SUR-SUR

Scraping the recurrent findings: a case study of Yogyakarta city government, Indonesia

Detrás de los hallazgos recurrentes: un estudio de caso del gobierno de la ciudad de Yogyakarta, Indonesia

Scraping the recurrent findings: a case study of Yogyakarta city government, Indonesia

RELIGACIÓN. Revista de Ciencias Sociales y Humanidades, vol. 4, núm. 15, Esp., pp. 290-297, 2019

Centro de Investigaciones en Ciencias Sociales y Humanidades

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-SinDerivar 4.0 Internacional.

Recepción: 18 Enero 2019

Aprobación: 12 Mayo 2019

Abstract: A great difference between a private sector audit and a public sector audit is between the promotion of audit opinions and the prevention of recurrent findings. In this study, a recurrent finding will be investigated deeply in the case of Yogyakarta City. The scope of this study will be delivered in a range of the implementation of the follow-up of the Audit Board audit results in the Government of Yogyakarta City from 2010 to 2015. So, the focus of this study is related to the occurrence of recurrent findings in the fiscal year 2010 to 2015. By the case study approach, a learning process in this study will be raised in the efforts that have been implemented by the Yogyakarta City Government for the prevention of recurrent findings.

Keywords: Follow-up of the Audit Board audit results, recurrent findings, local government financial statement.

Resumen: Una gran diferencia entre una auditoría del sector privado y una auditoría del sector público es entre la promoción de opiniones de auditoría y la prevención de hallazgos recurrentes. En este estudio, un hallazgo recurrente será investigado profundamente en el caso de la ciudad de Yogyakarta. El alcance de este estudio se entregará en una gama de la implementación del seguimiento de los resultados de la auditoría de la Junta de Auditoría en el Gobierno de la ciudad de Yogyakarta de 2010 a 2015. Por lo tanto, el enfoque de este estudio está relacionado con la aparición de recurrentes hallazgos en el año fiscal 2010 a 2015. Por el enfoque del estudio de caso, se levantará un proceso de aprendizaje en este estudio en los esfuerzos que ha implementado el gobierno de la ciudad de Yogyakarta para prevenir los hallazgos recurrentes.

Palabras clave: Seguimiento de los resultados de auditoría de la Junta de Auditoría, hallazgos recurrentes, estado financiero del gobierno local.

Introduction

Legislation regulates that examination results and follow-up is the final process of audit. The examiner’s task ends when preparing the Examination Result Report (LHP) upon completion of the examination and issuing an opinion. Opinion development to be better over Local Government Financial Statements (LKPD) from year to year shows increasing. Yogyakarta City Government just succeeded obtaining opinion of WTP in fiscal year of 2015. Since 2009 to 2014, Yogyakarta City Government was only able to achieve opinion of WTP with the explanatory paragraph. The statement of Head of the Audit Board of Republic of Indonesia in DIY was mentioned that several explanatory paragraphs need to be noted and the explanations on LHP almost the same for each year (Antara News Yogyakarta 2014).

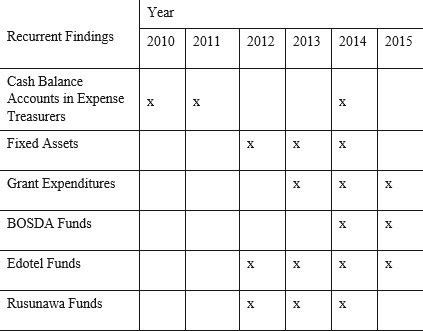

The findings of Audit Board will be useful if followed up by repairing the system so it will reduce the recurring (Akbar, 2013). The problems of recurrent findings become the problems that also face by Yogyakarta City Government. Table 1.1 shows a number of accounts in financial statements that show as recurrent findings in 2010 to 2015. Examiner should consider the previous examination results also the follow-up to the significant recommendation and related to the objectives of on-going examination (SPKN, 2007).

Table 1.

Classification of Findings in Examination Result Report of Audit Board of Yogyakarta City Government in 2010 to 2015

Source: Processed from LHP Yogyakarta City in 2010 to 2015

Effectiveness of Audit Board examination will be achieved if the entities examined implement the follow-up over their examination result report (BPK RI 2015). Results of findings and recommendations should be able to be used as instrument to repair the management and responsibility of all the funds’ users of Regional Budget (Ahmad, 2016).

