Sur-Sur

The demand for life insurance: a quantitative study among “generation y” in the Klang Valley, Malaysia

La demanda de seguros de vida: un estudio cuantitativo entre la “generación y” en el Valle de Klang, Malasia

The demand for life insurance: a quantitative study among “generation y” in the Klang Valley, Malaysia

RELIGACIÓN. Revista de Ciencias Sociales y Humanidades, vol. 5, núm. 25, pp. 302-314, 2020

Centro de Investigaciones en Ciencias Sociales y Humanidades

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-SinDerivar 4.0 Internacional.

Aprobación: 28 Agosto 2020

Publicación: 30 Septiembre 2020

Abstract: Despite the importance of life insurance as an investment for protection, especially the young generation, they still are unaware of the importance of purchasing their own life insurance. Therefore, the objective of this study was to investigate factors related to the demand for life insurance among “Generation Y” in the Klang Valley, Malaysia. Using a purposive sampling method, a total of 320 respondents from Klang Valley, Malaysia were involved in this study. All data gathered were tabulated and analyzed using SPSS, employing Descriptive Analysis, Independent Sample T-Test, One-way ANOVA, Pearson’s Correlation Analysis, and Multiple Linear Regression Analyses. The results showed that there is a moderately important level of demand for life insurance among the “Generation Y”. Significant differences were found in the demand for life insurance in accordance with gender, age group, monthly income, and education level. Besides, significant relationships were found between income level, knowledge of life insurance, income protection, risk attitude, and demand for life insurance. Furthermore, risk attitude, income level, knowledge of life insurance, and income protection were the predictor factors of demand for life insurance.

Keywords: Life insurance, “Generation Y”, quantitative, Malaysia.

Resumen: A pesar de la importancia del seguro de vida como inversión para la protección, especialmente de la generación joven, éstos todavía no son conscientes de la importancia de adquirir su propio seguro de vida. Por lo tanto, el objetivo de este estudio fue investigar los factores relacionados con la demanda de seguros de vida entre la “Generación Y” en el Valle de Klang, Malasia. Utilizando un método de muestreo intencional, un total de 320 encuestados del Valle de Klang, Malasia, participaron en este estudio. Todos los datos reunidos fueron tabulados y analizados usando SPSS, empleando Análisis Descriptivo, Prueba T de Muestra Independiente, ANOVA unidireccional, Análisis de Correlación de Pearson, y Análisis de Regresión Lineal Múltiple. Los resultados mostraron que hay un nivel moderadamente importante de demanda de seguros de vida entre la “Generación Y”. Se encontraron diferencias significativas en la demanda de seguros de vida de acuerdo con el género, el grupo de edad, los ingresos mensuales y el nivel de educación. Además, se encontraron relaciones significativas entre el nivel de ingresos, el conocimiento de los seguros de vida, la protección de los ingresos, la actitud de riesgo y la demanda de seguros de vida. Además, la actitud de riesgo, el nivel de ingresos, el conocimiento de los seguros de vida y la protección de los ingresos fueron los factores predictivos de la demanda de seguros de vida.

Palabras clave: Seguro de vida, “Generación Y”, cuantitativo, Malasia.

1. INTRODUCTION

1.1 Background of the Study

Nowadays, many Malaysians constantly face risks and uncertainties, and they could not foresee when they may fall sick or when they need a huge amount of money to cover their medical costs. In the worst case, they may even have to face a sudden death. Fundamentally, life insurance is protection from the fact that policyholders or specific recipients will get some measure of compensation from insurance organizations when faced with uncertainties, such as genuine illness or death (Loke & Goh, 2012). Insurance policies can even give a stable income during retirement. Regularly, the maturity of the life insurance policy takes a long-term period, and it needs periodic premium payments either monthly, quarterly, or annually (Beck & Webb, 2003).

In past decades, life insurance isn’t acclaimed in Malaysia considering the reality that the misinterpretation of insurance (Bank Negara Malaysia [BNM], 2018). Most Malaysians considered that insurance can be a fraud and is like a paper with a guarantee and is not essential. It may take some time for Malaysians to purchase insurance coverage. However, they do not accept the fact that insurance agencies politely compensate claims, nor do they believe in the protection that insurance can offer to support them throughout their lives. Many people are suffering from a well-known crisis, admitting that they are not at risk, even though they are clearly in danger, but they choose to ignore it. Other times, some citizens don’t buy insurance in the prior due to the un-realization on their prospective money related to chance and lack of financial resources (Malaysian Takaful Association [MTA], 2019).

In the past, one in ten Malaysians had a life insurance policy. To date, the rate has increased slightly to

3.5 for 10 Malays (Ng, 2018). This will be of concern because the rate of invasion of life coverage did not increase dramatically as expected. The Malaysian population was weak in the face of the danger of the presence that may have always denied its future benefit. The main reason for this test territory being investigated is the low rate of invasive life cover in Malaysia.

The protection standpoint for Malaysians by the end of the year 2018 is commonly positive as open entryways for the protection area still existing (BNM, 2018). Solid interest in life coverage and the riches of the board items continue being upheld by positive long-haul basic patterns in Malaysia. These consolidate the low rate of penetration of protective advertising, the rapid expansion of the population of common workers, the high social security based on cash passes through the same as the improvement of life expectancy on earth. The auxiliary patterns provoke a solid interest in life insurance items above. However, there is also a part of Malaysians who can’t deal with the money related assurance.

This reality is increasingly articulated against the setting of rising healthcare costs, products and ventures turning out to be progressively costly and questionable public-sector safety nets. Because of this, Bank Negara Malaysia, combined with the insurance companies, presented in November 2017 a moderate insurance scheme known as “Perlindungan Tenang” (BNM, 2018). Getting rid of the three fundamental measures of attainability, availability, and straightforwardness, the goal of the plan is to propose reasonable insurance coverage to satisfy the budgetary insurance needs of the base 40% households (The Star, 2018).

