SUR-SUR

The effects of internal control implementation and organizational culture on financial reporting quality. Study on Local Government of Jakarta, Indonesia

Los efectos de la implementacion del control interno y la cultura organizacional en la calidad de la informacion financiera. Estudio sobre el gobierno local de Yakarta, Indonesia

The effects of internal control implementation and organizational culture on financial reporting quality. Study on Local Government of Jakarta, Indonesia

RELIGACIÓN. Revista de Ciencias Sociales y Humanidades, vol. 4, núm. 16, pp. 236-244, 2019

Centro de Investigaciones en Ciencias Sociales y Humanidades

Esta obra está bajo una Licencia Creative Commons Atribución-NoComercial-SinDerivar 4.0 Internacional.

Recepción: 06 Enero 2019

Aprobación: 22 Mayo 2019

Abstract: This study examines the influence of internal control implementation and organizational culture on financial reporting quality. The study is applied and descriptive research, using a questionnaire for data collection. The validity and reliability of the questionnaire were estimated using AVE, with a Cronbach’s alpha greater than 0.5 and 0.7, respectively. Data analysis was conducted using partial least square (PLS). The results showed that Internal control implementation influenced financial reporting quality while organizational culture had no effect on financial reporting quality.

Keywords: Internal Control Implementation, Organizational Culture, Financial Reporting Quality.

Resumen: Este estudio examina la influencia de la implementación del control interno y la cultura organizacional en la calidad de la información financiera. Se aplica el estudio y la investigación descriptiva, utilizando un cuestionario para la recolección de datos. La validez y confiabilidad del cuestionario se estimaron utilizando AVE, con un alfa de Cronbach superior a 0,5 y 0,7, respectivamente. El análisis de los datos se realizó utilizando el mínimo cuadrado parcial (PLS). Los resultados mostraron que la implementación del control interno influyó en la calidad de la información financiera, mientras que la cultura organizacional no tuvo ningún efecto sobre la calidad de la información financiera.

Palabras clave: Implementación de control interno, Cultura organizacional, Calidad de la información financiera.

INTRODUCTION

Law Number 17 Year 2003 regarding State Finance requires central and local government agencies to prepare financial statements for accountability of state and regional government. Phenomenon the quality of financial statements in the regional government is still low, many regional goverments got unqualified opinions according to Harry Azhar (chairman of supreme audit board , December 2014). Local governments have an obligation to responsible their local finances by making local financial reporting.

Based on supreme audit board report, the Jakarta Capital Special Region obtained a unqualified opinion. In addition, supreme audit board found that the internal control system for the management and accountability at 2014 and the first semester 201 in Jakarta Provincial Government (Department of Communication and Transportation) has not been adequately conducted and weaknesses or deviations from the provisions of legislation. The weaknesses that occur both from internal control aspects and compliance with laws and regulations. Government Regulation Number 60 Year 2008 regarding Government Internal Control System explains the definition of the Internal Control System is an integral process in the actions and activities undertaken continuously by the leadership and all employees to provide reasonable assurance on the achievement of organizational goals through effective and efficient activities, reliability of financial reporting, security of state assets, and regulatory compliance legislation. Government Internal Control System applied both to central and local governments. to provide reasonable assurance for the achievement of effectiveness and efficiency in achieving the objectives of state governance, reliability of financial reporting, security of state assets, and compliance with laws and regulations. A number of internal control weakness issues consist of weaknesses of accounting and reporting control systems. Nunuy and Peny (2015) research on local goverment agency in districts, municipalities and provinces in South Sumatra revealed that internal control have a significant effect on the quality of financial reporting. From the research shows that the internal control is very large influence. Internal control is a process undertaken by boards of directors, management and subordinates to provide reasonable assurance for the purpose of protecting assets, maintaining records, providing accurate and reliable information, applicable financial reporting standards, promoting changes in operational efficiency, promoting compliance managerial policies, comply with applicable laws and regulations (Romney and Steinbart,2009;Arens et.al 2012). Control environment, is an objective condition that exists in the organization. This condition is largely determined by the leadership of the organization, where the control environment includes values of integrity and ethics, commitment to competence, participation of the supervisory board, management philosophy and operating style, organizational structure, delegation of authority and responsibility and human resource policies and practices (Arens et al : 2003: 274-276).