Follow-up is the answer generated from identification and documentation of auditee progress in implementing the audit recommendations (Rai, 2011). According to legislation, period of sixty days after examination result report is received, become the deadline of follow-up. Based on the meeting of data update of Audit Board examination results follow-up in 2016, the follow-up completion of Yogyakarta City Government cumulatively from fiscal year of 2003 to 2015 in 75% (Inspektorat 2016). The Inspectorate also delivers as much as 166 items of recommendation (86,91%) have completed the followed up from total of 191 recommendations in 2010 to 2014. This result shows conformity with the Audit Board target in 2016. The Audit Board targeted the figure of 75% of state institution compliance that manage the finance from public property taxes no later than in 2020 (BPK 2016).

Examined entity management responsibilities are to follow-up the recommendations as well as create and maintain a process to monitor follow-up status over the intended recommendation (SPKN, 2007). This recommendation completion is expected to be able to minimize the effect of deviation in management and financial responsibility (Rai, 2011).

Related to the facts above, the study of the causes of recurrent findings in the Government of Yogyakarta City in fiscal year of 2010 to 2015. So that efforts that have been implemented by the Government of Yogyakarta City in following up the findings can be evaluated objectively. In this case, the problem of findings on recurrent findings can be solved.

The Follow-Up of Examination Findings

In order to improve the effectiveness and impact of the audit report, a review of the effectiveness of recommendations and may be undertaken by the examined entity (Bastian 2014) can be implemented in the implementation of follow-up, monitoring of follow-up executions, and reporting on follow-up results.

According to Rai (2011), an action plan implemented by auditee is the basis for follow-up audit findings. Formal form is the Letter of Regional Head on the preparation of follow-up plan.

An action plan will open up opportunities for grouping follow-up results, namely: completion; in the process; has not been followed-up; and cannot be followed-up. The realization will be reported in a resume that describes the legal basis of the examination, information on follow-up findings based on development status; and the need for subsequent monitoring.

According to Tugiman (1997) in Bastian (2014), the follow-up examination findings are generated from a comparative process between “what should be” and “what turns out to be”. In this case, follow-up findings may be specified on conditions; criteria; effect; and cause. Clearly, recurrent findings are a result of follow-up phase findings.

Follow-up completion requires the role of several parties to implement the recommendations and audit objectives. The role of the auditee remains the main one in the implementation of the follow-up. Several case study researches address the role of auditee in issues related to audit follow-up programs. The audit follow-up findings based on the Alkins (2012) study, affect the auditee in adopting audit recommendations. In the case of follow-up examinations at the Roslyn School District (Hufner, 2010), the role of inspector is the factor of the ordering or audit findings management.

In different cases, follow-up findings on the Environmental Impact Assessment (EIA) are strongly influenced by project uncertainty factor. Meanwhile, Nobel and Storey (2004) and Ross (2003) research based on the case in Ekati Diamond Mine (BHP Billiton) the Northwest Territories, Canada confirmed the role of impact estimates, and the effectiveness of the policy on recommendations of the findings led to recurrent findings.

Kusuma’s research (2014) on the role of Inspectorate and regional government in recurrent findings indicates the ineffectiveness factor of findings handling and factors of internal government control system. Recurrent findings will occur if coordination is not going well, there is no operational standard in supervision, and there is no sanction for institutions with recurrent findings.

Ahmad’s research (2016) is more highlighting the commitment of regional heads in handling recurrent findings. The derivation of the commitment factor of regional heads is the mutation policy variable, quality of human resources the variable, the variable of the low compliance with the legislation, and the complicated regulatory variable. This is in line with the results of research by Lasan (2016) in Mimika Regency.

Hartanto’s research (2015) highlights the aspects of experience and communication in handling recurrent findings. Leadership type and the length period of regional leadership in regional government become the main variables on the occurrence of recurrent findings.

A large understanding on some previous researches and reports has been delivered into a significance grounded study in a recurrent finding phenomena in a public sector field. In this case, a case method approach will be promoted for investigating many empirical data and facts in a form of documents and interview transcripts Through a reduction stage, some early analytical findings are explored into some sharp conclusions. These study process are designed for answering the study objectives. As a result, some analysis on grounded data can be done sharply.

