Artigos

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial 4.0 Internacional.

Recepción: 07 Marzo 2024

Aprobación: 19 Junio 2024

Publicación: 09 Julio 2024

DOI: https://doi.org/10.19094/contextus.2024.93100

Abstract:

Background: Cryptocurrency assets, known for their high risk, have seen a significant increase in the number of users, driven by the search for new investment opportunities and portfolio diversification. This research aims to explore and evaluate the factors that determine the intention and behavior of investing in cryptocurrencies.

Purpose: The main objective of the study is to understand the effects of the intention to invest in cryptocurrencies using a behavioral theory, adding cultural moderation to the investment behavior model.

Method: Quantitative research that uses the Unified Theory of Acceptance and Use of Technology (UTAUT) as the theoretical lens, the research applied an online questionnaire and obtained 222 valid responses for analysis, data collected from February to May 2021. Data analysis was based on structural equation modelling, with estimation using the partial least squares method.

Results: The results revealed the contribution that UTAUT has on the intention to invest in cryptocurrencies, and that the variables of performance expectancy, social influence and facilitating conditions affect the intention to invest in cryptos.

Conclusions: The level of education, in the sample represented by the majority of risk-prone investors, was a significant and moderating factor in the variations in the result of using the UTAUT in the context of the behavior of cryptocurrency investors.

Keywords: cryptocurrencies, UTAUT, culture, level of education, investor behavior.

Resumo:

Contextualização: Os ativos de criptomoedas, conhecidos por seu alto risco, têm registrado um aumento significativo no número de usuários, impulsionado pela procura por novas formas de investimento e pela diversificação de portfólios. Esta pesquisa se propõe a explorar e avaliar os fatores que determinam a intenção e o comportamento de investimento em criptomoedas.

Objetivo: O objetivo principal do estudo é compreender os efeitos da intenção de investir em criptos usando uma teoria de comportamento, acrescentando ao modelo a moderação cultural no comportamento de investimento em criptomoedas.

Método: Pesquisa quantitativa que utiliza a Teoria Unificada da Aceitação e Uso da Tecnologia (UTAUT) como lente teórica, a pesquisa aplicou um questionário on-line e obteve 222 respostas válidas para análise, dados coletados de fevereiro a maio de 2021. A análise de dados partiu da modelagem de equações estruturais, com estimação pelo método partial least squares.

Resultados: Os resultados revelaram a contribuição que a UTAUT tem na intenção de investir em criptomoedas, e que as variáveis de expectativa de performance, influência social e condições facilitadoras afetam a intenção de se investir em criptos.

Conclusões: O nível de escolaridade, na amostra representada de maioria investidores propensos ao risco, foi fator significativo e moderador das variações no resultado do uso da UTAUT no contexto do comportamento de investidores em criptomoedas.

Palavras-chave: criptomoedas, UTAUT, cultura, nível de escolaridade, comportamento do investidor.

Resumen:

Contextualización: Los activos de criptomonedas, conocidos por su alto riesgo, han registrado un aumento significativo en el número de usuarios, impulsados por la búsqueda de nuevas formas de inversión y la diversificación de carteras. Esta investigación se propone explorar y evaluar los factores que determinan la intención y el comportamiento de inversión en criptomonedas.

Objetivo: El objetivo principal del estudio es comprender los efectos de la intención de invertir en criptomonedas utilizando una teoría del comportamiento, añadiendo al modelo la moderación cultural en el comportamiento de inversión en criptomonedas.

Método: Investigación cuantitativa que utiliza la Teoría Unificada de Aceptación y Uso de la Tecnología (UTAUT) como lente teórica, la investigación aplicó un cuestionario en línea y obtuvo 222 respuestas válidas para el análisis, datos recogidos de febrero a mayo de 2021. El análisis de datos se basó en el modelado de ecuaciones estructurales, con estimación mediante el método de mínimos cuadrados parciales.

Resultados: Los resultados revelaron la contribución que tiene la UTAUT sobre la intención de invertir en criptomonedas, y que las variables de expectativa de desempeño, influência social y condiciones facilitadoras afectan la intención de invertir en criptomonedas.

Conclusiones: El nivel de educación, en la muestra representada por la mayoría de inversores propensos al riesgo, fue un factor significativo y moderador de las variaciones en el resultado del uso de la UTAUT en el contexto del comportamiento de los inversores en criptodivisas.

Palabras clave: criptodivisas, UTAUT, cultura, nivel de educación, comportamiento de los inversores.

1 INTRODUCTION

Cryptocurrency is an innovative investment alternative worldwide, considered a high-risk asset in a market with exponential user growth (Borri, 2019). This asset moves more than trillions in capitalization (Coinmarketcap, 2024) and experts believe that the future will bring a natural integration of the cryptocurrency market with the capital market, more than what is already seen today. It is no longer believed in the extinction of this asset, but rather in the various forms of integration and possibilities of cryptocurrencies with the world (Donatelli & Colombo, 2021).

This behavior of investing in cryptocurrencies was researched in the unstable and insecure moment of the COVID-19 pandemic, where people reacted asymmetrically in their investments compared to the advance of the disease (Iqbal, Fareed, Guangcai & Shahzad, 2020). Thus, the cryptocurrency market environment has remained attractive and increasingly capitalized during the pandemic (Conlon et al., 2020; Corbet et al., 2018; Lahmiri & Bekiros, 2020).

In studies on investment behavior, various theories seek to explain this phenomenon. One of them, the one used in this study, is the Unified Theory of Acceptance and Use of Technology (UTAUT) (Venkatesh et al., 2003), which seeks to understand investment intention in the context of cryptocurrencies.

However, when different authors apply these theories to study crypto investment, they come up with different results. Jung et al. (2018) conducted research on investment intention in China, Vietnam and Korea, and attributed the inconsistencies found to the different cultural contexts of these countries. For example, the authors suggest that, in Korea, where a long-term cultural orientation prevails, the willingness to take risks is greater than in Vietnam. Thus, investment in cryptocurrencies tends to be more significant in Korea than in Vietnam.

Shahzad et al. (2018) and Walton & Johnston (2018) suggest, in the limitations of their research, that individual culture interferes and can explain the differences in the results of what impacts the intention to invest in cryptocurrencies. For example, the social influence construct in Nseke's (2018) research carried out in Africa has a significant impact on the intention to invest in cryptocurrencies. On the other hand, in Spain, the same social influence was not significant for cryptocurrency investment (Oliva et al., 2019).

Therefore, given the differences in the behavior of investing in cryptocurrencies in these countries, there is a gap in the literature related to the impacts of cultural moderation between the intention to invest and the purchasing behavior of each individual, which should change depending on the country analyzed.

Therefore, the objective of this study is to analyze the factors that influence the intention and behavior of investors to invest in cryptocurrencies and to understand the impact of cultural moderation on this behavior in Brazil.

To provide evidence of these relationships, this study used determinants of investment in cryptocurrencies, used in the international literature on the subject (Kwateng et al., 2019), Jung et al, 2018; Williams, et al., 2015), components of the Unified Theory of Acceptance and Use of Technology (UTAUT) (Venkatesh et al., 2003),, components of the Unified Theory of Acceptance and Use of Technology (UTAUT) (Venkatesh et al., 2003), considering the technological and innovative nature of this asset. As seen in the literature, it is important to add the variable of perceived risk in the model tested, since the essential treatment is in the applicability of cryptocurrencies as an investment (Nseke, 2018; Oliva et al., 2019).