In short, life insurance is essential for all Malays, especially for the young generation as an investment for protection. Life insurance is an important capacity to protect family members as well as provide security funds to people. In any case, the demand for life insurance from Malaysians is still not desirable. Despite increasing pressure on medical costs, many Malays, however, are still not aware of the importance of acquiring their own life insurance.

1.2 The Objective of the Study

The objective of this study is to investigate factors that related to the demand for life insurance among “Generation Y” in the Klang Valley, Malaysia.

1.3 Research Questions

The primary research questions to be addressed in this study are as follows:

- 1. 1.3.1 What is the level of the demand for life insurance among “Generation Y” in the Klang Valley, Malaysia?

- 2. 1.3.2 Is there any difference on the demand for life insurance among “Generation Y” in accordance with gender, age group, monthly income and education level?

- 3. 1.3.3 What is the relationship between income level, knowledge of life insurance, income protection, risk attitude, social influence and the demand for life insurance?

1.4 Hypotheses

-

H1: Income level is positively related to the demand for life insurance.

-

H2: Knowledge of life insurance is positively related to the demand for life insurance.

-

H3: Income protection is positively related to the demand for life insurance.

-

H4: Risk attitude is positively related to the demand for life insurance.

-

H5: Social influence is positively related to the demand for life insurance.

2. LITERATURE REVIEW

2.1 The Demand for Life Insurance

The study of demand on life insurance was initiated by Yaari in the 1960s’. The conceptual basis for life insurance demand was formulated by Yaari in 1965. Yaari’s work was grounded in the Theory of Consumer Choice that discussed determining factors of the demand for life insurance, namely price change, income, reference, and use-value. Yaari argued that any decision made by an individual on purchasing life insurance is also depending on his/her willingness to pass on money to family members as well as contribute income for retirement. It was placed that the demand for life insurance is a component of wealth, expected income over an individual’s lifetime, interest rates, life insurance policy expenses such as cost of administration, and the expected subjective discount in current expenses over future ones.

Beck and Webb (2003) continued Yaari’s work and expanded the previous framework by integrating the inclinations of dependents and beneficiaries into the model. The researchers argued that the demand for life insurance increases with income potential, knowledge of life insurance, the current value of beneficiary expenditures, and the level of risk aversion. On the other hand, another researcher, Todd (2004), found that the demand for life insurance decreases with the policy load factor, household wealth, and social influence, especially of loved ones: family, friends, colleagues, etc.

According to Mitra (2017), per capita, premium expenditure is a major factor that contributed to the demand for life insurance. Similarly, in the earlier studies by Tennyson and Yang (2014), Hwang and Greenford (2005), Browne and Kim (1993), Yuengert (1993) had an identical view. They also revealed that risk on the return of investment may seem to be a significant strong factor that influences the demand for life insurance.

Other researchers such as Ghimire, (2017), Sarkodie and Yusif (2015), Stroe and Iliescu (2013) added to the literature that consumers’ attitudes and perceptions influence the decision to purchase life insurance. For Loon et al. (2019), Redzuan (2014), Mahdzan and Victorian (2013), Loke and Goh (2012), they revealed that the determinants for life insurance in Malaysia were income, knowledge of the insurance, income protection on the investment, attitude towards life insurance and social influence.

2.2 Income Level and the Demand for Life Insurance

With current economics, the demand to buy life insurance is mainly influenced by one’s salary or income. Previous studies by Loon et al. (2019), Ghimire (2017), Fukuchi (2016), Shahriari & Shahriari (2016), Sarkodie and Yusif (2015), Redzuan (2014), Mahdzan and Victorian (2013) revealed that there was a significant and positive relationship between income level and demand for life insurance. The researchers agreed that the demand for life insurance would have been affected by their amount of income and source of income. Naturally, this led to a lower intensity of life insurance for low-income workers due to the fee of life insurance is expensive. On the contrary, those with higher incomes will have a higher demand for life insurance. Therefore, the following hypothesis is derived: H1: Income level is positively related to the demand for life insurance.

2.3 Knowledge of Life Insurance and the Demand for Life Insurance

Conceptually, lack of knowledge on insurance will lead to not buying a life insurance policy (Loon et al., 2019; Loke & Goh, 2012). According to the Life Insurance Association of Malaysia (LIAM, 2020), Malaysia’s life insurance industry has shown an impressive 14.9% growth in new business in 2019 This healthy performance was the result of the increase in awareness or knowledge among consumers on the life insurance protection that had raised their confidence and intension to buy the insurance. Therefore, people would normally seek professional advice before deciding on any purchase of an insurance policy. Previous studies indicated that there was a significant and positive relationship between knowledge of insurance policies and the intention to purchase the policy (Loon et al., 2019; Sarkodie & Yusif, 2015; Tennyson & Yang, 2014; Lee, 2012; Ioncica et al., 2012; Loke & Goh, 2012). Hence, the hypothesis that can be derived here is: H2: Knowledge of life insurance is positively related to the demand for life insurance.

2.4 Income Protection and the Demand for Life Insurance

The legacy is that an individual leaves his/her wealth to the beneficiaries as well as the beneficiaries enjoy the inherited wealth. Generally, as breadwinners, they try to leave their heirs with more wealth and have more requirements for life insurance. This phenomenon is known as the bequest motive by a financial planner (Arun et al., 2012; Bernheim, 1991; Fischer, 1973). Scholars such as Lewis (1989) and Bernheim (1991) established that a person who hoped to leave a lot of wealth in order to raise the demand for life insurance. They wanted to secure their income from being utilized in unsafe situations. The present value of beneficiary utilization as the demand for life insurance rises as the policyholder is aware of the uncertain life expectancy and greater legacy purpose. Previous researchers found that there was a significant and positive correlation between income protection and demand of life insurance (Loon et al., 2019; Ghimire, 2017; Mitra, 2017; Fukuchi, 2016; Mahdzan & Victorian, 2013; Arun et al., 2012; Loke & Goh, 2012). Therefore, the following hypothesis is established H3: Income protection is positively related to the demand for life insurance.

