Gender equality: A study of female participation in management roles in auditing firms in Brazil

Igualdade de gênero: Um estudo da participação feminina em cargos de gestão em firmas de auditoria no Brasil

Igualdad de género: Un estudio de la participación femenina en cargos gerenciales en firmas de auditoría en Brasil

Thais Helen Andrade Santos thaishelenandradesantos@gmail.com

Luziberto Barrozo Carneiro luzibertojr@gmail.com

Thais Helen Andrade Santos thaishelenandradesantos@gmail.com

Luziberto Barrozo Carneiro luzibertojr@gmail.com

Gender equality: A study of female participation in management roles in auditing firms in Brazil

Contextus – Revista Contemporânea de Economia e Gestão, vol. 22, núm. 1, Esp., e85274, 2024

Universidade Federal do Ceará

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial 4.0 Internacional.

Recepción: 31 Marzo 2023

Aprobación: 09 Agosto 2024

Publicación: 17 Septiembre 2024

Abstract:

Background: The female presence in the business world has been growing, however there are still several obstacles to achieving equal opportunities in management roles. Women have low representation in management roles, especially high-ranking ones. This study was carried out to analyze female representation in management roles in auditing firms in Brazil. Purpose: This study analyzes female representation in leadership positions in Big Four auditing firms in Brazil between the period 2016-2023. Method: In this sense, documentary research was carried out, inspecting the GRI Sustainability Reports of these organizations. Information about the programs developed that contribute to the rise of women in the role of leader was also sought through the companies' websites. Results: The results demonstrated that female representation, especially in the role of partner, is still low when compared to male representation, although it has evolved in the years analyzed, progressing from 16% (2016) to 25% (2023) in the case of the firm EY and 16% (2016) to 26% (2023) at KPMG. The Big Four initiated gender equity and female talent development policies. Conclusions: It is concluded that the Glass Ceiling is still present in these organizations and is being gradually deconstructed.

Keywords: gender equality, glass ceiling, female representation, big four, audit.

Resumo:

Contextualização: A presença feminina no mundo dos negócios vem crescendo, todavia ainda existem vários obstáculos para alcançar a igualdade de oportunidades em cargos gerenciais. As mulheres têm baixa representatividade em cargos de gestão, principalmente os de alto escalão. Este estudo foi feito para analisar a representatividade feminina nos cargos gerenciais em firmas de auditoria no Brasil. Objetivo: Este estudo analisa a representatividade feminina em cargos de liderança nas firmas de auditoria Big Four do Brasil entre o período de 2016-2023. Método: Neste sentido, foi realizada uma pesquisa documental, inspecionando-se os Relatórios de Sustentabilidade GRI destas organizações. Também foram buscadas, através dos sites das empresas, as informações acerca dos programas desenvolvidos que contribuem para a ascensão da mulher na função de líder. Resultados: Os resultados demonstraram que a representatividade feminina, principalmente no cargo de sócia, ainda é baixa quando comparada com a masculina, embora tenha tido evolução nos anos analisados, progredindo de 16% (2016) a 25% (2023) no caso da firma EY e 16% (2016) a 26% (2023) na KPMG. As Big Four iniciaram políticas de equidade de gênero e desenvolvimento de talentos femininos. Conclusões: Conclui-se que o Teto de Vidro ainda se faz presente nestas organizações e está sendo descontruído aos poucos.

Palavras-chave: igualdade de gênero, teto de vidro, representatividade feminina, big four, auditoria.

Resumen:

Contextualización: La presencia femenina en el mundo empresarial ha ido creciendo, sin embargo aún existen varios obstáculos para alcanzar la igualdad de oportunidades en puestos directivos. Las mujeres tienen una baja representación en puestos directivos, especialmente en los de alto rango. Este estudio se realizó para analizar la representación femenina en puestos directivos en empresas de auditoría en Brasil. Objetivo: Este estudio analiza la representación femenina en puestos de liderazgo en las Big Four firmas auditoras de Brasil entre 2016-2023. Método: En este sentido, se realizó una investigación documental, inspeccionando los Informes de Sostenibilidad GRI de estas organizaciones. También se buscó información a través de los sitios web de las empresas sobre los programas desarrollados que contribuyen al ascenso de la mujer en el rol de líder. Resultados: Los resultados demostraron que la representación femenina, especialmente en el rol de pareja, sigue siendo baja si se compara con la representación masculina, aunque ha evolucionado en los años analizados, pasando del 16% (2016) al 25% (2023) en el caso de las mujeres. firma EY y del 16% (2016) al 26% (2023) en KPMG. Los Cuatro Grandes iniciaron políticas de equidad de género y desarrollo del talento femenino. Conclusiones: Se concluye que el Techo de Cristal sigue presente en estas organizaciones y poco a poco se está deconstruyendo.

Palabras clave: igualdad de género, techo de cristal, representación femenina, big four, auditoría.

1 INTRODUCTION

The female presence in the corporate world has been growing, however, there are still several obstacles to achieving effective equality of workplace opportunity. In Brazil, women have low representation in management positions, especially high-ranking ones (Carneiro et al, 2021). This also occurs in economically developed countries, such as the United States of America (Cohen et al, 2020; Glass & Cook, 2016), England (Morgenroth, 2020; Machado, 2012), China (Sung, 2022; Xie & Zhu, 2016) and Qatar (Naguib & Madeeha, 2023). This also can be observed in accounting (Santos, Melo & Batinga, 2021) and auditing firms (Cheng & Wang, 2023; Cruz et al, 2018). Low female representation in management roles, especially high-ranking ones, is referred to in the literature as the glass ceiling.

The Federal Glass Ceiling Commission in the United States (1995) defines it as “artificial barriers to the development of women and minorities”. In other words, it is an invisible, yet insurmountable barrier that makes it difficult for minorities and women to climb the corporate ladder, regardless of their qualifications. This phenomenon is segmented by Carneiro (2021) into several social, cultural, and institutional factors, ranging from gender stereotypes, difficulties balancing personal and professional life, and the absence of opportunities and policies for inclusion in companies. Topic (2020) also identified that women are excluded from business decisions and that office culture based on male social interactions and support as well as male-to-male mentoring hinders female development at work.

In 1983, the eight largest auditing firms in the world had approximately 6.000 partners, of which only 62 were women (Gould, 1983). In 1986, according to a report from the Census Bureau, the main government agency in the United States federal statistical system responsible for producing data on the population and economy, 45% of all accountants were women. Although progress has been made, the Census Bureau shows differences in male and female earnings, with women earning an average of 69% less (Pear, 1987).

This data has accentuated the issue over the decades and consequently, organizations have emerged seeking to encourage gender equality in companies. We highlight the comprehensive Women's Empowerment Principles – WEP initiative, structured by the United Nations (UN) (Rodrigues et al., 2017). The principles are aimed at the corporate environment to help companies adapt existing policies and practices or even create new practices to achieve women's empowerment (UN Women, 2016).

