GENERAL

Financial performance analysis of Zakat management organization in Indonesia

Análisis del desempeño financiero de la organización de gestión de Zakat en Indonesia

Financial performance analysis of Zakat management organization in Indonesia

RELIGACIÓN. Revista de Ciencias Sociales y Humanidades, vol. 4, núm. 15, Esp., pp. 103-107, 2019

Centro de Investigaciones en Ciencias Sociales y Humanidades

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-SinDerivar 4.0 Internacional.

Recepción: 15 Enero 2019

Aprobación: 04 Mayo 2019

Resumen: Este estudio tuvo como objetivo analizar el desempeño financiero de las organizaciones de gestión de zakat. La muestra de la aplicación de medición de informes de Internet es el sitio web de la Organización de Gestión de Zakat registrado en la Dirección General de Regulación Fiscal No. PER-15 / PJ / 2012. Esta investigación utiliza un muestreo intencional que puede acceder al informe financiero por completo. El método de análisis de investigación utilizado es un análisis de contenido y medición del desempeño de la parte principal del desempeño financiero emitido por Indonesia Magnificence of Zakat (IMZ) en Indonesia Zakat Development Report (IZDR) 2011. La evaluación del desempeño financiero, en general, se considera Bastante bien.

Palabras clave: Zakat Management Organization, estados financieros y desempeño financiero.

Abstract: This study aimed to analyze financial performance of zakat management organizations. Sample in measurement of internet reporting application is Zakat Management Organization website registered in Directorate General of Taxation Regulation No. PER-15 / PJ / 2012. This research use purposive sampling that can be access the financial report completely. The method of research analysis used is content analysis and performance measurement of prime part of financial performance issued by Indonesia Magnificence of Zakat (IMZ) in Indonesia Zakat Development Report (IZDR) 2011. The assessment of financial performance in general is considered quite good.

Keywords: Zakat Management Organization, financial statement, and financial performance.

INTRODUCTION

One of the factors of poverty in particular in developing countries including Indonesia is the exploitation of colonizers, economic dualism, financial dualism, inequality, low human resource productivity, inefficiency and market imperfection causing uneven distribution of wealth and incomes (Bank Indonesia and UII, 2016). To overcome this, it is necessary to optimize the role of zakat as an instrument of community empowerment.

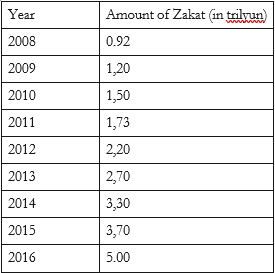

According to calculations performed by BAZNAS and IPB, based on the 2010 GDP potential of zakat in Indonesia amounted to Rp217 Trillion. With the extrapolation method, the potential of zakat in 2015 amounts to Rp280 trillion and the realization is estimated at Rp 4 trillion or less than 1.4% of its potential (Hartono, Directorate General of Taxes, 2016). Meanwhile, according to data obtained from BAZNAS, the realization of ZIS funding nationally 2008 to 2015 is shown in the following table.

Table 1.

Collection of Zakat in Indonesia

Sources: (Pusat Kajian Strategis Badan Amil Zakat Nasional, 2016)

This enormous potential of zakat can be a source of funds for society and government. However, the huge difference between the potential and realization implies a problem in the management of zakat (Hartono, Directorate General of Taxes, 2016). These problems are like; first, zakat is only seen as a religious obligation. Secondly, the increased awareness of Muslims in paying zakat is not accompanied by comprehensive planned collection and distribution. Third, the formal legal supporters are less proactive in looking at the potential of zakat as well as the application of religious obedience to Muslims (Mughni, 2015).

To optimize the role of zakat, Islam encourages the growth of social institutions to help each other in difficult times (Yuniartati, 2012), one of them is the Organization of Zakat Management (ZI). ZI is a non-profit organization that aims to help Muslims channel zakat, infaq, shodaqoh to the rightful. However, in such management sometimes fund managers are not the people or institutions that are really known by the funders, thus raising the need for accountability and transparency in the management of zakat funds (Ari Kristin, 2011), it is very important to do because, wrongly one factor causing the non-achievement of optimal zakah acceptance from muzaki is the low level of public trust in ZI (Septiarini, 2011), this can be seen in research conducted by Public Interest Research and Advocacy Center (PIRAC) in 2007 in 11 cities (59%) of respondents distributed zakat through amil mosque around the house, or directly to the eligible, and through BAZ and LAZ about 6% and 1.2% (respectively) PIRAC, 2007). In addition, based on a survey conducted by Dompet Dhuafa Republika in 2009 regarding public perception related to zakat mal and zalcat management for jabodetabek region obtained the result that, muzaki who membesarkan zakatnya directly to mustahiq equal to 33,2%, mosque equal to 18,3% BAZ and LAZ are 2.1%, scholars are 2.1%, and social foundations are 2.1%, and the rest do not answer (Nurul huda, 2015). The low public trust in ZI is also caused by the many cases of irregularities perpetrated by irresponsible amil, such as the cases as decribed by Rini (2016).