Recurrent Findings in Yogyakarta City

Given the importance of handling recurrent findings, the Yogyakarta city government wants a deep understanding of the causes of recurring findings, follow-up efforts that have been implemented by the Yogyakarta City Government, and solutions to follow-up on findings and recommendations to avoid recurrent findings.

Based on the results of semi-structured interviews to informants, ie auditees and follow-up teams in the Yogyakarta City Government from 2010 to 2015; and reinforced by review of Audit Board’s audit reports, follow-up procedures, monitoring follow-up monitoring matrix of examination results, IHPS, legislation relating to findings and follow-up of Audit Board’s recommendations; hence, recurrent findings in the Yogyakarta city government have an opportunity to find a pattern of scraping the recurrent findings.

The results of analysis in the form of procedures or SOPs for the handling of recurrent findings will involve the auditee and follow-up teams. So that the weakness in the application of the procedure can be minimized from the time of designing.

Analysis of recurrent findings in Yogyakarta City Government

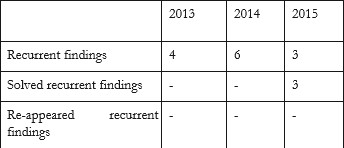

Recurrent findings started occurring in 2013. The table below shows it:

Table 2.

Recurrent Findings in Examination Result Report of Audit Board in Yogyakarta City Government in 2010 to 2015

These recurrent findings started to become problematic since 2013, where there are 4 recurrent findings occurring in fixed assets, grant expenditures, edotel funds and rusunawa funds. This condition worsened in 2014, where the recurrent findings became 6. The addition of recurrent findings occurred on cash balance accounts at expense treasurers and BOSDA fund accounts. However, conditions improved in 2015, with the solving of three recurrent findings, namely the cash balance account on the expense treasurer and the BOSDA fund account.

The lesson from this recurrent findings handling can be detailed as follow:

1. Grants 2013 - 2015 is a form of non-compliance with legislation

Under the State Auditing Standards, the Audit Board should be able to disclose non-compliance with the statutory regulations of the auditee. So far, the Regional Apparatus Organization (OPD) has run the procedure but not in accordance with the general guidelines. This is due to limited understanding in running the rules. Some findings are deemed inconsistent with the regulations of other ministries or higher institutions, leading to Audit Board’s recommendation to improve the Mayor Regulation. Suwanda (2013) mentions that external factors that cause problems in the financial statements of the weakness of regulation. Generally the weakness of regulation that occurs due to the inconsistency of the rules that have been set.

Administrative weaknesses are not only about internal control but also related to regulatory compliance. Based on the classification of findings in IHPS (2013), it is mentioned that the administrative weaknesses are related to noncompliance. Unaccountable or incomplete accountability is an administrative weakness.

Accountability is not orderly related to the grantee who is deemed not obedient to Mayor Regulation of Yogyakarta No. 49 of 2012 on the Management of Grants Spending in the form of money. In the findings of grant responsibility in 2014, Audit Board found that not all grant recipients have submitted accountability reports for the use of funds.

BOSDA 2014 – 2015, cash balance in expense treasurer in 2010 – 2011, 2014, rusunawa expenditure in 2012 -2014, and grant expenditure in 2013 – 2015 reflects the roles of the parties are not yet optimal.

These three recurrent findings relate to the balance cash in treasurers, BOSDA expenditures, and grant expenditures related to other parties outside the OPD. The balance cash in treasurers involves the finance section of all OPD, but includes the revenue and expenditure data in the OPD. For the Education Department, schools have an important role to account for the use of substantial funds on BOSDA. The Rusunawa Stimulant grant fund faces the same obstacles. Factors outside the control of the OPD, the grantee’s perception of being the encourage of recurrent findings problems. The community as grantees has a big influence. Public perceptions about grants also make it difficult for OPD technically to hold the responsibility for the use of funds as grants are regarded as honorariums.