The Big Four lead the audit market, a nomenclature used to refer to the four main companies: Deloitte, Ernst & Young, KPMG, and PwC. These organizations stand out for their decades-old reputation and expansive network, with offices in many countries worldwide, including Brazil (Capital Now, 2020). In recent years, these companies have implemented programs aimed at providing equal opportunities for women and men so that the entry and development opportunities in the corporate environment are the same.

In view of the above, this research problem focuses on female representation in management positions, especially high-ranking ones, in the Big Four auditing firms present in Brazil from 2016 to 2023.

We aimed to analyze female representation in high-level management positions at Big Four auditing firms in Brazil.

In order to achieve the study objective, the following specific objectives were defined: (i) analyzing the impact of the glass ceiling on executive positions in the auditing environment, a profession that has historically been considered masculine (Bolton & Muzio, 2008); (ii) check policies implemented by the Big Four to encourage greater female participation in leadership positions.

Investigating the main audit firms in Brazil regarding this phenomenon is necessary as there are still few specialized studies on women executives in audit firms and the glass ceiling in this sort of company. This was evidenced by researching the Web of Science, Scopus, and Scielo databases. This perception of a research gap is also noted by Cheng & Wang (2023). The authors also identified that although women are occupying jobs as auditors, proportionality with men continues to be insufficient regarding higher positions, especially that of partners. As such, it is necessary to investigate female representation in senior positions in auditing firms, which is the central focus of this paper.

In addition to the academic contribution of promoting national studies relating to the issue of gender inequality in external audit companies, we seek to contribute to the discussion about this concern so that it encourages entities and society to discuss, propose, and implement changes in favor of gender equality at work in leadership positions. It also collaborates as a source of research for auditing companies, promoting consideration of gender policies in their institutions, as well as the importance of women as an integral part of their technical/professional staff (Cruz et al, 2018).

In 2016, a similar study was carried out by Crestani and Rodrigues, which analyzed how the auditing companies KPMG and PwC were promoting gender equity and female empowerment based on their Sustainability Reports in the years 2014 and 2015. This paper aims to contribute to the cited study, as well as to the area of research related to women managers in auditing firms, updating the data and analyzing a larger sample from 2016 to 2023.

The paper is structured as follows: following the introductory aspects of this section, the theoretical framework, methodological procedures, data analysis, discussion, and conclusion.

2 THEORETICAL FRAMEWORK

2.1 Phenomena: Glass ceiling, sticky floor, and glass cliff

Women face a set of barriers when entering the job market when seeking career advancement, and when assuming high-level management positions. In this scenario, more specifically regarding the promotion to high-level management positions, the concept of the glass ceiling comes into play. According to Steil (1997), the glass ceiling is a transparent and subtle barrier, but strong enough to prevent women from ascending to senior levels in companies. A series of factors shape this barrier. According to the author, this definition of the glass ceiling phenomenon was first introduced in the United States in the 1980s based on its observation.

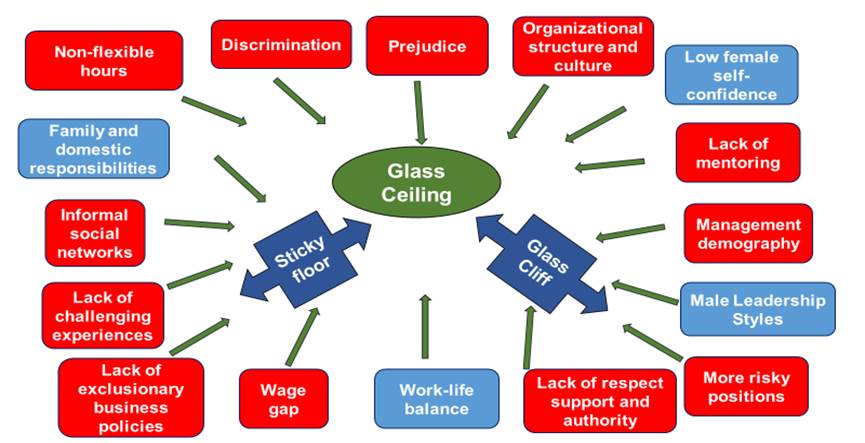

Investigating and understanding the glass ceiling phenomena concluded that it is the end product of a number of factors, precedents, and consequences of female promotion to high-level hierarchical positions in organizations (Carneiro, 2018). Figure 1 presents all the factors found from the study of this phenomenon carried out by Carneiro:

Figure 1

Factors and study focuses that affect the glass ceiling

Source: Adapted from Carneiro (2018, p. 28).

According to Carneiro (2018, p. 28), “the factors listed in blue are those which the woman and her family can interfere and control to a greater extent, while those in red intersect company and societal culture as its main agents.” The sticky floor occurs in a business environment in which women have the same capacity as men but are commonly appointed to lower positions, while men get promoted to higher roles (Ahmad & Naseer, 2015).

The glass ciff is the phenomenon in which the “aptitude” perceived by women for senior positions tends to increase under conditions of organizational crisis (Vetter, 2021). That is, women are more likely to be in positions associated with deterioration, while men are more likely to be chosen for leadership roles, thus being associated with increased rather than decreasing performance (Haslam & Ryan, 2008; Bruckmüller et al, 2014).

These phenomena attempt to explain the low participation of women in prominent roles (Pena, 2015). Research focuses on these barriers from the moment women enter an organization to salary equality and career advancement (Carneiro, 2018). As such, gender equality means much more than just the dispute for space in the job market. It is also about professional development, growth opportunities, remuneration, and respect for women (Robert Half Brazil, 2016).

2.2 The barriers to women’s evolution in the corporate workplace

Distributing positions by gender or sex is a result of the division of labor in the pre-industrial era. Advances in women's work performance were achieved in some areas during the industrial era. The increase in human rights resulted in an increase in the workforce available in the capitalist market. This made it possible for women's work to have lower remuneration than men's (Meinhard & Faria, 2020).

Thus, other problems arose as women entered the job market, such as those related to remuneration. Brighenti, Jacomossi, and Silva (2015) investigated evidence of gender inequality among accountants and auditors in the labor market in the state of Santa Catarina, Brazil. The results show that women’s average salary is lower than that of men, although the average level of education is the same. This highlights the situation remains an issue even in recent years.

Meinhard and Faria (2020) analyzed the representation of women in companies that adopt the practices recommended by the Women’s Empowerment Principles - WEP. The authors concluded that changes in gender relations are still reliant on changes in the male position in the company.

Santos, Tanure, and Carvalho (2014) carried out a study on the glass ceiling phenomena in Brazilian organizations and found that only 23% of Brazilian strategic-level executives are women. The authors found that the explanation for the limited ratio is due to the significant entry of women into the job market that took place a few decades ago.

The labyrinth theory, proposed by Eagly et al (2007), suggests that the issue regarding women's representation in the labor market is not exclusively regarding women's empowerment: “The scarcity of women in leadership positions is the sum of several aspects of discrimination that operate at all levels. There is no evidencae of a specific obstacle to the poor advancement of women when they approach the top” (Eagly et al, 2007, p. 65).

