Artículos

Incidence of the pricing system on the performance of handcrafted wood furniture production enterprises

Incidencia del sistema de precios en los resultados de las empresas artesanales de producción de muebles de madera

Incidence of the pricing system on the performance of handcrafted wood furniture production enterprises

Journal of business and entrepreneurial studies, vol. 5, núm. 3, 2021

Universidad de Oriente

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-CompartirIgual 4.0 Internacional.

Recepción: 14 Marzo 2020

Aprobación: 04 Febrero 2021

Abstract: The artisan activity has turned some areas of Ecuador into benchmarks for the manufacture of wooden furniture. The experience of the artisan is hegemonic to the technification, however, these productive units have not established guidelines that allow the artisan to have a clear financial overview, reflecting the reality of manufacturing wooden furniture, limiting the producers a futuristic vision of growth. In the research, the incidence of pricing in the financial results obtained in the last year is analyzed, with information provided by the artisans through the application of research techniques and supported by the theoretical framework. The analysis of the results allowed to know the incidence of the variables pricing and commercialization in the behavior of the financial results, making necessary the application of a simple method for the accumulation of costs, which allows a decision of prices according to the characteristics of the sector.

Keywords: Pricing, marketing, profitability.

Resumen: La actividad artesanal ha convertido algunas zonas del Ecuador en referentes de fabricación de muebles de madera. La experiencia del artesano es hegemónica a la tecnificación, sin embargo, estas unidades productivas no han establecido lineamientos que permita al artesano tener un claro panorama financiero, que reflejen la realidad de fabricar muebles de madera, limitando a los productores una visión futurista de crecimiento. En la investigación, se analiza la incidencia de fijación de precios en los resultados financieros obtenidos en el último año, con información proporcionada por los artesanos mediante la aplicación de técnicas de investigación y sustentada en el marco teórico. El análisis de los resultados permitió conocer la incidencia de las variables fijación de precios y comercialización en el comportamiento de los resultados financieros, haciendo necesario la aplicación de un método sencillo para la acumulación de costos, que permita una decisión de precios acorde a las características del sector.

Palabras clave: Fijación de precios, comercialización, utilidades.

INTRODUCTION

As defined at the International Symposium on Handicrafts and the International Market, handicraft products have stood out for having as their inputs the component of manual labor, work with natural materials and creativity in design, the latter being their main letter of presentation. Therefore, the special nature of handicraft products is based on their distinctive characteristics, which may be utilitarian, aesthetic, creative, culturally linked, decorative, functional, traditional, symbolic and religiously and socially significant.

Similarly, the improvement of the production process and the variety of designs have been key factors for the development of activities, making manufacturers more committed to their work. However, increased competition and the inadequate use of costing techniques have brought the following problems to the sector:

A contraction in sales as a result of the economic recession, which has had a direct impact on sales results. Inadequate pricing system without a technical study or pricing formulas that guarantee the recovery of production costs. Overvalued or undervalued production costs. The marketing of wood furniture is not related to product demand, making it difficult to maintain a competitive advantage by wasting installed capacity and, in other cases, overproducing without considering an operational break-even point, directly impacting operating income.

However, the handicraft sector, despite being important in the country's economy, has not received the attention it deserves, causing shortcomings in its normal development and growth. In the results of the research on SMEs, "the price of the products of manufacturing companies is an important factor that can be measured in the dimension of the pricing mechanisms of a product, since the income of the companies will depend on this decision".

In the development of the research, three categories of study are proposed: pricing, furniture commercialization and financial results. The purpose of this is to analyze the existing problems in the wood furniture production sector in order to determine if the pricing system effectively covers the needs of the factories. For data collection, research techniques were applied to artisans qualified by the National Board for the Defense of Artisans who have wood furniture manufacturing workshops in the Huambaló Parish, in order to evaluate each variable and test the hypothesis. Consequently, the development of the research aims to analyze from pricing and its variables, what are the parameters that define the decision to assign the price of the products, the marketing guidelines used by artisan producers of wooden furniture and how these affect the financial results (Ron & Sacoto, 2017, p. 9).