The limitations in quantity and quality of Human Resources

The employee quality element is the most important internal control system element. Increasing the element of quality of human resources then other control elements can be reduced to the minimum and able to produce reliable financial accountability (Bastian and Gatot, 2003). The theme of limitations in the quantity and quality of human resources as the cause of recurrent findings relates to a number of recommendations issued by Audit Board. The treasurer and head of OPD are expected to improve governance in their respective OPD. The quality and quantity of human resources become one of the causes in the findings of BOSDA funds and balance cash. The problem of the quantity of human resources becomes the obstacle of the accountability of BOSDA funds in elementary school because there is no special officer. The quality of human resources leads to some recommendations that being addressed by Audit Board to the expense treasurer. Limited number and availability of human resources who understand the systems and procedures for regional financial management (Suwanda, 2013).

The incomplete follow-up implementation

The understanding of incomplete is supported by Audit Board’s statement in LHP in 2015 on two recommendations that have not been followed up by the Education Department for the findings of 2014. In addition, the delay in depositing the balance cash in the expense treasurer three times becomes a finding within the last six years. Findings not only appear in the same institution, but more often appear as findings in different institutions. Several times appearing as a finding and considered that there has not been a thorough improvement.

The weakness of internal control system

Audit Board’s examination results on internal control system shows that the Government of Yogyakarta City has not fully designed and implemented the elements of internal control system as required in legislation. Recurrent findings that occurred involving several parties and the implementation are not suitable to the mechanism. The weakness of internal control is also caused by a complicated and lengthy bureaucratic process so that it is included in the category of weakness of the internal control structure listed in the explanation of IHPS.

Discussion on internal control is inseparable with environmental issues of control involving commitments from the OPD leadership and staff roles. The cause of recurrent findings can occur due to lack of supervision from the OPD leadership. This has not yet shown a strong commitment from the OPD leadership to resolve the findings thoroughly. On the other hand, the commitment of employees is also expected that the implementation of internal control system can run. Commitment carried out by employees can be a follow-up of Audit Board’s recommendations.

The efforts of recurrent findings follow-up

Steps of follow-up plan implementation

The initial step of preparing the action plan begins with the publication of management letter and attached with the concept of LHP by the Audit Board. Coordination meetings were held in response to the Audit Board’s issued management letter and drafting an action plan. The action plan prepared by the OPD is a plan of follow-up implementation program.

Preparation of action plans in the Government of Yogyakarta City is still administrative and narrative. The preparation of an action plan is based solely on the responses to what is recommended and explains administrative follow-up. The preparation of an action plan should include a series of concrete steps towards improving regional government governance to identify steps to be taken, implementers, time, inputs and output (Suwanda, 2013). Other findings in this study indicate that there is no timeframe and sanctions in the completion of findings or recommendations.

The preparation of the action plan adjusted to the content of the recommendation, then implemented as a followup plan. Implementation of follow-up plans for action plans includes alerting actions to third parties, alerting financial managers, and developing mechanisms for optimizing financial management. Mayor Regulation No. 92 of 2012 explains the follow-up concerning third parties or outside the OPD is the responsibility of the OPD, related to the settlement. This step is therefore the responsibility of the education department and related units to coordinate to the parties mentioned in the Audit Board recommendation by giving them warning.

Follow-up implementation

Implementation of follow-up by interviewees includes actions taken by OPD technically, DPDPK as the organizer of financial report of regional government, and Inspectorate as follow-up team in following up recurrent findings. The follow-up implementation is a special program to deal with recurrent findings or differentiate follow-up to findings that re-appearing in institution is not found in the results of this research analysis.

Follow-up is implemented to address the emerging findings related to the weakness of the internal control system and non-compliance with legislation. The follow-up effort implemented aims to improve the effectiveness of the internal control system in OPD. Internal control according to Hiro (2006) includes preventive, detective, corrective, directive, and compensative control. The results of this study indicate some actions as a form of followup implementation, namely preventive, detective, and corrective action.

Preventive action is an attempt made to prevent the occurrence of the same findings in the future. The cause of recurrent findings is one of them related to the weakness of internal control that occurred in Yogyakarta City Government. Preventive measures that have been implemented by the OPD include: a) conducting coaching; b) preparing SOP (Standard Operating Procedure); c) carrying out socialization; and d) improving coordination.