There are three main mechanisms through which gender inequality is reproduced in the corporate world. The first is salary discrimination (i), given that women tend to receive lower pay than men, even occupying identical roles (Giuberti & Menezes-Filho, 2005; Roth, 2007). The second is occupational segregation (ii), due to women occupying less qualified positions with lower pay than men in general (Souza & Guimarães, 2000; Lavinas, 2001; Cambota & Pontes, 2007). Finally, the glass ceiling (iii), refers to the difficulty in professional advancement for women akin to a barrier that blocks the promotion of women and minorities to senior levels in organizations (Morrison & Glinow, 1990; Steil, 1997).

2.3 Previous studies

Carneiro et al. (2021) published a survey seeking to verify the perception of women managers about breaking the glass ceiling. The study obtained 62 valid responses from women, who currently or previously held management positions. The results showed that the main strategies and actions these women employ to break the glass ceiling are: professional qualification, female empowerment, family education, self-confidence, and legitimacy through competence and results.

Cohen et al (2020) carried out an analysis of the glass ceiling in the United States among the accounting profession. The results show that the glass ceiling interferes with the promotion of women to higher positions, which occurs due to structural and cultural norms. From an organizational point of view, opportunities for mentoring, networking, and high-profile job assignments exclude women. From a cultural perspective, there was a lack of social support from male leaders within the organization. According to the study, accountants from industrial companies identified the glass ceiling phenomena in their companies in a greater proportion than accountants from public companies.

Cruz et al. (2018) researched gender inequality in external audit companies and concluded that the main barrier to women's advancement in the audit career is the difficulty in reconciling professional and personal life, mainly due to the number of working hours during periods of high demand.

Although some studies show that women have gained more positions in the job market, there is still significant segregation when comparing different work areas (Jaime, 2011; Smith, 2014; Souza & Guedes, 2016).

Lupu and Empson (2015) sought to understand why experienced professionals who have achieved rather high status within their companies comply with organizational pressures toward work overload. In this scenario, it is common for women to undergo “body planning”, that is, to control their fertility and motherhood to minimize the impact on their professional career, as a way of compensating for not having the characteristics of an “ideal worker”, considered to be those of a “standard professional”. (Lupu & Empson, 2015; Rudman & Glick, 1999).

Pena (2015) sought to answer the following question: although gender diversity has been widely discussed within companies, especially in the composition of senior management, why is female representation so low in the corporate structure of the Big Four auditing firms? “Analyzing the responses, we observed that the interviewed professionals assumed the male environment identified in the audit as common and did not highlight the twofold effort they often had to make to fulfill their tasks” (Pena, 2015, p. 90). The author concluded that there clearly are barriers related to gender in the development of professionals' careers, be it related to the challenges of work or social life that influenced their choices for career development.

Lupu (2012) aimed to explore the mechanisms that promote the rareness of women in management positions in French accounting firms. Their research expanded the body of knowledge regarding gender practices in the Big Four and focused on understanding how the discursive and practical factors of daily routines contribute to the reproduction of gender culture in these firms. In the external audit market, previous studies found that the work environment is not conducive to the professional development of women, and the number of those who manage to reach the top of their careers is rather small (Lupu, 2012; Lupu & Empson, 2015).

3 METHODOLOGY

This research is classified as descriptive concerning its purposes, documentary regarding its procedures, and qualitative in terms of approach to the problem, as it does not employ a statistical instrument. This is justified by being an adequate way to understand the nature of a social phenomenon (Richardson, 1999).

This is a multi-case study. The companies included in the survey are Brazilian audit firms from the Big Four group, due to their strong influence and credibility in the global market. To this end, data collection was carried out through documentary research, consolidated from the analysis of sustainability reports from the following independent audit firms: Ernst & Young, Deloitte, PWC, and KPMG.

Sustainability reports were used as the main source of the study as they provide reports of the positive or negative impacts of companies on society, the environment, and the economy. As such, it is where the risks, opportunities, and environmental and social performance of an organization are demonstrated. It is also possible to locate information about the distribution of employees by category, the proportion of salaries between women and men within the same role, and career plan development.

To prepare the sustainability report, the firm must follow the guidelines defined by the Global Reporting Initiative, an international, non-profit organization and pioneer in developing a comprehensive Sustainable Reporting structure (Polen, 2021). The guidelines constitute an international reference for all parties interested in disseminating information regarding how organizations are managed, their social, environmental, and economic performance, and the impacts in those areas, in addition to offering useful subsidies for preparing documents that require this disclosure (Global Reporting Initiative, 2013).

The information found in the sustainability reports of the studied companies makes it possible to analyze female representation in management positions through the GRI 405-1 indicator – Composition of groups responsible for governing and separating employees by functional category, gender, age range, minority status, and other diversity indicators (Global Reporting Initiative, 2013).

Additionally, we also analyzed the companies’ compliance with the sixth Women's Empowerment Principle established by the UN regarding the corporate field: promote equality through community initiatives and advocacy; and whether they are seeking to achieve the fifth Sustainable Development Goal – SDG, gender equality.

As such, the principle and goal serve as a parameter to identify whether the Big Four are promoting programs that encourage greater female participation and whether these are achieving their purpose, that is, mitigating gender inequality in high-ranking management positions.

We analyzed the sustainability reports ranging from 2016 to 2023. The goal was to identify the variation in female representation during these five years in executive positions and make a comparative analysis of the results of each Big Four company individually. We researched the company's websites and sustainability reports to verify which policies the firms are implementing to minimize the glass ceiling phenomenon in the workplace.

Regarding data analysis, we conducted a descriptive analysis to compare data on female representation in management positions and arenas of power in companies. We conducted a descriptive check to learn and understand the implemented programs and what actions are being carried out by the companies to promote and encourage the breaking of the glass ceiling.

4 ANALYSIS AND DISCUSSION

This section presents the results obtained from the analyses carried out in this study. The first refers to how each Big Four company evolved, individually, during the period from 2016 to 2023 regarding female presence in executive positions. Next, incentive programs for each firm are presented to promote the number of women in the corporate environment, including in the roles of partner, director, and manager. This way it is possible to uncover whether the measures that companies are implementing are contributing to breaking the glass ceiling phenomenon.

Each position has its hierarchy level and specificities. Partner is a position at the top of the hierarchy, as the professional who assumes this role is responsible for legally responding to the company, runs the day-to-day business, and is on the front line of the company. The director is the professional appointed by shareholders to monitor and regulate the company's activities, being responsible for providing leadership, establishing plans, and policies, and is in charge of either the success or failure of the organization. Finally, the manager leads, supervises, and instructs subordinates. While a manager professional fits middle-level management, a director belongs to top-level management.

