Theoretical-empirical Article

Understanding De-dollarization Among BRICS Nations: Systematic Review of the Factors and Fallout

Compreendendo a Desdolarização entre os Países do BRICS: Revisão Sistemática de Fatores e Consequências

Samer Ajour El Zein sajour@eae.es

Florin Teodor Boldeanu boldeanuflorinteodor@yahoo.com

Samer Ajour El Zein sajour@eae.es

Florin Teodor Boldeanu boldeanuflorinteodor@yahoo.com

Understanding De-dollarization Among BRICS Nations: Systematic Review of the Factors and Fallout

Revista de Administração Contemporânea, vol. 29, no. 2, e240197, 2025

Associação Nacional de Pós-Graduação e Pesquisa em Administração

Received: 17 July 2024

Revised document received: 25 January 2025

Accepted: 12 February 2025

Published: 07 May 2025

ABSTRACT

Objective: this research paper reviews the political and economic factors surrounding the phenomenon of de-dollarization among the BRICS nations.

Theoretical approach: de-dollarization refers to the strategic shift away from the United States dollar as the dominant currency in international trade and financial transactions. BRICS is a power group similar to the group of seven that features the five most important emerging economies, consisting of Brazil, Russia, India, China, and South Africa.

Method: we used a systematic literature review method employing keyword search in Web of Science.

Results: the resulting filtered publications helped us to get a comprehensive picture of the main factors and implications of the de-dollarization process in those countries.

Conclusion: based on these findings, we introduce new perspectives grouped into challenges, implications, and future lines of research.

Keywords: De-dollarization+ BRICS+ political factors+ economic factors.

RESUMO

Objetivo: A presente pesquisa oferece uma revisão sistemática abordando os fatores políticos e econômicos relacionados ao fenômeno da desdolarização entre os países do BRICS.

Marco teórico: A desdolarização diz respeito a estratégia de afastamento em relação ao dólar norte-americano como moeda dominante no comércio internacional e em transações financeiras. Os BRICS incluem cinco das mais importantes economias emergentes - Brazil, Rússia, Índia, China e África do Sul - e representa um bloco de poder similar ao Grupo dos Sete (G7).

Método: O estudo adota o método da revisão sistemática da literatura, usando a pesquisa de palavras-chave na base de dados Web of Science.

Resultados: As publicações encontradas contribuíram para a obtenção de um panorama abrangente dos principais fatores e consequências do processo de desdolarização nesses países.

Conclusão: Esses resultados dão suporte a novas perspectivas, apresentadas como desafios, implicações e futuras linhas de pesquisa.

Palavras-chave: Desdolarização, BRICS, fatores políticos, fatores econômicos.

INTRODUCTION

In recent years, the phenomenon of de-dollarization has gained significant attention, particularly among the emerging economies known as BRICS countries - Brazil, Russia, India, China, and South Africa (Kagiri, 2017). This research paper addresses different dimensions of de-dollarization among the BRICS nations in order to shed light on the potential consequences for both the BRICS nations and the global financial landscape. The phenomenon of de-dollarization is of utmost significance since it concerns the stability of many G20 nations as well as carrying significant implications surrounding the stability and dominance of the United States economy in years to come (Milam, 2023).

For years, the United States has maintained a dominant free-market economy that allowed the United States dollar to be established as the world reserve currency since 1944 (Wang & Zhang, 2023). The dominance of the USD in international trade and finance has long been a subject of scrutiny, as it confers significant advantages to the United States, such as lower borrowing costs and the ability to impose economic sanctions (Gourinchas, 2021).

The BRICS countries, collectively representing over 40% of the world’s population and a significant share of global GDP, have expressed a growing desire to diversify their currencies away from the USD. The BRICS nations have recognized the need to reduce their vulnerability to external shocks and enhance their economic sovereignty (Nayyar, 2018). The increase in de-dollarization across various nations threatens the strength of the United States dollar and the competitive advantages that are included with operating as the reserve currency.

The approaches taken by countries to reverse dollarization commenced in the 1980s by regulatory and legal reforms, such as in Nicaragua, Peru, and Bolivia (Zendejas & Nodari, 2023), and by administrative enforcement (Luft, 2023). At a later stage, the rise of the BRICS countries in 2012 in the global economy explored the historical context of a process of moving away from the world’s reliance on the U.S. dollar (USD) as the chief reserve currency, with the formation of an alternative reserve currency that allowed them to propel their economic growth (Iida, 2024). China has stepped in as a driver of de-dollarization, aiming to position its renminbi as a reserve currency with a positive impact on the international business landscape. These nations emerged as significant players in the global economy (Sweidan, 2023), with their combined economic power and influence reshaping the international business landscape (Zhang et al., 2013). In April 2023, Alexander Babakov, deputy chairman of Russia’s State Duma, announced that BRICS nations are spearheading a BRICS currency for cross-border trade (Ojekemi et al., 2023). This move from BRICS would not only impact the strength of the United States dollar, but it could also likely bring about political fallout as well, with tensions between the G7 and BRICS already high from Russia’s invasion of Ukraine, China’s military action surrounding Taiwan, and many other factors. BRICS countries have significantly increased their presence in global trade, challenging the dominance of traditional economic powers. Their emphasis on regional integration, trade agreements, and investment in infrastructure has facilitated their trade growth (Becker, 2014), and furthermore, they have emerged as important actors in global governance, advocating for a more multipolar and representative international order. Their initiatives, such as the New Development Bank and the Contingent Reserve Arrangement, aim to provide alternative sources of financing and challenge the dominance of Western-led institutions (Arapova, 2019).

One of the key motivations behind the de-dollarization efforts in BRICS countries is to mitigate the risks associated with currency volatility and fluctuating exchange rates (Sjøli, 2023). The USD’s role as the global reserve currency exposes BRICS nations to the consequences of U.S. monetary policy decisions and fluctuations in the value of the dollar. Furthermore, the geopolitical landscape has also played a crucial role in driving de-dollarization among the BRICS nations, as political tensions increase from trade talks, economic sanctions, and military actions. BRICS countries perceive de-dollarization as a means to reduce their exposure to such risks and enhance their resilience against external pressures. By diversifying their currency reserves and promoting bilateral and multilateral trade settlements in their local currencies, BRICS nations can strengthen their economic ties and foster a more balanced global financial architecture (Asomaning, 2023).

The implications of de-dollarization in BRICS countries extend beyond their own economies. The shift away from the USD has the potential to reshape the global financial system, leading to the emergence of multiple reserve currencies and diversified payment systems. While this process may introduce greater financial multipolarity, it also presents challenges and uncertainties. The impact on global trade, financial markets, and the USD’s position as the dominant reserve currency will be considered in this paper, with a qualitative hypothesis surrounding the economic impact of de-dollarization in BRICS countries (Buckley & Trzecinski, 2023).

The volume of literature on BRICS has grown over the past decade, reflecting the rising significance of these economies internationally. Both academic research and broader publications have been central to contemporary discourse, with frequent updates and continuous citation activity. BRICS’s robust economic growth - particularly in China and India - is known for its significant contributions to global GDP growth (Kumar et al., 2023), which has been shown an increasing political influence of BRICS on global platforms (Stuenkel, 2020). Moreover, the increased socio-cultural interactions and exchanges among BRICS countries are augmenting mutual understanding and cooperation with the West, and growing investment and trade relations (Li et al., 2016). Research reveals that BRICS has transformed into a powerful bloc shaping economic, political, and socio-cultural narratives globally. Its role in global governance, burgeoning trade and investment relations, substantial economic growth, and accelerated infrastructure development underpin its rising importance. Moreover, the literature on de-dollarization among BRICS countries has gained significant attention in recent years. Researchers and scholars have explored various dimensions of this subject, shedding light on the processes, challenges, and implications of reducing reliance on the U.S. dollar in international transactions.

Thus, given the importance of this process, a systematization of the existing literature is essential to improve our understanding of the motivation of BRICS countries and the respective consequences. Then, the main purpose of this study is to improve the current knowledge by critically examining existing related literature about the BRICS countries and evaluating the advantages and disadvantages of the dollarization that stem from the main BRICS pillars. This systematic review suggests three main research objectives (ROs):

RO1. To understand the causes of the BRICS de-dollarization movement.

RO2. To identify and discuss implications and potential consequences in terms of possible advantages and disadvantages of de-dollarization.

RO3. To propose and generate new perspectives and argumentations.

As far as we know, this study is the first to conduct a systematic literature review to understand the de-dollarization process in BRICS countries and formulate potential consequences. Our study contributes to the literature in different ways. First, we conducted a systematic review of the literature about the de-dollarization process in general and in BRICS countries. Our review has been narrowed to top publications in the Web of Science framework to collect significant insights. Second, these studies were analyzed in different domains: geopolitical and economic factors contributing to de-dollarization, implications, advantages and disadvantages, and future lines of research. Contrary to some literature reviews that only focus on a descriptive analysis, our study, in addition to conducting a systematic review, identifies the main motivations underlying this process and proposes a set of potential consequences. So, our study would help future researchers really unfold the de-dollarization process, and then address specific dimensions of this process in their research. For policymakers and investors, it would help to develop specific policies and investments respectively, which will consider potential fallouts and associated risks.