The Craftsmen's Defense Law states in its first article that craftsmen are protected to assert their rights personally or through trade associations, unions and interprofessional associations in any of the branches, arts, trades or services. It also defines important terms to be considered in the artisan sector:

"Artisanal activity: The activity practiced manually for the transformation of raw material destined to the production of goods and services, with or without the aid of machines, equipment or tools;

Artisan: A manual worker, workshop master or self-employed artisan who, duly qualified by the National Board for the Defense of Artisans and registered with the Ministry of Labor and Human Resources, develops his activity and work personally and has invested in his workshop, in work implements, machinery and raw materials, an amount not exceeding twenty-five percent (25%) of the capital fixed for small industry. Likewise, a manual worker is considered an artisan even if he has not invested any amount in work implements or lacks workers;

Workshop Master: The person of legal age who, through the technical colleges of artisan education, artisan training establishments or centers and legally constituted trade organizations, has obtained such title granted by the National Board for the Defense of Artisans and endorsed by the Ministries of Education and Culture and of Labor and Human Resources;

Operator: A person who, without fully mastering the theoretical and practical knowledge of an art or craft and having ceased to be an apprentice, contributes to the production of handicrafts or the provision of services, under the direction of a workshop master;

Apprentice: Is the person who enters an artisan workshop or an artisan teaching center, with the purpose of acquiring knowledge on an artisan branch in exchange for personal services for a determined time, in accordance with the provisions of the Labor Code; and, Artisan Workshop: Is the premises or establishment in which the artisan habitually exercises his profession". (National Assembly of Ecuador, 2008, p. 5).

Artisanal production units are all organizations or workshops that manufacture goods or services that are handmade or that in their production process 70% involve the skills of the workshop master, operator and apprentices. The characteristic that differentiates handmade products is qualitative in that "each product that comes out of the artisan's hands is unique and unrepeatable. From the above derives the importance of handicraft production units as a legacy of culture and an important part of the social and economic development of a country, as well as generators of sources of employment.

As a consequence of its activities, the daily development of the artisan workshops requires the joint work of all administrative and financial areas such as:

First the production function where the transformation of raw material into finished products is developed, in the case of furniture manufacturing, the production process is established in five defined processes. The success of the company depends to a great extent on this function.

Secondly, the financial area, where the economic resources resulting from the business line are managed, and the cost center, which is the function specialized in proposing a methodology for the accumulation of production costs incurred in each transformation process.

Third, the administrative function in two areas where the activities of the administrative process and human resources are developed, regarding the selection, hiring and induction of operators, apprentices in the production area, as well as workers in general for marketing and administration areas.

Finally, commercialization and marketing where guidelines are established to determine the sales channel and promotion of the products (Aguero 2018, p. 10).

"The pricing process represents one of the many issues that are fundamental to organizations. It is taken in this way because it is one of the most complex obstacles faced by management bodies. The operating income in the income statement, will be one of the starting points to achieve the profit margins that are established in the budgets of the companies." (Cadena, 2017, p. 10).

Pricing in handicraft workshops is a determining administrative decision directly related to income and consequently to profits. For this reason, it is essential that companies establish strategies that serve as a guideline for optimal product pricing. In this regard, it indicates that there are multiple methods or strategies for pricing and the marketing and finance departments are in charge of finding the most optimal one.

The strategy of setting a target oriented to the expected return establishes a specific level of profits as a goal. Many companies seek a stable yield, which is set according to the characteristics of each company and has managerial advantages in large companies.