It is worth noting that from 2013 until June 30, 2018, the GRI guidelines were presented in the G4 version. As of July 1, 2018, the GRI Standard version came into force. The new format is a transition to a set of global standards and presents a flexible modular structure that more rigorously establishes the criteria that the reporting company must follow when using the methodology.

Due to the delimitation of the report study period from 2016 to 2023, changes were identified in the guideline codes from the 2018 sustainability report. As such, the guideline indicator of the G4 version was correlated with that of the GRI Standard version, which will be used as a criterion for identifying published data regarding the number of women in the companies, as shown in Table 1:

| Indicator - G4 | Indicator - GRI Standard | Description |

| G4-LA12 | GRI 405-1 | Diversity of governance |

We also emphasize that the information in the companies’ sustainability reports is not presented identically despite following the GRI guidelines. In other words, each company adopts a different layout for advertising the information.

4.1 Analysis of female representation in management positions in auditing firms

To carry out this study, an electronic search was carried out through the Sustainability Reports of the selected firms using the following keywords: Sustainability report; GRI; Global Reporting Initiative; Annual report; and Impact Report. Thereafter, a documentary analysis was carried out on the Sustainability Reports of independent audit companies: EY, KPMG, PWC, and Deloitte. To prepare the analyses, a sample of 20 Sustainability Reports published between 2016 and 2023 was examined. Finally, we designed figures to present the data extracted from the analyzed documents.

4.1.1 EY

EY is a global organization and may refer to one or more affiliates of Ernst & Young Global Limited, each an independent legal entity. It operates in the areas of assurance, consulting, strategy, tax, and transactions. It has diverse teams in more than 150 countries worldwide. It has 15 offices in Brazil and employs 8.734 professionals (EY, 2024).

Based on data published in EY Sustainability Reports regarding the diversity of governance bodies and employees, which meets the GRI 405-1 indicator, we verified the number of partners, directors, and managers in Brazil divided by gender, as well as the data percentage. The information provided in the reports was compiled and structured to allow better visualization of the development rate of women employed as partners, directors, or managers throughout the study period, according to Figure 2.

Figure 2

Female representation in the roles of managers directors and partners at EY

Source: Research data.

Through Figure 2 it is possible to identify a positive variation in the roles of manager and partner. In other words, female representation grew in these roles, even if slightly. It is worth highlighting the increase in the number of partners. As of 2016, there were 16% of women working in this role; out of a total of 200 partners, 32 were women. In 2023, the percentage grew to 25%; out of 323 total partners, 82 were women. Regarding the position of manager, we observed a 9% increase.

However, it is also possible to infer a 4% decrease in the number of female directors in 2020 when compared to the period in 2016, rising again in 2021. In 2023, the percentage of female directors remained the same as in 2016, showcasing stagnation in this high-ranking role even though eight years have passed. Based on the results observed regarding the rates of female representation in the roles of partners, directors, and managers at EY, we verified that the firm shows a gradual increase in women occupying executive positions, representing a gradual break of the glass ceiling. However, considering the data presented in the figure above, it can be noted that it will still take a considerable amount of time for the ratio to reach at least 50% of women occupying the directors and partner roles.

4.1.2 KMPG

KPMG Auditores Independentes is a simple society, which is part of KPMG International Limited, a private English company with limited liability. It provides professional services in the areas of audit, tax, and advisory, and employs about 5.000 professionals distributed throughout Brazil in 15 cities (KPMG, 2024).

Based on the information disclosed in the KPMG Sustainability Reports regarding the diversity of governance bodies and employees, which meets the GRI 405-1 indicator of the Standard version, we only analyzed the number of partners, due to the reports from 2016 to 2018 not providing the number of women occupying the roles of directors or managers. The only data available was regarding the number of employees, interns, temporary staff, and partners.

In 2019, the firm only presented the percentages of female representation in the partner, manager, staff, trainee, and intern roles. In 2020, the percentages of women in leadership regarding the roles of partners, directors, and managers were published.

Therefore, only the index regarding the representation of partners at KPMG was used as a parameter for analysis, as this was the shared information found in all its published reports. The information provided in the reports was compiled in Figure 3.

Figure 3

Female representation as partners at KPMG

Source: Research data.

As shown in Figure 3, during the analyzed period from 2016 to 2023, there was an increase of approximately 10% in the role of partners. The result is comparable to that of EY, which had the same average growth considering the same period. The progress is considered positive, although it is still possible to observe the impact of the glass ceiling in the organizational context. In 2023, of the total of 507 partners at KPMG Brazil, 133 were women (KPMG, 2024).

4.1.3 PwC

PwC refers to PricewaterhouseCoopers Brazil Ltda, which is part of PricewaterhouseCoopers. It operates 18 offices in Brazil and employs approximately 5.000 professionals. The company provides audit and assurance services, business transaction advisory, tax and corporate consultancy, and business consultancy (PwC, 2024b).

The company was contacted via telephone and e-mail and asked about the existence of reports published following the GRI standard or any other report containing information about the number of women in management roles, especially high-level positions (partner and/or director) for the last eight years. The company’s response suggested we use the website's publications and market information as reference material. No material related to the number of employees per role was found on other websites.

Searching the organization's website, we only found the sustainability report for the 2016-2017 biennium. It does not provide information regarding the number of employees by role, or by gender. However, PwC published an annual report in 2020 that does not reference the GRI indicators but presents the ratio of female representation in the workforce in Brazil, as illustrated in Figure 4.

Figure 4

Female representation in manager senior manager director and partner roles at PwC

Source: Research data.

As can be observed in the data, it appears that manager roles have the most representative rates of the analyzed sample. For instance, in 2019, the percentage of women in manager roles reached almost 50%. However, it is also clear that there was a decline in most indexes in 2020. Regarding partner roles, there was a positive variation of 1%. However, the representation of women in this role is much lower comparatively. No other report was found after the 2020 report containing information regarding female percentage by position in the company. We observed the pattern that men are still the vast majority holding leadership positions, which may be indicative of the barrier faced by women in the corporate arena.

4.1.4 Deloitte

Deloitte refers to one or more companies within Deloitte Touche Tohmatsu Limited (“DTTL”). It has been in the market for over 178 years, provides auditing, financial advisory, consulting, risk advisory, tax advisory, and related services, and operates 17 offices in Brazil.

The firm publishes sustainability reports in compliance with GRI standards. However, the reports are global and address all offices on the continents, not just one country. Therefore, information about the number of employees in Brazil was unavailable until 2020. Regarding the 405-1 GRI Standard indicator, the company informs that it is difficult to define “minority groups” throughout Deloitte due to the global nature of the organization (Deloitte, 2021).

From 2021 onwards, Deloitte Brazil Impact Reports start being published, which present information on representation by gender in the Brazilian firm, but not specifically by role. In 2021, the company’s ratio was of 51% male and 49% female employees (Deloitte, 2022). Since 2022, the company has added information about the participation of women in the organization's leadership and management group in its Impact Reports, as shown in Figure 5.

Figure 5

Female representation in executive and partner roles at Deloitte

Source: Research data.