2.5 Risk Attitude and Demand for Life Insurance

Risk attitude has a crucial effect on buying a decision on life insurance. Risk is often referred to as the likelihood or threat of any negative event caused by measurable loss, injury, liability, loss, or external or internal weaknesses that can be prevented by active actions. The study of people’s attitudes towards risk has become of great concern in the developing field of behavioral finance, focusing on their financial planning as well as their methods of risk management, as the risk of an insurance group or individual is transmitted to another people or organization (Tennyson & Yang, 2014; Hwang & Greenford, 2005; Browne & Kim, 1993; Yuengert, 1993). Furthermore, the proportion of personal risk to purchase life insurance was split into numerous parts. The first concerns their financial risk in terms of their perceptions of health risks. Secondly, it is the exposure to safety and environmental risks, and thirdly, it concerns their events (Stroe & Iliescu, 2013).

Researchers like Loon et al. (2019), Fukuchi (2016), Ackah and Owusu (2012), argued that the demand for life insurance was affected positively as the increase in policy holder’s attitude towards the risk of his/her medical accidents and no provision of medical treatment for certain illness. Another study conducted by Stroe and Iliescu (2013), found that there was a significant connection between attitude towards risk and environmental context with the purchase of life insurance. Tennyson and Yang (2014) suggested those life experiences can affect the demand for life insurance as risk perceptions change. In this context, H4 is derived from H4: Risk attitude is positively related to the demand for life insurance

2.6 Social Influence and the Demand for Life Insurance

Social influence includes the influence of peers, family members, insurance agents, etc. The factors that influence the demand for life insurance are worth mentioning. Previous research showed a significant and positive correlation between social influence and the demand for life insurance (Loon et al., 2019; Fukuchi, 2016; Stroe & Iliescu, 2013; Ackah & Owusu, 2012; Cai et al., 2011). In their research, they found that there was a significant, positive, and strong relationship between these two variables. They argued that when a person buys insurance, it is because others do. In fact, they freaked them out when they saw their friends, neighbors, and family members engaged in a frivolous uninsured tragedy and began to trust in the importance of insurance protection. As a result, a person may have perhaps the same preferences and may also decrease their search cost. These findings supported an earlier study conducted by Dercon et al. (2011) that had determined the peer referral therapy, which is good for buyers who are able to persuade people to buy a life insurance policy. Loon et al. (2019), Fukuchi (2016), Sarkodie and Yusif (2015), Ackah and Owusu (2012), and Cai et al. (2011) revealed that most people will have a greater intention to buy insurance policy if they were introduced and referred by their significant others to an insurance agent. Therefore, the following hypothesis is derived from H5: Social influence is positively related to the demand for life insurance.

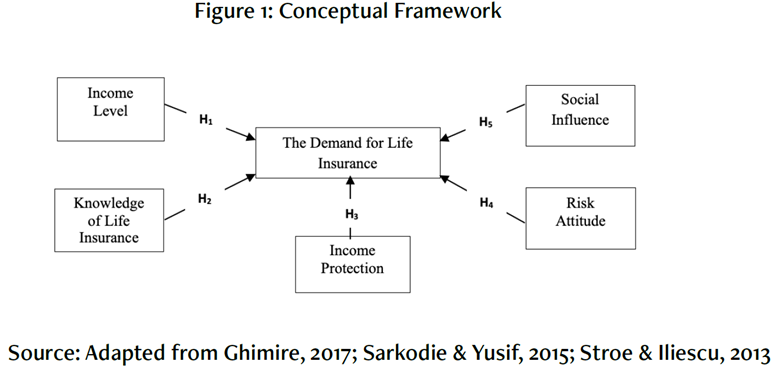

2.7 Conceptual Framework

Based on the literature review, this study posits that income level, knowledge of life insurance, income protection, risk attitude and social influence significantly related to the demand for life insurance. Figure 1 shows the conceptual framework for this study. It was adapted from the conceptual framework developed by Ghimire (2017), Sarkodie and Yusif (2015), Stroe and Iliescu (2013). The demand for life insurance is the dependent variable. Meanwhile, income level, knowledge of life insurance, income protection, risk attitude, and social influence are the independent variables.

Figure 1

Conceptual Framework

Adapted from Ghimire, 2017; Sarkodie & Yusif, 2015; Stroe & Iliescu, 2013

Based on the literature review, this study posits that income level, knowledge of life insurance, income protection, risk attitude, and social influence are significantly related to the demand for life insurance. Figure 1 shows the conceptual framework for this study. It was adapted from the conceptual framework developed by Ghimire (2017), Sarkodie and Yusif (2015), Stroe, and Iliescu (2013). The demand for life insurance is a dependent variable. Meanwhile, income level, knowledge of life insurance, income protection, risk attitude, and social influence are independent variables.

3. METHODOLOGY

3.1 Research Design

The objective of this study was to investigate factors that related to the demand for life insurance among “Generation Y” in Klang Valley, Malaysia. The quantitative research method was employed with an emphasis on objective measurements and numerical analysis. Both descriptive and inferential analyses were used to test the hypotheses and subsequently address the research questions. A cross-sectional study approach was implemented where the data were collected once at a particular time across the entire research area in Klang Valley, Malaysia.

3.2 Sampling Method

This study employed the Purposive Sampling Method whereby data was collected on a targeted population, i.e. “Generation Y” who lives in Klang Valley, Malaysia. This method was chosen as it aimed to delve into the key factors motivating life insurance purchase amongst “General Y” within the targeted research area. The online version of the questionnaire was distributed to 1,200 residents in the Klang Valley. However, only 425 of them responded, and only 320 of them were deemed usable. Referring to Krejcie and Morgan’s Table for Determining Sample Size (Krejcie & Morgan, 1970), this sample size is sufficient enough.

