2026

25

24102025

01122025

Yussuf Masoud ymasoud024@gmail.com

Edwin Musheiguza musheiguzae@gmail.com

Abstract: The aim of this study was to examine the moderating effect of political interference on procurement performance in Tanzania's parastatal entities. Specifically, the study examined the moderating effect of political interference on ethical practices and internal auditing toward achievement of procurement performance in the parastatal organizations in Tanzania and make recommendations for improvement. The structural questionnaire was used to collect data from heads of departments from 93 state-owned organizations in the Dar es Salaam Region. The sample of 256 respondents were randomly selected using the Yamane formula from the population of 712 heads of departments. Out of 256 questionnaires that were distributed to the respondents, 241 were collected promptly filled and were used for analysis. The data were descriptively analyzed to establish the mean and standard deviation. Following that, the data were compiled using frequency distribution tables before being analyzed using a structural equation model. The findings show that political interference negatively affects procurement performance by undermining the internal audit function and ethical practices among the procurement function within the parastatal organizations in Dar es Salaam. The study recommended that the management of the parastatal organizations should institute effective control mechanisms by ensuring that the politicians should not get room to interfere with the procurement process. This study adds to a new body of knowledge as there are few studies that have studied these variables in parastatal organizations in sub-Saharan Africa.

Keywords: Political interference, Ethical practices, Internal auditing Staff Competence, Procurement performance.

Artigos

INFLUENCE OF ETHICAL PRACTICES AND INTERNAL AUDITING ON PROCUREMENT PERFORMANCE AMONG PARASTATAL ORGANIZATIONS IN DAR ES SALAAM REGION: THE MODERATING ROLE OF POLITICAL INTERFERENCE

Recepción: 24 Octubre 2025

Recibido del documento revisado: 18 Noviembre 2025

Aprobación: 01 Diciembre 2025

Publicación: 26 Enero 2026

Public procurement is one of the most crucial functions in government organizations. It deals with the acquisition of all requirements by the organization, starting with the construction projects, delivery of services, and supplies of goods (Lăzăroiu et al., 2020). It accounts for about 29% of total general government expenditure in Organization for Economic Co-operation and Development (OECD) countries and closer to 50% of public spending in developing countries (OECD, 2019; Dávid-Barrett & Fazekas, 2020). In Tanzania, the public procurement is considered the country’s second largest government expenditure after personnel emoluments (Kajimbwa, 2018). Due to the magnitude of money used in public procurement, many governments throughout the world have been forced to undertake a lot of reforms to ensure that there is efficiency in procurement and that value for money is achieved from the procured goods, works, or services (Changalima et al., 2022; Masoud, 2023).

Regardless of the various reforms implemented by governments around the world, procurement performance is not impressive (Changalima et al., 2022, Rendon and Rendon, 2016). Governments have enacted and amended public procurement regulatory frameworks, implemented an e-procurement system, and conducted continuous procurement audits, but their performance has been inadequate (Yussuf et al., 2021; Dávid-Barrett & Fazekas, 2020; Sarawa & Masu'd, 2019). According to studies, the procurement process is still associated with poor quality goods, long bureaucratic procedures, corruption, late delivery or completion of projects, cost overruns, a lack of transparency, a lack of competition, ineffective monitoring system and the like (Mahmood, 2010; Hui et al., 2011; Rendon and Rendon, 2016; Nemec et al., 2020).

Because of poor procurement performance in many parts of the world (Rendon and Rendon, 2016; Dávid-Barrett & Fazekas, 2020). Many scholars have been drawn to study in this sensitive function within the public sectors, in order to find out the causes of this misery and come up with constructive resolutions aiming to improve its status and values for money to be realized, which may undoubtedly ensure the availability of public services to the majority of citizens in developing countries, who are still suffering from getting better education, clean water, good health services, passable transportation, and passable housing (Changalima, et al., 2022, Masoud, 2023). For instance; Some scholars have highlighted those unethical practices among the professionals, conflict of interest, ineffective internal auditing functions, and a lack of staff competence, political interference have recently become overwhelming issues in procurement performance (Sarawa and Masu’d, 2019; Matto, 2021; Changalima and Mdee, 2023).