Based on the percentages above, we observe an evolution from 2022 to 2023. However, the representation of partners is still much lower compared to the executive role, which would be equivalent to the role of managers and directors. The low representation of partners reflects the glass ceiling’s invisible barrier that prevents women from reaching prominent positions.

4.2 Initiatives related to gender equity

The Brazilian indicators for the Sustainable Development Goals and the Women's Empowerment Principles have been strong allies in the movement to fight for gender equality, as both seek to encourage companies in Brazil to adopt a set of principles and actions to boost gender equity, and sustainable development, among others.

The United Nations has established 17 goals, which address the main challenges faced by people in Brazil and worldwide. These are called the Sustainable Development Goals (SDGs). Among them we highlight the 5th principle, which addresses gender equality, aiming to guarantee the full and effective participation of women, especially equal opportunities for leadership at all levels (United Nations Brazil, 2022).

The Women’s Empowerment Principles (WEPs) recognize and reward entities for their advances in implementing actions related to gender equality. The WEPs were created by UN Women in 2010 and are committed to encouraging companies to achieve an increasingly higher score on each of the seven established principles.

To meet the specific objective of verifying the policies that the Big Four are implementing to encourage greater female participation in leadership roles, we verified whether the auditing firms are achieving the 6th principle of women's empowerment, promoting equality through community initiatives and advocacy and whether they are promoting female empowerment. By accomplishing this principle, the 5th indicator of the SDG is also fulfilled.

The companies' websites were used to verify the implemented policies. Each one was covered in the following subtopics presenting the programs being implemented.

4.2.1 EY

EY believes that gender-diverse leadership is linked to a company's ability to innovate and generate profits. It also believes in the ethical values of a pluralized and inclusive society. It is among the companies recognized in the Large Company category of the WEPs Brazil 2019 Award and has been a signatory to the Global Compact Brazil Network since 2016, connecting its indicators to the SDGs created by the UN. It also participates in the Alliance Group for Female Empowerment created by UN Women in 2011 (EY, 2020).

As such, it created programs to encourage the advancement of women within the company. Some of these are Winning Women, which works as a mentorship for entrepreneurs, supporting them with knowledge and network; Women Fast Forward, a global platform that engages EY people, clients, and communities to advance gender equity; Power Up – Female Power, a workshop aimed at women to provoke reflections, debates, learning, and engagement on the topic of female empowerment; Women of Brazil, an initiative where EY professional women from different segments meet monthly to debate and propose actions related to entrepreneurship, education, quotas for women, and social projects (EY, 2020). Furthermore, there is also the She Belongs initiative, a program that lasts three months and offers individual mentoring sessions to socially vulnerable entrepreneurs to strengthen their strategic management knowledge, helping them to consolidate their businesses (EY, 2024).

We observed EY is complying with the 6th Women's Empowerment Principle as the initiatives created by the company are promoting the breakdown of gender inequality and are also in line with the 5th SDG.

4.2.2 KPMG

KPMG was one of the first companies to adhere to the UN Women's Empowerment Principles. The company believes that promoting different perspectives and respecting the individuality of each person, regardless of personal characteristics or beliefs, helps to promote a collaborative culture, inclusion, and diversity. It is also voluntarily involved and aligned with the 17 UN SDGs (KPMG, 2021a).

The company implemented KNOW (KPMG's Network of Women), which coordinates initiatives related to gender equality. Some initiatives include increasing female participation in leadership, promoting good practices aimed at women's development, and improving the comfort of professional women during and after management, among others. KNOW was created in 2009 and aims to help the career development of the company's professionals, enable networking between executives, and provide a more inclusive environment.

This inclusion policy promotes several programs, including Mentoring for You, in which partners act as mentors for KPMG managers and managing partners for six to nine months. The Mentoring for You program contributed greatly to the company being recently awarded as a leading company in applying the WEPs (KMPG, 2021b).

To its sustainability report, KPMG also holds internal events, videos, and discussion spaces on parenting, masculinity, and other topics favoring the engagement of men in encouraging and accelerating female careers, also known as the “#heforshe” cause (KMPG, 2024).

It appears that KPMG is following the 6th WEP established by the UN and, additionally, is enacting the SDG that addresses gender equality in leadership positions.

4.2.3 PwC

PwC seeks to measure the evolution of diversity in the leadership pipeline to inform strategic decisions. The company recognizes that, although 52% of the firm's workforce is represented by women, this representation regresses when considering board and executive roles.

One of PwC's priorities is to increase female participation in leadership roles. To achieve this, it has carried out some programs. One of them is Women in Leadership (WiL), created in 2016, where outstanding professionals are accompanied for six months by senior partners and can discuss their careers, barriers, and difficulties, develop a network of relationships, and improve their strengths. Since the beginning of the program, 61% of participating professionals have been promoted to partner or associate partner. Because of PwC's performance regarding gender diversity, it won the WEPs Brazil award in the silver category in 2019 (PwC, 2020). Furthermore, there is also the Women in Focus (WiF) program, which aims to expand positive impacts for gender equity by bringing in directors as mentors for women in management roles (PwC, 2024).

The company is contributing to UN Women's sixth SDG of female empowerment and the fifth SDG, gender equality.

4.2.4 Deloitte

It has been a signatory to the WEPs since 2017. In 2020, it was recognized by the GPTW Women Award as one of the best companies for women to work for. It also voluntarily enrolled in the Global Compact and the 17 Sustainable Development Goals (Deloitte, 2024b).

Deloitte aims to increasingly value women so they can conquer their space. For this goal, it has developed strategies to bring more opportunities to its professionals.

One of the initiatives created was the Hers program, which aims to strengthen the culture of equality between men and women, developing their skills through training, promoting an inclusive culture, and connecting a support network. This program is part of the ALL-IN strategy, which is aimed at maximizing female representation and solidifying the culture of diversity and inclusion. The Hers program focuses on fostering a support network, including leadership, mentors, and sponsors; and implementing policies where professionals can reconcile personal and professional lives, such as flexible working hours, and home office, among others.

Deloitte is practicing initiatives that favor gender equality. As a result, it is in line with SDG 5 and is promoting the presence of women in management roles, as required by the 6th WEP.

5 CONCLUSIONS

In this study, we sought to analyze female representation in leadership roles in the Big Four auditing companies in Brazil from 2016 to 2023, to examine whether the glass ceiling phenomenon still has a strong influence on women's careers, and to find out whether these companies are promoting policies to encourage the presence of women in senior positions. For this goal, we analyzed sustainability reports standardized by the Global Reporting Initiative to obtain data regarding the number of companies' employees by role. We also researched information about policies encouraging female empowerment and career advancement on the companies' websites.

We concluded that the representative rates of female partners and directors in the studies firms are still much lower when compared to the rates of men who occupy these same roles. Comprehensively, the evolution of female participation in the corporate organization is happening very timidly. Although the Big Four are implementing internal programs to enable gender equality, especially in leadership roles, the glass ceiling is still present in these organizations.