The moderation of culture was captured through two of Hofstede's (2001) cultural dimensions, as these indicated significantly high results in Brazil. Hosfstede (1980) provided a detailed analysis of how national culture is an important dimension in organizations and is appropriate for different groups at the organizational and professional levels. Hosfstede (1980) deals with cultural indicators in technology companies, and this metric is more contextualized to test culture in cryptocurrency investment intentions, as these carry technological characteristics.

Therefore, this study contributes to the literature by highlighting the understanding of the sustainability of cryptocurrencies in the financial markets. It also adds to discussions about the rationality of high-risk investment intentions and the impact of schooling on these investments. In practice, considering that superpowers such as China are in the process of testing their own digital currency, studies on cryptocurrencies are valid, as they provide evidence that the future may belong to this technology (Shen, 2021). Finally, as a practical implication, this research helps cryptocurrency developers, policymakers, investors and companies that adopt a sharing economy model to think about the determinants of investment in these high-risk alternatives.

2 THEORETICAL FRAMEWORK

Lahmiri and Bekiros (2020) and Conlon et al. (2020) examined that, during the global COVID-19 pandemic, cryptocurrency markets were considered to be more unstable and irregular. At the time of writing, research shows that investors analyze the advance of the disease in the world in order to position their investments in cryptos (Sahoo, 2021) and diversify their portfolio towards cryptocurrencies in order to obtain short-term gains (Iqbal et al., 2020; Rognone, et al. 2020). This reinforces the curiosity of what would lead people to the financial behavior of investing in cryptocurrencies.

To understand what drives people to invest in cryptocurrencies, research analyzes the intention that precedes the behavior or the final purchase action (Abramova & Böhme, 2016; Folkinshteyn & Lennon, 2016; Walton & Johnston, 2018; Shahzad, 2018; Mutambara, 2019; Oliva, Borondo & Clavero, 2019; Agustina, 2019; Alkashri, Alqaryouti, Siyam & Shaalan, 2020). Authors such as Venkatesh et al. (2012), Fishbein and Ajzen (1975), Fishbein and Ajzen (1980) and Davis (1986) have built some of the Behavioral Intention Theories and their variables in the literature with regard to purchase intention.

UTAUT, one of these theories, has a theoretical framework that contributes to studies on technological, innovative and disruptive phenomena, which are characteristic of cryptocurrencies (Oliva et al., 2019). This theory was designed to explain how an emerging technology is accepted by people and organizations (Kwateng et al., 2019), with three main determinants or predictors of user behavioral intention: (i) performance expectancy, (ii) effort expectancy and (iii) social influence (Venkatesh et al., 2003). The model also adds a direct relationship between facilitating conditions and investment behavior. The behavior intention construct is understood as a predisposition to consume and the investment behavior construct is the final action already taken (Venkatesh et al., 2003).

2.1 Theoretical model

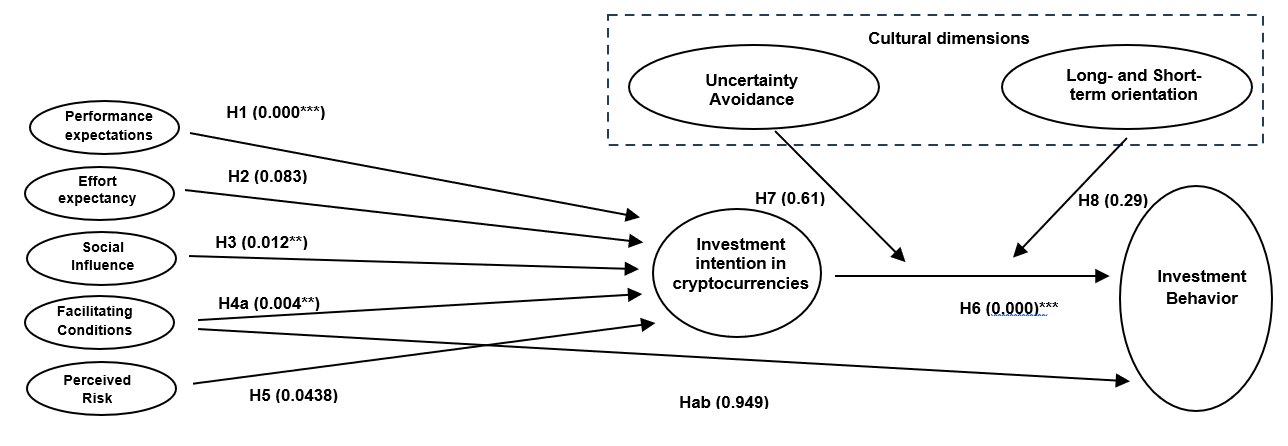

After compiling the initial considerations, the proposed model is composed of the UTAUT theory, as it carries the constructs that best capture the intention to invest in cryptocurrencies, appropriately capturing social aspects and external facilitators, as well as technological factors of cryptocurrencies (Jung et al., 2018). Hypotheses H1 to H4 and H6 emerged from the UTAUT. A construct that has proved important in cryptoasset investment research was added to the model: perceived risk, as shown in hypothesis H5. In the cultural hypotheses taken from Hofstede's (2003) understanding of a country's culture, to analyze an individual's cultural moderation between the intention and behavior to invest, follow the hypotheses H7 and H8.

Figure 1

Proposed model

Source: Developed by the author.

This research uses an adaptation from the models used by Baptista and Oliveira (2015) and Khan et al. (2017), who studied the adoption of Internet Banking in African countries and Pakistan, respectively, being more compatible, robust and, in part, similar to the model of this research, shown in Figure 1. In this model, in addition to analyzing UTAUT in Brazil, cultural moderation is added between behavioral intention and the behavior of investing in cryptocurrencies.

2.2 Performance expectations

Venkatesh et al. (2003) explained that performance expectancy is considered the most important predictor of behavioral intentions. Given the purpose of investment, to generate profitability, cryptocurrencies are inserted into investment portfolios to add profitable performance (Conlon et al., 2020). Gil-Alana et al. (2020) identified a potential role for cryptocurrencies in investor portfolios as a significant diversification option for investors, with particular emphasis on Bitcoin and Ethereum. In Spain, the study by Oliva et al. (2019), performance expectations had the greatest impact on investment intentions. Therefore, the more useful the purchase of cryptocurrencies is in the individual's cognitive perception, the greater their intention to invest:

H1: The expectation of performance has a positive influence on the intention to invest in cryptocurrencies.

2.3 Effort expectancy

Effort expectancy measures the degree to which the emerging technology is easy to use, more precisely its complexity (Venkatesh et al., 2003). The expectation of effort is similar to the idea of ease of use, used by the technology acceptance model (TAM) (Nseke, 2018), which has been tested in cryptocurrencies by researchers such as Abramova and Bohme (2016), who point to access passwords and difficulty in purchasing as insignificant factors in the intention to invest.

Therefore, people are not influenced by the complexity of the keys and systems to buy cryptoassets. However, Folkinshteyn and Lennon (2016) and Shahzad et al. (2018) present contrary results, showing that cryptocurrencies have instant transfers and an easy-to-use interface, which is relevant to the intention to invest. This gives rise to the second hypothesis of this research:

H2: The expectation of effort has a positive influence on the intention to invest in cryptocurrencies.