The fixation strategy with "the sales-oriented objective tries to reach some level of sales or market share without relating to profits, many companies are more interested in sales growth than in the level of profits. "Market share objectives are very frequent, they are based on the premise that the higher the volume of sales in the future, the greater the justice to sacrifice profits in the short term. (Viteri et al., 2018, p. 21) In other words, "They are called Differential Strategies and involve price discrimination according to the economic capacity, sociodemographic characteristics and price sensitivity of the different market segments. This discrimination may be carried out on a temporal or spatial basis..." (Pérez, 2006, p. 9) From the above, two strategies can be extracted: one assumes that the product is sold at the same price and with the same sales conditions, and the other is random discounting, which is the reduction of the price at any time. This strategy involves selling in large volumes in such a way that the yield is not in the profit margin but in the quantity sold (Pérez, 2006, p. 7).

Starting from the product "Crafts is a truly economic activity and the core of the development process is marketing. The customer does not buy out of a sense of sympathetic interest in the craftsman; the product has to be competitively priced, aesthetically pleasing, functional and useful. The product can only be marketed if it is attractive to consumers, that is, if the traditional technique is adapted and designed to meet the taste and needs of the contemporary consumer. Craft producers cannot be economically viable if they cannot be marketed." (Rica et al., 2010, p. 45) "Obviously, price and product are closely related, the price sends signals to the buyer about the quality of the product. In addition, the incidence of the product life cycle must be considered; at the beginning of the product life cycle prices tend to be high as a consequence of the existence of a single seller, but as competition increases prices tend to decrease." Therefore, the variety of products that the workshops offer to the market will have a greater impact on the level of income, directly affecting their financial situation. As a result of the above, product differentiation factors must be established, which are framed in aspects such as quality, variety of products, designs, shapes, payment facilities, delivery facilities and the acquisition of such products. (Rica et al., 2010, p. 30).

A second factor is the distribution channel of handcrafted products, specifically wood furniture for the home, it is important to determine how the product leaves the manufacturer and reaches the final consumer.

The distribution channels affect the financial situation, since the system used may increase operating costs, "The product's marketing channels will significantly condition the final price of the product. Marketing margins incorporate significant expenses on the final price to the consumer". Consequently, the sale of wood furniture is carried out through distribution channels directly from the manufacturer to the final consumer and indirectly from the manufacturer through the intermediary to the final consumer, as summarized below (Pérez, 2006, p. 23).

"From the point of view of finance, the branch of financial management gathers most of the approaches of economic theory and adapts them with a simple algebraic development and the same two basic objectives: the maximization of profit and the maximization or increase of income..." Having a control over the financial situation and results of the company allows the management an optimal control and decision making, as well as having a clear awareness of production costs, and consequently a pricing more in line with the reality and the environment where companies are developed (Cadena, 2017, p. 10).

As indicated by Márquez, income is defined as the price of the products sold or services rendered. Under this precept, operational income is the income derived from the business line, which is the product of the sale of the goods produced by the company and is directly related to the setting of the price, since the price will determine the level of income and, consequently, the profit margins. (Márquez, 2005, p. 13).

Non-operating revenues are values that correspond to sales of goods or services derived from or complementary to the business, without being the main activity of the company.

"It is defined as the value sacrificed to acquire goods or services that is measured in dollars by reducing assets or incurring liabilities at the time benefits are earned. At the time of acquisition, the cost incurred is to achieve present or future benefits. When these benefits are utilized, the costs become expenses."

Expense in turn is defined as a cost that has produced a benefit and has expired. Unexpired costs that may yield future benefits are classified as assets.

The gross margin provides information on the profitability of sales versus cost of sales and the company's ability to cover operating expenses and generate profits before deductions and taxes. The calculation formula is presented below:

(1)

(1)The operating margin is of great importance because it reflects whether or not the business is profitable regardless of how it has been financed, since this margin is influenced by the cost of sales but also by operating expenses (administration and sales).

In reference to the above, it is important to know that financial expenses are not considered as operating expenses, since without them the company can operate without difficulty. The calculation formula is as follows:

(2)

(2)The net margin shows the profit per unit of sale, for this calculation not only the operating margin is studied but also other income, with the following calculation formula:

(3)

(3)The operating return on equity ratio identifies the profitability that the company is able to offer to the partners or shareholders on the capital they have invested in the company, without taking into account the impact of financial expenses, taxes and employee participation.