Detective action is concerned with finding or detecting a problem after the problem occurs. Detective controls include checking and comparison (Sawyer et al, 2005). Detective measures that have been carried out by the OPD include: a) improving monitoring; and b) reconciliation. Reconciliation relates to the findings of the balance cash in the expense treasurer. The difference between budget and realization in financial reporting requires both internal and external reconciliation among OPD.

According to Sawyer (2005) management should develop systems that focus on undesirable conditions until the conditions are improved, and should establish procedures for prevention. Corrective action is implemented to improve the conditions from these findings. This is realized by the Yogyakarta city government as follows: a) compliance with legislation (system improvement refers to the prevailing provisions); b) sending warning letters addressed to parties that are late in submitting accountability reports.

Implementation of programs, policies, and procedures for recurrent findings follow-up

OPD technically develops procedures to follow-up on Audit Board’s findings and recommendations. The procedures that have been prepared in the Government of Yogyakarta City include the management of BOSDA and disbursement of grant funds. Implementation of programs and policies includes programs handling the delay in depositing balance cash especially in facing the end of the year for SPP, SPM, and GU. Further regulated in Mayor Regulation No. 57 of 2015 on Local Financial Management System and Procedure of Yogyakarta City.

BOSDA fund accountability policies and programs include assistance programs, regular school visits, and warning letters and BOSDA submission notices for each period. Other policies that have been formulated related to BOSDA are the Mayor Regulation of Yogyakarta No. 12 of 2014 and the Mayor Regulation of Yogyakarta No. 11 of 2017 on Guidance on Provision of Regional School Operational Assistance (BOSDA) for the Primary Education Unit conducted by Local Government.

The grant programs that have been implemented include socialization of grant regulation changes especially regarding the limits on the use of grant funds. The related technical OPD also conducts routine monitoring and evaluation using sampling test, where the results are submitted to the Mayor. The policy used in the management of these grants refers to the Mayor Regulation of Yogyakarta No. 31 of 2016 on the Management of Grants Spending in the form of Money.

Learning Forward

Long-term follow-up completion

Long-term follow-up completion is important as a solution to prevent recurrent findings because so far it is considered as short-term. The long-term completion measures are: a) generalize the findings that appear in other institutions; b) increasing the cooperation of various parties, especially the involvement of other parties outside the OPD to implement according to the procedures and rules that apply; c) procedures are carried out in accordance with regulations especially for grant findings involving the community; d) it is necessary to conduct coaching for financial manager in OPD as well as other financial managers outside OPD.

The application of strict sanctions

Sanctions involve other parties outside the OPD. The issue of strict sanctions for parties outside the OPD is very difficult to implement because considering the findings of BOSDA and grants involved the community and the fund itself is an assistance. What can be done for sanctions is to reinforce the existing rules.

Other sanctions involve OPD that have not completed follow-up. So far, no sanctions have been given if the recommendation status is still in process or not according to the Audit Board. However, this sanction should be supported by the time period to be agreed between the OPD and the Inspectorate based on the type of follow-up that must be implemented in each OPD.

Strengthening the roles of parties involved

Role becomes an important factor in the completion of follow-up. Strengthening roles in the OPD can be undertaken by appointing special personnel who have the responsibility to monitor the follow-up of the OPD both short-term and long-term recommendations to it is completed. Recommendations generally contain the preparation of SOP so that special teams are required to prepare procedures or SOP in the OPD.

The Inspectorate is expected to be more intensive in terms of reminding the OPD of Audit Board’s findings and recommendations on a regular basis. Recurrent findings should also be concern to the follow-up team so that the socialization and monitoring process can be carried out more intensively on OPD that have recurrent findings.

Preparing follow-up SOP

Based on the results of the initial interviews and other findings indicate there is a weakness in the follow-up process in the OPD and there is no follow-up SOP. Schemes or procedures of follow-up are developed based on weaknesses in the implementation of follow-up and modify based on several journals on audit follow-up. The preliminary guideline uses Mayor Regulation No. 92 of 2012 and also based on the procedures established by the Inspectorate. The process of preparing SOP is then supported with a weakness analysis in the application of followup procedures. Weakness in the application of procedures that have been designed that is on the limitations in determining the period of completion and limitations of human resources.