2.4 Social Influence

Venkatesh et al. (2003) said that social influence is the degree to which a person listens to and is influenced by the opinions of other people. Social influence has a strong impact on individual perceptions and user mentality when it comes to adopting new technologies (Davis, 1989; Venkatesh & Davis, 1996). In this case, the individual is sensitized by external communication interference, which has a significant influence on the individual's life, making them feel professional and modern when adopting cryptocurrencies (Oliva et al., 2019). Social influence, via the web, promotes positive cross-correlation results between web traffic, social network attributes and cryptocurrency performance indicators, significantly impacting cryptocurrency market capitalization, trading volume and price (Park & Park, 2020; Nseke, 2018). Therefore:

H3: Social influence has a positive impact on the intention to invest in cryptocurrencies.

2.5 Facilitating Conditions

Facilitating condition is the perception that the existence of infrastructure and organization helps in the use of technology, the perception of a favorable or unfavorable environment for action (Venkatesh et al, 2003). In this variable, in particular, the UTAUT model brings the influence of facilitating conditions directly to bear on behavior (Venkatesh et al, 2003). However, Venkatesh et al. (2012) adapts UTAUT to the context of consumer use of technology, claiming that the environment available to each investor varies, which would lead to variation in access to investment brokers, investment devices and so on. Therefore, facilitating conditions will influence both intention and behavior (Venkatesh et al. 2012).

To invest in bitcoins, for example, one must use the internet, as well as having skills and knowledge about security and purchasing systems (Bunjaku, Gjorgieva-Trajkovska & Miteva-Kacarski, 2017). An investor who has access to a favorable set of conditions that make it easier, such as a step-by-step process or customer service support, will have a greater intention to use (Baptista & Oliveira, 2015). The facilitating condition has already been shown in tests in other countries to have a significant influence on intention and behavior when it comes to investing in cryptocurrencies (Oliva et al., 2019), which leads to the hypotheses:

H4a: The facilitating condition has a positive influence on the intention to invest in cryptocurrencies.

H4b: The facilitating condition has a positive influence on investment behavior.

2.6 Perceived risk

It is worth clarifying that the UTAUT does not include the perceived risk construct. However, following the reasoning of several researchers on the subject of cryptoasset investment, such as Abramova and Bohme (2016), Folkinshteyn and Lennon (2016), Walton and Johnston (2018) and Oliva et al. (2019), this research also includes in its model the analysis of perceived risk as an important predictor of behavioral intention.

After Bauer (1960) presented the theory of perceived risk, several authors included the relevance of this variable in their research. Due to their predominantly volatile nature, cryptocurrencies have become high-risk investment speculation assets, with risk itself being the language perfectly included in the literature to understand everything from price phenomena (Möser et al., 2014) to investment intentions (Folkinshteyn & Lennon, 2016).

As Abramova and Bohme (2016) point out in their research on bitcoins, the significance of the risk is high and is due, in part, to the fluctuating value, the risk of financial losses in the event of a malfunction and a breach of the security of service provider systems or users' own devices. This reinforces the importance of perceived risk in predicting behavioral intentions. The view of perceived risk is identified with the doubtful feelings and tension of cryptocurrency acceptance. So, the hypothesis is given:

H5: Perceived risk has a negative influence on the intention to invest in cryptocurrencies.

2.7 Investment Intention and Investment Behavior

Following the understanding of UTAUT, which argues that individual behavior is predictable and influenced by individual intention (Yu, 2012; Baptista & Oliveira, 2015; Khan et al., 2017), this psychological model supports the belief that behavioral intention has a substantial influence on final behavior (Venkatesh et al., 2003), thus on investment. This influence has been studied and found to be significant in research with other objects of study (Baptista et al., 2015). So, here's the hypothesis:

H6: The intention to invest in cryptocurrencies has a positive impact on usage behavior.

2.8 Culture

Works such as Hofstede's (1980) have gained importance and influence in the analysis of countries' culture, as he collects and analyzes a robust empirical base from many countries on five dimensions of culture. Hofstede's (1980) data collection was carried out in technology companies, which is an analysis of organizational culture, which is more familiar with the investment environment analyzed in this research.

Relevant to the study of investment behavior, and with high significance in Brazil, only two of Hofstede's (2001) dimensions were chosen: (i) uncertainty avoidance index (UAI), (ii)long versus short-term orientation (LTO).

The dimension of uncertainty avoidance (UC) measures the degree of discomfort of each individual in the face of uncertainty. Countries with a high degree of aversion maintain their strong beliefs and behaviors, such as Brazil, which has a high uncertainty, avoidance with a score of 76, being conservative, a strategy for market consolidation, confirmed by a complex framework of laws for various social regulations (Hofstede, 2003; Hofstede et al., 2010). Individuals who avoid uncertainty will be less inclined to invest in cryptos (Abramova & Bohme, 2016). Cryptocurrencies are classified as a high-risk diversifying investment. Therefore, high uncertainty aversion distances people from investing in the asset, given its volatility (Makarov & Schoar, 2020). Hence, the hypothesis is discussed:

H7: Uncertainty avoidance moderates (weakens) behavioral intention (BI) and use behavior (UB).

The long-term orientation dimension means fostering virtues oriented towards future rewards, in particular perseverance and thrift (Hofstede, 2001). Brazil has a high long-term orientation, with persistence and adaptation to new circumstances, and is therefore considered to be a society that is adept at change and transformation, with forward-looking values (Hofstede, 2003). Cryptocurrencies, despite their characteristics as a risky asset, are incorporated into a disruptive technology and with the possibility of future rewards, long-term countries are more likely to invest in them. So, the hypothesis arises:

H8: Long/short term moderates (strengthens) behavioral intention (BI) and usage behavior.

3 METHODOLOGY

The aim of this study is to analyze the factors that influence the intention and behavior of investors with different levels of education to invest in cryptocurrencies and to understand the impact of cultural moderation on this behavior. To achieve these objectives, the research method chosen is primary data collection using a quantitative, descriptive and cross-sectional approach.

A non-probabilistic method was used and data was collected using a structured questionnaire, which was applied online using Google Forms. The study population is made up of anyone who intends to invest in cryptocurrencies in Brazil, thus allowing for a cultural separation of this country.

The questionnaire began with a paragraph explaining the purpose and target audience of the survey. For population control purposes and to reach this target audience, the following questions were initially inserted: "Have you ever heard of cryptocurrencies?", "Have you ever heard of bitcoin?" and "Do you want to invest in cryptocurrencies?". If the participant answered "yes" to all three questions, they were assigned to the rest of the questionnaire, while anyone who answered "no" to one of these questions was excluded from the database.