Beside internal controls there are may affect the quality of financial reporting. Quality of financial reporting can also be influenced by organizational culture factors. The Egu U Innah et.all (2014) study revealed that organizational culture has a significant effect on financial reporting practices in Nigeria, Companies with ethical culture will be more committed to complying with regulations and producing quality financial reporting. Hafiza Aishah Hashim (2012) research conclude that organizational culture influences the financial reporting in Malaysia. This research reveals that the quality of financial reporting can not be free from the influence of organizational culture and directly influence government policy broadly. Culture affects every single interaction in the workplace and human interaction is the most important that determines the competitiveness of an organization.

Organizational culture is defined as a form or pattern of behavior or the way users act based on shared values, assumptions, beliefs, and norms in using accounting information systems that are considered valid, believed, thought and perceived as the correct way which then taught to new users of accounting information systems to produce quality accounting information (Robbins & Judge, 2011: 554, Jones 2010: 30, Anthony et al 2003: 54, Gibson et al 1991: 46, Gibson et al, 2009: 30 , and Barthol & Marthin, 1998: 91).Organizational culture can create quality financial reporting in the company. Hofstede et.all (2010, suggests behind the symbols, heroism, and rituals in accounting there are values. At least activity is determined by technical needs, all governed by values and influenced by cultural differences. The purpose of this study is to illustrate:

- 1.

1) Describe the effect of internal control on the quality of financial reporting.

2) Describe the organizational culture of influence on the quality of financial reporting

Implementation of internal control

Implementation of internal control means design of general control and application controls to ensure that all internal control elements are implemented in the specific application systems contained within each organizational transaction cycle. The management objectives to design and establish the effective internal control systems are as follows (Elder et al, 2010: 290):

- 1.

1) Financial reporting reliability. Management assumes both legal and professional responsibilities to ensure that information has been reasonably presented in accordance with reporting requirements such as generally accepted accounting principles (GAAP). The objective of effective internal control over financial reporting is to fulfill the financial reporting responsibilities.

2) Operational efficiency and effectiveness. Control within the company will encourage the use of resources efficiently and effectively to optimize the company’s suggestions. An important objective of internal control is to obtain accurate financial and non-financial information about the company’s operations for decision making purposes

3) Obedience to laws and regulations. All public companies are required to issue reports on the effectiveness of the implementation of internal control over financial reporting. In addition to complying with legal provisions, public, non-public, and non-profit organizations are required to comply with various laws and regulations.

Internal Control on Quality of Financial Reporting

Elbannan (2009) implementation of the effectiveness of internal controls can increase its capacity to meet the financial statements and the role of quality accounting information. Jason Wood, et al (2013) The Internal Control component consisting of critical four components to achieving the financial reporting reliability objectives, integrated internal control components working together to reduce the risk of reliable and generally acceptable financial reporting process designed to provide reasonable assurance about the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.

The quality of financial reporting is influenced by internal control factors (Elder et al (2010: 290) .The reason why management designs an effective internal control system is to achieve three general objectives:

(a) reliability of financial reporting, (b) effectiveness and efficiency of company operations, and (c) compliance with laws and regulations (Messier et al., 2006: 220). Internal controls are designed to ensure the accuracy of data processing, storage methods and the accuracy of results (information). Good internal controls within the organization will help management efforts protect the company’s assets from loss and embezzlement and to maintain the accuracy of the company’s financial data (Jones and Rama, 2003: 7

Organizational culture

Culture is a set of basic understandings and assumptions that are shared by a group, such as in an ethnic or a state (Stair et al, 2010: 51). Bound et al (1994: 89) states that culture is related to the way of thinking and acting which is the characteristic (characteristic) of a particular social or organizational society. Then Hofstede & Hofstede (2005: 4) stated that culture consists of unwritten social game rules. Still according to Hofstede & Hofstede (2005: 4) culture is a collection of thoughts that can distinguish members of one group or category of people with other groups or categories of people.Furthermore, the culture that takes place within a company or organization is called a corporate culture or organizational culture. Bartol & Martin, (1998: 91). In the Ministerial Empowerment of State Apparaturs and Bureaucratic Reform of the Republic of Indonesia Number 39 (2012.3) on guidelines for the development of work culture, organizational culture is defined as a shared value system within the organization that becomes the reference of how employees perform activities to achieve the goals or ideals of the organization.