The next section is a brief history of dollarization and de-dollarization, followed by a systematic review methodology. This is followed by a discussion section of the findings. Finally, in the discussion sections, we show advantages, disadvantages, implications, and future lines of research.

CONTEXT AND MOTIVATION OF THE DOLLARIZATION AND DE-DOLLARIZATION

Dollarization and de-dollarization defined

The literature on de-dollarization among BRICS countries has gained significant attention in recent years. Researchers and scholars have explored various dimensions of this subject, shedding light on the processes, challenges, and implications of reducing reliance on the U.S. dollar in international transactions. One aspect that stands out in the literature is the breadth of publications available. Numerous academic papers, books, and reports have been published, enabling a comprehensive understanding of the de-dollarization phenomenon in the BRICS countries. Key topics covered include the motives behind de-dollarization, policy measures undertaken by BRICS nations, the impact on financial markets, and the potential consequences for the global economy.

While many countries today are focused on pursuing de-dollarization, it’s important to briefly discuss what led to dollarization in the first place. In 1944, 44 countries created the Bretton Woods Agreement, which established the U.S. dollar as the world’s reserve currency (Khan, 2023). These countries pegged their currencies to the U.S. dollar, which eventually came to be known as ‘dollarization.’ As most of the world continued to follow the original 44 countries and align their currencies with the U.S. dollar, the United States was able to greatly strengthen its position in geopolitics and the global economy. The U.S. dollar has since dominated global trade and finance due to the relative stability of its value, the size of the U.S. economy, the geopolitical influence of the United States, and the market for U.S. debt (Liu & Papa, 2022). While the U.S. dollar accounted for 58.36 percent of global foreign exchange reserves at the end of 2022, data from the International Monetary Fund show that this is down from more than 70 percent since 1999 (Phillips, 2023). This comes as many countries are looking to create opportunities to move away from the U.S. dollar; this trend has become known as ‘de-dollarization.’ Countries typically look to de-dollarize with the goal of becoming more independent of the U.S. dollar and the hope that they can ultimately increase their influence in geopolitics and the global economy. Additional reasons include economic, political, and strategic motivations (Luft, 2023). The literature highlights factors such as the desire to minimize vulnerability to U.S. monetary policy, diversify currency reserves, enhance economic sovereignty, and challenge the U.S. hegemony in the global financial system, export competitiveness, and economic growth among BRICS countries by leading to a depreciation of the real exchange rate (Chkili & Nguyen, 2014; Weiping, 2023). Debates within this theme focus on the effectiveness of de-dollarization strategies and the potential consequences for both the BRICS countries and the international monetary system (Elizabeth et al., 2023).

Evolution over time

Scholars have identified several motivations behind the reasons driving de-dollarization, such as reducing vulnerability to U.S. monetary policy, diversifying currency risks, and promoting regional economic integration. By understanding these motivations, policymakers can make informed decisions regarding their own de-dollarization strategies, potentially leading to more stable and resilient financial systems. Moreover, the literature in this field encompasses a wide range of geographical locations, including both developed and emerging economies. Researchers have conducted empirical studies to analyze the trends and patterns of de-dollarization in different regions, providing important insights into the global dynamics of currency diversification.

A shift toward a multi-currency international monetary system could have significant implications for de-dollarization. Thus, after the commencement in the 1980s, the eurozone has found the potential to rival the U.S. dollar as an international currency due to the size and stability of the eurozone economy, as well as the depth and liquidity of euro-denominated financial markets.

At a later stage, in 2011, the role of financial innovation and technological advancements played a key role in facilitating de-dollarization. Eichengreen (2011)examined the historical dominance of the U.S. dollar as the global reserve currency and explored the potential challenges and implications of its decline. He analyzed the factors that contributed to the dollar’s privileged position and discussed the consequences of a shift toward a multi-currency international monetary system through the development of alternative payment systems, digital currencies, and blockchain technology in reshaping the international monetary system. This highlighted the potential opportunities and risks associated with these innovations and their implications for the future of de-dollarization.

In 2017, the literature discussed the challenges and potential benefits of adopting regional currencies, as well as the impact on regional economic cooperation. The regional dynamics of de-dollarization and the emergence of regional currencies were examined through case studies of different regions, such as Asia, the Middle East, and Latin America, to understand the motivations behind regional monetary integration. Bordo and Meissner (2016) argue that the crises faced by these countries led to a loss of confidence in the dollar as a safe haven currency, prompting them to diversify their reserves and reduce reliance on the U.S. dollar, leading to shifts in global reserve currency (Reinhart & Rogoff, 2009).

Overall, the literature on the evolution over time of de-dollarization yields valuable findings that contribute to our understanding of the economic and financial implications of reducing reliance on the U.S. dollar. By addressing the motivations, challenges, and impacts of de-dollarization, this research provides a foundation for policymaking and decision-making at both national and international levels.

Recent events (tendencies)

With the recent financial innovations, technological advancements, and commodity crisis, scholars argue that countries have been motivated to reduce reliance on the U.S. dollar due to concerns about political influence, economic stability, and the desire for more control over their own currency. Gouvea and Gutierrez (2023a) studied the motivations behind countries’ efforts to reduce their reliance on the U.S. dollar and the potential benefits and challenges associated with the use of digital currencies as an alternative. The main study analyzed was Honduras, which has implemented digital currencies with an immense de-dollarization effort whose success depends on various factors, including technological infrastructure, regulatory frameworks, and international cooperation. Furthermore, Agur et al. (2022) investigated the relationship between central bank digital currencies (CBDCs) and de-dollarization efforts. After 2022, three central banks considered the implications and trade-offs associated with CBDC implementation in the context of de-dollarization. Their success was associated with factors such as public trust, technological readiness, and regulatory frameworks (Auer et al., 2022).

De-dollarization from a regional perspective has been present in Asia and Latin America. In China, economic statecraft has become an increasingly prominent part of their foreign policy drivers. The challenges faced with the continued Ukraine Crisis drove China to redouble its efforts to increase economic self-reliance in critical technologies and sectors through de-dollarization (Wong, 2023).

Furthermore, Argentina once again faces high, persistent, and volatile inflation despite the historical theory of dollarization being an effective commitment device, (Ocampo, 2023) and current economic experts and scholars are seriously considering de-dollarization (Thiagarajan et al., 2023). As a matter of fact, Nigeria’s new policy to ease its over-dependency on the USD by adopting proper management of exchange rate policy will help reduce the continuous depreciation of its naira currency (Obaji, 2023).

METHODS

Considering that there is a comparatively narrow literature in this area of research, this paper is based on an exploratory qualitative approach to understand the various factors of de-dollarization as well as its impacts on major economies. An overview of systematic reviews as a research approach allows researchers to close the gap between research and practice (Bero et al., 1998). Moreover, this method has been thought to be appropriate for producing useful insights regarding the experiences and thoughts of scholars, practitioners, and policymakers (Wallace et al., 2006).

This systematic review has used Web of Science (WoS), since it is the most-used database (Rodriguez-Rojas et al., 2022), to extract and synthesize publications (Birkle et al., 2020). The results of systematic reviews have been viewed as reliable indexes of major research findings to contribute to a new insight contribution (Agarwal et al., 2016). Thus, such utilization of guidelines and thorough systematic data extraction (Harris et al., 2014) addressed our Research objectives.