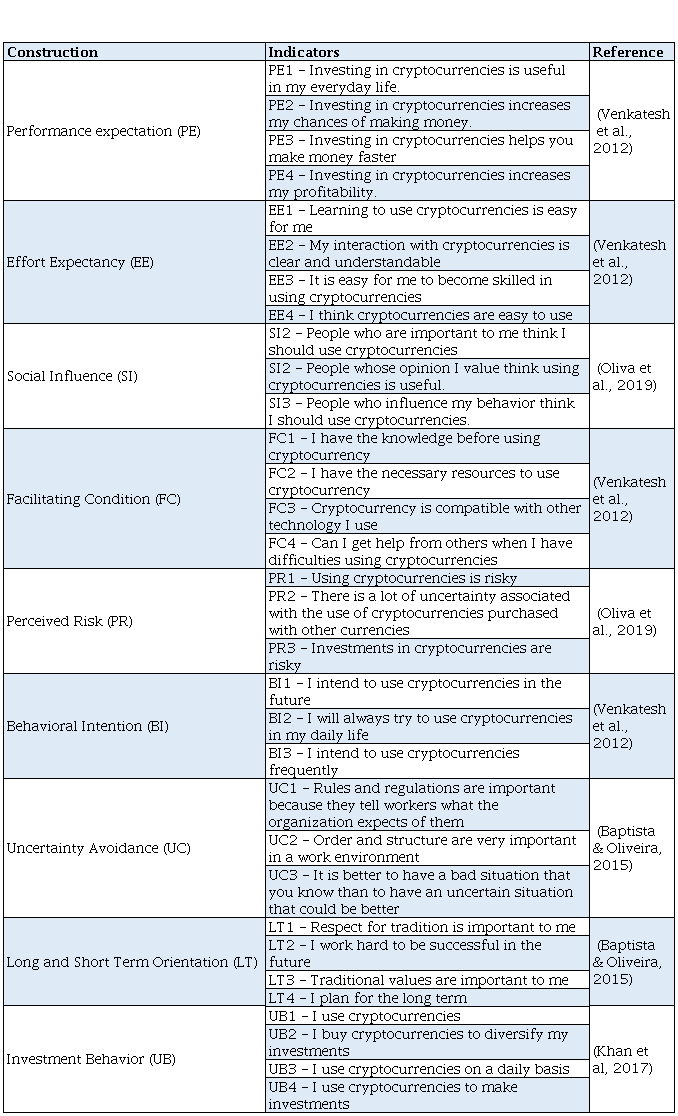

The constructs were evaluated based on 32 statements, answered on a seven-point Likert scale, ranging from 1 (totally disagree) to 7 (totally agree). The constructs were measured using scales already validated by Davis (1986), Venkatesh and Davis (2000), Venkatesh, Morris et al. (2003), and adapted to the context being measured.

The performance expectancy, effort expectancy and facilitating conditions constructs were adapted from Venkatesh et al. (2012), containing four statements each. Behavioral intention was measured using the scale by Venkatesh et al. (2012) and has three statements. The social influence and perceived risk constructs were measured using the Oliva et al. (2019) scale, with three statements. Investment behavior was measured using the scale by Khan et al. (2017). Where necessary, the wording of the items has been adapted to cryptocurrencies.

In the constructs of cultural moderators, uncertainty aversion and long and short-term orientation, the questions are adapted from the scale by Baptista and Oliveira (2015), containing three and four questions respectively. The complete table of constructs and their indicators used in the research can be found in Appendix A.

At the end of the questionnaire, all participants were asked to provide information about their sociodemographic data: age, gender, level of education, area of training, income and region in which they live. In addition to two more questions about investment behavior: whether the respondent already invests and, if so, the level of investor they believe they fit into. This makes it possible to carry out analyses with control variables.

In order to resolve doubts and correct flaws in the items due to the translation into the cryptocurrency context, the questionnaire was first made available to 11 respondents as a pre-test. Once the necessary changes had been made, the questionnaire was applied and made available in electronic form (internet), accessible via a link that was circulated on social networks such as Facebook, WhatsApp, emails, cryptocurrency events, etc. The questionnaire can be found in Appendix B.

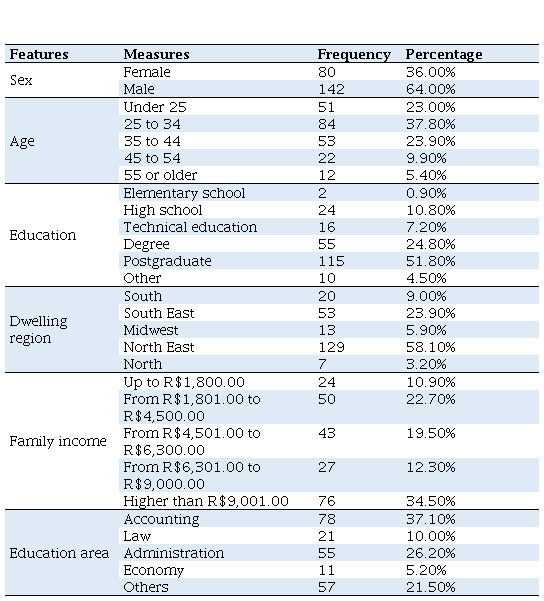

The survey was carried out and the data was collected from February 2021 to May 2021, totaling 380 responses, excluding those in which the respondent declared not knowing what cryptocurrencies are or not intending to invest in them, leaving 222 valid responses for analysis. The sample had the following demographic and socioeconomic characteristics, which can be seen in Table 1.

Sample Characterization

Source: Research dataNote: Sample of 222 respondents.

For data analysis purposes, structural equation modeling was used with data estimation by the PLS method (Partial Least Squares), as it is a complex model with many constructs (Hair, Risher, Sarstedt, & Ringle, 2019). The measurement model was analyzed using confirmatory factor analysis (CFA) to check factor loadings and convergent and discriminant validities. To check internal consistency, composite reliability (CR) and Cronbach's alpha tests were carried out. Convergent validity was measured by analyzing the average variance extracted (AVE). To check for discriminant validity, the Fornell and Larcker (1981) criterion was used to validate the constructs. Hypotheses were then tested to check the quality of the model's fit (R²) and its predictive validity (Q²) and, finally, collinearity was checked using the variance inflation factor (VIF).

4 ANALYSIS AND DISCUSSION OF RESULTS

4.1 Validation of the Measurement Model

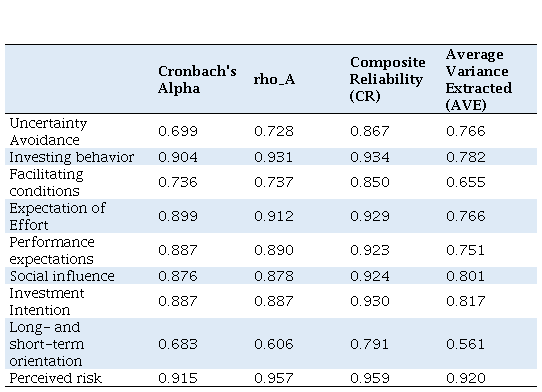

Once the data had been collected, they were analyzed, starting with the validation of the measurement model, which is the first step in evaluating the results in PLS-SEM (Hair et al., 2019). All the constructs in this model are reflective. In order to check internal consistency and convergent and discriminant validity, a confirmatory factor analysis (CFA) was carried out to verify the factor loadings of the construct indicator items, with values greater than 0.708 being accepted as valid (Hair et al., 2019). The indicator for the long- and short-term orientation construct, LT2, had a factor load of 0.49 and was removed from the model. The same goes for the indicators of facilitating conditions, FC4 factor load 0.68, perceived risk, PR2 factor load 0.56 and uncertainty avoidance, UC3 factor load 0.54, improving the consistency of the model. The other constructs did not present any problems for further analysis.

Hair et al. (2019) also suggests checking other indicators of internal consistency reliability, in this case testing Cronbach's alpha (values between 0.70 and 0.95 allowed) and composite reliability (CR) (values greater than 0.7 are allowed). In this study, the CR was between 0.79 and 0.95 and Cronbach's alpha between 0.68 and 0.91, suggesting good reliability of the instrument's indicators (Churchill, 1979; DW Straub, 1989), as shown in Table 2.