(4)

(4)The financial profitability index is an important indicator that measures the net profit generated in relation to the investment of the shareholders or owners, and is calculated as follows:

(5)

(5)MATERIALS AND METHODS

Based on similar studies, a shortcoming in the SME sectors is the way of setting prices, therefore, two independent variables and a dependent variable were determined to establish whether the pricing and marketing system used by artisans to determine the selling price of wooden furniture, index in the profit margins.

Once the information gathering techniques were applied to the artisan producers of wooden furniture, the analysis of the results allows evaluating the incidence of pricing on the financial results of these productive units. The information collected responds to each item, variable and consequently to each of the study categories as established in the operationalization matrix that summarizes the aspects that were investigated. Consequently, each of the variables or categories responds to the specific and general objectives set out in this research, which were:

To analyze the incidence of the pricing system in the handicraft sector producer of wooden furniture in the parish of Huambaló, canton Pelileo through quantitative and qualitative methods to measure the behavior of the financial results. Determine the pricing mechanisms used in the commercialization of wooden furniture in the artisan sector dedicated to the activity of manufacturing wooden furniture in Huambaló. Determine the marketing procedures of wooden furniture of the handicraft companies of Huambaló. To evaluate the financial and operational results of the artisan wood furniture manufacturing companies. Therefore, an adequate methodology was established, with the application of information gathering techniques and procedures that provide elements of analysis; adequate for the population under study. The sample was established with the database of the Internal Revenue Service, delimited to the artisan taxpayers qualified by the JNDA and are producers of wooden furniture, for this task an unstructured interview was applied to two of the oldest artisans in the sector.

Once the collection instruments were applied, the results were obtained with which the analysis was structured by objective, category, variable and item, for a better understanding. Consequently, it was possible to test the alternative hypothesis and conclude that the pricing of wood furniture is done based on the current situation (competition) without conducting a study of production costs, while the marketing of furniture is predominantly done in an indirect channel of distribution (Cadena, 2017, p. 23).

The two considerations mentioned above have a direct impact on the financial results of these productive units, reducing the expected net profit margin from 20% to 9.41%. However, the artisans do not have a real awareness of their net profit because the cash flow is constant, product of the permanent sale of furniture, and they measure their profits based not on a technical study but on the increase of their production inputs. The analysis of all the results obtained in the research is presented below.

RESULTS

After reviewing the factors that influence the pricing of wooden furniture, it can be concluded that the artisans in Huambaló set their prices based on the current situation, i.e., maintaining a balance in the strong competition that exists in the sector. As a secondary point, their prices are focused on the profit generated by the sale of their products, setting an expectation of twenty percent net profit, as reflected in the following table:

| always | almost always | Sometimes | Never | |

| 31 or more | 21 a 30 | 11 a 20 | less than 10 | |

| Results-oriented | 11% | 33% | 56% | 0% |

| Sales-oriented | 0% | 0% | 28% | 72% |

| Oriented to the current situation | 78% | 17% | 0% |

The data obtained show that the most sold product is bedroom sets, which, according to the distribution chain, can be produced in any of the five stages of the production process (carpentry, coating, lacquering, upholstery, finishing), with the carpentry stage being the most marketed. A point of analysis in marketing is the differentiation factors which constitute standards that allow the consumer to make the decision to purchase a product or service.

| Alternative | f. | f. r | F. A. |

| The price of furniture | 0 | 0% | 0% |

| Payment facilities | 0 | 0% | 0% |

| Variety of furniture | 33% | 33% | |

| The quality of the furniture | 50% | 50% | |

| Customer service | 17% | 17% | |

| Total | 100% |

Table 2 shows the factor that the artisans consider as the plus of their products, 50% the quality of the furniture, 33% the variety in terms of design and 17% the service they provide.