At EY in 2023, out of 323 partners, 82 are women, equivalent to 25%. At KPMG, in the same period, the rate of female partners was 26%; and at Deloitte, it was 19%. PwC did not provide information on the number of employees by roles in Brazil in 2023. The only information available is regarding 2020, which presented 17% of women occupying the role of partner.

We note that considering that each company adopts a different information presentation for disclosing GRI indicators, the percentages between them are close even though the analyses were carried out individually.

The Big Four promote programs that encourage gender equality. The group's companies were recognized by the Women's Empowerment Principles 2020/2021 award, a UN initiative that aims to encourage and recognize the efforts of organizations that promote women's empowerment and gender equality in Brazil. We observed that the firms have similar programs. For instance, partners offering mentoring to women with their careers on the rise during a pre-determined period. As such, it appears that companies are complying with the 6th Women's Empowerment Principle, which consists of promoting equality through community initiatives and advocacy. They also appear to be seeking the 5th SDG established by the UN, gender equality.

Some limitations of this work relate to the research instrument, as not all companies disclose information on the number of employees by role and gender, such as PwC for instance. Regarding Deloitte specifically, until 2020 there was no concrete information regarding female representation in Brazil. Therefore, it became difficult to survey the scenario of female representation in these companies in the country. Another limiting factor is that the published reports have different information layouts. Up to 2018, KPMG did not disclose the number of directors or managers, for instance. As a result, there is no way to delimit the analysis of the same roles for the four companies. The only information that they all disclose in common is regarding the percentage of partners.

For future research, it is suggested to increase the sample size by drawing a parallel between the indexes found in Brazil and those found in other offices around the world. This would enable researchers to gather a comprehensive view and compare the speed at which there is an evolution in the participation of women in senior roles in auditing firms in different countries. We also suggest a more in-depth analysis of the programs developed by the Big Four, verifying their level of effectiveness and contribution to the breakdown of the glass ceiling phenomenon.

REFERENCES

Ahmad, M., & Naseer, H. (2015). Gender bias at workplace: Through sticky floor and glass ceiling: A comparative study of private and public organizations of Islamabad. International Journal of Management and Business Research, 5(3), 249-260. https://sanad.iau.ir/fa/Journal/ijmbr/DownloadFile/810516

Bolton, S., & Muzio, D. (2008). The paradoxical processes of feminization in the professions: the case of established, aspiring and semi-professions. Work, employment and society, 22(2), 281-299. https://doi.org/10.1177/0950017008089105

Brighenti, J., Jacomossi, F., & Silva, M. Z. (2015). Desigualdades de gênero na atuação de contadores e auditores no mercado de trabalho catarinense. Enfoque: Reflexão Contábil, 34(2), 109-122. https://doi.org/10.4025/enfoque.v34i2.27807

Bruckmüller, S., Ryan, M. K., Rink, F., & Haslam, S. A. (2014). Beyond the glass ceiling: The glass cliff and its lessons for organizational policy. Social Issues and Policy Review, 8(1), 202-232. https://doi.org/10.1111/sipr.12006

Cambota, J. N., & Pontes, P. A. (2007). Desigualdade de rendimentos por Gênero Intra-ocupações no Brasil, em 2004. Revista de Economia Contemporânea, 11, 331-350. https://doi.org/10.1590/S1415-98482007000200006

Capital Now (2020). Big Four: Quem são as maiores empresas de auditoria? https://www.capitalresearch.com.br/blog/investimentos/big-four/

Carneiro, L. B. (2018). Teto de vidro: um estudo sobre os fatores deste fenômeno no brasil sob a percepção das mulheres gestoras (Master's thesis). Universidade Federal do Rio Grande – FURG. Rio Grande, Rio Grande do Sul, Brasil. https://repositorio.furg.br/handle/1/7886

Carneiro, L. B., Gomes, D. G., Horz, V., & Souza, M. A. (2021). Perception of women managers about the glass ceiling breakage. Revista Produção e Desenvolvimento, 7. https://doi.org/10.32358/rpd.2021.v7.530

Cheng, H., & Wang, J. (2023). What’s in store for females after breaking the glass ceiling? Evidence from the Chinese audit market. Frontiers in Psychology, 14, 1321391. https://doi.org/10.3389/fpsyg.2023.1321391

Cohen, J. R., Dalton, D. W., Holder-Webb, L. L., & McMillan, J. J. (2020). An analysis of glass ceiling perceptions in the accounting profession. Journal of Business Ethics, 164, 17-38. https://doi.org/10.1007/s10551-018-4054-4

Crestani, J. D. S., Rodrigues, D. A., & Rodrigues, A. T. (2017). Auditoria Externa: Um Estudo Sobre Equidade De Gênero Em Empresas De Auditoria. Anais do II Congresso de Contabilidade da UFRGS. Porto Alegre, Brasil. 2. https://www.ufrgs.br/congressocont/index.php/congresso/congressocont/paper/download/60/27

Cruz, N. G., Lima, G. H., Oliveira Durso, S., & Cunha, J. V. A. (2018). Desigualdade de gênero em empresas de auditoria externa. RevistaContabilidade, Gestão e Governança, 21(1), 142-159.

Deloitte. (2021). FY2020 Global Reporting Initiative (GRI) Index. https://www2.deloitte.com/content/dam/Deloitte/global/Documents/About-Deloitte/gx-2020-GRI-Index.pdf.

Deloitte. (2022). Construindo futuros melhores. Relatóriode impactos – Brasil. Ano fiscal 2021. https://www2.deloitte.com/content/dam/Deloitte/br/Documents/about-deloitte/RelatorioImpactosDeloitteBrasilFY21.pdf.

Deloitte. (2023). Construindo futuros melhores. Relatóriode impactos – Brasil. Ano fiscal 2022. https://www2.deloitte.com/content/dam/Deloitte/br/Documents/about-deloitte/Relatorio-Impactos-Deloitte-Brasil-FY2022.pdf

Deloitte. (2024a). Construindo futuros melhores. Relatóriode impactos – Brasil. Ano fiscal 2023. https://www2.deloitte.com/content/dam/Deloitte/br/Documents/about-deloitte/Relato%CC%81rio%20de%20Impactos%202024%20(ref.%20FY%2023).pdf

Deloitte. (2024b). Prêmios e Reconhecimentos. https://www2.deloitte.com/br/pt/pages/about-deloitte/articles/premios-reconhecimentos.html?icid=wn_premios-reconhecimentos

Eagly, A. H., Carli, L. L., & Carli, L. L. (2007). Through the labyrinth: The truth about how women become leaders (Vol. 11). Boston, MA: Harvard Business School Press. https://doi.org/10.1108/gm.2009.05324aae.001

Ernst & Young - EY. (2017). Relatório de sustentabilidade 2016. www.ey.com.br/relatoriosustentabilidade