Convergent validity was tested by checking the proportion of the variance of the items that is explained by the construct to which they belong, which was done by checking the average variance extracted (AVE), and all constructs are accepted when the AVE is equal to or greater than 0.5, indicating that the construct explains at least 50% of the variance of its items (Fornell & Larcker, 1981; Henseler et al., 2009; Hair et al., 2019), the model's AVE results were all satisfactory and above 0.56, indicating that convergent validity was invariably satisfied, see Table 2.

Reliability and Convergent Validity

Source: Research data

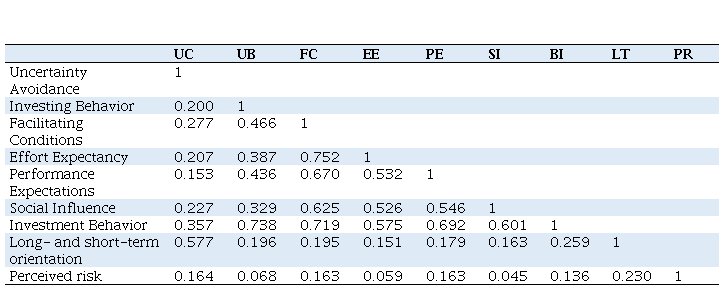

Discriminant validity was also checked to verify the relationship between the indicators and their constructs, indicating the degree of differentiation between one construct and the others (Hair et al., 2014). Henseler et al. (2015) proposed the heterotrait-monotrait ratio (HTMT) of correlations, proposing a limit of up to 0.90 for similar constructs. Table 3 shows the results of the discriminant validity. In addition to this analysis, Table 4 shows the cross-load analysis. Thus, based on all the results, the model showed satisfactory convergent and discriminant validity.

Heterotrait-Monotrait Discriminant Validity (HTMT)

Source: Research dataNote: Average value of the correlations of the items between the constructs, in relation to the (geometric) mean of the average correlations for the items measuring the same construct. As the values are less than 0.90, there is discriminant validity under the HTMT ratio (Hair et al., 2019).

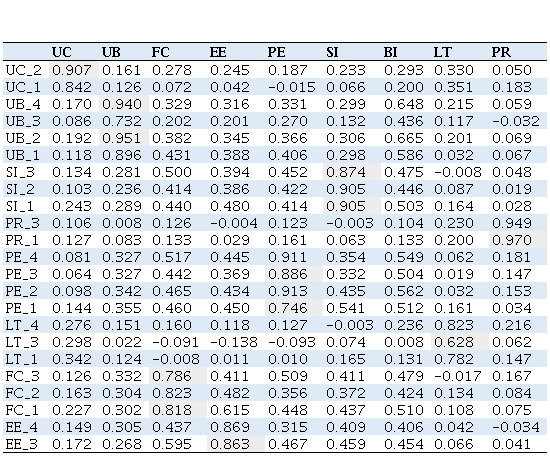

Cross Load Analysis

Source: Research dataNote: The loads of the construct indicators have a greater attraction value with their constructs, compared to the loads of the other indicators

4.2 Validation of the Structural Model

The validation of the structural model was verified through the coefficients of determination, R², which explains the endogenous constructs and predictive relevance, Q², which indicates, in percentage, how much the model can explain the observed values (Hair et al., 2014). The coefficient of determination, R², above 0.19 to 0.33, is considered weak; 0.33 to 0.67, moderate; and above 0.67 substantial (Chin, 1998). In the model tested, the intention to invest in cryptocurrencies had an R² of 0.52 and the investment behavior construct had an R² of 0.45, both considered moderate.

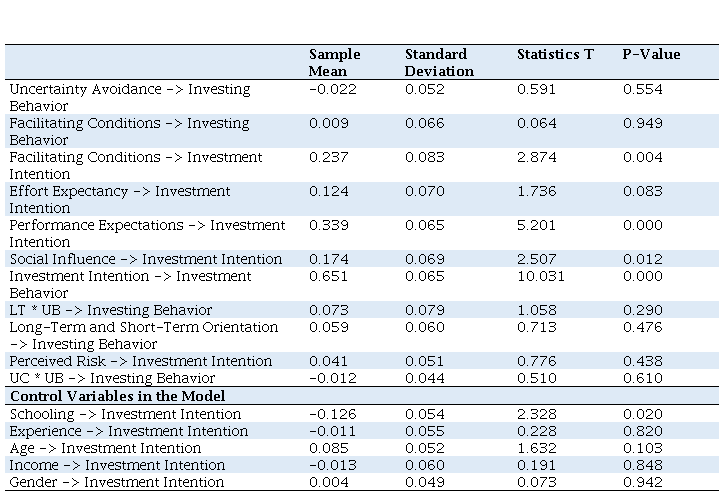

The analysis of hypotheses and construct relationships was based on the examination of standardized paths. Path coefficient levels were estimated using the bootstrapping method (Henseler et al., 2009), with 5000 resampling interactions (Chin, 1998). The p-value results are summarized in Tables 5 and 6. The factors that positively influence investment intention and indirectly investment behavior are effort expectancy, performance expectancy and social influence. It has no effect on the intention to invest in cryptoassets and indirectly on the final behavior, the perceived risk and the expectation of effort. The facilitating conditions construct has no direct effect on behavior. Cultural constructs had neither a direct nor a mediating effect on behavior.

Significance Results of Path Coefficients

Source: Research dataNote: LT * UB and UC * UB are the effects of cultural mediators on investing behavior.

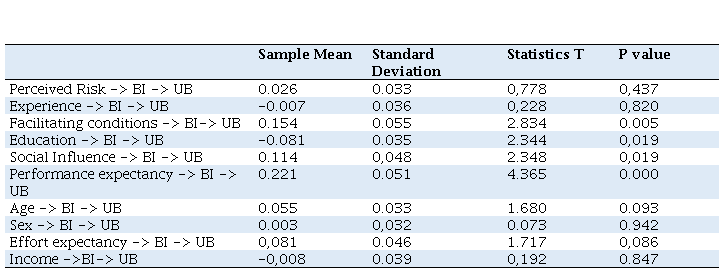

Indirect Effects on Investing Behavior

Source: Research data.Note: Data run with control variables, for significance of the indirect effect on the behavior of investing in cryptocurrencies.

The model has predictive relevance (Q²), the results are considerably accepted, with Q² above zero (Hair et al., 2017) and the values found indicated a good predictive value of 0.41 for behavioral intention and 0.34 for investment behavior. Therefore, hypotheses H1, H3, H4a and H6 are significant and accepted. The result is shown in Figure 2.

Figure 2

Final Model

Source: Developed by the author.

Note: Significance table (*p<0.05; **p<0.01; ***p<0.001)

4.3 Results Discussion

The aim of this study was to analyze the factors that influence the intention and behavior of investing in cryptocurrencies, as well as to understand the impacts of cultural moderation on said behavior. The data analysis revealed significant relationships between the proposed hypotheses, H1, H3, H4a, and H6, finding evidence that the variables of performance expectancy, social influence, and facilitating conditions can indeed influence the intention to invest in cryptocurrencies and indirectly the investing behavior. It was also observed that the cultural variables in this sample do not moderate the relationship between intention and behavior.

The first hypothesis investigated in this study (H1) sought evidence that performance expectancy influences the intention to invest (Venkatesh et al., 2003), with the expected and confirmed significant and positive relationship between them. The hypothesis was tested and supported (p-value < 0.001), replicating findings from authors such as Oliva et al. (2019). The results highlight, as suggested in the literature, that in Brazil, cryptocurrencies are seen as having the potential to diversify investments and maximize gains (Conlon et al., 2020).