Organizational Culture on Quality of Financial Reporting

Hofstede et.all (2010, 318-319) suggests behind the symbols, heroism, and rituals in accounting there are values influenced by different cultures. Gray, S. J. (1988) argues that the cultural values reflected in the development of attitudes related to accounting and accounting systems, for which accounting values derived from cultural values (Hofstede’s theory) affect the development of the country’s financial reporting system.

In general, organizational culture has a positive influence on organizational effectiveness when organizational culture can provide support to organizational goals, widely shared and deeply embedded in every member of the organization (Barthol & Martin 1998: 91)

Loudon & Loudon (2010: 94) argued that organizational culture entered as one of the central organizational factors at the time of planning a new system for financial reporting.

METHODOLOGY

This research is a descriptive-analytical research. The type of investigation used in this study is a causal study in which the researcher wanted to find the effect of one or more problems. The data used only once collected over a certain period in order to answer a research question (questionnaire) called the Cross Sectional study.

2 questionnaires distributed to Sub service in Jakarta Province for each agency. The provincial office of Jakarta Province Region was taken because of the findings of supreme audit board there was a weakness in the internal control. Number of samples are 32 Department of sub service in Jakarta Provinces (West Jakarta and South Jakarta). Data analysis used to test used Partial Least Square-Path Modeling (PLS-PM) approach. Structural Equations:

RESULTS

Measurement Model (outer model)

Convergent Validity

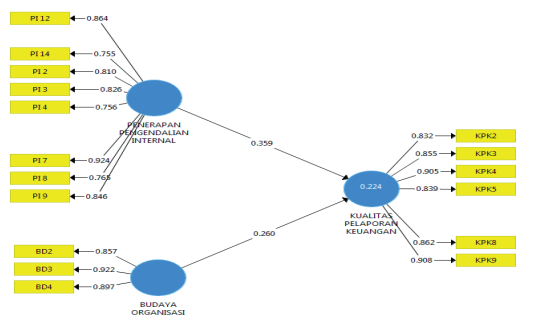

Convergent Validity Testing of measurement model with reflective indicator is assessed by correlation between construct Individual indicators are considered valid if they have correlation values above 0.70. By looking at the output of correlation between the indicator with the construct as shown in the table and the structural figure below:

Figure 1. PLS Algorithm

The result of the modification of the second convergent validity test in figure, can be seen that the factor loading value is above 0.70 then the data has been called valid.

b) Discriminant Validity

Discriminant validity test, reflective indicator can be seen on cross-loading between indicator with its construct. An indicator is valid if it has the highest loading factor to the target construct compared to the loading factor to another construct. discriminant validity use the square root of average variance extracted (AVE) value of each construct above 0.7 with the correlation between constructs with other constructs in the model, it is said to have a good discriminant validity value.

| Variabel | AVE |

| Internal Control Implementation | 0.673 |

| Organizational Culture | 0.797 |

| Financial Reporting Quality | 0.752 |

| Org Culture | Financial Report Quality | Internal Control | |

| Organizational Culture | 0.893 | ||

| Financial Reporting Quality | 0.313 | 0.867 | |

| Internal Control | 0.148 | 0.397 | 0.820 |

From table 1 and 2 it can be concluded that the square root of the average variance (AVE) value of all variables above 0.7. Based on the above statement then the constructs in the model are estimated to meet the criteria of discriminant validity.