3.3 Research Instrument

In this study, a self-administered questionnaire which was adapted from Loon et al. (2019) was used as the main instrument to gather data. The questionnaire consists of three sections, namely Section A, Section B, and Section C with a total of 33 questions. The questionnaire was uploaded and distributed via Google Forms to the respondents. Section A, asked about demographic information of the respondents (i.e. gender, age group, monthly income, and educational level). Section B contains questions about the five independent variables in this study (i.e. income level, knowledge of life insurance, income protection, risk attitude, and social influence). Section C consists of questions that identified the level of demand for life insurance.

A pilot study for the draft questionnaire was carried out in order to examine its reliability and construct validity. The results of the pilot study revealed that the Cronbach’s alpha coefficients for all variables were relatively high: Demand for life insurance (0.873), income level (0.899), knowledge of life insurance (0.866), income protection (0.852), risk attitude (0.832), and social influence (0.868). However, three items that scored lesser than 0.70 were deleted to make the overall reading of Cronbach’s Alpha coefficients settle at 0.865 which showed a high degree of reliability. On the other hand, item analysis revealed that all the items from the questionnaires reached a significant level at 0.05. Furthermore, the results of the factor analysis also showed adequate construct validity.

3.4 Statistical Analysis

Before choosing a statistical analysis or test, the researcher addressed the issue of whether the data are parametric or not. In this context, all data in this study are parametric. Therefore, there were five types of analyses administrated in this study, namely, Descriptive Analysis, Independent Sample T-Test, One- way ANOVA, Pearson’s Correlation Analysis, and Multiple Linear Regression Analyses. Descriptive Analysis was carried out on the distribution of the demographic variables and to address research question 1: What is the level of demand for life insurance policy among “Generation Y” in Klang Valley, Malaysia? Independent Sample T-Test and One-way ANOVA tests were conducted to test the difference in the demand for life insurance policy among “Generation Y” in accordance with gender, age group, monthly income, and education level. Pearson’s Correlation was conducted to test hypothesis H1 to H5. It was further strengthened by Multiple Linear Regression Analyses that finally a model was developed as follows:

LINS_DEM = a + β1INCOME + β2KNOWLEDGE + β3PROTECT + β4RISK + β5INFLUENCE

Where a is a constant, LINS_DEM denotes the demand for life insurance, INCOME refers to the income level, KNOWLEDGE refers to the knowledge of life insurance, PROTECT is the income protection, RISK relates to risk attitude, INFLUENCE refers to social influence, and B1-5 are the coefficients to be tested.

4. RESULT AND ANALYSIS

4.1 Demographic Profile of the Respondents

Table 1 provides details of the demographics of the respondents. The factors investigated in this study were gender, age group, monthly income, education level, and insurance agency.

| Factor | Category | Frequency | Percentage |

| Gender | Male Female | 209 111 | 65.3% 34.7% |

| Age group | <19 years 19-29 years 30-39 years | 12 158 150 | 3.8% 49.4% 46.9% |

| Monthly income | <RM1000 RM1000 – RM2000 RM2001 – RM3000 RM3001 – RM4000 | 27 110 32 151 | 8.4% 34.4% 10.0% 47.2% |

| Education level | Diploma Bachelor Master Professional | 83 148 79 10 | 25.9% 46.3% 24.7% 3.1% |

| Insurance agency | Allianz Prudential Great Eastern AIA Kurnia Manulife | 69 14 71 155 8 3 | 21.6% 4.4% 22.2% 48.4% 2.5% 0.9% |

The results show that 209 or 65.3% and 111 or 34.7% are male and female respondents respectively. There are 12 or 3.8%, 158 or 49.4%, and 150 or 46.9% of the respondents aged below 19 years old, 20-29 years old, and 30-39 years old respectively. Most of the respondents (151, 47.2%) indicated they earned RM3001- RM4000 monthly. 34.4% (110) of them indicated their monthly income are RM1000-RM2000. Only 10% (32) and 8.4% (27) of them have a monthly income of RM2000-RM3000 and below RM1000 respectively. From the factor of education level, 83 respondents (25.9%) with diploma qualification, 148 respondents (46.3%) with bachelor degree qualification, 79 respondents (24.7%) with master degree qualification and only 10 respondents (3.1%) with professional qualification. It seems that most of the respondents had purchased life insurance from AIA (155, 48.4%). This is followed by Great Eastern (71, 22.2%) and Allianz (69, 21.6%). Only 4.4% (14), 2.5% (8), and 0.9% (3) of the respondents purchased life insurance from Prudential, Kurnia and Manulife respectively.

4.2 The Level of the Demand for Life Insurance among “Generation Y” in Klang Valley, Malaysia

Table 2 shows the mean and standard deviation for number of insurance policies hold by the respondents and their amount of annual premium paid.

| Demand of Life Insurance | Mean ( ) | StandardDeviation(SD) |

| Number of policies Amount of annual premium | 1.79 2421.30 | 0.72 243.25 |

In the term of the number of policies, the mean value is 1.79, which means each respondent holds 1.79 insurance policies. In this case, the number of insurance policies held by respondents is considered moderately high. In the term of the annual premium of respondents, the mean value is 2421.3, which means each respondent paying RM2421.3 for their annual premium. In this case, the amount of the annual premium is considered moderately high too. Therefore, it is summarised that the level of the demand for life insurance among “Generation Y” in Klang Valley, Malaysia is moderately important.

