016-0111

Iglesias, F., & Alfinito, S. (2006). A abordagem multi-metodológica em comportamento do consumidor: dois programas de pesquisa na área de serviços. Revista Psicologia: Organizações & Trabalho, 6, 138–165.

Izzo, M. F., Ciaburri, M., & Tiscini, R. (2020). The Challenge of Sustainable Development Goal Reporting: The First Evidence from Italian Listed Companies. Sustainability, 12(8), 3494. https://doi.org/10.3390/su12083494

Jensen, J. C., & Berg, N. (2011). Determinants of Traditional Sustainability Reporting Versus Integrated Reporting. An Institutionalist Approach. Business Strategy and the Environment, 21, 299–316. https://doi.org/10.1002/bse.740

Jung, S., Nam, C., Yang, D. H., & Kim, S. (2017). Does corporate sustainability performance increase corporate financial performance? Focusing on the information and communication technology industry in Korea. Sustainable Development, 26(3), 243–254. https://doi.org/10.1002/sd.1698

Khaled, R., Ali, H., & Mohamed, E. K. A. (2021). The Sustainable Development Goals and corporate sustainability performance: mapping, extent and determinants. Journal of Cleaner Production, 311(15), 127599. https://doi.org/10.1016/j.jclepro.2021.127599

Landin, S. A. (2020). Social economy as the means to help achieve the targets of sustainable development goal 14. Sustainability, 12, 4529. https://doi.org/10.3390/su12114529

Lei 10.165, de 27 de dezembro de 2000 (2000). Altera a Lei no 6.938, de 31 de agosto de 1981, que dispõe sobre a Política Nacional do Meio Ambiente, seus fins e mecanismos de formulação e aplicação, e dá outras providências. http://www.planalto.gov.br/ccivil_03/Leis/L10165.htm

Mair, S., Druckman, A., & Jackson, T. (2019). Higher Wages for Sustainable Development? Employment and Carbon Effects of Paying a Living Wage in Global Apparel Supply Chains. Ecological Economics, 159, 11–23. https://doi.org/10.1016/j.ecolecon.2019.01.007

Mohammad, E. M., & Wasiuzzaman, S. (2021). Environmental, Social and Governance (ESG) disclosure, competitive advantage and performance of firms in Malaysia. Cleaner Environmental Systems, 2, 100015. https://doi.org/10.1016/j.cesys.2021.100015

Muff, K., Kapalka, A., & Dyllick, T. (2017). The Gap Frame- Translating the SDGs into relevant national grand challenges for strategic business opportunities. The International Journal of Management Education, 15, 363–383. https://doi.org/10.1016/j.ijme.2017.03.004

Nirino, N., Santoro, G., Miglietta, N. & Quaglia, R. (2021). Corporate controversies and company's financial performance: Exploring the moderating role of ESG practices. Technological Forecasting & Social Change, 162, 1–7. https://doi.org/10.1016/j.techfore.2020.120341

Ng, T. H., Lye, C.T., Chan, K. H., Lim, Y. Z., & Lim, Y. S. (2020). Sustainability in Asia: The Roles of Financial Development in Environmental, Social and Governance (ESG) Performance. Social Indicators Research, 150, 17–44. https://doi.org/10.1007/s11205-020-02288-w

Porter, M.E., & Kramer, M.R. (2018). Creating Shared Value. Managing Sustainable Business, 323–346.

Saygili, E., Arslan, S., & Birkan, A. O. (2021). ESG practices and corporate financial performance: Evidence from Borsa Istanbul, Borsa Istanbul Review.https://doi.org/10.1016/j.bir.2021.07.001

Sharma, G., & Gupta, S. (2020). Modelling the impact of corporate sustainability on economic performance with reference to Indian financial industry’. World Review of Entrepreneurship, Management and Sustainable Development, 16(3), 317–328.

Sobrosa Neto, R. de C. S., Lima, C. R. M. De, Bazil, D. G., Veras, M. De O. & Guerra, J. B. S. O. De A. (2020). Sustainable development and corporate financial performance: A study based on the Brazilian Corporate Sustainability Index (ISE). Sustainable Development, 28 (4), 1–18. https://doi.org/10.1002/sd.2049

Tamimi, N. & Sebastianelli, R. (2017) Transparency among S&P 500 companies: an analysis of ESG disclosure scores. Management Decision, 55(8), 1660–1680. https://doi.org/10.1108/MD-01-2017-0018

Van der Waal, J., Thijssens, T. & Maas, K. (2020). The innovative contribution of multinational enterprises to the Sustainable Development Goals. Journal of Cleaner Production, 285, 125319. https://doi.org/10.1016/j.jclepro.2020.125319

Van der Waal, J., Thijssens, T. & Maas, K. (2021). Corporate involvement in sustainable development goals: exploring the territory. Journal of Cleaner Production, 252, 119625. https://doi.org/10.1016/j.jclepro.2019.119625

Velte, P. (2017). Does ESG have an impact in financial performance? Evidence from Germany. Journal of Global Responsibility, 8(2), 169–178. https://doi.org/10.1108/JGR-11-2016-0029

Xia, D., & Wang, X.-Q. (2020). The synergetic impact of environmental and innovation information disclosure on corporate financial performance: An empirical study based on China coal listed companies. Technovation, 102179. https://doi.org/10.1016/j.technovation.2020.102179

Wang, D., Li, X., Tian, S., He, L., Xu, Y., & Wang, X. (2021). Quantifying the dynamics between environmental information disclosure and firms’ financial performance using functional data analysis. Sustain. Prod. Consum, 28, 192–205. https://doi.org/10.1016/j.spc.2021.03.026

Wang, S., Wang, H., Wang, J., & Yang, F. (2020). Does environmental information disclosure contribute to improve firm financial performance? An examination of the underlying mechanism. Science of The Total Environment, 714, 136855. https://doi.org/10.1016/j.scitotenv.2020.136855

Yoon, B., & Chung, Y. (2018). The effects of corporate social responsibility on firm performance: A stakeholder approach. Journal of Hospitality and Tourism Management, 37, 89–96. https://doi.org/10.1016/j.jhtm.2018.10.005

Información adicional

redalyc-journal-id: 4775