Composite Reliability dan Cronbach’s Alpha

Testing composite reliability and cronbach’s alpha aims to test the reliability of the instrument in a research model or measure internal consistency and its value should be above 0.60. If all values of latent variables have composite reliability or cronbach alpha ≥ 0.7 it means that the construct has good reliability or the questionnaire used as a tool in this research has been reliable or consistent.

| Variabel | Composite Reliability | Result |

| Organizational Culture | 0.922 | Reliabel |

| Financial Reporting Quality | 0.948 | Reliabel |

| Internal Control Implementation | 0.942 | Reliabel |

| Variabel | Cronbach’s Alpha | Result |

| Organizational Culture | 0.878 | Reliabel |

| Financial Reporting Quality | 0.934 | Reliabel |

| Internal Control Implementation | 0.933 | Reliabel |

Based on the table 3 and 4 the results of composite reliability testing and cornbach alpha test results showed the value ≥ 0.7, it can be concluded the construct has good reliability or questionnaire used as tool in this research have been reliable or consistent.

2. Testing Structural Model / Hypothesis Testing (Inner Model)

Inner model testing is the development of concept-based models and theories in order to analyze the relationship between exogenous and endogenous variables.

a) R-square value

The value of R-square which is a goodness-fit test model.

Source: PLS Output

The structural model indicates a value of 0.224. the value can be interpreted that construct variability of Financial Reporting Quality can be explained by constructive variability of Internal Control and Organizational Culture are 22.4% while 77.6 % is explained by other variables outside of the studied.

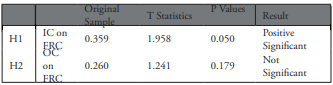

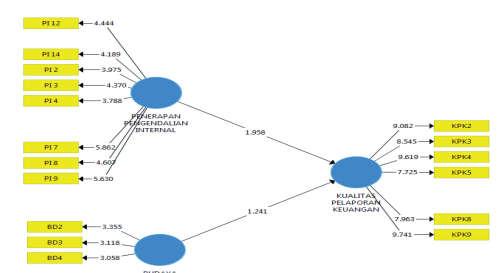

b) Hypothesis Testing Results

Estimated value for path relation in structural model should be significant by looking at the value of the parameter coefficient and the significance value of T-statistics on the. algorithm boostrapping report. From Table 6 and Figure 2, Internal Control have significant, while Organizational Culture has no significant influence.

Sumber: output PLS

Figure 2. Boosstrapping

DISCUSSION

Internal Control affects the Quality of Financial Reporting. The results of this study provide empirical evidence that the better of Internal Control in the agency (Sub Service) it will support the quality of financial reporting in all Sub Service Instancy in Jakarta Region Province (West Jakarta and South Jakarta).

Organizational Culture does not affect the Quality of Financial Reporting. The results of this study provide empirical evidence that the organizational culture does not affect in the process of preparing the correct and qualified financial statements at all sub service in the Jakarta region province because each sub service perform activities to achieve the goals must be follow the Law Number 17 Year 2003 and Ministerial Empowerment of State Apparaturs and Bureaucratic Reform of the Republic of Indonesia Number 39 (2012.3) than cultural values or attitudes related to how employees perform activities.

CONCLUSION

Inadequate and deviation of internal control system in management and accountability of Financial Statement, it makes Jakarta region get the audit opinion of unqualified. While Organizational culture does not affect the quality of financial reporting because to publish the financial statements every agency must be obey the rules based on Goverment Accounting Standard and Law no 17/2003. Organizational culture have not provide support to organizational goals, widely shared and deeply embedded in every member to prepare the quality of Financial Statement.

BIBLIOGRAPHIC REFERENCES

Arens,Alvin A, Elder,Randal J, Mark S. Beasley. (2012). Auditing and Assurance Service, An Integrated Approach,19tn Edition,Prentice Hall,Englewood Clifts,New Jersey.

Aisha Hashim (2012)

Boynton (2001). Modern Auditing. Seventh Edition. John Wiley & Son, Inc.: New York..

Charles H. Gibson (2009). Financial Reporting & Analysis, Eleventh Edition. South-Western Cengage Learning.

Egu U Innah et.all . (2014). Organizational Culture and Financial Reporting Practices in Nigeria. Research Journal of Finance and accounting ISSN 2222-2847. Vol.5, No.13.