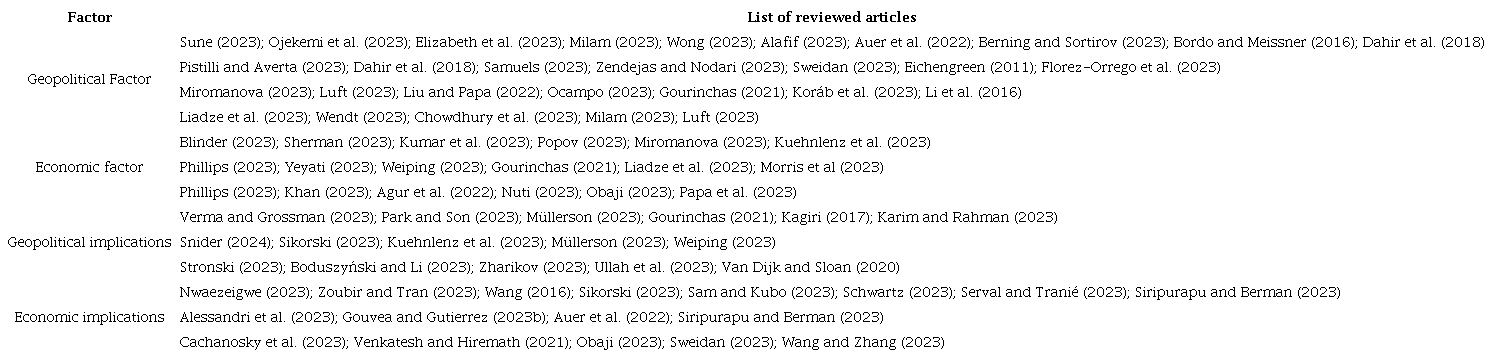

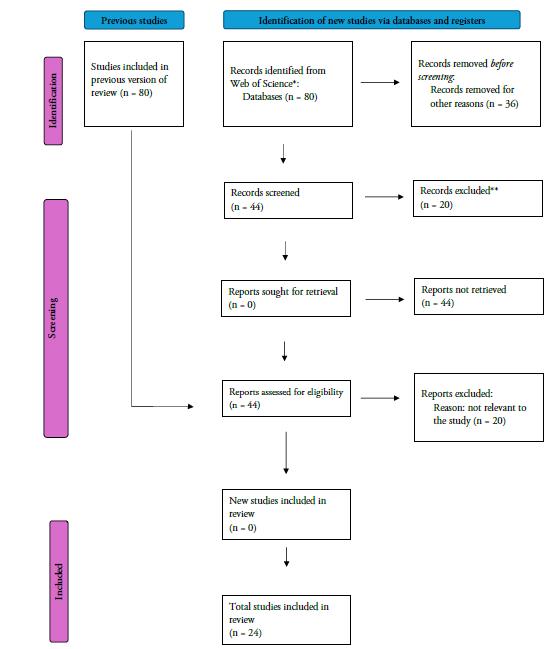

This study has been undertaken as a systematic literature review based on the original guidelines as proposed by Motylska-Kuzma (2017). So, this study is categorized as a tertiary literature review. The steps are described in Figure 1. To identify the relevant articles, a Boolean search was conducted using the terms ‘dollarization’ and ‘de-dollarization’ as keywords in the literature review process. The information gathered from these articles also made it possible to determine existing trends in research and emerging themes of a specific research domain. The resulting analysis would be useful to review the existing gaps in the literature and to show direction to future research areas in the domain. The criteria used aimed to include systematic literature reviews (Paul & Barari, 2022). The selected articles are summarized in Table 1.

Note. Source: Own elaboration.

Figure 1

Literature review protocol.

Source: Own-elaboration, based on PRISMA protocol.

Firstly, the journals were selected and sorted out by those that include either empirical studies or literature reviews with major contributions and that have been used as sources for other systematic literature reviews related to financial economics (Nakano & Muniz, 2018). In particular, the search process was a manual search of selected articles from the journal papers in WoS using the abovementioned keywords in records from 1992 to 2023, with a selection of 80 studies included in the previous version of the review. Secondly, in this selection, the papers handled literature surveys with defined research questions, search processes, data extraction, and data presentation (Budgen et al., 2018), with 36 records removed before screening. From the remaining 44, reports and records were screened, extracted, and synthesized per fields related to Economics, Business Finance, International Relations, Political Science, Business, History, Social Issues, and Social Sciences and were assessed for eligibility. Thirdly, the data collection process was conducted with a data refinement process by classifying and importing the information into a data analytics platform in an accurate, consistent, and well-organized approach to identify trends and derive actionable insights (Madaan et al., 2024). We verified the abstracts and keywords of all the papers found and 20 reports were excluded for not being relevant to the study. Lastly, the final search approach to the data analysis adhered to the concepts of two thematic analyses: geopolitical factor and economic factor. This resulted in 22 total studies included in the review, with the full reference, scope, main topic area, the author(s) and their affiliations, as well as a summary of the study including the main research questions with the aim of contributing with new insights.

This whole process has been followed by several literature review studies (Figure 1).

RESULTS AND FINDINGS OF THE ARTICLE REVIEWS

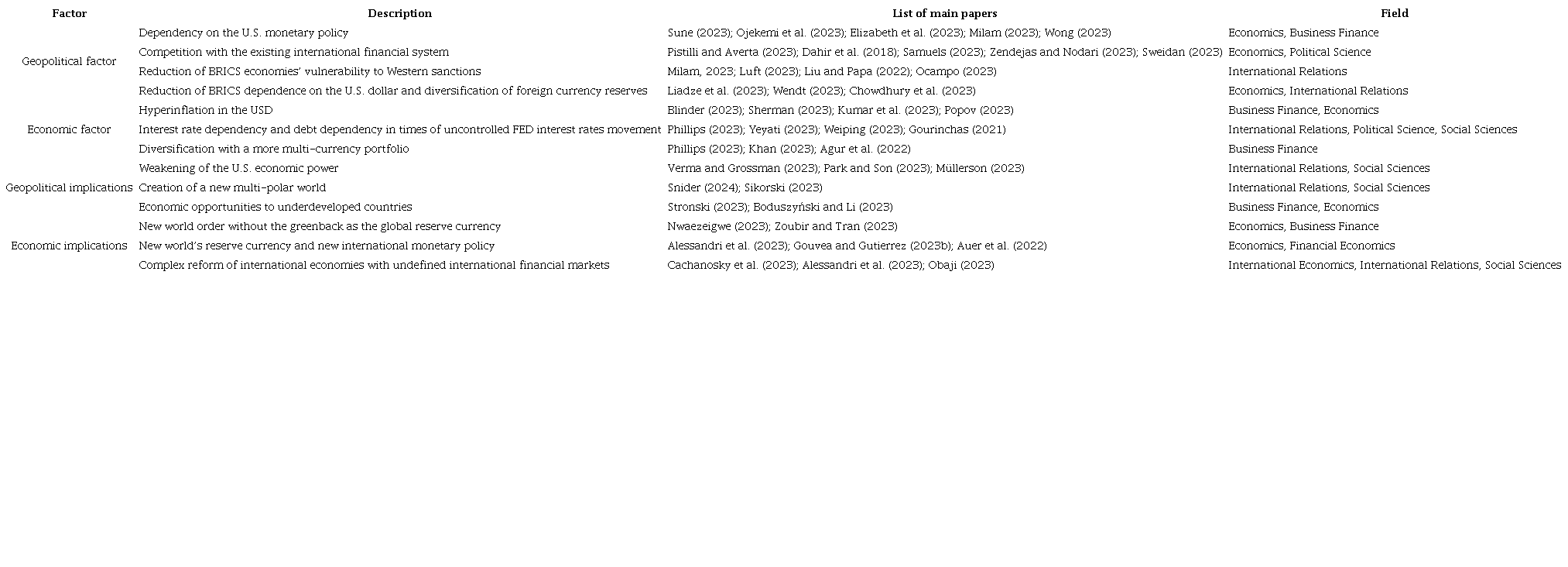

As a summary, Table 2 shows the main papers on the factors (causes) and implications of de-dollarization.

Note. Own elaboration.

Causes of BRICS de-dollarization

Geopolitical factors contributing to de-dollarization

There are numerous geopolitical factors at play when it comes to why many countries want to de-dollarize. As stated previously, the U.S. dollar is the dominant currency in global trade and finance, and it accounts for “nearly 60 percent of the world’s central banks’ foreign exchange reserves,” which more or less serve as a country’s “rainy-day funds” (Prasad, 2023, p. 6). The U.S. dollar is also used to price and settle “almost all commodity contracts, including those for oil,” as well as “a majority of international financial transactions” (Prasad, 2023, p. 6). The U.S. dollar is so widely used internationally that nearly all countries are both heavily reliant on and invested in it. That being said, any transaction involving the U.S. dollar also involves the U.S. banking system, meaning that when countries aren’t cooperative with U.S. policies, the U.S. government can use its leverage to punish these countries (Sune, 2023).

The two countries that have been pushing for de-dollarization the hardest are Russia and China, who are major geopolitical and economic rivals with the United States. Russia has taken numerous steps in the last few years to de-dollarize, the first of which came in June 2021 when the Russian government “announced it was eliminating the U.S. dollar from its National Wealth Fund” (Miromanova, 2023, p. 1121). This was Russia’s first effort to “reduce its vulnerability to Western sanctions” which later came into play following Russia’s invasion of Ukraine in February 2022 (Gould-Davies, 2023, p. 8). In response to the invasion, the United States and its allies in Western Europe imposed numerous financial sanctions on Russia and its oligarchs. In doing so, almost half of Russia’s foreign currency reserves, totaling more than 300 billion U.S. dollars, were frozen. In addition, Russian banks had their access removed to SWIFT, “a critical interbank messaging service that enables international payments” (Barisitz & Evdokimova, 2023, p. 23). Initially, these sanctions resulted in significant price increases in Russia and people taking their money out of Russian banks (Liadze et al., 2023). The sanctions have also posed substantial barriers to Russia carrying out international transactions, which “forced Russia to explore alternative financial systems to mitigate the effects” (Wendt, 2023, p. 1). Russia being frozen out of nearly half of its foreign currency reserves was the sanction that turned Russia into, arguably, the leading proponent of de-dollarization. This action showed how much leverage the United States had on Russia, whose reserves largely consisted of U.S. dollars (Chowdhury et al., 2023). Russia has been working to “reduce their dependence on the U.S. dollar” (Chowdhury et al., 2023, p. 166131) and has found allies looking to do the same.