According to Goldman et al. (2013), political boards connected to the current ruling political party in the United States (US) have an influence over contract awarding. Hui et al. (2011) claim that politicians in Malaysia influenced the procurement procedure by instructing procurement officers to give contracts to their affiliated businesses. Purnomo et al. (2018) established that a number of factors, including political meddling and a lack of staff competence, have an impact on Indonesia's procurement performance. Furthermore, unethical procurement practices are a recurring disaster in Bangladesh procurement and supply chain, as Mahmood (2010) revealed that corruption and mismanagement have been a poor scenario in public procurement, resulting in the loss of public funds, with nearly $3 billion lost each year as a result of public procurement corruption.In a similar vein, procurement officers in India choose procurement methods and evaluate tenders in violation of applicable laws and regulations in order to profit personally from procurement transactions (Schnequa & Alexandru, 2012). On the other hand, the lack of an effective internal auditing unit has been linked to poor procurement performance within the procuring entity as a result of the failure to detect associated malpractices and fraud prior to losses occurring (Badara, 2012; Boateng et al., 2014). While Yusof et al. (2019) claims that the lack of independence of the internal audit function in Malaysia is a major cause of its ineffectiveness, he fails to highlight weaknesses in the procurement function in many Malaysian public-sector organizations.

In Ghana for instance, the studies show that politicians interfere with the procurement process by appointing the procurement officer, selection of suppliers, the selection of procurement method and procurement planning (Chikwere et al., 2019 as Nuertey et al., 2018): In South African as revealed by Myeza et al. (2022) public procurement is challenged with lack of knowledge of procurement legal frameworks, inadequate planning and monitoring in the procurement process, corruption and unethical behavior and political interference. Basheka (2011) in Uganda argued that politicians interfere with procurement processes by ensuring that contracts are awarded to companies or their allies. As Gilly and Patrick (2015) demonstrate, procurement performance in Kenya is harmed by a lack of transparency, ineffective competitive bidding, a lack of professionalism, and substandard sourcing and certain politicians use any means necessary to secure lucrative contracts for their enterprises. In Nigeria as portrayed by Ezinwa et al. (2020) many organizations lack skilled and competent procurement personnel, which lead to poor performance of the procurement function.

The United Republic of Tanzania as many other countries, its procurement function is not without challenges. As Mtasigazya (2019) indicates that politicians influence tenders to benefit their firms or their allies. The radar and the Richmond Saga are vivid illustrations of how political interference affects Tanzania's procurement process (Gray, 2015). Also, Pastory (2019) revealed that politician’s interference the procurement plan. He went further by insisting that some politicians provide order to undertake certain projects which are out of procurement plan and without allocated funds. Additionally, unethical procurement practices have been observed across a range of industries, and numerous incidents have been linked to corruption and malpractice (PPRA, 2018). According to Controller and Auditor General (CAG) report of 2023 shows that the Ministry of Health did not sign a formal contract with UNICEF for the purchase of motor vehicles worth TZS 10.75 billion. Also, there was a delay in the delivery of these motor vehicles, which was agreed to be delivered in August 2022; however, up until the time of auditing (December, 2022), the delivery was not undertaken.

Additionally, the CAG report of 2023 shows that the contractor, M/s Tanjo Builders Company Limited, who was engaged by TANROADS-Rukwa for construction projects had abandoned the project worth TZS 903.60 million. There were procurements from different ministries using a single source and restricted tendering without justification valued at TZS 6.01 billion and delayed completion of construction projects worth TZS 197.36 billion across government institutions. Also, malpractices were evidenced in the Ministry of Education, Science, and Technology (MoEST), and Shenzhen Benton Technology Company Limited signed a contract for the supply of 150,000 tablets for USD 20.28 million (TZS 46.86 billion), which was not sent to the Attorney General for vetting. Also, studies show that public funds are misappropriated due to ineffective internal auditing functions and a staff shortage of procurement expertise (Yussuf et al., 2021).