As for the quality of the furniture, a limiting factor is the wood, the new regulations of the Ministry of the Environment have established a rigorous registry for those who demand this raw material. The financial information was collected based on estimates of annual sales and production costs, considering 2017 as a reference point. The relevant data regarding production costs represent 86.46% of income, i.e., for every dollar of income 0.87 cents is to recover the investment in costs. Net income is 9.41% after covering operating and financial expenses.

Likewise, the estimation of assets and liabilities was made based on the artisans' perception. It was established that 70% of the assets are made up of equity capital and 30% of third party capital.

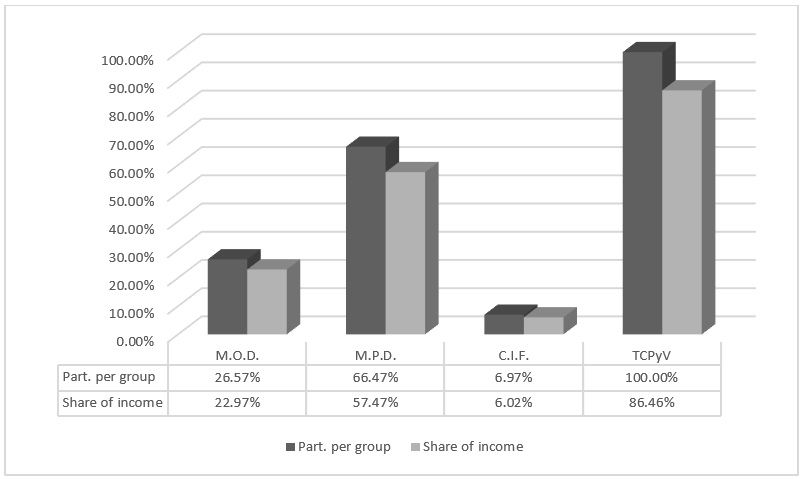

Fig. 1

Share of production cost

When analyzing the participation of costs as shown in Figure 1 in relation to operating income, total costs represent 86.46% of which 22.97% corresponds to direct labor, 57.47% to raw material inputs and 6.02% to indirect manufacturing costs.

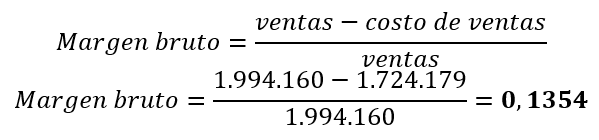

The analysis of the profit margins gives a guideline of the level of efficiency of the handicraft companies, the gross margin represents 13.54% of sales, from this percentage we deduct 4.02% of administrative and selling expenses, leaving an operating margin of 9.52%, while financial expenses correspond to 0.11%.

The net margin after covering operating and financing costs and expenses is 9.41%. This indicates that the selling price does not meet the artisans' expected net profit of 20%, even though the gross margin covers administrative, sales and financial expenses.

An important point to clarify in reference to operating expenses is that 72% of the artisans do not have showrooms or direct sales premises, so this item is not representative.

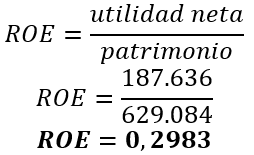

The calculation of the profitability index shows a positive effect of leverage, as ROE (29.83%) is higher than ROA (22.19%), which indicates that the financing of assets with debt has made it possible to increase financial profitability.

As shown in Table 3, the gross margin on furniture sales represents 13.54% and indicates that the workshops are able to cover operating expenses and obtain a net profit margin.

| Total income | 1.994.160 | |

| Total costs | 1.724.178 | |

| Gross margin | 269.981 | |

| Gross margin index | 13,54% |

(6)