Russia’s invasion of Ukraine and the extensive sanctions from the United States that followed were driving factors that led to the formation of BRICS, which stands for Brazil, Russia, India, China, and South Africa. These five countries are “looking to establish a new reserve currency backed by a basket of their respective currencies” in order to become more independent of the U.S. dollar and the leverage that can come with it (Pistilli & Averta, 2023, p. 112664). Should this new currency be formed, BRICS would look to “compete with the existing international financial system,” which the U.S. dollar currently dominates (Pistilli & Averta, 2023, p. 112664). For reasons mentioned already, political tensions are extremely high between the United States and Russia. China, which currently boasts the world’s second-largest economy behind that of the United States, has also experienced increasing political tensions with the United States in recent years on issues such as trade and the fate of Taiwan (Dahir et al., 2018). Should BRICS form a new currency, and if countries were to add it to their foreign currency reserves, this would diversify these countries’ reserves, thereby making them less reliant on the U.S. dollar and reducing the geopolitical leverage that the U.S. government has on countries. This could weaken the effectiveness of U.S. sanctions and the U.S.’s influence in global politics. Weakening the United States’ political power on the global stage is exactly what its rivals, like Russia and China, would want to take place as they continue to feud with the United States, with this being another reason why they are both such strong proponents of de-dollarization (Samuels, 2023).

Economic factors contributing to de-dollarization

The U.S. economy is the second biggest in the world after China, and its successes and failures have a significant impact on the global economy (Morrison, 2019). The United States has been struggling with high inflation over the last 18 months, with the U.S. inflation rate coming in at 4.93% in April 2023, which is a notable improvement from an inflation rate of 8.26% a year earlier (Blinder, 2023). These figures are significantly higher than the U.S. Federal Reserve’s target inflation rate of 2% (Blinder, 2023). As a result, the Fed has had to take serious measures to reduce inflation by adjusting its monetary policy. In doing so, the Fed has increased its interest rate 10 times in the last 14 months, with the latest rise at the start of May 2023 bringing it to 5.25% (Sherman, 2023). The actions the Fed has taken in the last year and a half have had a substantial impact on countries around the world that rely heavily on the U.S. dollar. As discussed earlier, a sizable portion of most countries’ foreign currency reserves is made up of U.S. dollars. So, when inflation rises in the United States, the U.S. dollar depreciates, and countries’ foreign currency reserves holding U.S. dollars lose value in turn. In response to the Fed’s interest rate increases, the central banks of many countries have also had to “raise interest rates to stem capital outflows and a sharp depreciation of their own currencies” (Phillips, 2023, p. 924). This chain of events has caused many countries to consider de-dollarization and to further “diversify their holdings into a more multi-currency sort of portfolio” (Phillips, 2023, p. 925). This makes alternative currency options, such as the potential new BRICS currency, more attractive to countries looking to reduce their exposure to the U.S. economic and financial systems (Khan, 2023). This also comes at a time when there have been three major banking failures in the United States this year alone, which creates uncertainty and provides another reason for countries to reduce their dependence on the U.S. dollar. Many countries have had these concerns surrounding the U.S. dollar going back to the last major U.S. recession and global financial crisis in 2008, which “highlighted some of the weaknesses of the U.S. financial system” (Khan, 2023, p. 1). Despite the U.S. dollar’s relative dominance in global trade and finance, countries share various economic concerns with interest rate dependency, debt dependency, and economic output that contribute to the push toward de-dollarization (Yeyati, 2023).

Implications of BRICS de-dollarization

The geopolitical fallout of de-dollarization

Many nations, part of the so-called East, have strived for decades to weaken the United States’ broad economic strength and control over the global economy. The United States dollar, set as the global reserve currency, has not only provided the nation with economic strength and might, but further a large seat at the so-called geopolitical table. The economic power of the U.S. has led to influence in all regions of the world, from Pacific nations like the Marshall Islands and Kiribati to Western Europe and African nations (Verma & Grossman, 2023). In an effort to yield the United States’ political power and prominence, nations and organizations such as BRICS have been set up to challenge the U.S. as the leader of the free world. Specifically, China and Russia have been the most able and willing to express their disaffection with the state of geopolitics. Particularly, Russian President Vladimir V. Putin has called for the creation of a new multi-polar world for well over the past decade (Snider, 2024). One major aim of achieving this goal is to weaken the U.S. economically. One way to do this? Attempt to dethrone the U.S. dollar. Park and Son (2023) examined how de-dollarization can affect export competitiveness and exchange rate dynamics. They found that reducing dollarization can lead to a depreciation of the real exchange rate, which can enhance export competitiveness and stimulate economic growth.

While efforts so far have been unsuccessful and muted, nations have tried, such as Kazakhstan (Barisitz & Evdokimova, 2023). But the larger political threat to the U.S. is the unease of a new cold war and political tension on the rise with China and Russia. Further, nations such as Turkey and Hungary, both NATO (North Atlantic Treaty Organization) members, to varying degrees siding with Russia in the Ukrainian War, show splits in the geopolitical landscape. Russia’s courtship of African nations such as Uganda, Mali, and Burkina Faso shows an attempt to shatter the economically important continent (Stronski, 2023). What de-dollarization would look like on a geopolitical stage is far from certain. But examining the attempts made so far by Russia, China, BRICS, and other nations will offer a glimpse into what the so-called new world order will look like without the greenback as the global reserve currency (Müllerson, 2023). One thing is certain in the outcome of de-dollarization: the U.S. will lose the once massive political force it held (Ize & Yeyati, 2006).

Global organizations such as the EU (European Union), NATO, and the UN (United Nations) will come under strain, and their words and actions will not be viewed as they once were. To examine this effect, let’s take the case of Turkey. During Russia’s so-called ‘Special Military Operation’ in Ukraine, Turkey has served as a great hindrance to European and Western support for NATO and Ukraine. Turkey has blocked and repeatedly refused to give acceptance to Sweden to join the NATO military alliance. While some American analysts have called for the expulsion of Turkey, there are no articles in NATO that lay out a process for expulsion (Van Dijk & Sloan, 2020). These cracks in NATO have developed at a time when Russian aggression was supposed to bring the organization closer together and increase GDP spending for defense by its member states. In a world where the U.S. dollar falls from its once high position, the organizations the U.S. supplies and influences the most could see even European nations turn from NATO from the inside (Sikorski, 2023). Furthermore, the rise of anti-Western sentiment around the world will coincide with the loss of economic influence of the U.S. dollar (Boduszyński & Li, 2023). African and Central European nations have long been courted by the global West and the global East since the fall of the Soviet Union (Nwaezeigwe, 2023). With anti-Western sentiment and propaganda soaring in these nations, a loss of economic prosperity and opportunity from the West can easily tilt the seesaw in BRICS’s favor.

BRICS would gain significantly in the event of de-dollarization. Their political battle for the minds and will of nation-states will be elevated to a degree yet to be seen on the global political landscape. The inroads made by China in the Middle East and African nations such as Sudan and Namibia will spread into surrounding nations (Zoubir & Tran, 2023). Russia’s Central Asian partners, who have been slowly debating a turn to the West for economic and political alliances, may quickly turn the tide. BRICS’s main gain politically in the event of de-dollarization will likely be greater political influence and collaboration between the states. As many BRICS countries are still forced to hold the U.S. dollar as reserves and trade in the dollar, an effort to collaborate and create a new financial system will not only bring the alliance closer but also promote the opportunity to court more nations onto its side. De-dollarization will inevitably cause greater geopolitical power for the BRICS alliance - greater autonomy, collaboration, and increased economic independence.

The economic fallout of de-dollarization

The stability of the global economic system would be the largest economic threat in the case of de-dollarization (Milam, 2023). There have been a few instances in recent history where a global reserve currency has markedly changed; one such example would be during the 1970s and the move away from the gold standard. After WWII, the transition from the British pound to the U.S. dollar began. At this time, the Bretton Woods system was established, essentially allowing for the free exchange of the U.S. dollar for gold. However, in 1971, President Richard Nixon took the U.S. off the gold standard, and the world’s reserve currency with it (Alessandri et al., 2023). The time immediately after the removal of the gold standard led to short-term instability within the global financial markets and currency conversion rates. However, the effects were not as major as some would have imagined. The removal of the gold standard, however, allowed the United States more flexibility in its monetary policy and led to long-term, but stable, devaluation and inflation of the U.S. dollar (Karim & Rahman, 2023).

While de-dollarization and the removal of the gold standard would be vastly different events, some of the lessons learned during that time still hold true. Cachanosky et al. (2023) emphasized how dollarization is a complex reform that can be implemented in many different ways, considering the central bank as an unnecessary institutional vulnerability that facilitates compulsive de-dollarization. It is also important to note that the transition away from the gold standard was slow and gradual. If de-dollarization were to happen only over the course of a few years, the economic effects would be further magnified. Certain global markets would be increasingly unstable and the U.S. dollar would lose most of its once-perceived value (Wang & Zhang, 2023). More importantly, other nations would be presented with the opportunity to diversify their assets and attempt to make a claim on the new global payment system (Alessandri et al., 2023). This is an opportunity the U.S. is wary of and one BRICS has been planning and pushing for. But the U.S. dollar is heavily ingrained into the modern financial system; it is even used as the de facto currency in eight sovereign states and pegged to another 22 (Gouvea & Gutierrez, 2023b). This leads many experts and analysts to point out that a true de-dollarization, in the sense the BRICS nations may prefer it, is unlikely to happen in the near future or at all.