Numerous studies have been conducted to investigate the factors affecting procurement performance on organizations, for instance; Panga and Mahuwi (2020) examined the effect of procurement planning, monitoring and staff training on the procurement performance among public higher learning institutions. Kirai and Kwasira (2016) investigated the factors influencing procurement performance in Kenya, including the effect of resources allocation, staff competence, stakeholder influence and procurement planning. Additionally, Changalima and Mdee (2023) examined the factors that contribute to poor procurement performance in Tanzania, focusing on the effects of procurement skills mediating with procurement planning. Despite the available principles underlined with procurement practices, still, in some instances, political leaders provide guidelines and insights which require procurement professionals to act immediately. However, this possible influence of directives and interferences from political leaders on procurement performance has not been exhaustively examined. This study seeks to close this gap by examining the moderating effects of political interference on the relationship between ethical procurement practices and internal auditing, on procurement performance among parastatal organizations in Dar es Salaam, Tanzania.

This study is extremely important because the results may help parastatal organizations identify the factors that negatively affect their performance and determine the best ways to improve it. It is well known that public procurement consumes more than half of the annual budget for most developing countries. (OECD, 2019; Dávid-Barrett & Fazekas, 2020). As a result, their improper use costs the public organization a lot of money. On the other hand, it results in significant misery and suffering for the general populace as it denies them access to services like clean water, better healthcare, reliable transportation, and other fundamental amenities that the majority of civil society still lacks.

i) To determine the effect of ethical procurement practices among procurement officers on procurement performance in the parastatal organisations in Dar es Salaam region.

ii) To examine the effect of internal auditing on procurement performance in the parastatal organisations in Dar e Salaam region.

iii) To examine the effect of political interference on procurement performance in parastatal organisations in Dar es Salaam region.

iv) To determine the moderating effect of political interference on the relationship between ethical practices and procurement performance among parastatal organisations in Dar es Salaam region.

v) To examine the moderating effect of political interference on the relationship between internal auditing and procurement performance among parastatal organisations in Dar e salaam region.

This study is grounded in the principal-agent theory. The theory explains the relationship between the principal and the agent: the principal hires the agent to carry out work on the principal's behalf (Jensen and Meckling, 1976; Moe, 1984). The theory assumes that both principal and agent are self-interested which lead to conflict of interest, and there is an information asymmetry that gives the agent discretionary authority (Eisenhardt, 1989). Scholars have proposed a number of monitoring mechanisms that can be used by the principal to mitigate the agent's interest behavioural patterns, like having a governing body, internal auditing unit, contract management team, and the like (Panda and Leepsa, 2017; Matto, 2021). In this study, the principal is the governing body of procurement entity and the agent is the procurement officer who have been hired to execute the procurement function. According to this study, the internal auditing function has been used as a monitoring mechanism that the procuring entity might use to monitor the agent when executing the contracted assignment to ensure that the agent performed as agreed (Jensen & Meckling, 1976; Panda & Leepsa, 2017). Therefore, this theory is very useful to this study as it shows to what extent the agent's divergent interests might affect the performance of the organization and the importance of having an internal auditing unit that minimizes the risks associated with the agent when executing the procurement function. However, this theory did not demonstrate the impact of the thirty-part intervention on the principal-agent relationship; consequently, stakeholder theory has been adopted to address this gap, as it appropriately encompasses the involvement of multiple participants in business operations.

Stakeholder theory was proposed by Freeman in 1984 who defined a stakeholder as any group or individual who can affect or is affected by the achievement of an organization's objectives, and identified four groups as stakeholders: suppliers, customers, investors, and employees. Friedman and Miles (2006) expanded the definition of stakeholder to include more types of stakeholders who may have an impact on the goals of an organization, such as the media, the general public, suppliers, government, regulators, political groups, trade associations, policymakers, and others.The stakeholder theory does not mandate that all stakeholders participate equally in all processes and decisions, according to Donaldson and Preston (1995). This implies that one type of stakeholder may participate in a given function to a much greater extent than other types of stakeholders. For instance, empirical research reveals that, in contrast to other stakeholders, politicians often meddle in the procurement process (Boatemaa-Yeboah & Tamakloe, 2019; Nuertey et al., 2018; Sandada & Kambarami, 2016). Due to the degree to which politicians are linked to procurement performance (Chikwere et al., 2019; Sarawa & Mas' ud, 2020), this study has chosen to use them as one type of stakeholder.