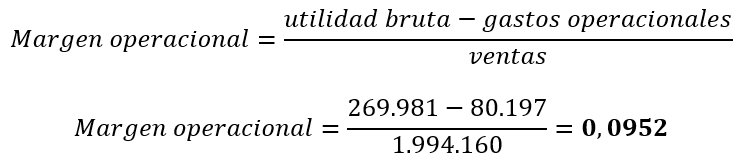

(6)When the calculation is made as shown in Table 4, the result of the operating margin index is 9.52% with respect to sales, this indicator shows that the business of manufacturing and selling furniture is profitable regardless of the form of financing. It is important to add that, for the population under study, it is not in line with the expectations that they expect to obtain from the sale of their furniture because of all that is involved in its manufacture.

| Gross profit | 269.981,08 |

| Operating expenses | 80.196,96 |

| Operating margin | 189.784,12 |

| Operating margin index | 9,52% |

(7)

(7)The net profit for the year is obtained from the operating profit minus financial expenses; in the case of artisanal companies, the net margin is 9.41% in relation to sales.

| Operating income | 189.784 |

| Financial expenses | 2.148 |

| Sales | 1.994.160 |

| Net income | 187.636 |

| Net margin | 9,41% |

(8)

(8)In the specific case of artisans qualified by the Junta Nacional de Defensa del Artesano, they are exempt from paying 15% for profit sharing to workers, and as for income tax, since most of them are individuals, they are not required to keep accounting records; each taxpayer maintains different contribution percentages, which is why the calculation of taxes has not been considered for this study.

The financial profitability ratio relates a dynamic element (profit for the year) and a static element (equity), which makes it possible to know how a company's capital is used in the development of its activities.

(9)

(9)From the calculation of financial profitability, the artisanal wood furniture manufacturing company represents 29.83%, which indicates that for every dollar of capital invested, it has a return of 0.29 cents.

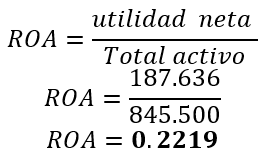

ROA determines how much of the company's resources contribute to the generation of economic benefits, i.e., how quickly the resources provided to finance the company are converted into cash.

(10)

(10)The calculation of the return on assets of the artisan workshops yields a result of 22.19%, which indicates the efficiency in converting the investment into profits, i.e., for every dollar invested, the workshop generates $0.22 cents.

DISCUSSION

The results obtained are the product of the information collected for each category of study and the analysis of the quantitative and qualitative data from the population studied in aspects of pricing, product marketing (wood furniture) and the financial results presented by them. Consequently, with the most relevant aspects, the hypothesis is proved and it is established that the way of assigning the price of the furniture has an impact on the profits of the companies. When comparing the profit margin that the artisans expect or consider they are earning of 20% with the results obtained in terms of net profit of 9.41%, there is a difference of 10.59%.

CONCLUSIONS

From the literature review and once the information on pricing, marketing and production costs of artisans qualified by the National Board for the Defense of Artisans had been processed, the information was analyzed in a structured manner for each item, variable and category of study, which responded to the objectives formulated and the verification of the hypothesis proposed.

As a result of the research, it was determined that pricing is defined by the current market situation, i.e. the competition, while the marketing of products is predominantly done through an indirect distribution channel, which affects the financial results by having a profit margin that does not meet the expectations and growth levels of the artisan wood furniture manufacturing units. Therefore, the way of setting prices is not adequate, but more than a production cost, an important and essential factor falls on the workshop master craftsman who is the right person to contribute, develop and generate new ideas, which can improve the company's guidelines.

Artisan wood furniture manufacturers set the price of their products based on the current situation, i.e. without a previous study, which has resulted in a net profit margin of 9.41%, compared to the expected 20%.

The above is understood in the sense that the price is set according to the standard price or under the price established by the competition. There are 110 taxpayers in the sector, 59% of which are natural persons engaged in marketing, while 41% are artisan manufacturers or workshop operators. In conclusion, 75% of the 110 taxpayers are directly involved with the competition in the sector.

External factors play an important role in the price decision because 61% of the buyers are manufacturers from other parts of the country, mainly Quito, Cuenca and Guayaquil, who purchase the blank products for subsequent finishing. This means that the price is fixed in the first production process only with the estimation of how much "more or less" it costs. In addition, since other manufacturers bargain on prices, net profit margins are further reduced.