NEW PERSPECTIVES OF DE-DOLLARIZATION

Based on the results of our systematic review, we develop new perspectives of the de-dollarization process. Overall, the literature review on the trend of de-dollarization and its impact on the global economy and local currencies provides a comprehensive understanding of the potential consequences and benefits associated with reduced reliance on the United States dollar (Kshetri, 2023). The research in this field highlights that de-dollarization can strengthen local currencies, reduce vulnerability to external shocks, and enhance economic stability in developing nations. Moreover, it can decrease the dominance of the U.S. dollar in international trade and finance, leading to a more diversified and balanced global monetary system. However, the literature also acknowledges potential challenges and risks, such as the need for adequate infrastructure and financial instruments to support alternative currencies, potential disruptions in global financial markets, and geopolitical consequences. For instance, Koráb et al. (2023) investigated the implications and insights of de-dollarization on the global economy. The authors analyze the factors driving de-dollarization, such as trade imbalances, financial stability, and geopolitical tensions. They find that de-dollarization can have both positive and negative effects on the global economy. However, we can highlight that while there are signs of some de-dollarization, given the U.S.’s long-standing political influence, stability, and partnerships, it is unlikely to happen suddenly unless there’s a major crisis. Additionally, for another country to position its currency, like China’s renminbi, as a true alternative to the dollar, it would take decades of effort to convince global markets. While this process can enhance financial stability and reduce vulnerability to external shocks, it may also lead to increased exchange rate volatility and higher borrowing costs. In this vein, a comprehensive approach involving domestic and international policy measures is necessary to promote the use of local currencies.

Our findings guide us to propose the following reflection as a new insight: historically, de-dollarization has been seen as a post-war effect. With the U.S. imposing sanctions on Russia due to the ongoing war and the trade conflicts with China, the U.S. dollar is expected to face rapid de-dollarization. However, this is not expected, as the U.S. has strong alliances and loyal trading partnerships. This will help the U.S. dollar maintain stability and remain the dominant currency used for about 60% of international trade transactions. In contrast, the Chinese currency is only used for about 2% of international trade transactions. So, we can highlight that as of now, the Fed has huge horizons on many countries and their interest rates - if this command were to fade away, our domestic interest rates within the States would likely skyrocket. This would also create a domino effect into many countries losing interest in taking positions with debt at U.S. banks. A lower influx of foreign investment would make it much more difficult to invest in public programs, as their government spending would have to be lowered significantly. Overall, de-dollarization would pose many effects for many different countries that currently rely on the U.S. dollar. It poses serious threats to the U.S. economic system and would likely lead to financial disruption for decades (Pinchetti & Szczepaniak, 2023).

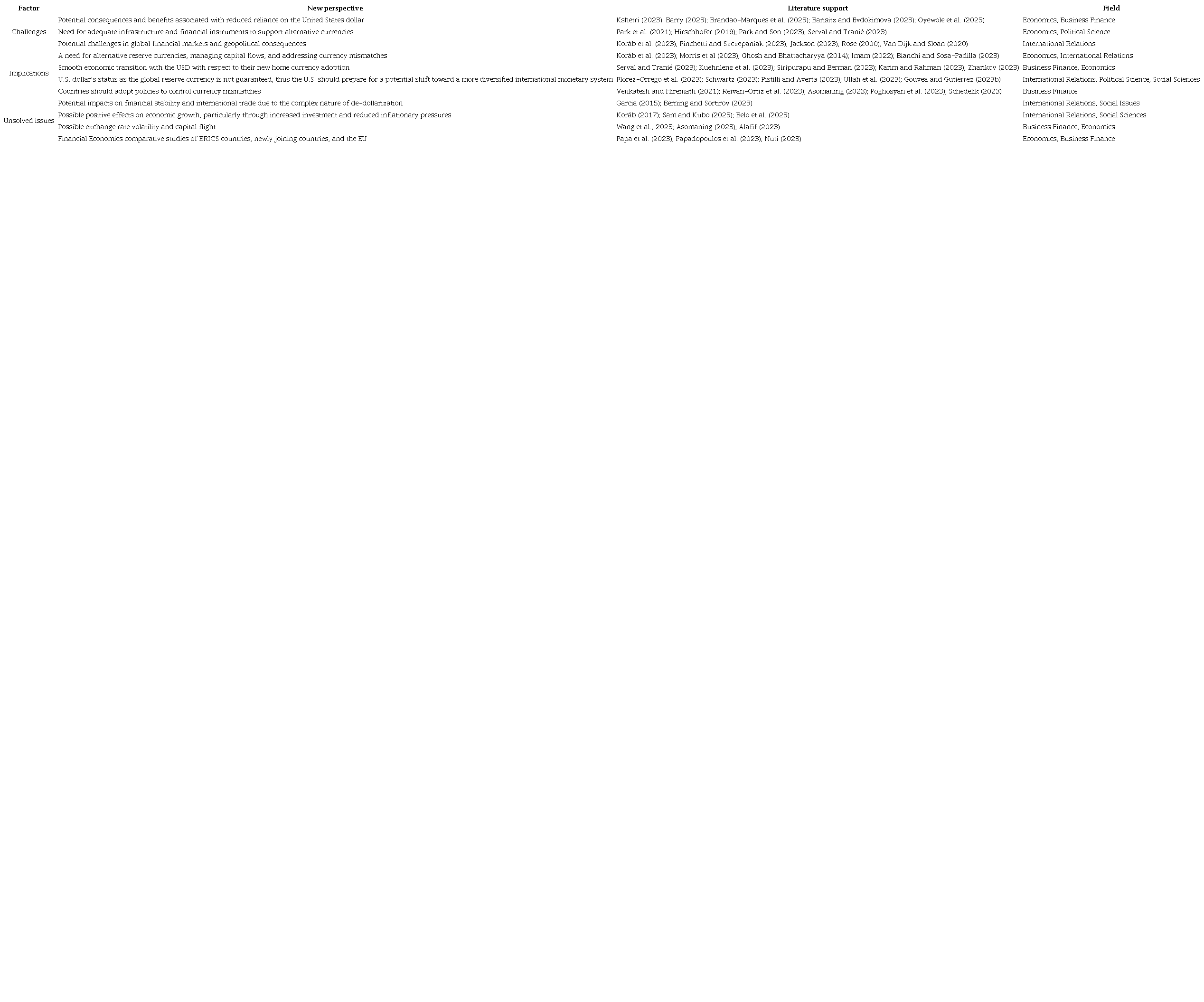

In this study, besides covering the two research questions, we try to contribute to the literature showing how our review can benefit researchers, investors, and policymakers. We show the main challenges of the de-dollarization process, not only for BRICS countries but also for the rest of the world. Moreover, we provide evidence for future de-dollarization in other regions such as Argentina, Nigeria, and China. Finally, we also suggest future lines of research because of our review process. In Table 3, we show our main theoretical argumentations and new approaches derived from the review: challenges, implications, and future lines of de-dollarization.

Note. Own elaboration.

Challenges of de-dollarization

Potential consequences and benefits associated with reduced reliance on the United States dollar

There is increasing evidence that dollarization hurts local economies. An empirical study conducted on 30 countries experiencing dollarization between 2000 and 2016 suggests that dollarization has a negative overall impact on the economy, which naturally increases inflation and decreases national financial efficiency (Park & Son, 2023). The study showed that countries that switched from a dollar-pegged exchange rate to floating exchange rates at some point in the 16-year period experienced more effective responses to local monetary policy changes. It can therefore be concluded that countries with floating exchange rates have more control over their economies than countries with an exchange rate pegged to the dollar. De-dollarization gives countries more economic autonomy and has a positive impact on economic growth. Nevertheless, we can bestow that despite the fact de-dollarization can have a positive impact such as financial stability, it can be dangerous for countries that do not have a robust infrastructure to support it.

Dollarization has also been shown to have a negative impact on a nation’s export value. When two countries engage in trade using the U.S. dollar, the quantity of goods afforded to their financial investment decreases in response to dollar appreciation. Hirschhofer (2019) pointed out that whenever the U.S. currency appreciates against the rest of the world by one percent, a 0.6 to 0.8 percent decline in global trade is predicted within the next year. This is due to the high number of dollarized countries. Importers can afford to purchase less of a given product from dollarized exporters due to this appreciation, which hurts the income of exporters. Exporters trading with dollarized currencies are exposing themselves to financial shocks and policy changes in the United States, without having the ability to adjust monetary policy in response. Thus, we accentuate the manner in which the execution of de-dollarization would have a massive effect on both the U.S. economy and the international economy at large. While it is difficult for scholars to determine the exact effects it would have, many have similar theories. For the U.S., de-dollarization would most likely cause drops in the stock market, increase borrowing costs, and lead to the U.S. having less access to capital overall. Internationally, we would most likely see higher exchange rate volatility, higher import costs, and higher interest rates on debt denominated in foreign currency. While de-dollarization has become a more enticing idea for many countries, its implementation will most likely cause unfortunate and unforeseen circumstances worldwide (Fantacci & Gobbi, 2024).