To increase public trust, transparency and accountability of ZI operational activities need to be undertaken. Non-profit organizations have various weaknesses related to accountability due to the lack of information to the public. However, along with the advancement of technological progress, ZI can utilize the internet as a medium of information to the public, by building website (Gatot Soepriyanto, 2011) and implementing internet reporting (Rini, 2016).

Performance measurement of ZI is urgent, especially with the number of ZI in Indonesia that is around 38.013 Organization (Nikmatuniah, 2015). Based on the description, this research is made to increase public trust to ZI, by measuring ZI accountability level through internet reporting and performance appraisal, especially on financial performance.

RESEARCH METHODS

This research is descriptive qualitative research. This study will discuss the level of ZI accountability through the implementation of internet reporting and financial performance assessment. The method of determining the sample in this research is judgment sampling with ZI criteria registered in the regulation of Director General of Taxes No. PER-15 / PJ / 2012. There are 19 ZI that mention in the regulation. For the financial performance measurement object used is the financial statements of ZI who have made the preparation of financial statements Sharia Financial Accounting Standards 101 concerning the presentation of financial statements, the prepared reports shall consist of reports of changes in funds. The data used in this research is secondary data. The source of data in this study comes from every ZI website. Observations of the website were conducted during March 2017.

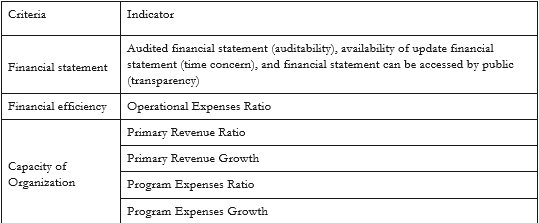

In the assessment of financial performance, researchers used measurements based on IZDR 2011 by IMZ. The measurement of financial performance is divided into three assessment criteria. Here are the three measurement criteria used. The final result of the ZI financial performance assessment is the sum of all values obtained by ZI. Furthermore, the result of that value is converted into the rank set in IZDR 2011.

Tabel 3.

Indicator of Financial Performance Assesment for Zakat Institution

Source: IMZ

RESULT AND DISCUSSION

Analysis of Financial Performance Assessment of ZI

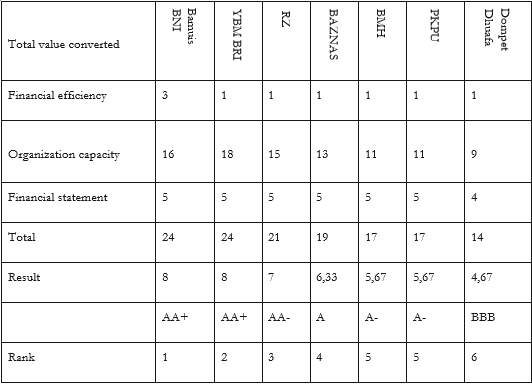

This study discusses the assessment of financial performance against 7 ZI, namely: BAZNAS, BMH, YBM BRI, BNI BNI, RZ, PKPU and DD. Based on the results of the assessment of financial efficiency, it can be concluded that most of the ZI got a bad assessment, except LAZ Bamuis BNI who got a value of 3 or enough. The poor rating is due to the high operational cost of each ZI when compared to total expenditure. ZI should strive to minimize operational expenditure of up to less than 5%.

Assessment of organizational capacity is measured through four criteria. The results of the financial performance measurement of this organizational capacity component as a whole are summed up quite well.

Furthermore, assessment of financial performance in terms of financial statements then most of the ZI got a very good assessment. This is due to high ZI awareness of accountability and transparency in reporting management activities to the community through the preparation of financial statements. However, not all ZIs have fully compiled the components of financial statements in accordance with SFAS 101. c. Criteria for valuation of financial statements.

Based on the assessment of financial performance in terms of financial statements then most of the ZI got a very good assessment. This is due to high ZI awareness of accountability and transparency in reporting management activities to the community through the preparation of financial statements. However, not all ZIs have fully compiled the components of financial statements in accordance with SFAS 101.

The final result of the ZI financial performance assessment is the sum of all values obtained by ZI. The results of these values are then converted into the ratings set out in IZDR 2011. This ranking can be seen below

Table 4.

Value of financial performance of ZI

Explanation: 5: excellent, 4: good, 3: Fair, 2: Less, 1: poor

Source: Data processedConclusion

Based on the measurement of financial performance appraisal conducted on seven ZI, it can be concluded in general, ZI financial performance is considered good enough. The best ranking was obtained by BNI BNI, YBM BRI was ranked second. Then, in the third rank achieved by the RZ, then the fourth ranking achieved by BAZNAS. While the fifth ranked achieved by BMH and PKPU. Last ranked sixth was achieved by Dompet Dhuafa Republika (DDR).