Ernst & Young - EY. (2018). Relatório de sustentabilidade 2017. https://assets.ey.com/content/dam/ey-sites/ey-com/pt_br/topics/corporate-social-responsibility/relat%C3%B3rio-anual-2017-/ey-relatorio-anual-2017-.pdf

Ernst & Young - EY. (2019). Relatório de sustentabilidade 2018. https://assets.ey.com/content/dam/ey-sites/ey-com/pt_br/topics/corporate-social-responsibility/relat%C3%B3rio-anual-2018/ey-relatorio-anual-2018-ey-brasil.pdf

Ernst & Young - EY. (2020). Relatório de sustentabilidade 2019. https://www.ey.com/pt_br/corporate-responsibility/relatorio-anual-2019

Ernst & Young – EY. (2020). Relatório Anual | Empoderamento feminino. https://www.ey.com/pt_br/corporate-responsibility/empoderamentofeminino

Ernst & Young - EY. (2021). Relatório de sustentabilidade 2020. https://www.ey.com/pt_br/corporate-responsibility/relatorio-anual-2020

Ernst & Young - EY. (2022). Relatório de sustentabilidade 2021. https://assets.ey.com/content/dam/ey-sites/ey-com/pt_br/topics/corporate-social-responsibility/relat%C3%B3rio-anual-2021/ey-relatorio-anual-2021.pdf

Ernst & Young - EY. (2023). Relatório de sustentabilidade 2022. https://assets.ey.com/content/dam/ey-sites/ey-com/pt_br/topics/corporate-social-responsibility/relatorio-anual-2022/ey-relatorio-anual-2022.pdf

Ernst & Young - EY. (2024). Relatório de sustentabilidade 2023. https://assets.ey.com/content/dam/ey-sites/ey-com/pt_br/topics/corporate-social-responsibility/relatorio-anual-2023/ey-relatorio-anual-integrado-2023-vf.pdf

Federal Glass Ceiling Commission. (1995). Glass Ceiling Commission - Good for Business: Making Full Use of the Nation´s Human Capital. Washington, D.C. https://ecommons.cornell.edu/bitstream/handle/1813/79348/GlassCeilingFactFindingEnvironmentalScan.pdf?sequence=1&isAllowed=y

Giuberti, A. C., & Menezes-Filho, N. (2005). Discriminação de rendimentos por gênero: uma comparação entre o Brasil e os Estados Unidos. Economia Aplicada, 9, 369-384. https://doi.org/10.1590/S1413-80502005000300002

Glass, C., & Cook, A. (2016). Leading at the top: Understanding women's challenges above the glass ceiling. The Leadership Quarterly, 27(1), 51-63. https://doi.org/10.1016/j.leaqua.2015.09.003

Global Reporting Initiative. (2013). G4 Diretrizes para Relato de Sustentabilidade – Manual de Implementação. Amsterdam. https://sinapse.gife.org.br/download/global-reporting-initiative-g4-manual-de-implementacao

Gould, C. (1983). One Percent of the Big Eight. Working Woman.

Gri Standards. (2017). Mapping G4 to the GRI Standards. https://www.globalreporting.org/standards/media/1098/mapping-g4-to-the-gri-standards-disclosures-full-overview.pdf.

Haslam, S. A., & Ryan, M. K. (2008). The road to the glass cliff: Differences in the perceived suitability of men and women for leadership positions in succeeding and failing organizations. The Leadership Quarterly, 19(5), 530-546. https://doi.org/10.1016/j.leaqua.2008.07.011

Jaime, P. (2011). Para além das pink collars: gênero, trabalho e família nas narrativas de mulheres executivas. Civitas-Revista de Ciências Sociais, 11(1), 135-155. https://doi.org/10.15448/1984-7289.2011.1.6811

Kpmg Auditores Independentes-KPMG. (2017). Relatório de sustentabilidade 2016. https://sustentabilidade.kpmg.com.br/html/arquivos/relatorioKPMG2016-completo.pdf

Kpmg Auditores Independentes-KPMG. (2018). Relatório de sustentabilidade 2017. https://sustentabilidade.kpmg.com.br/html/arquivos/relatorioKPMG2017-completo.pdf

Kpmg Auditores Independentes-KPMG. (2019). Relatório de sustentabilidade 2018. https://sustentabilidade.kpmg.com.br/html/arquivos/relatorioKPMG2018-completo.pdf

Kpmg Auditores Independentes-KPMG. (2020). Relatório de sustentabilidade 2019. https://sustentabilidade.kpmg.com.br/html/relatorio/KPMG2020_Completo_PT.pdf

Kpmg Auditores Independentes-KPMG. (2021a) Relatório de sustentabilidade 2020. https://sustentabilidade.kpmg.com.br/html/relatorio/KPMG2020_Relato_PT.pdf

Kpmg Auditores Independentes-KPMG. (2021b). Rumo à igualdade. KPMG Business Magazine. https://home.kpmg/content/dam/kpmg/br/pdf/2017/03/br-kpmg-business-magazine-40-capa.pdf

Kpmg Auditores Independentes-KPMG. (2022) Relatório de sustentabilidade 2021. https://midia.kpmg.com.br/site/2022/11/2021_KPMG-Brasil-Relatorio-Sustentabilidade-completo.pdf.

Kpmg Auditores Independentes-KPMG. (2023) Relatório de sustentabilidade 2022. https://assets.kpmg.com/content/dam/kpmg/br/pdf/2023/5/2022_KPMG-Brasil-Relatorio-Sustentabilidade-OIP-completo.pdf

Kpmg Auditores Independentes-KPMG. (2024) Relatório de sustentabilidade 2023. https://assets.kpmg.com/content/dam/kpmg/br/pdf/2024/02/KPMG_no_Brasil_Relatorio_de_Sustentabilidade_2023.pdf

Lavinas, L. (2001). Empregabilidade no Brasil: inflexões de gênero e diferenciais femininos. Rio de Janeiro: IPEA, 2001. https://repositorio.ipea.gov.br/handle/11058/2064

Lupu, I. (2012). Approved routes and alternative paths: The construction of women’s careers in large accounting firms. Evidence from the French Big Four. Critical Perspectives on Accounting, 23(4-5), 351-369. https://doi.org/10.1016/j.cpa.2012.01.003

Lupu, I., & Empson, L. (2015). Illusio and overwork: playing the game in the accounting field. Accounting, Auditing & Accountability Journal. https://doi.org/10.1108/AAAJ-02-2015-1984

Machado, D. G. (2012). Influência da política de remuneração dos executivos no nível de gerenciamento de resultados em empresas industriais brasileiras, estadunidenses e inglesas. (Doctoral thesis). Universidade Regional de Blumenau, Blumenau, Santa Catarina, Brasil. http://bu.furb.br/docs/TE/2012/350408_1_1.pdf

Meinhard, V. R., & Faria, J. H. (2020). Representatividade das Mulheres na Hierarquia de Empresas: Estudo de caso com base no Women's Empowerment Principles. Revista Eletrônica de Ciência Administrativa, 19(1), 33-60. https://doi.org/10.21529/RECADM.2020002

Morgenroth, T., Kirby, T. A., Ryan, M. K., & Sudkämper, A. (2020). The who, when, and why of the glass cliff phenomenon: A meta-analysis of appointments to precarious leadership positions. Psychological Bulletin, 146(9), 797. https://doi.org/10.1037/bul0000234

Morrison, A.M., & Glinow, M.A.V. (1990). Women and minorities in management. American Psychologist, 45(2), 200-208.