Hypothesis H2 sought to verify whether there is evidence that effort expectancy positively influences the intention to invest, with the hypothesis not supported in line with Abramova and Bohme (2016), who indicate that password access and purchase difficulty are relatively insignificant factors in investment intention. This contrasts with the findings of Folkinshteyn and Lennon (2016) and Shahzad et al. (2018). Thus, cryptocurrencies in this sample from Brazil are not intentionally attractive due to ease of access and simple interfaces. Interestingly, the survey respondents, despite their familiarity with the technologies used for investing (72.5% of respondents already invest in the financial market), do not perceive this as a factor affecting investment intention.

Hypothesis H3 sought evidence that social influence positively impacts the intention to invest. Tested, the hypothesis was supported (p-value < 0.05). Unlike countries like Spain, where people are not influenced to invest in cryptocurrencies (Oliva et al., 2019), in Brazil, the result was significant, possibly proving the influence that media and internet channels have on investment intention (Park & Park, 2020). This analysis is also found in research on stocks and risky assets, where the popularity of stocks can diverge from their fundamental value and increase attractiveness (Yoshinaga & Rocco, 2020).

Hypothesis H4a confirms that facilitating conditions positively impact the intention to invest (p-value < 0.01) and indirectly, behavior (p-value < 0.005). The sample in this study possesses skills and access that make investment intention attractive, yet it does not significantly affect direct investment behavior (H4b). It is noted that over 80% of respondents have a college or post-graduate degree and have a salary income that allows them access to internet channels and investments.

In Hypothesis H5, confirming research by Abramova and Böhme (2016) and Oliva et al. (2019), it is noted that perceived risk does not negatively influence the intention to invest in cryptocurrencies. Respondents do not perceive risk as a predictive factor for investment intention, potentially due to the sample's characteristics, as depicted in Figure 3, showing that 72.5% of respondents already invest in the financial market, with 46% considering themselves intermediate investors. Therefore, they have a risk-appropriate profile. Those predisposed to investing in cryptocurrencies already have a low sensitivity to risk as a determining factor for their intentions, which may explain the lack of significance of risk in this study.

Figure 3a.

Characterization of the sample regarding experience in risky investments.

Source: Developed by the author.

Figure 3b.

Characterization of the sample regarding experience in risky investments.

Source: Developed by the author.

Hypothesis H6 was supported (p-value < 0.001), confirming that factors directly influencing investment intention compose only an indirect influence on investment behavior.

Finally, the analysis moved to the moderators in the proposed model, aiming to verify if culture moderates behavioral actions. None of the hypotheses were supported (H7, p-value < 0.77 and H8, p-value < 0.57). The results of the cultural dimension constructs in this surveyed sample suggest that, despite conservative cultures focused on future planning tending to be cautious with investments, this is not a significant moderating factor for whether or not to invest in cryptocurrencies.

However, it is important to consider that the non-significant moderating effect of culture stems from a sample where 72.5% of individuals already invest, with 46% of these considering themselves intermediate-level investors in risky investments. Therefore, this result reflects characteristics inherent to the risk-prone group. There might be a sample selection bias, as indicated by the sample characteristics in Table 1: predominantly male, from the Northeast region, predominantly college or post-graduate educated, investors with reasonably comfortable income for risky investments.

In addition to these findings, when separating the sample by educational level (control variable), the moderating effect of the cultural variable of long-term orientation appears significant. Respondents with post-graduate or undergraduate degrees (p-value < 0.033) culturally lean more towards buying cryptocurrencies with a strategic future outlook. Conversely, respondents with only primary, technical, or secondary education (p-value < -0.072) show the opposite effect, not inclined towards purchasing risky assets. This suggests that culturally, the respondent sample understands at their knowledge level that investing in cryptocurrencies is economically profitable and strategic.

Therefore, the gaps identified in the literature regarding changes in behavior in high-risk asset investment intentions may also be determined by variables that have not yet been identified.

5 FINAL CONSIDERATIONS

This study provides theoretical contributions and implications by applying the UTAUT model in Brazil to analyze the factors influencing the intention and behavior of investing in cryptocurrencies. It aims to understand the impacts of cultural moderation in this country on cryptocurrency investment behavior.

In terms of practical contributions, the results largely align with research from other countries, showing that performance expectancy, social influence, and facilitating conditions can influence the intention to invest in cryptocurrencies and, indirectly, the actual investment behavior. The findings provide evidence as to why cryptocurrencies have gained significant traction and growth. The belief in their growth performance and profitability, the influence of social cycles among users, and the conditions of risk-prone investors make cryptocurrencies an attractive investment alternative. It's also noteworthy that in this predominantly investor sample, cryptocurrency users do not heavily consider risk in their decision-making; their positive familiarity with risk either predisposes them to accept the inherently risky nature of cryptocurrencies or gives them a sense of security in them.

Despite these contributions, the study has limitations. One limitation is related to sample selection bias due to the use of non-probabilistic sampling, which restricts the generalizability of results. Another limitation is the cross-sectional nature of the study, capturing respondents' perceptions during a period of global pandemic. These perceptions may change over time, potentially altering the study's outcomes.

Regarding control variables, they were solely used to isolate the causal relationship between constructs, as per Hair et al. (2019), without implying significant relationships. However, separating the sample by educational level shows that cultural moderation appears to influence individuals' propensity to invest in cryptocurrencies among those with higher education, whereas the opposite effect is observed among those with lower education levels, both influenced by a culture of long-term orientation (LT), which is prevalent in Brazil.

Due to the small sample size when separated, inference cannot definitively state that in cultures with a high LT, educational level determines investment behavior in high-risk assets. Moreover, high educational attainment does not necessarily correlate with high financial literacy regarding decision-making interpretation. Thus, these findings warrant further exploration in future research to understand the role of socioeconomic characteristics in individuals' intentions and behaviors regarding cryptocurrency investment.

However, without separating by education, the results of cultural moderation do not appear significant. Therefore, differences in results from other countries may arise from economic and regulatory aspects, among other unexplored factors. Additionally, cultural psychologists argue that theories tested on members of a culture, within small samples thereof, are susceptible to ethnocentric biases in respondents' reasoning processes, potentially yielding results that cannot be generalized to the population (Malhotra & McCort, 2001). This highlights the need for a deeper understanding of why culture in this research does not moderate investment intentions, considering the specificities of the sampled population.

Another limitation is the exclusion of all variables existing in the literature within behavioral models, leaving room for future research using the Unified Theory of Acceptance and Use of Technology 2 (UTAUT2), incorporating variables such as price value, habit, and hedonic motivation, which are crucial for investigating investment intentions.

This article does not definitively reveal investment behavior intentions, given that the collected sample exists within a pandemic context. Rather, it provides a snapshot diagnosis that can inform strategies for entities promoting cryptocurrencies and/or for governments developing digital currencies.

In summary, research into cryptocurrency investment behavior remains open to further investigation, which can produce valuable contributions to both literature and the advancement and adoption of cryptocurrencies globally.