Suggestion

Future research is expected to expand the scope of the research by measuring the performance of sharia compliance, legality, and institutional, management performance, performance of economic empowerment and performance of social legitimacy. It aims to make the results of the research produced more comprehensive and reliable.

REFERENCIAS

Ari Kristin, U. K. (2011). Penerapan Akuntansi Zakat pada Lembaga Amil Zakat. VALUE ADDED, Vol. 7 , No.2, 72.

Badan Pusat Statistik. (2016). Number and Percentage of Poor People,Poverty Line, Poverty Gap Index, Poverty Severity Index by Province,. Jakarta: BPS.

Badan Pusat Statistik. (2017, Mei 1). Persentase Penduduk Miskin Maret 2015 Mencapai 11,22 persen. Diambil kembali dari Badan Pusat Statistik: http://www.bps.go.id/

Bank Indonesia dan Universitas Islam Indonesia. (2016). Pengelolaan Zakat yang Efektif: Konsep dan Praktik di Berbagai Negara. Jakarta: Departemen Ekonomi dan Keuangan Syariah Bank Indonesia.

Gatot Soepriyanto, R. A. (2011). Evaluasi Pengungkapan Laporan Keuangan Daerah di Situs Internet: Studi Pada Pemerintah Daerah Indonesia. Binus Business Review Vol. 2 No. 1, 192-201.

Indonesia Magnificence of Zakat. (2011). Indonesia Zakat and Development Report 2011: Kajian Empiris Peran Zakat dalam Pengentasan Kemiskinan. Ciputat: Indonesia Magnificence of Zakat.

Laela, S. F. (2010). Analisis Faktor-Faktor Yang Mempengaruhi Kinerja Organisasi Pengelola Zakat. TAZKIA Islamic Finance & Business Review, 126.

Lili Bariadi, M. Z. (2005). Zakat dan Wirausaha. Jakarta: Centre For Entrepreneurship Development.

Miftah, A. A. (2008). Pembaharuan Zakat Untuk Pengentasan Kemiskinan di Indonesia. Innovatio Vol VII No 14, 423.

Mughni, L. (2015, September selasa). Permasalahan Zakat di Indonesia. Diambil kembali dari Al Ittihad darussaadah: http://www.darussaadah.or.id/

Nikmatuniah, M. (2015). Akuntabilitas Laporan Keuangan Lembaga Amil Zakat di Kota Semarang. Mimbar, 485-486.

Nurul huda, N. Y. (2015). Zakat Perspektif Mikro-Makro: Pendekatan Riset. Jakarta: Prenadamedia Group.

PIRAC. (2007). Meningkat, Kesadaran dan Kapasitas Masyarakat dalam Berzakat. Jakarta: PIRAC.

Prasetyoningrum, A. K. (2015). Pendekata Balance Scorecard Pada Lembaga Amil Zakat di Masjid Agung Jawa Tengah. Economica Jurnal Pemikiran dan Penelitian Ekonomi Islam, 9-10.

Puji Lestari, U. P. (2015). Identifikasi Faktor Organisasional dalam Pengembangan E-Governance pada organisasi Pengelola Zakat. Mimbar Vol 31 Nomor 1, 224.

Pusat Kajian Strategis Badan Amil Zakat Nasional. (2016). 2017 Outlook Zakat Indonesia. Jakarta: Pusat Kajian Strategis Badan Amil Zakat Nasional.

Rini. (2016). Penerapan Internet Financial Reporting untuk Mendukung Akuntabilitas pada Organisasi Pengelola Zakat di Indonesia. Jurnal Akuntansi Multiparadigma Vol 7 No 2, 156-323.

Septiarini, D. F. (2011). Pengaruh Transparansi dan Akuntabilitas Terhadap Pengumpulan Dana Zakat, Infaq dan Shodaqoh pada LAZ di Surabaya. Akrual Jurnal Akuntansi, 177-180.

Shamharir Abidin, R. A. (2014). Evaluating Corporate Reporting on the Internet: The Case of Zakat Institutions in Malaysia. Jurnal Pengurusan 42, 19 - 29.

Sucipto, A. (2011, Maret 16). Membangun Transparansi dan Akuntabilitas Lembaga Pengelola Zakat. Diambil kembali dari El Zawa Pusat kajian zakat dan Wakaf UIN MALIKI Malang: http://elzawa.uin-malang. ac.id/membangun-transparansi-dan-akuntabilitas-lembaga-pengelola-zakat/#more-274

Yuniartati, L. A. (2012). Akuntabilitas Lembaga Pengelola Zakat di Kabupaten Jember. Conference In Business Accounting and Management, 1194.