Ethical behavior entails avoiding conflicts of interest and not abusing one's position (Kabubu et al., 2015). When performing the procurement function, procurement practitioners are required to adhere to a code of ethics (Mrope, 2018). They are expected to abstain from the conflicts of interest and corruption that frequently impair procurement performance (Obicci, 2015; Masoud, 2023). Due to the critical nature of procurement, professionals adhering to a code of ethics is a paramount aspect. As a result, the Procurement and Supplies Professionals and Technicians Board (PSPTB) created Code of Ethics and Conduct No. 365 of 2009 and required all procurement and supplies professionals to adhere to it when performing procurement and supplies functions. There is a need of ensuring that procurement functions are carried out diligently, efficiently, equitably, thoroughly, courteously, honestly, and truthfully, and with transparency (Lema and Mrope, 2018). The assumption in Figure 1 is that if procurement is conducted ethically and without political interference, procurement performance in parastatal organizations may improve significantly.

Ho1: Ethical practices among the procurement officers moderated by political interference have no significant effect on procurement performance in the parastatal organisations in Dar es Salaam region.

Internal auditing is a non-disclosure process that businesses use to minimize record-keeping errors, asset misappropriation, and fraud (Obeng, 2016). Due to the critical nature of internal auditing within an organization, Tanzania requires all procuring entities to have an internal auditing unit which is required to audit the organization’s operations, including the procurement function, and prepare audit reports quarterly (PPA, 2011). Effective internal auditing ensures that procurement malpractice and fraud are detected early and that appropriate action is taken to prevent the organization from incurring financial and other operational losses. (Yussuf et al., 2021). However, the studies indicate that, in addition to having an internal auditing function within the organization, procurement malpractice has been conducted in a number of procuring entities and has gone unnoticed.They are typically discovered during external audits such as of Controller and Auditor General(CAG, 2020, and CAG, 2021). The assumption in Figure 1 is that if internal auditing is conducted effectively and seriously without political interference, procurement performance in parastatal organizations may improve significantly.

Ho2: Internal auditing moderated by political interference has no significant effect on procurement performance in the parastatal organisations in Dar e salaam region.

Political interference occurs when senior officials and political leaders use their power to intervene in the procurement process for their own personal gain (Pillay, 2004). Political meddling in the procurement process is a widespread occurrence in the majority of third-world countries (Basheka, 2011; Thai, 2001). By understanding that the PPA of 2011 and its regulations attempt to protect the public interest by requiring that institutional organs within the procuring entity operate independently. However, contrary to regulatory requirements, political interference in the procurement process is a common occurrence; the cases of Richmond and the Rada saga serve as excellent examples (Gray, 2015). According to studies, politicians influence the procurement process significantly by awarding contracts, hiring procurement officers, and enacting procurement laws (Hui et al., 2011; Mando and Mutuku, 2017; Nuertey et al., 2018).

Ho3: Political interference has no significant effect on procurement performance in the parastatal organisations in Dar e salaam region.

The procurement process should be carried out in such a way that it brings value for money. The procured goods, works or services should be of the right quality, delivered at the right time and at a reasonable cost, but also satisfy the users’ departments; if the procurement process is undertaken while it does not ensure value for money and customer satisfaction, the whole procurement process may become useless (Lyson and Farrington, 2016).

The study employs an explanatory research design in order to establish a causal relationship between variables (Saunders et al., 2012). The study was conducted in the Dar es Salaam region because 70.5 percent (103) of all parastatal organizations are based there, and thus the findings may applicable throughout the country.

The sample size is calculated using a simplified Yamane Formula (1967) given by n=N/((1+Ne^2)) where n represents the number of samples required, N represents the target population, and e represents the level of confidence, which was set at 5%. Given the value of N = 712 (PPRA, 2018), the value of n =256. the number n =256 (approximated). So only 256 individuals were chosen from user departments out of a total workforce of 309 employees. The simple random sampling technique was used to select 256 study participants. The RANDBETWEEN excel command was used to randomly identify participants, after assigning them with unique identifiers from 1 to 712 based on their organizations of origin. In case, the selected number appears in the next stage, were skipped so as to avoid multiple selection of the same respondent. Respondents with numbers greater than 712 were recruited in the study. Confidentiality was highly maintained during this practice, by use of unique identifiers.

The data was gathered through the use of a standardized questionnaire. The questionnaires were distributed to randomly selected participants, and the drop-and-pick-later approach was adopted. However, in case the respondent is ready to out-fill the form immediately, this was in the favor of the researcher. All study items were measured using a five-point Likert scale ranging from 1 to 5.