REFERENCES

Abramova, S., & Böhme, R. (2016). Perceived benefit and risk as multidimensional determinants of bitcoin use: a quantitative exploratory study. International Conference on Information Systems, Dublin, Republic of Ireland, 37. https://informationsecurity.uibk.ac.at/pdfs/Abramova2016_Bitcoin_ICIS.pdf

Agustina, D. (2019). Extension of Technology Acceptance Model (ETAM): Adoption of Cryptocurrency Online Trading Technology. Jurnal Ekonomi, 24(2), 272-287. https://doi.org/10.24912/je.v24i2.591

Alkashri, Z., Alqaryouti, O., Siyam, N., & Shaalan, K. (2020). Mining Dubai government tweets to analyze citizens’ engagement. Recent advances in intelligent systems and smart applications (pp. 615-638). Cham: Springer International Publishing. https://link.springer.com/chapter/10.1007/978-3-030-47411-9_33

Baptista, G., & Oliveira, T. (2015). Understanding mobile banking: The unified theory of acceptance and use of technology combined with cultural moderators. Computers in Human Behavior, 50, 418-430. https://doi.org/10.1016/j.chb.2015.04.024

Bauer, R. A. (1960). Consumer behavior as risk taking. Proceedings of the 43rd National Conference of the American Marketing Association, Chicago, Illinois, 43. https://cir.nii.ac.jp/crid/1572543025452826496

Borri, N. (2019). Conditional tail-risk in cryptocurrency markets. Journal of Empirical Finance, 50, 1-19. https://doi.org/10.1016/j.jempfin.2018.11.002

Bunjaku, F., Gjorgieva-Trajkovska, O., & Miteva-Kacarski, E. (2017). Cryptocurrencies – Advantages and Disadvantages. Journal of Economics, 2(1), 31-39. https://js.ugd.edu.mk/index.php/JE/article/view/1933

Chin, W. W. (1998). The partial least squares approach for structural equation modeling. In G. A. Marcoulides (Ed.), Modern methods for business research (pp. 295–336). Lawrence Erlbaum Associates Publishers.

CoinMarketCap. (2024). CoinMarketCap. https://coinmarketcap.com/

Conlon, T., Corbet, S., & McGee, R. J. (2020). Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Research in International Business and Finance, 54, 101248. https://doras.dcu.ie/25978/1/R19.pdf

Corbet, S., Meegan, A., Larkin, C., Lucey, B., & Yarovaya, L. (2018). Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters, 165, 28-34. https://doi.org/10.1016/j.econlet.2018.01.004

Davis, F. D. (1986). A technology acceptance model for empirically testing new end-user information systems. Cambridge, MA, 17.

Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 319-340. https://doi.org/10.2307/249008

Donatelli, O., Neto & Colombo, J. A. (2021). The Impact of Cryptocurrencies on the Performance of Multi-Asset Portfolios: Analysis from the Perspective of a Brazilian Investor. FGV EESP - Working Paper Series.https://hdl.handle.net/10438/30900

Fishbein, M., & Ajzen, I. (1975), Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research. Read-ing, MA: Addison-Wesley.

Fishbein, M., & Ajzen, I. (1980). Understanding attitudes and predicting social behavior. Prentice-Hall.

Folkinshteyn, D., & Lennon, M. (2016). Braving Bitcoin: A technology acceptance model (TAM) analysis. Journal of Information Technology Case and Application Research, 18(4), 220-249. https://doi.org/10.1080/15228053.2016.1275242

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39-50. https://doi.org/10.1177/002224378101800104

Gil-Alana, L. A., Abakah, E. J. A., & Rojo, M. F. R. (2020). Cryptocurrencies and stock market indices. Are they related? Research in International Business and Finance, 51, 101063. https://doi.org/10.1016/j.ribaf.2019.101063

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2-24. https://doi.org/10.1108/EBR-11-2018-0203

Hofstede, G. (1980). Culture's consequences: International differences in work-related values. Beverly Hills/London: Sage.

Hofstede, G. (2001). Culture's consequences: Comparing values, behaviors, institutions and organizations across nations. Sage publications.

Hofstede, G. (2003). Cultural Dimensions. www.geert-hofstede.com

Hofstede, G., Garibaldi de Hilal, A. V., Malvezzi, S., Tanure, B., & Vinken, H. (2010). Comparing regional cultures within a country: Lessons from Brazil. Journal of Cross-Cultural Psychology, 41(3), 336-352. https://journals.sagepub.com/doi/10.1177/0022022109359696

Iqbal, N., Fareed, Z., Guangcai, W., & Shahzad, F. (2020). Asymmetric nexus between COVID-19 outbreak in the world and cryptocurrency market. International Review of Financial Analysis, 73, 101613. https://doi.org/10.1016/j.irfa.2020.101613

Jung, K. J., Park, J. B., Phan, N. Q., Bo, C., & Gim, G. Y. (2018, June). An international comparative study on the intension to using crypto-currency. International Conference on Applied Computing and Information Technology (pp. 104-123). Springer, Cham. https://doi.org/10.1007/978-3-319-98370-7_9

Khan, I. U., Hameed, Z., & Khan, S. U. (2017). Understanding online banking adoption in a developing country: UTAUT2 with cultural moderators. Journal of Global Information Management (JGIM), 25(1), 43-65. https://doi.org/10.4018/JGIM.2017010103

Kwateng, K. O., Atiemo, K. A. O., & Appiah, C. (2019). Acceptance and use of mobile banking: an application of UTAUT2. Journal of Enterprise Information Management, 32(1), 118-151. https://doi.org/10.1108/JEIM-03-2018-0055

Lahmiri, S., & Bekiros, S. (2020). The impact of COVID-19 pandemic upon stability and sequential irregularity of equity and cryptocurrency markets. Chaos, Solitons & Fractals, 138, 109936.

Makarov, I., & Schoar, A. (2020). Trading and arbitrage in cryptocurrency markets. Journal of Financial Economics, 135(2), 293-319. https://doi.org/10.1016/j.jfineco.2019.07.001

Malhotra, N. K., & McCort, J. D. (2001). A cross‐cultural comparison of behavioral intention models‐Theoretical consideration and an empirical investigation. International Marketing Review. 18(3), 18-40 https://doi.org/10.1509/jimk.18.3.18

Möser, M., Böhme, R., & Breuker, D. (2014). Towards risk scoring of Bitcoin transactions. International Conference on Financial Cryptography and Data Security (pp. 16-32). Springer, Berlin, Heidelberg. https://maltemoeser.de/paper/risk-scoring.pdf

Mutambara, E. (2019). Predicting FinTech innovation adoption in South Africa: the case of cryptocurrency. African Journal of Economic and Management Studies, 11(1), 30-50. https://doi.org/10.1108/AJEMS-04-2019-0152

Nseke, P. (2018). How crypto-currency can decrypt the global digital divide: bitcoins a means for African emergence. International Journal of Innovation and Economic Development, 3(6), 61-70. https://doi.org/10.18775/ijied.1849-7551-7020.2015.36.2005

Park, S., & Park, H. W. (2020). Diffusion of cryptocurrencies: web traffic and social network attributes as indicators of cryptocurrency performance. Quality & Quantity, 54(1), 297-314. https://doi.org/10.1007/s11135-019-00840-6

Rognone, L., Hyde, S., & Zhang, S. S. (2020). News sentiment in the cryptocurrency market: An empirical comparison with Forex. International Review of Financial Analysis, 69, 101462. https://doi.org/10.1016/j.irfa.2020.101462

Sahoo, P. K. (2021). COVID-19 pandemic and cryptocurrency markets: an empirical analysis from a linear and nonlinear causal relationship. Studies in Economics and Finance, 38(2), 454-468. https://doi.org/10.1108/SEF-09-2020-0385