4.3 The Difference on the Demand for Life Insurance among “Generation Y” in Accor- dance with Gender, Age Group, Monthly Income and Education Level

Table 3 below shows the results of the Independent Samples T-Test of gender difference on the demand for life insurance.

| Gender | N | Mean () | SD | df | t | Sig. |

| Male | 209 | 4.1077 | .5927 | 318 | 2.434 | .015 |

| Female | 111 | 3.9257 | .7123 |

The results show us that there is a significant difference on the demand for life insurance among the “Generation Y” in Klang Valley (t = 2.434, df = 318, p < .05). The male respondents (= 4.1077, SD = .5927) showed higher demand for life insurance in comparison with the female respondents ( = 3.9257, SD = .7123). Table 4 shows the results of the One-Way ANOVA Test of age group difference on the demand for life insurance.

| SumofSquare | df | Mean Square | F | Sig. | |

| Between groups | 9.636 | 2 | 4.818 | 12.553 | .000 |

| Within groups Total | 121.667 131.303 | 317 319 | .384 |

It is clear that there is a significant difference in the demand for life insurance between age groups as determined by One-Way ANOVA [F (2, 317) = 12.553, p < .01]. A Tukey Post-Hoc Test revealed that the demand for life insurance is significantly higher for those aged 30-39 years old (4.143 ± 0.8 policies, p <.01) in comparison with those aged 19 – 29 years old (3.843 ± 0.5 policies, p < .01). However, there are no statistically significant differences between the <19 years old and 19 – 29 years old groups (p > .05).

Table 5 shows the results of the One-Way ANOVA Test of the monthly income difference in the demand for life insurance.

| SumofSquare | df | Mean Square | F | Sig. | |

| Between groups | 5.238 | 3 | 1.746 | 4.377 | .005 |

| Within groups Total | 126.065 131.303 | 316 319 | .399 |

The results show that there is a significant difference on the demand for life insurance between the four groups of monthly income as determined by One-Way ANOVA [F (3, 316) = 4.377, p < .01]. A Tukey Post- Hoc Test showed that the demand for life insurance is significantly higher for those who earned RM1000 – RM2000 monthly (3.943 ± 0.78 policies, p < .01) in comparison with those who earned below RM1000 monthly (3.543 ± 0.45 policies, p < .01). However, there is no statistically significant difference between the income group of below RM1000 and other two groups (p > .05).

Table 6 shows the results of the One-Way ANOVA Test of education level difference on the demand for life insurance.

| SumofSquare | df | Mean Square | F | Sig. | |

| Between groups | 6.319 | 3 | 2.106 | 5.325 | .001 |

| Within groups | 124.984 | 316 | .396 | ||

| Total | 131.303 | 319 |

From Table 6, it is clear that there is a significant difference on the demand for life insurance in accordance with the four groups of education level as determined by One-Way ANOVA [F (3, 316) = 5.325, p < .01]. A Tukey Post-Hoc Test showed that the demand for life insurance is significantly higher for those who obtained a Bachelor Degree (4.043 ± 0.68 policies, p < .01) in comparison with those who a Diploma (3.713 ± 0.40 policies, p < .01). However, there is no statistically significant difference on the demand for life insurance between Diploma holders and other two groups of education level (p > .05).

4.4 Hypothesis Testing

To measure the strength of the relationship between the five independent variables and the demand for life insurance, the Table of Correlation Value Interpretation developed by Bartlett, Kontrlik, and Hinggins (2001) is referred.

| Correlation Value (r) | Relationship Strength |

| ± 0.70 – 0.99 | Very Strong |

| ± 0.50 – 0.69 | Strong |

| ± 0.30 – 0.49 | Moderately strong |

| ± 0.10 – 0.29 | Weak |

| ± 0.01 – 0.09 | Very weak |

4.5 Relationship between Income Level, Knowledge of Life Insurance, Income Protection, Risk Attitude, Social Influence and the Demand for Life Insurance

Table 8 shows the results of the Pearson’s Correlation Analysis on income level, knowledge of life insurance, income protection, risk attitude, social influence, and the demand for life insurance.

| Variable | LINS_DEM | INCOME | KNOWLEDGE | PROTECT | RISK | INFLUENCE |

| LINS_DEM | - | |||||

| INCOME | .636* | - | ||||

| KNOWLEDGE | .641* | .121 | - | |||

| PROTECT | .593* | .451* | .521* | - | ||

| RISK INFLUENCE | .643* -.075 | .615* -.200 | .398* -.031 | .414* -.042 | - -.045 | - |

From Table 8, it is found that there is a significant, positive, and strong relationship between income level and the demand for life insurance (r = .636, n = 320, p < .01). The positive relationship shows that a higher come can increase the demand for life insurance and vice-versa. Therefore, H1: Income level is positively related to the demand for life insurance. The results are consistent with the conceptual link that those with higher income will have a higher demand for life insurance (Stroe & Iliescu, 2013; Beck & Webb, 2003; Yaari, 1965). The results also supported previous research findings (Loon et al. (2019), Ghimire (2017), Fukuchi (2016), Shahriari & Shahriari (2016), Sarkodie, and Yusif (2015), Mahdzan and Victorian (2013).

A significant, positive, and strong relationship also found between the knowledge of life insurance and the demand for life insurance (r = .641, n = 320, p < .01). The positive relationship shows that a higher level of knowledge in life insurance will result in a higher level of demand for life insurance and vice-versa. Therefore, H2 is supported. The results concur with the previous findings (Loon et al., 2019; Sarkodie & Yusif, 2015; Tennyson & Yang, 2014; Lee, 2012; Ioncica et al., 2012; Loke & Goh, 2012).

Similarly, there is a significant, positive, and strong relationship between income protection and demand for life insurance (r = .593, n = 320, p < .01). The positive relationship shows that high protection of expected income can increase demand for life insurance and vice versa. Therefore, H3 is supported. This result supported the findings from previous studies and the conceptual link between these variables (Loon et al., 2019; Ghimire, 2017; Mitra, 2017; Fukuchi, 2016; Mahdzan & Victorian, 2013; Arun et al., 2012; Loke & Goh, 2012).