REFERENCIAS

Ahmad, Aswadi. (2016). Identifikasi Faktor yang Mempengaruhi Tindak Lanjut Rekomendasi Pemeriksaan Badan Pemeriksa Keuangan (Studi Kasus pada Pemerintah Provinsi Sulawesi Barat).Tesis Magister Akuntansi. Universitas Gadjah Mada Yogyakarta.

Akbar, Bahrullah. (2013). Akuntansi Sektor Publik Konsep & Teori. Jakarta: CV Bumi Metro Raya.

Alkins, Stephen Kwamena. (2012). Determinants of Auditee Adoption of Audit Recommendations: Local Government Auditors Perspectives. Journal of Public Budgeting, Accounting & Financial Management. Vol. 24 (2): 195-220.

Antara News Yogyakarta. (2014). Kota Yogyakarta Lima Kali Berturut-Turut Raih WTP. Jogja Terkini, 22 Mei. Diakses pada 12 November 2016. http://jogja.antaranews.com/berita/322646/kota-yogyakarta-limakali-berturut-turut-raih-wtp.

Badan Pemeriksa Keuangan RI. (2002). Surat Keputusan Badan Pemeriksa Keuangan Republik Indonesia Nomor: 37/SK/I/08/2002 tentang Panduan Manajemen Pemeriksaan BPK RI Tahun 2002.

Badan Pemeriksa Keuangan RI. (2007). Peraturan Badan Pemeriksa Keuangan Republik Indonesia Nomor 1 Tahun 2007 tentang Standar Pemeriksaan Keuangan Negara.

Badan Pemeriksa Keuangan RI. (2010). Peraturan Badan Pemeriksa Keuangan Republik Indonesia Nomor 2 Tahun 2010 tentang Pemantauan Pelaksanaan Tindak Lanjut Rekomendasi Hasil Pemeriksaan Badan Pemeriksa Keuangan.

Badan Pemeriksa Keuangan RI. (2013). Ikhtisar Hasil Pemeriksaan Semester I. Jakarta: Badan Pemeriksa Keuangan. Accessed on August 11, 2016. http://www.bpk.go.id/assets/files/ihps/2013/I/ ihps_i_2013_1409018306.pdf

Badan Pemeriksa Keuangan RI. (2015). BPK Menyampaikan 10.154 Temuan dalam IHPSI2015. Accessed on August 11, 2016. http://www.bpk.go.id/news/bpk-menyampaikan-10154-temuan-dalam-ihps-i-2015.

Badan Pemeriksa Keuangan RI. (2016). BPK Targetkan Kepatuhan Instansi 75%. Accessed on February 23, 2017. http://www.bpk.go.id/news/bpk-targetkan-kepatuhan-instansi-75.

Bastian, Indra, Gatot Soepriyanto. (2003). Sistem Akuntansi Sektor Publik, Konsep untuk Pemerintah Daerah. Jakarta: Salemba Empat.

Bastian, Indra. (2014). Audit Sektor Publik Pemeriksaan Pertanggungjawaban Pemerintahan. Jakarta: Salemba Empat.

Boynton, William C, Johnson, dan Kell. (2014). Modern Auditing. Eighth edition. Chichester: John Wiley and Sons, Inc.

Hartanto, Rudy. (2015). Analisis Penyelesaian Tindak Lanjut Hasil Pemeriksaan BPK RI (Perspektif Karakteristik Auditee, karakteristik Auditor BPK, Karakteristik Eksekutif dan Karakteristik Legislatif Daerah).Tesis Magister Akuntansi. Universitas Sebelas Maret Surakarta.

Inspektorat. (2016). Wawancara pendahuluan. Inspektorat Kota Yogyakarta.

Tugiman, Hiro. (2006). Standar Profesional Audit Internal. Yogyakarta: Kanisius.

Huefner, Ronald J. (2010). Local Government Fraud: The Roslyn School District Case. Management Research Review. Vol. 33 Iss 3: 198-209. Accessed on December 16, 2016. http://dx.doi.org/10.1108/01409171011030363.

Institut Akuntan Publik Indonesia. (2011). Standar Profesional Akuntan Publik. Jakarta: Salemba Empat.