The study used both descriptive and inferential analysis. Descriptively, the study summarized the data using frequency distribution tables. Data were summarized using frequency and percentages, and the measures of central tendencies were computed where appropriate. Inferentially, the study used structural equation model to determine the causal relationship between dependent and independent variables. All analyses were conducted using IBM SPSS version 26. Although IBM SPSS version 26 was used to conduct the descriptive analysis, the structural equation modeling (SEM) was carried out using the SPSS add-on tool "AMOS version 23." The analysis was divided into two stages: the first stage involved exploratory factor analysis (EFA) for testing the validity and reliability of the data. The second stage involved using confirmatory factor analysis (CFA) for testing the model fit indices, thereby allowing causal inferencing. This was achieved by the use of structural equation modelling which has the capability of taking into account of moderating effects as compared to the usual linear regression models.

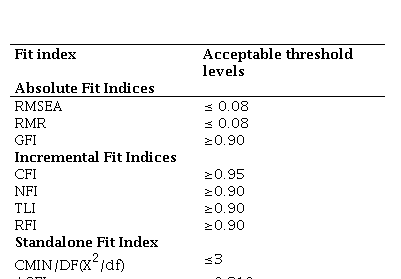

Based on EFA, the Keiser Meiyer Olikn Measure (KMO) was computed so as to determine the necessity of undertaking the EFA. The principal component analysis was undertaken as a part of the variable deduction technique, items with factor loadings above 0.5 were retained for further analysis. Study constructs were determined based on the number of components formulated after EFA, overlapping items were dropped from further analysis. The CFA involved testing the set of model fit indices. If the model fit indices assumptions are met, then we were confident with the obtained results for causal inferences. These indices include the Comparative Fit Index (CFI), Root Mean Square Error of Approximation (RMSEA), Goodness of Fit Index (GFI), Tucker Lewis Index (TLI) and the Ratio of Minimum Discrepancy to Degree of Freedom (CMIN/DF) as well as the Root Mean Square Residual (RMR). Both the structural and measurement models were formulated, thereby identifying that the basic cut-offs for each index are met (Hooper et al., 2008; Gupta and Singh 2015; Hair et al, 2006; Malhotra et al.,2017). A summary of these indices is as presented here below.

Moreover, to assess the moderating effect of PI on the relationship between IA and ETH on PP, the multigroup analysis was conducted. This was done after expressing PI as a summated score thereby categorizing into three levels, low (below 2.5), medium (2.5 to 3.5) and high (3.6 to 5). The medium group has observations below 50 which could not suffice for SEM. Therefore, we remained with two groups (low and high PI) for multigroup analysis. The measurement invariance, configural and metric invariance analysis was undertaken to determine the equivalence of measurement models and factor loadings across the two groups. After the invariance was observed, the final step was to test the identified hypotheses, the relationship was considered statistically significant at a 5% level.

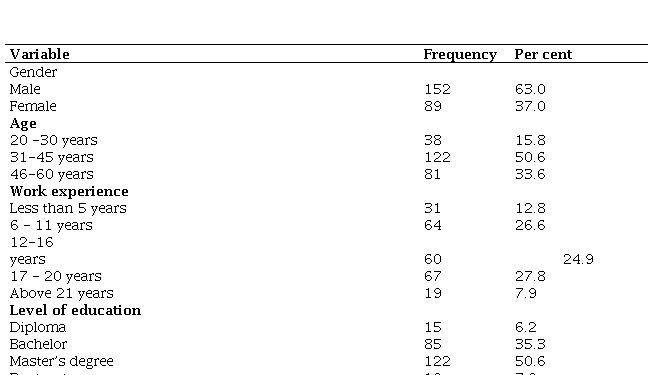

The assesses participant demographic characteristics included; gender, age, professional experience as well as level of education. The description on each of these variables is as presented here below.

The gender of the respondents was analyzed, revealing that male respondents constituted 152 (63.0%), whilst female respondents included 89 (37.0%). This indicates that males ascended to the apex of departmental leadership.

The respondents' ages were categorized for the descriptive analysis of this study. A majority of 122 individuals (50.6%) were aged between 31 and 45, while 38 individuals (15.8%) were aged between 20 and 30, and 81 individuals (33.6%) were aged between 46 and 60. A significant percentage of responders (84.2%) are intellectually capable people aged 25 and older.