Likewise, there is a significant, positive and strong relationship between risk attitude and the demand for life insurance (r = .643, n = 320, p < .01). The positive relationship shows that any increase in risk attitude will increase the demand for life insurance and vice versa. Hence, H4 is supported. This result supported the findings from previous studies (Loon et al., 2019; Fukuchi, 2016; Tennyson & Yang, 2014; Stroe & Iliescu, 2013; Ackah & Owusu, 2012).

Surprisingly that there isn’t any significant relationship between social influence and the demand for life insurance (r = -.075, n = 320, p > .05). Therefore, H5 is failed to be supported. The results somewhat contradict with the previous findings (Loon et al., 2019; Fukuchi, 2016; Stroe & Iliescu, 2013; Ackah & Owusu, 2012; Cai et al., 2011) and fail to support the conceptual link between the variables (Sarkodie & Yusif, 2015; Stroe & Iliescu, 2013).

In summary, as predicted income level, knowledge of life insurance, income protection, and risk attitude show a significant positive relationship with the demand for life insurance. However, this study found no significant relationship between social influence and the demand for life insurance.

4.6 Predictor Factors of the Demand for Life Insurance

Table 9 shows the results of the Multiple Regressions Analysis on the predictor factors of the demand for life insurance.

| Independent variable | r | Beta (β) | Sig. |

| INCOME | .636* | .515* | .000 |

| KNOWLEDGE | .641* | .592* | .000 |

| PROTECT | .593* | .491* | .000 |

| RISK | .643* | .597* | .000 |

| INFLUENCE | -.075 | -.012 | .583 |

| F = 14.142 R2 = .691 | Adjusted R2 = .683* |

a. Predictors: (Constant), income level, knowledge of life insurance, income protection, and risk attitude.

b. Dependent Variable: Demand for life insurance

From Table 9, it is learned that all the factors statistically significantly predict the demand for life insurance [F (5, 320) = 14.142, p < .01], except for social influence (p > .05). The combined influence of all the predictor factors explained 68.3% of the variance change in the demand for life insurance (R = .831, Adj. R2 = .683, p < .01). Moreover, risk attitude is found to be the best predictor factor of the demand for life insurance (β = .597, p < .01). Income level (β = .515, p < .01), knowledge of life insurance (β = .592, p < .01) and income protection (β = .491, p < .01) are also good predictor factors of the demand for life insurance. The results supported largely on the existing conceptual link of the demand for life insurance and previous researches (Loon et al., 2019; Ghimire, 2017; Sarkodie & Yusif, 2015; Redzuan, 2014; Mahdzan & Victorian, 2013; Stroe & Iliescu, 2013; Ackah & Owusu, 2012; Loke & Goh, 2012; Pliska & Yeh, 2007; Todd, 2004; Beck & Webb, 2003; Cleeton & Zellner, 1993; Burnett & Palmer, 1984; Yaari, 1965).

5. CONCLUSION AND IMPLICATIONS

The overall objective of this study was to examine the relationship between the five factors related to the demand for life insurance among the “Generation Y” in Klang, Malaysia. The descriptive statistics of this study show that there is a moderately important level of a number of insurance policies purchased and the value of the annual premium paid among the “Generation Y” in Klang Valley. T-Test shows a significant difference in the demand for life insurance in accordance with gender. ANOVA Analysis shows that there is a significant difference in the demand for life insurance between age groups of 19-29 and 30-39, monthly income of Less than RM1000 and RM1000 — RM2000, education level of Diploma and Bachelor. The inferential statistics of this study show that there is a significant, strong, and positive relationship between income level, knowledge of life insurance, income protection, and risk attitude and the demand for life insurance. Interestingly, this study found no significant relationship between social influence and the demand for life insurance. In addition, Regression Analysis reveals that risk attitude is the most dominant predictor of the demand for life insurance. Income level, knowledge of life insurance, and income protection are also found to be good predictor factors of the demand for life insurance.

The results of this research have implications not only for the insurance agencies, policyholders but also for the entire population of Malaysia, especially the “Generation Y”. The findings show that risk attitude, income level, knowledge of life insurance, and income protection dominate the demand for life insurance emphasize the need for those who are directly involved in this industry to initiate a greater responsibility in promoting the importance and benefits of life insurance, besides putting in higher awareness in cultivating knowledge of life insurance among the “Generation Y” or perhaps even in the broader community groups. These moves will slowly but steadily cultivate and enhance a positive culture and/or attitude toward life insurance.

Drawing on the four factors as discussed above, gives the following expectation if the demand for life insurance among “Generation Y” is to be improved. First and foremost, from the perspective of risk attitude, in which if an insurance agency could come out with convincing policies that offer attractive protection to the policyholder in the event of the occurrence of any negative event caused by measurable loss, injury, liability, external or internal weaknesses. How far could the insurance agency go in instilling positive values of life insurance into the community? A high-risk attitude will have a significant impact on the demand for life insurance.

From the perspective of income level, marketers of life insurance would normally focus on efforts on individuals who have higher income, since these are the group of people who can afford to purchase life insurance. However, the low- income earners should not be neglected as these individuals are the ones who most probably are the least protected. In the matter of fact, insurance companies should emphasize the importance of life insurance to this group of individuals and promote term life insurance which is relatively cheaper as opposed to whole life insurance or investment-linked policies. With a lower insurance premium, low-i income earners would be able to afford similar protection and investment in life insurance. Ultimately, the demand for life insurance in Malaysia will be increased.