Elbannan (2009). Quality Of Internal Control Over Financial Reporting,Corporate Governance And Credit Rating. International Journal of Disclosure and Governance , 6(2):127–149.

Gelinas U, &Dull, B. Richard. (2012). Accounting Information Systems. 9th ed. USA:South Western Cengage Learning.

Ghozali, Imam, (2011). AplikasiAnalisis Multivariate Dengan Program IBM SPSS 19, Edisi 5. Semarang: BadanPenerbitUniversitasDiponegoro.b

Gibson, James L. John M. Ivancevich & James H. Donnelly, JR. (2009) .Organization: Behavior – Structure- Processes.13th Edition. NY: Mc-Graw-Hill.

Gareth,Jones. (2010). Organization Theory, Design and Change. 6th Editions: Pearson

Gray, S. J. (1988). Towards a Theory of Cultural Influence on the Development of Accounting Systems Internationally. ABACUS, Vol. 24, No. I, I988.

Harry Azhar Azis.(2014). Ketua Badan Pemeriksa Keuangan BPK. BPK sebut kualitas laporan keuangan daerah masih rendah. Antara News, 8 Desember 2014.

Hafiza Aishah Hashim (2012). The Influence of Culture on Financial Reporting Quality in Malaysia. Asian Social Science; Vol. 8, No. 13; 2012 ISSN 1911-2017 E-ISSN 1911-

Hair, Joseph F.& William C Black et al. (2010). Multivariate Data Analysis, A Global Perspective.7th Edition. NJ: Prentice Hall.

Hofstede, Geert, &Gert Jan Hofstede. (2010). Cultures and Organizations Software Of The Mind. NY: Mc-Graw-Hill.

Jan A Pfister (2009). Managing Orgnization Culture for Effective Internal Control. Springer

Jason Wood, et all. (2013). IT Auditing and Application Controls for Small and Mid-Sized Enterprises Revenue, Expenditure, Inventory, Payroll, and More. John Wiley & Sons.

Kementerian Pendayaan Aparatur Negara RI, (2012). Peraturan Menteri Pendayaan Aparatur Negara dan Reformasi Birokrasi No. 39 tentang Pedoman Pengembangan Budaya Kerja

Khotari. C.R. (2004). Research Methodology:Methods and Techniques. New Delhi: New Age International (P) Ltd.,Publishers.

Loudon, Kenneth C. & Jane P. Laudon. (2012). Manajemen Information System: Managing The Digital Firm.12Th Edition. NJ: Prentice-Hall.

Marshal B. Romney dan Paul John Steinbart.2006.Accounting Information System. Prentice Hall.

Nunuy dan Peny. (2015). The Effect of the Implementation of Government Internal Control System (GICS) on the Quality of Financial Reporting of the Local Government and its Impact on the Principles of Good Governance: A Research in District, City, and Provincial Government in South Sumatera.Elsevier Procedia - Social and Behavioral Sciences 211 ( 2015 ) 811 – 818.

Republik Indonesia. Peraturan Pemerintah RI Nomor 71 Tahun (2010) tentang Standar Akuntansi Pemerintahan.

Randal J. Elder, Mark S. Beasley, & Alvin A. Arens. (2010). Auditing and Assurance Sevices an Integrated Approach. NJ: Prentice-Hall.

Romney. Marshal B. & Paul John Steinbart (2009). Accounting Information Systems, Eleventh Edition: New Jersey: Pearson-Prentice-Hall

Sekaran, Uma & Roger Bougie. (2013). Research Methods For Business; A Skill Building Approach. UK: John Wiley & Sons,New York

Stair, Ralph M. &George W. Reynolds. (2010).Principles Of Information Systems, Course Technology. 9th Editions. NY: Mc-Graw-Hill

Schein, E. (1992). Organizational Culture and Leadership.2nd Edition.Jossey-Bass.Sanfrancisco: Publishers.

Undang-Undang Nomor 17 Tahun (2003) tentang Keuangan Negara

Wood Jason,William Brown, Harry Howe et all (2013). IT Auditing and Apllication Controls for SME. John Wiley and Sons, Inc. USA.