Nações Unidas Brasil. (2022). Objetivosde Desenvolvimento Sustentável.https://www.google.com/search?q=como+referenciar+site+abnt&rlz=1C1GCEB_enBR953BR953&oq=como+referenciar+site+&aqs=chrome.1.69i57j0i512l9.10377j0j7&sourceid=chrome&ie=UTF-8

Naguib, R., & Madeeha, M. (2023, May). “Making visible the invisible”: Exploring the role of gender biases on the glass ceiling in Qatar's public sector. Women's Studies International Forum, 98, 102723. https://doi.org/10.1016/j.wsif.2023.102723

Pear, R. (1987). Women reduce lag in earnings but disparities with men remain. New York Times, September, 4, 1. https://www.nytimes.com/1987/09/04/us/women-reduce-lag-in-earnings-but-disparities-with-men-remain.html

Pena, É. D. P. (2015). Carreira de sucesso sob a perspectiva de sócias auditoras de Big Four no Brasil. (Master’s thesis). University of São Paulo, São Paulo, São Paulo, Brasil. https://doi.org/10.11606/D.12.2018.tde-15032018-160257

Polen. (2021). Global Reporting Initiative (GRI): Tudo o que você precisa saber. https://www.creditodelogisticareversa.com.br/post/t-global-reporting-initiative-gri-tudo-o-que-voce-precisa-saber

Pricewaterhousecoopers Brasil Ltda - PwC. (2020). Relatórioanual 2020. https://www.pwc.com.br/pt/publicacoes/assets/2020/relatorio_anual_20-b.pdf

Pricewaterhousecoopers Brasil Ltda - PwC. (2024a). Transparency reporte 2023. PwC Brasil.https://www.pwc.com.br/pt/estudos/servicos/auditoria/2023/Transparency-Report-2023-PT.pdf

Pricewaterhousecoopers Brasil Ltda - PwC. (2024b). PwC Brasil. Quem somos. https://www.pwc.com.br/pt/quem-somos.html#:~:text=PwC%20no%20Brasil,em%20todas%20as%20regi%C3%B5es%20brasileiras

Princípio de Empoderamento das Mulheres (WEPs). (2016). ONU Mulheres Brasil. http://www.onumulheres.org.br/referencias/principios-de-empoderamento-das-mulheres/

Richardson, R. J. (1999). Pesquisa Social: Métodos e técnicas (3 ed.). São Paulo: Atlas.

Robert, H. A. L. F. (2016). Mulheres e o Mundo Corporativo. https://www.roberthalf.com.br/sites/roberthalf.com.br/files/legacy-pdfs/robert_half_-_mulheres_e_o_mundo_corporativo.pdf

Rodrigues, M. S., Júnior, Oliveira, M. C., Marcos, I. M. A. R. A., & Rodrigues, G. R. (2017). Divulgação de informações sociais Relativas a Gênero pelas empresas Brasileiras Signatárias dos Women’s Empowerment Principles. Journal on Innovation and Sustainability RISUS, 8(4), 3-23. https://doi.org/10.24212/2179-3565.2017v8i4p3-23

Roth, L. M. (2007). Women on Wall Street: Despite diversity measures, Wall Street remains vulnerable to sex discrimination charges. Academy of Management Perspectives, 21(1), 24-35. https://doi.org/10.5465/amp.2007.24286162

Rudman, L. A., & Glick, P. (1999). Feminized management and backlash toward agentic women: the hidden costs to women of a kinder, gentler image of middle managers. Journal of Personality and Social Psychology, 77(5), 1004. https://doi.org/10.1037/0022-3514.77.5.1004

Santos, C. M. M., Tanure, B., & Carvalho, A. M., Neto. (2014). Mulheres executivas brasileiras: o teto de vidro em questão. Revista Administração em Diálogo, 16(3), 56-75. https://doi.org/10.20946/rad.v16i3.13791

Santos, M. A. D., Melo, M. C. O. L. & Batinga, G. L. (2021). Representatividade da Mulher Contadora em Escritórios de Contabilidade e a Desigualdade de Gênero na Prática Contábil: Uma Questão ainda em Debate? Sociedade, Contabilidade e Gestão, 16(1), 148-163. https://doi.org/10.21446/scg_ufrj.v0i0.30679

Smith, R. (2014). Images, forms and presence outside and beyond the pink ghetto. Gender in Management: An International Journal, 29(8), 466-486. https://doi.org/10.1108/GM-02-2014-0012

Souza, L. P., & Guedes, D. R. (2016). A desigual divisão sexual do trabalho: um olhar sobre a última década. Estudos Avançados, 30, 123-139. https://doi.org/10.1590/S0103-40142016.30870008

Souza, A.E., & Guimarães, V. N. (2000). Gênero no espaço fabril. Anais do XXIV Encontro da Associação Nacional de Pós-Graduação e Pesquisa em Administração - ENANPAD. Florianópolis, Brasil, 24. https://arquivo.anpad.org.br/eventos.php?cod_evento=&cod_evento_edicao=4&cod_edicao_subsecao=51

Steil, A.V. (1997). Organizações, gênero e posição hierárquica – compreendendo o fenômeno do teto de vidro. Revista de Administração da Universidade de São Paulo (RAUSP), 32 (3). http://rausp.usp.br/wp-content/uploads/files/3203062.pdf

Sung, S. (2022). The economics of gender in China: women, work and the glass ceiling (1 ed.). New York: Taylor & Francis. https://doi.org/10.4324/9781003307563

Topić, M. (2020). It’s something that you should go to HR about'–banter, social interactions and career barriers for women in the advertising industry in England. Employee Relations: The International Journal, 43(3), 757-773. https://doi.org/10.1108/ER-03-2020-0126

Vetter, J. (2021). The Glass Cliff – Women’s Thrive to Save Poor Performance and how to Approach it in the Workplace. Junior Management Science, 6(1), 39–59. https://doi.org/10.5282/jums/v6i1pp39-59.

Xie, Y., & Zhu, Y. (2016). Holding up half of the sky: womwn managers’ view on promotion opportunities at enterprose level in China. Journal of Chinese Human Resource Management. https://doi.org/10.1108/JCHRM-11-2015-0015

Información adicional

Special Call: (In)Equality, Diversity and Inclusion – Organizational and Accounting Approaches: Guest editors: Carlos Adriano Santos Gomes Gordiano, Sandra Maria Cerqueira da Silva & Joao Paulo Resende de Lima