Need for adequate infrastructure and financial instruments to support alternative currencies

Beyond BRICS, we found other examples such as Ecuador, which is a nation whose economy suffers greatly as a result of dollarization, specifically due to the drawbacks mentioned previously: vulnerability to dollar appreciation and lack of monetary policy control. Ecuador abandoned its national currency in 2000 due to an economic crisis and adopted the dollar as its national currency. Although this move allowed Ecuador to regain financial stability, the adverse effects on the economy have lately been severe. Due to dollar appreciation, Ecuador’s export value fell 5.9 percent in a single year. The price of goods has risen in comparison to other Latin American countries, and potential importers have turned to competition due to high prices (Wang, 2016).

After this review, we can draw the attention that de-dollarization occurs when other nations reduce their use of the U.S. dollar for international trade and other financial transactions, thereby diminishing the U.S. dollar’s power and stability. This can cause the U.S. dollar to be perceived as unstable, a poor investment, and a currency with high inflation rates. As a result, emerging countries may prefer alternative currencies that are seen as more stable and liquid, such as the Chinese renminbi, which is used by a few Latin American countries (Pettis, 2024). Ecuador’s suffering economy and lack of economic control is a cautionary tale for dollarization, and a strong argument for de-dollarization (Wang, 2016). Likewise, Zimbabwe’s introduction of a new currency documents the pattern of dollarization in African economies and illustrates that despite an improved macroeconomic environment, dollarization should decline going forward provided that macroeconomic stability is achieved and preserved (Imam, 2022). Thus, deposit de-dollarization and non-transformation of foreign currency deposits into local currency loans can be complemented with non-transformation of foreign currency deposits into local currency loans. For a safer strategy, this can further involve foreign currency deposits into local currency loans of the country per se (Kaminskyi & Versa, 2018).

In assessing the effects of de-dollarization, Belo et al. (2023) also claimed that dollarizing countries are able to take immense advantage of the administrative expenses, better reliability and liquidity of the USD, and greater stability of inflation and interest rates. According to the U.S. Federal Reserve, the 2023 operating budget for the dollar currency is set to be $931.4 million dollars, and this includes all the production costs, research and development, and all the related manufacturing and maintenance costs. With that being said, countries that are planning to de-dollarize from the U.S. would incur a considerably large amount of cost to produce and maintain their own currencies, especially for countries with fragile, less developed financial tools and markets (Schedelik, 2023). Thus, our new viewpoint in this research is to reflect on the many reasons for de-dollarization, including establishing economic independence from the United States, avoiding potential sanctions that could lead to economic isolation, and reducing the vulnerability to U.S. dollar exchange rate fluctuations. The economic sanctions imposed upon Russia by the United States, caused by Russia’s invasion of Ukraine, have sparked the most recent increase in de-dollarization. Common alternatives to the U.S. dollar in recent years include gold and the Chinese renminbi, along with currencies from smaller economies including the Australian dollar, the Canadian dollar, the Swedish krona, and the South Korean won (Banik & Das, 2024).

Park and Son (2023) investigated the effectiveness of monetary policy instruments under dollarization in association with economic growth and inflation and found that the monetary aggregates, M2, are more relevant policy instruments, while the interest rates, including policy rates, exhibit overall limited effectiveness. De-dollarized countries can no longer maintain the quality and efficiency of their financial services and currency that were previously monitored and controlled by the United States. Consequently, it leads to the devaluation and loss of trust in the new currency and reduces the foreign investments and the incentives that they could gain, therefore leading to an increase in volatility in currency exchange rates, especially during the transition period (Serval & Tranié, 2023). For example, during the period of the implementation of the Vietnamese government’s de-dollarization policy, it experienced the inconvertibility of currencies and a great loss in public confidence, leading to the public preference for gold and foreign currencies and a large depreciation of the VND (the Vietnamese dong currency).

Potential challenges in global financial markets and geopolitical consequences

Some potential effects of the U.S. dollar losing its status as the world’s top currency include a substantial increase in borrowing costs in the United States, the United States stock market significantly losing value, and the United States losing its flexibility in taking on debt for government spending and international trade (Jiang et al., 2024). On top of that, the process of de-dollarization could drive up the country’s inflation and interest rates, making their own currency and investments less comparative and desirable to the public (Koráb et al., 2023). High interest rates discourage the borrowers and investors from using the currency (Alafif, 2023), therefore limiting economic growth and hampering the financial activities (consumer spending, investing, business expansion) in the nation.

Thus, we can contribute with another factor to consider for a de-dollarizing country: the country’s potential to default. As the country increases its foreign debt, it also increases the likelihood of being unable to repay it by its own currency (Barry, 2023). Especially with commodities priced and traded in dollars, shifting away could complicate international transactions and hamper foreign direct investment and capital flows, causing their debts with the U.S. and foreign partners to become more expensive for it to repay. Defaulting on the existing debts would decrease the overall market trust in the currency (Brandao-Marques et al., 2023).

The dollarized economies can promote a more cooperative environment and offer more opportunities for international trade (Jackson, 2023). By eliminating the risk of devaluation, countries that have fully adopted the dollar will have a common currency with their key trading partner, decreasing transaction costs and fostering trade between them. Rose (2000) discovers that trade between two nations using the same currency is greater than trade between nations using different currencies. Thus, de-dollarized countries are limited from conducting international trade as well as reaching financial integration (Serval & Tranié, 2023).

Implications for investors and policymakers

Need for alternative reserve currencies, managing capital flows, and addressing currency mismatches

The literature analyzes how the decreasing influence of the U.S. dollar may affect the role of other reserve currencies, the stability of the global financial system, and the power dynamics within international institutions (Bianchi & Sosa-Padilla, 2023). Our study examines the reactions of traditional economic powers, such as the U.S., toward de-dollarization trends, and the challenges faced by BRICS countries in their efforts to de-dollarize their economies. It discusses the reasons for de-dollarization, such as reducing dependence on the U.S. dollar and increasing monetary policy autonomy.

Smooth economic transition with the USD with respect to new home currency adoption

The study identifies various challenges, including the need for alternative reserve currencies, managing capital flows, and addressing currency mismatches. Debates within this theme focus on the potential for cooperation or conflict between the established and emerging economies, the need for global currency reforms, and the future evolution of the international monetary system (Morris et al., 2023). Ghosh and Bhattacharyya (2014) investigated the relationship between capital inflows and economic growth, finding that the impact of capital inflows on growth, depends on the level of financial development and the composition of capital flows. They argue that while capital inflows can stimulate growth in countries with well-developed financial systems and productive investment opportunities, they can also pose risks to macroeconomic stability and growth in countries with weak institutions and excessive reliance on short-term capital. This paper highlights how and why de-dollarization in BRICS countries is a complex process that involves various challenges. However, if successfully implemented by policymakers, it can lead to increased monetary policy autonomy and reduced dependence on the U.S. dollar. Thus, this research helps policymakers and market participants understand the potential risks and adjustments that may arise during the de-dollarization process by a smooth economic transition with the USD with respect to their new home currency adoption (Serval & Tranié, 2023), credible rules under domestic jurisdiction easily reversible, enabling them to better prepare for and manage the impact of de-dollarization on their respective economies (Kuehnlenz et al., 2023).

Potential shift toward a more diversified international monetary system

Another aspect explored in the literature pertains to the challenges associated with de-dollarization. Studies highlight that reducing dollar dependency is not an easy task due to the dominant position of the U.S. dollar in global trade and finance (Florez-Orrego et al., 2023). Analysis of the challenges can inform policymakers on potential hurdles, enabling them to design better policy measures to mitigate risks and maximize the benefits of de-dollarization. Simultaneously, the U.S. dollar’s status as the global reserve currency is not guaranteed and could be challenged in the future. Thus, in the same line of strengthening monetary policy frameworks in the Caucasus and Central Asia (Poghosyan et al., 2023), we recommend that policymakers should anticipate and prepare for a potential shift toward a more diversified international monetary system.

Countries should adopt policies to control currency mismatches

Finally, countries with a similar profile need to adopt policies to control currency mismatches, which are consistent with their growth-oriented policies. Despite the fact that debt is indispensable to fuel economic growth, with a leverage profile, adopting such measures helps these economies benefit from financial integration and globalization, and foreign currency borrowing boosts growth (Venkatesh & Hiremath, 2021).

Unsolved issues

Potential impacts on financial stability and international trade due to the complex nature of de-dollarization

This section critically examines the challenges and limitations associated with de-dollarization efforts by the BRICS countries in the existing literature and what we discovered to be missing from the chosen articles. It addresses issues such as the stability of emerging economies and the integration of financial markets. Further research about the potential risks of currency depreciation (Reivan-Ortiz et al., 2023), capital flight (Oyewole et al., 2023), and financial volatility during the de-dollarization process is needed (Asomaning, 2023).

Possible positive effects on economic growth, particularly through increased investment and reduced inflationary pressures

We also consider the constraints imposed by existing trade and financial arrangements, international institutions, and the globalized nature of supply chains (Berning & Sotirov, 2023). Debates within this theme often involve assessing the feasibility of complete de-dollarization and proposing strategies to mitigate associated risks. Garcia (2015) highlighted the complex nature of de-dollarization and emphasized the need for careful consideration of further research into its potential impacts on financial stability and international trade. Koráb (2017) suggest that de-dollarization can have positive effects on economic growth, particularly through increased investment and reduced inflationary pressures. However, the study also highlights the potential risks associated with de-dollarization, such as exchange rate volatility and capital flight. Furthermore, policymakers must carefully manage the potential risks and challenges associated with de-dollarization, such as exchange rate volatility and capital flight (Asomaning, 2023; Wang et al., 2023).