31 (12.8 percent) of respondents possessed one to five years of experience. Sixty-four respondents (26.6 percent) possessed between 6 and 11 years of experience; sixty respondents (24.9 percent) had 12 to 16 years of experience; twenty-eight respondents (27.8 percent) had between 17 and 20 years, and nineteen respondents (7.9 percent) had above 21 years of experience. The results demonstrate that a significant percentage of respondents possess over five years of experience.

An analysis of the respondents' educational attainment indicated that 15 (6.2%) possessed a diploma, while 85 (35.3%) held a bachelor's degree. Among the responders, 122 (50.6%) possessed a master's degree, whereas 19 (7.9%) earned a PhD. The data indicates that a significant majority of respondents (93.2%) possessed a bachelor's degree or higher.

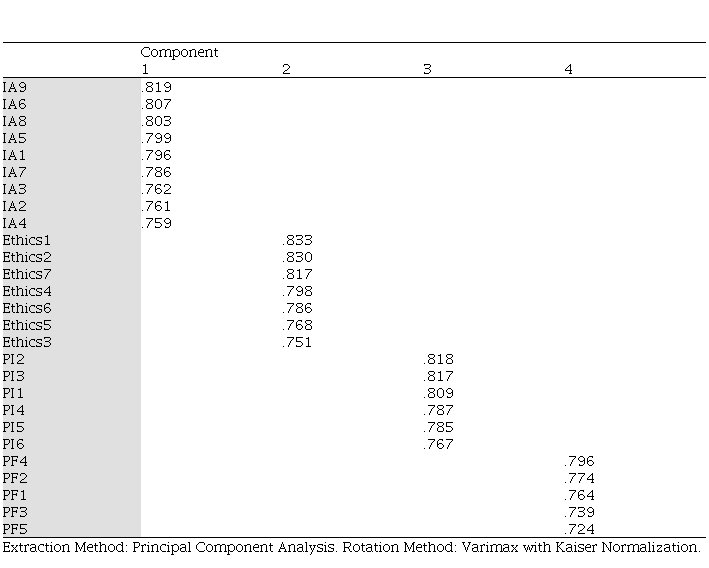

The EFA involved the assessment of items coherence in forming particular study constructs. Out of the 21 study items, only 4 constructs were formed following PCA. As presented in Table 3, each of the study item had a factor loading of at least 0.5.

The measurement models were constructed for both individual study constructs as well as the overall combination of study constructs. As recommended, each of the study constructs attained the minimum thresholds of 0.9 for CFI, TLI as well as RFI while RAMSEA was below 0.3 as depicted in Figure 2. These results imply that the models fitted well the data hence allowing for next step of formulating the overall measurement and structural models for assessing the postulated study hypotheses.

The measurement and structural models were constructed based on three different steps. The first step excluded the moderating variable (PI) while the second step involved the moderating variable, however the moderator was treated as an independent variable while the third step involved the use of a moderator (PI) for multigroup analysis. The Figure 3 presents the overall measurement and structural models of the study constructs before including the moderator. As expected, the minimum thresholds of 0.9 for CFI, TLI as well as RFI while RAMSEA was below 0.3 were attained hence implies that both the measurement and structural models fitted well the data, thus allowing for assessment of relationship between variables under consideration.

The Figure 4 presents the measurement and structural models when treating the PI as an independent variable. The results evidenced by the model fit indices with the minimum thresholds of 0.9 for CFI, TLI as well as RFI while RAMSEA was below 0.3 were underlining to our expectations. Moreover, these results allow for assessment of relationship between variables under consideration.

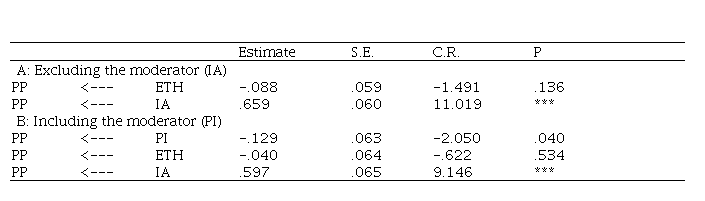

The influence of EP and IA on PP was assessed with and without accounting for PI. The study revealed the positive significant effect of IA on PP, as for each score increase in IA, the PP increased by 0.66 (p<0.001) when PI is not accounted for. However, the EP had a negative insignificant effect on PP at 5% level. Figure 3 and Table 4 (A).