Insurance companies and agents should also play a more active role in cultivating and enhancing knowledge of life insurance and its benefits among the “Generation Y” in Malaysia. The knowledge of income protection, bequest motive, and other aspects of financial planning should be constantly instilled into the “Generation Y”. Plausibly, the findings of this study suggest that Malaysians perceive life insurance as a secured and long-term measure of accumulating wealth due to the strong and prudent financial record of the major life insurance companies in Malaysia. Therefore, life insurance companies should take note of these results and repackage their insurance policies with more attractive elements of return in investment and/or savings. Life insurance companies should also highlight the benefits in income protection, bequest, life cycle, and precautionary aspects of life insurance to make their products and services more attractive and visible to the entire society.

This study is a preliminary study investigating factors related to the demand for life insurance with the focus on the “Generation Y” in Klang Valley, Malaysia. Therefore, the results may not be able to generalize to the entire Malaysian population. Hence, there is ample room for future research to be carried out in the broader area and society of Malaysia, especially those underdeveloped, rural areas, where life insurance penetration can be expected to be low. Such research efforts would allow greater generalizations to be made and facilitate the efforts in increasing the demand for life insurance throughout the nation. Other aspects of life insurance demand should also be considered for further studies, inclusive but not limited to, behavioral aspects of financial decision-making, such as risk aversion and one’s willingness to invest in life insurance.

AUTHOR

Jee Fenn Chung. (PhD). Research focus: Quantitative Research Methodology, Educational Management, Organisational Behaviour, and Strategic Human Resource Management. Expertise: Quantitative Research Methodology (rated world 7 th in Google Scholar) and Organisational Behaviour (rated world 22 th In Google Scholar).

CONFLICT OF INTEREST

No potential conflict of interest is reported by the author(s).

Funding

No financial assistance from parties outside this article.

Acknowledgments

N/A

REFERENCES

Ackah, C., & Owusu, A. (2012). Assessing the knowledge of and attitude towards insurance in Ghana [Paper presentation]. International Research Conference on Microinsurance, Twente.

Arun, T.G., Bendig, M., & Arun, S. (2012). Bequest motives and determinants of micro life insurance in Sri Lanka. World Development, 40(8), 1700-1711. https://doi.org/10.1016/j.worlddev.2012.04.010

Bank Negara Malaysia. (2018, July 12). Governor’s remarks at the Malaysian Insurance Institute (MII) Summit.Innovation in a Disruptive Era. https://www.bnm.gov.my/index.php?ch=en_speech&pg=en_speech&ac=808

Bartlett, J. E., Kontrlik, J.W., & Hinggins, C.C. (2001). Organizational research: Determining appropriate sample size in survey research. Information Technology, Learning, and Performance Journal, 19(1), 43-50.

Beck, T., & Webb, I. (2003). Economic, demographic, and institutional determinants of life insurance consumption across countries. The World Bank Economic Review, 17(1),51-88. https://doi.org/10.1093/wber/lhg011

Bernheim, B.D. (1991). How Strong Are Bequest Motives? Evidence Based on Estimates of the Demand for Life Insurance and Annuities. Journal of Political Economy, 99(5), 899-927. http://dx.doi.org/10.1086/261783

Browne, M.J., & Kim, K. (1993). An international analysis of life insurance demand. The Journal of Risk & Insurance, 60(4), 616-634. https://doi.org/10.2307/253382

Burnett, J.B., & Palmer, B.A. (1984). Examining life insurance ownership through demographic and psychographic characteristics. Journal of Risk and Insurance, 51(3), 453-467. https://doi.org/10.2307/252479

Cai, J., De Janvry, A., & Sadoulet, E. (2011). Social networks and insurance take up: Evidence from a randomized experiment in China. International Labour Organization, Microinsurance Innovation Facility Research Paper. http://www.impactinsurance.org/publications/rp8

Cleeton, D.L., & Zellner, B.B. (1993). Income, risk aversion, and the demand for insurance. Southern Economic Journal, 60, 146-156. https://doi.org/10.2307/1059939

Dercon, S., Gunning, J.W., & Zeitlin, A. (2011). The demand for insurance under limited credibility: Evidence from Kenya [Paper presentation]. The International Development Conference, DIAL, Paris.

Fischer, S. (1973). A life cycle model of life insurance purchases. International Economic Review, 14(1), 132–152. https://dioi.org/10.2307/2526049

Fukuchi, K. (2016). An empirical study of the demand for modern individual life insurance in Japan. “Hokengakuzasshi”. Journal of Insurance Science, 633, 1-31. https://doi.org/10.5609/jsis.2016.633_1

Ghimire, R. (2017). Perception of uninsured person towards the life insurance policy. Journal of Management and Development Economics, 6(1), 111-123. http://dx.doi.org/10.2139/ssrn.3042662

Giné X., Townsend, R., & Vickery, J. (2008). Patterns of rainfall insurance participation in rural India. The World Bank Economic Review, 22(3), 539-566. https://doi.org/10.1093/wber/lhn015

Hair, J., Bush, R., & Ortinau, D. (2006). Marketing Research within a Changing Environment, (3rd ed.). McGraw Hill.

Hwang, T., & Greenford B. (2005). A cross-section analysis of the determinants of life insurance consumption in mainland China, Hong Kong, and Taiwan. Risk Management and Insurance Review, 8(1), 103-125. https://doi.org/10.1111/j.1540-6296.2005.00051.x

Ioncica, M., Petrescu, E.C., Ioncica, D., & Constantinescu, M. (2012). The role of education on consumer behavior on the insurance market. Procedia Social and Behavioral Sciences, 46, 4154-4158. https://doi.org/10.1016/j.sbspro.2012.06.217

Krejcie, R.V., & Morgan, D.W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30, 607-610.