Possible exchange rate volatility and capital flight

It is also important to delve deeper into the specific strategies and policies adopted by different BRICS countries in their de-dollarization efforts. Financial economic comparative studies of BRICs countries, newly joining countries, and the EU can provide valuable insights into the effectiveness of various approaches and identify best practices (Papa et al., 2023). Additionally, more research is needed on the potential impacts of de-dollarization on major economies outside the BRICS group and its impact on Ukraine, Argentina, Korea, and Saudi Arabia (Papadopoulos et al., 2023). Understanding how these economies respond and adapt to the changing dynamics of the international monetary system will help in assessing the broader implications of de-dollarization on global financial stability and economic relations. Moreover, exploring the role of digital currencies, such as central bank digital currencies (CBDCs), in facilitating de-dollarization among BRICS countries is an area that requires further examination (Schwartz, 2023). Analyzing the potential benefits and challenges of CBDC adoption within the context of de-dollarization can contribute to a more comprehensive understanding of the future of international monetary systems.

Financial economics comparative studies of BRICS countries, newly joining countries, and the EU

We can interpret and provide investors with how this implementation may have damaging effects on the stock market, as companies may be valued lower due to the increased borrowing costs and other effects of de-dollarization. The United States government would also be affected, as being the reserve currency in the present has allowed the government to run large deficits in spending. On a global scale, it would likely weaken the economic position of the U.S. and countries heavily reliant on trade with the U.S. (Nelson, 2024). In terms of areas for further research, a more comprehensive understanding of the effectiveness of de-dollarization measures would be valuable. Research should consider the impacts of different approaches to de-dollarization, such as promoting local currency usage, developing regional payment systems, or establishing alternative reserve currencies. Additionally, examining the interplay between de-dollarization and other global economic trends, such as increasing protectionism or geopolitical tensions, could provide valuable insights into the potential challenges and opportunities for countries pursuing de-dollarization.

CONCLUSIONS

The historical context of de-dollarization also includes various financial crises that have shaken confidence in the U.S. dollar and the stability of the global financial system. The Asian financial crisis in 1997, the global financial crisis in 2008, and the subsequent European debt crisis highlighted the vulnerability of the dollar-centric system. These crises exposed risks associated with excessive reliance on a single currency and prompted countries to explore alternatives. Our systematic review study summarized the literature on the de-dollarization process in BRICS to assess several dimensions of this process. We systematized the existing literature on this topic, showing factors, fallouts, implications, and future lines of research.

De-dollarization has its benefits and drawbacks, but it also needs to be taken into consideration amongst many other factors, such as its economics, politics, social regulations, and policies (Zharikov, 2023). For instance, in Vietnam, as a less-monetized country, de-dollarization has had a generally negative impact on the nation; however, the other determinants, such as its high inflation rate, the amount of foreign currency in circulation, and the significant differentials of the deposit rates between the VND and the USD, constitute factors that impeded the process of de-dollarization. From what we have learned, we should not neglect the impact that dollarization can have on the foreign markets (Nuti, 2023), and looking back at today’s economy, foreign currencies are more stable than they ever have been, therefore decreasing the need for dollarization now.

After reviewing recent and relevant articles, whereby Table 2 shows the results of the procedure, we observe that the dollar is still relatively stable and many countries still engage in dollarization (Siripurapu & Berman, 2023). Nearly 90% of currency trading is conducted according to the U.S. dollar (Pistilli & Averta, 2023). We found significant drawbacks of dollarization due to the threat of dollar appreciation and lack of monetary policy control, particularly in the case of Ecuador. This demonstrates strong evidence for de-dollarization. However, de-dollarization can also cause an additional amount of cost in the production of currency and administration fees (Gouvea & Gutierrez, 2023b), pose disadvantages on the quality and effectiveness of its financial services and institutions (Sam & Kubo, 2023), and raise inflation and interest rates, which hamper the country’s economic growth as well as its financial integration and international trade. A major insight in this research is the consequence of de-dollarization as a possible effect on global economic stability. As nations move away from using the dollar, currency exchange rates and financial markets could become more volatile, creating uncertainty and disrupting global trade and investment. With less demand for the dollar, its value may drop, which could cause higher inflation and reduce the purchasing power of American consumers. Additionally, the U.S. government might struggle to fund its budget deficits if fewer countries want to buy U.S. Treasury bonds.

While the literature review offers valuable insights, we were able to make a contribution with several areas for further research. Firstly, more analysis is needed to understand the potential impact of de-dollarization on developed economies, as most studies have focused on developing nations. Exploring how de-dollarization may affect global financial centers and the stability of advanced economies can provide a more comprehensive understanding of the broader consequences of this trend (Ullah et al., 2023). Secondly, further research is required to assess the potential role of digital currencies, such as cryptocurrencies or central bank digital currencies, in facilitating de-dollarization efforts. Studying the compatibility, efficiency, and regulatory aspects of alternative digital currencies can shed light on how they can contribute to the shift away from the U.S. dollar (Kuehnlenz et al., 2023). Lastly, investigating the geopolitical implications of de-dollarization and how it may reshape global power dynamics is an important avenue for further research. Understanding the potential consequences, conflicts, and collaborations that emerge from a reduced reliance on the U.S. dollar can help guide policymakers and foster international cooperation. However, the extent of non-overlapping content between WoS and Scopus indexes was determined to vary greatly across topics (Pranckutė, 2021). In this specific case, Scopus offers wide coverage, both in publications and in citations for the financial economics field. Since substantial studies published in Scopus weren’t included in the systematic review of this paper, future research reviews should include publications indexed in Scopus and other databases.

Our findings provide academics, investors, and policymakers with new information on the subject. After reviewing all the literature, research could delve deeper into the implications of de-dollarization on global financial institutions and markets. Exploring the potential adjustments in the international monetary system and the role of international financial institutions in a de-dollarized world could provide guidance for global governance reforms. Policymakers should get acquainted with building frameworks for smooth economic dependency transitioning.

Our study aims to offer valuable insights into the dollarization review and the potential benefits and challenges associated with this shift. It contributes to a broader understanding of monetary systems, encourages policymakers to diversify reserves, and fosters international cooperation. However, further research is needed to explore the implications for developed economies, assess the role of digital currencies, and examine the geopolitical consequences. This research provides society with a foundation upon which policymakers can make informed decisions and work toward a more balanced and resilient global economic system.

Through this, we emphasize that de-dollarization presents challenges for the global financial system. The dominance of the U.S. dollar has given the United States considerable influence over key international financial institutions like the IMF (International Monetary Fund) and the World Bank. As more countries shift away from relying on the dollar, these institutions might need to undergo reforms to better align with the evolving global economy. For U.S. consumers, de-dollarization could have a direct negative impact - with the U.S. dollar acting as the world’s reserve currency; if that supply were to come back home with the same (if not a decreasing) level of demand, it could cause U.S. inflation. This would reduce potential buyers of U.S. debt. With the U.S. losing its place atop the global financial system, it could lead to higher borrowing costs in the U.S. and negative effects on the stock market. One effect of de-dollarization is that it decreases the United States government’s ability to run a large deficit on spending, which I think is something that concerns many Americans. If de-dollarization continues at a fast rate, the U.S. may be forced to address its significant national debt, leading to negative effects not only on the U.S. but also on other countries that rely on the U.S. dollar for economic stability.

In conclusion, de-dollarization carries major implications and challenges for the global economy and power structures. It could transform the international monetary system, weaken U.S. dominance, and introduce both new opportunities and risks. Coordinated policies and thoughtful management will be essential in handling the complexities of this shift and maintaining stability in the global financial system.

REFERENCES

Agarwal, A., Durairajanayagam, D., Tatagari, S., Esteves, S. C., Harlev, A., Henkel, R., Roychoudhury, S., Homa, S., Puchalt, N. G., Ramasamy, R., Majzoub, A., Ly, K. D., Tvrda, E., Assidi, M., Kesari, K., Sharma, R., Banihani, S., Ko, E., Abu-Elmagd, M., Gosalvez, J., & Bashiri, A. (2016). Bibliometrics: Tracking research impact by selecting the appropriate metrics. Asian Journal of Andrology, 18(2), 296-309. https://pmc.ncbi.nlm.nih.gov/articles/PMC4770502/

Agur, I., Ari, A., & Dell’Ariccia, G. (2022). Designing central bank digital currencies. Journal of Monetary Economics, 125, 62-79. https://doi.org/10.1016/j.jmoneco.2021.05.002

Alafif, H. A. (2023). Interest rate and some of its applications. Journal of Applied Mathematics and Physics, 11(6), 1557-1569. https://doi.org/10.4236/jamp.2023.116102

Alessandri, P., Venditti, F., & Jordà, O. (2023). Decomposing the monetary policy multiplier. Bank of Italy Temi di Discussione No, 1422.