Accounting for PI, still the IA had a statistically significant positive effect of 0.597 on PP at p<0.001. evenly, the ETH was revealed to have an insignificant negative effect on PP while a similar pattern was observed for PI although being statistically significant at 5% level. Figure 4 and Table 4 (B). This finding contradicts the finding of Israel et al. (2021), who revealed that ethical practices, which include issues of transparency, fairness, professionalism, and accountability, have a significant influence on procurement performance. In the same vein, the findings also contradict the findings of Odero and Machuki (2023), who revealed that procurement ethics has a significant influence on procurement performance.

The moderating effect of PI on the influence of EP and IA on PP was assessed by constructing the multigroup analysis using both the measurement and structural models as presented in Figure 5. The corresponding model fit indices as basic assumptions for SEM including CFI and TLI were within the prescribed cut-offs of above 0.8 while the RAMSEA was below 3 as recommended.

On top of the model fit indices, the measurement model showing the relationships between latent variables and observed indicators was equivalent across the groups low and higher level groups of PI. This means that the way in which latent variables were measured was the same across groups of PI. Moreover, the configural invariance assessing the same factor structure (the same number of factors and pattern of loadings) was revealed present in all groups while the metric invariance which assesses the factor loadings (i.e., the strength of the relationship between latent variables and their indicators) were equal across groups of PI.

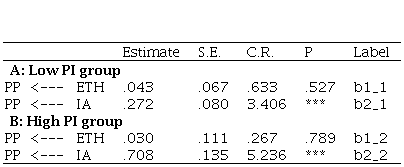

Looking on the moderating role of PI on the relationship between IA and ETH on PP, the results were presented as in Table 5 as obtained from Figure 5 (right). The study revealed that both IA and ETH had a positive effect on PP, however, the statistically significant effect was for IA on PP. Interpreted as for each score increase in IA, the PP increases by 0.272 among the group with low PI. Based on the group with high PI, we revealed that for each unit increase in IA, the PP increased significantly by 0.71 (p<0.001). This result is in line with the result of Karikari Appiah et al. (2023), who revealed that internal audit has a significant influence on procurement performance at Ghana organizations. Also, these findings concur with the finding of Gedion and Wanyama (2021), who revealed that the internal audit function has a significant impact on organization financial performance. Furthermore, David (2019) demonstrated that internal audit competencies, procedures, and autonomy positively influence the contribution of internal audit to the efficacy of procurement operations in local government.

The above results implies that the influence of AI on PP was different across the groups of PI. This was evidenced by higher effects of 0.7 among the highest group of PI as compared to low group PI with 0.37. a similar observation was for the influence of ETH on PP, however in both groups of PI, the non-statistically significant positive effect was observed with a slightly difference of 0.04 and 0.03 for the low and high group PI respectively. This finding is in line with the findings of Masoud (2023) who revealed that political interference has positive effect on procurement performance. Also, Nuertey et al. (2018) concurred with the finding that political interference had significant effects on procurement functions in Ghana. The researchers further demonstrated the various ways in which politicians interfered with the procurement process, including the selection of suppliers/contractors, the selection of procurement officials, the circumvention of the procurement process, and the selection of projects, all of which ultimately impacted the procurement's performance. Furthermore, Chikwere et al. (2019) concluded that political meddling is the main factor causing public institutions in Ghana to disregard procurement laws.

The objective of this study was to examine the moderating effect of political interference on procurement performance in Tanzania's parastatal entities. Specifically, the study examined the moderating effect of political interference on ethical practices and internal auditing toward the achievement of procurement performance in the parastatal organizations in Tanzania. The study found that the political interference has a negative influence on ethical practices as well as the internal auditing function. Therefore, the study suggests that the management of the parastatal organizations should institute effective control mechanisms by ensuring that the politicians should not get room to interfere with the procurement process, as their interference has a bad reputation for the organizations. Finally, it is important to acknowledge the study's limitations, as they can guide future research. This study only focused on the public sector by examining the moderating effects of political interference on ethical practices and internal auditing functions. Therefore, this study suggested that other researchers may study in private sectors and use the same or other factors to assess their influence on organizational performance.

redalyc-journal-id: 4775