Suppliers are selected considering several aspects, mainly the quality of inputs and raw materials involved in the manufacture of furniture, an important factor is the ease of payment, as they benefit the artisans, thus making suppliers financiers of production for a period of up to 90 days, an importance that was confirmed in the calculation of return on assets.

The lack of internal factors has a direct impact on pricing; artisans do not have a costing method that allows them to determine an optimal price for their products, and consequently the planning of production volumes is affected by the lack of awareness of their installed capacity. This is due to the lack of policies, strategies or guidelines defined to serve as guidelines for pricing decisions. Production costs are estimated sporadically when manufacturing a new design, thereafter the estimate is based on market prices. The marketing system is defined by an indirect distribution channel where the artisan sells his products in white to other manufacturers and these to the final consumer, only a small part of the marketing is through a direct channel, this form of marketing affects the profit margins because the artisan is in the scenario of setting a lower price, being the manufacturer or retailer who benefits. Income is derived from the sale of wood furniture, of which the total value corresponds To operating income, since the artisans do not have other activities derived from the business.

Production costs are not calculated technically, but on the basis of estimates, which has led to an undervaluation of costs, selling products at prices that cover the cost but do not satisfy the expected profit margin for everything involved in the production process.

Operating and financial expenses are not representative at the moment because they do not have administrative or sales personnel, while financial expenses derive from interest paid on loans that were invested in the business. However, the impact of this factor is important because having trained personnel would provide the artisans with real cost data and give them a boost in the area of sales.

The calculation of the profitability indexes shows a positive effect of leverage, as ROE is higher than ROA, which indicates that the financing of assets with debt has made possible an increase in financial profitability.

REFERENCES

Aguero D. E. (2018). La estrategia ambiental en pequeños negocios de artesanía, un ejemplo de medición. Investigación y Ciencia, 26(73), 74–83. http://www.redalyc.org/articulo.oa?id=67454781009

Ley De Defensa Del Artesano, Registro Oficial 71 1 (2008). http://www.artesanos.gob.ec/institutos/wp-content/uploads/downloads/2018/01/LEY-DE-DEFENSA-DEL-ARTESANO-1.pdf

Cadena, J. B. (2017). La Teoría Económica Y Financiera Del Precio: Dos Enfoques Complementarios. Criterio Libre, 9(15), 59–80. https://doi.org/10.18041/1900-0642/criteriolibre.2011v9n15.1202

Márquez, A. (2005). Una mirada integral a la decisión de precios de la organización. Revista Visión Gerencial, 0(1), 42–52.

Medina, S. A., Ruata, S. A., Contreras, S. F., & Cañizalez, B. D. C. (2018). Contabilidad de Costos. In Contabilidad de Costos. https://doi.org/10.29018/978-9942-792-03-7

Pérez, D., & Pérez, I. (2006). El Precio. Tipos y Estrategias de fijación. EOI Marketing, 4, 53.

Rica, U. D. C., González, C., Julia, R., Actual, E., Sobre, Y. P., Comercialización, L. A., Rica, U. D. C., Universitaria, C., Monge, C., & Rica, C. (2010). PRODUCTOS ARTESANALES EN EL CANTÓN DE POCOCÍ. Intersedes, 6(20), 192–206. http://www.redalyc.org/articulo.oa?id=66619992012

Ron, R., & Sacoto, V. (2017). Las Pymes ecuatorianas: su impacto en el empleo como contribución del Pib Pymes al Pib total. Espacios, 38, 11. https://www.revistaespacios.com/a17v38n53/a17v38n53p15.pdf

Viteri, F. E., Herrera-Lozano, L. A., & Bazurto-Quiroz, A. F. (2018). Marketing Online: Un enfoque global. Polo Del Conocimiento, 2(12), 258. https://doi.org/10.23857/pc.v2i12.449

Notas de autor