Lee, Y.W. (2012). Asymmetric information and the demand for private health insurance in Korea. Economics Letters, 116(3), 284-287. https://doi.org/10.1016/j.econlet.2012.03.021

Lewis, F. (1989). Dependents and the demand for life insurance. American Economic Review, 79(3), 452–466. https://ideas.repec.org/a/aea/aecrev/v79y1989i3p452-67.html

Life Insurance Association Malaysia. (2020, March 16). LIAM: Life insurance records double digit growth in 2019. http://www.liam.org.my/news/?lg=en&ct=3

Loke, Y.J., & Goh, Y.Y. (2012). Purchase decision of life insurance policies among Malaysians. International Journal of Social and Humanity, 2(5), 415-420. http://www.ijssh.org/show-32-365-1.html

Loon, A.C., Tee, K.H., & Santhanarajan, M.E. (2019). Factors influencing life insurance consumption in Malaysia. In G.Y. Xiao, et al. (Eds.), EBIMCS ‘19: The 2019 2nd International Conference on E-Business, Information Management and Computer Science (pp. 1–5). Association for Computing Machinery. https://doi.org/10.1145/3377817.3377825

Mahdzan, N.S., & Victorian, S.M.P. (2013). The determinants of life insurance demand: A focus on saving motives and financial literacy. Asian Social Science, 9(5), 274-284. http://dx.doi.org/10.5539/ass.v9n5p274

Malaysian Takaful Association. (2019). Annual Report 2019. https://www.malaysiantakaful.com.my/sites/default/files/2020-04/mta_ar2019.pdf

Mitra, A. (2017). Influencers of life insurance investments: Empirical evidence from Europe, Australasian Accounting, Business and Finance Journal, 11(3), 87-102. https://shorturl.at/lqrQS

Ng, M.S. (2018, October 15). Insurance sector’s consolidation is not easy. The Malaysian Reserve. https://shorturl.at/efxB2

Pliska, S., & Ye, J. (2007). Optimal life insurance purchase and consumption/investment under uncertain lifetime. Journal of Banking & Finance, 31(5), 1307-1319. https://doi.org/10.1016/j.jbankfin.2006.10.015

Redzuan, H. (2014). Analysis of the demand for life insurance and family takaful. Proceedings of the Australian Academy of Business and Social Sciences Conference in partnership with the Journal of Developing Areas (pp.1–16). https://pdfs.semanticscholar.org/4919/70d5aed75daedf198d2d6b14cc8a2da8997b.pdf

Sarkodie, E.E., & Yusif, H.M. (2015). Determinants of life insurance demand, consumer perspective - A case study of Ayeduase-Kumasi Community, Ghana. Business and Economics Journal, 6(170), 1-4. https://shorturl.at/f0238

Shahriari, S., & Shahriari, M. (2016). The effect of social and demographic and economic factors on life insurance demand. International Journal of Management and Social Science Research Review, 1(28), 200-207. https://shorturl.at/ehW29

Soo, H. H. (1996). Life insurance and economic growth: Theoretical and empirical investigation. [Doctoral Thesis, University of Nebraska] https://digitalcommons.unl.edu/dissertations/AAI9712527

Stroe, M.A., & Iliescu, I.M. (2013). Attitudes and perception in consumers’ insurance decision. Global Economic Observer, 1(2), 112-120. https://econpapers.repec.org/article/ntuntugeo/vol1-iss2-13-112.htm

Tennyson, S., & Yang, H.K. (2014). The role of life experience in long term care insurance decision. Journal of Economic Psychology, 42(1), 175-188. https://doi.org/10.1016/j.joep.2014.04.002

The Star. (2018). Trends in and outlook for the Malaysian assurance industry. The Star Online. https://shorturl.at/yPW47

Todd, D. (2004). Integrative life insurance need analysis. Journal of Society of Financial Service Professionals. 58(2), 57

Wang, H.H., & Rosenman, R. (2007). Perceived need and actual demand for health insurance among rural Chinese residents. China Economic Review, 18(4), 373-388. https://doi.org/10.1016/j.chieco.2006.11.002

Yaari, M.E. (1965). Uncertain lifetime, life insurance and the Theory of the Consumer. The Review of Economic Studies, 32(2), 137-150. https://doi.org/10.2307/2296058

Yuengert, A.M. (1993). The measurement of efficiency in life insurance: Estimates of a Mixed Normal-Gamma Error Model. Journal of Banking and Finance, 17(2-3), 483-496. https://doi.org/10.1016/0378-4266(93)90047-H

Información adicional

Contenido: ABSTRACT 302 RESUMEN 302 1. INTRODUCTION 303 1.1 Background of the Study 303 1.2 The Objective of the Study 303 1.3 Research Questions 303 1.4 Hypotheses 304 2. LITERATURE REVIEW 304 2.1 The Demand for Life Insurance 304 2.2 Income Level and the Demand for Life Insurance 304 2.3 Knowledge of Life Insurance and the Demand for Life Insurance 304 2.4 Income Protection and the Demand for Life Insurance 305 2.5 Risk Attitude and Demand for Life Insurance 305 2.6 Social Influence and the Demand for Life Insurance 305 2.7 Conceptual Framework 306 3. METHODOLOGY 306 3.1 Research Design306 3.2 Sampling Method 306 3.3 Research Instrument 306 3.4 Statistical Analysis 307 4. RESULT AND ANALYSIS 307 4.1 Demographic Profile of the Respondents 307 4.2 The Level of the Demand for Life Insurance among “Generation Y” in Klang Valley, Malaysia 308 4.3 The Difference on the Demand for Life Insurance among “Generation Y” in Accordance with Gender, Age Group, Monthly Income and Education Level 308 4.4 Hypothesis Testing 309 4.5 Relationship between Income Level, Knowledge of Life Insurance, Income Protection, Risk Attitude, Social Influence and the Demand for Life Insurance 310 5. CONCLUSION AND IMPLICATIONS 311 REFERENCES 313 AUTHOR 314 CONFLICT OF INTEREST 314

sin nombre: Chung, J. F. (2020). The demand for life insurance: a quantitative study among “generation y” in the Klang Valley, Malaysia. Religación. Revista de Ciencias Sociales y Humanidades, 5(25), 302-314. https://doi.org/10.46652/rgn.v5i25.662