Kusuma, Widya Ardiyanti. (2014). Dinamika Hubungan Inspektorat dengan Objek Pemeriksaan dalam Penanganan Temuan Pemeriksaan yang Berulang Tahun 2010 - 2013 (Studi pada Inspektorat Kabupaten Bojonegoro).Tesis Magister Administrasi Publik. Universitas Gadjah Mada Yogyakarta.

Lasan, Lukas Luli. (2016). Faktor-Faktor yang Memengaruhi Penyelesaian Tindak Lanjut Rekomendasi Pemeriksaan Badan Pemeriksa Keuangan Atas Laporan Keuangan Pemerintah Daerah (Studi Kasus pada Pemerintah Daerah Kabupaten Mimika).Tesis Magister Akuntansi. Universitas Gadjah Mada Yogyakarta.

Menteri Dalam Negeri Republik Indonesia. (2007). Peraturan Menteri Dalam Negeri Nomor 59 Tahun 2007 tentang Perubahan atas Peraturan Menteri Dalam Negeri Nomor 13 Tahun 2006 tentang Pedoman Pengelolaan Keuangan Daerah.

Menteri Pendayagunaan Aparatur Negara Republik Indonesia. (2004). Keputusan Nomor 40 Menteri Pendayagunaan Aparatur Negara Nomor 4 Tahun 2004 tentang Pedoman Pelaksanaan, Pemantauan, dan Pelaporan Tindak Lanjut Hasil Pemeriksaan Badan Pemeriksa Keuangan pada Instansi Pemerintah.

Noble, Bram, dan Keith Storey. (2004). Towards Increasing the Utility of Follow-up in Canadian EIA. Environmental Impact Assessment Review. Vol. 25 (2005): 163-180. Accessed on Desember 16, 2016. www.elsevier.com/locate/eiar.

Rai, I Gusti Agung. (2011). Audit Kinerja pada Sektor Publik. Edisi Ketiga. Jakarta: Salemba Empat.

Republik Indonesia. (2004). Undang-Undang Nomor 15 Tahun 2004 tentang Pemeriksaan Pengelolaan dan Pertanggungjawaban Keuangan Negara.

Ross, William A. (2003). The Independent Environmental Watchdog A Canadian Experiment in EIA Follow-up.

Sawyer, Lawrence B, Mortimer A, dan Scheiner. (2005). Internal Auditing, Diterjemahkan oleh: Desi Adhariani. Jilid I. Edisi 5. Jakarta: Salemba Empat.

Sekaran, Uma dan Roger Bougie. (2013). Research Methods for Business. Edisi Keenam. Chichester: John Wiley & Sons Ltd.

Sugiyono. (2011). Metode Penelitian Kuantitatif, Kualitatif, dan R&D. Bandung: Alfabeta.

Suwanda, Dadang. (2013). Strategi Mendapatkan Opini WTP Laporan Keuangan Pemda. Jakarta: PPM.

Walikota Yogyakarta. (2012). Peraturan Walikota Yogyakarta Nomor 92 Tahun 2012 Tentang Pedoman Tindak Lanjut Hasil Pemeriksaan Badan Pemeriksa Keuangan Republik Indonesia Pada Pemerintah Kota Yogyakarta.

Walikota Yogyakarta. (2012). Peraturan Walikota Yogyakarta Nomor 49 Tahun 2012 tentang Pengelolaan Belanja Hibah berupa Uang.

Walikota Yogyakarta. (2015). Peraturan Walikota Yogyakarta Nomor 57 Tahun 2015 tentang Sistem dan Prosedur Pengelolaan Keuangan Daerah Kota Yogyakarta.

Walikota Yogyakarta. (2016). Peraturan Walikota Yogyakarta Nomor 31 Tahun 2016 tentang Pengelolaan Belanja Hibah berupa Uang.

Walikota Yogyakarta. (2017). Peraturan Walikota Yogyakarta Nomor 11 Tahun 2017 tentang Pedoman Pemberian Bantuan Operasional Sekolah daerah (BOSDA) untuk Satuan Pendidikan Dasar yang Diselenggarakan Pemerintah Daerah.

Yin, Robert K. (2014). Case Study Research: Design and Methodology. Edisi Kelima. California: Sage Publications, Inc.