Arapova, E. Y. (2019). The “BRICS Plus” as the first international platform connecting regional trade agreements. Asia-Pacific Social Science Review, 19(2), 30-46. http://dx.doi.org/10.59588/2350-8329.1220

Asomaning, K. O. (2023). Asymmetric Effects in Geopolitical Risk and Foreign Reserves Accumulation Among BRICS Countries. https://digitalcommons.sacredheart.edu/cgi/viewcontent.cgi?article=1032&context=wcob_theses

Auer, R., Frost, J., Gambacorta, L., Monnet, C., Rice, T., & Shin, H. S. (2022). Central bank digital currencies: Motives, economic implications, and the research frontier. Annual review of economics, 14, 697-721. https://doi.org/10.1146/annurev-economics-051420-020324

Banik, N., & Das, K. C. (2024). Riding the dragon: Ascent of China’s renminbi and the decline of dollar dominance. https://www.econstor.eu/bitstream/10419/307455/1/1911105361.pdf

Barisitz, S., & Deswel, P. (2023). Russia’s banking sector and its EU-owned significant banks, against the backdrop of war and sanctions. Focus on European Economic Integration, (Q1/23), 23-41. https://ideas.repec.org/a/onb/oenbfi/y2023iq1-23b2.html

Barisitz, S., & Evdokimova, T. (2023). Dedollarization efforts in Russia’s foreign trade against the backdrop of Russia’s war in Ukraine and intensifying Western sanctions (2013-2023). Focus on European Economic Integration, (Q3/23), 29-51. https://ideas.repec.org/a/onb/oenbfi/y2023iq3-23b2.html

Barry, E. (2023). Currency conflict: Dollar dominance, contemporary de-dollarization and The Chinese Yuan’s Place in The Global Economy. https://www.scienceopen.com/hosted-document?doi=10.13169/worlrevipoliecon.15.4.0566

Becker, U. (2014). The BRICs and emerging economies in comparative perspective. London and Routledge.

Belo, T. F., Freitas, J. R., Monteiro, A. L., Djo, L. M. K., & Marques, D. L. (2023). The Impact of dollarization on consumption and savings behavior in Dili Timor-Leste (Case Study: Permanent Civil Servants). Timor Leste Journal of Business and Management, 5, 32-48. https://scispace.com/papers/the-impact-of-dollarization-on-consumption-and-savings-35wq6g73qd

Berning, L., & Sotirov, M. (2023). Hardening corporate accountability in commodity supply chains under the European Union Deforestation Regulation. Regulation & Governance. https://doi.org/10.1111/rego.12540

Bero, L. A., Grilli, R., Grimshaw, J. M., Harvey, E., Oxman, A. D., & Thomson, M. A. (1998). Closing the gap between research and practice: an overview of systematic reviews of interventions to promote the implementation of research findings. Bmj, 317(7156), 465-468. https://doi.org/10.1136/bmj.317.7156.465

Bianchi, J., & Sosa-Padilla, C. (2023). International sanctions and dollar dominance (No. w31024). National Bureau of Economic Research.

Birkle, C., Pendlebury, D. A., Schnell, J., & Adams, J. (2020). Web of Science as a data source for research on scientific and scholarly activity. Quantitative Science Studies, 1(1), 363-376. https://doi.org/10.1162/qss_a_00018

Blinder, A. S. (2023). Landings, soft and hard: The federal reserve, 1965-2022. Journal of Economic Perspectives, 37(1), 101-120. https://www.aeaweb.org/articles?id=10.1257/jep.37.1.101

Boduszyński, M. P., & Li, C. (2023). External autocratic influence, the balkans, and democratic decline. In Geopolitical Turmoil in the Balkans and Eastern Mediterranean (pp. 89-118). Springer International Publishing.

Bordo, M. D., & Meissner, C. M. (2016). Fiscal and financial crises. In Handbook of macroeconomics (Vol. 2, pp. 355-412). Elsevier.

Brandao-Marques, L., Casiraghi, M., Gelos, G., Harrison, O., & Kamber, G. (2023). Is high debt constraining monetary policy? Evidence from Inflation Expectations. Journal of International Money and Finance, 149, 103206. https://doi.org/10.1016/j.jimonfin.2024.103206

Budgen, D., Brereton, P., Williams, N., & Drummond, S. (2018). The contribution that empirical studies performed in industry make to the findings of systematic reviews: A tertiary study. Information and software technology, 94, 234-244. https://doi.org/10.1016/j.infsof.2017.10.012

Buckley, R. P., & Trzecinski, M. (2023). Central Bank Digital Currencies and the global financial system: The dollar dethroned? Capital Markets Law Journal, 18(2), 137-171. https://doi.org/10.1093/cmlj/kmad007

Cachanosky, N., Ocampo, E. & Salter, A. (2023). Lessons from Latin America Dollarization in the Twenty First Century. The Economists’ Voice, 20(1), 25-42. https://doi.org/10.1515/ev-2023-0001

Chkili, W., & Nguyen, D. K. (2014). Exchange rate movements and stock market returns in a regime-switching environment: Evidence for BRICS countries. Research in International Business and Finance, 31, 46-56. https://doi.org/10.1016/j.ribaf.2013.11.007

Chowdhury, P. R., Medhi, H., Bhattacharyya, K. G., & Hussain, C. M. (2023). Severe deterioration in food-energy-ecosystem nexus due to ongoing Russia-Ukraine war: A critical review. Science of The Total Environment, 902, 166131. https://doi.org/10.1016/j.scitotenv.2023.166131

Dahir, A. M., Mahat, F., Ab Razak, N. H., & Bany-Ariffin, A. N. (2018). Revisiting the dynamic relationship between exchange rates and stock prices in BRICS countries: A wavelet analysis. Borsa Istanbul Review, 18(2), 101-113. http://dx.doi.org/10.1016/j.bir.2017.10.001

Eichengreen, B. (2011). Exorbitant Privilege: The rise and fall of the Dollar and the Future of the International Monetary System. Oxford University Press.

Elizabeth, C. O. B., Patricio, C. P. A., Alfredo, T. T. L., Adalid, A. R. L., Alberto, C. L. L., & Gustavo, B. O. (2023). Convertibility and dollarization: Economic policy tools. Remittances Review, 8(4). https://www.researchgate.net/publication/373771153_Convertibility_and_Dollarization_Economic_Policy_Tools

Fantacci, L., & Gobbi, L. (2024). Stablecoins, central bank digital currencies and US dollar hegemony: The geopolitical stake of innovations in money and payments. Accounting, Economics, and Law: A Convivium, 14(2), 173-200. https://doi.org/10.1515/ael-2020-0053

Florez-Orrego, S., Maggiori, M., Schreger, J., Sun, Z., & Tinda, S. (2023). Global Capital Allocation (No. w31599). National Bureau of Economic Research. https://www.nber.org/papers/w31599

Garcia, M. (2015). De-dollarization: A comprehensive analysis of the challenges and limitations. Journal of International Economics, 42(3), 567-589. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4816196

Ghosh, A. (2014). How do openness and exchange-rate regimes affect inflation?. International Review of Economics & Finance, 34, 190-202. https://doi.org/10.1016/j.iref.2014.08.008

Ghosh, S., & Bhattacharyya, I. (2014). Spread, volatility and monetary policy: empirical evidence from the Indian overnight money market. In Macroeconomics and Markets in India (pp. 118-138). Routledge.

Gould-Davies, N. (2023). Russia, the West and sanctions. In Survival: Global Politics and Strategy (February-March 2020): Deterring North Korea (pp. 7-28). Routledge.

Gourinchas, P. O. (2021). The dollar hegemon? Evidence and implications for policymakers. In The Asian monetary policy forum: Insights for central banking (pp. 264-300). https://doi.org/10.1142/9789811238628_0007

Gouvea, R., & Gutierrez, M. (2023a). “BRICS Plus”: A new global economic paradigm in the making? Modern Economy, 14(5), 539-550. https://doi.org/10.4236/me.2023.145029

Gouvea, R., & Gutierrez, M. (2023b). De-Dollarization: The harbinger of a new globalization architecture? Theoretical Economics Letters, 13(4), 791-807. https://doi.org/10.4236/tel.2023.134046

Harris, J. D., Quatman, C. E., Manring, M. M., Siston, R. A., & Flanigan, D. C. (2014). How to write a systematic review. The American Journal of Sports Medicine, 42(11), 2761-2768. https://doi.org/10.1177/0363546513497567

Hirschhofer, H. (2019). Would gradual de‐dollarization and more financing in local currencies boost trade? Global Policy, 10(3), 435-439. https://doi.org/10.1111/1758-5899.12712

Iida, K. (2024). Change in the international economic order: From the perspective of political science. Changing Orders in International Economic Law, 1, 7-17. https://www.taylorfrancis.com/chapters/edit/10.4324/9781003193098-2/change-international-economic-order-keisuke-iida

Imam, P. A. (2022). De‐dollarization in Zimbabwe: What lessons can be learned from other sub‐Saharan countries? International Journal of Finance & Economics, 27(1), 770-801. https://doi.org/10.1002/ijfe.2177