Shahzad, F., Xiu, G., Wang, J., & Shahbaz, M. (2018). An empirical investigation on the adoption of cryptocurrencies among the people of mainland China. Technology in Society, 55, 33-40. https://doi.org/10.1016/j.techsoc.2018.05.006

Shen, W. (2021). New development on regulation of cryptocurrency in China. Journal of Investment Compliance, 22(2), 133-136. https://doi.org/10.1108/JOIC-11-2020-0045

Venkatesh, V., & Davis, F. D. (1996). A model of the antecedents of perceived ease of use: Development and test. Decision Sciences, 27(3), 451-481. https://doi.org/10.1111/j.1540-5915.1996.tb00860.x

Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186-204. https://doi.org/10.1287/mnsc.46.2.186.11926

Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User Acceptance of information technology: Toward a unified view. Management Information Systems Quarterly, 27(3), 425-478. https://doi.org/10.2307/30036540

Venkatesh, V., Thong, J. Y., & Xu, X. (2012). Consumer acceptance and use of information technology: extending the unified theory of acceptance and use of technology. MIS Quarterly, 157-178. https://doi.org/10.2307/41410412

Walton, A., & Johnston, K. (2018). Exploring perceptions of bitcoin adoption: The South African virtual community Perspective. Interdisciplinary Journal of Information, Knowledge & Management, 13, 165-182. https://doi.org/10.28945/4080

Williams, M. D., Rana, N. P., & Dwivedi, Y. K. (2015). The unified theory of acceptance and use of technology (UTAUT): a literature review. Journal of Enterprise Information Management, 28(3), 443-488. https://doi.org/10.1108/JEIM-09-2014-0088

Yoshinaga, C., & Rocco, F. (2020). Atenção do Investidor: O Volume de Buscas no Google é Capaz de Prever os Retornos de Ações?. BBR. Brazilian Business Review, 17, 523-539. https://doi.org/10.15728/bbr.2020.17.5.3

Yu, C. S. (2012). Factors affecting individuals to adopt mobile banking: Empirical evidence from the UTAUT model. Journal of Electronic Commerce Research, 13(2), 104. http://www.jecr.org/sites/default/files/13_3_p01_0.pdf

APPENDIX A - TABLE OF CONSTRUCTS

APPENDIX B – SURVEY QUESTIONNAIRE

Hello!

I am a master's degree student in Accounting at FUCAPE Business School – Fortaleza (CE). I am developing academic research on culture and investments in cryptocurrencies and would like to know your opinion.

This is a study specifically aimed at those who intend to invest in cryptocurrencies or already invest. It is completely confidential and there is no need for identification.

We invite you to participate in our research by answering the questionnaire below, which lasts a few minutes.

Your collaboration is very important. Thanks!

Julyanne Lages de Carvalho Castro

Professor Dr. Danilo Mont-Mor (adviser)

Professor Dr. Neyla TArdin ( advisor )

1. Have you ever heard of cryptocurrencies? Yes No

2. Have you ever heard of Bitcoin? Yes No

3. Have you ever considered investing in cryptocurrencies? Yes No

In the questions that follow, we want to know your opinion: whether you agree or disagree with the statements. To this end, responses are presented on a scale of 1 to 7 points, with 1 being "totally disagree" with the statement and 7 being "totally agree" with the statement.

4. Investing in cryptocurrencies is useful in my everyday life. ( TD) 1 2 3 4 5 6 7 (TA)

5. Investing in cryptocurrencies increases my chances of making money. (TD) 1 2 3 4 5 6 7 (TA)

6. Investing in cryptocurrencies helps you make money faster (TD) 1 2 3 4 5 6 7 (TA)

7. Investing in cryptocurrencies increases my profitability. (TD) 1 2 3 4 5 6 7 (TA)

8. Learning to use cryptocurrencies is easy for me (TD) 1 2 3 4 5 6 7 (TA)

9. My interaction with cryptocurrencies is clear and understandable. (TD) 1 2 3 4 5 6 7 (TA)

10. It's easy for me to become skilled at using cryptocurrencies. (TD) 1 2 3 4 5 6 7 (TA)

11. I think cryptocurrencies are easy to use. (TD) 1 2 3 4 5 6 7 (TA)

12. People who influence my behavior think I should use cryptocurrencies (TD) 1 2 3 4 5 6 7 (TA)

13. People who are important to me think I should use cryptocurrencies (TD) 1 2 3 4 5 6 7 (TA)

14. People whose opinion I value find using cryptocurrencies useful (TD) 1 2 3 4 5 6 7 (TA)

15. I have the knowledge before using cryptocurrency (TD) 1 2 3 4 5 6 7 (TA)

16. I have the resources needed to use cryptocurrency (TD) 1 2 3 4 5 6 7 (TA)

17. Cryptocurrency is compatible with other technology I use (TD) 1 2 3 4 5 6 7 (TA)

18. Can I get help from others when I have difficulties using cryptocurrencies (TD) 1 2 3 4 5 6 7 (TA)

19. Using cryptocurrencies is risky (TD) 1 2 3 4 5 6 7 (TA)

20. There is a lot of uncertainty associated with using cryptocurrencies purchased with other currencies (TD) 1 2 3 4 5 6 7 (TA)

21. Investments in cryptocurrencies are risky (TD) 1 2 3 4 5 6 7 (TA)

22. I intend to continue using cryptocurrencies in the future (TD) 1 2 3 4 5 6 7 (TA)

23. I will always try to use cryptocurrencies in my daily life (TD) 1 2 3 4 5 6 7 (TA)

24. I intend to use cryptocurrencies frequently (TD) 1 2 3 4 5 6 7 (TA)

25. Rules and regulations are important because they tell workers what the organization expects of them (TD) 1 2 3 4 5 6 7 (TA)

26. Order and structure are very important in a work environment (TD) 1 2 3 4 5 6 7 (TA)

27. It's better to have a bad situation that you know than to have an uncertain situation that could be better (TD) 1 2 3 4 5 6 7 (TA)

28. Respect for tradition is important to me (TD) 1 2 3 4 5 6 7 (TA)

29. I work hard to be successful in the future (TD) 1 2 3 4 5 6 7 (TA)

30. Traditional values are important to me (TD) 1 2 3 4 5 6 7 (TA)

31. I plan for the long term (TD) 1 2 3 4 5 6 7 (TA)

32. I wear cryptocurrencies (TD) 1 2 3 4 5 6 7 (TA)

33. I buy cryptocurrencies to diversify my investments. (TD) 1 2 3 4 5 6 7 (TA)

34. I use cryptocurrencies on a daily basis. (TD) 1 2 3 4 5 6 7 (TA)

35. I use cryptocurrencies to make investments (TD) 1 2 3 4 5 6 7 (TA)

Caption: TD – totally disagree, TA – totally agree.

36. Your sex Female Male

37. Your age From 18 to . �1 to 5 6 to 3 3 to 36 37 or older 38.

Your family income Up to R$ 1,8 . From R$ 1,81. to 4,5 . From R$ 4,51. to 6,3 . From R$ 6,31. to 9, . Higher than 9,1.

39. Your education Elementary school High school Technical education Degree Postgraduate Other

40. Your area of training Accounting Economy Law Administration Other

41. Region where you live South South East Midwest North East North

42. Do you invest in the financial market? Yes No

43. Do you consider yourself an investor: Beginner Intermediate Experienced

THANKS! If you can, share the link on your social networks with friends and acquaintances, especially those who know about cryptocurrencies. Everyone's participation is very important to us!